28

Streaming Music in 2015: A rapidly growing, maturing and consolidating marketplace Dr. Aram Sinnreich Associate Professor American University June 30, 2015 ram Sinnreich 2015

| Date post: | 07-Aug-2015 |

| Category: |

Business |

| Upload: | aram-sinnreich |

| View: | 303 times |

| Download: | 1 times |

Streaming Music in 2015:A rapidly growing, maturing and consolidating marketplace

Dr. Aram SinnreichAssociate ProfessorAmerican University

June 30, 2015Aram Sinnreich 2015

IntroductionAram Sinnreich, Ph.D.

Currently:

• Associate Professor, American University SOC• Author of 2 books: • Mashed Up (2010)• The Piracy Crusade (2013)

Previously:

• Assistant Professor, Rutgers University SC&I• Co-Founder, Managing Partner, Radar Research• Director, OMD Ignition Factory• Visiting Professor, NYU Media & Culture• Journalist, Wired, MediaPost, Billboard, NY Times• Senior Analyst, Jupiter Research

Aram Sinnreich 2015

Traditional Music and Copyright

Artists/Labels“Masters Rights”

Composers &Publishers

“Publishing Rights”

Retail Radio

• Retailers pay wholesale to labels• Labels pay royalties to artists

• Retailers pay wholesale to labels• Labels pay “mechanical” royalties to publishers• Publishers pay composers

• Broadcasters do NOT pay performance royalties on masters• Promotion and “payola”

• Broadcasters pay royalties to PROs (e.g. BMI)• PROs pay publishers and composers

Aram Sinnreich 2015

Traditional Retail: Value Chain

Aram Sinnreich 2015

Traditional Retail: Revenue Distribution

Aram Sinnreich 2015

Traditional Radio: Value Chain

Aram Sinnreich 2015

Traditional Radio: Revenue Distribution

Aram Sinnreich 2015

New Tech is Blurring the Lines

Programmed(Radio)

On-Demand(Retail)

Compulsory ?????????????????? Contractual

Aram Sinnreich 2015

Subscriptions Have Been Inevitable Since The Turn of the Century

Aram Sinnreich 2015

But the Industry Can Move Slowly

Aram Sinnreich 2015

Analysts are Still Bullish Today

Aram Sinnreich 2015

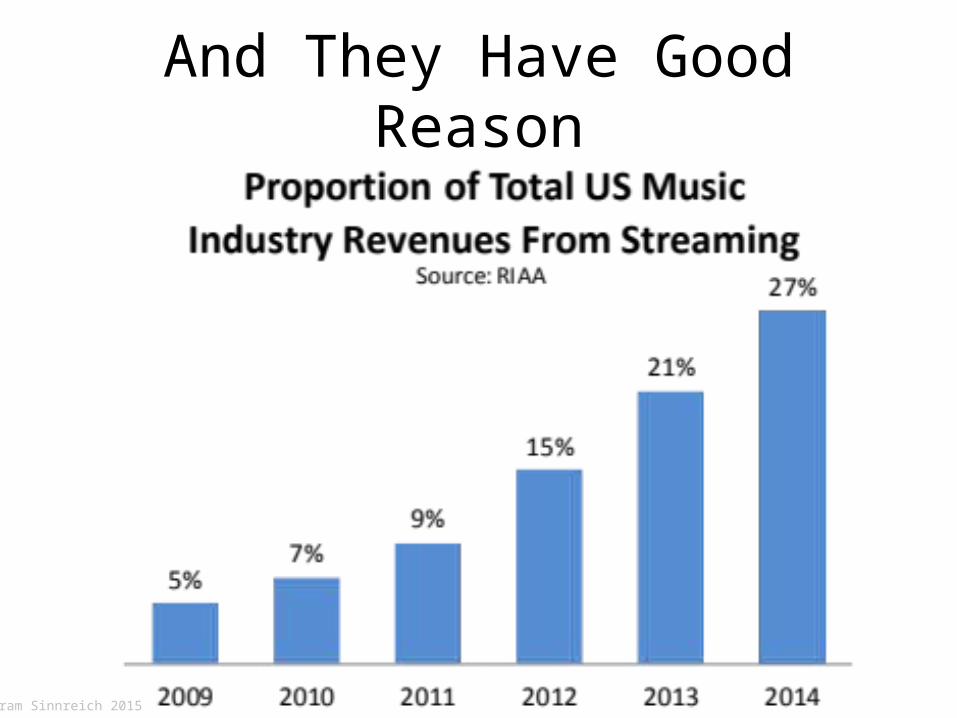

And They Have Good Reason

Aram Sinnreich 2015

2. Digital Music Revenue Distribution

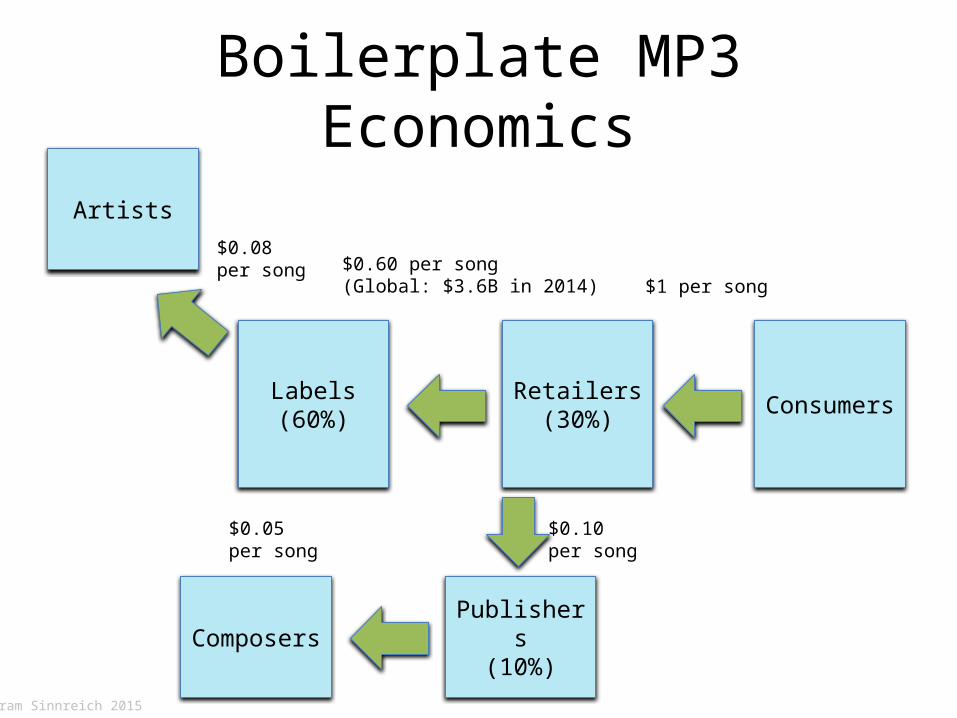

Boilerplate MP3 Economics

ConsumersRetailers(30%)

Labels(60%)

Artists

Publishers(10%)Composers

$1 per song$0.60 per song(Global: $3.6B in 2014)

$0.08per song

$0.10per song

$0.05per song

Aram Sinnreich 2015

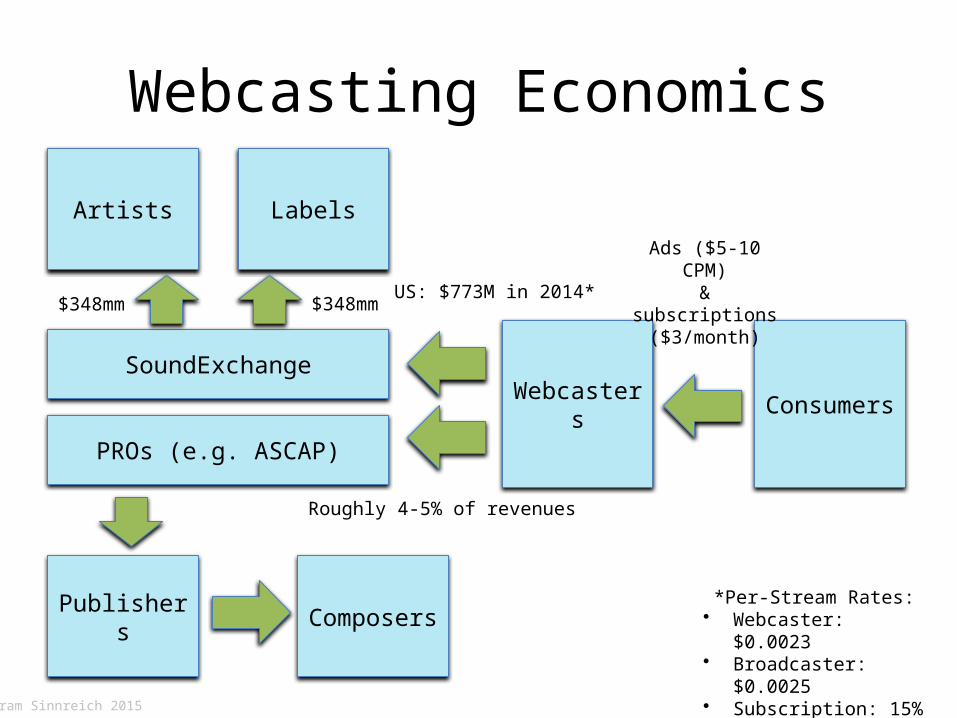

Webcasting Economics

ConsumersWebcasters

LabelsArtists

Publishers Composers

Ads ($5-10 CPM)& subscriptions

($3/month)

PROs (e.g. ASCAP)

SoundExchange

US: $773M in 2014*$348mm $348mm

Roughly 4-5% of revenues

*Per-Stream Rates:• Webcaster: $0.0023• Broadcaster: $0.0025• Subscription: 15% revs

Aram Sinnreich 2015

Boilerplate Subscription Economics

ConsumersRetailers(30%)

Labels(60%)

Artists

Publishers(10%)Composers

10.5% ofrevenues

Consumers generaterevenue both throughads and subscriptions

($5-10/month)

Pro rata or~$0.007

per stream(Global: $1.6B to

labels in 2014)$0.60 per 1,000 streamsEXCEPTIONS:- Recoupment- “Breakage”

5% ofrevenues

PROs(e.g. ASCAP)

OR5-7% ofrevenues

Aram Sinnreich 2015

The Creators’ Cuts

Aram Sinnreich 2015

Take This “Artists’ Rights” Advocate With a Big Grain of Salt

Aram Sinnreich 2015

3. Major Players in

Streaming Subscriptions

Deezer

Launched: 2009Territory: 182 countries (not US)Library: 35M tracksPlatforms: PC/mobile/devicesSubscribers: 6M paying / 16M active monthly usersPrice: $9.99/month (free limited version)Features: Lyrics, curated playlists, exclusive content, HDPartnerships: T-Mobile, Bose, Samsung, Sonos, PepsiRecent news: Acquired Stitcher Radio, 2014

Aram Sinnreich 2015

Rdio

Launched: 2010Territory: 85 countriesLibrary: 32M tracksPlatforms: PC/mobile/devicesSubscribers: N/APrice: $9.99/month (free limited version; $3.99 lite version)Features: Curated playlistsPartnerships: AXS Ticketing, LiveNation, Shazam, BoschRecent news: Amazon Fire TV integration, 2015

Aram Sinnreich 2015

Rhapsody/Napster

Launched: 2001 (spun off 2010)Territory: 32 countriesLibrary: 32M tracksPlatforms: PC/mobile/devicesSubscribers: 2.5MPrice: $9.99/month ($4.99 lite version)Features: Curated playlists, live radioPartnerships: Telefonica, SFR, Vodafone, T-MobileRecent news: Twitter music integration, 2015

Aram Sinnreich 2015

Tidal

Launched: 2014 Territory: 40+ countriesLibrary: 30M tracks, 75k vidsPlatforms: PC/mobile/devicesSubscribers: 40kPrice: $9.99 ($19.99 HD)Features: HD, playlist import, exclusive content, “discovery”Partnerships: Artists, Softbank, RaumfieldRecent news: High-profile defections incl. 2 CEOs in 4 mo.

Aram Sinnreich 2015

Spotify

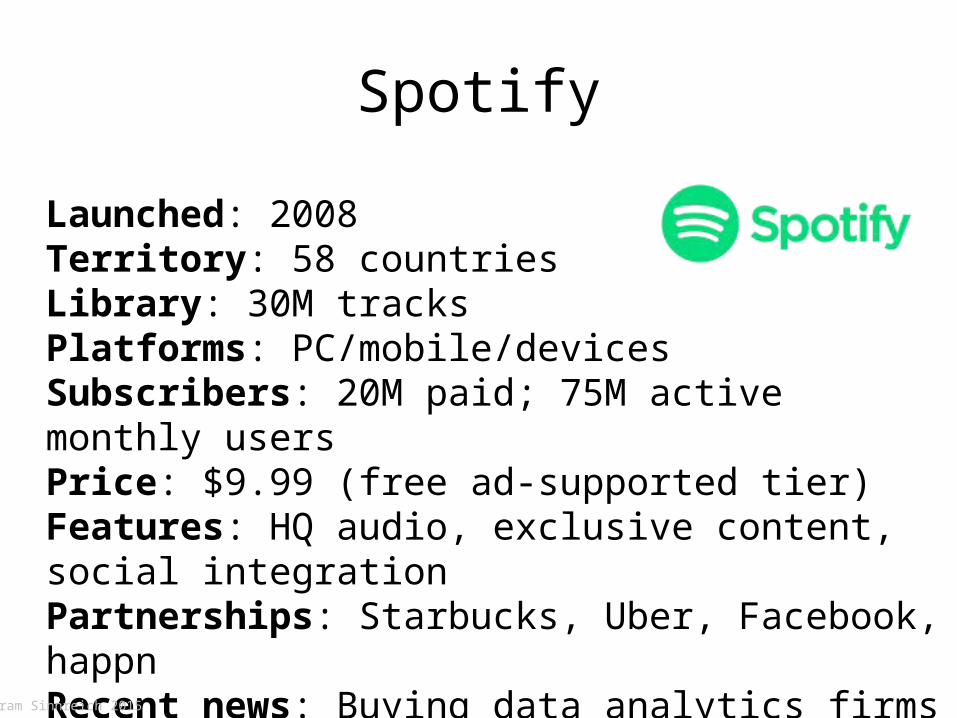

Launched: 2008Territory: 58 countriesLibrary: 30M tracksPlatforms: PC/mobile/devicesSubscribers: 20M paid; 75M active monthly usersPrice: $9.99 (free ad-supported tier)Features: HQ audio, exclusive content, social integrationPartnerships: Starbucks, Uber, Facebook, happnRecent news: Buying data analytics firms including Echo Nest & Seed Scientific

Aram Sinnreich 2015

Apple Music

Launched: Today (June 30, 2015)Territory: 100+ countriesLibrary: “tens of millions” of songsPlatforms: All iOS/OSX devices, PC, AndroidSubscribers: TBDPrice: $9.99 ($14.99 for family membership); 3-month trialFeatures: Exclusive content, Beats 1 radio, artist connectPartnerships: Pitchfork, Rolling Stone, TBDRecent news: Launching today

Aram Sinnreich 2015

Spotify: Strategic PositionSTRENGTHS• Streaming market leader• Market-defining brand• Battle-tested tech & design• Platform agnostic• Fresh cash infusion of $526M,

with an $8.5B valuation

WEAKNESSES• Undiversified business model• Consistent red ink (content costs)• Not much in the way of

proprietary IP or protectable service features

OPPORTUNITIES• Expanding into video

higher ad revenues• B2B partnerships e.g. Starbucks,

Uber, Sony PS3/PS4• Automotive integration

opportunities are growing• Big data!• On track to be default agnostic

platform for music streaming

THREATS• Negative PR from Taylor Swift etc.• Potential market pressure to

eliminate free tier• Market entry by Apple,

accelerating growth from other rivals e.g. Rhapsody

• Fickle consumers, rapidly evolving mobile market

• Mobile bandwidth not priced for heavy streaming

Aram Sinnreich 2015

Apple: Strategic PositionSTRENGTHS• World’s largest music retailer for

over a decade• 800M iTunes accounts worldwide• Deep integration with OS &

hardware• No profit imperative, plenty of

cash

WEAKNESSES• Slow, imperfect integration with

Android and Windows• Late market entry• History of failed or under-

performing music efforts• Few B2B partnerships• Reduced leverage compared to

iTunes market entry

OPPORTUNITIES• Attractive to indie & label artists

due to Connect platform• Deeper integration into OS with

iOS9 & OS X 10.11 (El Capitan)• Explore partnerships w/ retail,

automotive, console devices• Big data w/ Semetric acquisition

THREATS• Market power still contingent on

post-Steve Jobs device innovation• Spotify & others undermining

Apple’s source of leverage• Core download business may

implode faster than streaming grows

Aram Sinnreich 2015

4. Q&A

Let’s talk about royalties, revenues, Taylor Swift & all the rest…