At Stonetrust Commercial Insurance Company (Stonetrust), it is our mission to be a professional and capable partner to our producers and policyholders while providing workers’ compensation insurance coverage at competitive rates. Stonetrust seeks to develop a working relationship with each of our producers in selecting and servicing risks that place a priority on workplace safety and claims cost containment.

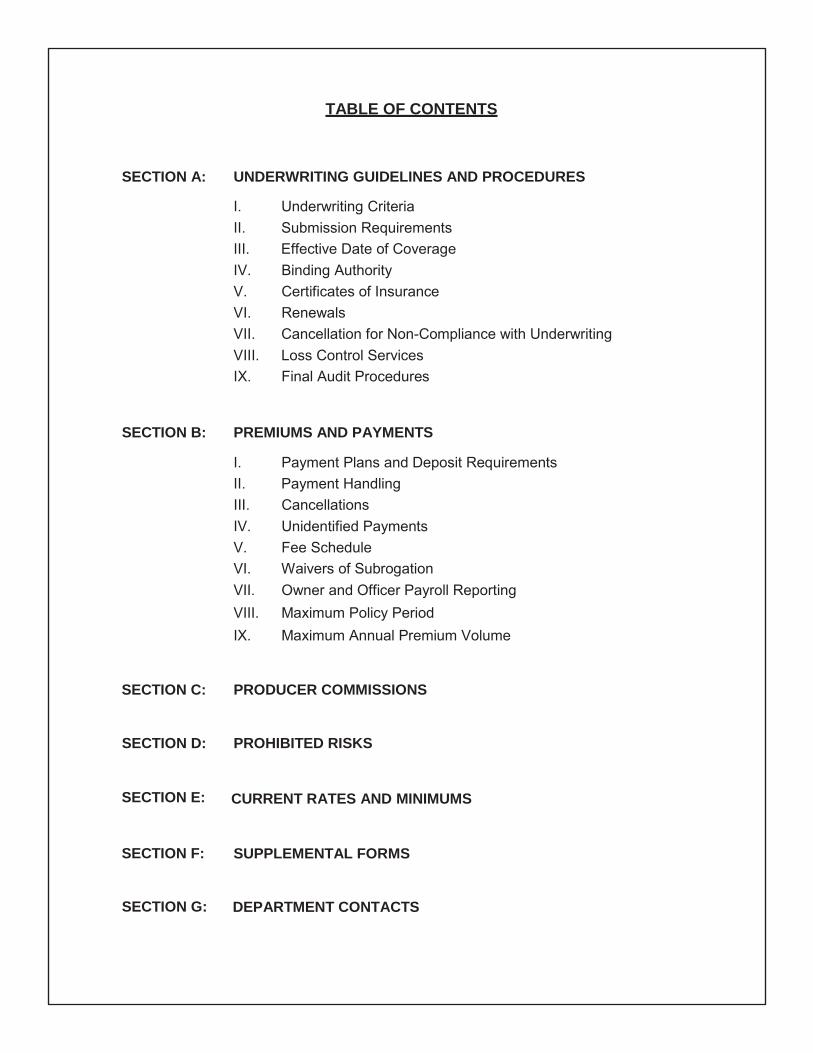

TABLE OF CONTENTS

SECTION A: UNDERWRITING GUIDELINES AND PROCEDURES

I. Underwriting Criteria II. Submission Requirements III. Effective Date of Coverage IV. Binding Authority V. Certificates of Insurance VI. Renewals VII. Cancellation for Non-Compliance with Underwriting VIII. Loss Control Services IX. Final Audit Procedures

SECTION B: PREMIUMS AND PAYMENTS

I. Payment Plans and Deposit Requirements II. Payment Handling III. Cancellations IV. Unidentified Payments V. Fee Schedule VI. Waivers of Subrogation VII. Owner and Officer Payroll Reporting VIII. Maximum Policy Period IX. Maximum Annual Premium Volume

SECTION C: PRODUCER COMMISSIONS

SECTION D: PROHIBITED RISKS

SECTION E:

SECTION F:

SECTION G:

CURRENT RATES AND MINIMUMS

SUPPLEMENTAL FORMS

DEPARTMENT CONTACTS

Underwriting Guidelines 1 Effective 6/4/2016

SECTION A

UNDERWRITING GUIDELINES AND PROCEDURES

I. UNDERWRITING CRITERIA

To be eligible for consideration, the risk must meet the following general criteria:

1) Must be an eligible class of business

2) Is willing to establish a loss prevention program and demonstrates a commitment toward safety

3) Has operated as a business for at least three years in subject line of work; if less than three years, must have five years experience in same industry

4) If no prior loss history, demonstrates good financial condition and credit rating

5) Minimum annual premium as filed with the governing body for their state (see Section E, Current Rates and Minimums)

6) No exposures outside Louisiana, Arkansas, Mississippi, Oklahoma or Texas

7) No seasonal operations or short term operations

8) No risk having more than 60% of work performed by subcontractors

9) Casual labor is assigned to appropriate class code

II. SUBMISSION REQUIREMENTS

1) Completed ACORD application with FEIN (and social security numbers with new

ventures)

2) Currently valued company loss runs for five policy periods. If five years of loss information is not available, three is acceptable. Accounts with a loss ratio in excess of 50% may be considered after detailed review.

3) NCCI experience rating worksheet

4) If risk is trucking, convenience store, restaurant, hotel/motel, contractor, EMS, or has automobile exposure, should include appropriate supplemental form (see Section H, Supplemental Forms)

5) For new ventures, an agent recommendation is required. Must have experience in their line of business, with appropriate financial and management skills.

6) Non-election form must be completed by all excluded owners/officers

Your submission can be easily uploaded through our online agency portal, EZStone.. You can also email your submission directly to your assigned underwriter or to the agency portal ([email protected]) or (fax it to (866) 923-1871. Our underwriting staff will review your submission immediately and respond the same day. Policies will be issued within two weeks of binding.

Coverage may be effective on the requested effective date or the date notice to bind coverage is received from the producer. Coverage cannot be backdated.

IV. BINDING AUTHORITY

Producers do not have binding authority. A risk is considered eligible for coverage once it is quoted by Stonetrust and subject to the conditions listed on the quote sheet. To request that coverage be bound, the producer must notify us in writing by letter, fax, email, or online. Coverage is bound upon notification to the producer by Stonetrust and is subject to receipt of the signed application, security deposit/down payment, and other required information within 10 days of the binder being issued.

V. CERTIFICATES OF INSURANCE

The producer is responsible for issuance and accuracy of Certificates of Insurance.

VI. RENEWALS

A renewal invoice will be sent to the policyholder, with a copy to the producer, approximately 45 days prior to the policy’s renewal date. The renewal invoice includes a section for the policyholder to complete to indicate whether they intend to renew the policy or not. If the policyholder is on an installment billing plan and elects to renew coverage, he must check the “renew” box, sign and date the invoice, and mail it along with payment to be received by the renewal date shown on the invoice. If the policyholder is on a monthly self-audit reporting plan and elects to renew coverage, no payment is currently due but the policyholder must check the “renew” box, sign, date, and return the invoice to be received by the renewal date. If the policyholder does not return the renewal invoice indicating that coverage is to be renewed, along with any required payment, by the renewal date shown on the invoice, coverage terminates on the renewal date.

VII. CANCELLATION FOR NON-COMPLIANCE WITH UNDERWRITING

Stonetrust may cancel an insured for underwriting reasons, including:

1) Failure to comply with audit requirements 2) Failure to maintain acceptable payment history 3) Failure to comply with safety and loss control requirements and recommendations 4) Failure to maintain an acceptable loss ratio 5) Failure to submit required applications, supplemental applications, or forms

requested 6) Failure to comply with claims reporting and handling procedures 7) Failure to maintain an acceptable minimum premium 8) Unfavorable risk evaluation by loss control 9) Fraudulently producing or altering a Certificate of Insurance

Underwriting Guidelines 3 Effective 6/4/2016

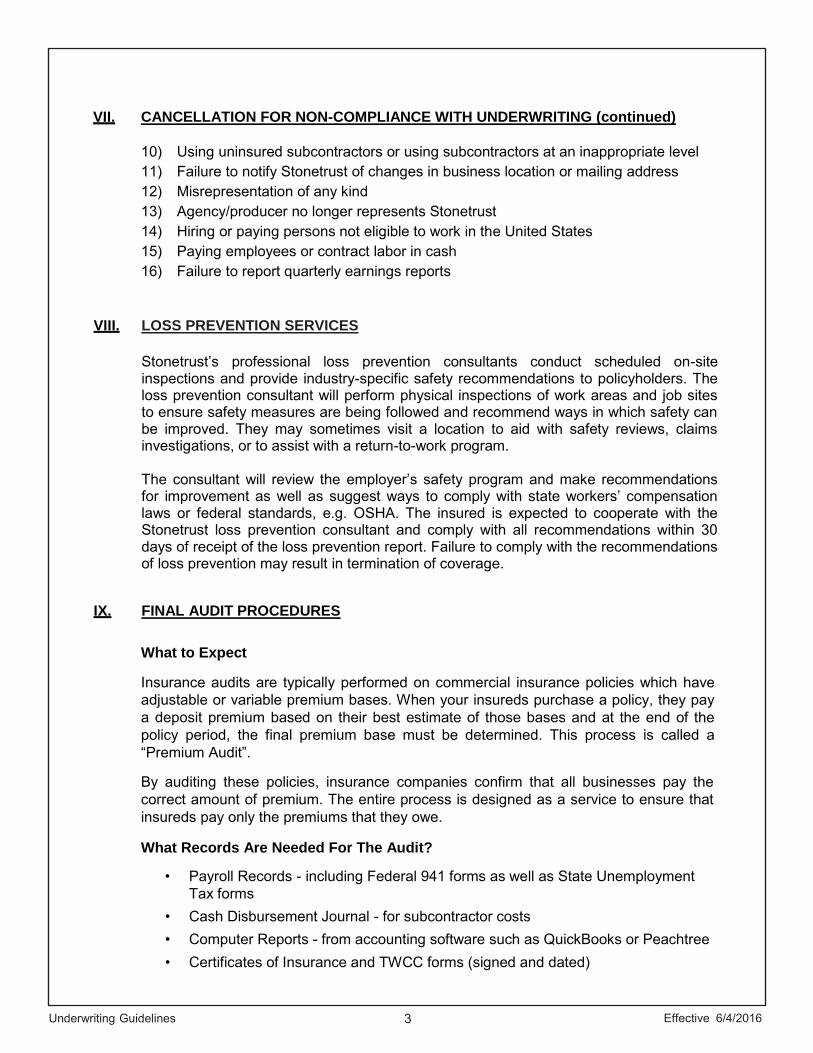

VII. CANCELLATION FOR NON-COMPLIANCE WITH UNDERWRITING (continued)

10) Using uninsured subcontractors or using subcontractors at an inappropriate level 11) Failure to notify Stonetrust of changes in business location or mailing address 12) Misrepresentation of any kind 13) Agency/producer no longer represents Stonetrust 14) Hiring or paying persons not eligible to work in the United States 15) Paying employees or contract labor in cash 16) Failure to report quarterly earnings reports

VIII. LOSS PREVENTION SERVICES

Stonetrust’s professional loss prevention consultants conduct scheduled on-site inspections and provide industry-specific safety recommendations to policyholders. The loss prevention consultant will perform physical inspections of work areas and job sites to ensure safety measures are being followed and recommend ways in which safety can be improved. They may sometimes visit a location to aid with safety reviews, claims investigations, or to assist with a return-to-work program.

The consultant will review the employer’s safety program and make recommendations for improvement as well as suggest ways to comply with state workers’ compensation laws or federal standards, e.g. OSHA. The insured is expected to cooperate with the Stonetrust loss prevention consultant and comply with all recommendations within 30 days of receipt of the loss prevention report. Failure to comply with the recommendations of loss prevention may result in termination of coverage.

IX. FINAL AUDIT PROCEDURES

What to Expect

Insurance audits are typically performed on commercial insurance policies which have adjustable or variable premium bases. When your insureds purchase a policy, they pay a deposit premium based on their best estimate of those bases and at the end of the policy period, the final premium base must be determined. This process is called a “Premium Audit”.

By auditing these policies, insurance companies confirm that all businesses pay the correct amount of premium. The entire process is designed as a service to ensure that insureds pay only the premiums that they owe.

What Records Are Needed For The Audit?

• Payroll Records - including Federal 941 forms as well as State Unemployment Tax forms

• Cash Disbursement Journal - for subcontractor costs • Computer Reports - from accounting software such as QuickBooks or Peachtree • Certificates of Insurance and TWCC forms (signed and dated)

Underwriting Guidelines 4 Effective 6/4/2016

IX. FINAL AUDIT PROCEDURES (continued)

Tips on Reducing Premium Payments • Have the proper person available to assist the auditor and answer their questions. • If employees are paid overtime, properly summarize overtime paid by individual

and class code. • Construction companies should maintain payroll records to show time spent in

different types of work. • The use of subcontractors or independent contractors requires certificates of

workers' compensation insurance from each subcontractor or independent contractor.

• Identify for the auditor any individuals who perform strictly clerical office duties, strictly outside sales duties, draftsmen, or strictly drivers.

• Keep a record of tips declared by restaurant employees.

When Will the Audit Be Completed?

Soon after the insured’s policy expires (or is canceled). Normally, they will be contacted within 30 days in regards to completing the Premium Audit. Most audits can be completed in a fairly short period of time (less than an hour) as long the proper records are in order beforehand.

How Will the Audit Be Completed?

It is necessary for the auditor to ask questions about the insured’s records and business operations. If they cannot be present, it is extremely important for someone to be available that is familiar with the specifics of their entire operation and the job duties of all employees. If the auditor is directed to an outside accountant, he or she will obtain as much of the necessary information from them as possible, but will likely still have to speak with the insured for additional information.

Frequently Asked Questions

Q: What gives you the right to look at the insured’s books and records?

A: The insurance policy is a legally binding contract between the insured and their insurance carrier. One of the conditions of the contract states, "You will let us examine and audit all of your records that relate to this policy."

Q: The insured works alone. The auditor has requested payroll records and since they

have no employees, they have no payroll records. Is the audit still necessary?

A: Yes, the auditor will need to verify that the insured does indeed work alone. To do that, he/she will look at disbursement records, check stubs, or possibly income tax returns. The auditor is also required to look for and review the relationship with any independent contractors who the insured may have used during the policy period.

Q: The insured canceled their policy and no longer has insurance with your company.

Do they need to be audited?

A: Yes, remember the purpose of the audit is to review their actual business activity for a prior period.

Underwriting Guidelines 5 Effective 6/4/2016

SECTION B

PREMIUMS AND PAYMENTS

I. PAYMENT PLANS AND DEPOSIT REQUIREMENTS

1) Stonetrust currently offers various payment options allowing for the flexibility of paying the full annual premium upfront or spreading it out monthly. Stonetrust does not offer quarterly installment or quarterly self-reporting payroll billing plans. A $5.00 install- ment fee is charged for each monthly self audit billing and premium installment billing. The fee is not charged on the security deposit billing or the premium deposit billing.

Plan Description Deposit Required

A1 Annual Pay - 1 Installment 100% due at inception A2 Annual Pay - 2 Installments 50% down; 50% due in 30 days A3 Annual Pay - 3 Installments 34% down; 33% due in 30 and 60 days 1 Monthly Self-Reporting 25% down; security deposit 2 Monthly Self-Reporting 10% down; security deposit 3 Nine (9) Equal Installments 25% down; premium deposit 4 Nine (9) Equal Installments 10% down; premium deposit

2) If an account’s annual premium is $1,500 or less, only the annual payment options

are available.

3) Accounts with non-seasonal payrolls should be placed on an installment billing payment plan, regardless of the annual premium size.

4) Accounts with seasonal payrolls and generating more than $10,000 in annual premium can be placed on monthly self-reporting invoicing.

II. PAYMENT HANDLING

Payments should be mailed to the following locations:

If payment has not been received on or before the due date shown on the invoice, a notice of policy cancellation will be issued. This notice will also reflect a cancellation fee of $50.00 added to the minimum amount due.

Underwriting Guidelines 6 Effective 6/4/2016

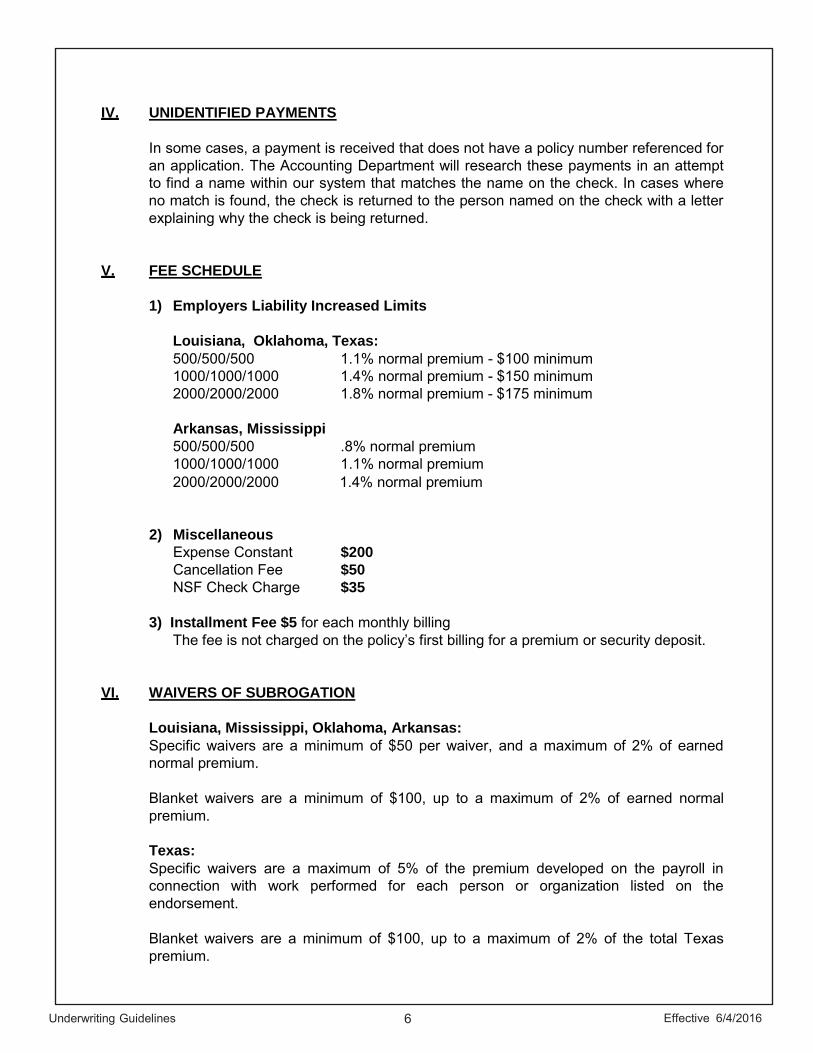

IV. UNIDENTIFIED PAYMENTS

In some cases, a payment is received that does not have a policy number referenced for an application. The Accounting Department will research these payments in an attempt to find a name within our system that matches the name on the check. In cases where no match is found, the check is returned to the person named on the check with a letter explaining why the check is being returned.

V. FEE SCHEDULE

1) Employers Liability Increased Limits

Louisiana, Oklahoma, Texas: 500/500/500 1.1% normal premium - $100 minimum 1000/1000/1000 1.4% normal premium - $150 minimum 2000/2000/2000 1.8% normal premium - $175 minimum

Arkansas, Mississippi 500/500/500 .8% normal premium 1000/1000/1000 1.1% normal premium 2000/2000/2000 1.4% normal premium

3) Installment Fee $5 for each monthly billing The fee is not charged on the policy’s first billing for a premium or security deposit.

VI. WAIVERS OF SUBROGATION

Louisiana, Mississippi, Oklahoma, Arkansas: Specific waivers are a minimum of $50 per waiver, and a maximum of 2% of earned normal premium.

Blanket waivers are a minimum of $100, up to a maximum of 2% of earned normal premium.

Texas: Specific waivers are a maximum of 5% of the premium developed on the payroll in connection with work performed for each person or organization listed on the endorsement.

Blanket waivers are a minimum of $100, up to a maximum of 2% of the total Texas premium.

Underwriting Guidelines 7 Effective 6/4/2016

VII. OWNER AND OFFICER PAYROLL REPORTING

Below are the National Council on Compensation Insurance (NCCI) minimum and maximum payrolls for business owners and officers included for coverage. Locate the appropriate state and verify the current effective date.

NOTE: NCCI minimum and maximum payrolls change frequently so please check

our website at www.stonetrustinsurance.com/payroll.html for updates.

VIII. MAXIMUM POLICY PERIOD

The maximum policy period is one year. Stonetrust will issue a policy for a term shorter than one year in order to synchronize the policyholder’s NCCI experience modifier anniversary rating date with the policy’s coverage dates. In this case, Stonetrust first issues a short term policy and then at first renewal, issues a one year term policy. For example, John Doe Enterprises, Inc. is experienced rated with NCCI with an anniversary rating date of July 1 each year. On March 15, 2008, John Doe Enterprises, Inc.’s application is approved and coverage bound. The first policy’s term will be March 15, 2008 to June 30, 2008. The policy would then renew on July 1, 2008 for a full one year term of July 1, 2008 through June 30, 2009.

IX. STONETRUST MAXIMUM ANNUAL PREMIUM VOLUME

The maximum annual “net written premium” volume shall at no time exceed three (3) times “surplus as regards policyholders”, as measured at December 31 of each calendar year, and as reported by Stonetrust Commercial Insurance Company in its annual statutory statement filed with the Louisiana Commissioner of Insurance. The terms “net written premium” and “surplus as regards policyholders” shall retain the same meaning as in the annual statutory statement.

Producer commissions are paid on collected normal earned premium on new and renewal business via monthly commission statements from Stonetrust. Commissions are not paid on security deposits; on any fee, including but not limited to, those charged for installment payment plans, NSF checks, and policy cancellation and reinstatement; or on any premium collected for Stonetrust by, or on behalf of, the company’s collection department.

I. 2016 NEW BUSINESS COMMISSION RATE

In 2016, a commission rate of 10% will be paid on all new business written with a policy effective date in 2016.

II. MONTHLY COMMISSION SCHEDULE

Producer commission statements are prepared and paid monthly. The Producer’s base commission rate is based on the Annual Total Net Collected Premium Schedule and is reviewed for changes in January of each year. The actual Annual Total Net Collected Premium amount for the previous year, January 1 through December 31, is used to determine any changes to the Producer’s commission rate for the coming year. New Producers are initially assigned the maximum commission rate of 10%, which is not subject to change until the executed Producer Agreement has been effective for a full year from January 1 through December 31.

Annual Total Net Collected Premium Schedule Commission Rate

Total Net Collected Premium < $50,000 8% Total Net Collected Premium ≥ $50,000 but < $100,000 9% Total Net Collected Premium ≥ $100,000 but < $1,000,000 10%

III. ANNUAL BONUS COMMISSION SCHEDULE

Bonus commissions are paid once a year in the month of January. Bonus commissions are paid to those Producers who generate Annual Total Net Collected Premium in excess of $1,000,000 from January 1 through December 31 of the year just ended.

Annual Total Net Collected Premium Schedule Commission Rate

Total Net Collected Premium ≥ $1,000,000 but < $2,000,000 1% Total Net Collected Premium ≥ $2,000,000 but < $3,000,000 2% Total Net Collected Premium ≥ $3,000,000 3%

Underwriting Guidelines 9 Effective 6/4/2016

SECTION D

PROHIBITED RISKS Applicable to the states of Arkansas, Louisiana, Mississippi, Oklahoma, and Texas

The following risks are specifically excluded:

A) Loss or liability excluded by the Nuclear Incident Exclusion Clause – Liability – Reinsurance and Nuclear Energy Risks Exclusion Clause

B) Operations employing the process of nuclear fission or fusion or handling of radioactive material

C) Manufacturing, production and refining of petroleum and its products D) Gas and Oil drilling operations (on shore or off shore) E) Professional sports teams F) Tunneling operations G) Wrecking or demolition of buildings, structures, or vessels H) The manufacturing, storage, or transportation of fireworks, ammunition, nitroglycerin or

other explosive devices I) Risks in the business of asbestos-related work or work conducive to occupational

disease exposures

J) Risks having Maritime exposures or risks having exposure under the U.S. Longshoremen’s and Harbor Workers’ Compensation Act (USL&H), Jones Act and/or Federal Employees Liability Act

K) Mining either above or below ground L) War and acts of war M) Manufacturing of any pharmaceutical or chemicals N) Amusement Parks, exhibitions including fireworks, carnivals or circuses (not including

batting cages or small, slow-moving, non-adult rides) O) Caissons or coffer dam work, dams, dikes, or locks construction P) Roofing contractors, unless written as part of a General Contractors Workers’

Compensation Policy and then not to exceed 15% of the policy’s payroll Q) Firefighters and Police Officers (not including Police Jury Systems or municipalities with

populations of less than 15,000) R) Fuse Manufacturing S) Transportation of hazardous (nuclear or other) waste or materials T) Railroad operations and construction, except for Sidetrack Agreements U) Stevedoring V) Public Utilities W) Bridge erection (not including small bridges over non-navigable waters, such as a creek) X) Temporary Staffing or Employee Leasing Agencies and Professional Employer

Organizations Y) Nuclear, chemical, and biological contamination Z) Aircraft owned, leased, operated or controlled