88

UNCDF | FFDO/UN-DESA DRAFT Joint Publication Strengthening Subnational Finance in LDCs Comment now on the draft publication! http://tinyurl.com/draft-publication-comments

| Date post: | 20-Mar-2018 |

| Category: |

Documents |

| Upload: | nguyendang |

| View: | 221 times |

| Download: | 1 times |

UNCDF | FFDO/UN-DESA DRAFT Joint Publication

Strengthening

Subnational Finance in LDCs

Comment now on the draft publication!

http://tinyurl.com/draft-publication-comments

2

Table of Contents

(I) Setting the stage – Municipal finance and the 2030 Agenda for Sustainable Development ...... 4

Localizing the new global development agenda ................................................................................. 4

Financing challenges at the local level ............................................................................................... 5

Special challenges for subnational finance in LDCs........................................................................... 7

Urbanization in LDCs ......................................................................................................................... 8

Challenges to fiscal decentralization efforts in LDCs....................................................................... 11

The global economic context ............................................................................................................ 14

(II) Challenges in raising subnational revenues ............................................................................... 14

Taxation at different levels of government ....................................................................................... 15

The challenges of levying common local taxes: property and business taxes .................................. 19

Perspectives on business taxes .......................................................................................................... 22

Subnational revenue composition in African LDCs ......................................................................... 23

Examples of subnational revenue composition in Asian LDCs ........................................................ 25

Introduction of user charges, fees and licenses ................................................................................. 27

Intergovernmental transfers in LDCs ................................................................................................ 30

Surcharges as a complement to intergovernmental transfers ............................................................ 31

(III) LDC experiences in improving municipal revenue generation .............................................. 33

Lao PDR (1): Land titling as a road to better property taxation ....................................................... 33

Mozambique (1): Facilitating intergovernmental transfers through implementation of a treasury single account.................................................................................................................................... 35

Ethiopia: Implementing a land value capture system during rapid urbanization .............................. 36

Uganda (1): The role of grants and intergovernmental transfers in a second-tier city – perspectives from Busia Municipal Council .......................................................................................................... 38

Lesotho: Local governments and revenue generation in Lesotho-Legally empowered but politically constrained ........................................................................................................................................ 39

(IV) Challenges in municipal financial management ....................................................................... 41

(V) LDC experiences in developing local participatory budgeting ................................................ 47

Nepal: Increasing citizen participation with participatory planning (PP) ......................................... 47

Bangladesh (1): Experimenting with inclusive budgetary processes at the local level .................... 48

Solomon Islands: Tackling local governance challenges in a small island developing state ........... 48

Senegal (1): The experience of PB experiments in Fissel and Ndiaganiao ...................................... 49

Madagascar: Building capacity for PB through donor support ......................................................... 50

Mozambique (1): Evolving PB approaches in Maputo ..................................................................... 50

3

(VI) Challenges in accessing long-term finance for capital investments ........................................ 52

Municipal bonds................................................................................................................................ 53

Institutional investors: an untapped source for sub-national infrastructure investment? .................. 64

(VII) LDC experiences in mobilizing long-term finance for capital investment ........................... 69

Uganda (2): A project-based partnership to finance municipal transportation in Busia ................... 69

Lao PDR (2): The Morphu Village water supply project: a local PPP done right ............................ 70

Bangladesh (2): Establishing a municipal development fund to finance local infrastructure ........... 71

Tanzania: Dar es Salaam’s water supply: a local PPP gone wrong .................................................. 72

Senegal (2): Dakar’s experience in (almost) getting a municipal bond to the financial market ....... 73

(VIII) International cooperation on municipal finance ................................................................... 75

Climate finance for subnational governments................................................................................... 77

How to strengthen international cooperation for subnational finance? ............................................ 78

(IX) Bibliography ................................................................................................................................ 81

4

(I) Setting the stage – Municipal finance and the 2030 Agenda for Sustainable Development

With the adoption of the 2030 Agenda for Sustainable Development, the Addis Ababa Action Agenda

(Addis Agenda), and the Paris Agreement in 2015, the international community has laid out a clear

vision and roadmap for achieving sustainable development in all of its three dimensions—economic,

social and environmental.1 Yet, while the 2030 Agenda is global, most of its implementation will

ultimately happen at the local level with the participation of subnational governments and local

stakeholders. Being closer to the people than central governments, local governments, and local

stakeholders are uniquely positioned to identify development needs and contribute to the development

of adequate policy measures to address them.

The importance of the local dimension has been recognized by world leaders. All landmark

agreements of 2015—the year of “global action” —recognized the imperative to work with local

authorities and at the local level. Sustainable Development Goal (SDG) 11 is a local objective in itself

and calls for cities and human settlements to be “inclusive, safe, resilient and sustainable”. The local

dimension permeates other SDGs, targets, and means of implementation, including those on basic

public service provision in health, energy, water and sanitation, education and other areas, climate

change-related planning, sustainable tourism, ecosystem and biodiversity, and the capacity of local

communities to pursue sustainable livelihood opportunities.

Localizing the new global development agenda

The Secretary-General of the United Nations, Mr. Ban Ki-moon, emphasized that “our struggle for

global sustainability will be won or lost in cities.” How to win that struggle and “localize” the 2030

Agenda and other landmark UN agreements of recent years is at the heart of the deliberations leading

up to the Third United Nations Conference on Housing and Sustainable Urban Development (UN

Habitat III, 17-20 October 2016). The Conference presents a timely opportunity to chart new

pathways in response to the challenges of urbanization and the implementation of the 2015 landmark

agreements. The outcome document of UN Habitat III, “The New Urban Agenda”, is envisaged to

promote a new model of urban development, one that integrates all dimensions of sustainable

development and helps align national and subnational priorities in support of inclusive and equitable

1 Lead authors were Daniel Platz (FFDO, UN-DESA), Vito Intini (UNCDF) and Tim Hilger (UNCDF). All EGM

participants (both Africa and Asia made important substantive contributions (annex forthcoming). Patrick Nally, Yixiao Fang and Yijun William Wu provided excellent research assistance. Comments from Paul Smoke, Dominika Halka and Shari Spiegel are gratefully acknowledged. The views and opinions expressed in this informal background paper are those of the lead authors and do not necessarily reflect those of the United Nations Secretariat or UNCDF. The designations and terminology employed may not conform to United Nations practice and do not imply the expression of any opinion.

5

economic and social development. Implementing the New Urban Agenda will rest on three pillars:

sound urban rules and regulations, farsighted urban planning and design, and strengthened municipal

finance.

Financing challenges at the local level

The financing required to implement the 2030 Agenda is estimated to be of the order of several

trillion dollars per year, and a significant portion of it will have to be mobilized and spent at the local

level. Indeed, mobilizing adequate funding for long-term investments in support of inclusive and

sustainable local development is perhaps the greatest challenge that local authorities face. The Addis

Agenda provides a natural starting point to discuss local finance in the context of the 2030 Agenda. It

presents a coherent framework for financing the 2030 Agenda for Sustainable Development, including

the Sustainable Development Goals, and puts forward a comprehensive set of corresponding policy

actions. In the Addis Agenda, Member States committed to fully engage local authorities in their

implementation efforts. Furthermore, the Addis Agenda promotes greater international cooperation

“to strengthen capacities of municipalities and other local authorities” (paragraph 34).

To meet the financing challenge, the Addis Agenda highlights the need to draw upon all sources of

finance (public, private, national, and international) and puts forward a policy framework that realigns

financial flows with public goals. It calls for an enabling environment comprising appropriate public

policies and regulatory frameworks that help unlock the transformative potential of people and

incentivize changes in consumption, production, and investment patterns in support of sustainable

development.

The comprehensive approach of the Addis Agenda translates well to the local level. For local

authorities, drawing upon all sources of finance implies the need to more effectively mobilize internal

(e.g., local taxes, user fees, land value capture) and external revenue streams (e.g., intergovernmental

transfers, donor support), in order to provide public goods and services and to finance large-scale

capital investments. A policy framework that realigns local financial flows with local public goals

implies a well-coordinated fiscal, political, and administrative decentralization effort, where local

expenditure responsibilities are backed by reliable intergovernmental transfers and fiscal

empowerment (e.g., the legal and technical capacity to levy taxes).

This report places particular emphasis on the challenges faced by local governments in least

developed countries (LDCs, see Box 1). The Addis Agenda pays special heed to LDCs as the most

vulnerable group of countries. It calls for global support to overcome the structural challenges they

face. It encourages donor countries to increase the allocation of official development assistance

(ODA) to the world’s poorest nations to 0.2 per cent of national income. The European Union

6

committed to do so by 2030. A major challenge for LDCs and donors alike will be to ensure that those

resources are effectively directed to and spent at the local level—where they are needed most.

Box 1.1: What are least developed countries (LDCs)?

LDCs are the poorest and most vulnerable countries. They comprise more than 880 million people*, or around 12 per cent of the world’s population, but account for less than 2 per cent of world GDP.

The low level of socio-economic development in LDCs is linked to weak human and institutional

capacities, low income converging with high inequality, and a lack of domestic financial resources.

Governance crises, political instability, and, in some cases, internal or external conflicts often

exacerbate the situation. LDCs often suffer from low productivity and low investment. Furthermore,

they are exposed to external shocks, for example from their dependency on the export of a few

commodities as the primary source of revenue or their often high vulnerability to climate change.

The United Nations define least developed countries (LDCs) as low-income countries suffering from

structural impediments to sustainable development. Every three years, the list of LDCs is reviewed by

the Committee for Development Policy (CDP), which gives recommendations for inclusion and

graduation of countries. Recommendations are then endorsed by the Economic and Social Council

(ECOSOC) and decided on by the General Assembly. The criteria used by the CDP for inclusion in

the list are (1) gross national income per capita; (2) the human assets index (HAI); and (3) the

economic vulnerability index (EVI). The CDP sets thresholds on each of the three criteria, and

country must satisfy all three at one triennial review to be added to the list. In addition, its population

must not be larger than 75 million inhabitants. However, decisions about inclusion and graduation are

not only based on the assessment of the three criteria, but also factor in country-specific information

and views from the government. To leave the LDC category, a country must cease to meet any two

criteria through two consecutive reviews.

7

Table 1.1: List of least developed countries as of May 2016 (year of inclusion in brackets):

Africa:

Angola (1994)

Benin (1971)

Burkina Faso (1971)

Burundi (1971)

Central African Republic (1975)

Chad (1971)

Comoros (1977)

Dem. Rep. of the Congo (1991)

Djibouti (1982)

Equatorial Guinea (1982)

Eritrea (1994)

Ethiopia (1971)

Gambia (1975)

Guinea (1971)

Guinea-Bissau (1981)

Lesotho (1971)

Liberia (1990)

Madagascar (1991)

Malawi (1971)

Mali (1971)

Mauritania (1986)

Mozambique (1988)

Niger (1971)

Rwanda (1971)

Sao Tome And Principe (1982)

Senegal (2000)

Sierra Leone (1982)

Somalia (1971)

South Sudan (2012)

Sudan (1971)

Togo (1982)

Uganda (1971)

United Rep. of Tanzania (1971)

Zambia (1991)

Asia and the Pacific:

Afghanistan (1971)

Bangladesh (1975)

Bhutan (1971)

Cambodia (1991)

Kiribati (1986)

Lao People’s Dem. Republic (1971)

Myanmar (1987)

Nepal (1971)

Solomon Islands (1991)

Timor-Leste (2003)

Tuvalu (1986)

Vanuatu (1985)

Yemen (1971)

Latin America and the Caribbean:

Haiti (1971)

Special challenges for subnational finance in LDCs

The state of subnational finance in LDCs is affected by conditions and developments at the local,

national and global levels. Certain megatrends, such as rapid urbanization, changes to the global

economic context, climate change, and natural disasters have particularly strong impacts at the local

level. Limited subnational financial capacities reduce the ability of local government authorities in

8

LDCs to effectively manage these impacts, as well as to improve local service delivery and finance

local infrastructure development. In addition to global megatrends, LDCs are confronted with

additional challenges from the national and local level in most areas of subnational finance. Weak

human and institutional capacities, low per capita income, low productivity, and shallow financial

sectors are frequently combined with political instability and high vulnerability to terms-of-trade

shocks due to the reliance on a limited number of commodities for export. At the subnational level,

these characteristics may translate into small local revenue bases; limited financial, expenditure, and

asset management capacities; unpredictable and insufficient intergovernmental transfers; and little to

no access to private capital. Other political constraints, e.g., insufficient local revenue authority, may

pose further challenges for subnational finance in LDCs.

Urbanization in LDCs

Cities around the world are expanding as a result of overall population growth and continuous

migration from rural to urban areas. Since 2007, the majority of the world’s population has been

living in urban areas. Africa and Asia are urbanizing faster than any other region. By 2050, an

additional 2.5 billion people are expected to live in cities, with almost 90 per cent of the growth

located in Africa and Asia (see Figures 1.1-1.3: Urban agglomerations in LDCs in 2000, 2014 and

2030)

9

Figure 1.1: Urban agglomerations in LDCs 2000:

Figure 1.2: Urban agglomerations in LDCs in 2014:

10

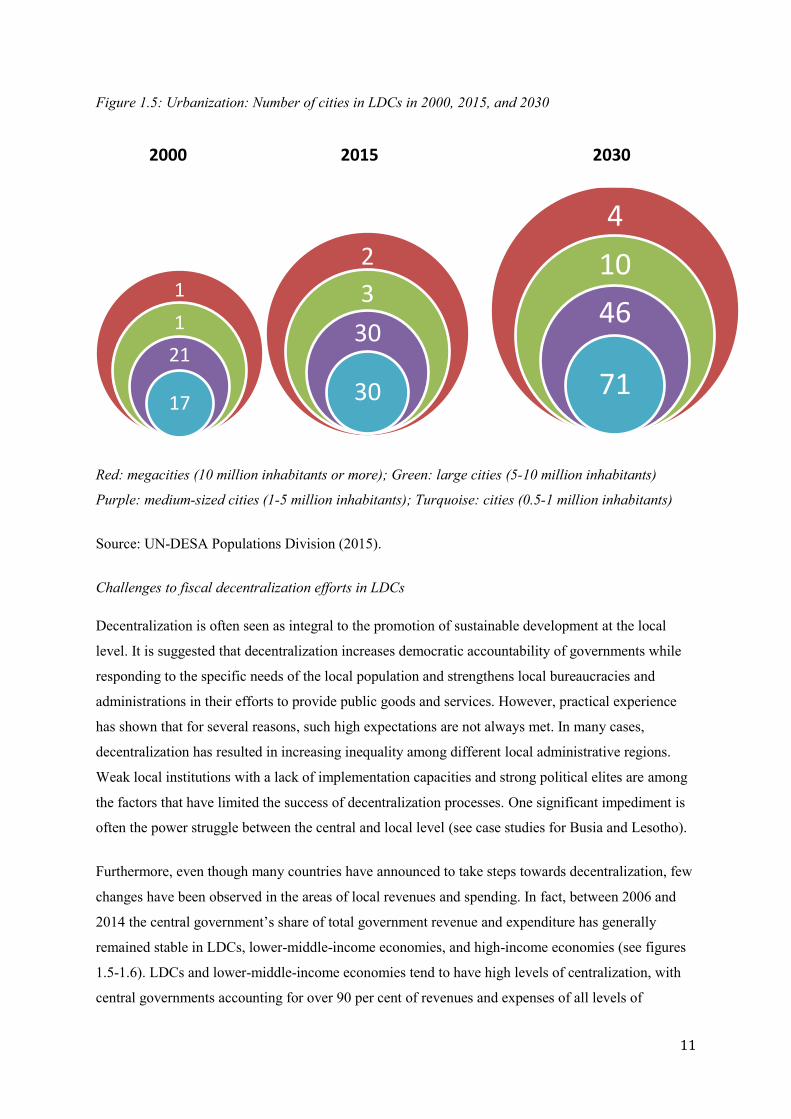

Figure 1.3: Projected urban agglomerations in LDCs in 2030:

The proportion of the urban population in LDCs is expected to increase from 31 per cent in 2014 to 49

per cent in 2050. LDCs such as the Democratic Republic of the Congo, the United Republic of

Tanzania, and Bangladesh are predicted to increase their urban population by 50 million people each.

While Kinshasa is currently the only megacity (more than 10 million inhabitants) in an African LDC,

Dar es Salaam and Luanda are both expected to surpass the 10 million mark by 2030. Rapid

urbanization affects not only the largest cities, but also smaller cities, in particular those with less than

500,000 inhabitants (Figure 1.4 shows the number of cities in LDCs by size). At the same time, rural-

urban linkages will remain critical in African and Asian countries, since around 44 per cent of the

African population and 33 per cent of the Asian population will still live in rural areas in 2050.

11

4

10

46

71

Figure 1.5: Urbanization: Number of cities in LDCs in 2000, 2015, and 2030

Red: megacities (10 million inhabitants or more); Green: large cities (5-10 million inhabitants)

Purple: medium-sized cities (1-5 million inhabitants); Turquoise: cities (0.5-1 million inhabitants)

Source: UN-DESA Populations Division (2015).

Challenges to fiscal decentralization efforts in LDCs

Decentralization is often seen as integral to the promotion of sustainable development at the local

level. It is suggested that decentralization increases democratic accountability of governments while

responding to the specific needs of the local population and strengthens local bureaucracies and

administrations in their efforts to provide public goods and services. However, practical experience

has shown that for several reasons, such high expectations are not always met. In many cases,

decentralization has resulted in increasing inequality among different local administrative regions.

Weak local institutions with a lack of implementation capacities and strong political elites are among

the factors that have limited the success of decentralization processes. One significant impediment is

often the power struggle between the central and local level (see case studies for Busia and Lesotho).

Furthermore, even though many countries have announced to take steps towards decentralization, few

changes have been observed in the areas of local revenues and spending. In fact, between 2006 and

2014 the central government’s share of total government revenue and expenditure has generally

remained stable in LDCs, lower-middle-income economies, and high-income economies (see figures

1.5-1.6). LDCs and lower-middle-income economies tend to have high levels of centralization, with

central governments accounting for over 90 per cent of revenues and expenses of all levels of

1

1

21

17

2

3

30

30

2000 2015 2030

12

governments, while high-income economies show more advanced fiscal decentralization with ratios

below 70 percent. 2

Figure 1.6: Local revenue as share of central government revenue

Source: IMF Government Finance Statistics Yearbook database

2 These findings build off of those from Dziobek, Mangas, and Kufa (2011), who found that with the exception

of countries transitioning from command to market economies, between 1995 and 2008, the level of decentralization has seen little change regardless of countries’ level of development or population.

2006 2007 2008 2009 2010 2011 2012 2013 2014

Afghanistan (LDC) 99 99 100 99 100 100 99 100

Bhutan (LDC) 100 100 100 100 100 100 100 100 100

Kiribati (LDC) 98 98 99

Timor-Leste (LDC) 100 100 100 100 100

Armenia 97 97 98 97 97 95 96 96

El Salvador 98 96 96 95 95 96 95 90

Honduras 95 99 96 95 95 95 95 98 96

Indonesia 91 89 87

Canada 47 47 46 45 45 44 45 45 46

Germany 66 65 65 66 66 65 65 65 65

Sweden 66 66 63 62 63 67 65 65 65

Switzerland 51 51 54 53 53 54 54 54

United States 57 57 54 55 56 57 57 60 60

0

20

40

60

80

100

120

Re

ven

ue

: Ce

ntr

al G

ove

rnm

en

t as

a s

har

e

of

gen

era

l go

vern

me

nt

reve

nu

es

13

Figure 1.7: Local expenditure as share of central government expenditure

Source: IMF Government Finance Statistics Yearbook database

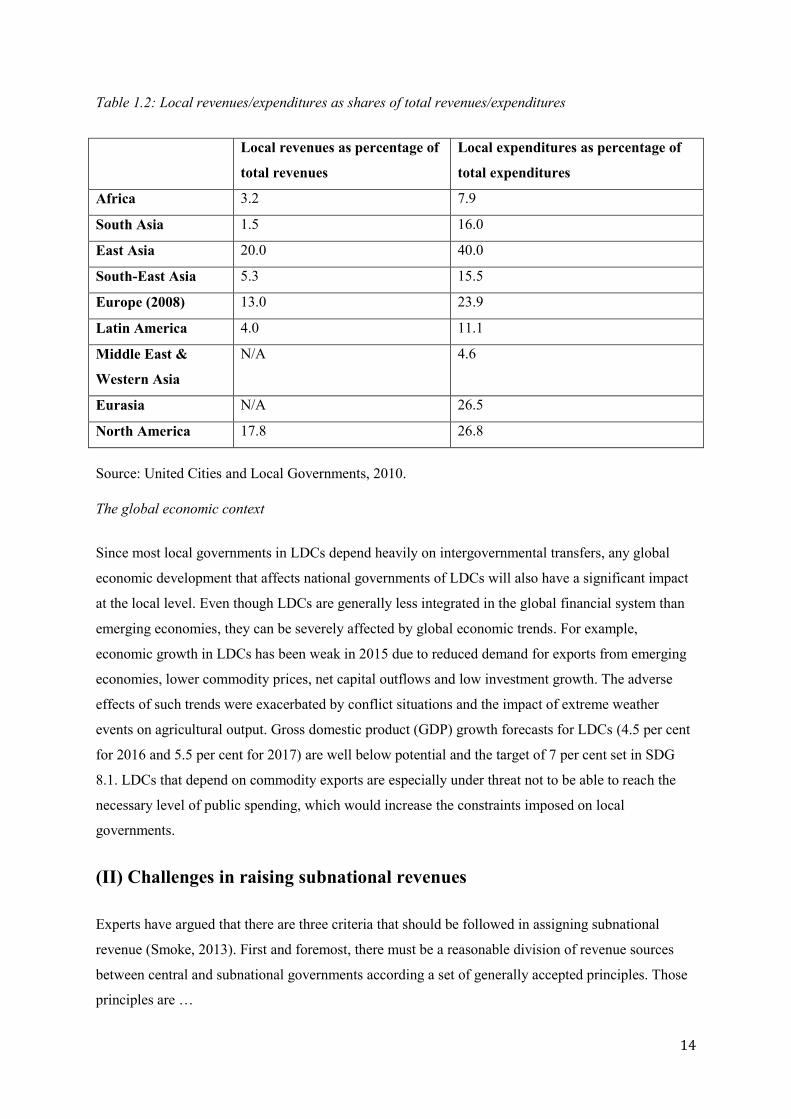

The level of local revenues and expenditures in comparison to total revenues and expenditures also

varies among regions (Table 1.2). In developing regions, countries in Latin America and South-East

Asia show slightly higher rates for local revenues and expenditures as a share of total revenues and

expenditures than Africa.

2006 2007 2008 2009 2010 2011 2012 2013 2014

Afghanistan (LDC) 101 99 100 100 100 100 100 100

Bhutan (LDC) 100 100 100 100 100 100 100 100 100

Kiribati (LDC) 97 97 98

Timor-Leste (LDC) 100 100 100 100 100

Armenia 97 97 98 98 98 96 96 97

El Salvador 102 99 99 99 99 100 99 93

Honduras 99 104 101 99 99 101 101 97 101

Indonesia 103 99 100

Canada 46 46 46 45 45 44 43 43 43

Germany 66 66 65 66 67 65 64 64 64

Sweden 64 64 62 63 64 67 67 67 67

Switzerland 54 58 55 53 54 54 53 53 52

United States 60 60 61 66 67 66 64 64 64

0

20

40

60

80

100

120Ex

pe

nd

itu

re:

Ce

ntr

al G

ove

rnm

en

t as

a s

har

e

of

gen

era

l go

vern

me

nt

exp

en

dit

ure

s

14

Table 1.2: Local revenues/expenditures as shares of total revenues/expenditures

Local revenues as percentage of

total revenues

Local expenditures as percentage of

total expenditures

Africa 3.2 7.9

South Asia 1.5 16.0

East Asia 20.0 40.0

South-East Asia 5.3 15.5

Europe (2008) 13.0 23.9

Latin America 4.0 11.1

Middle East &

Western Asia

N/A 4.6

Eurasia N/A 26.5

North America 17.8 26.8

Source: United Cities and Local Governments, 2010.

The global economic context

Since most local governments in LDCs depend heavily on intergovernmental transfers, any global

economic development that affects national governments of LDCs will also have a significant impact

at the local level. Even though LDCs are generally less integrated in the global financial system than

emerging economies, they can be severely affected by global economic trends. For example,

economic growth in LDCs has been weak in 2015 due to reduced demand for exports from emerging

economies, lower commodity prices, net capital outflows and low investment growth. The adverse

effects of such trends were exacerbated by conflict situations and the impact of extreme weather

events on agricultural output. Gross domestic product (GDP) growth forecasts for LDCs (4.5 per cent

for 2016 and 5.5 per cent for 2017) are well below potential and the target of 7 per cent set in SDG

8.1. LDCs that depend on commodity exports are especially under threat not to be able to reach the

necessary level of public spending, which would increase the constraints imposed on local

governments.

(II) Challenges in raising subnational revenues

Experts have argued that there are three criteria that should be followed in assigning subnational

revenue (Smoke, 2013). First and foremost, there must be a reasonable division of revenue sources

between central and subnational governments according a set of generally accepted principles. Those

principles are …

15

Second, individual revenue sources should be designed to follow a set of principles in a consistent

way (see below). Third, revenue system must be effectively implemented on the ground.

The most common subnational revenue sources in LDCs include user fees and charges, taxes/levies,

as well as intergovernmental transfers, sometimes financed or supplemented by foreign aid.3 These

sources may be supplemented by investment income, property sales, and licenses. User charges and

fees are mostly levied where people pay for the benefits and utilities they receive (e.g. water supply,

sanitation, energy, parking space). At the same time, the municipality typically provides a range of

public goods (police, ambulance, firefighters, streetlights etc.) whose consumption is not exclusive

and whose benefits it cannot directly assign to the individual consumers. In such cases, taxes are the

more appropriate tool as they target the entire community that stands to benefit from the service.

In general, revenue mobilization and management are very challenging in LDCs both at the national

level and subnational levels due to narrow tax bases

Taxation at different levels of government

Inconsistencies in the overall fiscal framework are not uncommon across the globe and they may be

more pronounced in countries with institutional settings, such as LDCs. Inconsistencies may appear in

the form of insufficient harmonization of central and subnational taxes. Limiting overlap with central

taxes and reducing revenue disincentives in transfer and lending mechanisms are important to ensure

that the full set of subnational revenues is consistent with the rest of the national fiscal system.

When it comes to the revenue potential at the local level, evidence suggests that, in general, there is a

positive correlation between the size of the local government (in terms of its population) and the role

of own-source revenues. For example, taxes and other local sources of revenue can account for as

little as 9 per cent of total revenue in small Brazilian municipalities (less than 5000 people) and over

50 per cent in large cities. The fact that larger local entities have more institutional capacity to raise

revenue is not surprising, all other things being equal, but where countries face severe institutional

constraints at all tiers of government, as is the case in most LDCs, the positive correlation may often

not hold. Indeed, in most cities in LDCs, the correlation is less pronounced, with even large cities

struggling with generating more than 10 per cent of their revenues through user fees and taxes (World

Bank, 2006).

3 Many publications on subnational finance list borrowing as a source of income. This paper treats borrowing separately.

Borrowed money is not income unless the loan or debt is forgiven. For example, a debt/income ratio, an important measurement of financial health, does not make sense if income includes debt.

16

The appropriate choice of which taxes to impose, how much to charge, and how to structure them

depends on a wide range of factors such as the size, the level of economic development, and the

demographic composition of the local authority. Across LDCs, one finds a wide array of local taxes at

both at the national and local levels (Table 2.1).

Table 2.1: Taxes assigned to/levied by different levels of selected LDC governments

Country Tier of Government Tax Authority

Burundi National Customs duties, VAT, excise duties, PIT, BPT

Local Vehicle tax, real estate tax

Rwanda National Customs duties, VAT, excise duties, PIT, BPT

Local Property tax, rental income tax, and trading licenses

Mali National Customs duties, VAT, excise duties, PIT, BPT

Local Regional and local development tax, income tax from local

civil servants, Property taxes, other taxes

Tanzania National Customs duties, VAT, excise duties, income tax

Local Development levy, property tax, service levy, business

license, fee on trade, crop and` livestock cess*, other fees

and user charges

Uganda National Customs duties, VAT, excise duties, PIT, BPT

Local Rents, rates, royalties, stamp duties, crop and livestock

cess, fees on registration and licensing and other fees and

taxes that parliament may prescribe (property taxes, license

and user charges)

Afghanistan National Customs duties, withholding tax, business receipts & CIT,

PIT, capital gains tax

Local Vehicle registration tax, toll tax, advertisement tax,

property tax, road tax

Bangladesh National Customs duties, excise duties, supplementary duties, PIT,

CIT, VAT, capital gains tax

Local Tolls, lighting rates, conservancy rates, holding tax, vehicle

tax, animal tax, marriage tax

Bhutan National Customs duties, excise duties, PIT, BIT, CIT, sales tax

Local Property taxes, property transfer tax, land taxes, cattle tax,

grazing tax, advertisement tax

Cambodia National Customs duties, excise duties, VAT, CIT, PIT, stamp duty

Local Property taxes, administrative fees (civil registry

17

functions), user fees and charges, land taxes

Lao PDR National Customs duties, excise duties, VAT, CIT, PIT, stamp duty

Local Property taxes, vehicle taxes, fuel taxes, fees and

administrative charges

Myanmar National Customs duties, excise duties, CIT, PIT, stamp duty,

capital gains tax

Local Property taxes, land taxes, development affairs

organization fees (public services including water, sewage

and trash collection), wheel tax

Nepal National Customs duties, excise duties, CIT, VAT, capital gains tax

Local Property taxes, municipal business tax, municipal tax on

vehicles, local development fee

Timor-Leste National Customs duties, excise duties, CIT, PIT, petroleum tax

Local NA

Yemen National Customs duties, excise duties, PIT, CIT, general sales tax

Local Property taxes, municipal business tax, administrative

service fees

PIT: Personal Income Tax, BPT: Business Profit Tax, VAT: Value Added Tax. * Cess: a tax

introduced in colonial times, often levied on livestock and produce.

Sources: Khadka (2015), Urban Management Centre (2010), World Bank (2015), IMF (2013), IMF

(2010), Huda (2009), Taliercio (2005), Crowe Horwath International (2015), Dickenson-Jones (2015),

Shrestha (2002), Remeo (2015).

Over the years, many attempts have been undertaken to evaluate local revenue sources according to a

set of key principles (Smoke, 2013). Such principles include:

Revenue adequacy: covering subnational budgetary needs (based on the “finance follows

function” principle).

Revenue buoyancy: growing in proportion to the economy and expenditure needs.

Stability: avoiding large fluctuations in revenue yields that would undermine the ability of

subnational governments to provide services.

Correspondence between payments and benefits (including limiting tax exporting).

Distortionary Impact: minimizing distortions of economic decisions made by individuals and

firms (e.g. resulting from differentiated base assessment and rates).

Autonomy and Accountability: allowing subnational governments discretion to make

independent decisions (creating a link between revenue generation and service delivery).

18

Administrative feasibility: ensuring the scale and complexity of administration is consistent

with capacity and affordable to the subnational government.

Political feasibility: maximizing the likelihood of acceptance of a source through consistency

with political reality, e.g. taxpayers see value for money, fair treatment, less visible/onerous

(small payments over time versus large lump sums).

Equity: ensuring fair treatment among equals (horizontal) and across different groups (equals)

framed in terms of income but can use other points of reference.

Table 2.2 illustrates some of the major challenges in adhering to these key principles at the local

level.

Table 2.2: Challenges in implementing principles for subnational taxes in LDCs

Principle Major challenge

Revenue adequacy Determining overall revenue adequacy (including transfers), is not simple since functional assignments from the central government are often vague, inconsistent and may be not fully adopted at the local level. Where functional assignments are clear and local revenues are deemed inadequate, typical challenges that may lead to low local revenues include low intergovernmental transfers, low functional capacity in tax administration and outdated valuation of the tax base as well as a low overall revenue base due to low per capita income and large informal sectors.

Revenue buoyancy Adequate revenue buoyancy is often elusive due to lack of administrative actions needed to ensure growth of the revenue base (e.g., revaluing and indexing property assessments).

Stability Stability requires good administration and a strong commitment to enforce collection during more difficult economic times or periods of political pressure, especially in periods leading up to subnational elections.

Correspondence between payments

and benefits

The correspondence between payments and benefits can be compromised by differential treatment of taxpayers or sectors in pursuit of policy objectives, poorly developed or enforced assessment and collection and tax exporting. i.e., the ability to shift tax burdens to people who live outside the city (although this is not universally opposed and may be to some extent seen as desirable in certain instances, such as taxes that fall primarily on foreign tourists).

Local Autonomy Revenue autonomy varies considerably, but it is often limited by the central

government due to concerns over national fiscal policy management and/or local capacity. At the same time, subnational governments may fall to take advantage of autonomy that is granted because they do not know how to do so where decentralization is new or capacity is weak. Alternatively, disincentives in the fiscal system or political conditions may undermine the

19

motivation of subnational governments to exercise their revenue powers.

Administrative feasibility

Administrative feasibility may be compromised by pursuing non-revenue raising objectives and or adopting poorly defined or unduly complex administrative procedures.

Political Feasibility

Political feasibility is often difficult to determine and effective adoption of subnational taxes may be challenging in developing country environments, especially in the poorest countries where citizens are not used to receiving and/or paying for services.

Equity Horizontal equity is generally a greater concern of subnational tax policy than vertical equity given potential spatial inefficiencies created by subnational redistributive taxation. Equity can be affected, for example, if there is preferential treatment of certain taxpayers or groups due to subnational tax regulations and weak or selective administration.

Source: based on Smoke (2013) and Bird (2010).

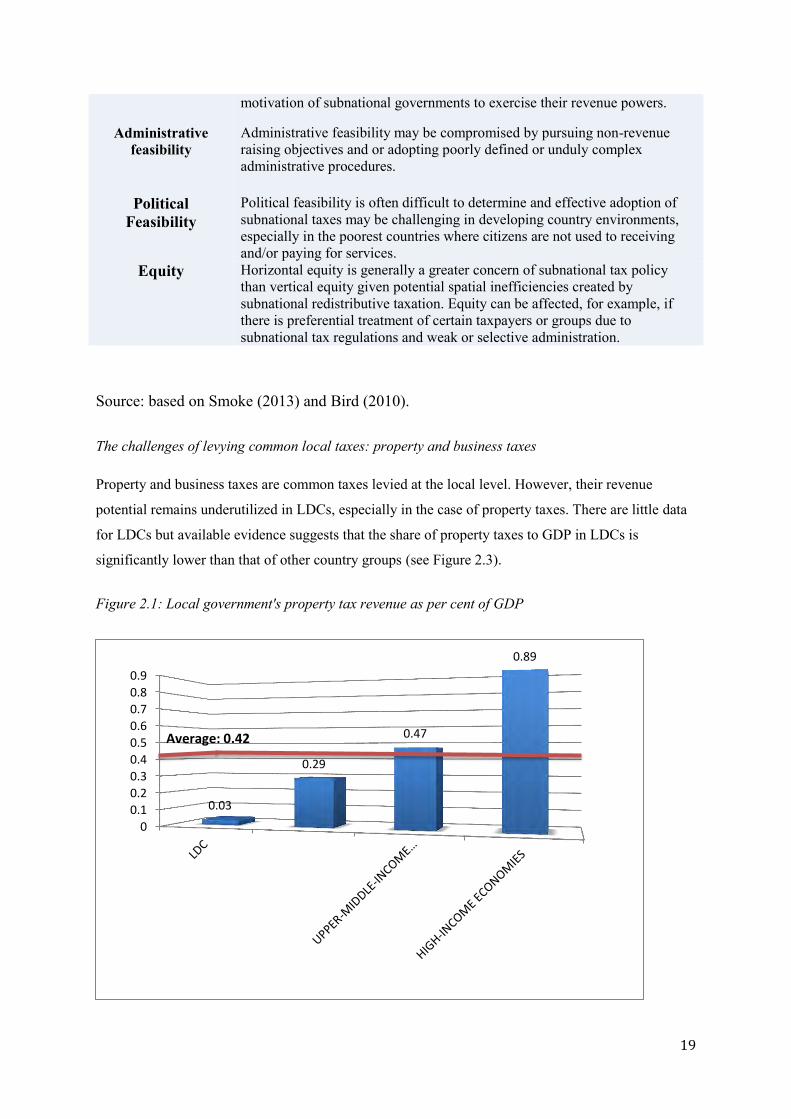

The challenges of levying common local taxes: property and business taxes

Property and business taxes are common taxes levied at the local level. However, their revenue

potential remains underutilized in LDCs, especially in the case of property taxes. There are little data

for LDCs but available evidence suggests that the share of property taxes to GDP in LDCs is

significantly lower than that of other country groups (see Figure 2.3).

Figure 2.1: Local government's property tax revenue as per cent of GDP

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.03

0.29

0.47

0.89

Average: 0.42

20

Source: IMF Government Finance Statistics Database, accessed August 2016.

Yet, important progress has been made in a range of LDCs. For example, figure 2.4 suggests the

performance of key taxes in Maputo, the capital of Mozambique, increased significantly between

2010 and 2014. In particular, the “SISA”, a set of tax levied on transfers of real estate, plays a

significant role in Maputo’s local revenue (figure 2.5).

Figure 2.2: Tax and fees coverage in the municipality of Maputo, 2010-2014

Source: Cumbe, 2016.

0

50,000

100,000

150,000

200,000

250,000

2010 2011 2012 2013 2014

Municipal Property Tax

Municipal Personal Tax

Real Estate Transfer Tax

Annual Vehicles Tax

Tax for Economic Activity

Tax for Building permit

Tax for Use of Municipal Land

Municipal Market Taxes

Advertising Taxes

Parking tax

Tax for Collection and treatment ofwasteOther Revenues

21

Figure 2.3: Composition of local tax revenue in the municipality of Maputo (per cent based on

average for 2010-2014)

Source: Cumbe, 2016.

One of the major challenges with levying property taxes in LDCs is the lack of proper titles for

residential premises and tax exemptions for low-value properties. For example, it is estimated that less

than 10 per cent of land in Africa, where most LDCs are located, is properly documented

(Byamugisha, 2013). Moreover, given the lack of suitably qualified staff and resources for local

governments in many LDCs, rising land values are not regularly assessed, leading to substantial

revenue shortfalls as old property values remain on the books. Consequently, where property taxes are

levied, they often do not keep pace with economic development. For this reason, some LDCs in

Africa have refused to establish direct property taxes and instead tax only rental income (Cameroon)

or apply a simplified occupancy tax (Burkina Faso). Property taxes also suffer from broader

challenges that affect other types of national taxes such as low nominal tax rates and low collection

rates.

Where title registration systems and fiscal cadastres (i.e. comprehensive and perpetual inventories that

describe and assess the value of landholdings) are not well developed, ‘street addressing’ (i.e. giving

streets names and/or numbers) is a constructive first step towards determining the tax base and

increasing tax revenues. Street addressing allows locating residents and greatly facilitates municipal

service provision. It also helps enforce the collection of user fees for water and electrical utilities. It is

important to see the building of fiscal cadastres and street addressing as complementary practices.

0.00

5.00

10.00

15.00

20.00

22

Indeed, the reconciling of street indices with fiscal registers can lead to substantial local revenue

increases (Habitat III, 2015).4

A property tax reform approach that places emphasis on updating the property tax roll through

building a fiscal cadastre and improving the accuracy of property valuation is generally referred to as

a “valuation-pushed reform”. Such a reform sometimes assumes that non-valuation administrative

processes are functional and that a major improvement in property tax revenue comes from improving

property valuations (Bird, 2015). Most academic literature, however, favours a “collection- led” to a

“valuation- pushed” reform in low-income and LDC countries (McCluskey 2015). It is argued that in

these countries non-valuation administrative functions are frequently not fully functional, i.e. that

efforts should be placed on improving collection and enforcement of the tax system and ensuring legal

enforcement rather than on valuation. Yet, over the past decades, reforms in LDCs like Sierra Leone

(Freetown), Tanzania (Dar es Salaam), and Uganda (Kampala) have focussed primarily on valuation

(Mc Clusky 2015). Whereas both approaches are essential components of a holistic reform effort, it is

important to find the right balance and appropriate sequencing of reforms (see Lao PDR Case Study

(1), Ethiopia Case Study). While valuation-based reforms may make sense in large cities in LDCs,

their applicability may be more limited in smaller urban and rural jurisdictions with limited local

administrative capacities and no central administrative support. Contrary to the current trend to push

new valuation techniques, many LDCs may therefore think about directing their scarce resources

towards “collection-based reform efforts” first, especially where institutional capacities are weak.

Perspectives on business taxes

In economic theory, business taxes at the local level are often seen as inefficient mechanisms of own

source revenue generation. It is argued that such taxes may discourage business formation, have

adverse effects on growth and investment, and lead to distorted capital allocation. At the same time,

subnational entities may compete in lowering their business taxes in a “race to the bottom” that erodes

the tax base and revenues.

However, there is no solid empirical evidence that business taxes have implications on growth, and in

practice, virtually every country imposes some sort of business tax, either at the national or local

level. Bird (2006) notes there are efficiency, equity, and political arguments that support the case of

the local business tax. The efficiency and equity rationale is captured in the principle of benefit

taxation. If firms receive identifiable, cost-reducing benefits through public sector services, they

should pay for the costs incurred in the provision of such benefits, e.g. wear and tear from large trucks

4 In the context of Sub-Saharan Africa, some non-LDCs like Botswana, Namibia and South Africa have well-developed

property markets. Their experience could help African LDCs in their property market reforms.

23

on a road or waste disposal expenditures. In this connection, business taxes are efficient in that they

ensure that someone pays for the costs related to providing a particular service. At the same time, they

are equitable and fair in that they ensure that firms pay for a service rendered by local authorities and

not just their citizens. In addition, taxing larger domestic and foreign businesses or corporations may

make political sense since negative externalities, such as environmental costs, may outweigh positive

effects, such as local job creation or skills transfers, as is often the case with extractive industries.

Local business taxes are also easier to administer and more elastic than property taxes and are

therefore a crucial source for expanding infrastructure and local services.

Subnational revenue composition in African LDCs

In many LDCs, business taxes are widely used. In West African LDCs, the “patente,” a differentiated

set of fixed tax rates that is based on size of premises, type of business, and number of employees has

made up for a sizable share of local revenues (Figure 2.6). In East Africa, Tanzania levies a local

business tax named ‘City Service Levy’ at a fixed percentage on the firm’s turnover. In the rest of

Anglophone Africa, local business licensing generates between 5 and 30 per cent of local government

own revenues in urban councils (Fjeldstad, and Heggstad, 2012). More research is needed on how

local business taxes should be imposed, structured, and administered in order to maximize their

revenue potential and effectiveness. Such research must also acknowledge that corporate tax evasion

remains a major challenge for imposing local business taxes, especially in the case of transnational

companies that may apply methods such as transfer or trade mispricing to deceit national local tax

authorities.5

5 See Report of the High Level Panel on Illicit Financial Flows from Africa, 2015, commissioned by the AU/ECA Conference of Ministers of Finance, Planning and Economic Development.

24

Figure 2.4: Composition of local tax revenue in West African LDCs (Averages for 1995-2008)

* The global tax (impôt synthétique) is levied on small business and combines taxes on commercial

and industrial profits, business licenses and value added tax.

Source: IMF, 2015.

Box 2.1: Lessons learned from UNCDF‘s efforts to improve local revenue collection in West African LDCs In order to strengthen self-management capacities of the local authorities, especially in rural areas, the United Nations Capital Development Fund (UNCDF) developed the Local Authorities Financial and Institutional Analysis System (LAFIAS). The system was initially introduced in three West African countries, Guinea, Mali and Benin. Initial experiences with the progamme highlight the strong effect of improved local management on revenue raising capacity. The following conclusions are highlighted in the report:

1. A minimum level of organization and capacity of local authorities (own services and personnel) is

essential for local development.

2. A minimum level of information on the potential resources in their territorial jurisdictions is

important for local authorities to play a more important role in mobilizing own source revenues.

3. The local tax system in West African LDCs—Mali is a prime example—includes many rural taxes

that are difficult to mobilize and that yield low revenue in the urban context, while the largest

potential resource -urban property- remains largely untapped. In addition, a simplification of the tax

code and flat-rate taxation could be explored to further strengthen revenue collection.

4. Quality beats quantity. It is important that levies/taxes not be too numerous and dispersed to avoid

high transaction costs.

25

5. Great resource potential lies in market activities and facilities (markets, terminals and other

income-generating infrastructures). A proper management of these facilities will allow the authorities

to diversify and considerably improve their resources.

6. The existence of economic infrastructures is a determining factor in resource potential and

consequently, the revenue of local authorities. For example, a lack of economic infrastructure explains

the challenges of the Socoura commune, which has the largest population size in the standard

communes in Mali, but has the lowest level of local revenue.

7. The LAFIAS analyses showed the limitations of a true economic development within the rural

spaces that make up the local authorities. Creating inter-community cooperation between local

authorities based on “development hubs” or “local cooperation territories” can help take advantage of

the socio-cultural, geographical, historical and economic opportunities that two or several local

authorities share together.

8. Finally, investment per se cannot stimulate improvement in local finances; it must be supplemented

by taxation support measures, but also communal management and local governance.

Source: UNCDF (2012).

Examples of subnational revenue composition in Asian LDCs

As shown in Figure 2.5, one third of municipal income in Nepal comes from central government

grants and revenue sharing. The second largest source of municipal income in Nepal is the Local

Development Fee, which is being collected by the central government at the rate of 1 per cent on

certain imported goods (Lamichhane, 2012).

26

Figure 2.5: Source of Income of municipalities in Nepal, 2006/07

Source: Lamichhane (2012).

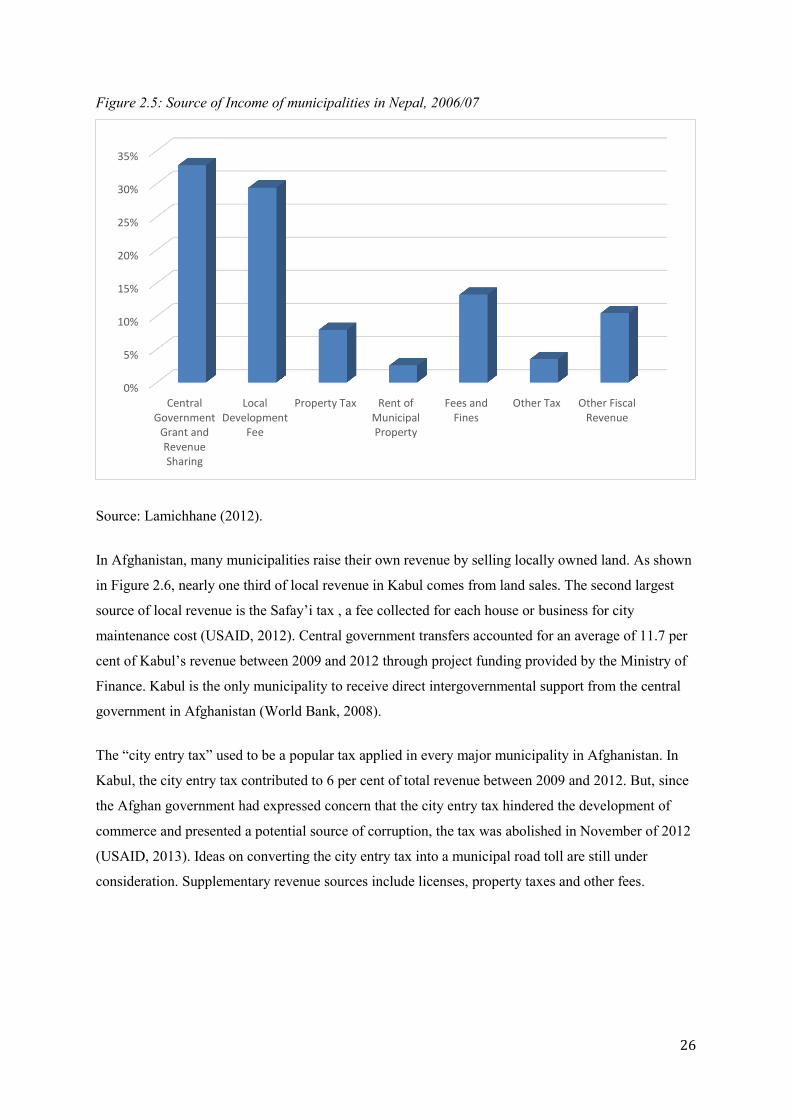

In Afghanistan, many municipalities raise their own revenue by selling locally owned land. As shown

in Figure 2.6, nearly one third of local revenue in Kabul comes from land sales. The second largest

source of local revenue is the Safay’i tax , a fee collected for each house or business for city

maintenance cost (USAID, 2012). Central government transfers accounted for an average of 11.7 per

cent of Kabul’s revenue between 2009 and 2012 through project funding provided by the Ministry of

Finance. Kabul is the only municipality to receive direct intergovernmental support from the central

government in Afghanistan (World Bank, 2008).

The “city entry tax” used to be a popular tax applied in every major municipality in Afghanistan. In

Kabul, the city entry tax contributed to 6 per cent of total revenue between 2009 and 2012. But, since

the Afghan government had expressed concern that the city entry tax hindered the development of

commerce and presented a potential source of corruption, the tax was abolished in November of 2012

(USAID, 2013). Ideas on converting the city entry tax into a municipal road toll are still under

consideration. Supplementary revenue sources include licenses, property taxes and other fees.

0%

5%

10%

15%

20%

25%

30%

35%

CentralGovernment

Grant andRevenueSharing

LocalDevelopment

Fee

Property Tax Rent ofMunicipalProperty

Fees andFines

Other Tax Other FiscalRevenue

27

Figure 2.6: Kabul Municipality Revenue *by Revenue Source (Averages for 2009-2012)

*Licenses include business license and vehicle license fees; Fees include market & parking fees and

construction fees

Source: USAID (2013).

Introduction of user charges, fees and licenses

User charges and fees comprise service charges (water, sewerage and parking), administrative fees

(building permits, registration) and business license fees. User charges are typically defined per unit

of consumption. They can promote an optimal level of consumption when the price equals the cost of

providing an additional unit of the service, which also referred to as marginal cost pricing. Some have

therefore argued that, “(whenever) possible, local public services should be charged for rather than

given away” (Bird 2001). However, getting prices right is easier said than done where the

infrastructure and capacity to set prices, measure usage, and collect fees are heavily constrained and

where many users live in abject poverty. Consequently, in a number of LDCs, user charges are

frequently set below costs, infrequently revised, and often inefficiently billed.

When setting their tariff structures, local governments typically try to take social justice concerns into

consideration and facilitate access to low-income households. Cross-subsidies, where richer segments

of the population subsidize access to services for the poor, have shown success in some countries.

0%

5%

10%

15%

20%

25%

30%

35%

28

One popular mechanism for cross-subsidies is a pricing system, whereby the per unit price of

consuming a municipal service, e.g. electricity, increases as more of it is consumed and may even be

free up to a designated level. Cross-subsidies are also possible between sectors. For example, cross-

subsidies are frequently used to reduce or eliminate user charges for health services, since these tend

to have a particular detrimental effect on the poor (Lagarde and Palmer, 2008). The elimination of

user charges for health services has led to significantly higher health system utilization rates. While

greater health care is likely to pay large dividends in the future, including through greater tax

revenues, the challenge for local governments is to replenish the lost revenue in the short and

medium-term through instruments like sectoral cross-subsidies, additional taxes or donor

contributions.

Whereas economic theory suggests that marginal cost pricing is the most efficient pricing method, it

works only in perfect market conditions where providers have complete information on the cost of the

product, as well as the opportunity cost. More practical methods include average cost pricing, where

expenditures required for providing a service are divided by the number of consumers or the volume

sold and average incremental pricing, which calculates how much it would cost to serve an additional

consumer based on the average cost price. There are also multipart tariffs, similar to those discussed

earlier, which include fixed charges for basic consumption and higher charges for greater

consumption and thus effectively cross-subsidize the consumption of low-income customers. Where a

clear pricing strategy is applied, average cost and multi-tariff bundling are more widespread than

marginal cost pricing, since these are easier to calculate and administer (World Bank, 2014).

The important role of intergovernmental transfers

There are no subnational governments in the world that can fully function without a certain level of

intergovernmental support. In practice, finance often does not follow function, and central

governments across the globe give local authorities more expenditure responsibilities than those can

finance from their own revenue sources. Generally, greater capacity to generate their own revenues

make subnational governments in developed countries less dependent on support from higher tiers of

governments than those in developing countries. Consequently, resource flows from higher to lower

tiers of governments average 70-72 per cent of local government funding in developing countries and

38-39 per cent in developed countries (Alam, 2014).

The traditional rationale for intergovernmental transfers is the objective for a welfare maximizing

government to reallocate resources between richer and poorer jurisdictions in order to reduce both

horizontal (same tiers of government) and vertical (different tiers of government) imbalances, and to

correct for externalities. The actual drivers for intergovernmental transfers can vary, however. Public

finance literature explores factors that are shaped by equity and efficiency considerations such as the

29

correction for vertical and horizontal imbalances. Public choice theory highlights how transfers can

become tools for political influence. Frequently, electoral concerns determine the distribution of fiscal

resources to local jurisdictions (Boex and Martinez-Vazquez, 2005). Political economy research

focuses on how intergovernmental transfers are shaped by political influence through the impact and

bargaining power of political interest groups. There is robust empirical evidence that local

governments with higher political representation per capita benefit from greater intergovernmental

transfers (Wright, 1974, Porto and Sanguinetti, 2001, Khemani, 2007, Caldeira, 2011).

The impact of intergovernmental transfers on local revenue generation remains under debate. Some

have argued that large unconditional intergovernmental grants lead to lump-sum tax reductions or

lower the incentives for local governments to collect fees and taxes, thus ‘crowding out’ own source

revenue mobilization. Others argue that most fiscal transfers are spent on the provision of public

goods and services, increasing local economic development and tax compliance, and consequently,

‘crowd in’ local tax revenues. Studies that highlight the crowding out effect mostly focus on more

developed countries with relatively well-developed fiscal systems and significant own source revenue

generation (Kalb, 2010; Zhuravskaya, 2000).

However, such capacity is highly constrained in most LDCs. In cases where local capacity to generate

own-source revenue is weak, intergovernmental transfers are a crucial lifeline and may further crowd

in local revenue generation. For example, evidence suggests that in Tanzania, a 1 per cent increase in

intergovernmental transfers leads to an extra 0.3-0.6 per cent increase in own source revenue

generation for local government authorities (LGAs) (Masaki, 2015). Moreover, intergovernmental

transfers are often the only regular source of local income for reasons of political interference in own

source revenue generation. In many LDCs, local governments are frequently dependent on central

government approval for taxes, fees and charges they wish to impose. In certain cases, local

governments may wait for years or even decades to get such approvals (see Lesotho Case Study).

Smoke (2015) argues that intergovernmental transfers make sense as part of smart division of

responsibilities between the central and local government based on their core advantages and

competencies. In this connection, the author highlights that “central governments have inherent

advantages in generating revenues and local and regional governments have inherent advantages in

providing certain key services, invariably necessitating intergovernmental transfers.” At the same

time, LRGs must be able to raise an adequate share of the resources to (i) reduce demands on central

budgets, (ii) create a fiscal linkage between benefits of local services and the costs of providing them,

and (iii) help repay loans on long-term capital investments (Smoke, 2015).

30

Intergovernmental transfers in LDCs

Figure 2.7 illustrates widely divergent sizes of intergovernmental transfers in LDCs, in particular in

Francophone and Anglophone Africa. Most Anglophone LDCs receive the majority of their income

through intergovernmental transfers. In Francophone and some other LDCs, the share of total local

resources to total public resources reveals some of the lowest ratios in the world (IMF, 2015).

Francophone countries tend to rely more on local taxes. However, those taxes are often set, collected

and disbursed by the central government, i.e. they are not “true” local taxes. The low levels of

transfers may also be the result of sectoral policies of the central governments that leave little

resources for local authorities, thus limiting resources and functions of local authorities and

compromising the decentralization process (UCLG, 2009).

Figure 2.7: Intergovernmental transfers in per cent of total local revenues in selected LDCs

Source: IMF Government Finance Statistics Database, accessed August 2016.

Yet, both groups of countries face enormous challenges in meeting their local expenditure, as

transfers are often neither adequate nor reliable and low central government support is not met with

adequate increases in local revenue generation. For example, in the case of Senegal, revenues at the

local level have increased over recent years but remain at a mere 6 per cent of the central tax

revenues. As a result, local resources remain insufficient to provide local basic public services.

Moreover, horizontal fiscal imbalances have become a problem: the resources of the ten poorest

0

20

40

60

80

100

Grey: Non-African LDCs Red: Francophone African LDCs Blue: Anglophone African LDCs

31

communes represent 1 per cent of the resources of the five richest ones (Caldeira, 2011)6. In Mali,

local taxes generate insufficient revenue and rely on a wide range of obsolete taxes that are

particularly difficult to collect.

The fact that LDCs with widely different transfer/total revenue ratios continue to face similar

development challenges at the local levels suggests that the share of central government transfers in

local revenues says little about the local authority’s capacity to generate sufficient own source

revenue. Whether the major source of subnational income comes from intergovernmental transfers or

local taxes does not matter if the total income is grossly inadequate. People will bear the

consequences in terms of poor quality and access of local service delivery. Cutting intergovernmental

transfer does not make sense where own-source revenue generation cannot fill the gap. To make

matters more complicated, international financial institutions, especially those that focus more on

overall macroeconomic stability than development, have frequently put pressure on LDCs to reduce

intergovernmental transfers in an effort to reduce central government deficits. Such a recommendation

must be weighed carefully against the adverse effects of lower transfers on access and quality of basic

services, especially where the capacity for own source revenue generation is low.

Surcharges as a complement to intergovernmental transfers

Surcharges are a form of subnational “piggybacking” on national or regional taxes, like income taxes.

For local surcharges, a higher level of government defines the tax base, collects both the tax and the

surcharge set by subnational governments, and remits the surcharge revenue to the local government.

While the national government collects the tax, surcharges are clearly local taxes in that local

governments are responsible for imposing the tax and spending the revenues.

This approach avoids the problems that occur when subnational jurisdictions define their tax base in

conflicting ways, use different apportionment formulas, and administer the tax in different ways. For

example, two local authorities may try to impose taxes on the same company since there are different

opinions as to where and in which subnational jurisdiction the firm operates. In such a case, it is more

practical for higher levels of governments to define the tax base and forward a share of the revenues

to the local authorities. However, surcharges are not a substitute for, but rather a complement to

intergovernmental transfers, since they do not provide for vertical or horizontal redistribution among

subnational jurisdictions. Looking ahead, more data and research is needed on how and to which

extent local surcharges are used effectively in LDCs.

6 Senegal is divided into eleven regions (règions) which are subdivided into 67 communes, 43 communes d’ arrondisements

which are further divided into 320 communautès Rurales (Caldeira, 2011).

32

The formulation of the most welfare-enhancing combination of local and central governments taxes is

a politically difficult balancing act. Another key challenge for central governments is to provide

incentives to local governments to collect all the taxes they are supposed to collect. While some

central government fund transfers have been linked to a reform agenda, there has been little

improvement in own source revenue collection in most cities (Habitat III, 2015). Frequently, politics

get in the way of empowering local governments to raise their own revenues (See Lesotho Case

Study).

33

(III) LDC experiences in improving municipal revenue generation

Lao PDR (1): Land titling as a road to better property taxation

Policy Lesson: Land titling initiatives must be accompanied by strong and transparent government

institutions in order to play a role in improving subnational revenue.

In 1975, the rise of the socialist government following a prolonged civil war meant that all land in

Laos became the property of the state. Despite this, land use rights became informally recognized over

time, and the government developed a system of administering and recording property transactions.

The decision in 1986 to turn towards market-oriented reforms in this sector was driven by the lack of

clear property rights and information as well as the fact that the majority of property transactions

occurred outside the purview of the government. In 1996, Laos’s national government, with donor

support, began a land titling project to provide a system of clear and enforceable land-use ownership

rights and developing a land valuation capacity. The project also supported national and provincial

governments in systematic land registration through mapping, computerization of land records,

development of a land registration system, and extensive training of government officials in the

process of land titling. It originally covered the Vientiane capital as well as urban and semi-urban

areas in four provinces, with four additional provinces added later. A second Land Titling Project,

also with donor support, built upon the first with efforts to further develop land policy and regulatory

framework, educate government officials, institute a land registration system, and accelerate land

titling through systematic registration. It also broadened the scope to all provinces of the country.

The first project resulted in the Law on Land of 1997, which formally established regulations for land

registration and administration. It also led to the registration of roughly 190,000 parcels of land,

which came at a time when registration was rare but fell significantly short of the original goal of

300,000. Efforts were hampered by initial shortages of government staff, technical issues, lack of

incentives for government officials, and lack of government funds. The nominal figures found in the

World Bank Implementation Completion and Results Report (ICR) suggest there was a remarkable

1087 per cent increase in government revenue from land taxes and land-related fees between fiscal

years 1995/1996 and 2004/2005; however, Laos’s high inflation over the period means that the real

gain in revenue was only 1.6 per cent over the entire nine year period and that land-based revenue

shrunk from .20 per cent of GDP to .14 per cent of GDP. The second project exceeded projections and

led to titling of approximately 382,000 parcels of land. It also coincided with an 86 per cent rise in

real land-related government revenue (FY 2002/2003-2008/2009); however, the rise was related

primarily to increases in land value determined to be unrelated to titling, and the project design did

not collect sufficient data to discern how much of an impact land titling had on government revenue.

Moreover, the revenue gains did not aid village and district revenue as much as they could have.

34

Anywhere between 4 and 60 per cent of the revenue stayed at the village level, of which 60 per cent

was used to pay the tax collector’s salary and 40 per cent is used to cover administrative expenditures.

At the district level, the money was used “mainly to pay for recurrent expenditures, including salary

and operational costs,” rather than service delivery or infrastructure projects. One issue is that Laos’s

government did not implement reforms or allocate special funding towards land administration and

tax collection, nor did donors successfully train government officials in these areas. Another is that

land registration fees varied wildly both between and within provinces, and they were not always

clearly stated, which called into question the integrity of the offices responsible for collecting them

and promoted informal transactions. Because the government of Laos did not commit to a long-term

land administration programme or allocate an adequate budget, the projects were donor-dependent

throughout their implementation, and with the withdrawal of donors in 2009, project sustainability has

come into serious doubt. Moreover, Laos has long struggled with transparency regarding land rights,

which severely limits the efficacy of land titles; there are even concerns that some land holders have

not received proper compensation when their land was expropriated by the government. There is no

evidence that either project led to a better regulatory framework or better enforcement of land rights,

or had discernible impacts on land values, local ability to borrow, or the frequency of land disputes.

A number of policy lessons emerge: For a land titling project to successfully impact government

revenues from land and property, government, from the local to national level, must first respect the

integrity of land rights, use eminent domain rationally and responsibly, and have clear legal and

regulatory systems in place to promptly settle disputes. Additionally, a government must commit to a

long-term programme of land administration and set up a transparent and well-funded body to ensure

sustainable impacts. Fees and taxes should be clear and uniform, and all concerned levels of

government should be mindful of administrative costs and have a plan to translate enhanced revenues

into better service and infrastructure delivery. Land titling must be introduced with broader policy and

regulatory reforms if it is to have any teeth. Lastly, in order to judge the impacts of a land titling

project, land values alone will not suffice; rather, a baseline survey, comparisons between titled and

untitled land, and data on the number of registered land transactions is necessary to determine whether

and how much titling matters. Land titling is a powerful tool for property/land tax efficacy, but it must

be treated as only one piece of the puzzle.

Sources: World Bank (2006. 2010a,b, 2016a,c)

35

Mozambique (1): Facilitating intergovernmental transfers through implementation of a treasury single account

Policy Lesson: Unifying public revenue and expenditure data through an electronic system can help

build trust with international donors and facilitate state-to-local government revenue transfers.

Over the past 18 years, Mozambique has embarked on a country-wide effort towards municipalisation

in order to bring the decision-making process for many government functions closer to the people

affected. When Mozambique began the process in 1998, 33 municipalities were established,

expanding to 53 in 2013. In Mozambique, municipalities are locally elected bodies that govern their

electorate directly and whose responsibilities generally include things such as service infrastructure,

public parks, public hospitals, and local roads. Mozambique has also strengthened and expanded its

use of districts governments, which are appointed by the federal government and responsible for

implementing federal policies at a more localized level.

One of the main challenges for Mozambique’s municipalities since decentralization has been trying to

match new revenue to new responsibilities, as the two often do not come hand in hand. Under current

law, municipalities are expected to make own-source revenue two thirds of their total, but most

struggle with poor revenue generation due to a lack of human, material, and financial resources as

well as poor tax implementation. The result is a lack of implementation capacity for basic services

including water, sanitation, electricity, roads, and housing; 45.5 per cent of urban residents lack access

to electricity, and 57.6 per cent lack access to improved sanitation. While there are laws on the books

for municipal taxes, the implementation of these laws is typically limited and haphazard. Municipal

property taxes and real estate transaction taxes in Mozambique are supposed to align with the current

market value of a given property, but property values for the most part have not been updated since

the colonial era (pre-1975), which means that many properties end up undervalued. Municipalities

own all land within their borders, which allows them to sell licenses for any land targeted for new

development, but this system is typically not coupled with a property tax registry, so often

municipalities receive a one-time windfall but not sustainable revenue. The last major potential

revenue source, the economic activity tax, is supposed to track commercial and industrial production

but instead is administered at a set rate by area, which limits its effectiveness.

With these limitations in place, most municipalities have failed to improve service delivery and many

refuse new responsibilities, knowing that they are often more of a burden than an opportunity. The

federal government’s response has been to put into place enhanced systems of government transfers

and accountability. It has established the Municipal Compensation Fund, which is a provision in the

federal budget that designates a minimum of 1.5 per cent of fiscal revenue for non-conditional use by

cities, as well as the Investment Fund for Municipal Initiative, which designates another 0.75 per cent

36

of federal fiscal revenue for conditional use, taking into account municipalities’ infrastructure needs

and justifications for funding requests. One of the main drivers behind the federal government’s push

for fiscal decentralization has been the implementation of a treasury single account (TSA) known as

e-SISTAFE, a unified electronic system that tracks the allocation, management, and spending of

government funds across all levels, from the ministry of finance down to municipal governments. The

legislation authorizing the development of e-SISTAFE was in part the result urgings by international

donors in 2002, and its implementation was aided by the IMF. It was fully implemented across all

levels of government in 2007. E-SISTAFE allows government (and international) officials to better

track where money is sent, helps budgets better align with regulations, and makes local governments

more accountable for the money they receive. This has helped make federal legislators and officials

more comfortable with the idea of increasing government transfers to local governments. State-to-

local government transfers went up from $23.4 million (1.17 billion Meticais) in 2010 to $60 million

(3.13 billion Meticais) in 2015. At the same time, much of the funding for federal initiatives has been

delegated to the district level. Between 2007 and 2016, district fiscal capacity increased from just 3

per cent of the total central government budget to 17 percent. Moreover, the transparency e-SISTAFE

provides has increased the willingness of international donor agencies to provide general budget

support to Mozambique’s government, rather than sector-specific or project-specific funding.

However, while it has helped improve the flow of government transfers, e-SISTAFE has not

addressed the other part of the revenue equation, local revenue generation. There is no such system to

track things like property valuations, commercial revenues, and land license fees; local own-source

revenues remain anemic. As a result, municipalities’ implementation capacities remain limited, access

to basic infrastructure has not significantly improved, citizens are frustrated, and they are not on a

path towards self-sustainability. E-SISTAFE is an example of how a treasury single account can play

a key role in decentralization efforts.

Sources: Pattanayak, Sailendra and Israel Fainboim(2010); World Bank, 2016c ; Dabán and Pesoa

(2007).

Ethiopia: Implementing a land value capture system during rapid urbanization

Policy Lesson: Land value capture systems differ among LDCs depending on the legal context, as

well as socio-economic and regulatory environment. Land value capture can provide additional

resources for local capital investments, but their implementation requires significant administrative

capacity. The tying of land value reform to the introduction and systematization of property taxes