38

Stochastic Calculus and Model of the Behavior of Stock Prices

| Date post: | 30-Dec-2015 |

| Category: |

Documents |

| Upload: | hanae-sparks |

| View: | 40 times |

| Download: | 3 times |

Stochastic Calculus and Model of the

Behaviorof Stock Prices

Why we need stochastic calculus

• Many important issues can not be averaged out.

• Some examples

Examples

• Adam and Benny took two course. Adam got two Cs. Benny got one B and one D. What are their average grades? Who will have trouble graduating?

Investment Return

• Suppose a portfolio either gain 60% with 50% probability or lose 60% with 50% probability. What is its average rate of return? What is the expected value of the portfolio after 10 years?

Solution

• The average rate of return is0.6*50% + (-0.6)*50% = 0

• The expected value of the portfolio after 10 years is therefore 1000. Right?

• Let’s calculate

• 1000*(1+0.6)^5*(1-0.6)^5 = ?

• What is the answer? Why?

Examples

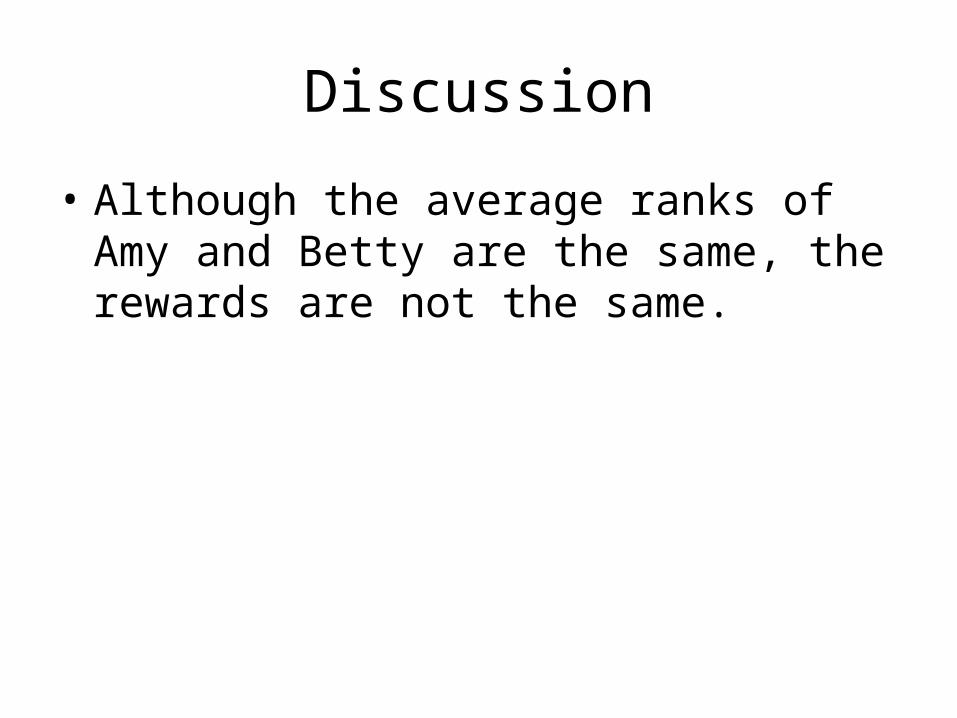

• Amy and Betty are Olympic athletes. Amy got two silver medals. Betty got one gold and one bronze. What are their average ranks in two sports? Who will get more attention from media, audience and advertisers?

• Rewards will be given to Olympic medalists according to the formula 1/x^2 million dollars, where x is the rank of an athlete in an event. How much rewards Amy and Betty will get?

Solution

• Amy will get

• Betty will get

million 5.02

12

2

million 11.13

11

2

Discussion

• Although the average ranks of Amy and Betty are the same, the rewards are not the same.

• Reproductive successes are closely related to the amount of resources one controls. While both male and female animals benefit from more resources, their precise relations are different.

• Assume the relation between the amount of resource under control and the number of offspring for female is n = 1.52x^0.5 and for male is n = 0.45x^2, where x is the amount of resources and n is the number of offspring. Suppose x can take the discrete values 1, 2 and 3. We further assume the probability of average numbers of females and males who obtain resources 1, 2 and 3 are {1/3, 1/3, 1/3}. What are the expected number of offspring for females and males? (To be continued)

• Suppose genetic systems can alter the ratios of males and females who can obtain different amount of resources. Specifically, under one type of genetic regulation, the new probability distributions for females and males to obtain resources of amount 1, 2 and 3 is {1/3-1/8, 1/3+1/4, 1/3-1/8} and under another type of genetic regulation, the new probability distributions for females and males to obtain resources of amount 1, 2 and 3 is {1/3+1/8, 1/3-1/4, 1/3+1/8} . What are the new average numbers of offspring for females and males? How genetic systems achieve such regulation?

Solution

• The expected number of offspring for females is

• The expected number of offspring for males is

1.2352.13/1252.13/1152.13/1

1.2345.03/1245.03/1145.03/1 22

• When female and male distribution is revised to {1/3-1/8, 1/3+1/4, 1/3-1/8}, the new expected number of offspring by females and males are 2.12 and 1.99 respectively.

• When female and male distribution is revised to {1/3+1/8, 1/3-1/4, 1/3+1/8}, the new expected number of offspring by females and males are 2.08 and 2.21 respectively.

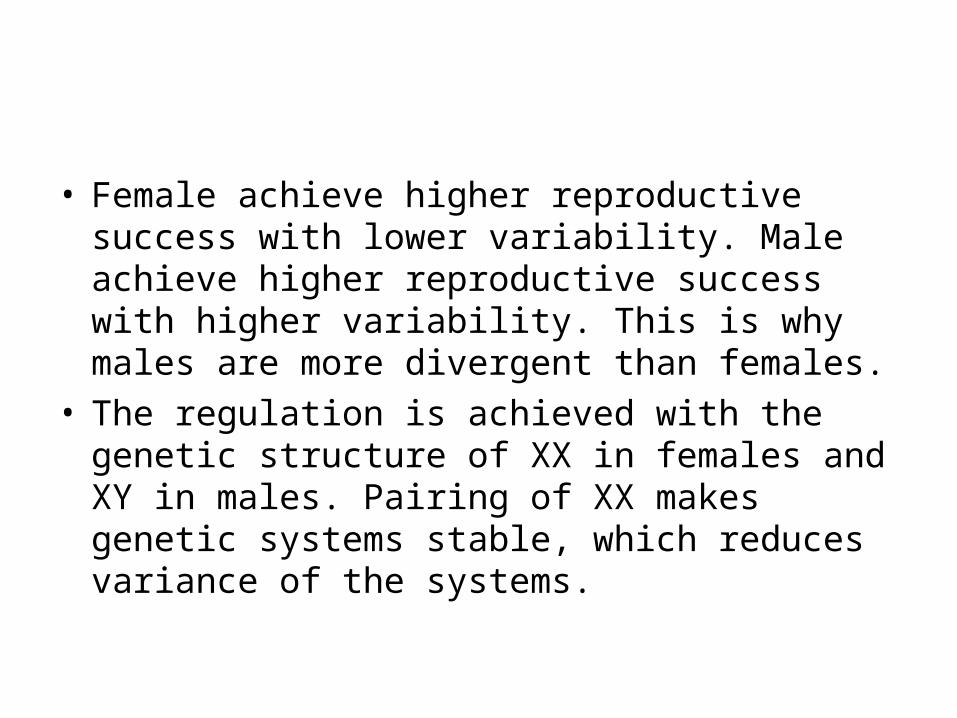

• Female achieve higher reproductive success with lower variability. Male achieve higher reproductive success with higher variability. This is why males are more divergent than females.

• The regulation is achieved with the genetic structure of XX in females and XY in males. Pairing of XX makes genetic systems stable, which reduces variance of the systems.

Square root function, concave

Square function, convex

General discussion

• One function is concave while the other function is convex, which are defined by the signs of the second order derivatives.

• This means that we need to study second order derivatives when dealing with stochastic functions.

Mathematical derivatives and financial derivatives

• Calculus is the most important intellectual invention. Derivatives on deterministic variables

• Mathematically, financial derivatives are derivatives on stochastic variables.

• In this course we will show the theory of financial derivatives, developed by Black-Scholes, will lead to fundamental changes in the understanding social and life sciences.

The history of stochastic calculus and derivative theory

• 1900, Bachelier: A student of Poincare– His Ph.D. dissertation: The Mathematics of Speculation – Stock movement as normal processes– Work never recognized in his life time

• No arbitrage theory– Harold Hotelling

• Ito Lemma– Ito developed stochastic calculus in 1940s near the end of WWII,

when Japan was in extreme difficult time

– Ito was awarded the inaugural Gauss Prize in 2006 at age of 91

The history of stochastic calculus and derivative theory (continued)

• Feynman (1948)-Kac (1951) formula, • 1960s, the revival of stochastic theory in

economics• 1973, Black-Scholes

– Fischer Black died in 1995, Scholes and Merton were awarded Nobel Prize in economics in 1997.

• Recently, real option theory and an analytical theory of project investment inspired by the option theory

• It often took many years for people to recognize the importance of a new heory

Ito’s Lemma

• If we know the stochastic process followed by x, Ito’s lemma tells us the stochastic process followed by some function G (x, t )

• Since a derivative security is a function of the price of the underlying and time, Ito’s lemma plays an important part in the analysis of derivative securities

• Why it is called a lemma?

The Question

t?and x of change with thechanges t)G(x, How

),(),(

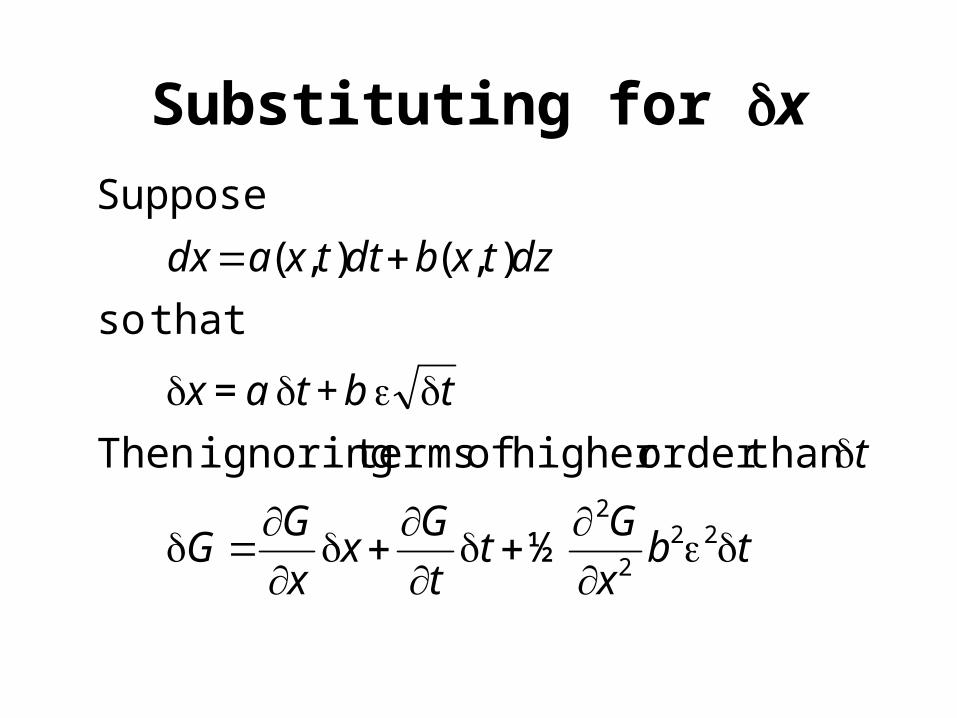

Suppose

dztxbdttxadx

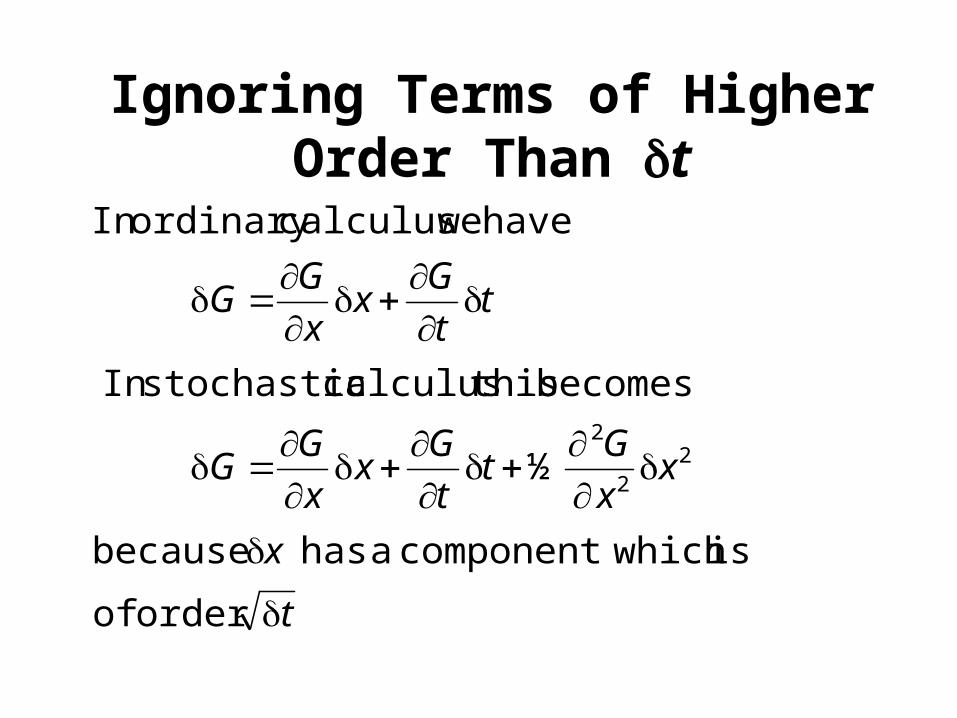

Taylor Series Expansion

• A Taylor’s series expansion of G(x, t) gives

22

22

22

2

tt

Gtx

tx

G

xx

Gt

t

Gx

x

GG

½

½

Ignoring Terms of Higher Order Than t

t

x

xx

Gt

t

Gx

x

GG

tt

Gx

x

GG

order of

is whichcomponent a has because

½

becomes this calculus stochastic In

have wecalculusordinary In

22

2

Substituting for x

tbx

Gt

t

Gx

x

GG

t

tbtax

dztxbdttxadx

222

2

½

than order higher of terms ignoring Then

+ =

that so

),(),(

Suppose

The 2t Term

tbx

Gt

t

Gx

x

GG

tt

ttE

E

EE

E

22

2

2

2

22

2

1

)(

1)(

1)]([)(

0)()1,0(

Hence ignored. be

can and to alproportion is of variance The

that follows It

Since

2

Taking Limits

Taking limits ½

Substituting

We obtain ½

This is Ito's Lemma

dGG

xdx

G

tdt

G

xb dt

dx a dt b dz

dGG

xa

G

t

G

xb dt

G

xb dz

2

22

2

22

Differentiation is stochastic and deterministic calculus

• Ito Lemma can be written in another form

• In deterministic calculus, the differentiation is

dtbx

Gdt

t

Gdx

x

GdG 2

2

2

2

1

dtt

Gdx

x

GdG

The simplest possible model of stock prices

• Over long term, there is a trend

• Over short term, randomness dominates. It is very difficult to know what the stock price tomorrow.

A Process for Stock Prices

where is the expected return is the volatility.

The discrete time equivalent is

dS Sdt Sdz

tStSS

Application of Ito’s Lemmato a Stock Price Process

dzSS

GdtS

S

G

t

GS

S

GdG

tSG

zdSdtSSd

½

and of function a For

is process price stock The

222

2

Examples

dzdtdG

SG

dzGdtGrdG

eSG

TtTr

2

ln 2.

)(

at time maturing

contract afor stock a of price forward The 1.

2

)(

Expected return and variance

• A stock’s return over the past six years are• 19%, 25%, 37%, -40%, 20%, 15%. • Question:

– What is the arithmetic return– What is the geometric return– What is the variance– What is mu – 1/2sigma^2? Compare it with the

geometric return. – Which number: arithmetic return or geometric return is

more relevant to investors?

Answer

• Arithmetic mean: 12.67%

• Geometric mean: 9.11%

• Variance: 7.23%

• Arithmetic mean -1/2*variance: 9.05%

• Geometric mean is more relevant because long term wealth growth is determined by geometric mean.

Arithmetic mean and geometric mean

• The annual return of a mutual fund is

• 0.150.2 0.3 -0.2 0.25

• Which has an arithmetic mean of 0.14 and geometric mean of 0.124, which is the true rate of return.

• Calculating r- 0.5*sigma^2 yields 0.12, which is close to the geometric mean.

Homework 1

• The returns of a mutual fund in the last five years are

• What is the arithmetic mean of the return? What is the geometric mean of the return? What is

• where mu is arithmetic mean and sigma is standard deviation of the return series. What conclusion you will get from the results?

30% 25% 35% -30% 25%

2

2

Homework 2

• Rewards will be given to Olympic medalists according to the formula 1/x^2, where x is the rank of an athlete in an event. Suppose Amy and betty are expected to reach number 2 in their competitions. But Amy’s performance is more volatile than Betty’s. Specifically, Amy has (0.3, 0.4, 03) chance to get gold, silver and bronze while Betty has (0.1, 0.8,0.1) respectively. How much rewards Amy and Betty are expected to get?

Homework 3

• Fancy and Mundane each manage two new mutual funds. Last year, fancy’s funds got returns of 30% and -10%, while Mundane’s funds got 11% and 9%. One of Fancy’s fund was selected as “One of the Best New Mutual Funds” by a finance journal. As a result, the size of his fund increased by ten folds. The other fund managed by Fancy was quietly closed down. Mundane’s funds didn’t get any media coverage. The fund sizes stayed more or less the same. What are the average returns of funds managed by Fancy and Mundane? Who have better management skill according to CAPM? Which fund manager is better off?

![An extension of stochastic calculus to certain non ... · The stochastic calculus of variations on the Wiener space, cf. [12], allows to construct an anticipating stochastic calculus](https://static.documents.pub/doc/80x56/5f3fdedb6dbd726b7247525b/an-extension-of-stochastic-calculus-to-certain-non-the-stochastic-calculus-of.jpg)