Order Code RL31870 CRS Report for Congress The Dominican Republic-Central America-United States Free Trade Agreement (CAFTA-DR) Updated January 16, 2008 J. F. Hornbeck Specialist in International Trade and Finance Foreign Affairs, Defense, and Trade Division Prepared for Members and Committees of Congress Congressional Service

Transcript

Order Code RL31870

CRS Report for Congress

The Dominican Republic-Central America-UnitedStates Free Trade Agreement (CAFTA-DR)

Updated January 16, 2008

J. F. HornbeckSpecialist in International Trade and FinanceForeign Affairs, Defense, and Trade Division

Prepared for Members andCommittees of Congress

Congressional

Service

The Dominican Republic-Central America-United States

Free Trade Agreement (CAFTA-DR)

Summary

The United States Trade Representative (USTR) and trade ministers from Costa

Rica, El Salvador, Guatemala, Honduras, Nicaragua, and the Dominican Republic

signed the Dominican Republic-Central America-United States Free Trade

Agreement (CAFTA-DR) on August 5, 2004. Nearly one year later, it faced a

contentious debate and close vote in both houses of the U.S. Congress. The Senate

passed implementing legislation 54 to 45 on June 30, 2005, with the House following

in kind 217 to 215 on July 28, 2005. President Bush signed the legislation into law

on August 2, 2005 (P.L. 109-53, 119 Stat. 462). The United States has implemented

the agreement for El Salvador, Honduras, Nicaragua, Guatemala, and the Dominican

Republic. In Costa Rica, legislative consideration of CAFTA-DR has been a

prolonged process, culminating in the decision to hold a national referendum. On

October 7, 2007, the people of Costa Rica voted in favor of CAFTA-DR 51.6% to

48.4% (subject to official recount), setting the stage for final consideration by the

National Assembly.

The CAFTA-DR is a regional agreement with all parties subject to “the same

set of obligations and commitments,” but with each country defining its own market

access schedule. It is a reciprocal trade agreement, basically replacing U.S. unilateral

preferential trade treatment extended to these countries under the Caribbean Basin

Economic Recovery Act (CBERA), the Caribbean Basin Trade Partnership Act

(CBTPA), and the Generalized System of Preferences (GSP). It liberalizes trade in

goods, services, government procurement, intellectual property, and investment, and

addresses labor and environment issues. Most commercial and farm goods attain

duty-free status immediately. Remaining trade will have tariffs phased out

incrementally over five to twenty years. Duty-free treatment will be delayed longest

for the most sensitive agricultural products. To address asymmetrical development

and transition issues, the CAFTA-DR specifies rules for transitional safeguards, tariff

rate quotas, and trade capacity building.

The CAFTA-DR is not expected to have a large effect on the U.S. economy as

a whole given the relatively small size of the Central American economies and the

fact that most U.S. imports from the region had already been entering duty free under

normal trade relations or CBI and GSP preferential arrangements. Adjustments will

be slightly more difficult for some sectors, but none are expected to be severe.

Supporters see it as part of a policy foundation supportive of both improved

intraregional trade, as well as, long-term social, political, and economic development

in an area of strategic importance to the United States. Opponents wanted better

trade adjustment and capacity building policies to address the potentially negative

effects on certain import-competing sectors and their workers. They also argued that

the labor, intellectual property rights, and investment provisions in the CAFTA-DR

needed strengthening. This report discusses issues and evolution of the CAFTA-DR

debate and will be updated.

The Dominican Republic-Central America-United States Free Trade Agreement

On August 5, 2004, the United States Trade Representative (USTR) and tradeministers from Costa Rica, El Salvador, Guatemala, Honduras, Nicaragua, and theDominican Republic signed the Dominican Republic-Central America-United StatesFree Trade Agreement (the CAFTA-DR; see Appendix 1, Chronology ofNegotiations). The CAFTA-DR is a regional trade agreement with all parties subjectto “the same set of obligations and commitments,” but with each country defming itsown market access schedule. It is a comprehensive and reciprocal trade agreement,replacing U.S. unilateral preferential trade treatment extended to these countriesunder the Caribbean Basin Economic Recovery Act (CBERA), the Caribbean BasinTrade Partnership Act (CBTPA), and the Generalized System ofPreferences (GSP).

The U.S. Congress did not consider implementing legislation for over a yearafter the CAFTA-DR was signed because it was so controversial. On June 30, 2005,the Senate passed S. 1307 by a vote of 54 to 45. The House followed on July 28,2005, passing H.R. 3045 by a vote of217 to 215. President Bush signed the bill intolaw on August 2, 2005 (P.L. 109-53, 119 Stat. 462). El Salvador, Honduras,Guatemala, the Dominican Republic, and Nicaragua also ratified the agreement, inthat order. The CAFTA-DR was expected to enter into force on January 1, 2006, butnone of the ratifying countries had completed the legal and regulatory measuresneeded to comply with the agreement. The USTR announced that the CAFTA-DRwould take effect on a rolling basis when countries fulfilled these obligations. Itentered into force on March 1, 2006 and has been implemented for El Salvador,Honduras, Nicaragua, Guatemala, and the Dominican Republic.

In Costa Rica, CAFTA-DR has been highly controversial because it wouldrequire major restructuring of public sector monopolies over electricity, insurance,and telecommunications. Public sector unions were at the center of this concern, butsmall farmers and other workers also voiced opposition. Oscar Arias won a slimpresidential victory in 2006 on a pro-CAFTA platform, but opposition in the NationalAssembly was able to delay consideration ofthe agreement. In the end, the ElectoralTribunal ruled in favor of a petition to hold a national referendum on the CAFTADR. On October 7, 2007, with a 60% participation rate, the people of Costa Ricavoted 5 1.6% to 48.4% in favor of CAFTA-DR. To be implemented for Costa Rica,the National Assembly must pass 13 implementing bills, which face continuingopposition in the legislature. To date, two have become law and the remainder arein various stages of consideration. Unless otherwise agreed to by all Parties to theCAFTA-DR, the agreement requires that it be implemented within two years of thedate when first entered into force (March 1, 2006), so Costa Rica is running a raceagainst the March 1, 2008 deadline and may yet decide to request an extension.

CRS-2

U.S. Congressional Action

The CAFTA-DR was the most controversial free trade agreement (FTA) vote

since the North American Free Trade Agreement (NAFTA) implementing legislation

was passed in 1993. Many lawmakers were uncomfortable with the agreement as

written, particularly with respect to the labor provisions, treatment ofcertain sensitive

industries (sugar and textiles), investor-state, pharmaceutical data protection, and

basic sovereignty issues. It was also caught up in an overarching congressional

controversy over how trade negotiation objectives are defined in FTAs based on the

Trade Promotion Authority (TPA) framework, as well as, concern by some Members

over the perceived ineffectiveness ofthe executive-legislative consultation process.’

These issues were raised repeatedly in “mock markups” of draft implementing

bills held by the Senate Finance and House Ways and Means Committees on June 14

and 15, 2005, respectively. The Senate Finance Committee voted 11-9 to approve

the draft legislation, with one non-binding amendment that would have extended the

trade adjustment assistance program to cover workers in services industries. The

House Ways and Means Committee voted 25-16 for approval of the draft legislation,

also adding a non-binding amendment with “a requirement that the Administration

report on activities conducted by the CAFTA-DR countries and the United States to

build capacity on labor issues,” and a provision requiring monitoring of CAFTA

DR’s effects on U.S. services industries. A “mock conference” was not held, to the

expressed consternation of some Members.

The Bush Administration sent the final implementing bill to Congress on June

23, 2005. It included a new Section 403, the House amendment requiring that the

Administration transmit biennial reports on progress made in implementing the labor

provisions, including the Labor Cooperation and Capacity Building Mechanism. It

also called for monitoring progress in meeting the challenges outlined in the so-called

White Paper on labor produced by the vice ministers of trade and labor of the

CAFTA-DR countries. Under TPA procedures, identical bills were introduced

jointly as H.R. 3045 and 5. 1307 and referred to the House Ways and Means and

Senate Finance Committees.

The Senate Finance Committee acted first, favorably reporting out S. 1307 by

voice vote on June 29, 2005. The House Ways and Means Committee followed suit,

reporting favorably by a vote of25 to 16 on June 30, 2005. The measure came before

the full Senate on June 30, 2005, where, following 20 hours of floor debate, 5. 1307

passed 54 to 45. H.R. 3045 did not come before the House until July 28, 2005,

where, following two hours of debate, it narrowly passed 217 to 215. On the same

day, the Senate voted 56 to 44 to substitute H.R. 3045 for S. 1307, a necessary

procedural vote to comply with the constitutional requirement that revenue bills

originate in the House. President Bush signed H.R. 3045 into law on August 2, 2005

(P.L. 109-53, 119 Stat. 462).

On TPA, see CRS Report RL743, Trade Promotion Authority: Issues, Options, and

Prospects, by J. F. Hombeck and William H. Cooper.

CRS-3

Passage in the Senate was by a slinuner margin than with earlier tradeagreements and required accommodation outside the implementing legislation tolabor, textile, and sugar interests. In a letter from USTR Rob Portrnan to Senator JeffBingaman, the Administration promised to allocate $40 million offiscal 2006 foreignoperations appropriations for “labor and environmental enforcement capacitybuilding assistance,” and to continue to request this level of funding in budgets forfiscal years 2007 through 2009. Some $3 million is to be used for fundingInternational Labor Organization (ILO) reporting on progress in labor lawenforcement and working conditions in these countries. An additional $10 millionannual commitment for five years was made for transitional rural assistance for ElSalvador, Guatemala, and the Dominican Republic, or until these countries canqualify for anticipated assistance from the U.S. Millennium Challenge Corporation.

In another letter, Secretary of Agriculture Mike Johanns assured Senator SaxbyChambliss and Representative Bob Goodlatte, the respective agriculture committeechairs, that the Administration would not allow the CAFTA-DR to interfere with theoperation of the sugar program as defined in the Farm Security and Rural InvestmentAct of 2002 (the Farm Bill) through FY2007, when it expires. In particular, hepromised to take steps should additional sugar imports due to the CAFTA-DR,NAFTA, and other trade agreements cause the import trigger threshold of 1.532million short tons per year be exceeded and jeopardize the sugar program operations.Should this occur, the U.S. Secretary of Agriculture agreed to preclude entry ofadditional sugar imports into the domestic sweetener market by either making directpayments to exporters or using agricultural commodities to purchase sugar to be usedfor nonfood use (ethanol production).

Separately, for the textile and apparel issues, promises were made to: (1) changethe rules of origin to require that all pocketings and linings come from the CAFTADR countries (rather than third party countries like China); (2) negotiate a newstricter customs enforcement agreement with Mexico before the CAFTA-DRcumulation rules take effect allowing Mexican inputs to be used in CAFTA-DRtextile and apparel products; and (3) require Nicaragua to increase use ofU.S. fabricto qualify as duty-free under their tariff preference levels.

Other accommodations were made to win House support of H.R. 3045,including passage in the House on July 27, 2005, of the U.S. Trade RightsEnforcement Act (H.R. 3283). This bill would allow greater recourse to pursue tradecomplaints against China and other non-market economies. Not all interest groups,however, could be appeased. Despite efforts to win over all groups, the sugarindustry and some textile groups chose not to support the bill and strong Democraticopposition remained over a number of other issues that may prove to be enduringchallenges to future trade agreements, if crafted from the CAFTA-DR framework.,

Why Trade More Freely?

Countries trade because it is in their national economic interest to do so, aproposition long supported by theory and practice. Comparative advantage has beenrecognized for nearly 200 years as a core principle explaining the efficiency gains

CRS-4

that can come from trade among countries by virtue oftheir fundamental differences.

It states that countries can improve their overall economic welfare by producing those

goods at which they are relatively more efficient, while trading for the rest. Intra

industry trade is the other major insight that explains trade patterns, in which the

benefits from exchange among countries occur based on specialized production,

product differentiation, and economies of scale. Many Latin American countries

have liberalized trade policies recognizing the contribution that trade (and related

investment) can make to economic growth and development. As an important

caveat, trade is at best only part of a broad development agenda, and is no substitute

for the promotion ofpolitical freedom, macroeconomic stability, sound institutions,

and the need for complementary social and economic policies.2

Comparative advantage provides the rationale for U.S.-Central American (and

Dominican Republic) trade in agriculture, textiles, apparel, and capital goods. Intra

industry trade (e.g., goods within the same harmonized tariff system (HTS) code

number) is based on specialized production, but in this case relies in large part on

differences in wages, skills, and productivity.3 Certain specialized jobs have

developed in Central America (and other developing countries), where they

frequently reside in production sharing (maquiladora) facilities. Economists have

come to refer to such specialized production as “breaking up the value added chain”

and it accounts for why products (and particularly parts thereof) as diverse as

automobiles, computers, and apparel are often made or assembled in Central America

and other countries in partnership with U.S. firms.4 This relationship, discussed in

more detail later, provides the basis for much of the labor policy debate on the

CAFTA-DR, and FTAs more generally.5

2 The role of trade is summarized well in: Rodrik, Dani. The New Global Economy and

Developing Countries: Making Openness Work. The Overseas Development Council,

Washington, D.C. 1999. p. 137 and Bouzas, Roberto and Saul Keifman. Making Trade

Liberalization Work. Afler the Washington Consensus: Restarting Growth and Reform in

Latin America. Kuczynski, Pedro-Pablo and John Williamson, eds. Institution for

International Economics. Washington, D.C. March, 2003. pp. 158, 165-67.

This differs from the standard intra-industTy case between two developed countries in

which goods, such as automobiles, are exchanged based on product differentiation and

economies of scale and where differences in wage levels are not a central factor.

For the theoretical foundation, see Krugrnan, Paul. Growing World Trade: Causes and

Consequences, in Brookings Papers on Economic Activity (1), William C. Brainard and

George L Perry, eds. 1995. pp. 327-76 and for the case in Central America, see Hufbauer,

Gary, Barbara Kotschwar, and John Wilson. Trade and Standards: A Look at Central

America. Institute for International Economics and the World Bank. 2002. PP. 992-96.

5Note that this trend has not been a driving force in the aggregate unemployment rate of the

United States, but does affect the distribution ofemployment among sectors ofthe economy.

It is also important to emphasize here that wage levels are only part of the issue. Lower

wages correlate closely with lower productivity, hence an abundance of low-skilled (low

productivity) workers attracts these types ofjobs. For a overview of the methodology of

measuring the effects of changes in trade policy, see Rivera, Sandra A. Key Methods for

Quantifying the Effects of Trade Liberalization. International Economic Review. United

States International Trade Commission. January/February 2003.

CRS-5

Measuring the benefits of freer trade is another difficult issue. There is atendency to count exports, imports, and the oft-misrepresented importance of thetrade balance as indicators of the fruits of trade. This approach often gives undueweight to exports at the expense of understanding benefits from imports, where thegains from trade are better understood by their contribution to increased consumerselection, lower priced goods, and improved productivity. For example, high-techintermediate goods imported from developed countries are the basis for future, moresophisticated, production in developing countries. In developed countries, importsfrom developing countries, whether final goods for consumers or inputs formanufacturing enterprises, reduce costs and contribute to productivity and economicwelfare. For all countries, exports are the means for paying for these imports andtheir attendant benefits.

Three caveats related to negotiating FTAs are important. First, the discussionof costs and benefits generally assumes that FTAs are implemented in a multilateralsetting. In fact, given the slow pace of World Trade Organization (WTO)negotiations, many countries are pursuing preferential arrangements, that is, regionaland bilateral agreements like the CAFTA-DR. Latin America is full of them anddepending on how they are defined, they may actually be trade distorting if theypromote trade diversion. This occurs when trade is redirected to countries within alimited agreement that does not take into account countries outside the agreement,some of which may be more efficient producers. Preferential trade agreements arealso cumbersome to manage, requiring extensive rules of origin, and economistsdisagree as to whether FTAs help or hinder the movement toward multilateral tradeliberalization.6

Second, trade, much like technology, is a force that changes economies. Itincreases opportunities for internationally competitive sectors and challenges importcompeting firms to become more efficient or do something else. This fact gives riseto the policy debate over adjustment strategies, because while consumers and exportsector workers benefit, some industries, workers, and communities are hurt.Economists generally argue that it is far less costly for society to rely on various typesof trade adjustment assistance than opt for selective protectionism, the frequent andforcefully argued choice oftrade-affected industries.7 The public policy difficulty isthat both options have costs and benefits, but result in different distributionaloutcomes.8 Because trade agreements raise difficult political choices for legislators

6U5 businesses operating in Latin America have had to interpret a difficult road map whendealing with multiple arrangements defined in the Caribbean Basin Trade Partnership Act,the Andean Trade Preference Act, and the North American Free Trade Agreement. Eachdistorts investment decisions in the region and can have a countervailing influence on theothers. Adding the many Latin American FTAs only makes the situation more confusing.‘ For a recent and accessible treatment of this subject, see Kletzer, Lori G. and HowardRosen. Easing the Adjustment Burden on US Workers. In: Bergsten, C. Fred., ed. TheUnited Stales and the World Economy. Washington, D.C.: Institute for InternationalEconomics, 2005. pp. 313-41.

8Jmpontly, when a staple, such as underwear, is produced abroad and sold in the UnitedStates as a lower-priced import compared to a domestically produced good, it is equivalent

(continued...)

CRS-6

in all countries, many of whom represent both potential winners and losers, FTA

provisions are typically limited in scope (so continue to protect partially or

completely certain products, industries, or sectors) and are phased in over time

(typically up to 15-20 years for very sensitive products).

Third, there are implications in the trade negotiation process for smaller

countries’ bargaining leverage when they choose to negotiate with a large country in

a bilateral rather than multilateral setting. Both Chile and the Central American

countries realized early in the process that there were negotiating issues over which

they would be able to exert little or no leverage. Both agreements, for example, do

not address antidumping and subsidies, reflecting an ongoing congressional concern,

and negotiations on certain agriculture issues were also limited, given the politically

sensitive nature of this issue.

The Impetus for a CAFTA-DR

The United States was motivated by both commercial and broader foreign

economic policy interests in deciding to negotiate preferential trade agreements with

Central America and the Dominican Republic. Geopolitical and strategic concerns

also sparked interest by all parties in pursuing the CAFTA-DR. Proponents expected

the CAFTA-DR to reinforce regional stability by providing institutional structures

that can undergird gains made in democracy, the rule of law, and efforts to fight

terrorism, organized crime, and drug trafficking. The CAFTA-DR may also be a way

to expand support for U.S. positions in the Free Trade Area ofthe Americas (FTAA),

and given that the January 2005 completion date has slipped, may also help

rationalize the system ofdisparate preferential trade agreements that currently define

Western Hemisphere trade relations.

Critics of the CAFTA-DR pointed to equally broad themes, such as the

pervasive social and economic inequality in much of the region, and so supported

strong labor and environment provisions as important negotiating objectives. There

was concern, for example, over the adequacy ofworking conditions and enforcement

of labor laws in the CAFTA-DR countries. The CAFTA-DR countries argued that

the agreement is one of many forces that can have a positive effect in raising labor

standards, although it is not sufficient to accomplish this goal on its own.

With the proliferation of regional agreements around the world, trade

negotiations have also become a tactical issue of picking off gains where they are

perceived relative to what other countries are doing. It was repeatedly argued by the

U.S. business community, for example, that the U.S.-Chile agreement, the first FTA

8 (...continued)to an increase in real income for the U.S. consumer. This can be significant for low-wage

workers in the United States. The same idea holds true for industrial products and business

consumers. So, there is a “trade off’ in the trade policy decision between keeping certain

jobs through protection and losing the income gains, or keeping the income gains and losing

certain jobs. One public policy response has been to pass trade adjustment assistance

legislation to help firms and workers transition more quickly to new opportunities.

CRS-7

after NAFTA, was necessary to equalize treatment ofU.S. businesses competing withCanadian finns that already enjoyed preferential treatment with Chile. The case wasmade for Central America as well, which has trade agreements with Canada andMexico, each with firms that compete with U.S. businesses in the region. Delayswith WTO and Free Trade Area of the Americas (FTAA) negotiations onlyreinforced this attitude.

In the context of regional trade agreements, history, geographic proximity, andeconomic complementarities also made the CAFTA-DR an apparently logical step.9Economic fundamentals shaped a trade relationship based on exports of traditionalagricultural products, and later apparel. From the early days of independence,agricultural exports were the centerpiece ofCentral American economic growth. TheBritish controlled primary export production (coffee, bananas, sugar, and beef) untilabout 1850, when U.S. interests won over. This trend continued until the 1 980s andpassage of the Caribbean Basin Economic Recovery Act (CBERA — P.L. 98-67),as part of the Caribbean Basin Initiative (CB1). By becoming eligible for unilateralpreferential tarifftreatment, U.S. investment increased in the region, fostering growthin Central American export sectors.

A major change to the CBI relationship occurred with passage of the CaribbeanBasin Trade Partnership Act of 2000 (P.L. 106-200). Tn response to repeatedconcerns over trade benefits negotiated with Mexico underNAFTA, Congress passedessentially NAFTA-equivalent treatment for the CBI countries. CBTPA targetedpreferences on textile, apparel, and other high-volume export goods not coveredunder the original CBI legislation. The benefits were extended temporarily for aperiod ending September 30, 2008, or until a beneficiary country enters into an FTAwith the United States.

The U.S.-Central American/Dominican Republic economic relationship changedimportantly under the CBTPA, creating an environment in which businesses forgedstrategic partnerships in the increasingly complex world of textile and garmentmanufacturing. From 1974 until 1995, global rules restricting trade in apparelbetween developed and developing countries (mostly quotas) were set out in theMultifiber Arrangement (MFA) and its successor, the WTO-sponsored Agreementon Textiles and Clothing (ATC), which served as a transitional arrangement to aquota-free system begun on January 1,2005. In this context, the CBTPA preferencesprovided an import benefit for the region’s export sectors.1°

The United States created the CBIJCBTPA to foster Caribbean economicdevelopment and to assist U.S. industry in responding to competition from similarproduction-sharing arrangements in Asia that were taking a toll on U.S. productionand employment in the textile and apparel industries. Still, U.S. textile andparticularly apparel industries have been hit hard by foreign competition, resulting

For an excellent economic history of the region, see Woodward, Ralph Lee Jr. CentralAmerica: A Nation Divided New York: Oxford University Press, third edition, 1999.10 For more on the evolution of these trade preference arrangements, see CRS ReportRL3395 1, US. Trade Policy and the Caribbean: From Trade Preferences to Free TradeAgreements, by J. F. Hombeck.

CRS-8

in a total job loss ofover 540,000 employees from 1998-2002.” The textile industry

(e.g., fiber, yams, fabric) has remained marginally competitive through use of

sophisticated production technologies. The apparel manufacturing industry (e.g.,

shirts, pants, undergarments) by contrast, is highly labor intensive, and in striving to

reduce costs, has moved production offshore to lower-wage countries.

As defined in the CBTPA, U.S. firms, through subsidiary or contractual

anangernents, are required to use mostly U.S. textiles as inputs to products that are

assembled and exported back to the United States — a mutually beneficial strategy.

In 2002, some 56% of U.S. apparel and textile imports from Central America was

assembled from U.S. materials, compared to less than 1% for apparel imports from

China.’2 Although this was a controversial move because of the reliance on foreign

low-wage workers to the detriment of some U.S. employment, many economists

argued that the alternative would have been an even greater loss of textile and

garment jobs to Asian competitors that use no U.S. inputs.’3

With the removal oftextile and apparel quotas in January 2005, the trade picture

changed again. The CAFTA-DR countries were already losing U.S. market share,

which from 1997 to 2002 declined from 11.7% to 9.4%. Over the same time period,

China’s market share increased from 9.1% to 13.0%. Given that U.S. textile and

apparel imports from CAFTA-DR countries are heavily concentrated in products

previously covered by quotas, the dominance of China and other low-cost Asian

producers is likely to continue. CAFTA-DR producers are less competitive on a pure

cost basis because of their higher labor costs relative to Asia, the CBTPA

requirement to use more expensive U.S. inputs, and the additional administrative

costs associated with U.S. preferential trade requirements.’4

Low-cost labor, however, is not the only or even the most important factor

driving competitiveness.’5 Studies suggest that the economic and social networks

that developed between U.S. and Central American firms effectively created a niche

“ United States International Trade Commission (USITC). The Economic Effects of

SignfIcant US. Import Restraints. Publication 3701. Washington, DC, June 2004. p. 60.

12 USITC. Production-Sharing Update: Developments in 2001. Industiy Trade and

Technology Review. November 2003. PP. 22 and B-l-4.

13 Chacón, Francisco. International Trade in Textile and Garments: Global Restructuring

of Sources of Supply in the United States in the I 990s. Integration and Trade, Vol. 4, No.

11, May-August 2000. Inter-American Development Bank, Washington, D.C. and United

States International Trade Commission. Production-Sharing Update: Developments in 2002.

Industry Trade and Technology Review. November 2003. p. 12.

‘‘ United States International Trade Commission. Textiles and Apparel: Assessment ofthe

Competitiveness ofCertain Foreign Suppliers to the US. Market. USITC Publication 3671.

Washington, D.C. January 2004. pp. 1-12, 3-22, and 3-33-35.

more subtle distinction made by one economist notes that, “How comparative advantage

is created matters. Low-wage foreign competition arising from an abundance of workers

is different from competition that is created by foreign labor practices that violate norms at

home. Low wages that result from demography or history are very different from low wages

that result from government repression ofunions.” See Rodrik, Dani. “Sense and Nonsense

in the Globalization Debate.” Foreign Policy. Summer 1997. p. 28.

CRS-9

market in the region for certain apparel that has held up even with the growingpresence of China in the market. This relationship was made possible by theproximity of production, operational efficiencies, and quick turn around times formeeting increasingly shortened deadlines demanded by large retailers. In a post-quota trading world, these advantages may allow a certain portion of textile andapparel production to remain in the CAFTA-DR countries. Although CAFTA-DRcountry representatives have emphasized that the passage ofthe free trade agreementis a critical component for maintaining this strategy, it is not certain that it cancounter the long-tenri trend in market share loss to Asia.’6

Strategic considerations were important, but ultimately it is fair to ask what eachcountry expects to gain commercially from the detailed agreement that has emerged.The dollar value of U.S. trade with Central America makes the region the UnitedStates’ third largest Latin American trading partner, right behind Brazil, but a fardistant third from Mexico. Still, these are small economies (see Appendix 2 foreconomic data) and although firms engaged in this trade may fmd its effectssignificant, total CAFTA-DR trade in 2004 represented only 1.5% of U.S. foreigncommerce, and so can be expected to have only a small macroeconomic effect.

For the United States, an FTA is a more balanced trade arrangement than theunilateral preferences provided in the CBIICBTPA. Market access issues (e.g., tariffrates, quotas, rules of origin) were core negotiating areas. Although CentralAmerican and Dominican tariffs were already relatively low, they were reducedfurther. In particular, U.S. business interests wanted equal or better treatment thanthat afforded to exports from Canada and Mexico based on their FTAs with CentralAmerican countries. Permanent and clarified trade rules also supported the jointproduction arrangements already in place between U.S. firms and those in the region.Finally, a bilateral agreement offered the United States a chance to deepen other tradecommitments that affect some of its most competitive industries, including rulescovering the treatment of intellectual property, foreign investment, governmentprocurement, e-commerce, and services.

From the Central American and Dominican perspectives, reducing barriers tothe U.S. market (especially for textile and agricultural products) was cause enoughto proceed. The CAFTA-DR also made permanent and expanded U.S. benefits givenunder the CBTPA legislation, but which require reauthorization by Congress.Permanence in trade rules is an enticement for U.S. foreign direct investment (FDI),which in turn can support the region’s export driven development strategy.

The CAFTA-DR countries also faced important vulnerabilities, such as thepossibility that U.S. agricultural exports of key staples, such as corn and rice, mightoverwhelm their small markets. Sensitivity to these and other key industry sectorswere addressed in the extended tariff phase-out and safeguard schedules, and as a

‘6USITC, Textiles andApparel, pp. 3-33, 4-2-4. Gereffi, Gary. The Transformation of theNorth American Apparel Industry: Is NAFTA a Curse or a Blessing? Integration andTrade. Vol. 4, No. 11. May-August 2000. Inter-American Development Bank. pp. 56-57.

CRS-1O

matter of development policy, by CAFTA-DR country efforts to diversify the

agricultural sector into non-traditional exports and non-farm employment.’7

Finally, there were two significant negotiation challenges. The first was the

need for better Central American integration as part of CAFTA-DR, which

historically has been hampered. Having multiple trade rules and rules of origin in a

small sub-region would complicate the trade picture. For the CAFTA-DR to work

well, the United States needed some assurance that goods would flow efficiently

within the region, which will be a significant benefit of the agreement, particularly

with Costa Rica heading toward ratification of CAFTA-DR. Second, there was a

difference in negotiating capacity between Central America and the United States.

U.S. and multilateral offers to assist these countries in developing such capacity were

viewed as generous, but also a little self-serving, which required sensitivity in the

negotiation process.

U.S. Trade Relations with Central Americaand the Dominican Republic

“Docking” the Dominican Republic FTA to CAFTA added the largest of six

trading partners covered by the CAFTA-DR agreement. Total U.S. trade with the

Dominican Republic in 2004 was one-third greater than with either Costa Rica or

Honduras, which tie as the next largest U.S. trading partner in Central America.

What made the process feasible was the Dominican Republic’s willingness to accept

the basic framework and rules ofCAFTA, while negotiating market access and some

other issues bilaterally, as was done with each ofthe five Central American republics.

In addition, the Dominican Republic’s economy and export regime are, in many

ways, similar to those of Central America. U.S.-Dominican Republic trade was

added to an earlier version of this report and is discussed in more detail separately.

U.S.-Central America Trade

Because ofits huge size and geographical proximity, the U.S. market is a natural

destination for Central American exports. Merchandise trade with the United States

has dominated Central America’s foreign commerce for 1 50 years, and as seen in

Figure 1, remains in that role today.

17 The CAFTA-DR countries have begun new exports projects in areas such as miniature

vegetables, cut flowers, cable manufacturing, among others, in expectation that moving

beyond subsistence agriculture and textile manufacturing is critical to achieve economic

diversification and development. What distinguishes this effort from the earlier agricultural

export model is the emphasis on integrating small producers into the export system. The

idea is not only to tap into naturally small production capabilities, but to help bring social

development to areas that previously were not integrated into the agricultural export

development model. It is still a relatively small effort and its widespread application has yet

to be fully realized, but the CAFTA-DR countries see the FTA as supporting this strategy.

CRS-ll

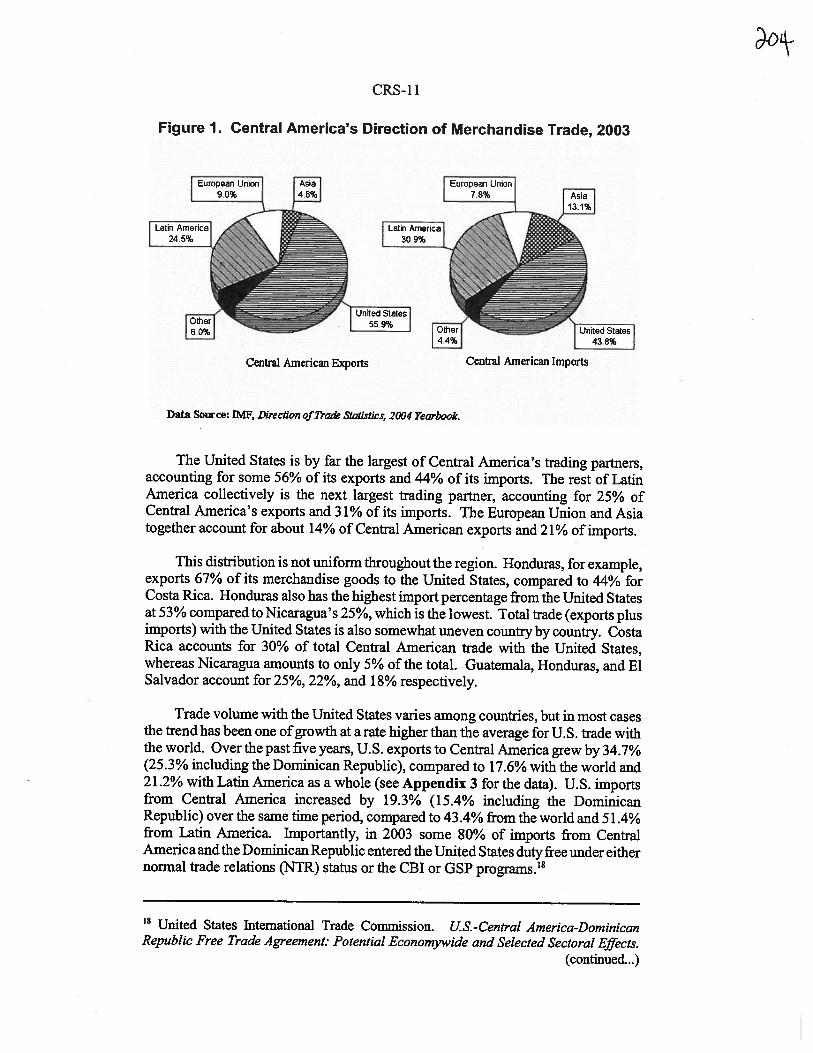

Figure 1. Central America’s Direction of Merchandise Trade, 2003

Data Source: IMF, Direction ofTrade StaIisIics 2004 Yearbook.

The United States is by far the largest of Central America’s trading partners,accounting for some 56% of its exports and 44% of its imports. The rest of LatinAmerica collectively is the next largest trading partner, accounting for 25% ofCentral America’s exports and 31% of its imports. The European Union and Asiatogether account for about 14% of Central American exports and 21% of imports.

This distribution is not uniform throughout the region. Honduras, for example,exports 67% of its merchandise goods to the United States, compared to 44% forCosta Rica. Honduras also has the highest import percentage from the United Statesat 53% compared to Nicaragua’s 25%, which is the lowest. Total trade (exports plusimports) with the United States is also somewhat uneven country by country. CostaRica accounts for 30% of total Central American trade with the United States,whereas Nicaragua amounts to only 5% of the total. Guatemala, Honduras, and ElSalvador account for 25%, 22%, and 18% respectively.

Trade volume with the United States varies among countries, but in most casesthe trend has been one of growth at a rate higher than the average for U.S. trade withthe world. Over the past five years, U.S. exports to Central America grew by 34.7%(25.3% including the Dominican Republic), compared to 17.6% with the world and21.2% with Latin America as a whole (see Appendix 3 for the data). U.S. importsfrom Central America increased by 19.3% (15.4% including the DominicanRepublic) over the same time period, compared to 43.4% from the world and 51.4%from Latin America. Importantly, in 2003 some 80% of imports from CentralAmerica and the Dominican Republic entered the United States duty free under eithernormal trade relations (NTR) status or the CBI or GSP programs.18

Central American Exports Central American Imports

United States International Trade Commission. US.-Central America-DominicanRepublic Free Trade Agreement: Potential Econoniywide and Selected Sectoral Effects.

(continued...)

CRS-12

For 2004, although trade growth varied among the five countries, U.S. export

growth to Central America doubled average export growth to the world, with all five

countries experiencing solid growth. U.S. imports from Central America, by

contrast, grew by less than half that of average import growth from the world. As

these trends suggest, the United States tends to run small merchandise trade deficits

with all the Central American countries and the Dominican Republic. In part, this

is the nature ofa production-sharing trade relationship, where parts and materials are

sent abroad for value-added processing and then returned to the United States.

Importantly, when services trade is added to the trade balance, the United States

tends to run trade surpluses with all these countries. This trend, too, is indicative of

the basic relationship between the United States, a service-based economy, and

developing countries.’9

U.S. Imports. Nearly three-quarters ofU.S. imports from Central America fall

into three main categories: fruit (mostly bananas) and coffee; apparel; and integrated

circuits. These three distinct categories, for various reasons, are not traded uniformly

by the five countries (see Table 1).

First, Central America has traditionally exported bananas and coffee, which is

dominated by Costa Rica and Guatemala. Coffee has actually declined for all

countries except Costa Rica and constitutes only 3.8% of U.S. imports from the

region. This reflects the competitive nature oftrade in coffee, which is grown in vast

quantities by Brazil, Colombia, and countries in Africa as well. Banana trade has

also declined in importance and accounts for only 5.0% ofU.S. imports from Central

America.

Second, knit and woven apparel has become the primary export goods for all

countries except Costa Rica and accounts for nearly 57% of total U.S. imports from

Central America. Because ofthe CBTPA benefits, some 56% oftextiles and apparel

imported from the six CAFTA-DR countries in 2002 was assembled from U.S. fabric

(from U.S. yarns). Of that amount, the Dominican Republic had 33% of the total

followed by Honduras with 30%, El Salvador with 18%, Costa Rica with 9%,

Guatemala with 8%, and Nicaragua with 2%. Under the CBTPA, these countries

may engage in greater value-added operations such as cutting and dyeing, which has

allowed them to remain selectively competitive with low-cost Asian exports. These

restrictions are further relaxed under the CAFTA-DR.2°The USITC points out that

‘ (...continued)USITC Publication 3717. August 2004. p. 7.

‘ This trend is not disputed, but the U.S. Department of Commerce does not disaggregate

U.S. bilateral services trade data with the Central American countries. Estimates are

provided in some of the Country Commercial Guides produced by the U.S. Department of

Commerce based on foreign country reporting.

20 United States International Trade Commission. Production-Sharing Update:

Developments in 2001. Industi-v Trade and Technology Review. November 2003. pp. 13,

22, Bl-4.

CRS-13

the CAFTA-DR countries have been losing market share to Asia since at least 1997,‘1and the CAFTA-DR is seen as a way to help abate this trend:

Table 1. Top Eight U.S. Merchandise Imports from CentralAmerica, 2004

($ millions): -

4pduct and HTSa4Total C R. .- Hon Guat El Sal Nic

-.-..

Total U.S. liriports 13,172 3,333 3,641 3,155 2,033 991

Top 8 as % of Total 83.7% 72.5% 89.6% 86.8% 88.5% 8 1.5%Data Source: U.S. Department of Commerce.#HTS = Harmonized Tariff Schedule

Third, Costa Rica attracted $500 million in foreign direct investment for acomputer chip assembly and testing plant, which has become its major exportgenerator. This investment was augmented by an additional $110 million in October2003 for the production line of “chipsets” for personal computers. In 2004, U.S.imports of integrated circuits constituted 18% of total imports from Costa Rica.Similar importance may be seen in the imports of Costa Rica’s medical equipment,another indicator of its relatively sophisticated production capabilities. Costa Ricais the fastest growing and most diversified trader in Central America, which explains,in part, why it has outpaced its neighbors on the development path.22

The CAFTA-DR is intended to build on these trends, support exportdiversification, and provide a long-term stable trade environment that will increaseU.S. foreign investment in the region. Evidence is already seen in alternativeagricultural exports such as cut flowers and miniature vegetables (in multipleCAFTA-DR countries), as well as, developing maquiladora operations to suppiy coilwrapped cables for the automotive sector (Honduras) and adapting apparel cuttingtechnology to supply insulation for aircraft engines (Costa Rica). Many non-apparel

21 USITC, Textiles and Apparel, p. 1-12.22 Hufbauer, Kotschwar, and Wilson, op. cit., p. 1003.

CRS-14

items that the United States imports from Central America face minimal or no tariffs.

Bananas, coffee, oil, most fish products, and Costa Rica’s integrated circuits and

medical equipment enter duty free. Some enter the United States under preferential

arrangements, but the majority is free of duty under normal (most favored nation —

MFN) tariff rates. Rules on U.S. apparel imports were enhanced and made

permanent under CAFTA-DR.

U.S. Exports. As seen in Table 2, the major U.S. exports to Central America

include electrical and office machinery (computers), apparel, yarn, fabric, and plastic.

Many of these goods are processed in some form and re-exported back to the United

States under production-sharing arrangements. For example, nearly 60% ofelectrical

machinery exports to Central America is integrated circuits going to Costa Rica for

processing and re-export. The same may be said for fabric and yams that are

exported to all countries, sewn and otherwise assembled, and re-exported back to the

United States. Some ofthese goods are consumed in the CAFTA-DR countries along

with capital goods (machinery and parts) and agricultural products.

Table 2. Top Eight U.S. Merchandise Exports to CentralAmerica, 2004

$ millions)

Product and HTS Costa PTotal . Hon Gnat El Sal Nic

Numbea. Thca

Total U.S. Exports 11,388 3,304 3,077 2,548 1,868 592

-Computer Parts (8471) (136) (43) (20) (32) (26) (10)

Cotton Yam, Fabric (52) 780 18 412 241 84 23

Mineral Fuel (27) 712 93 239 313 57 10

Knit/Crocheted Fabric 60 688 38 351 24 272 3

Plastic (39) 657 253 123 181 87 13

KnitApparel(61) 624 101 312 33 176 2

Cereals (10) 559 156 92 118 125 68

-Corn (1005) (242) (71) (31) (65) (64) (10)

-Wheat and Meslin 1001 (167) (38) (28) (34) (46) (21)

-Rice (1006) (149) (46) (33) (18) (16) (37)

Other 4,639 1,252 1,168 1,176 705 336

Top 8 as % of Total 59.3% 62.1% 62.0% 53.8% 62.3% 43.2%

Data Source: U.S. Department of Commerce. HTS Harmonized Tariff Schedule

Similar trends for U.S. import trade are evident in U.S. exports. In 2004, 78%

of knit apparel and 76% of knit, cotton, and yarn fabric went to Honduras and El

Salvador. Although the United States exports machinery and parts to all five

countries, electrical machinery and particularly integrated circuits, are sent to Costa

Rica. All five countries import U.S. cereals and some, such as corn and rice, are

CRS-15

among the more import sensitive products for the CAFTA-DR countries because theyare staple crops and grown by small, often subsistence fanners.23

The significant aspects of this trade structure are that it reflects: 1) the continuedhistorical trend of (largely duty-free) regional dependence on the large U.S. marketas an important aspect of trade and development policy; 2) a deepening economicintegration; and 3) growing U.S. direct investment over the long run.

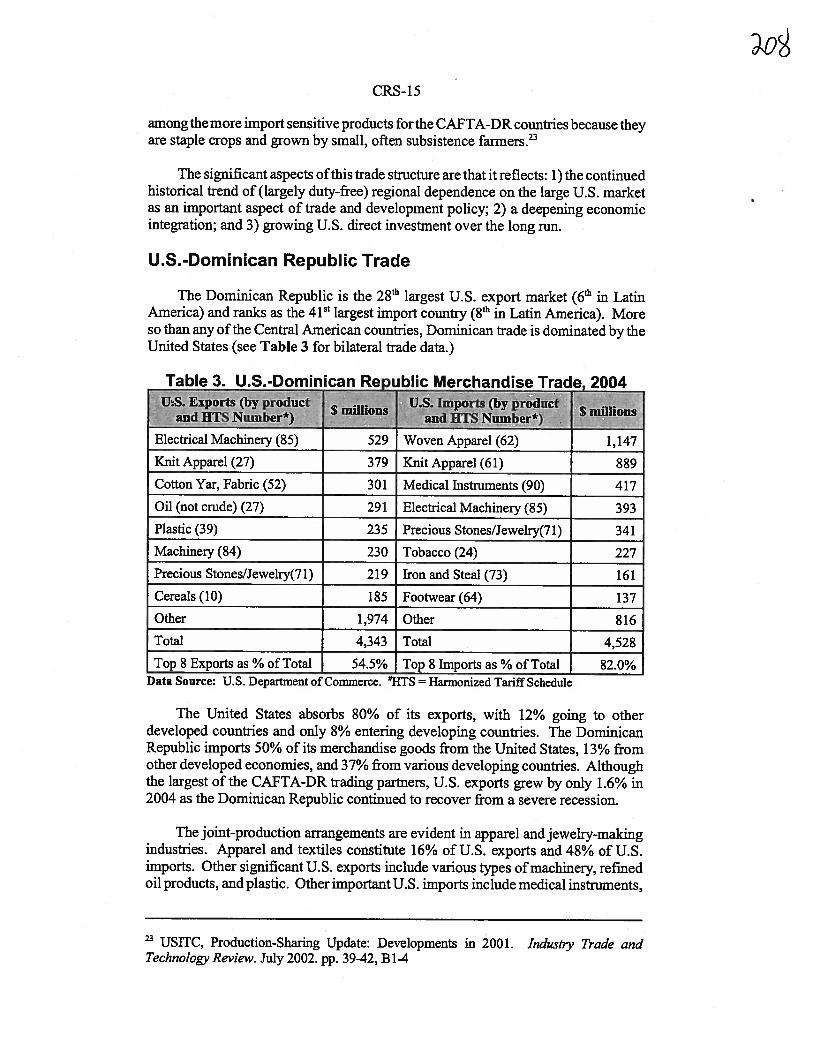

U.S.-Dominican Republic Trade

The Dominican Republic is the 28t largest U.S. export market (6th in LatinAmerica) and ranks as the 41st largest import country (8th in Latin America). Moreso than any of the Central American countries, Dominican trade is dominated by theUnited States (see Table 3 for bilateral trade data.)

Precious Stones/Jewelry(71) 219 fron and Steal (73) 161

Cereals (10) 185 Footwear (64) 137

Other 1,974 Other 816

Total 4,343 Total 4,528

Top 8 Exports as % of Total 54.5% Top 8 Imports as % of Total 82.0%Data Source: U.S. Department of Commerce. #HTS = Harmonized Tariff Schedule

The United States absorbs 80% of its exports, with 12% going to otherdeveloped countries and only 8% entering developing countries. The DominicanRepublic imports 50% of its merchandise goods from the United States, 13% fromother developed economies, and 37% from various developing countries. Althoughthe largest of the CAFTA-DR trading partners, U.S. exports grew by only 1.6% in2004 as the Dominican Republic continued to recover from a severe recession.

The joint-production arrangements are evident in apparel and jewelry-makingindustries. Apparel and textiles constitute 16% of U.S. exports and 48% of U.S.imports. Other significant U.S. exports include various types of machinery, refinedoil products, and plastic. Other important U.S. imports include medical instruments,

USITC, Production-Sharing Update: Developments in 2001. Industry Trade andTechnology Review. July 2002. pp. 39-42, Bl-4

-o9CRS-16

electrical machinery, tobacco, and plastic. In many ways, the structure of the U.S.-

Dominican trade is similar to that of U.S.-CAFTA trade, and hence the economic

logic of “docking” it to the Central American agreement.

U.S. Foreign Direct Investment

The CAFTA-DR countries also benefit from foreign direct investment (FDI) as

part of the trade relationship with the United States, which is the largest foreign

investor in all six countries. To the extent that an FTA can be considered a

stabilizing factor in economic relationships, it is expected to encourage more FDI and

thereby promote longer term economic growth and development. U.S. FDI in the

CAFTA countries is presented in Table 4.

The trends suggest that U.S. direct investment in the area is relatively small and

has stagnated or grown erratically in recent years. Some countries have fared better

than others and net foreign investment may increase or decrease because of both

economic and political trends, as well as opportunities in other parts of the world that

can affect business decisions. Investment patterns have been skewed toward Costa

Rica, which has over half of U.S. FDI in Central America.

Table 4. U.S. Foreign Direct Investment (FDI)in CAFTA-DR Countries

(S millions)

Country 1999 2000

Costa Rica 1,493 1,716 1,835 1,802 1,831

El Salvador 621 540 464 684 779

Guatemala 478 835 311 303 294

Honduras 347 399 227 181 270

Nicaragua 119 140 157 250 261

Total Central America 3,058 3,630 2,994 3,220 3,435

Dominican Republic 968 1,143 1,116 983 860

Total CAFTA-DR 4,026 4,773 4,1 10 4,203 4,295

Data Source: U.S. Department of Commerce. Bureau of Economic Analysis. Available at

[http://www.bea.doc.gov/bealdilusdlongcty.htmj. Data are stock of FDI on a historical-cost basis.

Review of the CAFTA-DR

One aspect of the congressional debate over trade agreements focused on their

potential economic effects on the United States. Congress mandated that the United

States International Trade Commission (USITC) assess these effects and it released

its final report in August 2004. This report provides quantitative and qualitative

estimates of the CAFTA-DR effects on the U.S. economy as a whole and for selected

sectors. Overall, it found that the “welfare value” or aggregate effect on U.S.

consumers and households of trade liberalization under the CAFTA-DR would be

lD

CRS-17

approximately $166 million (less than 0.0 1% of GDP) for each year the agreementis in effect.24

With respect to trade flows, the reduction ofrelatively higher tariffrates on U.S.goods is expected to increase U.S. exports more than imports with the region. TheUSITC model estimates that when the CAFTA-DR is fully implemented, U.S.exports to the CAFTA-DR countries will increase by $2.7 billion or 15%, whileimports will increase by $2.8 billion, or 12%. The effect of this trade growth onaggregate U.S. output and employment is estimated to be minimal. The largest sectorincreases were estimated to occur for U.S. grains (0.29% for output and 0.3 1% foremployment) and the greatest decrease to occur for sugar manufacturing (-2.0% forboth output and employment).25 These estimates are in line with expectations madeprior to the negotiations that the marginal effects of the CAFTA-DR will be small,but positive for the U.S. economy as a whole, given the CAFTA-DR countries hadsmall and already largely open economies.

The rest of this section briefly summarizes the major negotiation issues andreferences the ITC’s conclusions with respect to each major issue area, whereapplicable. Emphasis is given to those sectors and issues expected to be mostaffected by the agreement, or that generated the most contentious policy debate.

Market Access

Market access refers to provisions that govern barriers to trade such as tariffs,quotas, safeguards, and rules of origin, which define goods eligible for tariffpreferences based on their regional content. CAFTA-DR replaces and enhances ina permanent agreement U.S. preferential market access extended unilaterally underthe Caribbean Basin Economic Recover Act (CBERA), the Caribbean Basin TradePartnership Act (CBTPA), and the Generalized System ofPreferences (GSP), whichrequire periodic congressional reauthorization (except CBERA). Agriculture andtextile/apparel goods, Central America’s major exports, were the most important anddifficult market access issues to resolve.

Each traded good falls into one of eight tariff elimination “staging categories,”which defme the time period over which customs duties will be eliminated. Eachcountry negotiated a list of its most sensitive products for which duty-free treatmentis delayed. For manufactured goods, duties on 80% ofU.S. exports were eliminatedimmediately, with the rest phased out over a period of up to 10 years.26 Foragricultural goods, duties on over 50% ofU.S. exports were eliminated immediately,with the rest phased out over a period of up to 20 years. In some cases, duty-freetreatment is “back loaded” and will not begin for 7 or 12 years after the agreement

24 USITC, US.-C’entral America-Dominican Republic Free Trade Agreement, p. 64. Thestudy reviews literature on the CAFTA-DR and makes estimates of the economywide andsectoral effects of trade liberalization under CAFTA-DR based on a computable generalequilibrium (CGE) model. For details, see pages xiv, 2, and Appendix D.25 Ibid., pp. xxii and 64-70.26 Ibid., p. 25.

CRS-18

takes effect. For the CAFTA-DR countries, 100% ofnon-textile and non-agricultural

goods enter the United States duty free immediately.27 Safeguards are retained for

many products over the period ofduty phase out, but antidumping and countervailing

duties were not addressed in the CAFTA-DR, leaving all U.S. and other country trade

remedy laws fully enforceable, as required under Trade Promotion Authority (TPA).

Textiles and Apparel. The CAFTA-DR has less restrictive provisions

governing textile and apparel imports than those in the CBTPA. It removes all duties

on textile and apparel imports that qualify under the agreement’s rules of origin,

retroactive to January 1, 2004, and allows for special safeguard measures during the

duty phase-out period. The penrianence of the provisions and the more

accommodating rules of origin and administrative guidelines may generate a

marginal increase in apparel imports from the region. These provisions are intended

to address the decline in U.S. market share of textile and apparel imports from the

region over the past five years, most ofwhich have been displaced by Asian products,

despite the enhanced preferential treatment that Congress afforded to Central

American and Dominican imports under the CBTPA.28

Central American and Dominican apparel has been entering the United States

duty free for years, if it is assembled from U.S. yam and fabric under the so-called

“yarn forward” rule. The difference from the CBTPA is that duty-free access applies

to textiles and garments assembled from components made in either the CAFTA-DR

countries or the United States, rather thanjust the United States.29 Exceptions to this

rule include an enhanced “cumulation rule,” which allows duty-free treatment for a

limited quantity ofwoven apparel assembled from components made in Canada and

Mexico, to help U.S. textile firms invested in these countries. In addition, there are

exceptions for specified products (affecting less than 10% of trade), goods with

limited amounts of material from third countries, and for tariff preference levels

(TPLs) given to a few imports from Nicaragua and Costa Rica.

Although these rules were widely supported, some textile producers registered

concern that they are overly restrictive and therefore limited in their intended effect

of helping the region compete (by lowering costs) in the U.S. market against Asian

imports. U.S. and CAFTA-DR firms that produce for the U.S. market wanted as

much flexibility as possible to use fabrics from third countries. Others feared,

however, that they are too generous and that if customs procedures are not well

implemented, they could harm U.S. producers by increasing opportunities for the

illegal transshipment of fabrics or goods originating from outside the region, such as

China. There was also considerable debate over the expansion from the CBTPA of

the “short-supply” list. This is the list of goods given duty-free access if made from

materials that are determined to be commercially in “short supply” in the United

States. The CAFTA-DR may also increase U.S. exports of textiles, which have risen

27 Office of United States Trade Representative. Free Trade with Central America:

Summary ofthe US. -central America Free Trade Agreement. p. 1. Hereafter cited as the

CAFTA Suminaty. It may be found at [http://www.ustr.govj.

28 USITC, U.S. -Central American-Dominican Free Trade Agreement, pp. 28-29.

29 See CRS Report RS22 150, CAFTA-DR: Textiles andApparel, by Bernard A. Geib. p. 4.

CRS-19

significantly under CBTPA. On balance, however, the USITC study estimated thatit “will likely have a negligible impact on U.S. production or employment.”30

Concerns raised by certain sectors of the textile and apparel industry requiredassurances from the Bush Administration before support would be given to theCAFTA-DR. Promises were made to: (1) change the rules of origin for textiles andapparel to require that all pocketings and linings come from the CAFTA-DRcountries (rather than third party countries like China); (2) negotiate a new strictercustoms enforcement agreement with Mexico before the CAFTA-DR cumulationrules take effect allowing Mexican inputs to be used in CAFTA-DR textile andapparel products; and (3) require Nicaragua to increase use of U.S. fabric to qualifyas duty-free under their tariff preference levels. These assurances are not part of theformal CAFTA-DR, but have been implemented nonetheless.3’

Agriculture. Domestic support programs were not addressed in the CAFTADR, which focused on reducing tariffs and increasing quota levels, the most costlytrade-distorting policies. Average applied tariffs on agricultural goods by mostCAFTA-DR countries are relatively low, ranging from 7% to 23%. Most agriculturalimports face no tariff in the United States. For all countries, the pressing challengewas negotiating tariff rate quotas (TRQs — see below) for their most sensitiveproducts.32 Agricultural products have the most generous tariffphase-out schedules,with up to 20 years for some products (e.g., rice and dairy). This approachacknowledges that the agricultural sectors bear most ofthe trade adjustment costs andthat they will require time to make the transition to freer trade.33

All agricultural trade eventually becomes duty-free except for sugar importedby the United States, fresh potatoes and onions imported by Costa Rica, and whitecorn imported by the other Central American countries. These goods will continueto be subject to quotas that will increase, after a certain period, by approximately 2%each year in perpetuity, with no decrease in the size of the above-quota tariff.34 Overhalf of current U.S. farm exports to Central America became duty free upon

30CRS Report P.132895, Textile Exports to Trade Preference Regions, p. 2, by Bernard A.Geib. Inside U.S. Trade. CAFTA Textile Rules Pave Wayfor Increase in Foreign FabricUse. December 19, 2003 and Press Release. NTA Denounces CAFTA as Threat to US.Textile Industry. December 18, 2003 and USTR, CAFTA Summary, p. 2 and USITC, US.-Central American-Dominican Republic FTA, p. 30-32. Nicaragua received specialpreferential treatment for certain “non-originating apparel goods”(Annex 3.27) and CostaRica received limited special treatment for certain wool apparel goods (Annex 3.28).31 Washington Trade Daily, Tide Risingfor CAFTA Portman, July 26, 2005.32 For more details, including sanitary and phytosantiary (SPS) provisions, see CRS ReportRL32 110, Agricultural Trade in the US. -Dominican Republic-Central American FreeTrade Agreement (CAFTA-DR), by Remy Jurenas.‘ Salazar-Xirinachs, Jose M. and Jaime Granados. The US-Central America Free TradeAgreement: Opportunities and Challenges. In: Schott, Jeffrey J. ed. Free TradeAgreements: US Strategies and Priorities. Washington, D.C. Institute for InternationalEconomics. 2004. pp. 245-46.“ CRS Report RL321 10, Agriculture in the US.-Dominican Republic-CentralAmericanFree Trade Agreement (CAFTA-DR,), by Remy Jurenas.

CRS-20

implementation, including high quality cuts ofbeef, cotton, wheat, soybeans, certain

fruits and vegetables, processed food products, and wine.

Many other transitional provisions exist. Agricultural products are subject to

tariff-rate quotas, or limits on the quantity of imports that can enter the United States

before a very high tariff is applied. The phased reduction in agriculture protection

also includes the transitional use of volume-triggered safeguards, or applying an

additional duty temporarily on products that are being imported in quantities deemed

a threat to the domestic industry.35 Export subsidies are eliminated except when

responding to third party export subsidies.

Sugar was the most controversial agricultural issue to resolve and U.S. sugar

growers and processors were vehement opponents of the agreement to the end. The

U.S. agreed to slight numerical increases in sugar quotas for all six countries. Sugar

and sugar-containing products imported under the U.S. quota system enter the United

States duty-free, but exports above the quota face prohibitive tariffs. Raw sugar

receives the largest quota by volume, 28% of the total U.S. sugar quota for the world

was filled by the CAFTA-DR countries in 2003, and was a major issue for this

agreement. The U.S. market accounts for only 14% of the region’s sugar exports,

representing less than 10% of the region’s sugar production.36

The CAFTA-DR raises the U.S. quota by an amount equal to 35% ofthe current

quota in year one, rising to 50% by year 15, after which the quota increases each year

slightly in perpetuity. This may seem large, but the USITC notes that the initial

increase amounts to only 1% of U.S. production and consumption of raw sugar in

2003, and that the overall effects of the sugar provisions may be small. Two studies

done by the USITC and Louisiana State University estimated that the sugar

provisions could result in a decline in sugar prices of 1% (USITC) and 4.6% (LSU),

with perhaps largely offsetting employment effects in the sugar producing and sugar-

containing product industries.37 The United States may impose a sugar price

mechanism to compensate Central American sugar exporters in lieu of according

them duty-free treatment, but a key issue for some Members of Congress was

defining precisely how this mechanism will work.

Nonetheless, the sugar producing industry remained unsatisfied with these

provisions. The Bush Administration responded in a letter from Secretary of

Agriculture Mike Johanns to Senator Saxby Chambliss and Representative Bob

Goodlatte, the respective agriculture committee chairs, assuring the industry that the

CAFTA-DR would not be allowed to interfere with the operation of the sugar

program as defmed in the Farm Security and Rural Investment Act of2002 (the Farm

Bill) through FY2007, when it expires. In particular, he agreed to act should

u For example, in the case of beef the Central American countries have agreed to the

immediate elimination of tariffs on U.S. prime and choice cuts, but have a 15-year tariff

phase-out on other products, with a backloaded schedule (no tariff reductions in the early

years) and a safeguard. The United States has a 26% out-of-quota tariff on beef that will be

phased out over 15 years, with the quota schedule defined for each country.

36 USITC, U.S.-CentralArnerican-Dorninican Free Trade Agreement, p. 35.

Ibid., pp. 38-40.

CRS-21

additional sugar imports due to the CAFTA-DR, NAFTA, and other trade agreementscause the import trigger threshold of 1.532 million short tons per year to be exceededand threaten the sugar program operations. The U.S. Secretary ofAgriculture agreedthat in such a case, he would preclude entry of additional sugar imports into thedomestic sweetener market by either making direct payments to exporters or usingagricultural commodities to purchase sugar to be used for nonfood use (ethanolproduction). This offer also proved inadequate to bring about sugar industry supportfor the CAFTA-DR.

Increasing grain exports was another important goal for the United States.Wheat is not grown in the CAFTA-DR countries and there is already largely freetrade in this commodity. Staples for the CAFTA-DR countries, such as rice andwhite corn, however, remain protected and there is a complicated system for phasingout TRQs on U.S. exports over a 15-20 year period. As with sugar imports to theUnited States, U.S. exports of corn and rice will increase slowly due to the highlyrestrictive TRQs and special safeguard measures. The USITC estimates that changesin the quantity of exports from the United States will be small at first and rise byperhaps 20% by the end of the TRQ phase-out period. The USITC suggests that thelong-run effect may be small (1.2% of total U.S. grain exports), but notes that the“potential increase in grains exports offers significant market opportunities for U.S.white and yellow corn growers and U.S. rice growers.”38

Despite the lengthy transition period toward freer trade under the CAFTA-DR,concerns remain over the potentially harmful effects to Central America, particularlyto the small commercial and subsistence farmers, of further opening its markets toU.S. agriculture.39 Three recent studies, however, agree that overall, increasedagricultural trade can also be one source of Central American rural development. Inaddition to increasing Central American agricultural exports, the majority ofhouseholds are net consumers of agricultural goods, and so stand to gain from lowerprices, the equivalent to an increase in family income. Because subsistence farmers’produce generally does not reach the market, they are unlikely to be affected greatlyby changes in market prices.40

Still, for the minority of rural net producers of agricultural goods, economistsalso agree that adjustment policies are essential, beginning with targeted incomeassistance. For rural areas to benefit fully from the CAFTA-DR, there is also acritical need for increased investment in transportation and communications

38 Ibid., pp. 43-47.

39Oxfam International. A Raw DealforRice Under CAFTA-DR. Briefing Paper #68. 2004.40 Todd, Jessica, Paul Winters, and Diego Arias. CAFTA and the Rural Economies ofCentral America: A Conceptual Franeworkfor Policy and Program Recommendation.Inter-American Development Bank. Washington, D.C. December 2004. pp. 43-50, Mason,Andrew D. Ensuring that the Poor Benefitfrom CAFTA: Policy Approaches to Managingthe Economic Transition. Draft of Chapter 5 in forthcoming book. The World Bank.Washington, D.C. March 25, 2005. pp. 25-26, 35, and Arce, Carlos and Carlos FelipeJaramillo. El CAFTA y la Agriclutura Centroamericana. Paper presented at the WorldBank Regional Conference on International Trade and Rural Economic Development,Guatemala. February 21-22, 2005. p. 17.

CRS-22

infrastructure, education, and more fully developed financial services. This will

improve agricultural productivity, help transition workers toward alternative crops

or non-farm employment, and integrate the rural economy more fully with the

national and international economy. Without concerted effort in adjustment

assistance, the poorest segments of rural Central America may remain vulnerable to

the negative effects of freer trade.4

Investment

In 2003, the United States’ stock of foreign direct investment (FD1) in the

CAFTA-DR countries was $4.3 billion, which represents only 1.4% of U.S. FDI in

Latin America and the Caribbean. Some 43% of the FDI in CAFTA-DR countries

went to Costa Rica, followed by the Dominican Republic with 20%. The United

States has advocated clear and enforceable rules for foreign investment in all trade

agreements, which is largely accomplished by “standard” language requiring national

and most-favored-nation (nondiscriminatory) treatment. The CAFTA-DR clarifies

rules on expropriation and compensation, investor-state dispute settlement, and the

expeditious free flow ofpayments and transfers related to investments, with certain

exceptions in cases subject to legal proceedings (e.g., bankruptcy, insolvency,

criminal activity). Transparent and impartial dispute settlement procedures provide

recourse to investors.

Two investment issues stood out. First, an investor-state provision, common in

U.S. bilateral investment treaties (BITs) and used in earlier FTAs, was included. It

allows investors alleging a breach in investment obligations to seek binding

arbitration against the state through the dispute settlement mechanism defined in the

Investment Chapter. U.S. investors have long supported the inclusion of investor-

state rules to ensure that they have recourse in countries that do not adequately

protect the rights of foreign investors. Since bilateral investment treaties are usually

made with developing countries that have little foreign investment in the United

States, such a provision was not thought to be applied to the United States.

Circumstances changed, however, under NAFTA when Canada used investor-state

provisions to raise “indirect expropriation” claims against U.S. state environmental

regulations.42

Although none of the claims filed against the United States has prevailed,

Congress instructed in TPA legislation that future trade agreements ensure “that

foreign investors in the United States are not accorded greater substantive rights with

respect to investment protections than United States investors.” In response, Annex

10-C ofthe CAFTA-DR states that “except in rare circumstances, nondiscriminatory

regulatory actions by a Party that are designed and applied to protect legitimate

welfare objectives, such as public health, safety, and the environment, do not

constitute indirect expropriations.” This provision and one that allows for early

‘ ibid.42 Indirect expropriation refers to regulatory and other actions that can adversely affect a

business or property owner in a way that is “tantamount to expropriation.” This issue and

many cases are discussed in CRS Report RL3 1638, Foreign Investor Protection Under

NAFTA Chapter 11, by Robert Meltz.

CRS-23

elimination of“frivolous” suits were intended to address congressional concerns, butthere is uncertainty about how well the changes will operate.

Second, the CAFTA-DR countries requested greater flexibility in the treatmentof certain sovereign debt. Annex 10-A allows sovereign debt owed to the UnitedStates that has been suspended and rescheduled not to be held subject to the disputesettlement provisions in investment chapter, with the exception that it be givennational and MFN treatment. Annex 10-E extends from six months to one year theamount of time required before a U.S. investor may seek arbitration related tosovereign debt with a maturity of less than one year. Both provisions are intended,in the event of a financial crisis, to keep the CAFTA-DR from interfering in anysovereign debt restructuring process, and are viewed by the U.S. Treasury as anaccommodation to Central American interests.

Services

The United States is the largest services exporter in the world and services tradepresented a number of hurdles given that the Central American countries haveadopted few commitments of the WTO ‘s General Agreement on Trade in Services(GATS). There were also many industry-specific barriers that existed, such as:barriers to foreign insurance companies in Guatemala; “heavy” regulation licensingof foreign professionals in Honduras; local partner requirements in some financialservices in Nicaragua; and numerous services monopolies in Costa Rica (insuranceand telecommunications).43 The CAFTA-DR provides broader market access andgreater regulatory transparency for most industries including telecommunications,insurance, financial services, distribution services, computer and business technologyservices, tourism, and others. Banks and insurance firms have full rights to establishsubsidiaries, joint ventures, and branches. Regulation of service industries isrequired to be transparent and applied on an equal basis and e-commerce rules areclearly defined, a critical component of delivering services.’

The USITC suggests that the CAFTA-DR will have little effect on U.S. servicesimports because the market is already open. It does anticipate opportunities for U.S.firms to expand into Central America. In particular, Costa Rica agreed to theeventual opening ofits state-run telecommunications and insurance industries, wherethere has been strong political resistence to privatization and deregulation.45 Unlikethe other countries, doing so will constitute a major structural adjustment for theCosta Rican economy, will have implications for Costa Rican social policy, and willrequire amending domestic laws, all ofwhich, the Costa Ricans argued, was difficultfor their legislature to support if they did not receive concrete tradeoffs in other areas,such as agriculture and textiles. Negotiators resolved these issues in two week-longdiscussions held in January2004 and their detailed conunitments are presented in therelevant chapters ofthe CAFTA-DR. Because ofthis continued sensitivity, however,

USTR. 2004 National Trade Estimate Report on Foreign Trade Barriers. Washington,D.C. 2004.

44USTR, CAFTA Summary, p. 2-3.‘ Salazar-Xirinachs and Granados, op. cit., p. 260.

CRS-24

a vote on ratifying the CAFTA-DR is highly controversial in the Costa Rican

Congress.

Government Procurement

None of the CAFTA-DR countries is a signatory to the WTO Agreement on

Government Procurement and complaints against purchasing processes vary from

dissatisfaction with opaque and cumbersome procedures in Costa Rica to outright

corruption in Guatemala. El Salvador, Nicaragua, and Honduras passed new

government procurement laws in 2000/01, and in general, there have been

improvements in all countries in dealing with project bidding, although transparency

issues remain.46 Some analysts believe this is due in part to a lack of incentives given

that many of these countries will not be able to compete in the U.S. government

procurement market.47

The CAFTA-DR grants non-discriminatory rights to bid on contracts from

Central American ministries, agencies, and departments, with the exception of“low

value contracts” and other exceptions. It also calls for procurement procedures to be

transparent and fair, including clear advance notices of purchases and effective

review. Specific schedules detailing exceptions and limitations were written by each

country, covering such diverse issues as the sale of firearms to supplying school

lunch programs. In addition, each country provided a list ofsubnational governments

(e.g., states and municipalities) that agree to adhere to the government procurement

provisions. The CAFTA-DR also makes clear that bribery is a criminal offense

under the laws of all countries. In general, the provisions are supported by U.S.

businesses interested in doing or expanding opportunities in the region.48

InteiJectual Property Rights

All Central American countries are revising, or have revised, their intellectual

property rights (IPR) laws and are closing in on complying with the WTO Agreement

on Trade-Related Aspects of Intellectual Property Rights (TRIPS). That said, all

countries are subject to criticism for falling short of either clarifying or enforcing

penalties for noncompliance and in some cases have simply not adopted reforms that

many U.S. industries (e.g., sound and video recordings, pharmaceuticals, book

publishing, computer software) consider necessary to protect their intellectual