Stewart Investors Sustainable Funds Quarterly Client Update: Fourth Quarter 2015 1 October – 31 December 2015 For professional clients only Investment philosophy Since 1988 we have had an approach to investment founded on: – Stewardship – An absolute return mindset – Bottom-up analysis – Long-term thinking – Searching for quality companies – Finding sustainable and predictable growth – Strong valuation disciplines Investment objective To generate attractive long-term, risk-adjusted returns by investing in the shares of those companies which we believe are particularly well positioned to benefit from, and contribute to, the sustainable development of the countries in which they operate.

Transcript

Stewart Investors Sustainable FundsQuarterly Client Update: Fourth Quarter 20151 October – 31 December 2015

For professional clients only

Investment philosophySince 1988 we have had an approach to investment founded on:– Stewardship– An absolute return mindset– Bottom-up analysis– Long-term thinking– Searching for quality companies– Finding sustainable and

predictable growth– Strong valuation disciplines

Investment objectiveTo generate attractive long-term, risk-adjusted returns by investing in the shares of those companies which we believe are particularly well positioned to benefit from, and contribute to, the sustainable development of the countries in which they operate.

02

Sustainable FundsQ

uarterly Client U

pdate: Fourth Quarter 2015

Even as bottom-up investors, we still find benefit in exploring investment themes as they relate to sustainable development and which have potential implications for the companies in which we invest on our clients’ behalf. As part of our ongoing research and engagement process, we have created a list of issues to explore, ranging from the challenges presented by the rise of megacities to the opportunities and implications of the sharing economy, which you may have read about in our last quarterly report. This quarter, we have been working on deepening our understanding of the challenges companies face in sourcing sustainable palm oil.

Palm Oil In recent months, we have seen many photos in the news of forests burning across Malaysia and Indonesia, creating a haze over many parts of Southeast Asia. Driving these fires is the production of palm oil, one of the most widely used vegetable oils in the world. Palm oil has a high resistance to oxidation and consequently a long shelf life, making it an ideal ingredient for a variety of products from detergents to baked goods. It can now be found in half of all products in a supermarket. It also produces higher yields per hectare of land compared to other oils, such as rapeseed, sunflower and soy. It has become a major source of income for local communities and forms an important part of the rural economy in many countries where it grows. However, the rising demand for the popular oil has led to large-scale conversion of natural forest areas for plantations, resulting in carbon dioxide emissions, loss of high conservation value forests, soil erosion, air pollution, loss of biodiversity, as well as social conflict.

In an effort to address some of these challenges and promote the use of sustainable palm oil through credible global standards, The Roundtable for Sustainable Palm Oil (RSPO) was established in 2004. There are four types of RSPO certified palm oil, and unfortunately the most common types, GreenPalm and Mass Balance, are not completely deforestation free. The complete separation of certified and non-certified palm oil is expensive and difficult to achieve. Mass Balance is a cost-effective mixture of certified sustainable palm oil and non-certified palm oil. GreenPalm is an offset programme that allows manufacturers and retailers to buy GreenPalm certificates from an RSPO certified palm oil grower to offset each tonne of palm oil they purchase. The remaining two types of RSPO palm oil are Segregated and Identity Preserved, which ensure higher levels of traceability and physical separation of certified and non-certified palm oil. However, these are more expensive and not currently available in the quantities many large consumer companies require. Many companies have decided to require RSPO certification as a minimum requirement but are increasingly finding ways to build on RSPO criteria by directly working with their suppliers to ensure additional protection against forest loss and degradation and social conflict.

Commentary

Contents

02Commentary

04Significant portfolio changes

06Proxy voting

06Engagement

07Business update

09Trip report: Bangladesh

13Fund information

03

Sustainable FundsQ

uarterly Client U

pdate: Fourth Quarter 2015

An encouraging number of companies have made commitments to source sustainable palm oil. However, putting these goals into action can be an arduous task, as the palm oil supply chain is vast, complex and relies heavily on small processors and farmers whose palm oil is difficult to trace. Unilever, one of the world’s largest buyers of palm oil, is currently working to source all of their palm oil from traceable and certified sources by 2020. To achieve this target, they’ve started using a tool called Known Sources that allows them to gather information about their suppliers and ensure compliance with their Supplier Code. As of 2014, they achieved 70% traceability to known mills and have visibility of over 1,800 crude palm oil mills. Henkel, another consumer company has decided to phase out GreenPalm certificates and are working directly with their suppliers to ensure that they are at minimum Mass Balance certified. Both Unilever and Henkel are companies in which we invest.

Our approach to engagement is one that is always based on encouraging companies to protect long-term shareholder value. The forest fires in Indonesia continue to heighten the focus on deforestation and the multinational consumer goods companies purchasing palm oil are an easy target for concerned stakeholders.

However, large volumes of palm oil are also purchased by emerging markets consumer companies. The engagement with these companies can be a little more challenging because consumers are less engaged and NGOs less influential. However, we see this gradually starting to change. While not targeting palm oil, Singapore supermarket operators, including Sheng Siong held in some of our Asia strategies, stopped sourcing paper products from listed company Asia Pulp & Paper due to concerns around their green credentials in light of the Indonesian forest fires. We believe this may be a sign of things to come from a more environmentally engaged Asian community.

We are convinced that companies that choose to strengthen their supply chains will minimise risk and will be better placed over the long run to deliver improved shareholder value.

Commentary (cont)

04

Sustainable FundsQ

uarterly Client U

pdate: Fourth Quarter 2015

WorldwideDuring the quarter we did not initiate any new positions for the Worldwide strategy. Instead, we added to Dr Reddy’s (and also for Global Emerging Markets, Asia and India strategies) following share price weakness due to operational issues which, we feel confident it will overcome in due course.

We added to Draegerwerk after recent market overreaction to short-term results, Ansys following a meeting in Edinburgh, as well as SGS, a testing company which we feel offers a low risk means of gaining exposure to an out of favour resources sector. In order to manage cash, we also added to existing positions in a number of holdings including Henkel, Unicharm, Varian, Merck KGaA and Kansai Paint.

We sold out of Burckhardt Compression, a wonderfully-run Swiss company whose machines make lots of industrial processes more efficient, but which we feel on balance is poorly positioned for a lower carbon future given its exposure to the oil and gas sector. We also sold out of United Natural Foods – recent setbacks have forced us to conclude that the quality of franchise may not be sufficient to meet our criteria. We also reduced our holding in Chubb Corp following their takeover by ACE, in Lenzing following a sharp cyclical recovery in the shareprice, and in Ain Pharmaciez on valuations.

Emerging MarketsIn our Emerging Markets strategy we added to two of our favourite Brazilian companies that have fallen out of favour due to the recent political and economic turmoil. The first, WEG, is a global leader in electric motors with superb sustainability tailwinds and conservative family governance. The second, Banco Bradesco, as it remains a conservative financer, an Equator Principles pioneer and – under the stewardship of its Chairman who has, amazingly, been with the bank since the early 1940s – has ample institutional memory of macroeconomic turmoil and knows how to navigate it. We also added to Standard Bank in South Africa on compelling values when it collapsed 17% in USD over one day when the Finance Minister was replaced.

We sold out of Tiger Brands Consumer Goods, rectifying a mistake and recognising that a turnaround there may not be possible now. We also sold the residual of Axiata (also sold from the Asian strategy) following a dividend reinvestment. We reduced positions in Guaranty Trust Bank, as it remains a risky bank and has held up well in local currency. We also reduced SulAmerica, following a sharp re-rating and concerns about unemployment in Brazil; XL Axiata (also trimmed in the Asian strategy), following a bounce and recognising that this is not the strongest of franchises; and Jeronimo Martins, as future growth rate and expansion in Poland slows.

AsiaIn Asia we added to Dialog Axiata as it remains acceptably valued, and Giant Manufacturing and Commerical Bank of Ceylon as valuations became more palatable.

We sold out of Globe Telecom over competition concerns as a third operator has now entered the market, and trimmed Singapore Post as we lack confidence in management to successfully turn the business around.

Significant portfolio changes

Market capUSD 427m

Shareholders sinceJuly 2015

Sustainability classificationResponsible finance

Company descriptionA responsible finance institution with a strong sense of purpose that is committed to delivering steady profitable growth and assisting to build a democratic and poverty-free Bangladesh.

Investment rationaleBased in Bangladesh and founded to provide banking services to the large number of unbanked people that were not covered by traditional banks in Bangladesh. It is ~45% owned by the NGO BRAC – an international, non-government development organisation that is focused on eradicating poverty. The bank provides services to SMEs and microfinance organisations and its profits fund the NGO. Image source SI Team, November 2015

05

Sustainable FundsQ

uarterly Client U

pdate: Fourth Quarter 2015

IndiaIn India we initiated positions in Square Pharma, C T Holdings PLC and S H Kelkar & Co Limited.

Square Pharma is a leading generic pharma from Bangladesh that is currently trying to spread its wings overseas. Their global aspirations are encouraging; they have a wonderful track record and an evolving governance structure with the founding family stepping back and bringing in a professional management team.

C T Holdings PLC based in Sri Lanka operates through six segments: retail and wholesale distribution for supermarkets and convenience stores, manufacturing and distribution of food produce, restaurants, real estate and financial services. We are impressed by the sense of stewardship that the founders demonstrate as well as their commitment to stable and sustainable growth.

S H Kelkar & Co Limited is our first Indian IPO investment in six years. Founded in 1922 as an industrial perfumes manufacturer in British India, it is now one of India’s largest fragrance players producing raw materials for a number of consumer and household products that are exported globally to over 50 countries. Currently under its fourth generation of family ownership, there is lots of evidence of long termism in their vision and culture. Improvements have been made to their governance structure in terms of professionalising the board and workforce and their choice of auditor. Their focus and commitment to R&D is encouraging and they acknowledge that their franchise is built on trust and quality of product. They have produced the fragrances for a leading soap brand since the 60s and refuse to share the recipes with anyone even though there is no contract stopping them.

We sold out of HDFC Bank on worries about valuations and cultural deterioration, and trimmed positions in Great Eastern Shipping because of the structural headwinds they face longer term. We also sold Tube Investments, to rectify the position size, and Jyothy Labs, due to concerns around governance.

Significant portfolio changes (cont)

06

Sustainable FundsQ

uarterly Client U

pdate: Fourth Quarter 2015

During the quarter there were 128 company resolutions to vote on. We voted against 3 resolutions relating to corporate structure:

• We voted against Chubb Corporation’s approval of an US$80 million golden parachute payment for the CEO if he is terminated or voluntarily resigns because of a demotion as a result of their recent takeover.

• We voted against Jyothy Laboratories Ltd’s request to approve the modification of compensation for the Chief Executive; we felt that this would, in practice, unfairly accelerate payout in a way not in the interests of shareholders.

• We also voted against a shareholder proposal relating to United Natural Foods Inc., where shareholders were requesting the board of directors adopt a policy that would prohibit acceleration of vesting of shares upon a change in control, such as an employment agreement or equity incentive plan. We believe that the Company’s current double-trigger change in control provisions provide sufficient safeguards to ensure that executives do not receive windfall compensation upon a change in control.

Should any client like a full list of all proxy voting for the companies held in the strategies, please contact us directly.

Proxy voting

Company engagement is a critical part of our investment process. While we will never be able to calculate the exact investment contribution it makes, we are convinced that without it, our long-term returns would be lower and more volatile. Over the past decade, we have spent much time trying to find a good way of reporting our company engagement activities to clients. At one stage, we simply published all our correspondence with companies. However, over time, we have placed more emphasis on the importance of building long-term, strong relationships with company management teams in order to encourage and support change for the better. As a result, we have reviewed our current practice of reporting specific examples of company engagement and concluded that it runs the risk of having a negative impact on the engagement itself. While some companies are comfortable with us reporting our ongoing discussions in a public forum, there are many that are not. As a result, we have therefore decided to stop reporting specific company engagement in our quarterly reports. Should any client wish to speak directly to us on engagement, we will, of course, be delighted to discuss what we have been doing.

Engagement

07

Sustainable FundsQ

uarterly Client U

pdate: Fourth Quarter 2015

Fund Transitions to the Sustainable Funds Group On 9th November 2015, Stewart Investors announced its intention to make a number of changes to client portfolio management responsibilities. The effect of the changes will be to broaden responsibilities across the team, in line with our present investment capabilities. As with similar changes we have made before, they are part of a continuous focus on transparent succession planning and will take place over the coming months, and will be completed by 1st July 2016.

The following changes relate to the sustainable funds group:

• Angus Tulloch will hand over portfolio management responsibilities of the Stewart Investors Asia Pacific Leaders Fund, a sub fund of First State Investments ICVC (the ‘OEIC’), to David Gait and Sashi Reddy.

• David Gait will hand over portfolio management responsibilities of the Stewart Investors Worldwide Sustainability Fund, a sub fund of the OEIC, and Colonial First State Wholesale Worldwide Sustainability Fund to Nick Edgerton, but will remain as co-manager.

• Jonathan Asante will hand over portfolio management responsibilities of the Stewart Investors Worldwide Leaders Fund, a sub fund of the VCC; the Stewart Investors MPF Global Equity Fund and the Colonial First State Wholesale Worldwide Leaders Fund to Sashi Reddy and the sustainable funds group.

Our culture, philosophy and processes remain unchanged and our priority remains to protect client capital and deliver attractive long-term investment returns. These changes, as with others we have made over the years, must be seen in the context of the broader evolution of our business.

Team Updates To further support the above changes, during the quarter, we welcomed Robert Harley and Douglas Ledingham to the sustainable funds group.

Prior to joining the team, Rob worked in various investment management roles for ten years and in the not-for-profit sustainable development sector for eight years. He will work as an investment analyst based in our Edinburgh office.

Rob holds an MSc in International Strategy & Economics (distinction) from the University of St Andrews as well as a BA (Hons) in Political Science from the University of Natal, South Africa.

For the last three years, Doug has worked as an investment analyst in the Stewart Investors Asia Pacific team, which he joined after graduating from the University of Edinburgh. Doug holds an MA in Business Studies and Accountancy.

The intention is for Doug to be based in Edinburgh for the first quarter of the year before relocating to Sydney where he will to sit alongside Nick Edgerton, who returned there from Edinburgh in June 2015.

Over the next few months we will be looking to set-up a Stewart Investors Sydney office where both Nick and Doug will be based along with other members of the team.

Business update

08

Sustainable FundsQ

uarterly Client U

pdate: Fourth Quarter 2015

During the last quarter, the team based in Singapore relocated to a new separate Stewart Investors office based in Duxton Village. If you are ever travelling through Singapore please do let us know as we would love for you to drop in and visit the team and the new office.

ResearchOn 1st July 2015, Stewart Investors announced that we would unbundle payments for research from trading commissions and as a result pay for research from our own resources. The objective behind this decision was to improve transparency and gain greater insight into the value research providers are adding to the investment process, as well as to provide comfort to our clients that research costs are fully paid for by Stewart Investors.

In the past we were reasonably active in commissioning external, bespoke research that has been significant in helping us make investment decisions that continue to shape our client portfolios today. In recent years, our commissioning has dried up a little. We found it increasingly challenging to work with traditional ESG researchers who, because of industry consolidation, were less open to our detailed bottom-up company specific approach. Given we are not sector driven, intra-sector benchmarking and company rankings are of little relevance to us.

However, under our new structure we are excited to be able to drive and tender research to a range of researchers, from investment banks to NGOs and independent consultants, that we believe will contribute and enhance our investment decision-making over time. We hope to be able to share and engage with you on these findings.

Some themes that we will be tendering include:

• Diversity in corporate Asia;

• Sales practices of Asian pharmaceuticals;

• GEM leaders in packaging solutions;

• US remuneration practices;

• ESG leaders in mining; and

• Fossil fuel dependent capital equipment companies.

If you have contacts who you think might be able to support these research ideas, please do let us know, as we would welcome the opportunity to discuss them further with you.

Business update (cont)

09

Sustainable FundsQ

uarterly Client U

pdate: Fourth Quarter 2015

“ Being owned by an NGO, you know, we don’t have any pressure to polish the numbers… our accounts are real. There is no pressure for corner cutting here.”

The Chief Financial Officer of BRAC Bank’s opening comments immediately catch our attention. We are in Dhaka, Bangladesh; its late afternoon, and we are meeting with a bank which is 45% owned by BRAC, the world’s largest non-governmental organisation (NGO). Our host goes on to explain how whilst far from perfect, the bank’s practices reflect this ownership in avoiding lending to socially irresponsible sectors such as tanneries. To us this simply sounds like prudent risk management. There is a sense of purpose and dharma to the bank which becomes apparent through the meeting, something which is to our minds very important in ensuring banks remain wedded to their core mission. Indeed this organisation is one of the three founder members of the Global Alliance for Banking on Values, a network of institutions dedicated to ‘using finance to deliver sustainable economic, social and environmental development’1. An hour later we are discussing ambitions for the next ten years, summed up in the CFO’s phrase that “small is beautiful but big is impactful”. The bank’s mobile payment system, bKash, has just become the largest on the planet, having obtained 20 million subscribers in just four years. In a country where just 7% of the population have access to formal savings yet 40% have mobile phones, the financial inclusion opportunity is tremendous.

BRAC Bank is a good reminder as to why the team has visited Bangladesh twice in the last six months. On both occasions we have returned with a handful of new company ideas for our clients’ funds, and have initiated a number of new positions on the back of meetings such as that with the Chief Financial Officer of BRAC Bank.

The Bangladeshi market is small – a total market capitalisation of a little over $40bn. Putting this into a South Asian context, the combined value of every company on the Dhaka exchange is little larger than India’s single most valuable bank. There are nearly 300 listed companies in the country, but rather than trying to whittle that list down to 15 to meet with on our three day visit, we begin with a blank sheet of paper and pull together some names bottom up. We search for local subsidiaries of Western and Indian groups that we respect, identify shareholdings of high quality Indian parents in listed Bangladeshi entities, and scour for companies sharing Independent Directors with other well-governed companies.

Much like its giant neighbour, Bangladesh is blessed with a mixture of local family companies and a range of listed multinationals which provide ample investment opportunity. However, whereas India has many listed Public Sector Undertakings, the Bangladeshi equivalent are far higher quality from an alignment perspective. There are a handful of entities with core long-term shareholders who imbue their operations with a sense of dharma, of which BRAC Bank would be a prime example. Consequently it is no exaggeration to say that we have found it easier to identify new high quality ideas in this corner of Asia than in South Korea or China, markets of trillions of dollars in size, over the last two years.

Trip report: Bangladesh

1 Source http://www.gabv.org/about-us

10

Sustainable FundsQ

uarterly Client U

pdate: Fourth Quarter 2015

We end up quite excited about the local arm of a global consumer company which looks significantly undervalued compared to its peers in other markets in the region and in absolute terms. There are a number of financial institutions – both banks and housing finance companies – which feel high quality and are at very early stages of their development. Having spoken to everyone we meet about which families have the most integrity, we come away thinking of initiating a position in a family-run pharmaceuticals business which appears to be operated by an honest and competent family with big export ambitions. The limited size of these companies means that none can be large positions in our clients’ funds, but equally the combination of an impressive management team, sound business model and small market capitalisation gives us great cause for optimism about the possible ten-year returns for clients investing in Bangladesh.

This bottom-up stockpicking has occurred very much in spite of the top-down political situation. On our first day of meetings in Dhaka, a hartal – or general strike – has been called. The state had just executed two senior opposition leaders, and their supporters were out in force to make their feelings known.

Bangladeshi politics have never been smooth but have reached a new nadir in 2015. The historic ‘dysfunctional two-party system’ as the Economist puts it2 has now completely broken down. One of the two has used its turn in power to attempt to hold on indefinitely. Over 10,000 opposition members have been jailed, the third largest party, Jamaat-e-Islami, has been banned, and civil society hugely undermined. The week we were in Dhaka, email was intermittent and Facebook taken down, and over 500 soldiers deployed to set up road blocks and security checks on the capital’s streets. Democracy has been suspended in Bangladesh.

This situation renders a huge number of voters completely dispossessed of a voice. To date, Bangladesh has not been a ready source of jihadists going to fight in Afghanistan or Syria; instead its young men have become the largest single source of ‘blue helmet’ UN Peacekeepers. But increasing numbers of returnee migrants from Gulf states with Wahhabist views, plus a targeting by Islamic State, has seen an uptick in attacks on religious minorities in Bangladesh. The serious risk is that the mass of disenfranchised young men who would have voted for the banned Islamist opposition are a breeding ground for radicalisation.

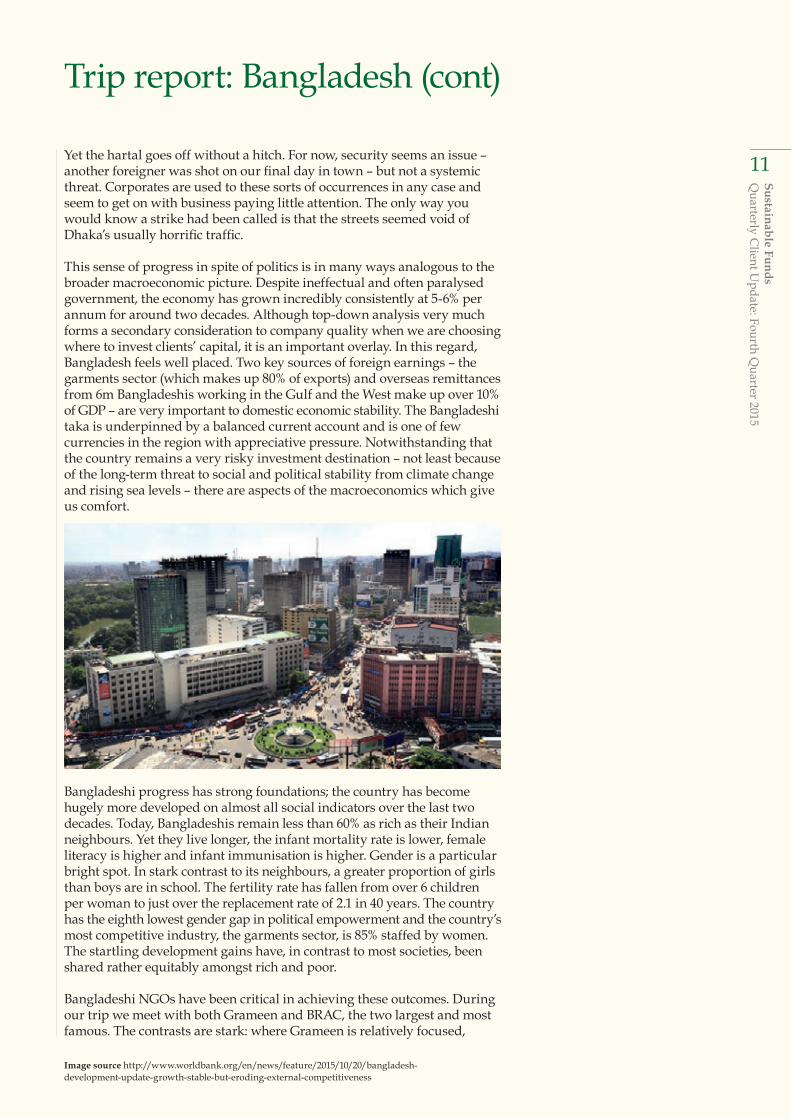

Yet the hartal goes off without a hitch. For now, security seems an issue – another foreigner was shot on our final day in town – but not a systemic threat. Corporates are used to these sorts of occurrences in any case and seem to get on with business paying little attention. The only way you would know a strike had been called is that the streets seemed void of Dhaka’s usually horrific traffic.

This sense of progress in spite of politics is in many ways analogous to the broader macroeconomic picture. Despite ineffectual and often paralysed government, the economy has grown incredibly consistently at 5-6% per annum for around two decades. Although top-down analysis very much forms a secondary consideration to company quality when we are choosing where to invest clients’ capital, it is an important overlay. In this regard, Bangladesh feels well placed. Two key sources of foreign earnings – the garments sector (which makes up 80% of exports) and overseas remittances from 6m Bangladeshis working in the Gulf and the West make up over 10% of GDP – are very important to domestic economic stability. The Bangladeshi taka is underpinned by a balanced current account and is one of few currencies in the region with appreciative pressure. Notwithstanding that the country remains a very risky investment destination – not least because of the long-term threat to social and political stability from climate change and rising sea levels – there are aspects of the macroeconomics which give us comfort.

Bangladeshi progress has strong foundations; the country has become hugely more developed on almost all social indicators over the last two decades. Today, Bangladeshis remain less than 60% as rich as their Indian neighbours. Yet they live longer, the infant mortality rate is lower, female literacy is higher and infant immunisation is higher. Gender is a particular bright spot. In stark contrast to its neighbours, a greater proportion of girls than boys are in school. The fertility rate has fallen from over 6 children per woman to just over the replacement rate of 2.1 in 40 years. The country has the eighth lowest gender gap in political empowerment and the country’s most competitive industry, the garments sector, is 85% staffed by women. The startling development gains have, in contrast to most societies, been shared rather equitably amongst rich and poor.

Bangladeshi NGOs have been critical in achieving these outcomes. During our trip we meet with both Grameen and BRAC, the two largest and most famous. The contrasts are stark: where Grameen is relatively focused,

BRAC is sprawling in its interests; where Grameen feels ideologically rigidly wedded to the founder’s principles, BRAC is continually evolving. It is the latter that, driving around Dhaka, you are constantly reminded of. On one street we simultaneously laid our eyes on the BRAC handicrafts shop, BRAC silk merchants, a billboard for BRAC milk which towered over a BRAC chicken stand; our next meeting was in a building owned by BRAC university and, at the previous one, the metal detectors were operated by BRAC security. The group forms something of a shadow state, providing schooling, health and other social services for over 115,000 staff. Without BRAC, Bangladeshi fertility, infant mortality and illiteracy would no doubt be far higher. The group’s reach is astounding; as The Economist highlights, there are even ‘more BRAC legal centres than police stations’ in Bangladesh3.

We feel incredibly fortunate therefore that our final meeting of the trip is a conversation with Sir Fazle Abed, the founder, Chairman and guiding hand of BRAC for the last 43 years. A sprightly 79 year old, our conversation covers everything from his reflections on the means to financial self-sufficiency for an NGO, how at BRAC University ethics is a compulsory course, and the long-term plan for BRAC’s different entities in the financial sector. We depart for the airport a little star struck and ever more impressed with the culture of our host’s organisation. Bangladesh remains a rich seam of high quality companies in which we may invest clients’ capital for many years to come.

£10bn+Portfolio Weight 6.9 12.2 18.1 16.1 22.4 20.9Index Weight 0.0 1.0 7.9 17.4 18.5 55.2Style Research does not always have full stock coverage; weights may not total 100%.

Contribution Analysis – twelve months to 31 Dec 2015

Data source: This information is calculated by Stewart Investors using the Barra Enterprise Performance system. Index information is provided by RIMES.* The inception date for performance measurement purposes is 19 Dec 2005. Returns are cumulative, net of fees and tax, and denominated in GBP.** The benchmark for the Stewart Investors Asia Pacific Sustainability Fund A Acc is the MSCI AC Asia Pacific ex Japan Index and is calculated net of tax.

Benchmark Return**

3 YearsChange (%)

£500m to £1bn

Top 3 Contributing StocksValue Added*

(bps)

Kasikornbank

£0 to £500m

Number of Holdings

Stock Name

Stock Name

£2.5bn to £5bn

Stock Name Sector

Sector

IndexWeight** (%)

Telecom Services

Portfolio Weight (%)

4 Years5 YearsSince Launch* 1 Year

PortfolioWeight* (%)

2 Years

Disposals – three months to 31 Dec 2015

Portfolio Weight (%)

6 Months 3 Months

ValueAdded* (bps)

£5bn to £10bn

£1bn to £2.5bn

Towngas ChinaTech Mahindra

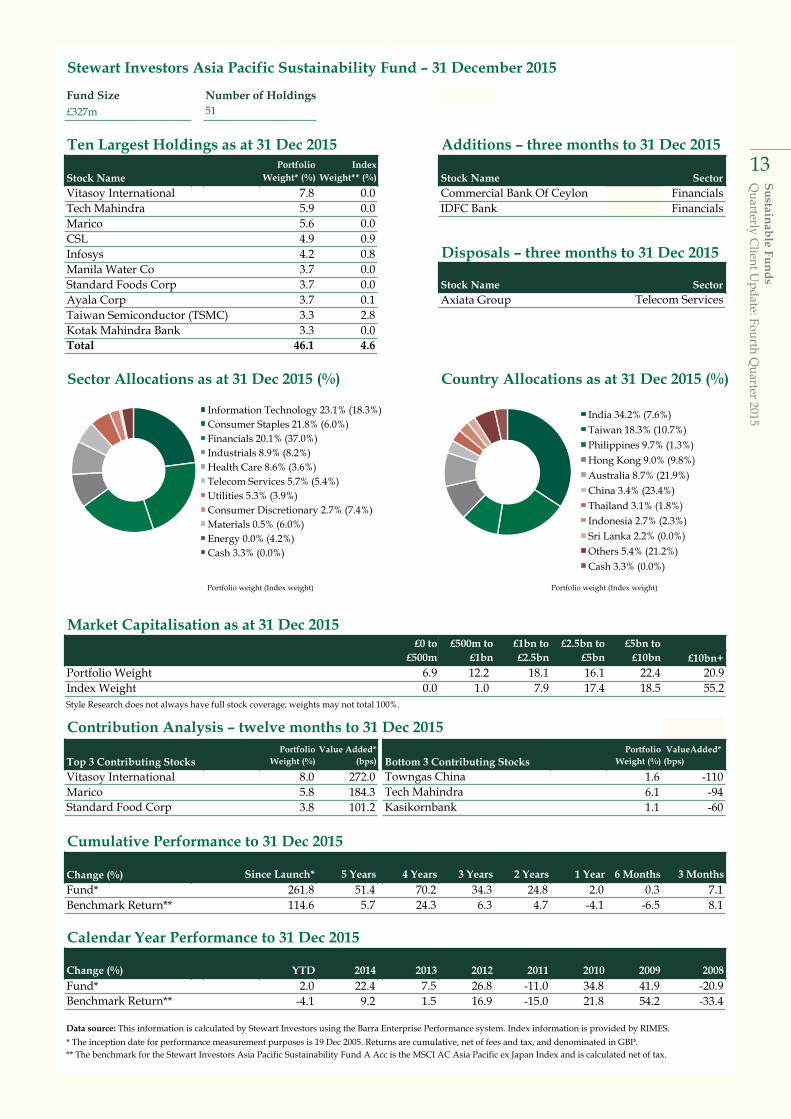

Information Technology 23.1% (18.3%) Consumer Staples 21.8% (6.0%) Financials 20.1% (37.0%) Industrials 8.9% (8.2%) Health Care 8.6% (3.6%) Telecom Services 5.7% (5.4%) Utilities 5.3% (3.9%) Consumer Discretionary 2.7% (7.4%) Materials 0.5% (6.0%) Energy 0.0% (4.2%) Cash 3.3% (0.0%)

India 34.2% (7.6%) Taiwan 18.3% (10.7%) Philippines 9.7% (1.3%) Hong Kong 9.0% (9.8%) Australia 8.7% (21.9%) China 3.4% (23.4%) Thailand 3.1% (1.8%) Indonesia 2.7% (2.3%) Sri Lanka 2.2% (0.0%) Others 5.4% (21.2%) Cash 3.3% (0.0%)

14

Sustainable FundsQ

uarterly Client U

pdate: Fourth Quarter 2015

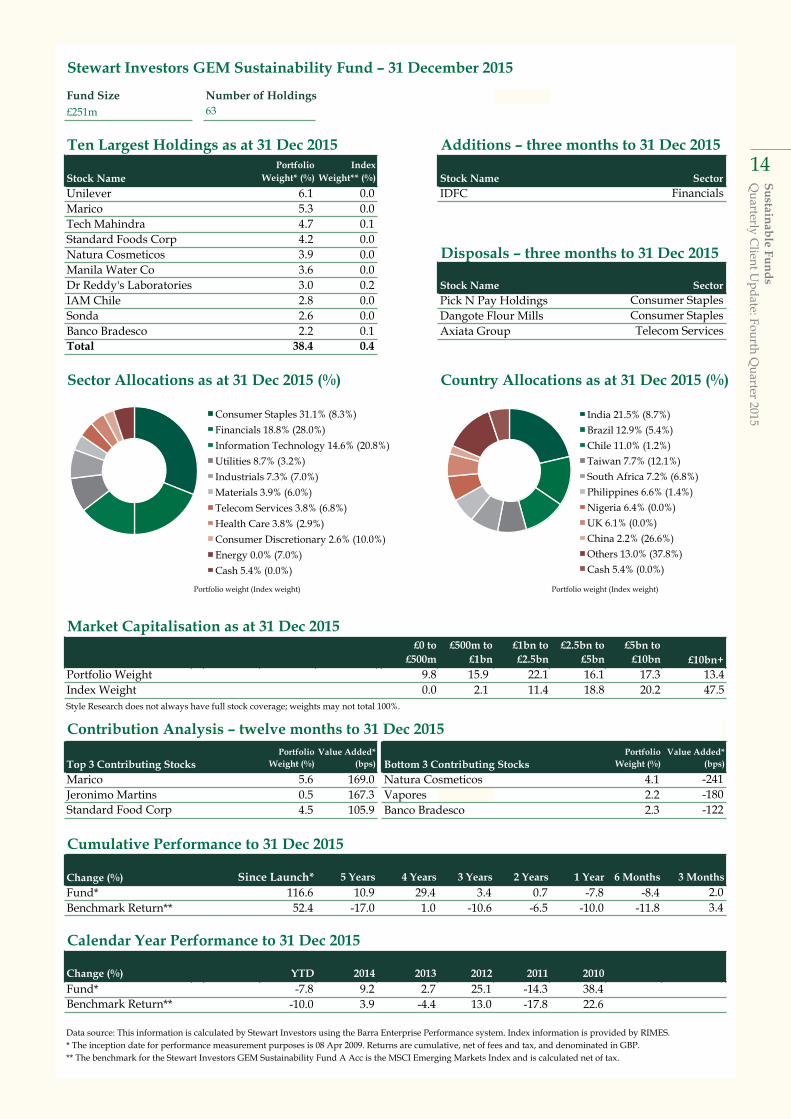

Stewart Investors GEM Sustainability Fund – 31 December 2015

Fund Size£251m 63

Ten Largest Holdings as at 31 Dec 2015 Additions – three months to 31 Dec 2015

Portfolio Weight 9.8 15.9 22.1 16.1 17.3Index Weight 0.0 2.1 11.4 18.8 20.2Style Research does not always have full stock coverage; weights may not total 100%.

Contribution Analysis – twelve months to 31 Dec 2015

Data source: This information is calculated by Stewart Investors using the Barra Enterprise Performance system. Index information is provided by RIMES.* The inception date for performance measurement purposes is 08 Apr 2009. Returns are cumulative, net of fees and tax, and denominated in GBP.** The benchmark for the Stewart Investors GEM Sustainability Fund A Acc is the MSCI Emerging Markets Index and is calculated net of tax.

Stock Name

4 Years

Disposals – three months to 31 Dec 2015

Sector

Bottom 3 Contributing Stocks

£2.5bn to £5bn

Portfolio Weight (%)

Value Added* (bps)

£10bn+

Stock Name Stock Name SectorPortfolio

Weight* (%)

Number of Holdings

IndexWeight** (%)

£1bn to £2.5bn

£0 to £500m

£500m to £1bn

Top 3 Contributing Stocks

Change (%)

Portfolio Weight (%)

Value Added* (bps)

Benchmark Return**

3.4

3 Months

-241-180

Since Launch*

2013

13.447.5

£5bn to £10bn

-122

2.0

Financials

Consumer StaplesConsumer StaplesTelecom Services

Consumer Staples 31.1% (8.3%) Financials 18.8% (28.0%) Information Technology 14.6% (20.8%) Utilities 8.7% (3.2%) Industrials 7.3% (7.0%) Materials 3.9% (6.0%) Telecom Services 3.8% (6.8%) Health Care 3.8% (2.9%) Consumer Discretionary 2.6% (10.0%) Energy 0.0% (7.0%) Cash 5.4% (0.0%)

India 21.5% (8.7%) Brazil 12.9% (5.4%) Chile 11.0% (1.2%) Taiwan 7.7% (12.1%) South Africa 7.2% (6.8%) Philippines 6.6% (1.4%) Nigeria 6.4% (0.0%) UK 6.1% (0.0%) China 2.2% (26.6%) Others 13.0% (37.8%) Cash 5.4% (0.0%)

15

Sustainable FundsQ

uarterly Client U

pdate: Fourth Quarter 2015

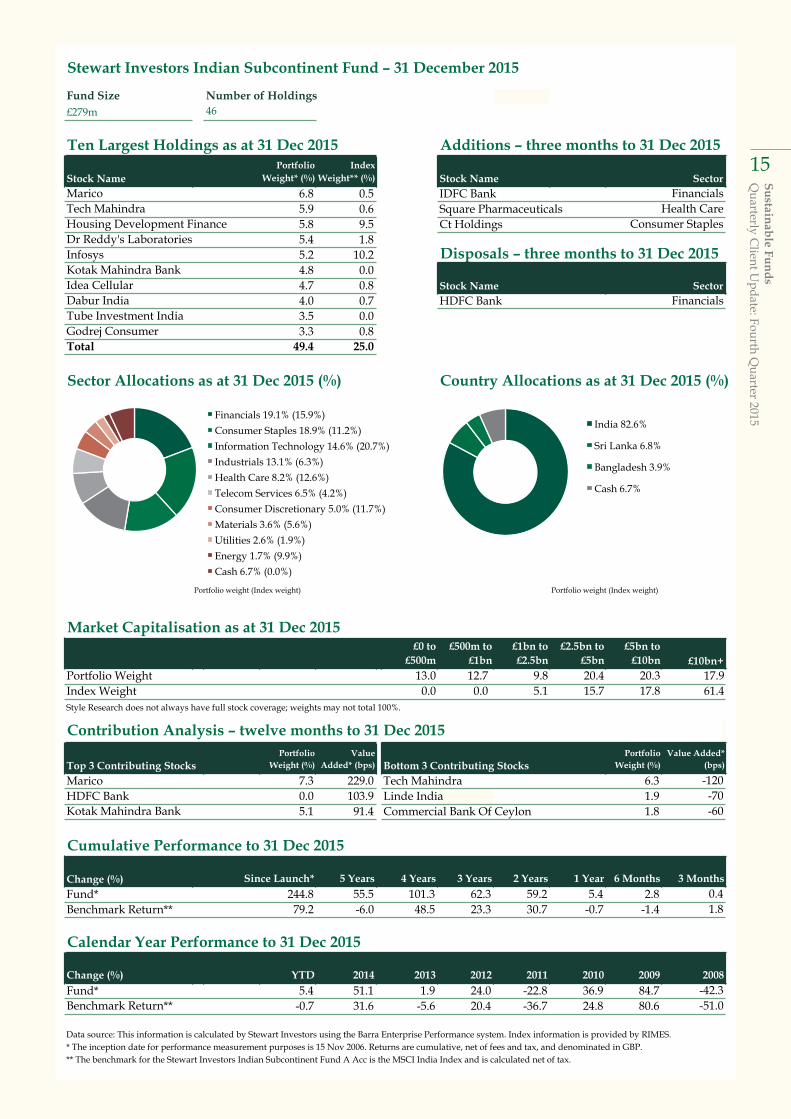

Stewart Investors Indian Subcontinent Fund – 31 December 2015

Fund Size£279m 46

Ten Largest Holdings as at 31 Dec 2015 Additions – three months to 31 Dec 2015

Portfolio Weight 13.0 12.7 9.8 20.4 20.3Index Weight 0.0 0.0 5.1 15.7 17.8Style Research does not always have full stock coverage; weights may not total 100%.

Contribution Analysis – twelve months to 31 Dec 2015

Marico 7.3 229.0 Tech Mahindra 6.3HDFC Bank 0.0 103.9 Linde India 1.9Kotak Mahindra Bank 5.1 91.4 Commercial Bank Of Ceylon 1.8

Data source: This information is calculated by Stewart Investors using the Barra Enterprise Performance system. Index information is provided by RIMES.* The inception date for performance measurement purposes is 15 Nov 2006. Returns are cumulative, net of fees and tax, and denominated in GBP.** The benchmark for the Stewart Investors Indian Subcontinent Fund A Acc is the MSCI India Index and is calculated net of tax.

Portfolio Weight 3.4 5.4 9.8 12.3 30.8Index Weight 0.0 0.2 2.0 7.0 14.1Style Research does not always have full stock coverage; weights may not total 100%.

Contribution Analysis – twelve months to 31 Dec 2015

AIN Pharmaciez 2.9 199.2 Vapores 1.5Chubb Corp 2.8 160.6 Natura Cosmeticos 2.1Jeronimo Martins 0.9 111.0 Tiger Brands 1.1

Cumulative Performance to 31 Dec 2015

Fund (net of fees)* 36.8 - - 33.5 12.1 5.4 4.6Benchmark Return** 40.0 - - 37.7 14.3 3.3 1.5

Calendar Year Performance to 31 Dec 2015

Change (%) YTD 2014Fund (net of fees)* 5.4 6.4 19.1

3.3 10.6 20.5

Data source: This information is calculated by Stewart Investors using the Barra Enterprise Performance system. Index information is provided by RIMES.* The inception date for performance measurement purposes is 23 Nov 2012. Returns are cumulative, net of fees and tax, and denominated in GBP.** The benchmark for the Stewart Investors Worldwide Sustainability Fund A Acc is the MSCI AC World Index and is calculated net of tax.

5.97.9

Stock Name

Top 3 Contributing Stocks

Change (%)

-140-124-50

5 Years

Stock Name Stock Name Sector

Disposals – three months to 31 Dec 2015

PortfolioWeight* (%)

IndexWeight** (%)

Benchmark Return**

Bottom 3 Contributing Stocks

Since Launch*

2013

Portfolio Weight (%)

Value Added* (bps)

4 Years

Number of Holdings

Sector

Information Technology

£2.5bn to £5bn

£1bn to £2.5bn

Consumer StaplesIndustrials

29.4

£0 to £500m

£500m to £1bn

76.7

£5bn to £10bn £10bn+

3 Years 2 Years 1 Year 6 Months 3 Months

Portfolio Weight (%)

Value Added* (bps)

Consumer Staples 23.9% (10.3%) Health Care 23.8% (12.5%) Financials 13.8% (21.5%) Industrials 13.3% (10.3%) Information Technology 8.3% (14.9%) Materials 4.9% (4.5%) Utilities 1.8% (3.2%) Consumer Discretionary 1.1% (12.9%) Telecom Services 0.0% (3.7%) Energy 0.0% (6.2%) Cash 9.1% (0.0%)

USA 22.2% (53.2%) Germany 13.7% (3.1%) India 10.0% (0.8%) Japan 7.6% (8.0%) UK 7.6% (6.7%) Switzerland 5.5% (3.3%) Australia 5.0% (2.4%) Brazil 3.7% (0.5%) Spain 2.8% (1.1%) Others 12.8% (20.9%) Cash 9.1% (0.0%)

17

Sustainable FundsQ

uarterly Client U

pdate: Fourth Quarter 2015

Important InformationThis document is directed at persons of a professional, sophisticated, institutional or wholesale nature and not the retail market.This document has been prepared for general information purposes only and is intended to provide a summary of the subject matter covered. It does not purport to be comprehensive or to give advice. The views expressed are the views of the writer at the time of issue and may change over time. This is not an offer document, and does not constitute an offer, invitation, investment recommendation or inducement to distribute or purchase securities, shares, units or other interests or to enter into an investment agreement. No person should rely on the content and/or act on the basis of any matter contained in this document.This document is confidential and must not be copied, reproduced, circulated or transmitted, in whole or in part, and in any form or by any means without our prior written consent. The information contained within this document has been obtained from sources that we believe to be reliable and accurate at the time of issue but no representation or warranty, express or implied, is made as to the fairness, accuracy or completeness of the information. We do not accept any liability for any loss arising whether directly or indirectly from any use of this document.References to “we” or “us” are references to Stewart Investors. The funds referred to in this report (the “Funds”) are sub funds of First State Investments ICVC, an open ended investment company with variable capital incorporated with limited liability and registered in England and Wales (the “Company”). Detailed information about the Company and the Funds is contained in the Prospectus and Key Investor Information Documents which are available free of charge by writing to: Client Services, Stewart Investors, 23 St Andrew Square, Edinburgh EH2 1BB or by telephoning 0800 587 4141 between 09:00 and 17:00 Monday to Friday or by visiting www.stewartinvestors.com. Telephone calls with Stewart Investors may be recorded. The Funds are not authorised for offer/sale to the public in certain jurisdictions. Please refer to the Funds’ offering documents for further details including risk factors.Neither the Commonwealth Bank of Australia (the ‘Bank’) ABN 48 123 123 124 nor any of its subsidiaries guarantees or in any way stands behind the performance of the Funds, or the repayment of capital by the Funds. Investments in the Funds are not deposits or other liabilities of the Bank or its subsidiaries, and the Funds are subject to investment risk including possible delays in repayment and loss of income and capital invested.Past performance is not a reliable indicator of future performance.Reference to specific securities (if any) is included for the purpose of illustration only and should not be construed as a recommendation to buy or sell. Reference to the names of any company is merely to explain the investment strategy and should not be construed as investment advice or a recommendation to invest in any of those companies.Hong Kong and SingaporeIn Hong Kong, this document is issued by First State Investments (Hong Kong) Limited and has not been reviewed by the Securities & Futures Commission in Hong Kong. In Singapore, this document is issued by First State Investments (Singapore) whose company registration number is 196900420D. Stewart Investors is a business name of First State Investments (Hong Kong) Limited. Stewart Investors (registration number 53310114W) is a business division of First State Investments (Singapore).The Funds are not authorised by the Securities & Futures Commission in Hong Kong and are not available for sale to the retail public in Hong Kong.AustraliaIn Australia, this document is issued by Colonial First State Asset Management (Australia) Limited AFSL 289017 ABN 89 114 194311. Stewart Investors is a trading name of Colonial First State Asset Management (Australia) Limited.United Kingdom and European Economic Area (“EEA”)In the United Kingdom, this document is issued by First State Investments (UK) Limited which is authorised and regulated in the UK by the Financial Conduct Authority (registration number 143359). Registered office: Finsbury Circus House, 15 Finsbury Circus, London, EC2M 7EB, number 2294743. Outside the UK within the EEA, this document is issued by First State Investments International Limited which is authorised and regulated in the UK by the Financial Conduct Authority (registration number 122512). Registered office 23 St. Andrew Square, Edinburgh, Midlothian EH2 1BB number SC079063. Stewart Investors is a trading name of First State Investments (UK) Limited and First State Investments International Limited.Middle EastIn certain jurisdictions the distribution of this material may be restricted. The recipient is required to inform themselves about any such restrictions and observe them. By having requested this document and by not deleting this email and attachment, you warrant and represent that you qualify under any applicable financial promotion rules that may be applicable to you to receive and consider this document, failing which you should return and delete this e-mail and all attachments pertaining thereto. In the Middle East, this material is communicated by First State Investments International Limited which is regulated in Dubai by the DFSA as a Representative Office. KuwaitIf in doubt, you are recommended to consult a party licensed by the Capital Markets Authority (“CMA”) pursuant to Law No. 7/2010 and the Executive Regulations to give you the appropriate advice. Neither this document nor any of the information contained herein is intended to and shall not lead to the conclusion of any contract whatsoever within Kuwait.UAE – Dubai International Financial Centre (DIFC)Within the DIFC this material is directed solely at Professional Clients as defined by the DFSA’s COB Rulebook. UAE (ex-DIFC)By having requested this document and/or by not deleting this email and attachment, you warrant and represent that you qualify under the exemptions contained in Article 2 of the Emirates Securities and Commodities Authority Board Resolution No 37 of 2012, as amended by decision No 13 of 2012 (the “Mutual Fund Regulations”). By receiving this material you acknowledge and confirm that you fall within one or more of the exemptions contained in Article 2 of the Mutual Fund Regulations.United States of AmericaIn the United States this document is issued by First State Investments International Limited, registered in the United States of America as an Investment Advisor under the Investment Advisors Act of 1940 (SEC file number 801-17900). Stewart Investors is the trading name of First State Investments International Limited. This material is solely for the attention of institutional investors already invested in the Sustainability strategies managed by Stewart Investors. It is not to be distributed to the general public, private customers or retail investors. The Funds are not available for investment by US persons.Fund information is being provided as an example of Stewart Investors’ expertise in the strategy. Differences between fund-specific constraints or fees and those of a similarly managed mandate would affect performance results. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance, strategy and results of your portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable for a client’s investment portfolio. Economic factors, market conditions, and investment strategies will affect the performance of any portfolio and there are no assurances that it will match or outperform any particular benchmark.The comparative benchmarks or indices referred to herein are for illustrative and comparison purposes only, may not be available for direct investment, are unmanaged, assume reinvestment of income, and have limitations when used for comparison or other purposes because they may have volatility, credit, or other material characteristics (such as number and types of securities) that are different from your account.

SUSQ4_0116_EMEA

For further information on institutional enquiries please contact [email protected]

For further information on wholesale enquiries please contact [email protected]