36

November 10, 2015 Alacero-56 Conference Steely Resolve: China and the Global Steel Industry Usha C. V. Haley, PhD West Virginia University http://usha.tel

November 10, 2015

Alacero-56 Conference

Steely Resolve: China and

the Global Steel IndustryUsha C. V. Haley, PhD

West Virginia University

http://usha.tel

“I call China the mystery meat of emerging

market countries…Nobody knows what’s there

and there’s a little bit of bologna, so we’re just

going to have to wonder going forward as to

the potential problems.”

Bill Gross

Founder/Managing Director/Co-CIO, Pacific Investment

Management Company (PIMCO)

February 5, 2014

Mystery Meat

Research from our bookOxford University Press, 2013

• China’s Move in a few years from Net Importer

to Largest Manufacturer and Largest Exporter in

Capital-intensive Industries, including Steel.

• Industrialized and Industrializing Countries

becoming primarily Exporters of Scrap and

Commodities to China, including Brazil.

• Effects on Business Strategy, Regulatory Policy

and National Competitive Advantage.

Hidden Advantage of Chinese Subsidies

Outline

Capitalism with Chinese Characteristics

Subsidies to Chinese Steel

The 13th 5 -year Plan & Uncharted Future

Our Data & Problems

Antidumping NME & Status

✓

✓

✓

✓

✓

1

2

3

4

5

• China uniquely Synchronizes Party,

Government, Military and Economy.

• Control of Capital Important.

• Flows of Capital Important but Poorly

Understood.

• Multi-organizational with State as

Paramount Shareholder.

Capitalism with Chinese

Characteristics

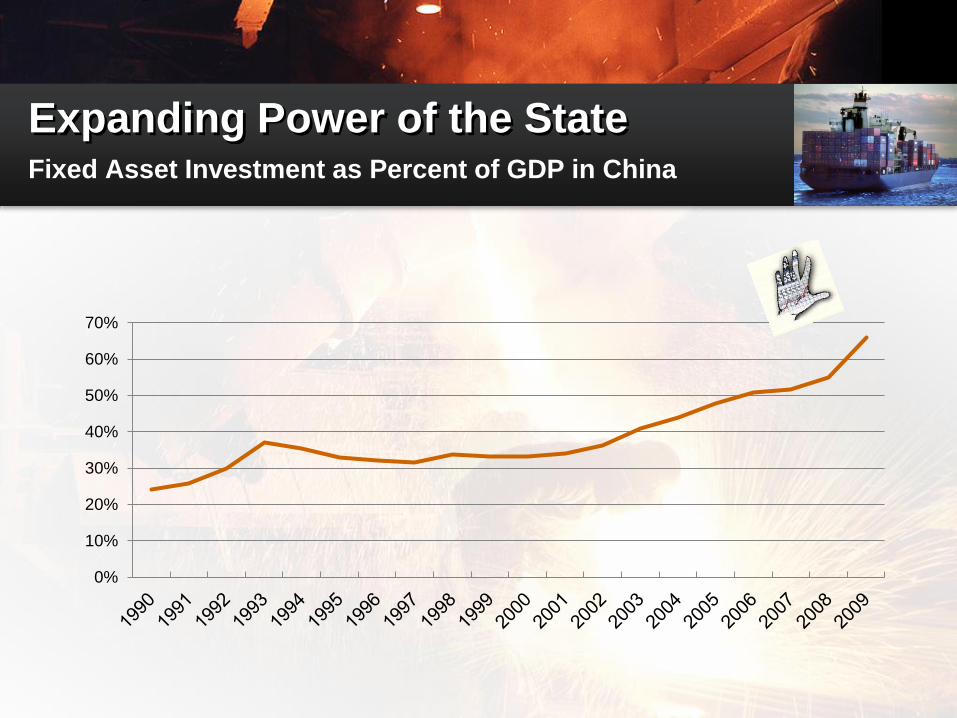

Expanding Power of the StateFixed Asset Investment as Percent of GDP in China

0%

10%

20%

30%

40%

50%

60%

70%

Ratio of Private to Government

Consumption in China

0

0,5

1

1,5

2

2,5

3

3,5

4

4,5

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

• Subsidies to Steel, Glass, Paper, Auto Parts and

Solar PV industries.

• Capital-intensive Manufacturing Industries with

Labor 2%-7% of Total Costs.

• Fragmented Industries with no Economies of

Scale or Scope.

• No Technological Advantage.

• Prices 25% - 30% Lower than US and EU.

China Subsidy Studies

• Free or Low Cost Loans.

• Subsidies to Energy (Electricity, Coal &

Natural Gas).

• Subsidies to Inputs (Soda Ash, Pulp,

Recycled Paper, Glass, Cold-Rolled

Steel), Land & Technology.

• Price-Gap Approach.

Subsidies Calculated

• Institutional Limitations.

• Lack of Rigorous Surveys.

• Opaque and Contradictory Accounting Data.

Therefore,

• Used Data from Governments, Companies,

NGOs, Investment Houses, Industry

Associations.

• Cross-checked and Discarded Data.

Data Problems & Solutions

• Steel is Pillar Industry with limited Foreign Investment Limited,

till now.

• In 2015, China is Largest Producer and Consumer of Steel with

about 50% of Production, Up from 16% in 1999.

• In 2005, China went from Net Steel Importer to Steel Exporter;

in 2006, China became the Largest Steel Exporter; in 2007,

China became the Largest Steel Producer

• Steel-making Capacity more than Doubled from 2005 to 2012

and is Continuing to Grow.

• From 2000 to 2006, Energy Subsidies grew by 1365%.

• Total Energy Subsidies from 2000 to mid 2007 were $27.11

billion.

China’s Steely Resolve

Highly Fragmented Steel Industry

Hebei Jiangsu Liaoning Shandong Shanghai Tianjin

Hubei Guangdong Shanxi Henan Sichuan Anhui

Jiangxi Beijing Hunan Nei Monggul Fujian Zhejiang

Guanxi Yunnan Jilin Gansu Shaanxi Xinjiang

Chongqing Heilongjiang Guizhou Qinghai Hainan Ningxia

Energy Subsidies to Chinese Steel

-2.000.000.000

-1.000.000.000

0

1.000.000.000

2.000.000.000

3.000.000.000

4.000.000.000

5.000.000.000

6.000.000.000

7.000.000.000

8.000.000.000

9.000.000.000

2000 2001 2002 2003 2004 2005 2006 2007 mid-year

Do

lla

rs

Year

Coking Coal Thermal Coal Electricity Natural Gas Total

Annual Percentage Growth of Chinese

Energy Subsidies, Steel Production & Steel

Exports

-500%

0%

500%

1000%

1500%

2000%

2500%

3000%

3500%

4000%

4500%

2000 2001 2002 2003 2004 2005 2006 2007EAn

nu

al

Pe

rce

nta

ge

Gro

wth

fro

m 2

00

0

Year

Subsidies Global Exports Production Exports to US

• In 2013, subsidies accounted for 47% of listed Chinese

steel companies’ total profits.

• In the first half of 2014, 2235 Chinese listed companies

(88%) received government subsidies totaling $5.24

billion.

• In 2014, subsidies accounted for 80% of listed Chinese

steel companies’ profits.

• In 2014, 20% of China’s 33 listed steel mills received

subsides accounting for more than half their profits.

• Yet, from 2013 to 2014, the Chinese steel sector’s profit

margin halved to 0.3%.

Continuing Subsidies to Chinese

Steel

Production Capacity in the

Chinese Steel Sector

• In 1958, Mao saw steel as one of two economic

development pillars and called for a furnace in every

backyard.

• Steel remains the prime beneficiary of bank lending and

stimulus packages, fueling enormous excess capacity.

• In 2014, steel-making capacity was 1.2 billion tons or 14

times annual US steel output.

• From 2008-2014, Chinese mills added 540 million tons

of steelmaking capacity, now 1.2 billion tons.

• Currently, Beijing has asked for cuts of 80 million tons

cuts of production, 7% of national capacity.

• Massive Excess Capacity in China with Supply Exceeding

Demand on Average by 20% Every Year.

• Annual New Capacity added in China is More than Total Output

of Japan, Second Largest Steel Producer.

• From 2000 to present, the USA has had Trade Deficit with China

on Steel for Every Year (except 2003).

• In 2012, the US Trade Deficit was 142% greater than in 2000

• Chinese Steel Costs between 20% to 30% less than US or EU

Steel, Depressing Prices Worldwide.

• From 2009, the US, EU, and now Latin America have Filed Trade

Complaints and Slapped Tariffs against China.

Some Effects

• China produces 6 times more steel than Latin

America.

• In the last 5 years, Chinese imports into Latin

America have grown from 6% to 13%.

• Latin America is the second most important

export destination for Chinese steel.

• Strikes, plant closures, redundancies and

cancelled investments currently pervade the

Latin American steel sector.

China and Latin America

Chinese Exports to South AmericaMillions of Tons

-100

-50

0

50

100

150

200

250

0

1

2

3

4

5

6

7

8

Chinese Exports

Percent YoY Change

Steel Declines

From January-September 2015

• China’s crude steel output fell 2% to 609

million tonnes.

• China’s apparent consumption of crude

steel fell 5.8% Y-o-Y.

• CISA: “The decline in output is still not

enough compared with the shrinkage in

demand.”

Chinese Supply-Demand Imbalance

“The Chinese are dumping in our core markets.

The question is how long the Chinese will

continue to export below their cost.”

Lakshmi Mittal

CEO, ArcelorMittal

November 6, 2015

Chinese Export Prices

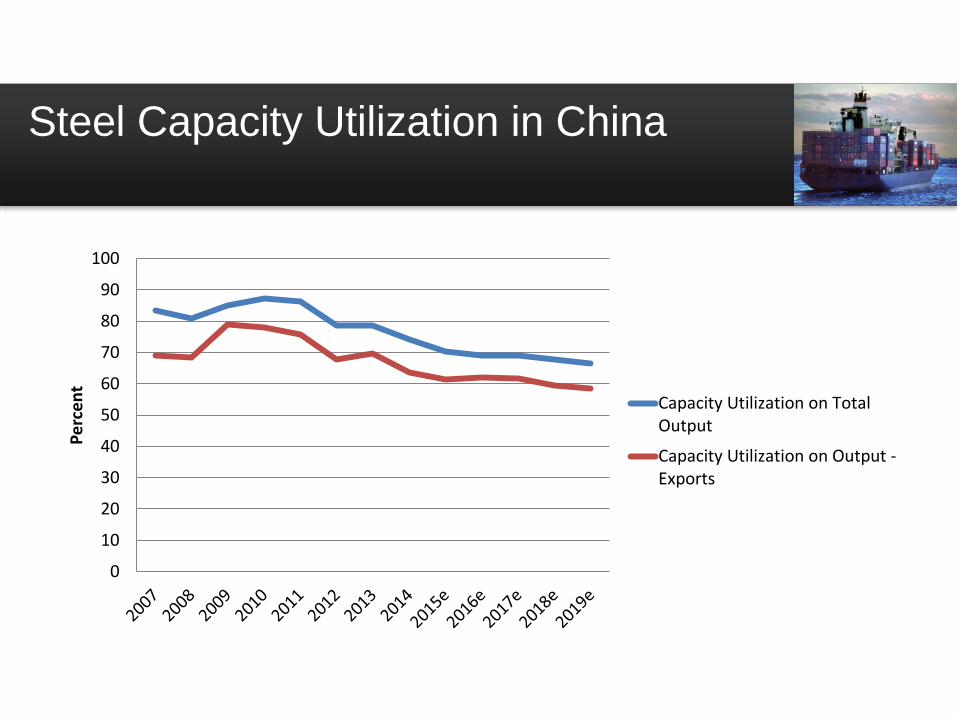

Steel Capacity Utilization in China

0

10

20

30

40

50

60

70

80

90

100

Percent

Capacity Utilization on TotalOutput

Capacity Utilization on Output -Exports

NME Methodology

• China’s “Protocol of Accession” allowed WTO

members to use external benchmarks (e.g.

surrogate firm’s costs in another country).

• NME results in higher antidumping duties (about

40%) than if China were treated as market

economy (about 10%).

• China argues that provisions of WTO accession

require that all members treat China as market

economy on December 11, 2016.

• US and EU disagree as only one provision is

expiring and the onus is on China.

Do Markets Set Prices in

China?

• When subsidies, negative externalities and

monopolies exist, then markets fail.

• China has used extensive subsidies of

energy, raw materials, land, and the cost

of capital, to support production and

exports in a wide range of industries

including steel, paper, glass, solar PV and

auto parts.

Do Markets Set Prices in China

- 2?

• The Chinese central government has maintained

extensive economic controls through 72 detailed

five-year plans and 22 national industrial-sector

plans.

• Provincial and local governments are heavily

involved in implementing national plans as well

as their local plans.

• PBOC interventions have subsidized China’s

exports.

Antidumping against China

• In 2014, the EU had 54 anti-dumping and anti-subsidy

orders against China, three-fifths of the total.

• In September 2015, the US had 129 anti-dumping and

countervailing duty orders against China, more than any

other country, 40% of the total.

• In 2013 and the first two months of 2014, US steel

producers filed more than 40 anti-dumping and

countervailing duty cases including against China.

• In September 2015, Latin America filed 27 anti-dumping

resolutions against China.

13th Five-Year Plan

• Double China’s real economy by 2020 compared to 2010

goals (GDP growth of 6.5% though not specified).

• Enforce climate targets to reduce coal usage which

would hit the steel sector.

• Provide stimulus for education, healthcare and

environmental protection.

• Seek innovative ways to make steel more efficient.

• Push steel factories overseas.

• Encourage foreign investors to take stakes in a sector

mostly off-limits to them.

Planned Steel Restructuring

• Quicken construction and trial runs of corporate

databank system.

• Increase cooperation among downstream and upstream

steel sectors including electric, shipbuilding and ocean-

engineering steel.

• Promote global marketing of high-quality steel.

• Conduct research in steel structures, urban plant

relocation, steelmaking with IF furnaces, steel exports,

and iron-ore supply security.

• Promote capacity reduction, mergers and acquisitions,

innovation, green development, enterprises going out

and curbing disorderly competition in steel industry.

Conflicting Official Messages

• PBOC routinely surprises markets with major

policy announcements on evenings and

weekends.

• In June, China Securities Regulatory

Commission outlined sweeping plans for private

companies to raise money by going public.

But,

• A week later, the agency banned new listings,

barred big share holders from selling and

ordered brokerages to buy aggressively.

Conflicting Official Messages -

2

• In October 2014, Finance Minister Lou announced plans

to clean up trillions of dollars of local government debt.

But,

• In November 2015, Prime Minister Li met with China’s

biggest banks and promised to subsidize companies in

financial trouble, including through capital.

• In October 2015, the government released a policy

document to overhaul SOEs.

But,

• A few days later, the CPC’s Central Committee ruled out

loosening the party’s grip on SOEs.

Challenges for Global

Companies

• Price: 25% fall in prices making steel cheapest

in a decade.

• Chinese Exports: Rose more than 50% in 2014

to 93 million tonnes; expected to rise to 100

million tonnes in 2015.

• Margins: Contracted as prices started falling

faster than raw materials.

• Product Mix: Companies with higher-value steel

in small volumes better off than lower grade and

commoditized steel.

Chinese Iron Ore Imports by Source

Changes in China’s Iron Ore Demand

Choppy Waters.

Questions?

Usha C. V. Haley

http://usha.tel

© Usha C. V. Haley, All rights reserved

Your Logo