25

Steven Priest Chamberlains SBR, Chartered Accountants Wagga / Dubbo / Shepparton Members Voluntary Liquidations

| Date post: | 24-Dec-2015 |

| Category: |

Documents |

| Upload: | alberta-burke |

| View: | 229 times |

| Download: | 0 times |

Steven PriestChamberlains SBR, Chartered

AccountantsWagga / Dubbo / Shepparton

Members Voluntary Liquidations

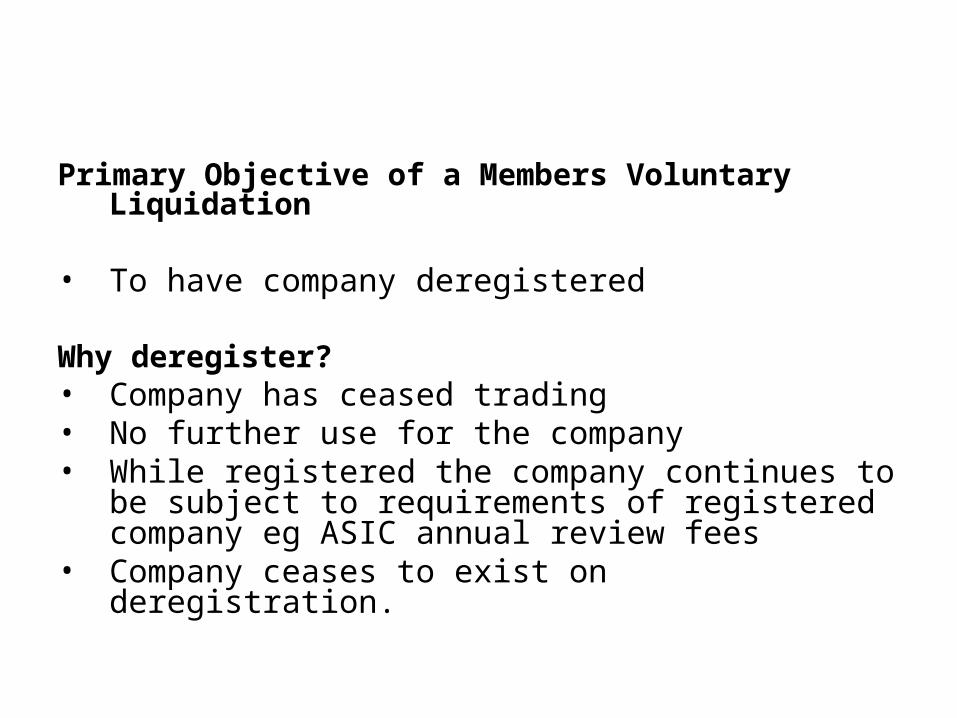

Primary Objective of a Members Voluntary Liquidation

• To have company deregistered

Why deregister?• Company has ceased trading• No further use for the company• While registered the company continues to be

subject to requirements of registered company eg ASIC annual review fees

• Company ceases to exist on deregistration.

How do we deregister a company?

Two ways in which it can be achieved: -

• Application to ASIC to have company deregistered (must meet certain legal requirements)

• Members Voluntary Liquidation

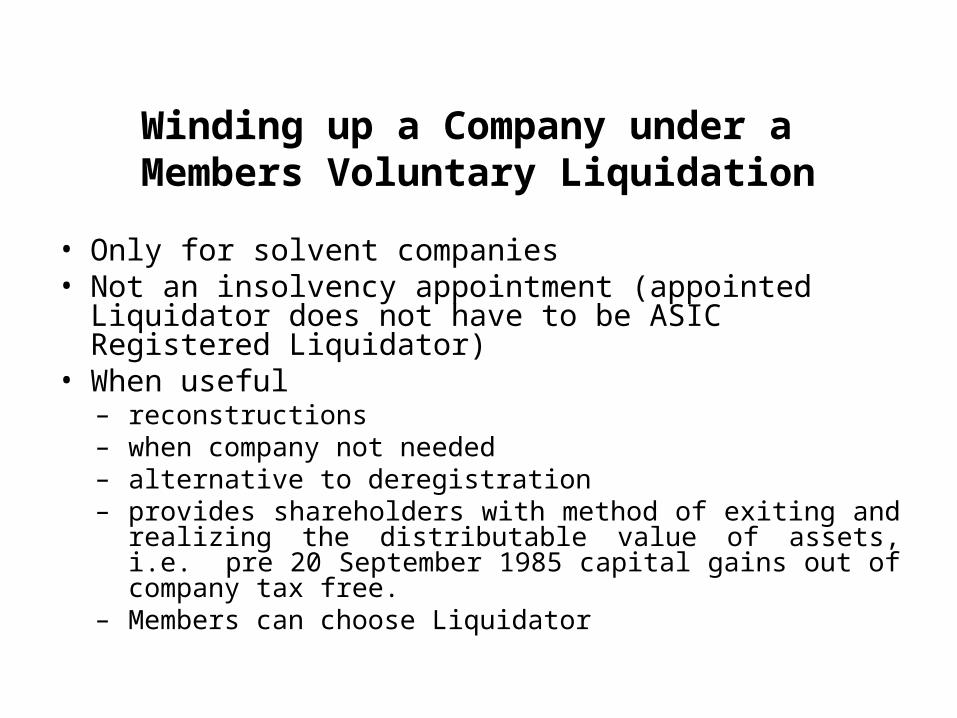

Winding up a Company under a Members Voluntary Liquidation

• Only for solvent companies• Not an insolvency appointment (appointed Liquidator

does not have to be ASIC Registered Liquidator)• When useful

– reconstructions– when company not needed– alternative to deregistration– provides shareholders with method of exiting and realizing

the distributable value of assets, i.e. pre 20 September 1985 capital gains out of company tax free.

– Members can choose Liquidator

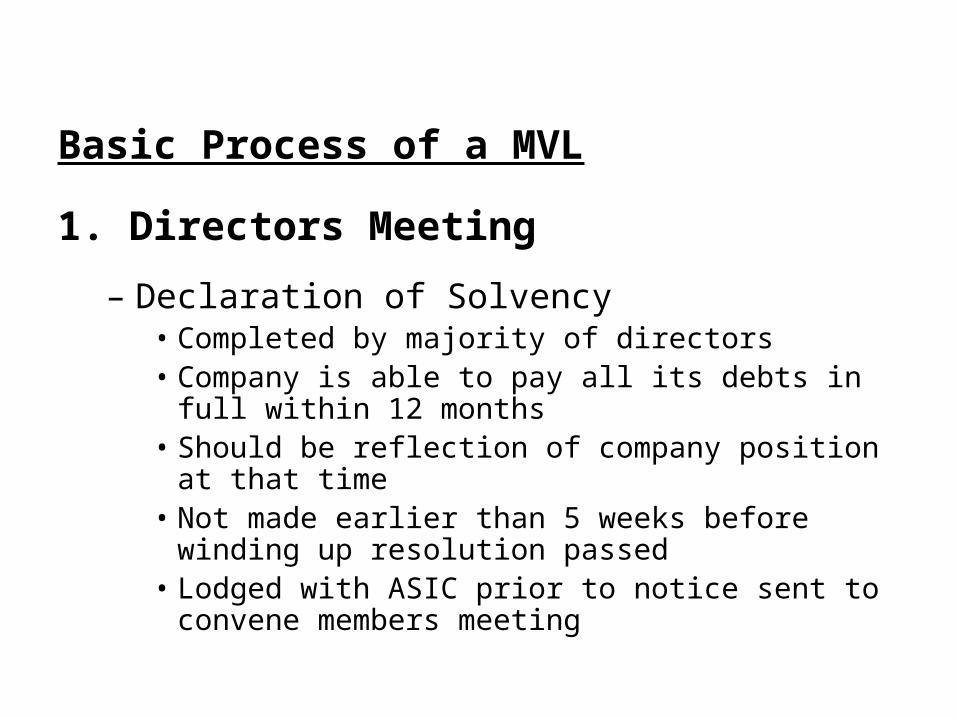

Basic Process of a MVL

1. Directors Meeting

– Declaration of Solvency• Completed by majority of directors• Company is able to pay all its debts in full within 12

months• Should be reflection of company position at that time • Not made earlier than 5 weeks before winding up

resolution passed• Lodged with ASIC prior to notice sent to convene

members meeting

2. Members Meeting

– 21 days notice for proprietary company (ability to hold earlier)

– Must pass special resolution to wind up company (75% in favour)

– Pass ordinary resolutions• Appointment of Liquidator(s)• Fixed Liquidator(s) remuneration• Destruction of Books & Records• How distribution of surplus assets are to occur

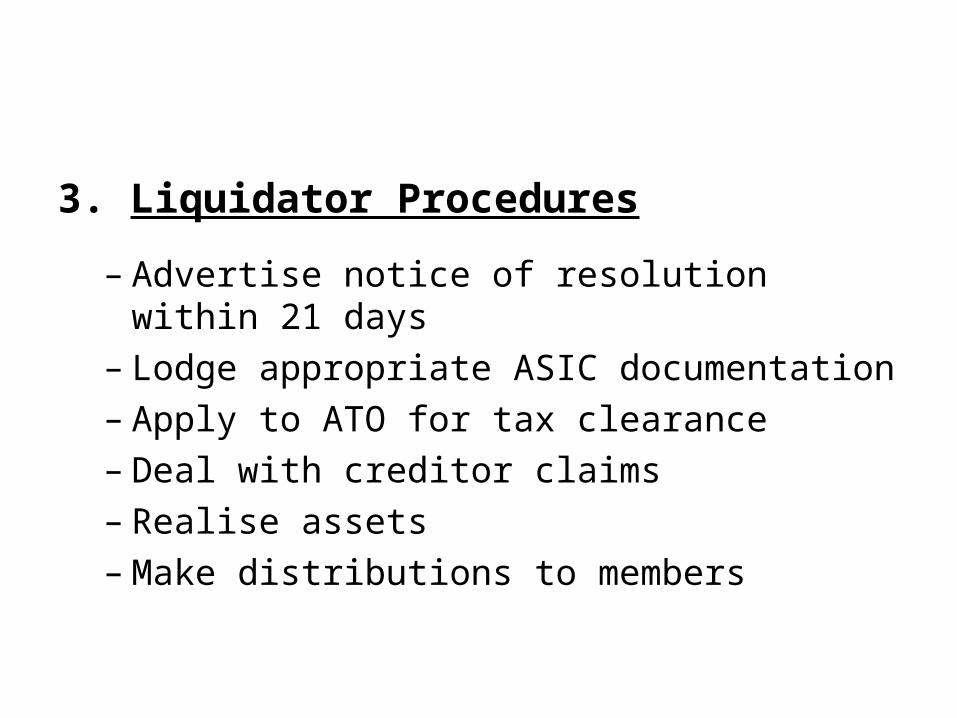

3. Liquidator Procedures

– Advertise notice of resolution within 21 days– Lodge appropriate ASIC documentation – Apply to ATO for tax clearance– Deal with creditor claims– Realise assets– Make distributions to members

Liquidator Procedures (continued)– Convene final meeting of members, lodge final

ASIC document

– Company will be deregistered 3 months from final meeting

– If at any time liquidator forms opinion company not able to pay its debts within 12 months

• Apply to Court

• Appoint voluntary administrator

• Convene meeting of creditors to proceed with CVL

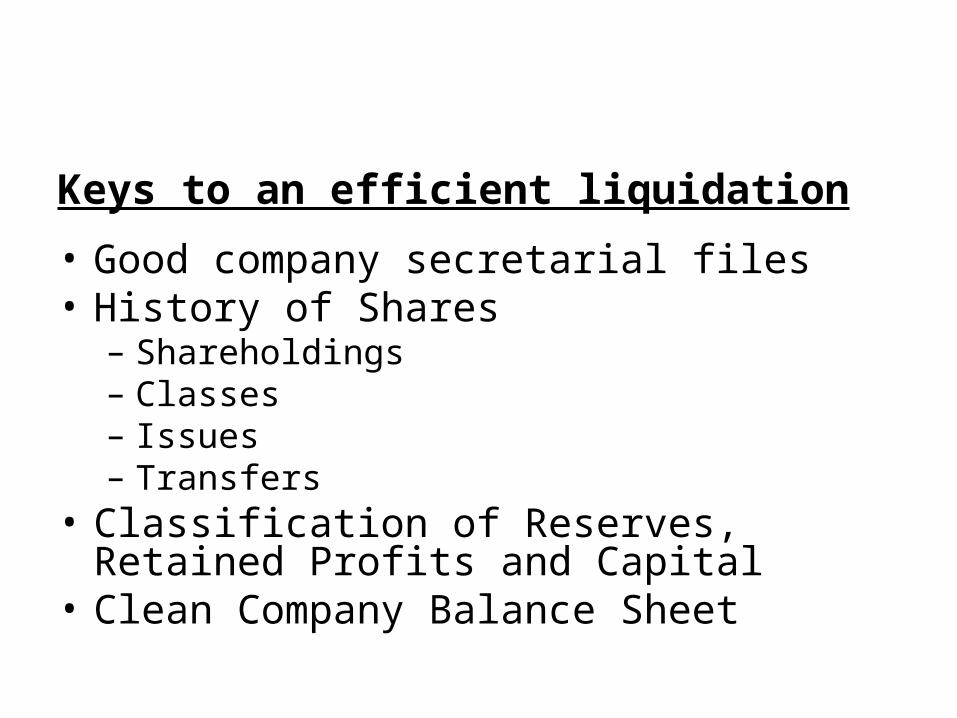

Keys to an efficient liquidation

• Good company secretarial files• History of Shares

– Shareholdings– Classes– Issues– Transfers

• Classification of Reserves, Retained Profits and Capital

• Clean Company Balance Sheet

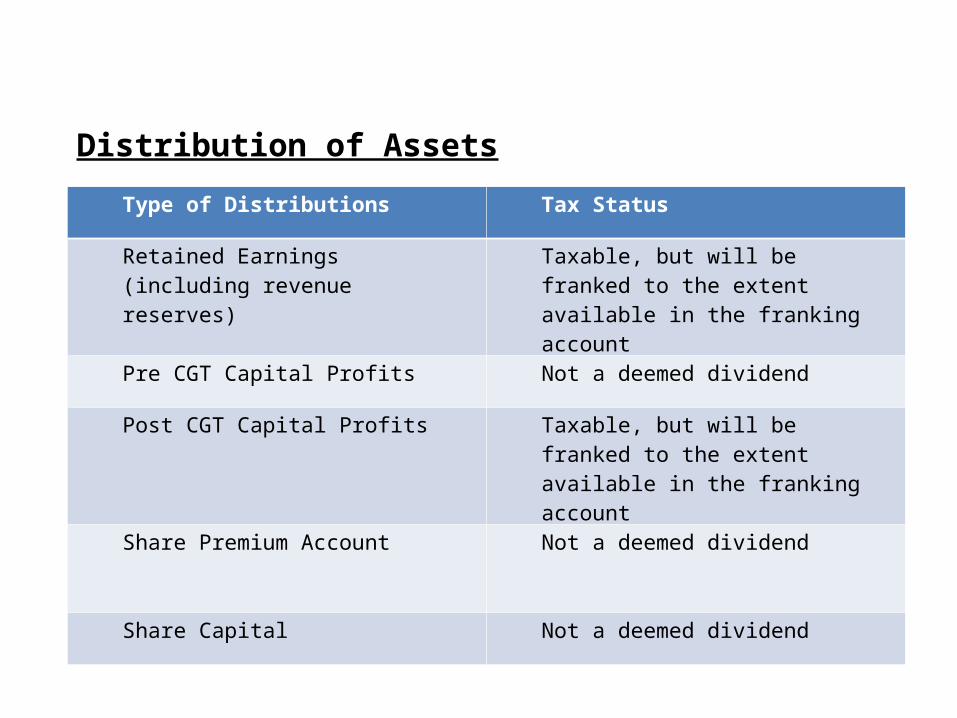

Type of Distributions Tax Status

Retained Earnings (including revenue reserves)

Taxable, but will be franked to the extent available in the franking account

Pre CGT Capital Profits Not a deemed dividend

Post CGT Capital Profits Taxable, but will be franked to the extent available in the franking account

Share Premium Account Not a deemed dividend

Share Capital Not a deemed dividend

Distribution of Assets

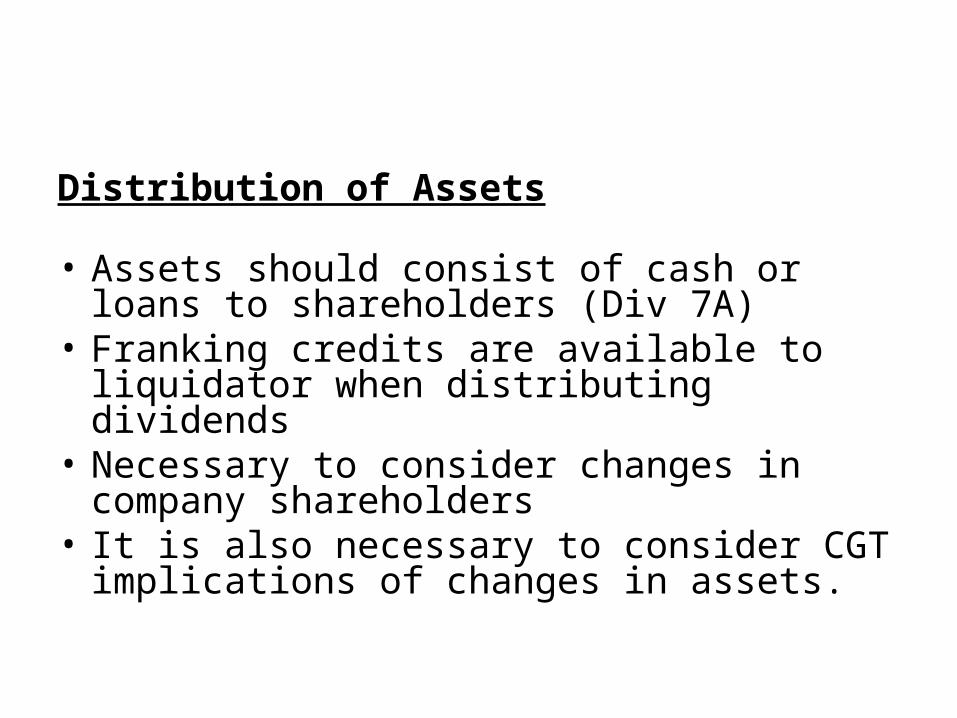

Distribution of Assets

• Assets should consist of cash or loans to shareholders (Div 7A)

• Franking credits are available to liquidator when distributing dividends

• Necessary to consider changes in company shareholders

• It is also necessary to consider CGT implications of changes in assets.

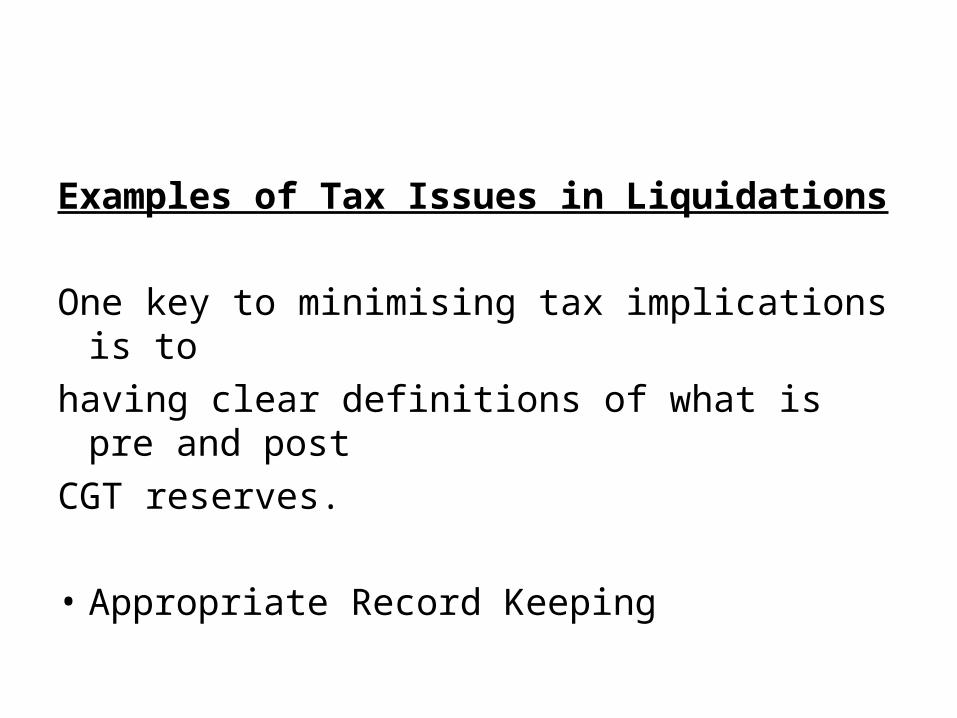

Examples of Tax Issues in Liquidations One key to minimising tax implications is tohaving clear definitions of what is pre and postCGT reserves.

• Appropriate Record Keeping

Example 1• Peter and Phil acquired all shares in Fine Flowers Pty Ltd in

January 1985 for $120,000. On 1 July 2009 both Peter & Phil decide to place the company into liquidation.

• Other factors– Paid up capital was $100,000– Pre CGT asset was sold in 1997 for a capital profit of $50,000 – In 1999 the company sold for $150,000 an asset acquired 14

months earlier for $90,000– In 1999 the company incurred a capital loss of $20,000 on the

sale of a post CGT asset– Accumulated profits total $140,000

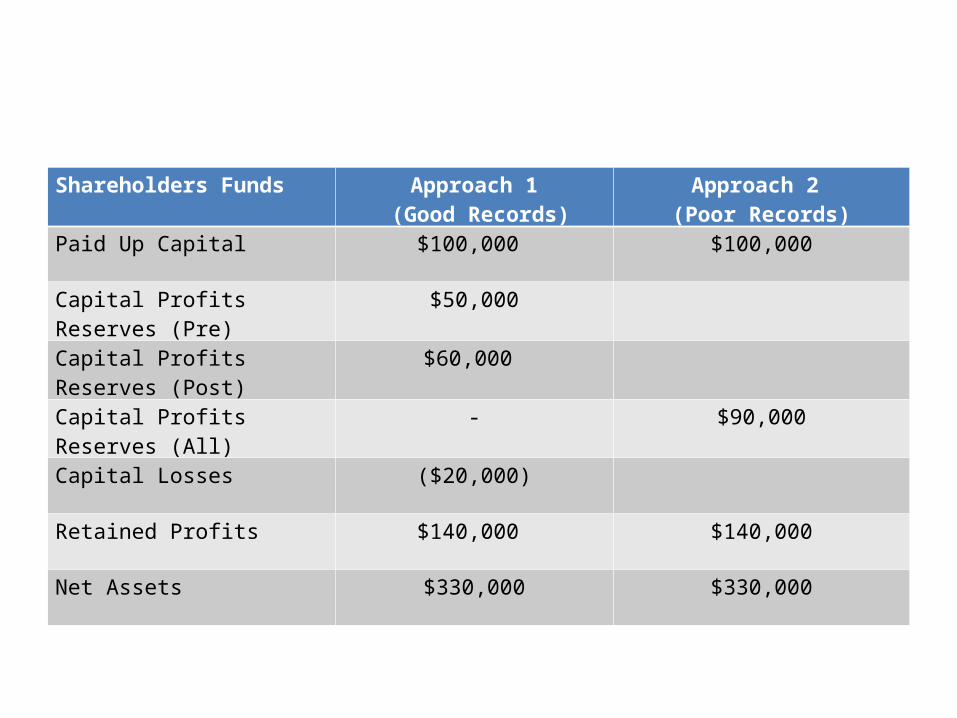

Shareholders Funds Approach 1 (Good Records)

Approach 2 (Poor Records)

Paid Up Capital $100,000 $100,000

Capital Profits Reserves (Pre)

$50,000

Capital Profits Reserves (Post)

$60,000

Capital Profits Reserves (All) - $90,000

Capital Losses ($20,000)

Retained Profits $140,000 $140,000

Net Assets $330,000 $330,000

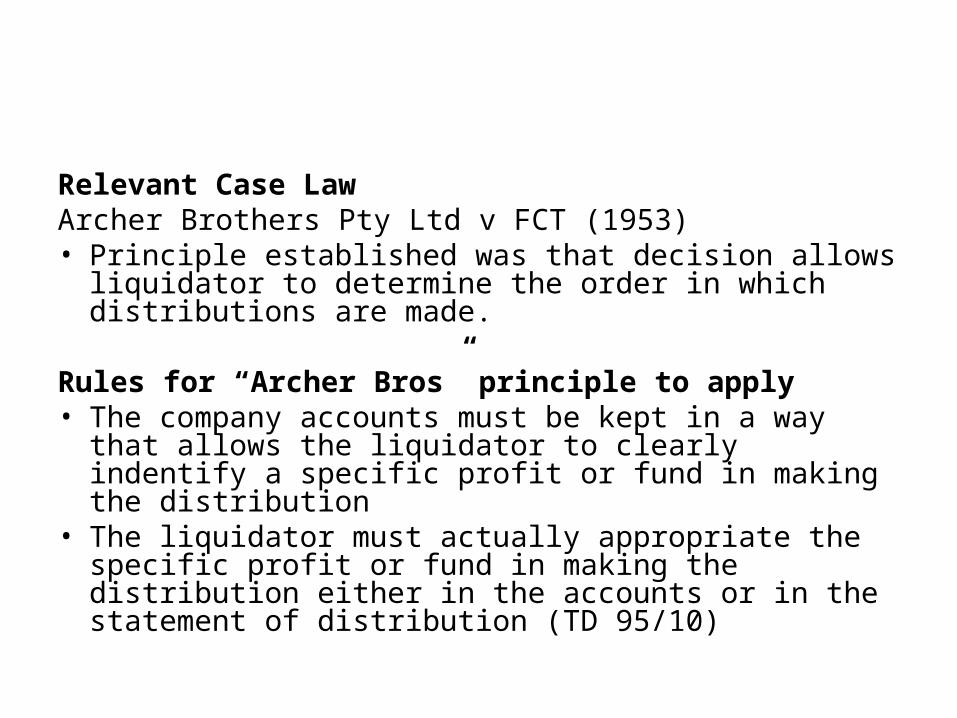

Relevant Case Law Archer Brothers Pty Ltd v FCT (1953)• Principle established was that decision allows liquidator to

determine the order in which distributions are made. Rules for “Archer Bros” principle to apply• The company accounts must be kept in a way that allows

the liquidator to clearly indentify a specific profit or fund in making the distribution

• The liquidator must actually appropriate the specific profit or fund in making the distribution either in the accounts or in the statement of distribution (TD 95/10)

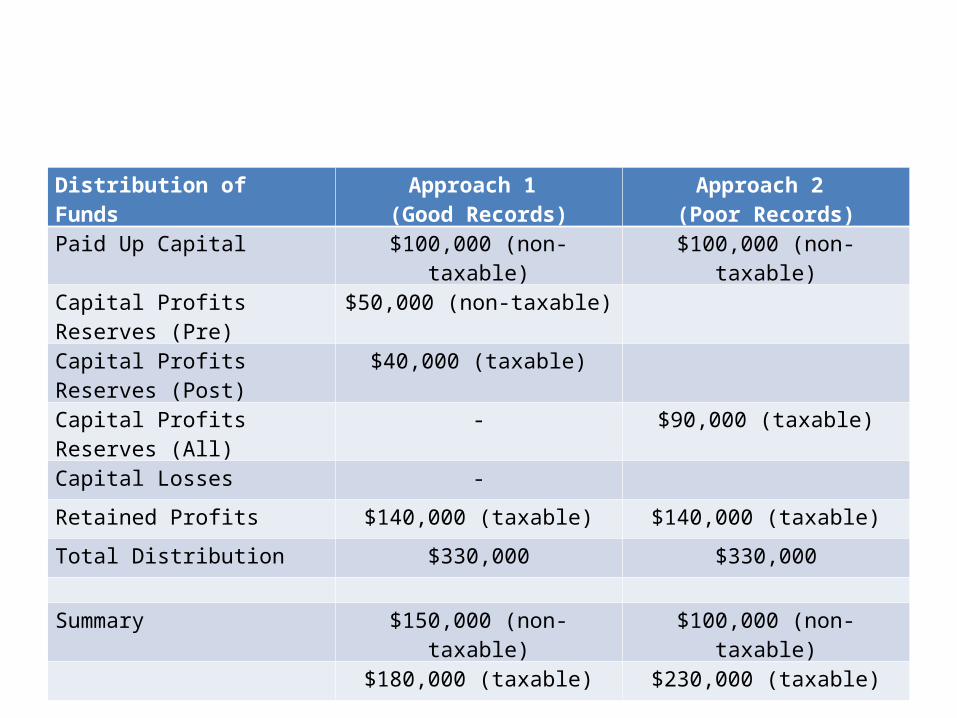

Distribution of Funds Approach 1 (Good Records)

Approach 2 (Poor Records)

Paid Up Capital $100,000 (non-taxable) $100,000 (non-taxable)

Capital Profits Reserves (Pre)

$50,000 (non-taxable)

Capital Profits Reserves (Post)

$40,000 (taxable)

Capital Profits Reserves (All) - $90,000 (taxable)

Capital Losses -

Retained Profits $140,000 (taxable) $140,000 (taxable)

Total Distribution $330,000 $330,000

Summary $150,000 (non-taxable) $100,000 (non-taxable)

$180,000 (taxable) $230,000 (taxable)

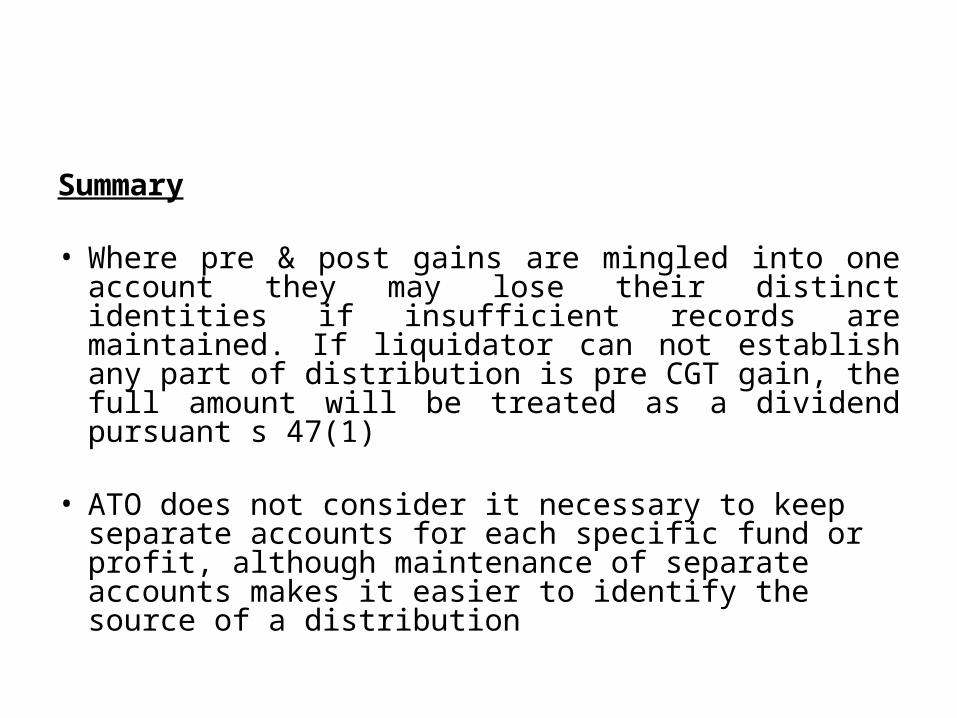

Summary

• Where pre & post gains are mingled into one account they may lose their distinct identities if insufficient records are maintained. If liquidator can not establish any part of distribution is pre CGT gain, the full amount will be treated as a dividend pursuant s 47(1)

• ATO does not consider it necessary to keep separate accounts for each specific fund or profit, although maintenance of separate accounts makes it easier to identify the source of a distribution

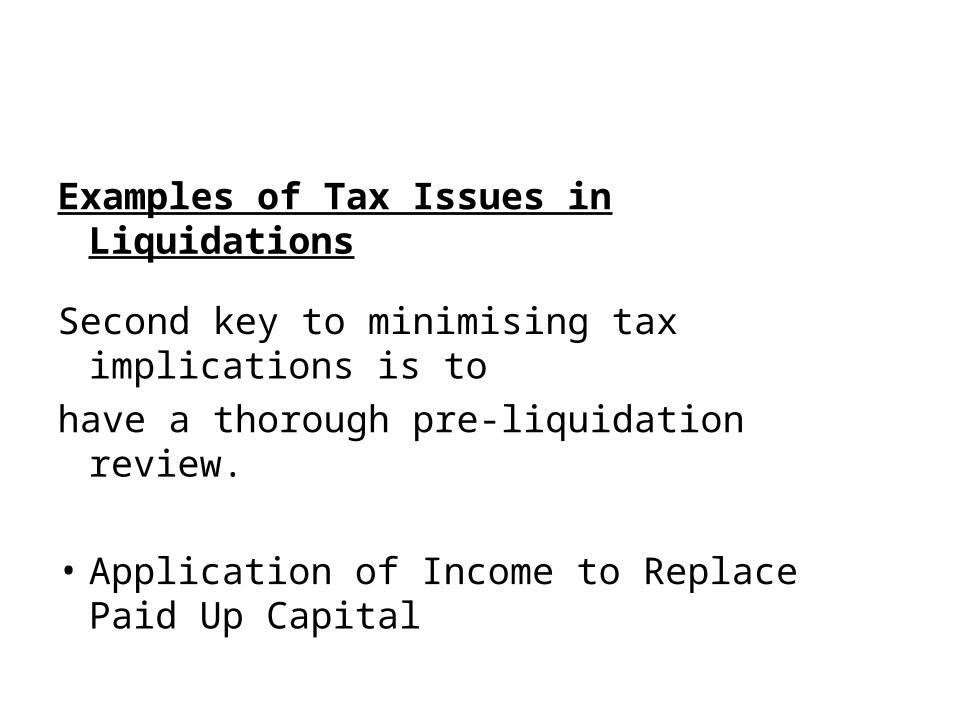

Examples of Tax Issues in Liquidations

Second key to minimising tax implications is tohave a thorough pre-liquidation review.

• Application of Income to Replace Paid Up Capital

AssetsCash on Hand 100

Equity

Paid Up Capital 150

Accumulated Losses (100)

Capital Profit Reserve 50

Total 100

Example 2

Can it be assumed the $100 could be distributed as Paid Up Capital? No

The Courts and the Tax Commissioner consider the accumulated losses have diminished the paid up capital

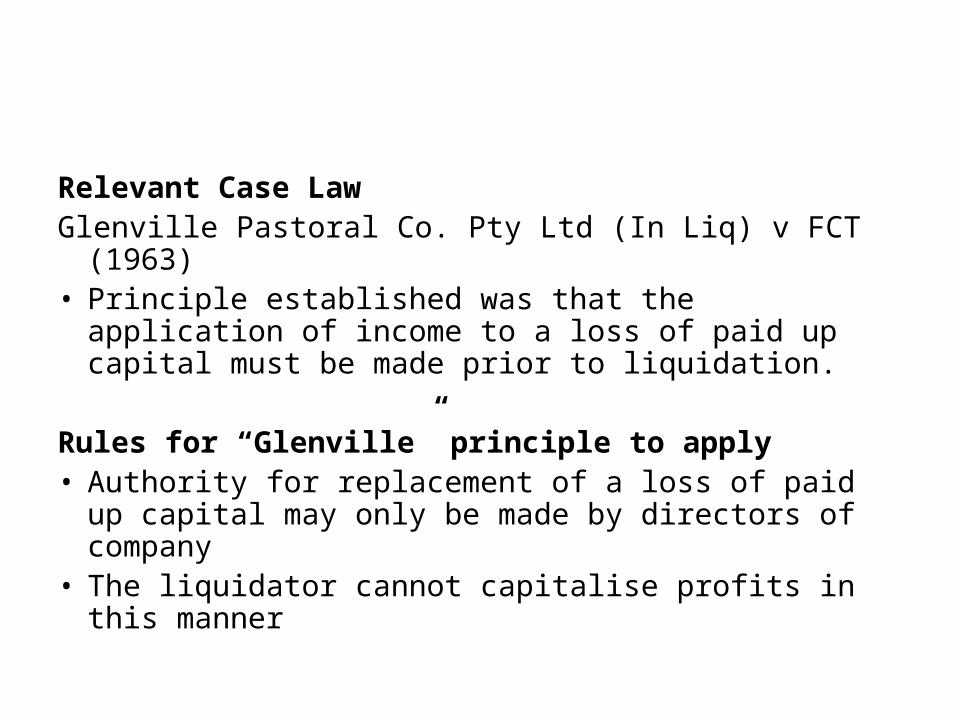

Relevant Case LawGlenville Pastoral Co. Pty Ltd (In Liq) v FCT (1963)• Principle established was that the application of

income to a loss of paid up capital must be made prior to liquidation.

Rules for “Glenville” principle to apply• Authority for replacement of a loss of paid up capital

may only be made by directors of company • The liquidator cannot capitalise profits in this manner

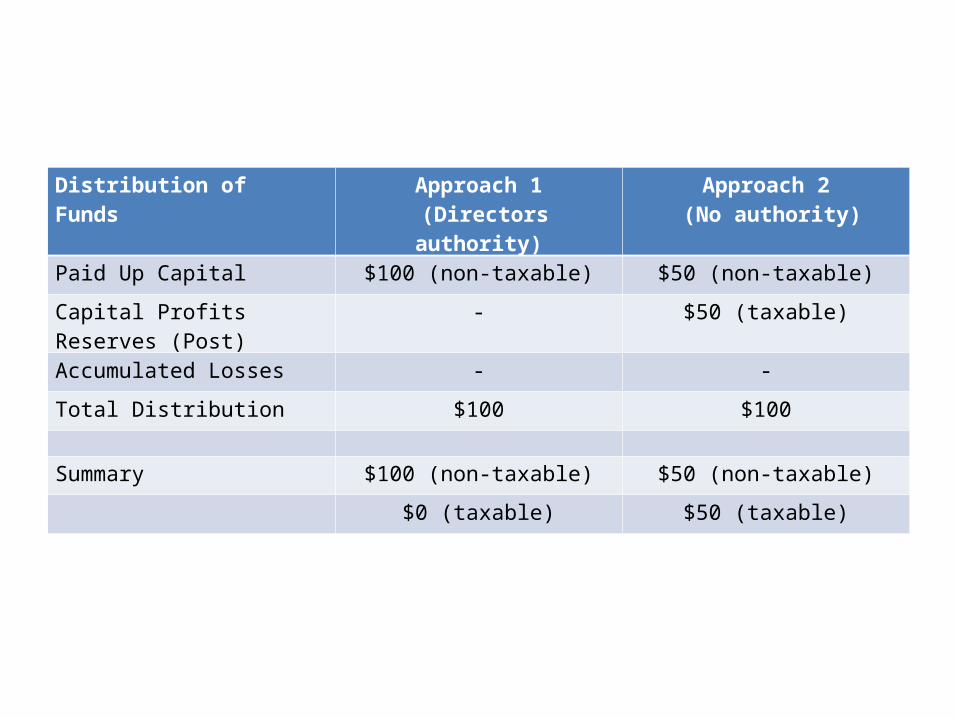

Distribution of Funds Approach 1 (Directors authority)

Approach 2 (No authority)

Paid Up Capital $100 (non-taxable) $50 (non-taxable)

Capital Profits Reserves (Post)

- $50 (taxable)

Accumulated Losses - -

Total Distribution $100 $100

Summary $100 (non-taxable) $50 (non-taxable)

$0 (taxable) $50 (taxable)

Summary

• To avoid this issue prior to liquidation the directors should pass a resolution in regard to application of income to replace paid up capital.

Options when errors are made?• Failing to identify a liability

– During Liquidation• Sufficient assets liquidator can pay• Insufficient assets

– parent make good– place into CVL

– After final distribution• Creditor claim extinguished• No sustainable claim without leave of court

Options when errors are made?

• Fail to identify an asset– During Liquidation

• Liquidator sell & distribute • Remove company from liquidation

– After final distribution• Application to reinstate company• ASIC may execute transfer documents

Options when errors are made?

• Fail to identify tax issues– During liquidation

• Shareholders exposed to payment of tax• Finalisation of liquidation will take additional time