Page 1

S.I. 144 of 2019

1

Statutory Instrument 144 of 2019.

[CAP. 22:11

Public Finance Management (Treasury Instructions), 2019

ITisherebynotifiedthattheMinisterofFinanceandEconomicDevelopment,hasintermsofsection78of the Public Finance Management Act [Chapter 22:19],approvedthefollowingTreasuryinstructions:—

Title

1. TheseinstructionsmaybecitedasthePublic Finance Management (Treasury Instructions), 2019.

2. These instructions shallcomeintoeffectonthedateofpublicationintheGovernmentGazette,andshallhenceforthreplaceandsupersedeallpreviousinstructions.

First Schedule

TREASURY INSTRUCTIONS

ARRANGEMENTOFSECTIONS

PART IPreliminary

Section 1. Title. 2.Interpretation.

PART IIadministration and General

3. Authority. 4.PurposeofissuingTreasury Instructions.5.ApplicationofTreasury Instructions. 6. Access to Treasury Instructions.7.ReviewofTreasury Instructions. 8.RelationshipbetweenTreasury Instructions,TreasuryCircularsandTreasuryCircularsMinutes.9.SuspensionofTreasury Instructionsprovisions. 10. Basis of accounting.11.Accountingpoliciesandconventions.12.ChartofAccounts.13.Accountingpackage.14.FinancialYear.15.FunctionalandReportingCurrency.

PART IIIPrinciPles oF Public Finance manaGement

16.PrinciplesofPublicFinanceManagement.17.ParliamentaryoversightofStaterevenuesandexpenditure.18.ConsolidatedRevenueFund.19.ChargesuponConsolidatedRevenueFund.20.AppropriationsfromConsolidatedRevenueFund. 21. Limits of Stateborrowings,publicdebtandState guarantees.22.SafeguardingofPublicFundsandProperty.23.Principlesofgenderbalance,equityandnon-discrimination.

DISTRIBUTED BY VERITAS e-mail: [email protected] ; website: www.veritaszim.net

Veritas makes every effort to ensure the provision of reliable information, but cannot take legal responsibility for information supplied.

Page 2

Public Finance Management (Treasury Instructions), 2019

2

PART IVadministration and institutional arranGements

Section 24. Treasury. 25. Secretary for Finance.26.Accountant-General.27.PrincipalDirectorresponsiblefordebtmanagement.28.Accountingofficers.29.PrincipalDirector/DirectorofFinance.30.HeadresponsiblefortheProcurementManagementUnit.

PART VbudGetinG and BudGetaryControl

31.Budgetpreparation.32.Budgetsubmission.33.Budgetapproval.34.Budgetauthorisation.35.Budgetimplementation.36.Budgetmonitoring.37.Virementing.38.Additionalandsupplementaryestimates.39.SpecialWarrants on Budgets.40.BudgetReporting.41.Condonationofunauthorisedexcessexpenditure.

PART VIrevenue manaGement

42.Receiversandcollectorsofrevenue.43.Receiptsandlicences.44.Manualreceiptbooks.45.Stampsandfacevalueinstructions.

PART VIIreceiPt and recordinG, custody and disPosal oF Public money

46.Receiptandrecordingandpublicmoneys.47.Custodyofpublicmoneys.48.Disposalofpublicmoneys.49.Recovery.

PART VIIIrecovery or Write-oFF oF Public moneys

50.Abandonmentofclaimsandwrite-offofpublicresources. 51. Treasury surcharges.52.Temporarydeposits.

PART IXexPenditure manaGement

53.Expenditurecontrolandclassification.54.Classificationofexpenditure.

Page 3

S.I. 144 of 2019

3

PART XexPenditure on emPloyment costs

Section

55.Establishments,appointmentandrecords.56.Salariesandwagescalculations.57.Deductions.58.Paymentofsalariesandwagesandstatutoryreturns.59.Expendituredocumentationandvalidation.60.Cashpaymentsandacquittances.

PART XIPaymaster General’s account: electronic Funds transFers, cheques, and oFFicial bankinG accounts

61.PaymasterGeneral’sAccount.62.Processingofpayments.63.Officialbankingaccounts.64.Advances.65.Travellingandsubsistenceallowances.66.Disallowancesanddepartmentalsurcharges.

PART XIIProcurement oF Goods, services and Works

67.Procurementpolicy.68.Evaluationcommittee.69.Typesoftender.70.InternationalTender.

PART XIIIProcurement Process For Goods, non-consultancy services and Works

71.Internalpurchaserequestforgoods,non-consultancyservicesandworks.72.Procurementmethodsforgoods,non-consultancyservicesandworks.73.Competitivebidding.

PART XIVuse oF Procurement methods other than comPetitive biddinG

74.Restrictedbiddingmethod.

75.Directprocurementmethod.

76.Requestforquotationmethod.

77.Tenderinvitation.

78.Requestforquotationsforgoods,on-consultancyservicesandworks.

79.Receiptandopeningofbids.

80.Selectionofvendorandnoticeofawardoftender.

81.Signingofcontracts.

82.Issueofpurchaseorders.

83.Purchasesexemptedfromtenderprocedures.

Page 4

Public Finance Management (Treasury Instructions), 2019

4

PART XVProcurement Process For consultancy services

Section

84.Requestforproposal.85.Methodsofsolicitingevaluatingandselectingconsultantbids.86.Evaluationofconsultancyproposalsandtenderaward.87.Qualityandcostbasedselection.88.Selectionunderfixedbudget.89.LeastCostSelection.90.Qualitybasedselectionmethod.91.Selectionamongstcommunityserviceorganisations.92.Single-sourceselection.93.Selectionofindividualconsultants.94.Confidentialityinprocurement.95.Receiptofgoods,services,worksandconsultancyservices.96.Managementofprocurementcontracts.97.Paymentrelatingtocontracts.

PART XVIasset ManaGement

98. Policy.99.AcquisitionofGovernmentassets.100.Recordingofassets.101.Useofassets.102.Controlofassets.103.Governmentvehicles.104.Fuelcoupons.105.Assetverification.106.Disposalofunserviceable,obsoleteorsurplusassets.107.Inventory.108.Livestock.109.Deficienciesin,damagetoanddestructionofGovernmentproperty. 110. Securities.

PART XVIIGiFts and donations

111.ResponsibilityformanagementPublicDebt. 112. Policy.113.Rejectinganofferofagiftordonation.114.Accountingforgiftsanddonations.115.Reportingandauditongiftsanddonations.

PART XVIIIFund accountinG

116. Policy.117.Submissionofannualbudgets.118.Managementcommittees. 119. Accounting.120.Financialreporting.121.Auditoffunds.

Page 5

S.I. 144 of 2019

5

PART XIXPublic debt manaGement

Section122.PublicDebtManagement.123.ResponsibilityformanagingPublicDebt.124.Borrowingpowers,limitsandmonitoring.125.Publicdebtandbudgeting.126.Purposeofborrowing.127.Raisingloans.128.Governmentguarantees.129.Publishingofloansandguarantees.130.Accountingforproceedsinconnectionwithloansandguarantees.131.Paymentsinconnectionwithloansandguarantees.132.AdministrationofPublicDebt.133.ReportingonPublicDebtactivities.134.Establishmentofsinkingfunds.

PART XXinternational develoPment assistance

135. Policy.136.Receivingdevelopmentassistance.137.Accountingfordirectpaymenttothesupplierorcontractor.138.Goodsandservicesreceivedinkindundergrantagreement.139.ResourcesprovidedthroughTreasury.

PART XXIGeneral

140.ClaimsbyandclaimsagainsttheGovernment. 141. Pensions.

PART XXIIliabilities

142.Commitments.143.Employeeentitlements.144.Contingentliabilities.

PART XXIII

transactions throuGh diPlomatic and consular missions

145. Policy. 146. Public Financial Management.147.Policy.148.SystemSecurity.149.SystemAdministration.150.Disasterrecoveryandback-upplan.151.DocumentationforthePFMS.152.Vendordatabasecreationandmaintenance.

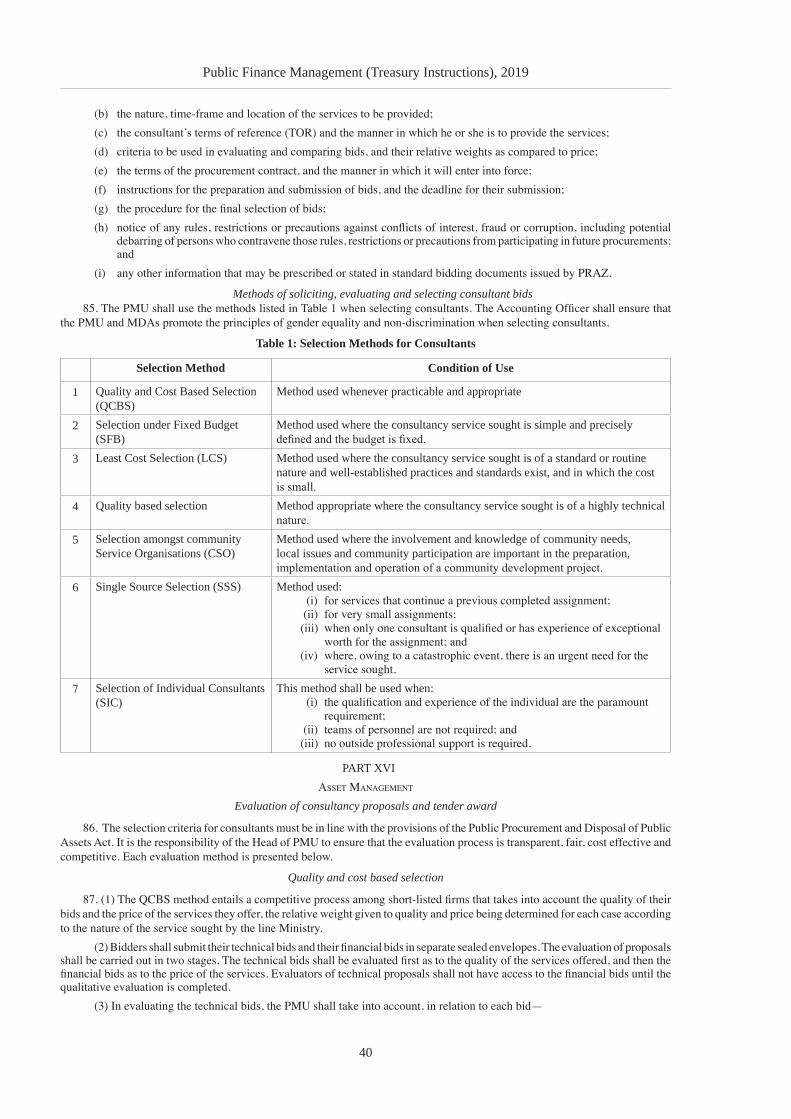

Page 6

Public Finance Management (Treasury Instructions), 2019

6

PART XXIV

Financial rePortinG

153.BasisofPreparationandPresentationofFinancialStatements.154.ContentsofFinancialStatements.155.Otherreports.156.AuditofFinancialStatements.

PART XXVinternal control

157.Policy.158.Officersoremployeesresponsibleforthereceipt,recordinganddisposalofpublicmoneys.159.Handingoverandtakingoverofduties.160.Safes,strong-rooms,strongboxesandcash-boxes.161.Internalaudit.162.Riskassessment.163.Auditcommittees.

aPPendix:GlossaryofAcronymsusedinthehandbook.

Interpretation

2.(1)IntheseInstructions— “Accountant-General”meansthepersonappointedassuchintermsofsection9ofthePublicFinanceManagementAct

[Chapter 22:19]; “accountingofficer”meansapersonwhoisprescribedtobeanAccountingOfficerintermsofsection10oftheAct,and

chargedwiththedutyofaccountingforanyserviceinwhichmoneyshavebeenappropriatedbyParliament; “accountingpolicies”arethespecificprinciples,bases,conventions,rulesandpracticesadoptedbyanentityinpreparing

andpresentingfinancialstatements; “accrualbasis”meansabasisofaccountingunderwhichtransactionsandothereventsarerecognisedwhentheyoccur

(andnotonlywhencashoritsequivalentisreceivedorpaid); “Act”meansthePublicFinanceManagementAct[Chapter 22:19]; “Auditor-General,”meansthepersonappointedassuchintermsofsection310oftheConstitutionofZimbabwe; “bidder”meansanactualorpotentialpartytoaprocurementcontractwithaprocuringentity; “cash”comprisescashonhand,demanddepositsandcashequivalents; “cashbasis’meansabasisofaccountingthatrecognisestransactionsandothereventsonlywhencashisreceivedorpaid; “chart of accounts”means a structured list of accounts used to classify and record budget revenue and expenditure

transactionsaswellasgovernmentassetsandliabilitiesonastandardbudgetclassificationssystem; “ConsolidatedRevenueFund”meanstheConsolidatedRevenueFundreferredtoinsection302oftheConstitutionof

Zimbabwe; “constructionwork”meansallworkassociatedwiththeconstruction,reconstruction,demolition,repairorrenovationof

anybuildingorinfrastructure; “consultancyservices”meanserviceswhichareofanintellectualandadvisorynature; “contingentliabilities”meansthoseobligationsthatmayormaynotbecomedue,dependingonwhetheraparticularevent

occurs; “debtcharges”includesinterest,sinkingfundcharges,therepaymentoramortisationofdebtandallexpenditurerelatedto

theraisingofloansonthesecurityoftheConsolidatedRevenueFundandtheserviceandredemptionofdebtcreatedby those loans;

“DirectorofFinance”meansapersonresponsibleforthefinancialaffairsofaMinistrywhoisdirectlyaccountabletotheAccountingOfficerofthatMinistry;

“facevalueinstruments”meansbonds,stocks,treasurybillsandanyothergovernmentfinancialinstruments. “financialyear”inrelationtotheStateorthefinancesoftheGovernmentofZimbabwemeansthetwelve-monthperiod

endingonthe31stDecember; “financialstatements”: 1. Inrelationtocashbasisofaccountingmeans— (a) astatementofcashreceiptsandpayments; (b) accountingpoliciesandexplanatorynotes; (c) whentheentitymakespubliclyavailableitsapprovedbudget,acomparisonofbudgetandactualamounts

Page 7

S.I. 144 of 2019

7

eitherasaseparateadditionalfinancialstatementorasabudgetcolumninthestatementofcashreceiptsandpayments;and

(d) otherreportsthattheAccountant-Generalmayrequire. 2. Inrelationtoaccrualbasisofaccountingmeans— (a) astatementoffinancialposition; (b) astatementoffinancialperformance; (c) astatementofchangesinnetassets/equity; (d) astatementofcash-flow; (e) whentheentitymakespubliclyavailableitsapprovedbudget,acomparisonofbudgetandactualamounts

eitherasaseparateadditionalfinancialstatementorasabudgetcolumninthefinancialstatement; (f) notes,comprisingasummaryofsignificantaccountingpoliciesandotherexplanatorynotes;and (g) otherreportsthattheAccountant-Generalmayrequire. “frameworkagreement”meansanagreementbetweenoneormoreprocuringentitiesandoneormorecontractors,bidders,

serviceprovidersorconsultantsthepurposeofwhichistoestablishthetermsgoverningordersforthesupplyofgoodsandrelatedservicesorrepairandmaintenanceworkstobeplacedduringagivenperiod,inparticularwithregardtoprice,and,whereappropriate,thequantityorquantitiesenvisaged;

“fruitless andwasteful expenditure”means expenditurewhichwasmade in vain andwould have been avoided hadreasonablecarebeentaken;

“loan”meansanyborrowingwithorwithoutinterestfromanysourceoranyissuanceofanationalgovernmentsecurity; “Minister”meanstheMinisterresponsibleforFinanceoranyotherMinistertowhomthePresidentmay,fromtimeto

time,assigntheadministrationofthePublicFinanceManagementAct[Chapter 22:19]; “Non-consultancyservices”meanservicesconsistingofphysicaljobperformance,usuallybycontractedlabourers; “procurement”means the acquisition by anymeans of goods, constructionwork or services (consultancy and non–

consultancy); “publicdebt”meansdomesticandexternal:— (a) Governmentdebt,lendingandguarantees; (b) localauthoritydebt,lendingandguarantees; (c) publicentitydebt,lendingandguarantees; “publicfunds”includesanymoneyownedorheldbytheStateoranyinstitutionoragencyofthegovernment,including

provincialandlocaltiersofgovernment,statutorybodiesandgovernment-controlledentities; “publicofficeroranofficer”meansanypersonasdefinedinthePublicServiceRegulations,2000[StatutoryInstrument

1of2000]asamended; “publicproperty”meansanypropertyownedorheldbytheStateoranyinstitutionoragencyofthegovernment,including

provincialandlocaltiersofgovernment,statutorybodiesandgovernment-controlledentities; “receipt”isanofficialdocumentissuedasanacknowledgementforcollectionofpublicmoneys; “receiverofRevenue”meansanypersonwhoisprescribedtobeaReceiverofRevenueintermsofsection10oftheAct; “revenues”meansalltaxes,feesandotherincomeoftheStatefromwhateversourcearising(notbeingmoneyswhich

arerequiredbylawtobepaidintoaseparatefund),includingtheproceedsofallloansraisedbytheStatewhich,intermsofsection302oftheConstitution,formpartoftheConsolidatedRevenueFund;

“SecretarytotheTreasury”istheheadoftheMinistryresponsibleforFinanceandthemainnationaleconomicadvisor. “Stateloan”meansasumofmoneyborrowedintermsofthePublicDebtManagementAct[Chapter 22:21]; “statutoryfund”meansanyfundestablishedbyorunderanyenactmentnotincluding—

afundestablishedundersection18ofthePublicFinanceManagementAct[Chapter 22:19]; orafundestablishedbyorforthepurposesofapublicentitywhichdoesnotcontainpublicmoney.

“tax”includesaduty,rate,levyorfeechargedonaproduct,incomeoractivity. “thresholds”meansthefinanciallimitsaboveorbelowwhichspecifiedprocurementmethodsshouldbeapplied. “treasury”meanstheDepartment(s)intheMinistryresponsibleforFinancethatistheleadadvisoronnationaleconomic,

financialmanagementandregulatorypolicy. “virement”meanstheapplication,asauthorisedbyanAppropriationAct,ofsavingsonasubheadofaVotetomeetexcess

expenditureonanothersubheadorexpenditureonanewsubheadofthesameVote; “vote”meansaheadoranappropriationofEstimates. “votedfunds”meansmoneyauthorisedbyanappropriationActforwithdrawalfromtheConsolidatedRevenueFund. (2)TheFirstSchedulecontainsaglossaryofacronymsusedinthehandbook.

PART IIadministration and General

Authority 3.(1)Theseinstructionsareissuedintermsofsection78readinconjunctionwithsection6ofthePublicFinanceManagementAct [Chapter 22:19].

Page 8

Public Finance Management (Treasury Instructions), 2019

8

(2)AnyinstructionsorcircularsthatareinconsistentorinconflictwiththeseinstructionsshallbereferredtoTreasuryforfurtherguidanceand/orclarification.

Purpose of issuing Treasury Instructions

4.Theseinstructionsareissuedpursuanttotheprovisionsofsections6and78oftheAct,toprovideguidanceonpublicfinancialmanagementmattersrelatingto: (a) thecollection,receipt,custody,control,issueorexpenditureofpublicmoney; (b) theacquisition,receipt,custody,control,issue,sale,delivery,transferordisposalofanyStateproperty; (c) expenditureonanyserviceinvolvingachargeontheConsolidatedRevenueFund; (d) theoperationofanystatutoryfund;and (e) theacceptance,onbehalfoftheState,ofanygift,donation,bequestorothergrantofmoneysorotherpropertywhich

ismadesubjecttoaconditionorislikelytoinvolveachargeontheConsolidatedRevenueFund. Application of Treasury Instructions

5.(1)TheseinstructionsshallapplytoGovernmentMinistries,agenciesandemployeesofanydepartmentoragencyasdefinedinthePFMActandPublicServiceRegulations. (2)ItistheresponsibilityofeveryAccountingOfficertoensurethattheseTreasuryInstructionsarecompliedwithatalltimesandatalllevels.

Access to Treasury Instructions

6.(1)ThecurrentversionoftheTreasuryInstructionsisobtainablefromMinistryofFinance’swebsiteandtheofficialGovernmentPrinter. (2)AccountingOfficersshallensurethatcopiesofTreasuryInstructionsareavailedtotheirstaffforreferenceandguidance.

Review of Treasury Instructions

7.(1)Theseinstructionsshallbereviewedandupdatedeveryfiveyears,andeveryupdatedversionofTreasuryInstructionsissuedshallsupersedeandreplaceallpreviousversions. (2)OnceTreasuryInstructionsareupdated,itshallbetheresponsibilityofeveryAccountingOfficertoensurethatthelatestversionisapplied.

Relationship between Treasury Instructions, Treasury Circulars and Treasury Circular Minutes 8.(1)ThemainpurposeofTreasuryCircularsandCircularMinutesistoprovideguidanceandinformation,andtorequestfinancialinformation.TreasuryCircularsandCircularMinutesmaycovermattersthatareoutsidethescopeofTreasuryInstructions,suchasthebudgettimetable. (2)TreasuryCirculars orCircularMinutesmay covermatters that are to take effect immediately (butmay later beincorporatedwithinTreasuryInstructionsaspartoftheupdate). (3)TreasuryCircularsorCircularMinutesshouldbecompliedwithinthesamewayasTreasuryInstructions.

Suspension of Treasury Instructions Provisions

9.OnlytheMinistermay,inwriting,temporarilysuspendanyoftheprovisionscontainedintheseTreasuryInstructions.

Basis of accounting

10.(1)ThebasisofAccountingthattheGovernmentofZimbabweusesshallbedeterminedbytheBoardresponsibleforsettingAccountingStandardsinZimbabwe. (2)TheGovernmentofZimbabwecurrentlyappliesthecashbasisforvotedfundsandaccrualbasisforstatutoryandotherfunds.

Accounting Policies and Conventions

11.(1)Revenueunderthecashbasisofaccountingshallberecognisedandaccountedforasincomeintheperiodinwhichitisreceived. (2)Revenueundertheaccrualbasisofaccountingisrecognisedasitisearned(andnotonlywhencashoritsequivalentisreceived)andthetransactionsareaccountedforandreportedintheperiodtowhichtheyrelate. (3)Expensesunderthecashbasisofaccountingarerecognisedandaccountedforwhentheactualcashisdisbursed. (4)Expensesundertheaccrualbasisofaccountingarerecognisedastheybecomedue(andnotonlywhencashoritsequivalentisdisbursed)andthetransactionsareaccountedforandreportedintheperiodtowhichtheyrelate. (5)Underthecashbasisofaccounting,assetsareexpensed(fullydepreciated)intheyearofpurchase. (6)Undertheaccrualbasisofaccounting,assetsaredepreciatedinaccordancewithpolicypronouncementsfromtheBoardresponsibleforsettingAccountingStandardsinZimbabweandTreasurypolicydirections.

Page 9

S.I. 144 of 2019

9

Chart of accounts

12.TheGovernmentofZimbabwehasadoptedtheInternationalMonetaryFundGovernmentFinanceStatistics(GFS)ChartofAccounts.AllGovernmentMinistries,Agencies,statutoryandotherfundsshalladoptthisclassificationsystem.

Accounting package

13.(1)TheGovernmentofZimbabweusestheSystemsApplicationsProducts(SAP)integratedpackage(VersionEEC6EHP7)hereinafterreferredtoasthePublicFinancialManagementSystem(PFMS). (2)StatutoryandotherfundsshallutilisethesameaccountingpackageunlessauthorisedbyTreasurytorunindependentsystems. (3)AllindependentsystemsshallbecompatiblewiththeSAPsystem.

Financial Year

14.ThefinancialyearoftheGovernmentofZimbabweshallbefrom1stJanuaryto31stDecemberofeachyear.

Functional and reporting currency

15.AlthoughZimbabweacceptsanumberofcurrencies,thefunctionalandreportingcurrencyistheUnitedStatesdollar(USD).

PART III

PrinciPles oF Public manaGement

Principles of Public Finance Management

16.TheprinciplesthatmustguidePublicFinanceManagementareprovidedforundersection298oftheConstitutionofZimbabwe.Theseincludethefollowing— (a) transparencyandaccountabilityinfinancialmatters.Governmentministries,departmentsandagenciesmustmake

clearwhathasbeendoneandwhyithasbeendone; (b) publicfinancesystemmustbedirectedtowardsnationaldevelopment,andinparticular— (i) theburdenoftaxationmustbesharedfairly; (ii) revenueraisednationallymustbesharedequitablybetweenthecentralgovernmentandprovincialandlocaltiers

ofgovernment;and (iii) expendituremustbedirectedtowardsthedevelopmentofZimbabwe,andspecialprovisionmustbemadefor

marginalisedgroupsandareas; (c) theburdensandbenefitsoftheuseofresourcesmustbesharedequitablybetweenpresentandfuturegenerations; (d) publicfundsmustbeexpendedtransparently,prudently,economicallyandeffectively; (e) financialmanagementmustberesponsibleandfiscalreportingmustbeclear; (e) publicborrowingandalltransactionsinvolvingthenationaldebtmustbecarriedouttransparentlyandinthebest

interestsofZimbabwe;and (f) notaxesmaybeleviedexceptunderthespecificauthorityoftheConstitutionofZimbabweoranActofParliament.

Parliamentary oversight of State revenues and expenditure

17.Section299oftheConstitutionofZimbabwemandatesParliamenttomonitorandoverseerevenueinflowsandexpenditurebytheGovernmentinordertoensurethat— (a) allrevenueisaccountedfor; (b) allexpenditurehasbeenproperlyincurred;and (c) anylimitsandconditionsonappropriationshavebeenobserved.

Consolidated Revenue Fund

18.TheConstitutionprovidesforaConsolidatedRevenueFundintowhichmustbepaidallfees,taxesandborrowingsandallotherrevenuesoftheGovernment,whatevertheirsource,unlessanActofParliament— (a) requiresorpermitsthemtobepaidintosomeotherfundestablishedforaspecificpurpose;or (b) permitstheauthoritythatreceivedthemtoretainthem,orpartofthem,inordertomeettheauthority’sexpenses.

Charges upon Consolidated Revenue Fund

19.(1)Section304oftheConstitutionofZimbabweprovidesthatthecostsandexpensesincurredincollectingandmanagingtheConsolidatedRevenueFundformthefirstchargeontheFund. (2)AlldebtchargesforwhichtheStateisliablemustbechargedupontheConsolidatedRevenueFund.

Page 10

Public Finance Management (Treasury Instructions), 2019

10

Appropriations from Consolidated Revenue Fund

20.(1)Section305oftheConstitutionprovidesthateveryyeartheMinisterresponsibleforfinancepresent,totheNationalAssembly,astatementoftheestimatedrevenuesandexpendituresoftheGovernmentinthenextfinancialyear. (2)WhentheNationalAssemblyhasapprovedtheestimatesofexpenditureforafinancialyear,anAppropriationActispromulgatedandit— (a) providesformoneytobeissuedfromtheConsolidatedRevenueFundtomeettheapprovedexpenditure;and (b) appropriatesthemoneytothepurposesspecifiedintheestimates,underseparateVotesforthedifferentheadsof

expenditurethathavebeenapproved.

Limits of State borrowings, public debt and State guarantees 21.Section300oftheConstitutionrequiresthatlimitsbesetonborrowingsbytheState;thepublicdebt;anddebtsandobligationswhosepaymentorrepaymentisguaranteedbytheState. (2)ThesetlimitsshallnotbeexceededwithouttheauthorityoftheNationalAssemblyandinaccordancewiththeprovisionsofthePublicDebtManagementAct[Chapter 22:21].

Safeguarding of public funds and property

22.(1)Section308(2)oftheConstitutionprovidesthat,itisthedutyofeverypersonwhoisresponsiblefortheexpenditureofpublicfundstosafeguardthefundsandensurethattheyarespentonlyonlegallyauthorisedpurposesandinlegallyauthorisedamounts. (2)Section308(3)oftheConstitutionprovidesthat,itisthedutyofeverypersonwhohascustodyorcontrolofpublicpropertytosafeguardthepropertyandensurethatitisnotlost,destroyed,damaged,misappliedormisused.

Principles of gender balance, equality and non-discrimination 23.(1)TheConstitutionofZimbabweisinformedbytheprinciplesofgenderbalanceandgenderequality.Itadvocates,amongotherthingsthatGovernmentinstitutionsensureequalrepresentationsforbothmenandwomeninallspheres. (2)Stateagenciesshalltakeactions,includinglegislativemeasurestorectifygenderdiscriminationandimbalancesresultingfrompastpracticesandpolicies. (3)Theseinstructionsshallbegendersensitive,andthebudgetaryprocessandoutcomesshallreflecttheprinciplesofgenderresponsivebudgeting.

PART IV administrative and institutional arranGements

Treasury 24.(1)Section6oftheActgivesTreasurytheresponsibilitytomanageandcontrolpublicresources.Treasuryisthereforeresponsiblefor— (a) managingtheConsolidatedRevenueFund; (b) determiningthemannerinwhichpublicresourcesshallbeaccountedfor;and (c) exercisinggeneraldirectionandcontroloverpublicresources. (2)Section4ofthePublicDebtManagementAct[Chapter 22:21]givesTreasurytheresponsibilityfordebtmanagementoperations. (3)ThepowersofTreasuryinrelationtopublicresourcesaresetforthinsection11oftheAct.

Secretary for Finance

25.ThedutiesandpowersoftheSecretaryforFinancewhoshallalsobethePaymaster-Generalaresetoutinsection8oftheAct.TheSecretaryshallensurethat— (a) thereisestablishedandoperatedaneffectivesystemforthecollectionofinformationtoensuretimelyandeffective

preparationoftheannualestimatesofexpenditureforconsiderationandapprovalbytheMinisterandsubmissiontoParliament;and

(b) suchestimates— (i) arepreparedinconjunctionwithanygeneralorspecificdirectionsoftheMinister;and (ii) reflect,ascanbestbeascertainedatthetime,goodvalueformoneyandtheeffectiveuseofpublicresources; and (c) asPaymaster-GeneralandsubjecttothedirectionsofTreasury,theSecretaryshallcontroltheissueofpublicmoney

toMinistriesandDepartmentsoftheGovernment,andperformsuchotherfunctionsastheMinistermayprescribe.

Accountant-General

26.(1)TheAccountant-Generalisappointedintermsofsection9oftheActandshallberesponsibletotheSecretaryforFinanceforthecompilationandmanagementofthepublicaccountsandthecustodyandsafetyofpublicresources.

Page 11

S.I. 144 of 2019

11

(2)TheAccountant-General’spowersarespecifiedinsection9(4)oftheAct. (3)TheresponsibilityoftheAccountant-GeneralincludesthedeterminationofappropriateinvestmentofmoneysintheConsolidatedRevenueFundinaccordancewithsection20oftheAct. (4)TheAccountant-Generalshallauthorisetheestablishmentofallbankingaccounts. (5)TheAccountant-GeneralisresponsibleforissuingexpenditurewarrantsauthorisingAccountingOfficerstospendfundsfromtheConsolidatedRevenueFundwithintheprescribedlimitsandsubjecttotheconditionscontainedtherein. (6) It is the responsibilityof theAccountant-General topreparemonthly,quarterlyandannual consolidatedfinancialstatementsandtosubmitsuchstatementstotherespectiveofficesasprovidedforbytheAct. (7)TheAccountant-GeneralshallberesponsibleforthepreparationandsubmissionofTreasuryMinutesexplainingtheactionthathasbeentakenonrecommendationsforimprovementsinpublicfinancialmanagementbytheSelectCommitteeonPublicAccountsandgivingreasonsforanyrecommendationsnothavingbeenimplemented. (8)TheActgivestheAccountant-GeneraltheresponsibilitytospecifyforeveryMinistry,reportingunitorstatutoryfund,thebasisoftheaccountingsystemtobeadoptedandtheclassificationsystemtobeused,andensurethatapropersystemofaccountsisestablishedineachofthem,andthatallmoneyreceivedandpaidbytheGovernmentisbroughtpromptlyandproperlyto account.

Principal Director responsible for debt management

27. (1)ThePrincipalDirector responsible forDebtManagement is appointed in termsof section6of thePublicDebtManagementActandshallberesponsibletotheSecretaryforFinanceforthecontrolandmanagementoftheoperationsofthePublicDebtManagementOffice(PDMO). (2)ThefunctionsofthePDMOarespecifiedinsection5(2)ofthePublicDebtManagementAct.Intermsoftheprovisionsofthesaidsection,thePDMOshallberesponsibleforthefollowingfunctions— (a) preparingandpublishingaMediumTermDebtManagementStrategyinaccordancewithsection8ofthePublicDebt

Management Act; (b) preparingandpublishinganannualborrowingplanwhichincludesaborrowinglimit,andparticipateinthepreparation

ofanissuancecalendarofGovernmentsecuritiesinlinewiththeannualborrowingplan; (c) advisingtheMinisteronallGovernmentborrowings,andparticipatinginallnegotiationswithcreditorsonGovernment

borrowingsandguaranteedloans; (d) undertakingannualdebtsustainabilityanalysis; (e) assessingtherisksinissuinganyguarantees,includingassessingthecapacityofthebeneficiaryofaguaranteeto

repaytheloan,andtopreparereportsonthemethodusedforeachassessmentandtheresultsthereofforapprovalbythe Minister;

(f) preparingannualreportsonoutstandingguarantees,andfacilitatingtherecoveryofanypaymentsincludinginterestandanyothercostsincurredbyGovernmentduetothehonouringofoutstandingguarantees;

(g) assessingthecreditriskinanylending,andpreparingreportsonthemethodusedforeachassessmentandtheresultsthereof for the attention of the Minister;

(h) preparingreportsonthedebtoflocalauthoritiesandpublicentities;aswellasassessing,monitoringandkeepingtrackofdebtlevelsofalllocalauthoritiesandpublicentities;

(i) storageofalloriginalloanagreementsanddebtadministrationrecordsinrelationtothepublicdebt; (j) compilation,verificationandreportingonallpublicdebtarrears,especiallyGovernmentpublicdebtarrears,and

designingastrategyforthesettlementofthese; (k) keeping timely, comprehensiveandaccurate recordsofoutstandingpublicdebt,guarantees andon-lending, in a

computeriseddatabaseandinparticular— (i) compilingdataonalldebtservicingobligationsoftheGovernment,localauthoritiesandpublicentities,and

prepareandpublishdebtstatisticalbulletinsinrelationtheretoregularly,eithergloballyoronaselectivebasisasrequired;and

(ii) validatingandreconcilingdebtdataconcerningcreditorsoftheGovernmentofZimbabwe; (l) preparingforecastsonGovernmentdebtservicinganddisbursementsaspartoftheyearlybudgetpreparations; (m) preparingbalanceofpaymentsprojections; (n) monitoringandevaluatingprojectsfundedorpartlyfundedbypublicdebttoensurethatborrowedfundsareusedfor

theirintendedpurposes; (o) preparinganannualreportonGovernmentdebtmanagementactivitiesincludingthedebtstockpositionandrelated

debtserviceprojections,newborrowing,guaranteesandlending; (p) operatingastheSecretariattotheExternalandDomesticDebtManagementCommitteeinaccordancewithsection

7(3)ofthePublicDebtManagementAct; (q) actingastheprincipaladviserinthedevelopmentofdomesticcapitalmarketsandissuanceofdomesticandexternal

debtsecuritiesonbehalfoftheGovernmentofZimbabwe;

Page 12

Public Finance Management (Treasury Instructions), 2019

12

(r) assessing,monitoringandreportingonanyotherimplicitandexplicitpublicsectorcontingentliabilitiesandadvisingon their management;

(s) maintainingandadministeringasecurecomputeriseddebtmanagementinformationsystem; (t) initiation,facilitationandmonitoringofdisbursementsonborrowingsandon-lending;and (u) analysingrequestsfromlocalauthoritiesandpublicentitiesforborrowings.

Accounting officers

28.(1)AccountingOfficersareprescribedintermsofsection10oftheAct.Thetitle“AccountingOfficer”denotestherelationshipinwhichsuchofficersstandtowardsParliamentandidentifiestheirresponsibilityforgeneralfinancialadministrationoftheVotesorfundsintheircharge.AccountingOfficersshallcontrolandbeaccountablefortheexpenditureofmoneyappliedtotheirVotebyanAppropriationActandforallrevenuesandotherpublicmoneyreceived,heldordisposedof,byoronaccountoftheirMinistry,reportingunit,publicentityorconstitutionalentityforwhichtheVoteprovides.AccountingAuthoritiesforreportingunits,publicentitiesorconstitutionalentitiesforwhichaVoteprovidesshallbeaccountabletotheAccountingOfficerforthemanagementofpublicresourcesundertheircontrol. (2)Theterm“AccountingOfficer”mustbedistinguishedfromtheterm“accountant”whichtermiscommonlyusedtodescribeofficersperformingdutiesofatechnicalnatureinconnectionwithbook-keepingandaccounting. (3)ThespecificresponsibilitiesofanAccountingOfficeraresetoutintheStatutoryInstrumentinforce. (4)TheAccountingOfficermustcommunicatedirectlywithTreasuryinregardtoallquestionsrelatingtotheirfinancialresponsibilitieswhichcannotberesolvedbyreferencetotheseInstructions. (5)TheAccountingOfficershallberesponsibleforallcorrespondencewhethersignedpersonallyorontheirbehalf. (6)AccountingOfficersshallnotdelegateresponsibilityfortheproperconductoffinancialbusinesstosubordinateofficerswhomaybeplacedinchargeofdepartmentalaccounts.ItisincumbentonAccountingOfficerstosatisfythemselves,bymeansofstatementsdulycertifiedbytheofficersentrustedwiththeoperationofanyaccount,astothecorrectnessandproprietyofthetransactionsonsuchaccounts.AccountingOfficershavetherightinwhatevermannertheychoosetosatisfythemselvesofanyactiontakenintheirnameswhichtheymaysubsequentlyhavetodefend. (7)WithintheframeworkoftheseInstructions,AccountingOfficersshallissuedetailedwritteninstructionsgoverningtheconductoffinancialbusinessandthecontrolofallpublicmoneysandthepropertyforwhichtheyareresponsible.Suchinstructionsshallincludedirectionsastotheoperationofinternalcheckandcontrolsystems. (8)AllinstructionsissuedintermsofInstructionNo.0332shallbeapprovedbyTreasuryandcopiesoftheapprovedAccountingOfficer’sInstructionsshallbetransmittedtotheAuditor-General. (9)AccountingOfficersshallensurethatinstructionsissuedinaccordancewithInstructionNo.0332,arereviewedatleasteveryfiveyearsforthepurposesofensuringthatanychangesofcircumstancesarecateredfor. (10)AccountingOfficersshallensurethattheprovisionsoftheseInstructionsarefollowedinrelationtoFundssetupintermsofsection18oftheAct(coveredinInstructionNos.1200-1299oftheseTreasuryInstructions)andwhichareadministeredbyofficersintheirofficialcapacitiesunlessspecificTreasuryauthorityforexemptionhasbeenobtained. (11)ItistheresponsibilityofAccountingOfficerstosubmittotherespectiveParliamentaryPortfolioCommittee,theunauditedannualfinancialstatementsoftheirrespectiveMinistrywithinninetydaysoftheendofthefinancialyearandintermsof Act.

Principal Director/Director of Finance

29.(1)ThePrincipalDirector/DirectorofFinance(hereinafterreferredtoasDirectorofFinance)providestheAccountingOfficerwithassistanceinthefinancialadministrationofVotesandFundsundertheircharge.TheirresponsibilityistoadviseAccountingOfficersonallfinancialmatters.Theymayalsoexamineandcommentonthefinancialaspectsofadministrativeactionandministerialpolicy. (2)EveryDirectorofFinanceshallhavefreeaccesstoallpapersrelativetotheirdutiesandmustreportdirectlytotheAccountingOfficer. (3)IntheabsenceofthepersonalcommentsoftheAccountingOfficer,TreasurywillexpecttheviewsoftheDirectorofFinancetoaccompanyanyfinancialproposalssubmittedtoTreasury. (4)TheDirectorofFinanceisanswerablefor— (a) theday-to-dayrunningoftheirrespectiveaccountsoffices; (b) thekeepingoffinancialrecordsandbooksofaccount; (c) thesafecustodyofthepublicmoneysentrustedtothem; (d) puttinginplacesystemsofinternalchecksandcontrolonfinancialadministration; (e) thepreparationandsubmissionofallfinancialstatements(monthly,quarterlyandannual),anyreturns,otherstatutory

reportsandtheaccountsofotherpublicmoneysthataretheresponsibilityoftheAccountingOfficer; (f) ensuringtheaccuracyoftheaccounts,anddrawingtheAccountingOfficer’sattentiontoallpointsofimportance

whichariseinconnectionwiththem; (g) ensuringthatthedeadlinesforpreparationandsubmissionofFinancialStatementstotheAccountingOfficerintheir

respectiveMinistryandtotheAccountant-Generalaremet;and

Page 13

S.I. 144 of 2019

13

(h) ensuringresponsestoAuditobservationsaretimely.

(5)TheDirectorofFinanceshallsubmittoTreasury,bythe20thworkingdayofthefollowingmonth,withacopytotheAuditor-General,theAccountingOfficer’sTreasuryCertificateinsuchformasdeterminedbyTreasuryfromtimetotime.ThecertificateshallbesignedonbehalfoftheAccountingOfficerbytheDirectorofFinance.

Head responsible for the Procurement Management Unit

30.ThePublicProcurementandDisposalofPublicAssetsAct[Chapter 22:23]providesfortheestablishmentofaProcurementManagementUnit(PMU).TheHeadofthePMUshallbetheAccountingOfficer.TheAccountingOfficershallbesupportedbyprocurementofficersandthePMUshallhavethefollowingresponsibilities— (a) puttinginplaceatransparentandcompetitivebiddingsystemthataffordsfairandequitabletreatmentofallbidders; (b) puttinginplaceasystemthatminimisesfruitlessandwastefulprocurement; (c) planningthePublicProcurementandDisposalofPublicAssetsActivitiesoftheMinistry,AgencyorDepartment; (d) recommendingtheappropriateprocurementmethod; (e) preparingsolicitationdocuments; (f) preparingbidnoticesandshortlists; (g) managingthebiddingprocess,includingpre-bidmeetings,clarifications,receiptandopeningofbids; (h) managingtheevaluationofbidsandanypost-qualificationornegotiationsrequired; (i) preparingevaluationreports,includingcontractawardrecommendations; (j) preparingcontractdocumentsandamendments; (k) managingcontractsoroverseeingcontractsmanagementbythedesignatedcontractsmanager; (l) preparingsuchprocurementreportsasrequiredbytheAccountingOfficer;and (m) promotingtheintegrityof,andfairnessandpublicconfidencein,theprocurementprocess.

PART VbudGetinG and BudGetary Control

Budget preparation

31.(1)Thissectionprovidesguidanceonbudgetpreparation,approval,execution,monitoringandreporting. TreasuryshallberesponsibleforprovidingguidanceandcommunicatingwithAccountingOfficersregardingthebudgetcalendarandtimetable.TreasuryshallissueaBudgetStrategyPaper(BSP),andaBudgetcallcircular(s). (2)AccountingOfficersshallensurethatalltheDepartmentsandentitiesundertheircontrolaremadeawareofthebudgetcalendarandtimetable.It istheresponsibilityofAccountingOfficerstoensurethattheirMinistriesmeetbudgetsubmissiondeadlines. (3)Thebudgetingprocessshallbeparticipatoryinnaturewithallstakeholdersinvolvedinpublicfinancemanagementgettinginvolvedinthebudgetformulationexercise. (4)TheDirectorofFinanceshallbeinchargeofcoordinating,providingguidanceonresourceavailabilityandconsolidatingtheirrespectivelineMinistry’sbudget.

Budget submission

32. (1) AccountingOfficersshallsubmittotheTreasury,bysuchdateandinsuchformastheTreasurymayprescribe,draftestimatesofrevenueandexpenditure,tobedefrayedduringtheensuingfinancialyearfrombudgetandfinancialaccountforeachVoteundertheircontrol.

(2)BidsforcapitalbudgetsshallbesubmittedbytheAccountingOfficertotheappropriateMinisterand,ifapproved,shallthenbereferredtotheTreasuryforconsiderationbytheappropriateDepartment.ThebidsforcapitalbudgetsshallincludealldepartmentsandstatutorybodiesforwhichMinistriesareresponsibleandshallbesubmittedbysuchdateandinsuchformastheTreasurymayrequire.

(3)NoproposalshallbesubmittedtotheTreasurywithoutfullinformationonitsfinancialaspectsandasaccurateanestimateaspossibleofthefundslikelytoberequired.

(4)NoproposalinvolvingadditionalestablishmentchargesmaybesubmittedtotheTreasuryforapprovalunlessithasbeenpreviouslyexaminedandauthorisedbythePublicServiceCommission.

Budget approval

33.(1)TheAccountingOfficerisresponsibleforscrutinisingandapprovingtherespectivelineministry’sbudget.Inexecutingthisrole,AccountingOfficersshallensurethattheirbudgetforecastsfullyaddresstheMinistry’smandate,goals,programmesandtheprioritiessetinthenationaleconomicblueprints,andanyotherpolicypronouncements.

Page 14

Public Finance Management (Treasury Instructions), 2019

14

(2)ItistheresponsibilityoftheAccountingOfficerstoensurethattheirMinistries’budgetsaregenderresponsive. (3)Treasuryhastheprerogativetoscrutinise,adjustandapprovelineMinistries’BudgetsaftertakingintoaccounttheMinistry’smandate,goals,programmesandprioritiesvis-à-vis national interest.

Budget authorisation

34.(1)TheresponsibilityforauthorisingbudgetsrestswiththeNationalAssemblywhichdoessothroughthepromulgationoftheAppropriationActandtheFinanceAct. (2)TheappropriationofmoneydoesnotautomaticallypermitlineMinistriestospend.Theauthoritytospendisconveyedthroughthefollowingwarrants— (a) Paymaster-General; (b) ConstitutionalandStatutoryprovisions;and (c) Accountant-General. (3)AllcapitalexpenditurereleasesshallbecoveredbyanAccountant-General’swarrant.

Budget implementation

35.(1)TreasuryhastheresponsibilityofinforminglineMinistriesoftheirauthorisedbudget.ThisinformationisconveyedthroughaPaymaster-General’sWarrantintermsofsection23(2)oftheAct.Quarterlywarrantsmaybeissuedshouldthecashforecasts so justify.

(2)TreasuryshallensurethattheauthorisedbudgetsforlineMinistriesareuploadedonthePFMS.FordecentralisedGovernmentUnitsthathavenoaccesstothePFMS,theAccountingOfficershallensurethattheauthorisedbudgetsaremanagedthroughacommitmentcontrolsystem.TheinformationmaintainedincommitmentcontrolrecordsshallbecapturedintothePFMSonaweeklybasis.

(3)ToenableTreasurytoadequatelyplanforfutureexpenditureandprioritisegovernmentrequests,AccountingOfficersshallpreparemonthlycashflowforecasts.Thesecashflowforecastsshalldisclosetheanticipatedincomefromallsourcesandtheforecastedexpenditure.

(4)TheDirectorofFinanceshallensurethattheirrespectivelineMinistry’scashplanningisdoneinaccordancewithTreasuryguidelinesandcashceilings(expendituretarget)givenfromtimetotime.

Budget monitoring

36.(1)TheAccountingOfficershallmonitortheperformanceofthebudgetregularlytoensuredeliveryofexpectedresultsandtoaddressanydeviationsfromtheirlineministry’stargets.

(2) Themonitoringofthebudgetshallbecarriedoutattransactionlevelwherebyeachbudgetlineischeckedforavailabilityoffundsbeforeauthorisingexpenditure.OfficersauthorisingexpenditureshoulddosoafterviewingthebudgetonthePFMSsystem.

(3)TheDirectorofFinanceshallundertakebudgetmonitoringthroughvarianceanalysiswheretheactualexpenditureperbudgetlineiscomparedtotheallocatedbudget.

(4)UndernocircumstancesshouldrequestsforservicesbemadeoutsidethePFMS.NorequestforservicemadeoutsidethesystemshallbehonouredbytheGovernment.AnyofficerwhomakessuchanordershallbeguiltyofanoffenceandliabletopenaltiessetoutintheAct.

(5)AccountingOfficersshallensurethatallproposedexpenditurefortheirMinistriesisinlinewiththebudgetandalltransactionsarecapturedonthePFMS.

(6)ForbudgetmonitoringtobeeffectivetheDirectorofFinanceshallensurethatallbooksofaccountsareuptodateandthemonthlyfinancialreportsthatcompareactualexpenditureagainstthebudgetarepreparedontimeasperTreasurydeadlines.

(7)TreasuryshallmonitortheperformanceofthenationalbudgetandtakeremedialactiononerrantlineMinistries.

(8)Treasurymay,onoccasionsduringthefinancialyear,calluponAccountingOfficerstosubmitforecastsofthetotalestimatedexpendituretobeincurredduringtheyearfromthevotesundertheircontrol.

(9) Treasury has theauthoritytowithholdfromaMinistryanyremainingfundsappropriatedforaspecificfunctionifthatfunctionistransferredtoanotherMinistryoranyotherinstitution.TreasuryshallallocatethoseremainingfundstotheMinistryorinstitutiontowhichthefunctionhasbeentransferred.

(10)TreasuryhastheauthoritytoauthorisethetransferofspecificassetstoaMinistryoranyotherInstitutionwherethefunctionservedbythatassethasbeentransferredtoanotherMinistry.

Virementing

37.(1)Thepowertovirementfromonesub-votetoanotherorthecreationofnewsub-headrestsonlywithTreasury.WiththeauthorityofTreasuryasavingonanysub-headmaybeappliedtomeetexcessbudgetrequirementsonanothersub-headoranewsub-headwithinthesameVote.

Page 15

S.I. 144 of 2019

15

(2)UnlesstheTreasuryexpresslyprecludesAccountingOfficersfromdoingso,theymayauthoriseasavingunderanyitemwithinasub-headorbetweensub-headstobeappliedtomeetexpenditureunderanotheritemwithintheVote.AccountingOfficersmay,withoutTreasuryauthority,virementfundswithinthesamesubhead. (3)AccountingOfficersshallensurethatnovirementsareeffectedontheirbudgetsduringthefirstsixmonthsofthefinancialyear. (4)AccountingOfficers shall ensure that their respective linesMinistries follow proper virementing procedures andapprovalsareobtainedinadvancenotaftertheevent.Itisanactoffinancialmisconduct,asdefinedbytheAct,tovirementfundsbetweensub-voteswithoutTreasuryapproval. (5)Treasuryhastheauthoritytoplacerestrictionsonvirementingfromcertainbudgetlineitems.Savingsonemploymentcostsmaynotbeappliedtomeetexcessexpenditureunderanyitemorsub-headwithoutpriorTreasuryauthority.Savingsoncapitalexpenditureorcapitalprojectsshallnotbevirementedtorecurrentexpenditureitemsorsub-votes.AlltransfersbetweencapitalexpenditureprojectsshallrequireTreasuryapproval.

Additional and supplementary estimates

38.(1)Theexpenditureonvotedserviceisarrangedandlimitedbytheprintedestimatesofexpenditure.ShoulditbecomeapparentthataprovisionisinadequateandtheAccountingOfficerissatisfiedthatnosavingsexistwhichcould,intermsofInstructionsNos.0436and0437,beappliedtothemeetingoftheadditionalexpenditure,AccountingOfficersshallapproachTreasuryforsupplementaryoradditionalestimatesasprovidedforintheAct. (2)Theresponsibilityfordealingwithlineministries’requestsforsupplementaryoradditionalfundsrestswithTreasury.These shall be dealtwith in accordancewith the provisions of theAct.AccountingOfficers shall also ensure that bids forsupplementaryoradditionalfundsarenotmadeunnecessarily. (3)AccountingOfficersshall,inatimelymanner,notifyTreasuryofanycasesofinescapableexpenditure.ShoulditbeagreedbytheTreasurythatspecialauthoritymaybesoughtintermsofsection24oftheAct,theAccountingOfficerconcernedshallsubmittotheTreasuryanapplicationintheformatdeterminedbyTreasury. (4)TheapplicationreferredtoinInstructionNo.0443aboveshallbesignedbytheAccountingOfficerpersonallyandshallbeaccompaniedbyamemorandumsettingoutthefulldetailsoftheexpendituretobeincurredandthereasonswhyitcannotbedelayed.Anindicationshallalsobegivenofsavingseffectedortobeeffectedonothersub-headsoftheVoteandofthepositionof the Vote in general.

Special warrants on budgets

39.(1)IftheAppropriationActforafinancialyearhasnotcomeintooperationbythebeginningofthatfinancialyear,Treasuryshall,withtheauthorityofthePresident,withdrawmoneyfromtheConsolidatedRevenueFundtomeetexpenditurenecessarytocarryontheservicesofthegovernmentforthefirstfourmonthsofthefinancialyear.Themoneywithdrawnshall— (a) notexceedonethirdoftheamountincludedintheestimatesforthepreviousfinancialyear;and (b) beincludedinanAppropriationActforthefinancialyearconcerned. (2)Treasuryshallwiththeauthorityof thePresident,withdrawmoneyfromtheConsolidatedRevenueFundtomeetexpenditurewhichwasunforeseenorwhoseextentwasunforeseenandforwhichnoprovisionhasbeenmadeunderanyotherlaw.Themoneywithdrawn— (a) shallnotexceedoneandone-halfpercentofthetotalamountappropriatedinthelastmainAppropriationAct; (b) mustbe included inadditionalorsupplementaryestimatesofexpenditure laidwithoutdelaybefore theNational

Assembly;and (c) iftheNationalAssemblyapprovestheestimates,themoneymustbechargedupontheConsolidatedRevenueFund

byanadditionalorsupplementaryAppropriationAct. (3) If Parliament is dissolved before adequatefinancial provision has beenmade for carrying on the services of theGovernment,Treasuryshall,withtheauthorityofthePresident,withdrawmoneyfromtheConsolidatedRevenueFundtomeetexpenditureneededtocarryonthoseservicesuntilthreemonthsaftertheNationalAssemblyfirstmeetsafterthedissolution.ThemoneywithdrawnshallbeincludedinanAppropriationActunderrespectivevotesforthedifferentheadsofexpenditure.

Budget reporting

40. (1)TheDirectorofFinance shallprepare for theAccountingOfficer,monthly,quarterlyandannualbudget reportscomparingbudgetedtoactualreceiptsanddisbursements.Thereportsshallalsoprovideexplanatorynotesonvariances. (2)TheAccountingOfficershallsubmitthemonthly,quarterlyandannualbudgetreportstoTreasuryunderhis/hersignature.Theprovisionsofsection83oftheActrequirethatannualreportssubmittedbytheAccountingOfficerincludeareportontheactivities,outputsandoutcomesoftheirrespectivelineMinistry.

Condonation of unauthorised excess expenditure

41.(1)AccountingOfficersshallnotifyTreasuryinwritingofanyunauthorisedexcessexpenditureinaccordancewiththeprovisionsofsection19(2)oftheAct. (2)FailuretoreportunauthorisedexcessexpenditureconstitutesanactoffinancialmisconductasdefinedinthePFMRegulations.

Page 16

Public Finance Management (Treasury Instructions), 2019

16

PART VIrevenue manaGement

Receivers and collectors of revenue

42.(1)Theobjectiveofthissectionistoensurethatthereareadequatesystemsinplaceforthepropermanagementofpublicfunds.Theinstructionsinthissectionaremeanttoensurethatallmoneyreceivedisproperlyaccountedforandthatthereisseparationofresponsibilitiesbetweenthehandlingandtherecordingofcash. (2)Receiversofrevenueareappointedintermsofsection10oftheAct, toberesponsibleforthecollection,receipt,custody,issueandcontrolofpublicmoneys. (3)TheSecretaryforFinanceshallberesponsibleforrevenuefromloansraisedbyGovernmentandallrevenuesthatisnottheresponsibilityofanyotherReceiverofRevenue. (4)ItisthedutyofReceiversofRevenuetosuperviseandasfaraspossibleenforcethepunctualcollectionanddisposalofrevenueandotherpublicmoneysinaccordancewiththelaws,regulations,instructionsoragreementsrelatingtheretoandtotakesuchactionasmaybenecessarytoensurethatrevenuecollectionsaresafeguardedandproperlybroughttoaccountinaccordancewiththeseinstructions.ReceiversofRevenueshallissue,totheDepartmentsundertheircontrol,suchdetailedinstructionsinconnectionwiththeforegoingfunctionsastheydeemappropriate. (5)ReceiversofRevenuemayappointCollectorstoassistthemincarryingouttheirfunctionsandsuchCollectorsshallcomplywithalllawfulinstructionsanddirectionsasmaybeissuedtothembyReceiversofRevenue. (6)WhereReceiversofRevenuehavebeenauthorisedtoruncomputerisedsystemsthatareindependentofthePFMS,theyshallensurethatfull,properandauditablebooksofaccountsarekeptforthetransactionsforwhichtheyareresponsible.TheminimumsetofbookstobemaintainedbothinelectronicandhardcopyshallbeprescribedbytheAccountant-Generalfromtime to time. (7)ReceiversofRevenueshallinstituteandmaintain,inadditiontotheprimaryanddetailedexaminationundertakenbyaccountants,appropriateindependentsystemsofinternalcheckandcontrolinrespectofrevenuesandotherpublicmoneysforwhichtheyareresponsible.CopiesofallwritteninstructionsissuedbyReceiversofRevenueshallbetransmittedtotheAccountant-GeneralforapprovalandtheAuditor-Generalforinformation. (8)ReceiversofRevenueshall,whenevercalledupontodoso,submitestimatesand/orforecastsofrevenuecollectionstotheTreasurybysuchdateandinsuchformastheTreasurymayrequire. (9)ReceiversofRevenueshall,wheneverpracticable,ensurethatallcontractsandagreementsinvolvingthepaymentofmoneystoGovernmentwithwhichtheirMinistriesmaybeconcernedareinwritingandexpressedinappropriateterms.WhereappropriatetheGovernmentAttorneyshallbeconsultedinthedrawingupofagreementstoensurethattheirtermsadequatelysafeguardGovernmentinterests.ReceiversofRevenueshallensurethat,sofarasitispossible,themonthofDecemberwillnotbeusedinsettingthedateonwhichmoneysduetoGovernmentbecomepayable. (10)ReceiversofRevenueshallensurethatparticularcareistakenwhenconcludingcontractsandagreementsbetweentheGovernmentandminorsandshallbecertainthat— (a) minorsareassistedbytheirguardiansandthatthisisproperlyrecordedinthecontractsbytheinclusionofthewords

“assistedbytheirguardian”intheappropriateplace;and (b) incasewhereminorsmakethemselvesliableformonetaryobligations,suretiesareinsistedupon. (11)Everyofficershalltakecognisanceoftherequirementsofanylaw(includingaruleofcourt)regardingthestampingofanyinstrumentwhichmaycomebeforethemintheirofficialcapacity.Noinstrumentwhichisliabletodutyorfee,oranyfine,additionaltosuchdutyorfeeandwhichisnotdutystamped,maybeissued,received,lodged,filed,enrolledorregistereduntilitisdulystampedasrequiredbylaw.Forcomputergeneratedinstruments,officersshallmakeuseofthedigitalstampingsystemwithinthePFMS.Accesstothedigitalstampingsystemshallbelimitedtoauthorisedofficersonly.Officersmanningthesystemshallnotgiveaccesscodestounauthorisedpersonnel.Desktopsfromwhichthesystemisaccessedshallbekeptinsecuredofficesandshallbesafeguardedinthesamemannerasphysicalstamps. (12)TheseinstructionsshallapplytostatutoryfundsinsofarassuchfundsareadministeredbyReceiversofRevenueintheirofficialcapacity.

(13)Anynewrates,scalesortariffsoranychangeinexistingrates,scalesortariffswhichmayaffectrevenueshallbereferredtotheTreasuryforapprovalbeforebeingsubmittedfortheassentofthePresidentorotherrequisiteauthority.Beforeanynewrates,scalesortariffsarebroughtintooperation,theReceiversofRevenueshallbeadvisedanditistheirresponsibilitytoconveysuchadvicetotheofficerprimarilyresponsibleforthecollectionofsuchrevenue. (14)Whereverpossibleandrelevant,ReceiversofRevenueshouldrequiretheelectronictransferoffunds,cheques,andanyotherauthorisedmethodsoftransferoffundstobemadepayabletotheExchequerAccountoftheConsolidatedRevenueFund. (15)IfaReceiverofRevenueisdirectedbyaMinisterorDeputyMinistertorefrainfromcollectinganypublicmoneyswhichsuchReceiverofRevenuebelieveshe/sheshouldcollect;ortodealwithpublicmoneysinamannerwhichtheReceiverofRevenueisnotauthorised,he/sheshallproceedintermsofsection14oftheAct.Similarlyifanofficerissodirectedbyasuperiorofficer,he/sheshallproceedintermsofsection14oftheAct.

Page 17

S.I. 144 of 2019

17

Receipts and licences

43.(1)Thepreferredmethodofacknowledgingreceiptoffundsisthroughelectronicreceipts.AllReceiversofRevenueshallissueelectronicallygeneratedreceiptsfromthePFMSandinduplicate.Onecopyshallbegiventothecustomerandtheotheroneshallbeplacedonfile.OnlyauthorisedofficersshallacceptrevenueandissueelectronicreceiptsfromthePFMS. (2)ManualreceiptsshallonlybeissuedonoccasionswherethePFMSisnotoperationalorwhentheissuingofficedoesnothaveimmediateaccesstothePFMS.ReceiversofRevenueshallensurethatmanuallyissuedreceiptsarepostedontothePFMSassoonasthesystembecomesavailableandwithinthree(3)workingdaysofissueofsuchreceipt.ReceiversofRevenuethatdonothaveimmediateaccesstothePFMSshallensurethatmanuallyissuedreceiptsarepostedontothesystemonaweeklybasis.Thefailuretopostmanuallygeneratedreceiptswithinthesetimelimitsconstituteanactoffinancialmisconduct. (3)Ifanycomputergeneratedreceipthastobevoidedorcancelledashortexplanationofthereasonforthecancellationshallbewrittenonthebackoftheprintedreceipt,andthereceiptstoredwithdocumentsrelatingtotheday’srevenuecollections.

Manual receipt books

44.(1)ReceiptandlicenceformsformanuallygeneratedreceiptsshallbeobtainedbypurchaseordersfromtheauthorisedGovernmentprinters.TheauthorisedGovernmentprintersshallissuethesereceiptandlicenceformsinsequentialorderandshallfurnishtheAuditor-Generalwithdetailsofallsuchissues. (2)Aholderofreceiptandlicenceformsmay,with thewrittenauthorityof theirReceiverofRevenue,supplyformsinnumerical sequence toanyotherofficeordepartment,at thesame timenotifying theAuditor-Generalof the transfer.Anacknowledgementshallbeobtainedfromanyofficetowhichbooksorformshavebeentransferred.Everyofficerhavingpossessionofreceiptandlicenceformsshallmaintainaregistershowingthenameofsupplieroftheforms;thelocation,andusageofeverysuchlooseformorbookofformsfromthetimeofitsreceiptuntilitsfinaldisposalintermsoftheseinstructions. (3)TheHeadofOffice,oranofficerappointedbythem,shallberesponsibleforthesafecustodyandcontrolleddisposalofreceiptandlicenceforms.Whennotactuallyinuseallreceiptandlicenceformsshallbekeptunderlockandkey,andifpossibleinasafeorstrong-room. (4)AtleastonceineverythreemonthstheexistenceofallformsrecordedintheregistershallbeverifiedandtheHeadofOfficeshallforwardawrittenreportoftheseriallettersandnumbersofanymissingformstotheirReceiverofRevenuewhoshallthereuponadvisetheAuditor-Generaloftheloss. (5)Providedthattherearenounadjustederrorstotheperiodcoveredbythecounterfoilsorfixedcopiesofusedreceipts,theymaybedestroyedaftertheexpiryofsixyearsfromthedateoftheirexaminationbytheAuditor-General.ElectronicrecordsshallbedestroyedinaccordancewithguidelinessetbyNationalArchives.

Stamps and face value instruments

45.(1)Themaindistributorsandsub-distributorsareappointedbytheTreasuryandtheyshallprovidetheAuditor-Generalwithdetailsofallstamps,facevalueinstrumentsandothersecurityitemsissuedbythem.AccountingOfficersandReceiversofRevenueshallprovidereceiptstodistributorsforstampsandinstrumentsreceivedbythemandshallaccountfortheminsuchmannerastheirDepartmentalInstructionsmaydirect.WhereTreasuryappointsorhasappointedadistributorofstampsandfacevalueinstrumentstheAccountingOfficerorReceiverofRevenueshallcausetobemaintainedanindependentrecordofexpendedrevenueout-turnstobereconciledwithpaymentsfromsuchdistributorsatsuchintervalsastheReceiverofRevenuemightdeemnecessary. (2)Distributors,ReceiversandCollectorsofRevenueshallmaintainrecordsofstamps,instrumentsandothersecurityitemsissued,received,sold,spoiledanddestroyedandofstampsandinstrumentsonhand. (3)Stocksofstampsandfacevalueinstrumentsshallbekeptinsafesorstrong-roomsunderthecontroloftheresponsibleofficer.Suppliesheldforimmediateuseshallbetreatedascashandcontrolledaccordingly. (5)Noholderofstampsandfacevalueinstrumentsapartfromadistributorshallsupplystampsandinstrumentstoanotherofficeexceptincasesofextremeurgency.AllsuchtransfersandanyreturnstodistributorsshallberecordedintheregisterofbothsupplyingandreceivingofficesandshallbereportedbybothofficestotheAuditor-General.Thereceivingofficershallgivethesupplyingofficerareceiptwhichshallberetainedinorwiththeregisterforauditpurposes. (6)Atthecloseofeachmonth,andatregularintervals,HeadsofOfficeshallexaminethestockofstamps,facevalueinstrumentsandothersecurityitemsinthecustodyoftheircollectors.TheyshallcheckandcertifyanyreportspreparedfortransmissiontotheReceiverofRevenue. Intheeventofstamps(bothphysicalanddigital)orfacevalueinstrumentsbecomingdamagedorotherwiseunfitforuse,thefactsshallbereportedbytheresponsibleofficertotheirReceiverofRevenue. (7)ProvidedtheReceiverofRevenueissatisfiedwiththeexplanationsgiven,theymayauthorizethewrite-offoftheitemsinquestion.TheReceiverofRevenueshalladvisetheAuditor-Generalofallitemsdealtwithintermsofthisinstruction. (8)SpoiledorobsoletestampsandfacevalueinstrumentsshallbedestroyedbyoneresponsibleofficerinthepresenceofanotherresponsibleofficernominatedbytheReceiverofRevenue.Bothofficersshallsignacertificateofdestructioninduplicate,specifyingtheitemsdestroyedandthemeansofdestruction.TheoriginalshallbesenttotheReceiverofRevenueandtheduplicateshallbefiledbythecollectorforauditpurposes. (9)Whereanylossordeficiencyofstamps,facevalueinstruments,orothersecurityitemsisdiscoveredtheprocedurelaiddowninInstructionNos.0528and0529shallbefollowed.

Page 18

Public Finance Management (Treasury Instructions), 2019

18

PART VIIreceiPt and recordinG, custody and disPosal oF Public money

Receipt and recording of public moneys

46.(1)ReceiptsintheseInstructionsareconsideredtoincludecurrency,coins,electronicfundstransfers(EFT),cheques,bankdrafts,moneyordersandanyothermethodofreceivingfundsthatisauthorisedbyTreasury.Electronicfundstransfersincludethefollowing— (a) realtimegrosssettlement(RTGS)andtelegraphictransfers(TT); (b) onlinebanktransferatpointofsale; (c) useofpaymentcardatpointofsale[swipecards(debitcardorcreditcard)];and (d) mobilebasedpaymentatpointofsale(i.e.telecash,eco-cash,onewalletetc.). (2)ThepreferredmodeforreceiptofrevenueiscashorEFT.ReceiversofRevenueshallensurethattheEFTmethodsadoptedaresecure,safeandobtainedfromreputablefinancialinstitutions.ThebrandandtypeofelectronicpaymentcardsthatareacceptableshallbedeterminedbyTreasuryfromtimetotime.Wherepracticableanofficeracceptinganelectronicbasedpayment,shallrecoveranycommissionorbankchargesinrespectofthatpayment.BankchargeswhicharenotrecoveredinthismannershallbechargedagainsttheVoteoftheMinistryorDepartmentreceivingthepayment. (3)WherefundsarecollectedthroughEFTmethod,PFMSgeneratedreceiptsshallonlybeissuedoncethetransactionhasbeensuccessfullycompleted.ThefollowinginformationshouldbeobtainedforallEFTtransactions— (a) nameofthepersontransferringfunds; (b) nationalidentitynumber; (c) physicaladdress; (d) phonenumber;and (e) signature(whereapplicable). (4)InadditiontotherequirementsinInstructionNo.0533,thefollowingcontrolsshallbeobservedonfundsreceivedthroughmobilebasedplatforms— (a) amerchantnumberandanear-fieldcommunication(NFC)enabledpointofsale(POS)machinethatislinkedtothe

Receiver’sauthorisedbankaccountmustbeused.ReceiversofRevenuearenotallowedtousemobilephonelinestocollectpublicfunds.Undernocircumstancesshallanindividual’smobileaccountbeusedtoreceivefundsonbehalfofGovernment;

(b) theNFCenabledPOSmerchantmachinesmustbeownedbytheMinistryandnotbyindividuals.ItistheresponsibilityofAccountingOfficerstoensurethatthisInstructioniscompliedwithatalltimes;

(c) inadditiontothereceiptprintedonthePOSprintout,aPFMSgeneratedreceiptshouldalsobeissuedwhenthemobiletransfertransactionshavebeensuccessfullycompleted;

(d) arrangementsshouldbemadewiththecommercialbanktosweepthefundsreceivedtotheSub-ExchequerAccountattheendofeachday;

(e) reconciliationsonthefundsreceivedthroughmobilefundstransfershouldbecarriedoutonadailybasis;and (f) theNFCenabledPOSmachinesmustbetreatedassecurityitemsandaccesstothesemachinesshouldberestricted

toauthorisedofficers. (5)WhereReceiversofRevenuehaveauthorisedtheuseofcardswipePOSmachines,thesemachinesasisprovidedinInstructionNo.0534,shallbelinkedtotheMinistry’sSub-ExchequerAccountandnottoindividualaccounts.ThePOSmachinesshallbeownedbytheMinistryandshallbetreatedassecurityitems. (6)Thereceiptofrevenuethroughonlinebanktransfers,RTGSandTTsshallbelinkedtotheMinistry’sSubExchequerAccount.Reconciliationsshallbedonedailytoconfirmreceiptoffunds.APFMSgeneratedreceiptshallonlybeissuedoncethebanktransfersarereflectedontheMinistry’sbankstatement. (7)Incaseswhererevenueisreceivedthroughdirectdeposits,ReceiversofRevenueshallensurethatthebankingcodesarealignedtotherevenueheadsinthePFMStofacilitateautomaticupdates.Therevenueheadsshallthereforebeprenumberedoneachdepositslip.ItistheresponsibilityofReceiversofRevenuetoensurethatreconciliationsarecarriedoutdailytoconfirmreceiptoffunds.APFMSgeneratedreceiptshallonlybeissuedoncethedepositedfundsarereflectedontheMinistry’sbankstatement. (8)Receiversofrevenueshallexercisediscretioninregardtotheacceptanceofcheques,providedthatwherepersonalchequesareinvolved,theyshallbebankcertified.Cheques,moneyorders,orothernegotiableinstrumentsfortheaccountofGovernmentshallbecrossed“notnegotiable”assoonastheyarereceived.Thisinstructionshallnotapplytothoseinstrumentswhicharereceivedforsubsequentencashment.WhereachequefortheaccountofGovernmentisdrawninfavourofapayeeotherthantheExchequerAccount,thepayeeshallendorsethechequebywritingatthebackofthecheque“PaytotheOrderoftheExchequerAccount”andappendingtheirsignature. (9)InstructionsNos.0540to0546relatetoremittancesandregistereditemsreceivedthroughthepostorcourierservices.WhereaReceiverofRevenuedeemstheinstructionstobeimpracticableinrespectoftheirMinistryoranydepartmentorofficetherein,theyshallintermsofthisinstructionframealternativeinstructionsforthepriorapprovaloftheAccountant-GeneralandforwardacopythereoftotheAuditor-General.

Page 19

S.I. 144 of 2019

19

(10)Allcash,negotiableinstruments,paymentinstructionsandregisteredmailreceivedthroughthepostorcourierservicesshallberecordedintheregisterprescribedforthepurposeandobtainedfromtheauthorisedGovernmentPrinter. (11)TheHeadofOfficeshallassigntoaresponsibleofficerthedutyofreceivingmailandrecordingintheprescribedregister,detailsofallremittancesorothernegotiableinstrumentsreceivedthroughthepost.Whereverpracticableasecondofficershallbeassignedtoassistinthisdutyandverifytheentries.ReceiversofRevenueshall,whereverpracticableensurethatofficersassignedthisdutyarenotthesameofficersresponsibleforreceiptingandbanking. (12)Inthecaseofincomingregisteredletters,thedateofreceiptandnumberoftheregisteredslipwithdetailsofalllettersrecordedoneachsliporadviceshallbeenteredintheregisterbeforetheregisteredslipissignedandreturnedtothePostOfficeormaildeliveryagent.Theregisteredlettersshallberecordedintherelevantregisterimmediatelyonreceipt. (13)Allmoneys,paymentinstructionsorothernegotiableinstrumentsreceivedandenteredintheregistershallbehandedoverwithoutdelaytotheofficerresponsibleforbringingthemtoaccountanddueacknowledgementobtainedintheregister.Themoneysshallremaintheresponsibilityoftheofficerwhosedutyitistoenterthemintheregisteruntilanacquittanceforthemhasbeenreceivedfromsomeotherofficer. (14)Wheretheresponsibleofficerisnotimmediatelyavailabletoreceiveremittancesdeliveredbyhand,theyshallberecordedintheregisteranddisposedofinthesamemannerasremittancesreceivedthroughthepost.Ifthesenderhasenteredtheitemina“letterdeliverybook”thereceivingofficershallverifythecontentsoftheenvelopeorpacketwiththeentryinthebookandshallsignthelatterinacknowledgementofreceipt. (15)AtleastonceaweektheHeadofOfficeoraresponsibleofficerdelegatedbythem,shallexaminetheremittanceregistertoensurethatallentriesarecompleteandcorrectandthattheremittanceshavebeendulybroughttoaccount.HeadsofOfficeshall,atthecompletionoftheirexamination,sign,dateandstamptheregisteraccordingly. (16)Noreceiptorlicenceformshallbeissuedinthecaseofmoneysreceivedinrespectof— (a) stamps(physicalordigital)ortokensimpressedbymeansofadiedenotinganyfeeordutyorrateofduty;or (b) cashsaleinvoices,inrespectofwhichTreasuryhasagreedthatreceiptsneednotbeissued. (17)SubjecttotheprovisionsofInstructionNo.0546officersshall,immediatelyuponreceivingmoneyintheirofficialcapacity,issueanelectronicreceiptorlicenceprescribedforthepurpose,asappropriate.Noreceiptshallbeissuedforachequeuntiltheduedateofsuchcheque.ThesameappliestopaymentinstructionsrelatingtoRTGS.IftheduedatefallsonaSundayoranon-businessdaythepaymentshallbereceiptedandbroughttoaccountinthemonthrelativetothedateofthechequeorpaymentinstructionsthoughthechequemaybedepositedintheensuingmonth. (18)Whetherrevenuehasbeencollecteddirectlyfromindividuals,throughthemailorbyEFT,thereceiptissuedshouldincludeasaminimum— (a) payer’sname; (b) amountofpayment.Theamountshallbestatedinfiguresandinwords.Thecurrencytenderedshouldalsobestated; (c) modeofpayment(cash,banktransfer,debitcard,moneyorder,etc.); (d) thedateinbankandserviceprovidertransactionnumber(forelectronicbanktransfers); (e) chequeormoneyordernumber(ifapplicable); (f) purposeofpayment; (g) dateofpayment; (h) nameofofficercollectingthemoney. (19)Wherepaymentismadebychequeandthereceiptismadeouttoanameotherthanthatofthedrawerofthecheque,thenthereceiptmustincludethenameofthedrawer.Wherepaymentismadebyadirectdeposittoanofficialbankingaccounttheactualdateofthedepositshallbenotedonthereceipt. (20)Allreceiptandlicenceformsthatarewrittenmanuallyshallbeissuedinsequentialorder.Blueorblackinkorindeliblepencilshallbeused.Theamountandfiguresonareceiptshallnotbealtered.Ifamistakeismadethereceiptorlicenceformshallbecancelledandafreshoneissuedinlieuthereof. (21)Ifmorethanonepersoninadepartmentareissuingmanualreceipts,eachpersonshallbeassignedtheirownreceiptbookandshallberesponsibleforthemaintenanceanddepositofrevenuerecordedinthatbook.Inaddition,aseparateReceiptBookorseriesoflicenceformsshallbeusedforeachCashBook.Allreceipts,includingvoidedandcancelledreceipts,mustbeaccountedfor.ThereceiptsshouldbeenteredinsequentialorderintherelativeCashBook. (22)Theoriginalandallcopiesofvoided,cancelledorspoiledformsshallberetainedforsubsequentexaminationbytheAuditor-GeneralexceptasisprovidedforinInstructionNo.0558. (23)Whenachequeforwhichareceipthasbeenissuedhasbeenreturnedtothedrawerforanyreason,nofurtherreceiptshallbeissuedonre-presentationtothebank.Thesameappliestoamerchantcardtransactionrejectedbythebankandtheanomalyisrectified. (24)Cash,chequesorotherinstrumentstenderedorexpressedinaforeigncurrencyshallbereceiptedusingtheexchangeconversionratesprovidedbythePFMSsystemonadailybasis.WhereaReceiverofRevenuedeemstheinstructionstobeimpracticableinrespectoftheirMinistryoranydepartmentorofficetherein,theyshallintermsofthisinstructionframealternativeinstructionsforthepriorapprovaloftheAccountant-GeneralandforwardacopythereoftotheAuditor-General. (25)Manualreceiptsissuedmay,ifadministrativeconvenienceisbetterservedthereby,beseparatelyscheduledandthetotalofthereceiptspostedtotheCashBookdailyoratsuchotherintervalsastheReceiverofRevenueorAccountingOfficermayprescribe;providedthatonthelastdayofthemonthallreceiptsnotpostedforthatmonthshallbebroughttoaccount.

Page 20

Public Finance Management (Treasury Instructions), 2019

20

(26)Thedateonwhichmoneysarereceivedgovernsthedateoftherecordingofthetransaction.Allreceiptsdateduptoandincludingthelastdayofthemonthorfinancialyearshallbebroughttoaccountinthatmonthorfinancialyearnotwithstandingthefactthattherelativemoneysarestillonhandorintransit.However,thiswillnotapplyinthecaseofFunds(seeInstructionNos.1200-1299)operatingonanaccrualbasiswheretheAccountingOfficerwillhaveissuedspecificinstructions,withTreasuryapproval,tothecontrary. (27)Moneysreceivedbydirectdepositintoanofficialbankingaccountshallbeintroducedbyjournalintothebooksofaccountifitisnotpossibletoissuetherelativereceiptsorlicencesbeforetheendofthefinancialyeartowhichtheyrelate.Suchactionshallnotobviatethenecessitytoissuereceiptsorlicencesinrespectofsuchmoneysinthenewfinancialyear. (28)WheretheReceiverofRevenuedirects,thecarboncopyofeveryreceiptorlicenceformissuedbyabranchofficetogetherwiththebankstampeddepositslips,shallaccompanythecashschedulessubmittedtoHeadOffice.Theoriginalandduplicatecopiesofvoided,cancelledorspoiledformsshall, if theReceiverofRevenuesodirects,be includedtoprovethenumericalsequenceoftheissues.

Custody of public moneys

47. (1)Exceptwhenrequiredfor immediateuse,orwhenbeing temporarilystored in thecourseofcollectionunder theimmediatecontroloftheofficershandlingit,moneyshallnotbeleftincash-boxesordrawerseveniflocked.Loosecashandcash-boxesshallbelodgedinasafeorstrong-roomateverypossibleopportunity.Wherenosafeisavailableintheofficeofofficersholdingpublicmoneys,theyshall,wherepracticable,lodgethemoneyorcash-boxinthesafeofsomeotherofficerwhoshouldfurnishareceiptforsuchmoneyorcash-box. (2)Money shall not be left in the care of, nor shall it be transferred to, another person unless they have given anacknowledgementinwritingthereoftotheresponsibleofficer. (3)TheHeadsofOfficeorofficersdelegatedbythemshall,atirregularintervalsandinanycasenotlessfrequentlythanonceamonthandatthemonthend,comparetheentriesintheCashBookswiththeduplicatecopiesofreceipts,counterfoilsoflicences,stocksorstampsandfacevalueinstruments,bankdepositslipsandchequecounterfoilsandanyotherrelevantdocuments.Theyshallsatisfythemselvesthattheinstructionsinthissectionhavebeencarriedoutandshallcertifytheirexaminationbysigninganddatingtherelevantrecords. (4)Anysurplusofcashdiscoveredshallbebroughttoaccountasrevenue—“Unclaimedandconfiscatedmoneyorproperty”andareceiptshallbeissuedaccordingly. (5)Whereanydeficiencyofcashorfacevalueinstrumentsisdiscoveredanditisnotsuspectedtobeduetotheftorfraudthefollowingprocedureshallbecarriedout— (a) wherethedeficiencydoesnotexceedthethresholdsetbyTreasury,theHeadofOfficeshallinvitetheofficerwhom

heorshedeemstoberesponsibleforthedeficiencytomakegoodtheamountinvolved.AtthesametimetheHeadofOfficeshalladvisetheofficerthatheorsheisnotcompelledtomakegoodthedeficiencyandmaychoosetohavethematterreportedtoTreasury.IftheofficerelectstomakegoodtheamountofsuchdeficiencythemattershallthenbereferredtotheTreasurygivingalltherelevantdetailswitharecommendationbytheReceiverofRevenue,supportedbyreasons,astotheamountifany,whichheorsheconsidersshouldbereimbursedtotheofficerconcerned.NocaseshallbesubmittedtotheTreasuryuntilthefullamountofthedeficiencyhasbeenmadegood.AnyreimbursementauthorisedbytheTreasuryshallbepaidfromtheVoteoftheofficer’sdepartmentunlessotherwisedirectedbytheTreasury;and

(b) wherethedeficiencyexceedsthethresholdforAccountingOfficerthataresetbyTreasury,themattershallbereportedbytheReceiverofRevenuetotheAccountant-General.

(6)Whereanylossordeficiencyofcash,stampsornegotiableinstrumentsisdiscoveredandafterpreliminaryinvestigationitissuspectedthatsuchlossordeficiencyisattributabletocriminalactionitshallimmediatelybereportedtothepoliceforinvestigationandtotheReceiverofRevenuewhoshallreportthemattertotheTreasury. Disposal of public moneys

48.(1)TheCommissioner-GeneraloftheZimbabweRevenueAuthorityandthoseReceiversofRevenuewhohavebeenauthorisedtooperatecontingencyaccountsinrespectoftheirrevenuemayretainintheirdepositorcontingencyaccountssuchsumsasarerequiredformakingrefundsofrevenueandforclearingcollectionstootherreceivers.ThebalanceshallbepaidintotheExchequerAccountatsuchintervalsastheTreasurymaydirect. (2)Refundsofoverpaymentsofrevenueormoneysbroughttoaccountinerrorwill,exceptintheinstancementionedinInstructionNo.0565,bemadebytheTreasuryfromastatutoryappropriation.ReceiversmustsubmitproperlycertifiedvoucherstotheTreasuryinthisrespect. (3)Exceptwhenauthorised inanywritten instructionsgivenbyReceiversofRevenue,all revenuesandotherpublicmoneysreceivedbycollectorsshallbedepositeddailyinthelocalbankforthecreditoftheExchequerAccountorotherseparateaccountsapplicableandmoneysnotsodisposedofshallbedepositedonthenextbankingday. (4)Allmoneyreceivedmustbebankedintactandinthecurrencyinwhichtheywerereceived.Nopersonalchequesoranyothermoneysincludingcashbackshallbemadefromthemoneythathasbeenreceipted.Noreceiptingofficershallunderanycircumstancesreceiptanymoney,otherthaninthecurrencyinwhichtheyreceivedthepaymentfromathirdparty. (5)Whenpreparingchequesfordepositing,theresponsibleofficershallensurethatthenameoftheaccounttobecreditedisindicatedonthereversesideofeachcheque.Theofficershallalsoindicateforeachchequeseparatelyonthedepositslipthefollowinginformation—

Page 21

S.I. 144 of 2019

21

(a) chequenumber; (b) drawer’sname; (c) draweebank; (d) theamountofchequeandensuretheslipcontainsdetailsof— (i) account number; (ii) depositnumber;and (iii) depositor’sbankingstationnumber. (6)Whereverpracticable,asecondofficershallbeassignedtocross-checkthecastingandotherdetailsonthedepositslip. (7)Whenadishonouredchequeisreturnedbythebankimmediatestepsshallbetakentocontactthedrawerandobtainpayment.Wherethechequeistobere-presenteditshallbeenteredonaseparatedepositslip,acrosswhichshallbemarkedboldly“Re-deposit”tofacilitateidentificationofsuchdeposits.Forrejectedpaymentcardtransactions,stepsshouldbetakentocommunicatewiththeownerofthedishonouredmerchantcardwithaviewtocorrecttheirregularityortoobtainpayment. (8)AllmonetarygiftstoGovernmentfromanysourcewhichfallunderthecategoryofsection6(2)(e)oftheActshallbenotifiedbytheReceiverofRevenuetotheTreasuryimmediatelyonreceiptofthegiftortheofferofthegift.TheTreasuryshalldirectwhetherthegiftshallbeacceptedornotandhowitshallbedisposedofandwilladvisetheAuditor-General.Giftsofanon-monetarynatureshallbedealtwithinaccordancewithInstructionNo.1104. (9)Exceptinregardtooverpaymentsorerroneouspaymentswhicharesubjecttodisallowances,inallothercases,receiptsorrecoveriesagainstVotedexpenditureshallbecreditedtorevenue. (10)WhereanyamountwhichisauthorisedtobeappropriatedinaidofaVoteisrelatedtoaspecificitemofexpenditurewithinthatVote,anyreceiptsinexcessoftheactualexpenditureonthatitemasattheendoftherelevantfinancialyearshallbepaidintorevenuenotwithstandingthatthereareshortfallsinreceiptsrelatedtootherexpenditureitemsorontheappropriation-in-aidasawhole. (11)NoofficershallincludeanyprivatemoneysinanofficialbankingaccountnoranypublicmoneysinaprivateaccountandnoofficershallpermitanymoneysotherthanpublicmoneystobekeptinaGovernmentcash-box,safeorstrong-room.

Recovery

49.(1)Asageneralrule,ReceiversofRevenueareresponsibleonlyforthecollectionoftheirownrevenuesanddebtsbuttheymayassistotherMinistriesordepartmentsbyaccepting,onanagencybasis,moneyswhichmaybetenderedinrespectofdebtsduetothoseotherMinistriesordepartments. (2)OfficersresponsibleforcollectingdebtsshalltakeadequatestepstocollectanysumsduetotheGovernmentonduedateandshallonnoaccountallowadebttobecomeextinguishedthroughlapseoftime.Theruleof“set-off”shouldbeappliedwhereappropriate.Anydebthavingaclearlydeterminedmoneyvalue,ofthesamenature,payableunconditionally,andlegallydueandpayablebyanyperson,maybesetoffagainstordeductedfromanymoneysowingbytheGovernmenttosuchperson. (3)AllofficersresponsibleforthecollectionofmoneysduetotheGovernmentshalltakenoteofGovernmentcontractswithdebtorsand,iftheyareexperiencingdifficultyincollectingsumsdue,shallrequesttheappropriateAccountingOfficer,subjecttoInstructionNo.0579,toarrangeforthedeductionsofsuchamountfromanypaymenttobemadetothedebtor. (4)WhenadebtowedtoGovernmentiscollectedbyset-off,thedepartmentconcernedshallinallcasesensurethatthefullamountpayablebyGovernmentisproperlychargedtotheVoteandthattheamountwithheldiscreditedtothedebtor’soutstandingaccount.Fulldetailsoftheactiontakenshallbeprovided,fortheinformationofthedebtor,bytheDepartmenteffectingtheset-off. (5)Amountsowingbyofficersmaybeset-offagainsttheirsalariesorwages.Ifthesetting-offofthewholeamountinonelumpsumwillresultinfinancialembarrassmenttotheofficerstheAccountingOfficershall,afterconsultationwiththeDepartmentrequiringthemtoapplytheset-off,deductthetotalamountbysuchinstalmentsasareapprovedbytheTreasuryintermsoftheAct. (6)Exceptinthecaseofdebtsduefromtheestateofadeceasedofficer,whenInstructionNo.0586shallapply,anamountowingbyapersonwhohasceasedtobeaGovernmentofficermaybeset-offagainstanysalary,pensionorotherbenefitpayabletothem.ThePensionsOfficermay,withagreementofthedepartmentrequiringthemtodoso,deducttheamountduebysuchinstalmentsasarefixedbytheTreasuryintermsoftheAct. (7)AnymoneysrecoveredfromapersonwhohasceasedtobeaGovernmentofficershallbeappliedinthefirstinstancetotheliquidationofdebtsduetoGovernment.WherethemoneysrecoveredareinsufficienttocoveralldebtsduetoGovernment,theyshallbeappropriatedasdirectedbytheTreasury. (8)Whenanofficergivesnoticeof resignationor is tobedischarged from theservice, it is the responsibilityof theAccountingOfficerstoascertainwhethertheofficerisindebtedtoanyGovernmentMinistryorDepartment.TheformprescribedforthispurposeshallbeforwardedtotheappropriateaddresseesandanyotherMinistryordepartmenttowhichtheofficermaybeindebted.DebtswhichhavebeenadvisedtoolateforcollectionbytheEstablishmentOfficershallbedeductedbytheAccountingOfficerfromthefinalpayandforwardedtothecreditorMinistries. (9)WhereadequatestepshavebeentakenbyReceiversofRevenueorAccountingOfficerstorecoveradebtduetotheGovernmentandsucheffortshaveprovedfruitlesstheymayrequesttheGovernmentAttorneytotakelegalactionfortherecoveryofthedebt.TheGovernmentAttorneyshallthereafterbesolelyresponsibleforthecollectionofthedebt.

Page 22

Public Finance Management (Treasury Instructions), 2019

22

(10)OnceadebthasbeenhandedovertotheGovernmentAttorneyforcollectionnonegotiationsshalltakeplacebetweentheMinistryordepartmentandthedebtorandanymoneyspaidbythedebtorshallbeacceptedonlybytheGovernmentAttorney.Thedepartmentshall,however,remainresponsibleformaintainingrecordsofdebtshandedover. (11)Where in the opinion of theGovernmentAttorney the information provided is insufficient for them to proceedsatisfactorilywiththecasetheymayrefusetoacceptit.Inaddition,wherethecostsofanactionarelikelytobedisproportionatelyhighwhencomparedwiththeamountofthedebt,theGovernmentAttorneymaydeclinetotakelegalactionforrecoveryandshallinformtheMinistryordepartmentofthereasonsfortheirdecision. (12)TheReceiverofRevenueorAccountingOfficershallensurethatclaimsaresubmittedagainstinsolvent,deceasedorassignedestatesandshalldeputeanofficertoprovesuchclaimsbyattendingallnecessarymeetingsofcreditors.ClaimsshouldnotbesubmittedwhereitappearsthatsuchacoursewillresultintheGovernmentbeingcalledupontocontributetotheestate.Inanycaseofdoubtregardingthelegalaspectofaclaim,theadviceoftheGovernmentAttorneyshallbesought.

PART VIII recovery or Write-oFF oF Public moneys Abandonment of claims and write-off of public resources

50.(1)NoclaimshallbewaivedorsetasideandnocompromiseacceptedwithoutthepriorapprovaloftheTreasury. (2)NodebtowingtotheGovernmentmaybewrittenoffwithoutpriorgeneralorspecificauthorityoftheTreasury.

Treasury surcharges