18

StealthGas Inc. 4 th Quarter 2012 Results February 21 st , 2013 CONSISTENCY & GREAT VALUE

| Date post: | 19-Jul-2015 |

| Category: |

Documents |

| Upload: | tradewindsnews |

| View: | 161 times |

| Download: | 0 times |

StealthGas Inc.

4th Quarter 2012 Results

February 21st , 2013

CONSISTENCY & GREAT VALUE

Disclaimer

Forward-Looking Statements

This presentation contains forward-looking statements within the meaning of applicable federal securities laws. Such statements are based upon current expectations that involve risks and uncertainties. Any statements contained herein that are not statements of historical fact may be deemed to be forward-looking statements. For example, words such as “may,” “will,” “should,” “estimates,” “intends,” and similar expressions are intended to identify forward-looking statements. Actual results and the timing of certain events may differ significantly from the results discussed or implied in the forward-looking statements. Among the factors that might cause or contribute to such a discrepancy include, but are not limited to the risk factors described in the Company’s Registration Statement filed with the Securities and Exchange Commission, particularly those describing variations on charter rates and their effect on the Company’s revenues, net income and profitability as well as the value of the Company’s fleet.

1

Business Strategy Implementation

Consolidation and fleet renewal

Took delivery of 2 Newbuilding LPG carriers in January & June 2012

Sold 2 LPG carriers in 2012

Acquired 4 Newbuilding LPG carriers to be delivered in 2014 & 2015

Moderate Leverage Q4 2012 net debt to capitalization: 46.4%

Visible Revenue Stream – Consistency

75% of voyage days fixed for FY 2013

42% of voyage days fixed for FY 2014

Modern Fleet Our fleet average age is 10.9 years

Close Customer Relations High quality customer base – low counterparty risk

Cost-Efficient Operations

Consistent Breakeven

Net Income Breakeven of $5,824 per day in Q4 2012 (net on interest rate swaps), compared to $5,991 per day in Q3 2012 to $5,816 in Q2 2012

and $5,847 in Q1 2012.

Share Repurchases 15 million share repurchase program, 1.8 million shares since the program’s inception (cost $8.5 million).

Business Strategy

2

Fleet Development

Newbuilding program of 12 LPG carriers completed with the 2 latest deliveries in 2012

Remaining newbuilding acquisitions have committed financing

With $45mil cash and 3 unencumbered vessels + leverage = $120mil dry powder

3

Fleet Employment Profile

4

Financial Highlights

5

Fourth Quarter 2012

Q4 Net Income of $7.8 million, net revenues of $30.6 million, EBITDA of $17.2 million.

EPS of $0.38 per share on 20.6 million shares outstanding.

Q4 Adjusted Net Income of $6.7 million and Adjusted EPS $0.33 per share, before net

non cash gain of $0.1 million on interest rate swaps, $1.0 million on swap interest paid.

Twelve Months 2012

FY Income of $29.0 million, net revenues of $119.2 million, EBITDA of $67.0 million. EPS

of $1.41 per share on 20.6 million shares outstanding.

FY Adjusted Net Income of $24.2 million and Adjusted EPS $1.18 per share, before net

non cash loss of $1.1 million on interest rate swaps, $4.6 million on swap interest paid,

$1.4 million gain on sale of vessel and $0.1 million unrealized exchange loss.

Cash balance of circa $42.3 million

2012 Income Statement

6

In US$ 000, except per share amounts

Q4 2011 Q4 2012 FY 2011 FY 2012

Net Revenues $28,884 $30,586 $118,281 $119,213

Voyage Costs 4,733 3,856 17,829 12,704

Running Costs 7,766 7,734 36,558 30,592

Operating Income 6,784 9,845 19,826 39,291

Net Income 4,446 7,759 8,550 28,958

Net Income, adjusted 3,438 6,709 11,631 24,177

EBITDA 13,614 17,200

44,539 66,922

EPS 0.22 0.38

0.41 1.41

EPS, adjusted 0.17 0.33 0.56 1.18

Number of Shares, diluted 20,552,568 20,552,568 20,909,154 20,552,568

Balance Sheet

7

December 31, December 31,

2011 2012

Cash and Cash Equivalents incl. restricted 51,793,666 50,913,655

Current Assets excl. cash 5,106,792 6,649,752

Vessels held for sale 921,285 --

Advances for vessels under construction 22,347,811 19,321,045

Vessels, net 613,832,973 634,634,671

Other assets 1,707,624 1,519,908

Total Assets 695,710,151 713,039,031

Current portion of long term debt 33,166,887 35,787,544

Current portion of long term debt associated with vessel held for sale 791,823 --

Current Liabilities 22,142,145 20,021,170

Long Term Debt 317,109,471 309,564,768

Other Liabilities 9,401,798 5,632,107

Stockholders' Equity 313,098,027 342,033,442

Total Liabilities and Stockholders Equity 695,710,151 713,039,031

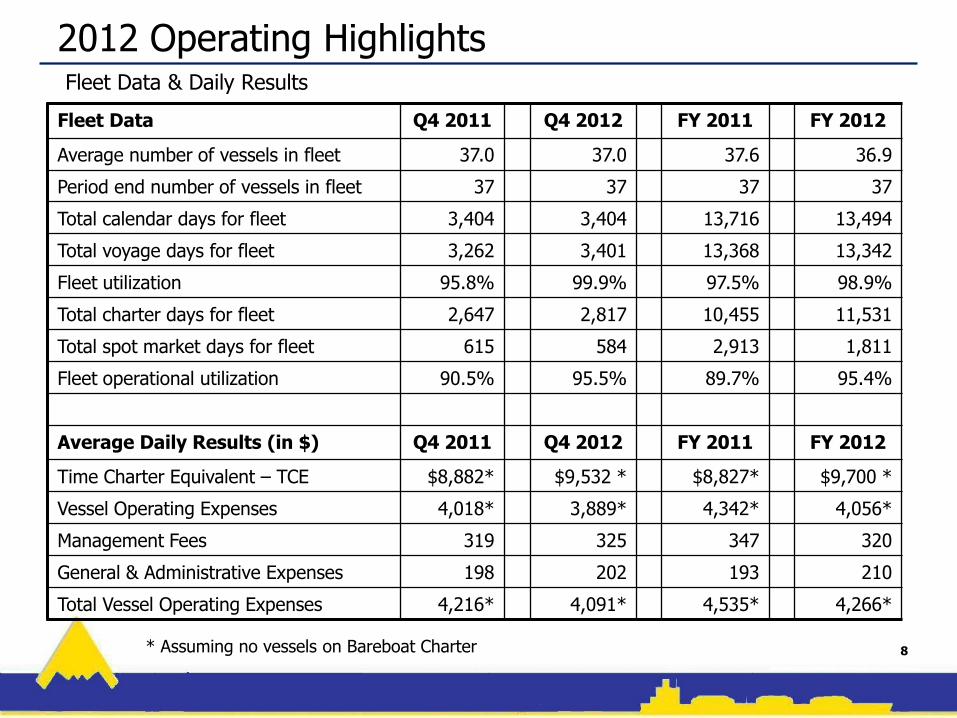

2012 Operating Highlights

8

Fleet Data & Daily Results

* Assuming no vessels on Bareboat Charter

Fleet Data Q4 2011 Q4 2012 FY 2011 FY 2012

Average number of vessels in fleet 37.0 37.0 37.6 36.9

Period end number of vessels in fleet 37 37 37 37

Total calendar days for fleet 3,404 3,404 13,716 13,494

Total voyage days for fleet 3,262 3,401 13,368 13,342

Fleet utilization 95.8% 99.9% 97.5% 98.9%

Total charter days for fleet 2,647 2,817 10,455 11,531

Total spot market days for fleet 615 584 2,913 1,811

Fleet operational utilization 90.5% 95.5% 89.7% 95.4%

Average Daily Results (in $) Q4 2011 Q4 2012 FY 2011 FY 2012

Time Charter Equivalent – TCE $8,882* $9,532 * $8,827* $9,700 *

Vessel Operating Expenses 4,018* 3,889* 4,342* 4,056*

Management Fees 319 325 347 320

General & Administrative Expenses 198 202 193 210

Total Vessel Operating Expenses 4,216* 4,091* 4,535* 4,266*

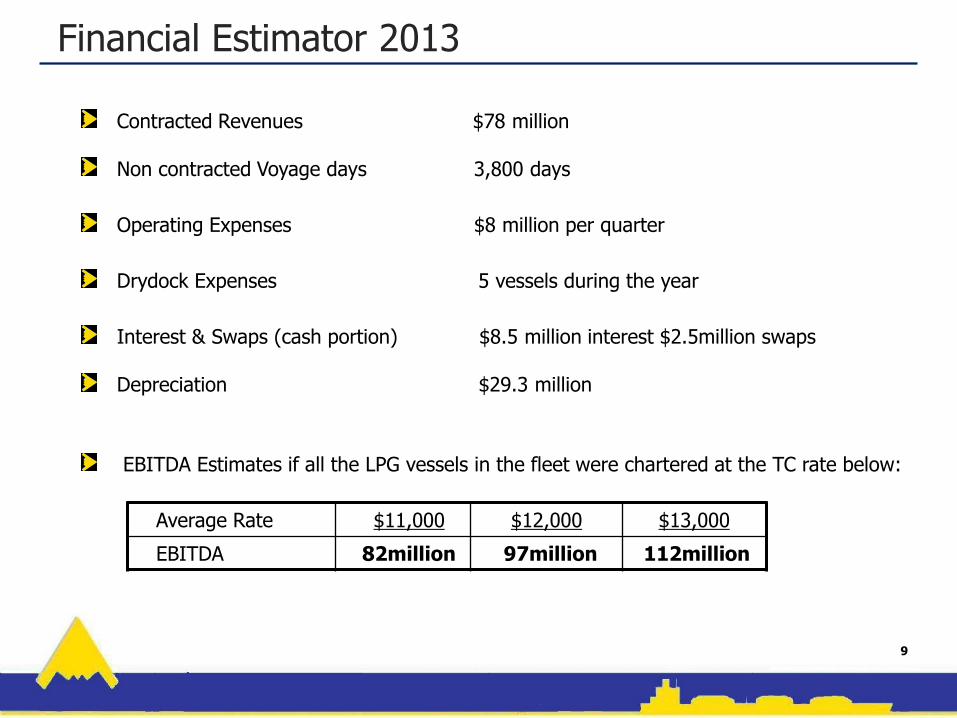

Financial Estimator 2013

9

Contracted Revenues $78 million

Non contracted Voyage days 3,800 days

Drydock Expenses 5 vessels during the year

Interest & Swaps (cash portion) $8.5 million interest $2.5million swaps

Operating Expenses $8 million per quarter

Depreciation $29.3 million

Average Rate $11,000 $12,000 $13,000

EBITDA 82million 97million 112million

EBITDA Estimates if all the LPG vessels in the fleet were chartered at the TC rate below:

Charter Market Rate Indicator (12 Month TCs)

Source: Lorentzen & Stemoco

10

Q3 2012 Average

Q4 2012 Average

Q1 2013 Forecast

3,200 CBM S/R 267,300 260,385 255,000

3,500 CBM P/R 241,730 234,615 237,500

5,000 CBM P/R 306,920 290,000 290,000

6,000 CBM 435,000 435,000 440,000

15,000 CBM 650,000 650,000 750,000

35,000 CBM 805,770 801,923 825,000

60,000 CBM 950,000 921,154 900,000

78,000 CBM 1,077,000 959,615 775,000

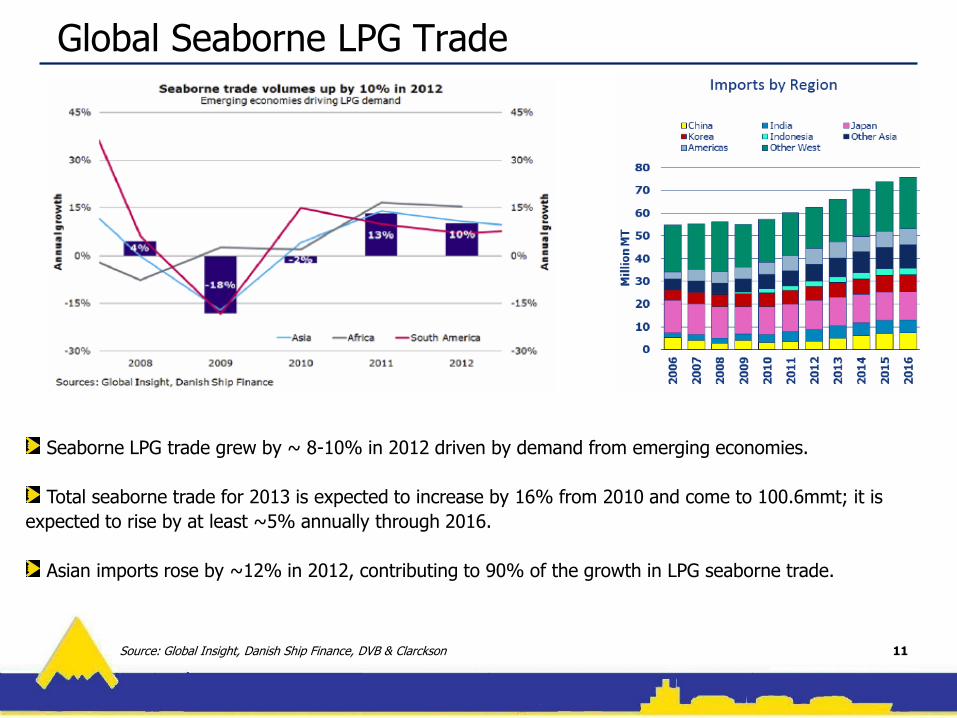

Global Seaborne LPG Trade

11

Seaborne LPG trade grew by ~ 8-10% in 2012 driven by demand from emerging economies.

Total seaborne trade for 2013 is expected to increase by 16% from 2010 and come to 100.6mmt; it is

expected to rise by at least ~5% annually through 2016.

Asian imports rose by ~12% in 2012, contributing to 90% of the growth in LPG seaborne trade.

Source: Global Insight, Danish Ship Finance, DVB & Clarckson

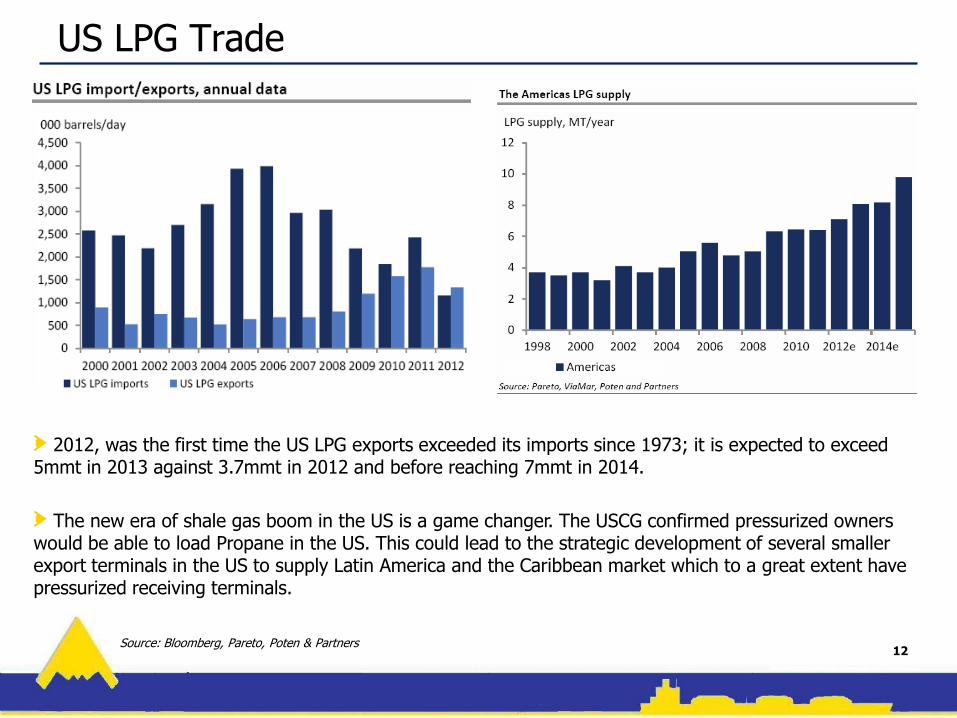

US LPG Trade

12

2012, was the first time the US LPG exports exceeded its imports since 1973; it is expected to exceed 5mmt in 2013 against 3.7mmt in 2012 and before reaching 7mmt in 2014.

The new era of shale gas boom in the US is a game changer. The USCG confirmed pressurized owners would be able to load Propane in the US. This could lead to the strategic development of several smaller export terminals in the US to supply Latin America and the Caribbean market which to a great extent have pressurized receiving terminals.

Source: Bloomberg, Pareto, Poten & Partners

LPG Major Trades

13

The Middle East remained the single largest contributor to growth in total LPG exports in 2012, with

an increase of LPG supply for exports by 8%.

LPG in the US is cheaper than the biggest suppliers in the Middle East, which account for ~35mmt a

year of the estimated 85mtt global seaborne trade. With strong growth in US NGL production from

shale ahead, the export capacity in the US is expected to rise to 12mmt in 2015 from 5mmt now.

An overloaded orderbook in mainstream segments But not in the LPG space

* Includes all LPG Carriers size categories

15

LPG orderbook still remains smaller than other shipping segments with a limited fleet

growth of pressurized vessels for 2012 and a negative fleet growth from 2013 onwards.

StealthGas is in a position to take advantage of positive market dynamics.

25%24%

19% 19%

12% 12%

0%

5%

10%

15%

20%

25%

30%

LNG Offshore Drybulk Container Crude Tankers LPG

3000-8000 cbm Fleet Development Vs. TC Rates/Earnings*

•TC equivalent spot earnings are assessed average earnings in the spot market excluding waiting time. Yearly average

•Fleet growth excl. Chinese fleet, assuming 30 year scrap age by end 2013.

Source: Inge Steensland AS 16

-5%

0%

5%

10%

-

100

200

300

400

500

600

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Flee

t gr

ow

th in

% (

bar

s)

TC e

qu

iv. s

po

t ea

rnin

gsTC

rat

es in

USD

10

00

's p

er m

on

th (

lines

)

Overall 3000-7999 fleet growth SR 3000-7999 fleet growth

SR 6500 cbm TCE SR 3500 cbm 1yr TC

PR 3500 cbm 1yr TC East

INGE STEENSLAND AS

Valuations comparison

Based on Seaborne Capital Advisors February 7th 2012. For StealthGas, based on company’s estimates. 17

Company P/NAV P/EPS 2012

GASLOG (GLOG) 505.5 % 62.6x

GOLAR LNG (GNLG) 178 % 24.3x

SCORPIO TANKERS (STNG) 176.1 % NA

CAPITAL PRODUCT PARTNERS (CPLP) 254.5 % NA

TSAKOS ENERGY NAVIGATION (TNP) 247.1 % NA

TEEKAY TANKERS (TNK) 162.3 % NA

STEALTHGAS (GASS) 75 % 7.7x

Shipping companies listed in the US listed operating in different sectors such as gas, tankers and drybulk,

are trading well above net asset values. Although there may be a variety of reasons for that, we believe there

are no other US listed company operating in a sector that has better fundamentals than our LPG sector; and

yet our stock continues to trade far below our net asset value.

Contacts

Company Contact: Konstantinos Sistovaris Visit our Website at: Chief Financial Officer www.stealthgas.com StealthGas Inc. 011-30-210-6250-001 E-mail: [email protected] www.stealthgas.com

Weekly LPG Market Report

updated every Monday

Comprehensive Investor

Relations Information

18