Stochastic Calculus, Application of Real Analysis in Finance Stochastic Calculus, Application of Real Analysis in Finance Workshop for Young Mathematicians in Korea Seungkyu Lee Pohang University of Science and Technology August 4th, 2010

Transcript

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus, Application of RealAnalysis in Finance

Workshop for Young Mathematicians in Korea

Seungkyu Lee

Pohang University of Science and Technology

August 4th, 2010

Stochastic Calculus, Application of Real Analysis in Finance

Contents

1 BINOMIAL ASSET PRICING MODEL

2 Stochastic Calculus

Stochastic Calculus, Application of Real Analysis in Finance

Contents

1 BINOMIAL ASSET PRICING MODEL

2 Stochastic Calculus

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Contents

1 BINOMIAL ASSET PRICING MODEL

2 Stochastic Calculus

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Binomial Asset Pricing Model

Assumptions:

Model stock prices in discrete time

at each step, the stock price will change to one of twopossible values

begin with an initial positive stock price S0

there are two positive numbers, d and u, with 0 < d < 1 < usuch that at the next period, the stock price will be either dS0or uS0, d = 1/u.

⇒ Of course, real stock price movements are much morecomplicated

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Binomial Asset Pricing Model

Assumptions:

Model stock prices in discrete time

at each step, the stock price will change to one of twopossible values

begin with an initial positive stock price S0

there are two positive numbers, d and u, with 0 < d < 1 < usuch that at the next period, the stock price will be either dS0or uS0, d = 1/u.

⇒ Of course, real stock price movements are much morecomplicated

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Binomial Asset Pricing Model

Objectives:

the definition of probability space and

the concept of Arbitrage Pricing and its relation toRisk-Neutral Pricing is clearly illuminated

Flip CoinsToss a coin and when we get a ”Head,” the stock price moves up,but when we get a ”Tail,” the price moves down.⇒ the price at time 1 by S1(H) = uS0 and S1(T) = dS1⇒ After the second toss,

S2(HH) = uS1(H) = u2S0, S2(HT) = dS1(H) = duS0

S2(TH) = uS1(H) = duS0, S2(TT) = dS1(T) = d2S0

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Binomial Asset Pricing Model

Objectives:

the definition of probability space and

the concept of Arbitrage Pricing and its relation toRisk-Neutral Pricing is clearly illuminated

Flip CoinsToss a coin and when we get a ”Head,” the stock price moves up,but when we get a ”Tail,” the price moves down.

⇒ the price at time 1 by S1(H) = uS0 and S1(T) = dS1⇒ After the second toss,

S2(HH) = uS1(H) = u2S0, S2(HT) = dS1(H) = duS0

S2(TH) = uS1(H) = duS0, S2(TT) = dS1(T) = d2S0

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Binomial Asset Pricing Model

Objectives:

the definition of probability space and

the concept of Arbitrage Pricing and its relation toRisk-Neutral Pricing is clearly illuminated

Flip CoinsToss a coin and when we get a ”Head,” the stock price moves up,but when we get a ”Tail,” the price moves down.⇒ the price at time 1 by S1(H) = uS0 and S1(T) = dS1

⇒ After the second toss,

S2(HH) = uS1(H) = u2S0, S2(HT) = dS1(H) = duS0

S2(TH) = uS1(H) = duS0, S2(TT) = dS1(T) = d2S0

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Binomial Asset Pricing Model

Objectives:

the definition of probability space and

the concept of Arbitrage Pricing and its relation toRisk-Neutral Pricing is clearly illuminated

Flip CoinsToss a coin and when we get a ”Head,” the stock price moves up,but when we get a ”Tail,” the price moves down.⇒ the price at time 1 by S1(H) = uS0 and S1(T) = dS1⇒ After the second toss,

S2(HH) = uS1(H) = u2S0, S2(HT) = dS1(H) = duS0

S2(TH) = uS1(H) = duS0, S2(TT) = dS1(T) = d2S0

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Binomial Asset Pricing Model

For the moment, let us assume that the third toss is the last oneand denote by

Ω = HHH,HHT ,HTH,HTT , THH, THT , TTH, TTT

the set of all possible outcomes of the three tosses.

The set Ω of all possible outcomes of a random experiment iscalled the sample space for the experiment, and the element ω ofΩ are called sample points.Denote the k-th component of ω by ωk.⇒ S3 depends on all of ω.⇒ S2 depends on only the first two components of ω, ω1 and ω2.

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Binomial Asset Pricing Model

For the moment, let us assume that the third toss is the last oneand denote by

Ω = HHH,HHT ,HTH,HTT , THH, THT , TTH, TTT

the set of all possible outcomes of the three tosses.The set Ω of all possible outcomes of a random experiment iscalled the sample space for the experiment, and the element ω ofΩ are called sample points.

Denote the k-th component of ω by ωk.⇒ S3 depends on all of ω.⇒ S2 depends on only the first two components of ω, ω1 and ω2.

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Binomial Asset Pricing Model

For the moment, let us assume that the third toss is the last oneand denote by

Ω = HHH,HHT ,HTH,HTT , THH, THT , TTH, TTT

the set of all possible outcomes of the three tosses.The set Ω of all possible outcomes of a random experiment iscalled the sample space for the experiment, and the element ω ofΩ are called sample points.Denote the k-th component of ω by ωk.⇒ S3 depends on all of ω.⇒ S2 depends on only the first two components of ω, ω1 and ω2.

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Basic Probability Theory

Probability space (Ω,F,P) like (R,B,µ), Lebesgue Measure

Ω: the set of all possible realizations of the stochasticeconomy

Ω = HHH,HHT ,HTH,HTT , THH, THT , TTH, TTT

ω: a sample path, ω ∈ ΩFt: the sigma field of distinguishable events at time t

P: a probability measure defined on the elements of Ft

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Probability Spaces

DefinitionIf Ω is a given set, then a σ-algebra F on Ω is a family F ofsubsets of Ω with the following properties:

∅ ∈ F

F ∈ F ⇒ FC ∈ F, where FC = Ω \ F is the complement of F inΩ

A1,A2, . . . ∈ F ⇒ A :=⋃∞i=1Ai ∈ F

The pair (Ω,F) is called a measurable space.

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Probability Spaces

DefinitionA Probability measure P on a measurable space (Ω,F) is afunction P : F → [0, 1] such that

P(∅) = 0, P(Ω) = 1

if A1,A2, . . . ∈ F and Ai∞i=1 is disjoint then

P

( ∞⋃i=1

Ai

)=

∞∑i=1

P(Ai)

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Random Variable

DefinitionIf (Ω,F,P) is a given probability space, then a functionY : Ω→ Rn is called F-measurable if

Y−1(U) := ω ∈ Ω; Y(ω) ∈ U ∈ F

for all open sets U ∈ Rn(or, equivalently, for all Borel setsU ⊂ Rn).In the following we let (Ω,F,P) denote a given completeprobability space.A random variable X is an F-measurable function X : Ω→ Rn.

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Arbitrage Price of Call Options

A money market with interest rate r

$1 invested in the money market ⇒ $(1+ r) in the next period

d < (1 + r) < u

European call option with strike price K > 0 and expiration time 1

this option confers the right to buy the stock at time 1 for Kdollars

⇒ Compute the arbitrage price of the call option at time zero, V0.

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Arbitrage Price of Call Options

Suppose at time zero you sell the call option for V0 dollars.

ω1 = H ⇒ you should pay off (uS0 − K)+

ω1 = T ⇒ you should pay off (dS0 − K)+

At time 0, we don’t know the value of ω1.

Making replicating portfolio:

V0 − ∆0S0 dollars in the money market.

∆0 shares of stock

⇒ the value of the portfolio is V0 at time 0.⇒ the value should be (S1 − K)

+ at time 1.

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Arbitrage Price of Call Options

Suppose at time zero you sell the call option for V0 dollars.

ω1 = H ⇒ you should pay off (uS0 − K)+

ω1 = T ⇒ you should pay off (dS0 − K)+

At time 0, we don’t know the value of ω1.Making replicating portfolio:

V0 − ∆0S0 dollars in the money market.

∆0 shares of stock

⇒ the value of the portfolio is V0 at time 0.⇒ the value should be (S1 − K)

+ at time 1.

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Arbitrage Price of Call Options

Thus,V1(H) = ∆0S1(H) + (1 + r)(V0 − ∆0S0) (1)

V1(T) = ∆0S1(T) + (1 + r)(V0 − ∆0S0) (2)

Subtracting (2) from (1), we obtain

V1(H) − V1(T) = ∆0(S1(H) − S1(T)), (3)

so that

∆0 =V1(H) − V1(T)

S1(H) − S1(T)(4)

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Arbitrage Price of Call Options

Thus,V1(H) = ∆0S1(H) + (1 + r)(V0 − ∆0S0) (1)

V1(T) = ∆0S1(T) + (1 + r)(V0 − ∆0S0) (2)

Subtracting (2) from (1), we obtain

V1(H) − V1(T) = ∆0(S1(H) − S1(T)), (3)

so that

∆0 =V1(H) − V1(T)

S1(H) − S1(T)(4)

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Arbitrage Price of Call Options

Substitute (4) into either (1) or (2) and solve for V0;

V0 =1

1 + r

[1 + r− d

u− dV1(H) +

u− (1 + r)

u− dV1(T)

](5)

Simply,

V0 =1

1 + r[pV1(H) + qV1(T)] (6)

where

p =1 + r− d

u− d, q =

u− (1 + r)

u− d= 1 − p

⇒ We can regard them as probabilities of H and T, respectively.⇒ They are the risk-neutral probabilities.

Stochastic Calculus, Application of Real Analysis in Finance

BINOMIAL ASSET PRICING MODEL

Arbitrage Price of Call Options

Substitute (4) into either (1) or (2) and solve for V0;

V0 =1

1 + r

[1 + r− d

u− dV1(H) +

u− (1 + r)

u− dV1(T)

](5)

Simply,

V0 =1

1 + r[pV1(H) + qV1(T)] (6)

where

p =1 + r− d

u− d, q =

u− (1 + r)

u− d= 1 − p

⇒ We can regard them as probabilities of H and T, respectively.⇒ They are the risk-neutral probabilities.

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

Contents

1 BINOMIAL ASSET PRICING MODEL

2 Stochastic Calculus

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

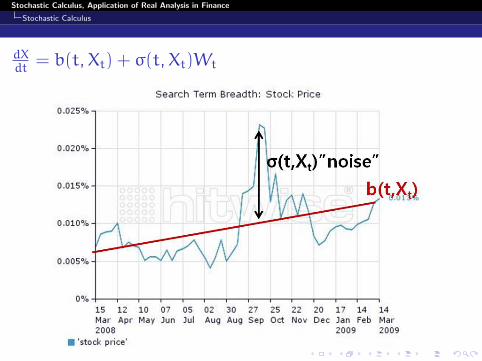

Problem - The Movement of Stock Price

A risky investment(e.g. a stock), where the price X(t) per unit attime t satisfies a stochastic differential equation:

dX

dt= b(t,Xt) + σ(t,Xt) · ”noise”, (7)

where b and σ are some given functions.

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

dXdt

= b(t,Xt) + σ(t,Xt)Wt

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

dXdt

= b(t,Xt) + σ(t,Xt)Wt

Based on many situations, one is led to assume that the ”noise”,Wt, has these properties:

t1 6= t2 ⇒ Wt1 and Wt2 are independent.

Wt is stationary, i.e. the (joint)distribution ofWt1+t, . . . ,Wtk+t does not depend on t.

E[Wt] = 0 for all t.

Let 0 = t0 < t1 < · · · < tm = t and consider a discrete version of(7):

Xk+1 − Xk = b(tk,Xk)∆tk + σ(tk,Xk)Wk∆tk, (8)

where Xj = X(tj), Wk =Wtk , ∆tk = tk+1 − tk.

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

dXdt

= b(t,Xt) + σ(t,Xt)Wt

Based on many situations, one is led to assume that the ”noise”,Wt, has these properties:

t1 6= t2 ⇒ Wt1 and Wt2 are independent.

Wt is stationary, i.e. the (joint)distribution ofWt1+t, . . . ,Wtk+t does not depend on t.

E[Wt] = 0 for all t.

Let 0 = t0 < t1 < · · · < tm = t and consider a discrete version of(7):

Xk+1 − Xk = b(tk,Xk)∆tk + σ(tk,Xk)Wk∆tk, (8)

where Xj = X(tj), Wk =Wtk , ∆tk = tk+1 − tk.

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

dXdt

= b(t,Xt) + σ(t,Xt)Wt

Replace Wk∆k by ∆Vk = Vtk+1 − Vtk , where Vtt>0 is somesuitable stochastic process.

It can be easily proved that Vtt>0 satisfies the four propertieswhich define the standard Brownian Motion, Btt>0:

B0 = 0.

The increments of Bt are independent; i.e. for any finite set oftimes 0 6 t1 < t2 < · · · < tn < T the random variablesBt2 − Bt1 ,Bt3 − Bt2 , . . . ,Btn − Btn−1 are independent.

For any 0 6 s 6 t < T the increment Bt − Bs has the Gaussiandistribution with mean 0 and variance t− s.

For all w in a set of probability one, Bt(w) is a continuousfunction of t.

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

dXdt

= b(t,Xt) + σ(t,Xt)Wt

Replace Wk∆k by ∆Vk = Vtk+1 − Vtk , where Vtt>0 is somesuitable stochastic process.It can be easily proved that Vtt>0 satisfies the four propertieswhich define the standard Brownian Motion, Btt>0:

B0 = 0.

The increments of Bt are independent; i.e. for any finite set oftimes 0 6 t1 < t2 < · · · < tn < T the random variablesBt2 − Bt1 ,Bt3 − Bt2 , . . . ,Btn − Btn−1 are independent.

For any 0 6 s 6 t < T the increment Bt − Bs has the Gaussiandistribution with mean 0 and variance t− s.

For all w in a set of probability one, Bt(w) is a continuousfunction of t.

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

dXdt

= b(t,Xt) + σ(t,Xt)Wt

Replace Wk∆k by ∆Vk = Vtk+1 − Vtk , where Vtt>0 is somesuitable stochastic process.It can be easily proved that Vtt>0 satisfies the four propertieswhich define the standard Brownian Motion, Btt>0:

B0 = 0.

The increments of Bt are independent; i.e. for any finite set oftimes 0 6 t1 < t2 < · · · < tn < T the random variablesBt2 − Bt1 ,Bt3 − Bt2 , . . . ,Btn − Btn−1 are independent.

For any 0 6 s 6 t < T the increment Bt − Bs has the Gaussiandistribution with mean 0 and variance t− s.

For all w in a set of probability one, Bt(w) is a continuousfunction of t.

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

dXdt

= b(t,Xt) + σ(t,Xt)Wt

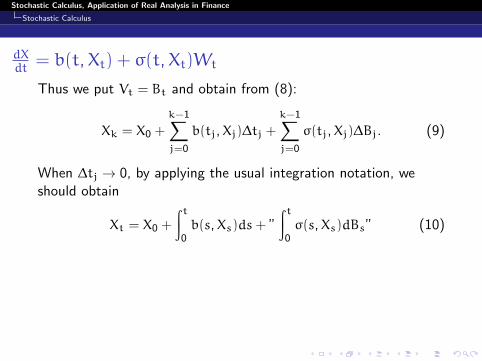

Thus we put Vt = Bt and obtain from (8):

Xk = X0 +

k−1∑j=0

b(tj,Xj)∆tj +k−1∑j=0

σ(tj,Xj)∆Bj. (9)

When ∆tj → 0, by applying the usual integration notation, weshould obtain

Xt = X0 +

∫t0b(s,Xs)ds+ ”

∫t0σ(s,Xs)dBs” (10)

Now, in the remainder of this chapter we will prove the existence,in a certain sense, of

”

∫t0f(s,ω)dBs(ω)”

where Bt(ω) is 1-dim’l Brownian motion.

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

dXdt

= b(t,Xt) + σ(t,Xt)Wt

Thus we put Vt = Bt and obtain from (8):

Xk = X0 +

k−1∑j=0

b(tj,Xj)∆tj +k−1∑j=0

σ(tj,Xj)∆Bj. (9)

When ∆tj → 0, by applying the usual integration notation, weshould obtain

Xt = X0 +

∫t0b(s,Xs)ds+ ”

∫t0σ(s,Xs)dBs” (10)

Now, in the remainder of this chapter we will prove the existence,in a certain sense, of

”

∫t0f(s,ω)dBs(ω)”

where Bt(ω) is 1-dim’l Brownian motion.

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

dXdt

= b(t,Xt) + σ(t,Xt)Wt

Thus we put Vt = Bt and obtain from (8):

Xk = X0 +

k−1∑j=0

b(tj,Xj)∆tj +k−1∑j=0

σ(tj,Xj)∆Bj. (9)

When ∆tj → 0, by applying the usual integration notation, weshould obtain

Xt = X0 +

∫t0b(s,Xs)ds+ ”

∫t0σ(s,Xs)dBs” (10)

Now, in the remainder of this chapter we will prove the existence,in a certain sense, of

”

∫t0f(s,ω)dBs(ω)”

where Bt(ω) is 1-dim’l Brownian motion.

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

Construction of the Ito Integral

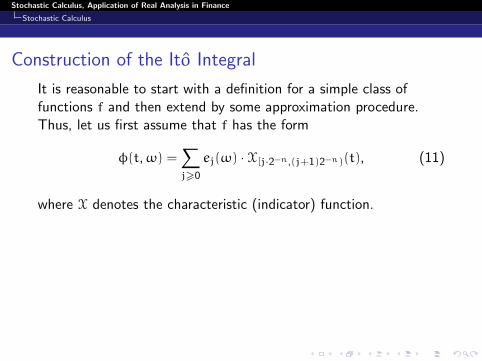

It is reasonable to start with a definition for a simple class offunctions f and then extend by some approximation procedure.Thus, let us first assume that f has the form

φ(t,ω) =∑j>0

ej(ω) · X[j·2−n,(j+1)2−n)(t), (11)

where X denotes the characteristic (indicator) function.

For such functions it is reasonable to define∫t0φ(t,ω)dBt(ω) =

∑j>0

ej(ω)[Btj+1 − Btj ](ω). (12)

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

Construction of the Ito Integral

It is reasonable to start with a definition for a simple class offunctions f and then extend by some approximation procedure.Thus, let us first assume that f has the form

φ(t,ω) =∑j>0

ej(ω) · X[j·2−n,(j+1)2−n)(t), (11)

where X denotes the characteristic (indicator) function.For such functions it is reasonable to define∫t

0φ(t,ω)dBt(ω) =

∑j>0

ej(ω)[Btj+1 − Btj ](ω). (12)

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

Construction of the Ito Integral

In general, as we did in Real Analysis, it is natural to approximatea given function f(t,ω) by∑

j

f(t∗j ,ω) · X[tj,tj+1)(t)

where the points t∗j belong to the intervals [tj, tj+1], specifically in

Ito Integral, t∗j = tj, and then define∫t0 f(s,ω)dBs(ω).

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

Construction of the Ito Integral

DefinitionThe Ito integral of f is defined by∫t

0f(s,ω)dBs(ω) = lim

n→∞∫t0φn(s,ω)dBs(ω) (limit in L2(P))

(13)where φn is a sequence of elementary functions such that

E

[∫t0(f(s,ω) − φn(s,ω))2dt

]→ 0 as n→∞. (14)

Note that such a sequence φn satisfying (14) exists.

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

Example

∫t0BsdBs =

1

2B2t −

1

2t.

(proof)

Put φn(s,ω) =∑Bj(ω) · X[tj,tj+1)(s), where Bj = Btj . Then

E

[∫t0(φn − Bs)

2ds

]= E

∑j

∫tj+1

tj

(Bj − Bs)2ds

=

∑j

∫tj+1

tj

(s− tj)ds

=∑ 1

2(tj+1 − tj)

2 → 0 as ∆tj → 0

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

Example

∫t0BsdBs =

1

2B2t −

1

2t.

(proof)Put φn(s,ω) =

∑Bj(ω) · X[tj,tj+1)(s), where Bj = Btj . Then

E

[∫t0(φn − Bs)

2ds

]= E

∑j

∫tj+1

tj

(Bj − Bs)2ds

=

∑j

∫tj+1

tj

(s− tj)ds

=∑ 1

2(tj+1 − tj)

2 → 0 as ∆tj → 0

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

Example

∫t0BsdBs =

1

2B2t −

1

2t.

(proof)Put φn(s,ω) =

∑Bj(ω) · X[tj,tj+1)(s), where Bj = Btj . Then

E

[∫t0(φn − Bs)

2ds

]= E

∑j

∫tj+1

tj

(Bj − Bs)2ds

=

∑j

∫tj+1

tj

(s− tj)ds

=∑ 1

2(tj+1 − tj)

2 → 0 as ∆tj → 0

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

Example

∫t0BsdBs = lim

∆tj→0

∫t0φndBs = lim

∆tj→0

∑j

Bj∆Bj.

Now

∆(B2j ) = B2j+1 − B

2j = (Bj+1 − Bj)

2 + 2Bj(Bj+1 − Bj)

= (∆Bj)2 + 2Bj∆Bj,

and therefore,

B2t =∑j

∆(B2j ) =∑j

(∆Bj)2 + 2

∑j

Bj∆Bj

or ∑j

Bj∆Bj =1

2B2t −

1

2

∑j

(∆Bj)2.

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

Example

∫t0BsdBs = lim

∆tj→0

∫t0φndBs = lim

∆tj→0

∑j

Bj∆Bj.

Now

∆(B2j ) = B2j+1 − B

2j = (Bj+1 − Bj)

2 + 2Bj(Bj+1 − Bj)

= (∆Bj)2 + 2Bj∆Bj,

and therefore,

B2t =∑j

∆(B2j ) =∑j

(∆Bj)2 + 2

∑j

Bj∆Bj

or ∑j

Bj∆Bj =1

2B2t −

1

2

∑j

(∆Bj)2.

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

Example

∫t0BsdBs = lim

∆tj→0

∫t0φndBs = lim

∆tj→0

∑j

Bj∆Bj.

Now

∆(B2j ) = B2j+1 − B

2j = (Bj+1 − Bj)

2 + 2Bj(Bj+1 − Bj)

= (∆Bj)2 + 2Bj∆Bj,

and therefore,

B2t =∑j

∆(B2j ) =∑j

(∆Bj)2 + 2

∑j

Bj∆Bj

or ∑j

Bj∆Bj =1

2B2t −

1

2

∑j

(∆Bj)2.

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

Example

∫t0BsdBs = lim

∆tj→0

∫t0φndBs = lim

∆tj→0

∑j

Bj∆Bj.

Now

∆(B2j ) = B2j+1 − B

2j = (Bj+1 − Bj)

2 + 2Bj(Bj+1 − Bj)

= (∆Bj)2 + 2Bj∆Bj,

and therefore,

B2t =∑j

∆(B2j ) =∑j

(∆Bj)2 + 2

∑j

Bj∆Bj

or ∑j

Bj∆Bj =1

2B2t −

1

2

∑j

(∆Bj)2.

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

The Ito Formula

The previous example illustrates that the basic definition of Itointegrals is not very useful when we try to evaluate a given integralas ordinary Riemann integrals without the fundamental theorem ofcalculus plus the chain rule in the explicit calculations.It turns out that it is possible to establish an Ito integral version ofthe chain rule, called the Ito formula.

Stochastic Calculus, Application of Real Analysis in Finance

Stochastic Calculus

The Ito Formula

TheoremLet Xt be an Ito process given by

dXt = udt+ vdBt.

Let g(t, x) ∈ C2([0,∞)× R). Then Yt = g(t,Xt) is again an Itoprocess, and

dYt =∂g

∂t(t,Xt)dt+

∂g

∂x(t,Xt)dXt +

1

2

∂2g

∂x2(t,Xt) · (dXt)2, (15)

where (dXt)2 = (dXt) · (dXt) is computed according to the rules