39

Commodity Outlook Navigating an economic slowdown, trade wars and geo-political risks December 2019 Strategy Team 1 Ole S. Hansen, Head of Commodity Strategy WWW.ANALYSIS.SAXO

Commodity OutlookNavigating an economic slowdown, trade wars and geo-political risks

December 2019

Strategy Team

1

Ole S. Hansen, Head of Commodity Strategy

WWW.ANALYSIS.SAXO

Saxo Bank

FREE TO SHARE

Page 2

This investment research has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Further it is not subject to any prohibition on dealing ahead of the dissemination of investment research. Saxo Bank, its affiliates or staff, may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives), of any issuer mentioned herein.

None of the information contained herein constitutes an offer (or solicitation of an offer) to buy or sell any currency, product or financial instrument, to make any investment, or to participate in any particular trading strategy. This material is produced for marketing and/or informational purposes only and Saxo Bank A/S and its owners, subsidiaries and affiliates whether acting directly or through branch offices (“Saxo Bank”) make no representation or warranty, and assume no liability, for the accuracy or completeness of the information provided herein. In providing this material Saxo Bank has not taken into account any particular recipient’s investment objectives, special investment goals, financial situation, and specific needs and demands and nothing herein is intended as a recommendation for any recipient to invest or divest in a particular manner and Saxo Bank assumes no liability for any recipient sustaining a loss from trading in accordance with a perceived recommendation. All investments entail a risk and may result in both profits and losses. In particular investments in leveraged products, such as but not limited to foreign exchange, derivatives and commodities can be very speculative and profits and losses may fluctuate both violently and rapidly. Speculative trading is not suitable for all investors and all recipients should carefully consider their financial situation and consult financial advisor(s) in order to understand the risks involved and ensure the suitability of their situation prior to making any investment, divestment or entering into any transaction. Any mentioning herein, if any, of any risk may not be, and should not be considered to be, neither a comprehensive disclosure or risks nor a comprehensive description such risks.

Any expression of opinion may be personal to the author and may not reflect the opinion of Saxo Bank and all expressions of opinion are subject to change without notice (neither prior nor subsequent).

DisclaimerNON-INDEPENDENT INVESTMENT RESEARCH

Engines of Disruption

3

Saxo Bank

FREE TO SHARE

Prepared by Saxo Group Global Strategy team

Althea Spinozzi @KVP_Macro @Dembik_Chris @Steen_Jakobsen @johnjhardy @Eleanor_Creagh @petergarnry @ole_s_hansen

4

Saxo Bank

FREE TO SHARE

1-2 on average...but that’s not the point!

What’s the hit rate?

5

Saxo Bank

FREE TO SHARE

Clients and people were angry and publically ridiculing us

Our most contested OP was gold to plunge in 2013

6

Saxo Bank

FREE TO SHARE

Broke below 1,200 on 27 June 2013

Gold plunged 30% in 2013

7

Saxo Bank

FREE TO SHARE

8

Saxo Bank

FREE TO SHARE

In 2020, the gold rally fizzles and oil rallies – cutting the gold-to-oil ratio in half from 2019 highs.

Reversal of fortune cuts gold-to-oilprice ratio in half

9

Gold begins 2020 hoping that a historic new move higher was set in motion in 2019. The crude oil market, meanwhile, remains worried about demand growth from slower GDP growth rates, as well as fears that longer-term demand may dry up on trade wars and the electrification of cars.

In 2020, the tables are turned on both markets. The gold market rally fizzles out as global central banks ease off the gas on further policy, in a grand admission of the policy error of negative rates. OPEC and Russia, sensing a slowdown in U.S. shale oil production seize the opportunity and announce a major additional cut to their oil production.

Saxo Bank

FREE TO SHARE

Rosneft and Norilsk both jump 50% in response to rising demand for oil and green energy-related metals.

Win-win for Russia on green and black energy

10

In 2020, OPEC and Russia, sensing a slowdown in U.S. shale oil production on lack of investment returns in the sector, seize the opportunity and announce a major additional cut to their oil production. Elsewhere, the long-term policy focus on electrical vehicles and pollution-control devices in cars continues to grow as climate policy commitments deepen all over the developed world.

Russia benefits from the move away from cobalt and toward increasing use of nickel in the EV-battery market. In 2020, nickel demand and price soars and Norilsk Nickel enjoys the tailwind and, like Rosneft, sees its share price advance 50%.

Saxo Bank

FREE TO SHARE

The ratio of the VDE fossil fuel energy ETF to ICLN, a renewable energy ETF, jumps from 7 to 12

In Energy, green is not the new black

11

The oil and gas industry came roaring out of the financial crisis after 2009, returning some 131% from 2008 until the peak in June 2014 as China pulled the world economy out of its historic credit-led recession. Since then, the industry has been hurt by two powerful forces. The first was the advent of US shale gas and rapid strides in globalising natural gas supply chains via LNG. Then came the US shale oil revolution, which saw the US become the world’s largest oil and petroleum liquids producer, dramatically pushing down prices and return on capital.

Saxo Bank

FREE TO SHARE

European banks rise 30% in 2020

ECB folds and hikes rates

When negative deposit rates were first introduced in the euro area, the purpose was to force commercial banks to seek better returns elsewhere in order to stimulate productive investment, which would result in theory in higher productivity and stronger growth. So, what has happened? The investment channel hasn’t really delivered yet, and productivity is still too slow in the eurozone. Looking at key innovative sectors, such as electric vehicles, industrial robots or green investments, the monetary union is still lagging behind Asia, most notably China.

12

Saxo Bank

FREE TO SHARE

Deglobalization triggers sharp move higher in TIPS yields

Trump announces America First Tax to reduce trade deficit

The year 2020 starts with reasonable stability on the trade policy front after the Trump administration and China manage at least a temporary détente on tariffs, currency policy and purchases of agricultural goods. But early in 2020 the US economy struggles for air and US trade deficits with China fail to materially improve, while Chinese purchases of agricultural products can’t realistically increase further. Eyeing polls showing a resounding defeat in the 2020 US Presidential election, Trump quickly grows restive and his administration drums up a new approach in a last-ditch effort to steal back the protectionist narrative: the America First Tax.

13

Saxo Bank

FREE TO SHARE

The 2020 US election puts Democrats in control of the president and both houses of Congress. Big healthcare and pharma stocks collapse 50%

Democrats win a clean sweep in the US 2020 election, driven by women and millennials

The polls going into 2020 don’t look promising for Trump, and nor does the electorate: 2018 mid-term elections and limited 2019 elections in the US showed that voters living in suburbs across the US are turning in droves against the Republican party of Donald J. Trump. Plus, the marginal Trump voter in 2016 and in 2020 is old and white, a demographic that is fading in relative terms.

14

Saxo Bank

FREE TO SHARE

Macro trends impacting markets

Page 15

Killer Dollar – strong US$ hurts global growth

Germany close to recession and in denial…

Negative Yields in Europe has reached their limits

Brexit – the never ending story.. Liberal Dem to win?

US vs. China – A waiting game which China is winning

Saxo Bank

FREE TO SHARE

Biggest decline in growth momentum since 2008South Korea is sending worrying signs…and raising questions about China’s rebound

Page 16

Saxo Bank

FREE TO SHARE

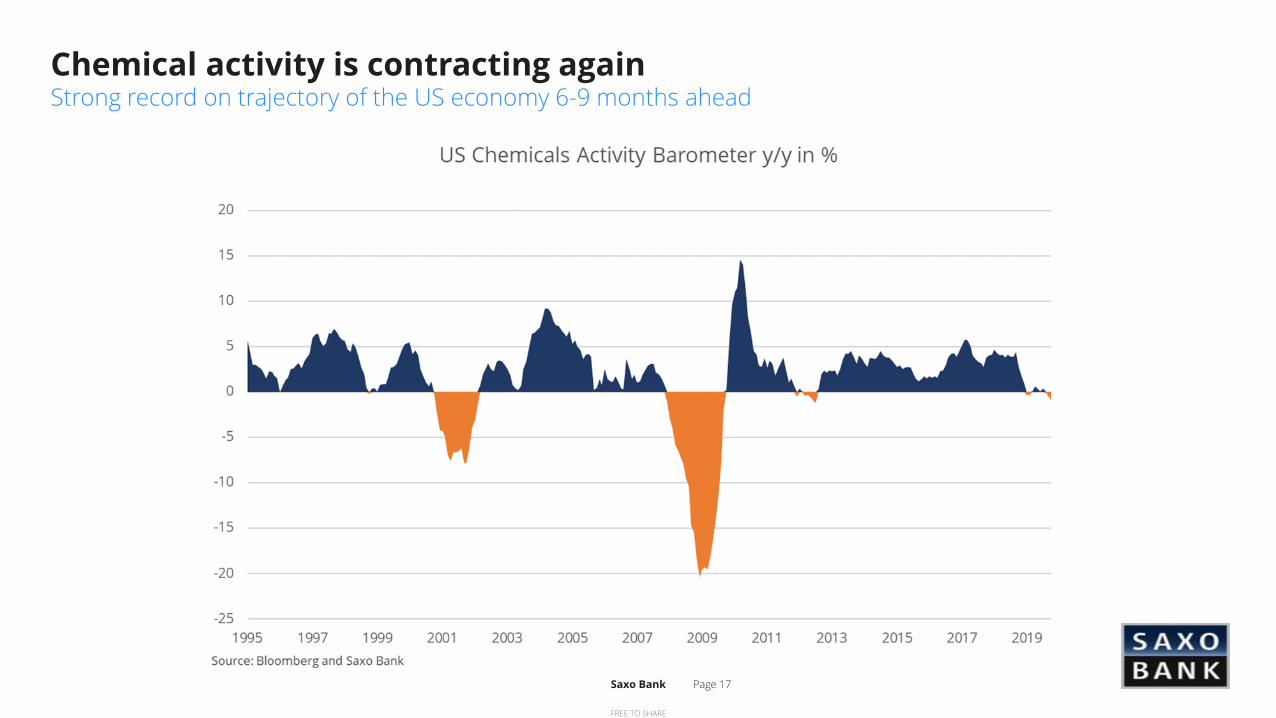

Chemical activity is contracting againStrong record on trajectory of the US economy 6-9 months ahead

Page 17

Saxo Bank

FREE TO SHARE

Record net speculative positioning in VIXUnder the right conditions the market could enter severe negative feedback loop

Page 18

Saxo Bank

FREE TO SHARE

Commodities: Year-to-date performance

19Source: Bloomberg, Saxo Bank

Saxo Bank

FREE TO SHARE

What impacts the price of commodities?

20

• Global economic growth

• Cost of production

• Supply versus demand

• Interest rates and the dollar

• Geopolitical events

• Speculative positioning

• Weather and climate change

Saxo Bank

FREE TO SHARE

COT reports: Why the focus on hedge funds behaviour?

21

The Commitments of Traders (COT) report is issued by the US Commodity Futures Trading Commission (CFTC) every Friday at 15:30 EST with data from the week ending the previous Tuesday. The report breaks down the open interest across major futures markets from bonds, stock index, currencies and commodities. The ICE Futures Europe Exchange issues a similar report, also on Fridays, covering Brent crude oil and gas oil.

In commodities, the open interest is broken into the following categories: Producer/Merchant/Processor/User; Swap Dealers; Managed Money and other.

In financials the categories are Dealer/Intermediary; Asset Manager/Institutional; Managed Money and other.

Our focus is primarily on the behaviour of Managed Money traders such as commodity trading advisors (CTA), commodity pool operators (CPO), and unregistered funds.

They are likely to have tight stops and no underlying exposure that is being hedged. This makes them most reactive to changes in fundamental or technical price developments. It provides views about major trends but also helps to decipher when a reversal is looming.

Saxo Bank

FREE TO SHARE

COT Report: What to look for?

22

Saxo Bank

FREE TO SHARE

COT Report: How to read the table

23

Saxo Bank

FREE TO SHARE

Demand concerns vs. geo-political risks and further production cuts

Source: Saxo Bank

Crude oil: Likely to remain stuck in the lower $60’s

Saxo Bank

FREE TO SHARE

OPEC production slump driven by Saudi Arabia, Iran and Libya

Rystad: OPEC must deepen cuts on record non-OPEC production surge

Saxo Bank

FREE TO SHARE

US shale boom stalls with growth beginning to slow

Falling returns and raised investor concerns causing producers to become selective

Saxo Bank

FREE TO SHARE

COT on crude oil: Buyers return on trade and OPEC optimism

27

Biggest weekly addition (103k) since Dec 2016 last week

Saxo Bank

FREE TO SHARE

NatGas: Record production needs stronger demand

Source: Saxo Bank

Saxo Bank

FREE TO SHARE

Gold pauses after yield collapse driven surge

29

➢ The US dollar

➢ Inflation and inflation expectations

➢ Real interest rates

➢ Opportunity costs (dividends and yields)

➢ Overall commodity price trends

➢ Paper demand through futures and ETFs

➢ Geopolitical/financial risks => tail-end protection

➢ Economic and financial crisis

➢ Elections and political votes

➢ Military attacks/strikes

Q4 Impact Yr to Q3 Impact

Gold -0.3% 15.3%

Silver -2.3% 11.2%

Currencies

Dollar Index -1.5% Positive 3.1% Negative

USDJPY 1.0% Negative -1.8% Positive

Bond yields

Dec-20 Fed Funds Future 0.13 Negative -1.04 Positive

US 2-year 0.03 Negative -0.94 Positive

US 10-year 0.14 Negative -1.05 Positive

US 10-yr Real yield -0.01 Neutral -0.86 Positive

Bonds

High Yield Corp (HYG) 0.1% Neutral 6.8% Positive

Emerging (EMB) -0.6% Neutral 8.2% Positive

Stocks

S&P 500 5.6% Negative 17.3% Negative

EuroStoxx50 3.9% Negative 17.2% Negative

Commodity trend

BBG CI 0.1% Neutral 2.8% Positive

S&P GSCI 3.8% Positive 6.8% Positive

Position change

ETF Holdings (tons) (3) Neutral 314 Positive

Hedge Funds (lots) (29,400) Negative 162300 Positive

Source: Bloomberg, Saxo Bank

Precious Metal Impact Monitor

Saxo Bank

FREE TO SHARE

Gold: What charts are we looking at?

30

Source: www.Focus.de

Saxo Bank

FREE TO SHARE

Speculative futures long cut by 30% while ETF holdings are down < 1.5%…robust and continued buying from Central Banks led by Russia and Turkey

31

Saxo Bank

FREE TO SHARE

Gold short-term focus on $1450/oz and $1520/oz

32Source: Saxo Bank

Spot Gold - Daily

Saxo Bank

FREE TO SHARE

Gold remains bullish above $1380/oz

33

Source: Saxo Bank

➢ The US Federal Reserve is likely to cut rates further

➢ U.S. – China trade war raising recessionary risks

➢ Nominal and real bond yields expected to stay low, in some

places negative

➢ Continued buying by Central Banks looking to diversify and for

some to reduce dependency on the dollar (de-dollarization).

➢ Robust demand for bullion-backed ETF’s. Up 345t y-t-d and just

18t below the December 2012 record of 2572t

➢ The dollar is potentially on its final leg of strength with the

emerging risk of US action to weaken the Greenback

Spot Gold - Monthly

Saxo Bank

FREE TO SHARE

HG Copper trapped between $2.62/lb and $2.72/lbSlowing supply growth and infrastructure vs. trade war and demand concerns

34Source: Saxo Bank

HG Copper - Weekly

Saxo Bank

FREE TO SHARE

2020 theme: Rising food price inflationOversupply (contango) has hurt investment returns since 2008

35 Source: Saxo Bank

Saxo Bank

FREE TO SHARE

Arabica Coffee: Specs are long for the first time since April 2017

Source: Saxo Bank

Saxo Bank

FREE TO SHARE

What’s the options market telling us?1480

Month P/C Strike Last price 5 day vol. Open Interest Expiry

JAN 20 C 1,500 7.20 12,075 11,177 12/26/2019

FEB 20 P 1,475 19.90 4,715 3,282 1/28/2020

JAN 20 P 1,450 2.80 3,439 7,505 12/26/2019

JAN 20 C 1,485 13.20 3,207 1,775 12/26/2019

JAN 20 C 1,550 1.30 3,151 4,232 12/26/2019

JAN 20 P 1,460 5.10 2,931 4,122 12/26/2019

FEB 20 C 1,575 4.50 2,812 10,937 1/28/2020

JAN 20 C 1,540 1.80 2,714 2,333 12/26/2019

MAR 20 P 1,400 2.70 2,614 9,622 2/25/2020

MAR 20 P 1,350 0.80 2,590 3,453 2/25/2020Source: Bloomberg and Saxo Bank

COMEX Gold - Top ten most traded strikes 58.33

Month P/C Strike Last price 5 day vol. Open Interest Expiry

JAN 20 P 55 0.43 15,577 19,226 12/16/2019

JAN 20 P 57 0.86 13,345 10,258 12/16/2019

JAN 20 P 54 0.29 13,242 7,839 12/16/2019

JAN 20 C 60 0.65 10,948 12,557 12/16/2019

JAN 20 C 59 0.98 10,331 8,612 12/16/2019

JAN 20 P 56 0.64 9,998 5,200 12/16/2019

JAN 20 P 53 0.20 9,702 7,085 12/16/2019

JAN 20 P 58 1.01 9,321 3,573 12/16/2019

JAN 20 P 56 0.50 9,237 6,224 12/16/2019

JAN 20 P 58 1.19 8,339 5,545 12/16/2019Source: Bloomberg and Saxo Bank

WTI Crude Oil - Top ten most traded strikes

121.85

Month P/C Strike Last price 5 day vol. Open Interest Expiry

MAR 20 C 130 3.61 10,331 4,157 2/12/2020

MAR 20 C 125 5.08 9,998 3,848 2/12/2020

MAR 20 P 105 0.86 9,702 1,810 2/12/2020

MAR 20 P 123 7.26 9,321 208 2/12/2020

JAN 20 C 125 1.02 9,237 1,555 12/13/2019

MAR 20 P 113 2.55 8,339 320 2/12/2020

JAN 20 C 128 0.52 7,767 807 12/13/2019

MAY 20 C 125 8.02 7,648 1,395 4/9/2020

FEB 20 C 135 1.17 7,353 701 1/10/2020

MAR 20 C 110 13.09 7,100 2,372 2/12/2020Source: Bloomberg and Saxo Bank

Arabica Coffee - Top ten most traded strikes

Month P/C Strike Last price 5 day vol. Open Interest Expiry

JAN 20 C 890 7.38 9,998 6,448 12/27/2019

JAN 20 C 880 12.00 9,702 3,041 12/27/2019

MAR 20 C 890 21.63 9,321 1,897 2/21/2020

JAN 20 P 880 10.13 9,237 6,911 12/27/2019

NOV 20 C 980 26.50 8,339 2,936 10/23/2020

JAN 20 C 910 2.88 7,767 5,067 12/27/2019

MAR 20 C 1,020 1.63 7,648 1,790 2/21/2020

JAN 20 C 930 0.88 7,353 3,630 12/27/2019

JAN 20 P 850 2.00 7,131 2,346 12/27/2019

JAN 20 P 860 3.50 7,100 4,052 12/27/2019Source: Bloomberg and Saxo Bank

CBOT Soybeans - Top ten most traded strikes

Saxo Bank

FREE TO SHARE

Daily Podcasts on Apple, Spotify, SoundCloud & Stitcher

38

Search for Saxo Market Call

FREE TO SHARE

@Ole_S_Hansenwww.tradingfloor.com

Daily commodities updates:

➢ Live morning update at 8:40 CET: morningcall.saxo➢ Replayed on TF called ”From the Floor”➢ Lunchtime update on TF: ”Mid-session Europe”

Thank you

@ole_s_hansen

www.analysis.saxo