71

STRENGTHENING THE EUROPEAN UNION EMISSIONS TRADING SCHEME AND RAISING CLIMATE AMBITION Facts, Measures and Implications Report by Öko-Institut Hauke Hermann, Felix Chr. Matthes

STRENGTHENING THE EUROPEAN UNION

EMISSIONS TRADING SCHEME

AND RAISING CLIMATE AMBITION

Facts, Measures and Implications

Report by Öko-Institut

Hauke Hermann, Felix Chr. Matthes

Öko-Institut (Institute for Applied Ecology) Strengthening the EU ETS

- 3 -

Executive Summary

EU energy and climate policy faces manifold challenges. The debate on tougher emis-

sions reduction targets for 2020 is gaining momentum, the need for an integrated

framework and long-term targets as well as consistent and interim targets for 2020 and

2030 is becoming clear and adjustments to the EU’s Emissions Trading Scheme (EU

ETS) seem to be indispensable to preserve its role as a central pillar of the EU’s ener-

gy and climate policy mix.

The EU is very close to fulfilling its recent greenhouse gas emission commitments for

2020. Including the committed and projected use of external emissions reduction cred-

its, only a gap of three percentage points remains, which is theoretically already gap-

filled with the cap of the EU ETS by 2020. The current situation is also challenging for

the EU ETS, which is facing significantly falling allowance prices. The fundamental rea-

son for this price trend is the massive supply of EU emission allowances (EUA) and

emission reduction credits which exceeds the demand significantly. This surplus was

950 million EUA in 2011, will reach approx. 2 billion EUA in 2013 and still amount to 1.4

billion EUA in 2020. It results from huge entitlements for the use of external emission

reduction credits from CDM and JI and the long-term impacts of the economic crisis.

Only a minor contribution to the surplus results from the support for renewable energy

sources (RES) with complementary policies to the EU ETS because the recent growth

plans for RES match quite well with the assumptions made for cap-setting in 2008.

Two different approaches were used to analyse potential interventions and adjustments

of the EU ETS. Firstly, a set aside of 1,400 million allowances combined with a tighter

cap for the EU ETS by increasing the linear reduction factor from a recent 1.74 % to

2.25 % from 2014 onwards. Secondly, the adjustment of the linear reduction factor was

derived from more ambitious goals for the total domestic emission reductions. An in-

crease of the linear reduction factor from 1.74 % to 2.6 % would be consistent with a

25 % domestic emission reduction, compared to 1990, and a linear reduction factor of

3.9 % would refer to a domestic target of -30 %. The analysis clearly shows that a sig-

nificant and timely reduction of the surplus is only possible with the combination of a

set aside and adjustments of the cap by increasing the linear reduction factor. Stand-

alone measures like a set aside on the one hand or the adjustments of the linear reduc-

tion factor on the other hand will have only extremely limited impacts on the surplus for

the next decade. However, set asides will only have an impact if the market partici-

pants believe that the respective amount of allowances will be held back for a sufficient

period of time (at least a decade) or will be retired. Furthermore, tighter caps for the EU

ETS will only achieve the intended effects if they are not complemented by an increase

in the entitlements for the use of external credits.

An assessment of the different options with a relatively simple allowance price model

enables key lessons on different types of interventions to emerge:

A stand-alone approach for a set aside which will be fully reintroduced to the

market before 2020 will have negligible price effects. The EUA price would re-

main at a level of less than 8 €/EUA in 2013 and approx. 14 €/EUA in 2020.

Strengthening the EU ETS Öko-Institut (Institute for Applied Ecology)

- 4 -

A set aside for a decade or longer will increase prices by about 2.50 €/EUA in

2013 and by about 4 €/EUA in 2020.

If the linear reduction factor is increased to 2.25 % alone, the price effect in

2013 would be very low (1 €/EUA) and slightly higher in 2020 (2 to 3 €/EUA).

If a long-term set aside is combined with a tighter linear reduction factor of

2.25 %, the price effects would be approx. 4.50 €/EUA for 2013 and about

15 €/EUA for 2020.

A tighter cap for aviation (applying the linear reduction factor of 2.25 % also to

the sub-cap for aviation) would further increase the EUA price by € 0.50.

The EUA price effects of a long-term set aside and an increase of the linear re-

duction factor to 2.6 % could increase the price in 2013 by about 5 €/EUA and

by up to 17 €/EUA in 2020.

The combination of a long-term set aside and an increase of the linear reduction

factor by 3.9 % would lift the EUA price by up to € 7 in 2013 and potentially and

with comparatively high uncertainties by more than € 20 by 2020.

Based on this analysis a set of four recommendations can be put forward for adjust-

ment of the EU ETS:

Firstly, a set aside can reduce the allowance surplus within the EU ETS in the

short term. However, the respective amount of allowances should be held back

for a period of a decade or more or retired at the earliest point in time.

Secondly, the long-term cap should be tightened by a significant increase of the

linear reduction factor, preferentially from 2014 onwards. The effective increase

is subject to fundamental political decisions on the overall emission reduction

targets. However, an increase of the linear reduction factor to less than 2.6 %

will be not consistent with overall targets of 25 % domestic emission reduction

and a factor of less than 3.9 % will not be consistent with an overarching target

of 30 % domestic action by 2020.

Thirdly, no additional entitlements for the use of external emission reduction

credits should be created in the process of tightening the EU ETS cap.

Fourthly, the implementation of high impact complementary policies (e.g. the

impact of the upcoming Energy Efficiency Directive on emissions in the EU ETS

sectors), a long-lasting change in fundamental drivers for baseline emissions

(e.g. a significantly lower economic growth for a longer period) or other changes

in the regulatory framework (e.g. the discontinuation of significant parts of the

aviation sector as net buyers in the market) should be reflected by a strictly

rule-based and high-threshold provision to lower the cap in the EU ETS.

These kinds of structural improvements could help to preserve the key role of the EU

ETS in an enabling policy mix for ambitious, effective and efficient climate policy.

Öko-Institut (Institute for Applied Ecology) Strengthening the EU ETS

- 5 -

Zusammenfassung

Die Energie- und Klimapolitik der Europäischen Union steht vor vielfältigen Herausfor-

derungen. Mit zunehmender Intensität werden ambitionierte Emissionsreduktionsziele

für 2020 diskutiert, die Notwendigkeit eines integrierten Ansatzes und langfristiger Kli-

maschutzziele sowie damit konsistenter Zwischenziele für 2020 und 2030 werden im-

mer deutlicher. Gleichzeitig erscheinen Veränderungen am Emissionshandelssystem

der Europäischen Union (EU ETS) unabdingbar, wenn dieses Instrument seine Rolle

als zentrales Element im Portfolio der europäischen Energie- und Klimapolitik behalten

soll.

Die bisherigen Treibhausgas-Emissionsminderungsziele für das Jahr 2020 hat die EU

bereits sehr weitgehend erfüllt. Unter Berücksichtigung der bereits realisierten und er-

wartbaren Minderungsgutschriften aus externen Projekten verbleibt nur noch eine Ziel-

erreichungslücke von etwa 3 Prozentpunkten, die faktisch durch das feste Emissions-

ziel des EU ETS bereits geschlossen ist. Aus dieser aktuellen Situation entsteht jedoch

für das EU ETS eine durchaus problematische Situation, vor allem angesichts massiv

zurückgehender Preise für die Emissionsberechtigungen des EU ETS (European Uni-

on Allowances – EUA). Fundamental sind diese Preisentwicklungen durch das sehr

große Angebot an Emissionsberechtigungen und externen Minderungsgutschriften

erklärbar, das den Bedarf erheblich überschreitet. Dieser Überschuss belief sich auf

950 Millionen EUA im Jahr 2011, wird bis 2013 auf etwa 2 Milliarden EUA ansteigen

und im Jahr 2020 immer noch 1,4 Milliarden EUS betragen. Hauptgründe dafür sind die

umfangreich zugelassene Nutzung externer Emissionsminderungsgutschriften aus

dem Clean Development Mechanism (CDM) und Joint Implementation (JI) sowie die

längerfristigen Auswirkungen der Finanz- und Wirtschaftskrise. Eine nur untergeordne-

te Rolle spielt dagegen der Überschuss, der sich aus der Förderung erneuerbarer

Energien mit Instrumenten jenseits des EU ETS ergibt, entsprechen doch die aktuellen

Ausbaupläne für erneuerbare Energien vergleichsweise gut den Annahmen, die im

Jahr 2008 bei der Festlegung des Emissionsziels für den EU ETS (Cap) getroffen wur-

den.

Die Analyse unterschiedlicher Veränderungen bzw. Anpassungen des EU ETS erfolgte

aus zwei unterschiedlichen Perspektiven. Erstens wurde die Herausnahme (Set aside)

von 1,4 Milliarden EUA aus dem EU ETS in Kombination mit einem ambitionierteren

Cap untersucht, die sich aus einer Erhöhung des linearen Reduktionsfaktors von bisher

1,74 % auf 2,25 % ab 2014 ergibt. Zweitens wurden Anpassungen des linearen Reduk-

tionsfaktors aus stärkeren Minderungszielen für die Gesamtemissionen der EU abge-

leitet. Eine ausschließlich in der EU erbrachte Emissionsminderung von 25 % gegen-

über 1990 entspricht dabei einer Erhöhung des linearen Reduktionsfaktors von 1,74

auf 2,6 %, eine Erhöhung des entsprechenden Ziels auf -30% wäre konsistent mit ei-

nem Anstieg des linearen Reduktionsfaktors auf jährlich 3,9 %. Die Analysen verdeutli-

chen, dass eine maßgebliche und rechtzeitige Rückführung des Überschusses an

Emissionsrechten nur mit der Kombination eines Set aside und einer Anpassung des

Caps mittels Verschärfung des linearen Reduktionsfaktors erreicht werden können.

Strengthening the EU ETS Öko-Institut (Institute for Applied Ecology)

- 6 -

Isolierte Ansätze wie ein Set aside für sich oder die Anpassung des linearen Redukti-

onsfaktors allein haben dagegen für die nächste Dekade nur sehr begrenzte Wirkun-

gen auf die Entwicklung des Überschusses an Emissionsberechtigungen. Dessen un-

geachtet kann ein Set aside nur dann eine Wirkung entfalten, wenn die Marktteilneh-

mer zu der Einschätzung gelangen, dass die entsprechenden Zertifikatsmengen für

einen ausreichend langen Zeitraum (mindestens eine Dekade) aus dem Markt ge-

nommen oder stillgelegt werden. Darüber hinaus werden verschärfte Caps im EU ETS

nur dann die intendierten Effekte zeitigen, wenn sie nicht mit einer Erhöhung der Nut-

zungsberechtigungen für externe Emissionsminderungsgutschriften einhergehen.

Die Bewertung der unterschiedlichen Modelle mit einem vergleichsweise einfachen

Modell zur Abschätzung von Preisen für Emissionsberechtigungen führt zu folgenden

zentralen Ergebnissen:

Ein Set aside ohne weitere Ergänzungen, das vor 2020 wieder vollständig dem

Markt zur Verfügung gestellt wird, hat nur vernachlässigbare Effekte auf den

Preis für Emissionsberechtigungen. Der Preis für Emissionsberechtigungen

würde auf einem Niveau von unter 8 €/EUA im Jahr 2013 und ungefähr

14 €/EUA im Jahr 2020 verbleiben.

Ein Set aside, das für eine Dekade oder länger aus dem Markt genommen wird,

erhöht die Zertifikatspreise um etwa 2,50 €/EUA im Jahr 2013 und ungefähr

4 €/EUA in 2020.

Wenn nur der lineare Reduktionsfaktor auf 2,25 % erhöht wird, ergibt sich für

das Jahr 2013 nur ein geringfügiger Preiseffekt (1 €/EUA) und für 2020 eine et-

was größere Zertifikatspreiserhöhung (2 bis 3 €/EUA).

Wenn ein längerfristig angelegtes Set aside mit einem verschärften linearen

Reduktionsfaktor von 2,25 % kombiniert wird, so ergeben sich Preiserhöhungen

von etwa 4.50 €/EUA für 2013 und ungefähr 15 €/EUA für 2020.

Ein ambitioniertes Cap für den Flugverkehr (über die Anwendung des linearen

Reduktionsfaktors von 2,25 % auch für diesen Teil des EU ETS) würde den

EUA-Preis um weitere 0,50 € erhöhen.

Als Effekt eines längerfristig angelegten Set aside in Kombination mit einer Er-

höhung des linearen Reduktionsfaktors auf 2,6 % könnte sich der Zertifikats-

preis im Jahr 2013 um 5 €/EUA und um bis zu 17 €/EUA im Jahr 2020 erhöhen.

Das Zusammenwirken eines längerfristig angelegten Set aside und einer Ver-

schärfung des linearen Reduktionsfaktors auf 3,9 % würde die EUA-Preise in

2013 um etwa 7 € und bis 2020 – bei vergleichsweise hohen Unsicherheiten –

um mehr als 20 € erhöhen.

Auf der Grundlage dieser Analysen ergeben sich für das EU ETS insgesamt vier Emp-

fehlungen:

Erstens kann mit einem Set aside der Zertifikatsüberschuss im EU ETS kurzfris-

tig reduziert werden. Die entsprechende Menge an Emissionsberechtigungen

Öko-Institut (Institute for Applied Ecology) Strengthening the EU ETS

- 7 -

sollte jedoch für eine Dekade oder mehr zurückgehalten oder frühestmöglich

stillgelegt werden.

Zweitens sollte das langfristige Cap über eine deutliche Erhöhung des linearen

Reduktionsfaktors verschärft werden, die vorzugsweise ab 2014 wirksam wer-

den sollte. Das Ausmaß dieser Erhöhung resultiert aus grundlegenden politi-

schen Entscheidungen zum übergeordneten Minderungsziel für die gesamten

Treibhausgasemissionen. Eine Erhöhung des linearen Reduktionsfaktors von

weniger als 2,6 % wäre jedoch nicht konsistent zu einem Minderungsziel für die

Emissionen in der EU von 25 %, eine Erhöhung um weniger als 3,9 % wäre

nicht konsistent mit einem Ziel für Emissionsminderungen in der EU von 30%

bis zum Jahr 2020.

Drittens sollten die Budgets für die Nutzung externer Emissionsminderungsgut-

schriften im Zuge einer Verschärfung des Caps für den EU ETS nicht erhöht

werden.

Viertens sollte die Umsetzung von zusätzlichen Politiken und Maßnahmen mit

weitreichenden Emissionsminderungswirkungen (z.B. die anstehende EU-

Richtlinie zur Energieeffizienz) sowie langfristig wirksame Veränderungen ent-

scheidender Treibergrößen für die Referenzentwicklung bei den Emissionen

(z.B. ein längerfristig deutlich verringertes Wirtschaftswachstum) oder andere

Änderungen (die z.B. den Wegfall eines Teils der Nachfrage aus dem Flugver-

kehr bewirken könnten) über eine entsprechende Eingriffsregelung für eine Ver-

ringerung des Caps berücksichtigt werden, die jedoch strikt regelbasiert sowie

mit hohen Eingriffsschwellen ausgestaltet werden sollte.

Solcherart ausgestaltete, strukturellen Verbesserungen könnten dazu beigetragen, die

Schlüsselrolle des EU ETS in einem nachhaltigen Portfolio ambitionierter, effektiver

und effizienter Klimapolitik zu bewahren.

Öko-Institut (Institute for Applied Ecology) Strengthening the EU ETS

- 9 -

Contents

Executive Summary .................................................................................................................... 3

Zusammenfassung ...................................................................................................................... 5

1 Introduction, scope and structure of the analysis ......................................................... 13

2 Trends and targets for the greenhouse gas emissions of the EU ................................ 16

2.1 Trends and targets for total greenhouse gas emissions of the EU .......................................... 16

2.2 Cap under the EU ETS from 2005 to 2020 and beyond .......................................................... 18

3 The recent problem: Allowance surplus from 2008 to 2011 .......................................... 23

3.1 Introduction, scope and structure of the analysis .................................................................... 23

3.2 Trend of verified emissions in the EU ETS for 2008 to 2011 ................................................... 23

3.3 Free allocation for 2008 to 2011 .............................................................................................. 24

3.4 Auctions and sales for 2008 to 2011 ....................................................................................... 24

3.5 Use of CDM and JI credits from 2008 to 2011 ........................................................................ 24

3.6 Demand and supply balance for 2008 to 2011 ........................................................................ 24

4 The future challenge: Projection for the EU ETS surplus until 2020 ........................... 26

4.1 Introduction, scope and structure of the analysis .................................................................... 26

4.2 Baseline emission trends for the EU ETS from 2012 to 2030 ................................................. 26

4.3 Free allocation from 2012 to 2020 ........................................................................................... 33

4.4 Auctions and sales from 2012 to 2020 .................................................................................... 34

4.5 Use of CDM and JI credits from 2012 to 2020 ........................................................................ 35

4.6 New entrant reserve for the second trading period ................................................................. 38

4.7 Total supply and demand balance for 2012 to 2020 ............................................................... 39

5 Interim summary: Demand and supply balance 2008 to 2020 ...................................... 41

6 Analysis of current proposals for intervention .............................................................. 44

6.1 Introduction, overview and structure of the analysis ................................................................ 44

6.2 Specification of the options for the analysis ............................................................................ 45

6.3 Reduction of the surplus in the EU ETS .................................................................................. 48

6.4 Potential range of price effects ................................................................................................ 50

6.4.1 Methodological approach .......................................................................................... 50

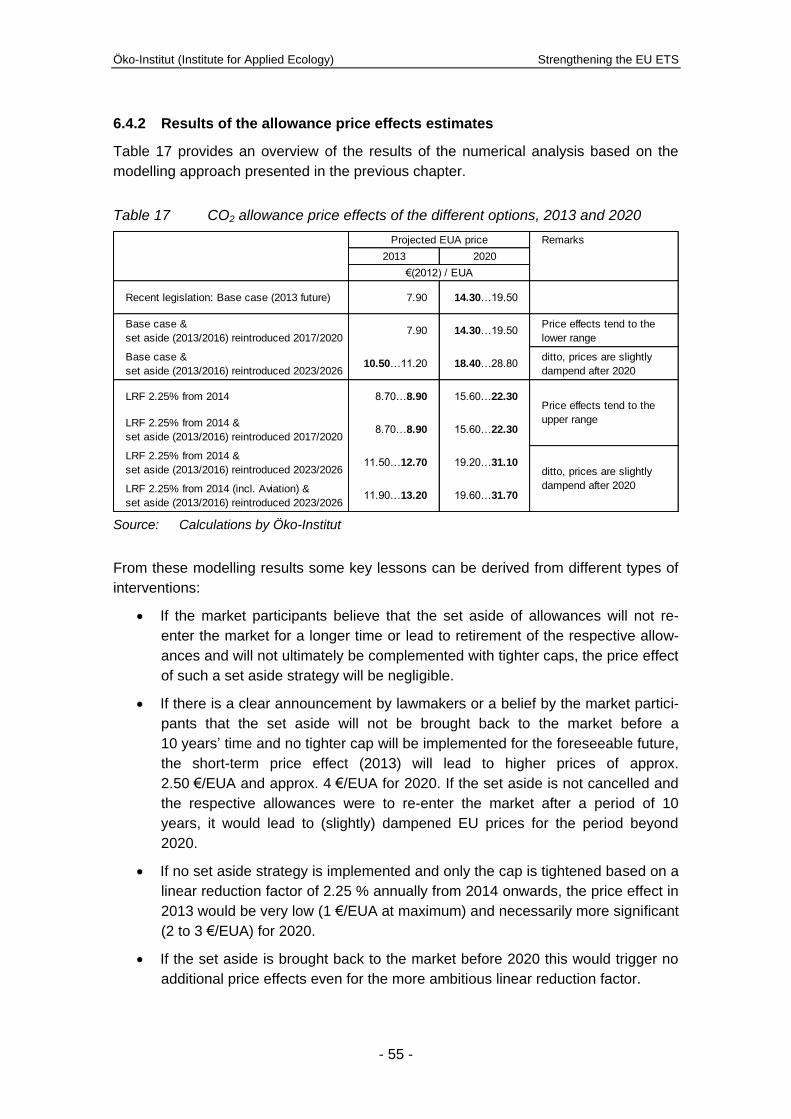

6.4.2 Results of the allowance price effects estimates ....................................................... 55

7 More ambitious greenhouse gas emission reduction targets for the EU:

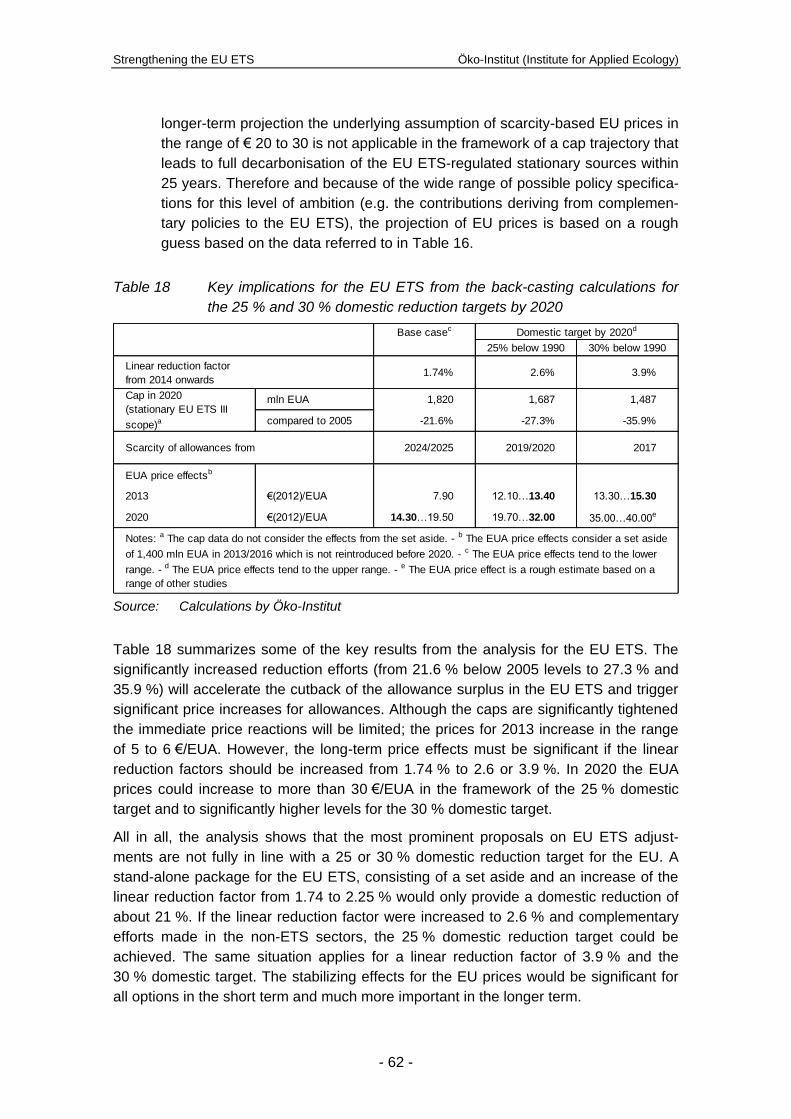

Analysis of implications for the EU ETS ......................................................................... 57

8 Summary and conclusions ............................................................................................... 63

9 References ......................................................................................................................... 67

Strengthening the EU ETS Öko-Institut (Institute for Applied Ecology)

- 10 -

List of tables

Table 1 Cap references for the second trading period of the EU ETS ........... 18

Table 2 Comparison of approaches to quantify the cap for the third trading period of the EU ETS (scope of the second period), 2013-2020 ......................................................................................... 20

Table 3 Cap for the EU ETS in the third trading period, 2013-2020 .............. 21

Table 4 Surplus of allowances in the EU ETS, 2008-2011 ............................ 25

Table 5 Updated baseline emission trends for the EU ETS sectors, 2005-2030 ......................................................................................... 33

Table 6 Amount of free allocation, 2008-2020 ............................................... 33

Table 7 Amount of free allocation from the new entrant reserve, 2013-2020 ......................................................................................... 34

Table 8 Amount of allowance auctions and sales, 2008-2020 ....................... 35

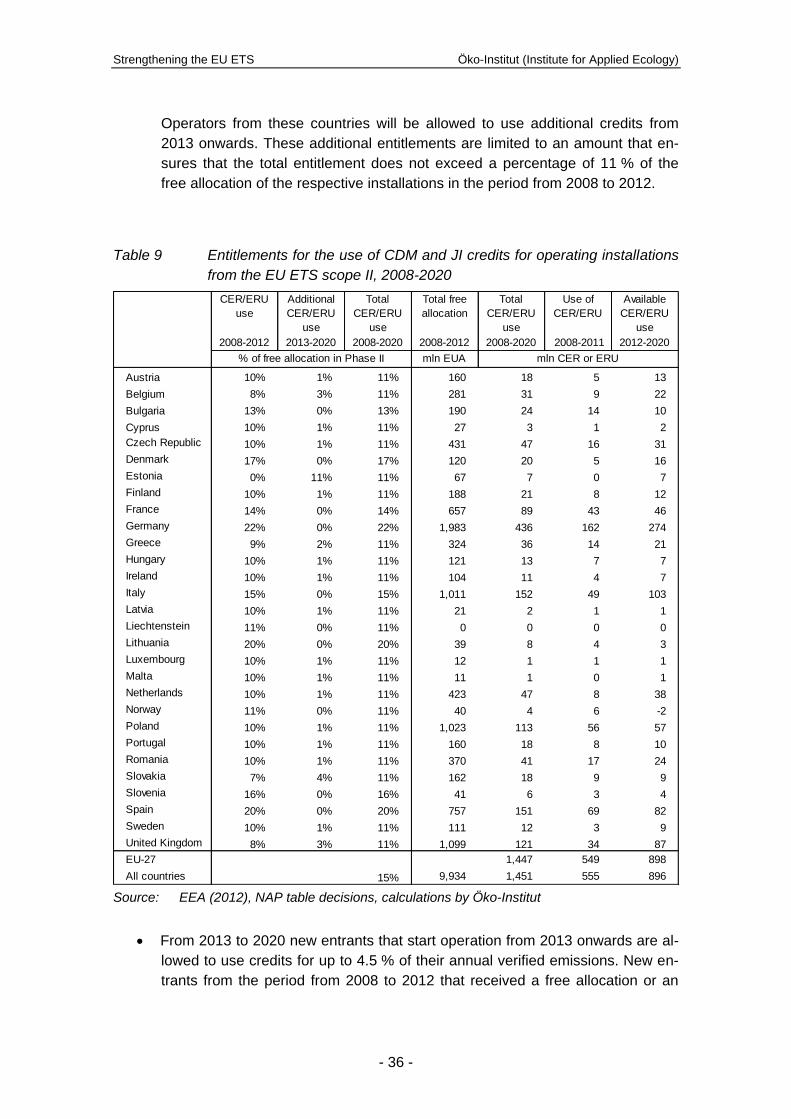

Table 9 Entitlements for the use of CDM and JI credits for operating installations from the EU ETS scope II, 2008-2020 .......................... 36

Table 10 Total entitlements for the use of CDM and JI credits, 2008-2020 .................................................................................................. 38

Table 11 Comparison of cap, free allocation, auctions and sales, 2008-2012 ......................................................................................... 38

Table 12 Demand and supply balance, 2012-2020 ......................................... 39

Table 13 Demand and supply balance for the second and third trading period, 2008-2020 ............................................................................. 41

Table 14 Additional reduction efforts resulting from different options to reduce the surplus in the EU ETS, 2013-2030 ................................. 47

Table 15 Projection for the supply of Certified Emission Reductions (CERs) eligible under EU ETS rules from 2013 to 2020 ................... 52

Table 16 Allowance price projections for the EU ETS from the EU Energy Roadmap 2050, 2020-2040 .................................................. 53

Table 17 CO2 allowance price effects of the different options, 2013 and 2020 ........................................................................................... 55

Table 18 Key implications for the EU ETS from the back-casting calculations for the 25 % and 30 % domestic reduction targets by 2020 ................................................................................. 62

Öko-Institut (Institute for Applied Ecology) Strengthening the EU ETS

- 11 -

List of figures

Figure 1 Total greenhouse gas emission trends and goals for the European Union (excluding LULUCF and including international aviation), 1990-2050 ..................................................... 17

Figure 2 Evolution of the caps for the EU ETS, 2005-2050 ............................ 22

Figure 3 Comparison of GDP projections for ETS-relevant modelling exercises for the European Union, 2005-2030 ................................. 27

Figure 4 Comparison of CO2 emission abatement contributions from renewable energy sources in the power sector for the EU, 2005-2020 ......................................................................................... 29

Figure 5 Update of the baseline projection for the EU ETS (scope of the second trading period), 2020 ...................................................... 30

Figure 6 Comparison of historical CO2 emissions data and baseline projections for the EU ETS (scope of the second period and aviation), 2005-2030 ......................................................................... 31

Figure 7 Evolution of the surplus in the EU ETS, 2008-2020 .......................... 42

Figure 8 Comparison of the effects of different options to reintroduce the set aside on the surplus in the EU ETS at a cap level based on the linear reduction factor of 1.74 %, 2013 to 2030 .......... 48

Figure 9 Comparison of the effects of options to implement an increased linear reduction factor on the surplus in the EU ETS, 2013 to 2030 ............................................................................ 49

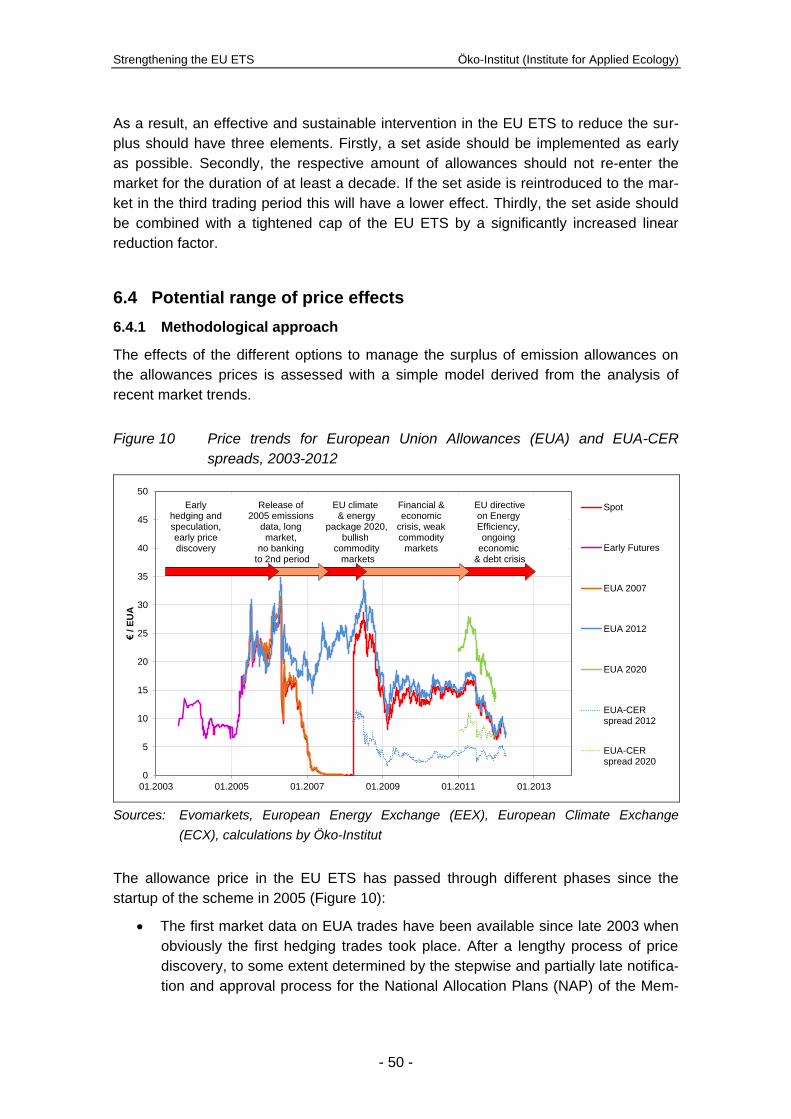

Figure 10 Price trends for European Union Allowances (EUA) and EUA-CER spreads, 2003-2012 ......................................................... 50

Figure 11 Discounted CO2 allowance prices for different periods of oversupply......................................................................................... 54

Figure 12 Total and domestic emission reductions according to the 2008 Climate and Energy Package, 2020 ........................................ 58

Figure 13 Adjustments of the ETS and the switch to more ambitious EU targets for greenhouse gas emission reductions in 2020 ........... 60

Öko-Institut (Institute for Applied Ecology) Strengthening the EU ETS

- 13 -

1 Introduction, scope and structure of the analysis

The climate and energy policy of the European Union (EU) and its Member States is

framed by the energy and climate package of 2008 which includes a set of binding tar-

gets for greenhouse gas emission reductions and the deployment of renewable energy

sources and a broad range of respective policies and measures. However, the Europe-

an climate and energy policy faces a series of challenges:

The EU has made significant progress towards meeting its unilaterally envis-

aged target of 20 % greenhouse gas reduction for the period from 1990 to

2020. However, the broad range of domestic action in many countries world-

wide, among them some important emerging countries (China, India, Brazil,

South Africa etc.) as well as key OECD countries (parts of the USA, Australia,

South Korea, Mexico etc.) challenge to the EU to tighten its emission reduction

efforts.

Due to several factors the greenhouse gas-based European Union Emissions

Trading Scheme (EU ETS) faces serious challenges in terms of its role as a

central and EU-wide pillar of the EU’s climate policy mix. The significant drop in

emission allowance prices and the obvious lack of scarcity in the market create

a need for appropriate action.

The EU ETS is thus at the core of a debate on the wider topic of future emissions re-

duction efforts of the EU (which are significantly framed by the EU ETS) as well as on

the EU ETS as a key economic instrument which combines environmental effective-

ness and economic efficiency:

The EU ETS generates a price on carbon dioxide (CO2) and other greenhouse

gases released into the atmosphere by the regulated entities. The market-

based price discovery for the costs of emission abatement creates a dynamic

long-term framework for emission reductions in the regulated sectors.

The EU ETS creates an extremely transparent quantitative framework for long-

term emission reduction strategies. The cap and its development over time

without a sunset clause provides clear signals for policy makers, the regulated

entities and the public of the trajectory of emissions and the contribution to

emission reduction that will be delivered by the regulated sectors.

The EU ETS will generate significant revenue streams after the main allocation

mechanisms of the scheme are shifted to the auctioning of allowances from

2013 onwards. Significant parts of these revenue streams should be available

for national, European and international climate financing.

This threefold role of the EU ETS should also be considered in the framework of the

recent challenges to the EU ETS.

After the significant price drop of CO2 allowances within the EU ETS (European

Union Allowances – EUA) after the financial and economic crisis, the price sig-

nal from the EU ETS no longer delivers sufficient price signals for investments

Strengthening the EU ETS Öko-Institut (Institute for Applied Ecology)

- 14 -

in low-carbon technologies. Given the emerging re-investment cycle for sectors

with long-lasting capital stocks (e.g. the power sector) this creates a major chal-

lenge for the EU ETS because of a risk of lock-in into CO2-intensive infrastruc-

tures.

The contributions of the EU ETS to climate financing will be much less signifi-

cant than originally assumed. This creates a problem for specific support pro-

grammes set up by the European Union (e.g. the financing of innovative tech-

nologies from the auctioning of 300 million allowances from the new entrants

reserve) as well as the wide range of climate financing efforts by the Member

States (e.g. the national and the international climate initiative from the German

energy and climate fund which will absorb fully the revenues from allowance

auctions in Germany).

The recent trajectory for the cap of the EU ETS is not fully consistent with the

long-term emission target of the EU to reduce greenhouse gas emissions by 80

to 95 % by the middle of this century, compared to 1990 levels, as well as con-

sistent interim emission reduction targets for 2020 and 2030, e.g. 30 % and

55 %, respectively. Furthermore, the emission reduction pathway of the EU

ETS is subject to change if the EU needs to increase its efforts in the context of

the activities abroad (which often include the set-up of EU ETS-like mecha-

nisms and underline the important function of the EU ETS as a role model).

After eight years of operation (2005-2012) and even after a major re-adjustment for the

trading periods from 2013 onwards, the EU ETS faces an emerging debate on how to

fix the problems mentioned above. However, these debates should reflect different

dimensions which interact with each other:

What are the main drivers for the recent problems that the EU ETS is facing?

What are the options for addressing these problems, which effects would these

options have over time and how could these options fit into the needs for ad-

justments of the overall climate policy framework?

The analysis presented in this study is based on a detailed analysis of a range of is-

sues, which are related to the two questions specified above:

In chapter 2 the most recent trends as well as the targets for total greenhouse

gas emissions and the evolution of the long-term cap for the EU ETS are de-

scribed in some detail.

Chapter 3 deals with the supply and demand for emission allowances and offset

credits in the first four years of the recent trading period and specifies the bal-

ance between demand and supply based on historical data.

In chapter 4 a comprehensive analysis is presented on the demand and supply

of allowances for the remaining year of the second period and the upcoming

third period up to 2020.

Öko-Institut (Institute for Applied Ecology) Strengthening the EU ETS

- 15 -

Chapter 5 summarizes the demand and supply situation for the whole period

from 2008 to 2020 and specifies the main sources for the surplus of emissions

allowances by 2020.

Chapter 6 presents the analysis of some options for adjustments of the EU ETS

to address the key challenges for the next decade, including the effects on al-

lowance prices which can be assumed. The starting points for this analysis are

prominent political proposals taken from the recent debates on the EU ETS.

In chapter 7 the approaches to addressing the specific EU ETS challenges are

set into context with tightened overall emission reduction targets for the Euro-

pean Union by 2020 and beyond. These proposals on adjustments for the EU

ETS are derived from ambitious greenhouse gas reduction targets for domestic

action by 2020 based on a back-casting approach.

Chapter 8 provides a series of conclusions derived from the quantitative and

qualitative analysis.

It should be highlighted that the analysis is focused on key issues of demand and sup-

ply of allowances in a longer-term perspective.

Broader options for approaching the EU ETS, like active price management

based on price floors or price corridors or a carbon market version of open mar-

ket policy (Grubb 2012, Perthuis/Trotignon 2012) are explicitly not subject to the

analysis presented in this study.

Within the framework of a more ambitious climate policy, broader approaches in

terms of appropriate targets as well as policies and measures will be necessary.

This is relevant for policies and measures beyond the EU ETS as well as for

policies and measures addressing sectors which are not regulated by the EU

ETS. These issues are not covered by the scope of the analysis presented in

this paper.

Last but not least, the issues handled in this paper are highly political and at the same

time highly technical ones. This tension creates a strong need for transparency. There-

fore the analysis and documentation presented in this paper has a two-fold purpose.

Firstly, the information should be usable as a compendium for key data and data links

which are important to navigate across the debates. Secondly, the findings should sup-

port specific action and thus be as explicit as possible.

The authors benefitted enormously from a broad range of discussions with many col-

leagues and partners and wish to thank them for this. This paper has been edited by

Vanessa Cook (Öko-Institut). However, any errors or inaccuracies remain the sole re-

sponsibility of the authors.

Strengthening the EU ETS Öko-Institut (Institute for Applied Ecology)

- 16 -

2 Trends and targets for the greenhouse gas emissions of

the EU

2.1 Trends and targets for total greenhouse gas emissions of the EU

The historical trends for greenhouse gas emissions of the European Union (27 Member

States) are characterized by three phases (Figure 1)1:

In the early 1990s the greenhouse gas emissions decreased significantly, main-

ly due to the transformation process in Eastern Germany and the Member

States who entered the EU in 2005 and 2007 (new Member States) and mainly

in sectors which have been regulated by the EU ETS since 2005. From 1990 to

1995 the emissions decreased by approx. 6 %.

During the period from 1995 to 2005 the emissions at the aggregate level tend

to stagnation or a slight decrease but indicate different sectoral patterns. For

the sectors regulated later under the EU ETS (power sector, energy intensive

industries) a slight increase occurred, the emissions from aviation increased

significantly and the emissions from the non-ETS sectors decreased. For the

whole period from 1990 to 2005 the total greenhouse gas emissions reduction

amounted to 7 %.

From 2005 the emissions drop significantly, in the first years exclusively from

non-ETS sectors and from 2008 dominantly in the ETS-regulated sectors

whereas the latter trend was obviously but not exclusively triggered by the fi-

nancial and economic crisis from 2008 onwards. In 2009 the total emissions re-

duction compared to 1990 reached 16 %, in 2010 the respective level was 14 %

below 1990 levels.

The EU ETS for stationary installations represents (at the scope of the scheme from

2013 onwards) a share of 42 - 45 % in the total greenhouse gas emissions, the inclu-

sion of the aviation sector (from 2012 onwards) increases this share to 45 - 48 %. The

European Union has defined a set of greenhouse gas reduction targets for different

time horizons:

1 For the purpose of consistency with the ETS-related analysis the quantitative analysis of

greenhouse gas emission trends includes the emissions from international aviation (which is not accounted for under the provisions of the Kyoto Protocol to the United Nations Frame-work Convention on Climate Change (UNFCCC) but excludes the emissions from land use, land use change and forestry (LULUCF)). However, it should be pointed out that the scope of the greenhouse gas inventories under the UNFCCC covers the fuel deliveries to aircrafts and differs from the emission accounting for aviation under the EU ETS. In order to make these two data sets compatible, relative change rates were applied when certain trends or patterns from the one database had to be transferred to the other one.

Öko-Institut (Institute for Applied Ecology) Strengthening the EU ETS

- 17 -

For 2020 the EU has committed itself to an emission reduction of 20 % below

1990 levels on a unilateral basis (CEU 2007, EU 2009a, EU 2009b). An in-

crease of the ambition level to 30 % is a subject of recent debate.

No formal commitment of the EU exists yet for 2030. However, the range from

40 to 55 % is discussed within the scope of debates surrounding the Low-

Carbon Economy Roadmap and the Energy Roadmap 2050 (CEC 2011d, CEC

2011e, Öko-Institut 2011).

The EU declared and re-affirmed on several occasions a long-term emission

reduction target of 80 to 95 % below 1990 levels by 2050 (CEU 2010, CEU

2011, EP 2010).

Figure 1 Total greenhouse gas emission trends and goals for the European Union

(excluding LULUCF and including international aviation), 1990-2050

0

1,000

2,000

3,000

4,000

5,000

6,000

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

mln

t C

O2

e

Aviation (national &international)

Non-ETS sectors

EU ETS (proxy datafrom 1990 to 2004)

2020 Goal-20...-30%compared to 1990

2030 Goal-40...-55%compared to 1990

2050 Goal-80...-95%

compared to 1990

Source: UNFCCC, European Commission, calculations by Öko-Institut

The comparison of the historical emission patterns (Figure 1) and the medium- and

long-term emission reduction targets highlights on the one hand that the sectors regu-

lated by the EU ETS must deliver a significant share of the required reduction efforts.

On the other hand the general trajectory towards the long-term targets is not fully con-

sistent with the 2020 targets as defined and addressed in recent debates. Given the

fact that the EU ETS is essentially parameterized in the framework of the 20 % emis-

sions reduction target for 2020 (as laid down in the energy and climate package of

2008) it will potentially require adjustments to maintain the appropriate investments,

which fit into the long-term trajectory towards an 80 to 95 % emission reduction by

2050.

Strengthening the EU ETS Öko-Institut (Institute for Applied Ecology)

- 18 -

2.2 Cap under the EU ETS from 2005 to 2020 and beyond

The emissions target of the EU ETS – the cap – is determined by the total amount of

allowances (European Union allowances – EUA) which are available to the regulated

entities either from free allocation or purchases or auctions. However, for the second

period of the EU ETS the exact number of these allowances is subject to changes, de-

pending on the decisions on the National Allocation Plans (NAP) of the Member States

which form as a total the EU-wide cap for the second period from 2008 to 2012.

Table 1 Cap references for the second trading period of the EU ETS

NAP decisions

(2006/2007)

NAP table decisions

(2008, 2009, 2010)

CITL "NAP Info"

(2012)

Austria 30.70 30.73 30.96

Belgium 58.50 58.49 58.49

Bulgaria 42.30 38.09 39.29

Cyprus 5.48 5.25 5.35

Czech Republic 86.80 86.74 86.74

Denmark 24.50 24.50 24.50

Estonia 12.72 13.10 13.10

Finland 37.60 37.56 37.56

France 132.80 131.99 134.37

Germany 453.10 451.47 452.34

Greece 69.10 68.31 68.31

Hungary 26.90 26.65 26.65

Ireland 22.30 22.28 22.29

Italy 195.80 201.59 201.59

Latvia 3.43 3.41 6.25

Liechtenstein 0.00 0.02 0.02

Lithuania 8.80 8.58 8.58

Luxembourg 2.50 2.49 2.49

Malta 2.10 2.14 2.14

Netherlands 85.80 87.47 87.47

Norway 15.05 15.05 15.05

Poland 208.50 205.70 205.70

Portugal 34.80 34.81 34.81

Romania 75.90 74.06 74.05

Slovakia 30.90 32.54 32.54

Slovenia 8.30 8.30 8.29

Spain 152.30 152.25 152.25

Sweden 22.80 22.47 22.47

United Kingdom 246.20 245.62 245.62

EU-27 2080.93 2076.60 2084.21

All EU ETS countries 2095.98 2091.66 2099.28

mln EUA

Note: The cap for Austria was corrected downwards for the allowances purchased by the Austrian government to

replenish the new entrant reserve and that are included in the NAP table decision and the CITL “NAP Info” for

Austria. Reserves for the use of emissions reduction credits from Joint Implementation are not taken into account

when calculating the caps. The total for all EU ETS countries includes Norway and Liechtenstein.

Source: NAP decisions2, NAP table decisions

3, CITL “NAP Info”

4, calculations by Öko-Institut

2 http://ec.europa.eu/clima/policies/ets/allocation/2008/documentation_en.htm.

3 http://ec.europa.eu/clima/policies/ets/registries/documentation_en.htm.

Öko-Institut (Institute for Applied Ecology) Strengthening the EU ETS

- 19 -

Table 1 summarizes the evolution of the cap in the EU ETS over time, which is charac-

terized by a slightly increasing trend. Based on the NAP decisions by the European

Commission in 2006/2007, the total of the national caps for the participating states

amounted to 2,096 million EUA. Based on the respective decisions on the so-called

NAP tables submitted by Member States in the years 2008 to 2010 (containing individ-

ual allocations for each installation) the total quantity slightly decreased to 2,092 million

EUA. However, over time the cap for the EU ETS undergoes further changes which are

documented in the Community Independent Transaction Log (CITL). As of May 2012

the exact cap amounted to 2,099 million EUA. The main reason for this increase is that

the cap of Latvia has doubled to 6 million EUA annually, according to the most recent

changes in the CITL (Table 1).5 The methodology and the transparency on the cap of

the EU ETS will increase significantly from 2013 onwards because the total cap will no

longer result from decentralized cap-setting in National Allocation Plans by the partici-

pating countries. From the start of the second trading period (2008-2012) the EU-wide

cap is centrally set by European legislation. This new cap-setting approach is based on

the EU-wide cap for the second period (expressed as the annual average of the re-

spective number of allowances) and a linear reduction factor (LRF). The linear reduc-

tion factor is applied to the cap level at the midpoint of the second trading period to

calculate a fixed number of allowances which is annually deducted from the cap for the

previous year. This annual deduction is also applied mathematically for the second half

of the second trading period but first takes effect in 2013. It is worth mentioning that the

EU ETS Directive as the legislative basis for the EU ETS does not specify any endpoint

for the application of the linear reduction factor and the linear reduction factor provides

long-term visibility of the emission reduction targets to be implemented by the EU ETS.

Although this general approach is complemented by some special provisions, e.g. for

installations which fall under the scope of the EU ETS from the beginning of the third

trading period, the transparency of the cap should significantly increase from 2013 on-

wards because the European Commission has to explicitly publish the respective cap

amounts.

For the analysis presented in this paper, the following approach was taken to specify

the cap: In order to not overestimate the cap from 2013 onwards the quantity of EUAs

stated in the NAP table decisions are taken as the average cap in the second trading

period of the EU ETS. This cap is reduced annually by a fixed amount of allowances

consistent to the linear reduction factor of 1.74 % annually in accordance with recent

4 CITL; Nap Info; Search; Country; First Commitment Period; History of the NAP; Total in

NAP. http://ec.europa.eu/environment/ets/napMgt.do?languageCode=en. 5 However, the total cap derived from the CITL data is likely to overestimate the cap because

in some cases governments (e.g. in Austria) bought allowances from the market to replenish the reserve for the free allocation to new entrants (new entrant reserve). In this case the EUAs are recorded twice in the CITL. On the one hand allowances are accounted for when they are initially issued (or auctioned/sold); on the other hand the allowances are recorded in the CITL when they are bought by governments and are issued to new entrants.

Strengthening the EU ETS Öko-Institut (Institute for Applied Ecology)

- 20 -

legislation. The respective cap from 2013 onwards has been published by DG Clima

(CEC 2010c and CEC 2010d) but it is important to note that this cap-setting is not the

final one. The most recent calculation of the cap (CEC 2010d) does not include allow-

ances from new entrant reserves that have not yet been allocated. This means that the

cap level published up to now is a preliminary one and it is very likely that it will be in-

creased in order to take into account allocations or auctions and sales from new en-

trant reserves.

Table 2 Comparison of approaches to quantify the cap for the third trading period

of the EU ETS (scope of the second period), 2013-2020

Total

average 2013 2014 2015 2016 2017 2018 2019 2020 2013-2020

Cap decision 2,039 1,932 1,897 1,861 1,826 1,790 1,755 1,719 1,684 14,464

Own calculation 2,077 1,968 1,932 1,896 1,860 1,824 1,788 1,751 1,715 14,734

Difference 38 36 35 35 34 33 33 32 31 269

2nd period 3rd trading period

Note: Own caculation is based on CITL data.

mln EUA

Source: CEC (2010b+d), calculations by Öko-Institut

Table 2 compares the cap from 2013 onwards for installations that already participated

in the second trading period (EU ETS II scope), including installations that opted-in to

the EU ETS in the second period (not including EUAs attributed to the non-EU coun-

tries Norway and Liechtenstein). The data compilation illustrates that compared to the

most recent cap decision it is likely that the final cap for the second and third trading

periods will increase by up to 38 million EUA per year.

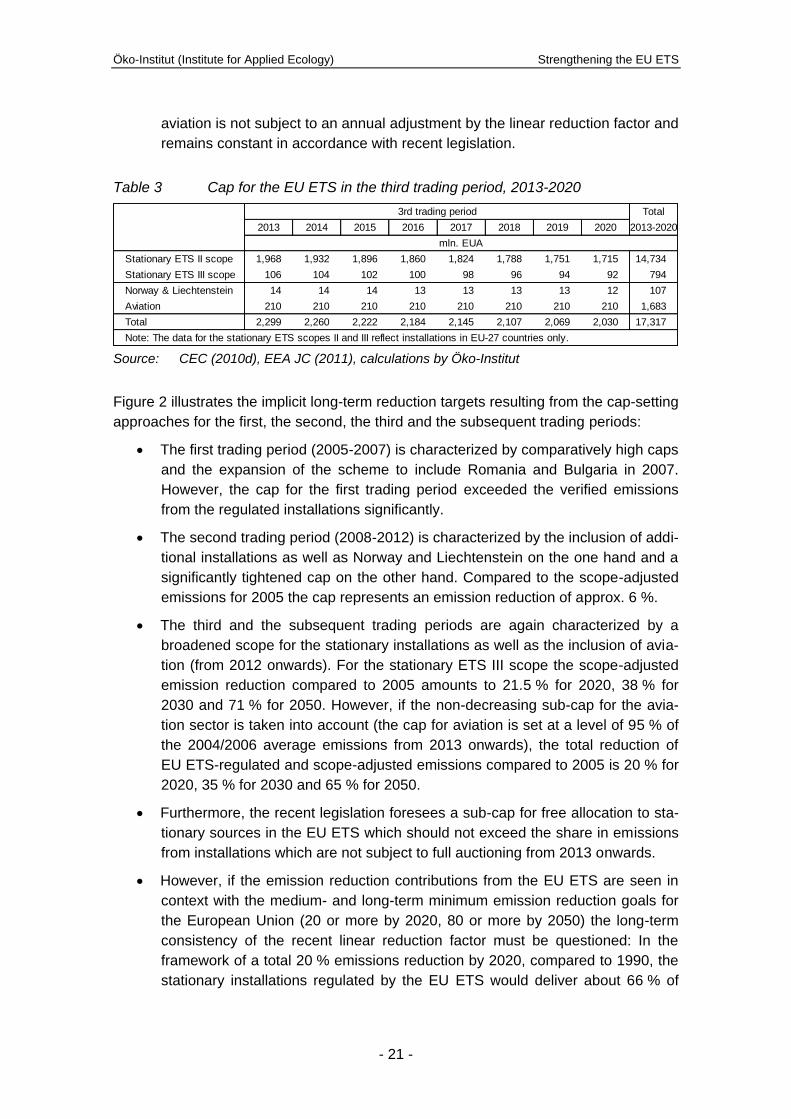

Table 3 indicates the cap data estimates for the EU ETS from 2013 onwards which

were used for the analysis. It should be highlighted that the analysis must reflect the

fact that the scope of the EU ETS changes over time (increasingly broadening the

scope of stationary sources as well as the inclusion of new sectors like aviation). In

detail the cap estimates are based on the following data and assumptions:

The cap data for stationary installations already participating in the second trad-

ing period from 2008 to 2012 (Stationary ETS II scope) are taken from Table 2

(the “own calculation” column).

The quantity of allowances available for stationary installations participating

from the third trading period onwards (Stationary ETS III scope) is based on

CEC (2010d).

The quantity of allowances available for Norway and Liechtenstein is based on

a multiplication of the linear factor and the cap for the second trading period as

documented in Table 1.

The cap for aviation (which is included in the EU ETS from 2012 onwards) is

based on EEA JC (2011) and includes flights starting from or landing in the EU-

27, Iceland, Norway and Liechtenstein. It should be noted that the sub-cap for

Öko-Institut (Institute for Applied Ecology) Strengthening the EU ETS

- 21 -

aviation is not subject to an annual adjustment by the linear reduction factor and

remains constant in accordance with recent legislation.

Table 3 Cap for the EU ETS in the third trading period, 2013-2020

Total

2013 2014 2015 2016 2017 2018 2019 2020 2013-2020

Stationary ETS II scope 1,968 1,932 1,896 1,860 1,824 1,788 1,751 1,715 14,734

Stationary ETS III scope 106 104 102 100 98 96 94 92 794

Norway & Liechtenstein 14 14 14 13 13 13 13 12 107

Aviation 210 210 210 210 210 210 210 210 1,683

Total 2,299 2,260 2,222 2,184 2,145 2,107 2,069 2,030 17,317

3rd trading period

Note: The data for the stationary ETS scopes II and III reflect installations in EU-27 countries only.

mln. EUA

Source: CEC (2010d), EEA JC (2011), calculations by Öko-Institut

Figure 2 illustrates the implicit long-term reduction targets resulting from the cap-setting

approaches for the first, the second, the third and the subsequent trading periods:

The first trading period (2005-2007) is characterized by comparatively high caps

and the expansion of the scheme to include Romania and Bulgaria in 2007.

However, the cap for the first trading period exceeded the verified emissions

from the regulated installations significantly.

The second trading period (2008-2012) is characterized by the inclusion of addi-

tional installations as well as Norway and Liechtenstein on the one hand and a

significantly tightened cap on the other hand. Compared to the scope-adjusted

emissions for 2005 the cap represents an emission reduction of approx. 6 %.

The third and the subsequent trading periods are again characterized by a

broadened scope for the stationary installations as well as the inclusion of avia-

tion (from 2012 onwards). For the stationary ETS III scope the scope-adjusted

emission reduction compared to 2005 amounts to 21.5 % for 2020, 38 % for

2030 and 71 % for 2050. However, if the non-decreasing sub-cap for the avia-

tion sector is taken into account (the cap for aviation is set at a level of 95 % of

the 2004/2006 average emissions from 2013 onwards), the total reduction of

EU ETS-regulated and scope-adjusted emissions compared to 2005 is 20 % for

2020, 35 % for 2030 and 65 % for 2050.

Furthermore, the recent legislation foresees a sub-cap for free allocation to sta-

tionary sources in the EU ETS which should not exceed the share in emissions

from installations which are not subject to full auctioning from 2013 onwards.

However, if the emission reduction contributions from the EU ETS are seen in

context with the medium- and long-term minimum emission reduction goals for

the European Union (20 or more by 2020, 80 or more by 2050) the long-term

consistency of the recent linear reduction factor must be questioned: In the

framework of a total 20 % emissions reduction by 2020, compared to 1990, the

stationary installations regulated by the EU ETS would deliver about 66 % of

Strengthening the EU ETS Öko-Institut (Institute for Applied Ecology)

- 22 -

the total required emissions reduction from 2005 to 2020. Aviation would deliver

about 1 % and the non-ETS sectors 33 %.

For an 80 % emission reduction by 2050 the EU ETS would deliver only 40 % of

the necessary emission reduction from 2005 to 2050. If the 2020 target would

be tightened to 30 % and the cap of the EU ETS, i.e. the linear reduction factor

would not be subject to change, the EU ETS would only deliver about 38 % of

the necessary emission reduction. Aviation would contribute less than 1 % and

the non-ETS sectors 60 % of the total emission reduction.

Figure 2 Evolution of the caps for the EU ETS, 2005-2050

0

500

1,000

1,500

2,000

2,500

3,000

2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

mln

EU

A

EU ETS cap 1st period

EU ETS cap 2nd period

EU ETS cap 3rd+ periods (LRF 1.74%)

Sub-cap for free allocation (LRF 1.74%)

Sub-cap aviation

1st 2nd Period 3rd Period 4th+ Periods

Source: CEC 2010b, EU 2009a, calculations by Öko-Institut

Consequently the debate on EU ETS caps must focus on the short- and medium-term

aspects (cf. chapter 3 to 6) as well as the longer-term consistency (cf. chapter 7).

Öko-Institut (Institute for Applied Ecology) Strengthening the EU ETS

- 23 -

3 The recent problem: Allowance surplus from 2008 to

2011

3.1 Introduction, scope and structure of the analysis

The analysis presented in the following chapters focuses on the surplus of allowances

which occurred from 2008 to 2011. For this period a consistent set of historical data is

available for the EU ETS. The analysis does not reflect the respective data from the

first trading period of the EU ETS because banking was not allowed from the pilot peri-

od (2005-2007) to the second trading period (2008-2012) and is consequently not rele-

vant for the surplus analysis.

The specification of the surplus for the period from 2008 to 2011 is based on the follow-

ing analysis:

1. The trends of verified emissions in the EU ETS specify the demand for emis-

sions allowances by the regulated entities (cf. chapter 3.2).

2. The supply of emissions allowances or substitutes arises from different sources

which are documented separately:

a. A major share of emissions allowances were made available by free al-

location to the operators of the respective installations (cf. chapter 3.3).

b. Some allowances were supplied by auctions or government sales at

market prices (cf. chapter 3.4);

c. The operators were entitled to use a certain amount of lower-priced

emissions reduction credits from the Clean Development Mechanism

(CDM) and Joint Implementation (JI) as a substitute for EU emission al-

lowances (cf. chapter 3.5).

The comparison of demand and supply (cf. chapter 3.6) allows the surplus accumulat-

ed by the end of 2011 and its pattern to be specified.

3.2 Trend of verified emissions in the EU ETS for 2008 to 2011

Data on verified emissions is available from the Community Independent Transaction

Log (CITL) on an installation level. Data on an aggregated level is published by the

European Environment Agency (EEA) in its EU ETS Dataviewer (EEA 2012).

In its current scope the EU ETS covers the 27 EU Member States, Norway and Liech-

tenstein. Verified emissions of all installations covered by the EU ETS were 2,123 mil-

lion tons of carbon dioxide (t CO2) in the year 2008. Due to the economic crisis emis-

sions dropped to 1,888 million t CO2 in the year 2009 and recovered to a level of 1,939

million t CO2 in the year 2010 (EEA 2012). In 2011 emissions decreased again to a

level of 1,903 million t CO2.

Strengthening the EU ETS Öko-Institut (Institute for Applied Ecology)

- 24 -

3.3 Free allocation for 2008 to 2011

Data on free allocation is also available from the Community Independent Transaction

Log (CITL) on an installation level. Data on an aggregated level is published by the

European Environmental Agency (EEA) in its EU ETS Dataviewer (EEA 2012).

Free allocation as recorded in the EU ETS Dataviewer was 1,961 million t CO2 in the

year 2008, increasing to 1,976 million t CO2 in the year 2009, 1,998 million t CO2 in the

year 2010 and 2,001 million t CO2 in the year 2011.

3.4 Auctions and sales for 2008 to 2011

Data on auctioned or sold volumes of EUAs are not provided by the CITL or by another

comprehensive data compilation. However, Member States generally publish the

amount of allowances which were brought to the market by auctions or sales. In addi-

tion, the website of DG Clima also keeps track of the amount of EUAs auctioned by

Member States.

Based on the data compiled by EEA (2012) the amount of EUAs auctioned or sold in

2008 was 45 million EUAs, exclusively from Germany and the UK. In 2009 this volume

increased to nearly 80 million EUAs in 2009, 92 million EUAs in 2010 and 83 million

EUAs in 2011. However, in some Member States auctions or sales were planned but

the set-up of auctions and sales was and is still delayed.

3.5 Use of CDM and JI credits from 2008 to 2011

Data on the amount of CDM and JI credits surrendered by operators is recorded and

published by the Community Independent Transaction Log (CITL) on an installation

level. Data on an aggregated level is published by the European Environmental Agency

(EEA) in its EU ETS Dataviewer (EEA 2012). In the years 2008 to 2011 operators cov-

ered by the EU ETS surrendered a total of 456 million offset credits from the CDM

(Certified Emissions Reduction Units – CER) and a total of 99 million emission reduc-

tion units from JI (Emission Reduction Units – ERU) to the competent authorities. Total

use of flexible mechanisms equals to 556 million CERs and ERUs in the four years

from 2008 to 2011.

3.6 Demand and supply balance for 2008 to 2011

Table 4 compares the amount of EUAs, CERs and ERUs available in the years 2008 to

2011 with the verified emission data for this period. In 2009, 2010 and 2011 the verified

emissions were lower than the free allocation to operators. As EUAs were auctioned on

top and operators used CERs and ERUs to cover their emissions a significant surplus

of EUAs has been accumulated.

Öko-Institut (Institute for Applied Ecology) Strengthening the EU ETS

- 25 -

Table 4 Surplus of allowances in the EU ETS, 2008-2011

Total

2008 2009 2010 2011 2008-2011

1,961 1,976 1,998 2,001 7,938

45 79 92 83 300

83 81 137 255 556

2,090 2,137 2,227 2,340 8,793

2,123 1,882 1,939 1,903 7,846

-33 255 289 436 947

-33 222 510 947Cumulated surplus

2nd trading period

Free allocation

Auctions and sales

CDM & JI

Total available units

Verified emissions

Surplus

mln EUA, CER, ERU or t CO2

Source: Calculations by Öko-Institut

The cumulated surplus of EUAs at the end of 2011 was nearly 1,000 million units. The

major share of this surplus (556 million EUAs) can be attributed to the fact that opera-

tors were allowed to surrender CERs and ERUs despite the fact that verified emissions

were below the available amount of EUAs.

The rest of the surplus (about 400 million EUAs) stems from the reduced emissions in

the years 2009 to 2011. This can mainly be attributed to the economic crisis during this

period.

Strengthening the EU ETS Öko-Institut (Institute for Applied Ecology)

- 26 -

4 The future challenge: Projection for the EU ETS surplus

until 2020

4.1 Introduction, scope and structure of the analysis

In contrast to the period from 2008 to 2011 no historical data can be used to specify the

potential surplus of allowances for the period from 2012 onwards and a projection for

the supply and demand must be developed.

1. The key determinant on the demand side is the baseline projection for emis-

sions regulated by the EU ETS. With respect to the baseline, three aspects are

of special importance: firstly the underlying assumptions on economic growth as

a key driver for greenhouse gas emissions, secondly the penetration of renew-

able energies as well as energy savings as a result of complementary policies

to the EU ETS and thirdly the effects of the extended scope of the EU ETS from

2013 onwards (cf. chapter 4.2).

2. The supply side for allowances and offset credits is analysed in respect of the

different sources of supply:

a. The decreasing share of free EUA allocation to the operators of the

regulated installations (cf. chapter 4.3);

b. The increasing share of allowances supplied at market prices via auc-

tions (cf. chapter 4.4);

c. The qualitatively and quantitatively restricted supply of offset credits

from the CDM or JI at prices lower than for EUAs (cf. chapter 4.5);

d. The free allocation to eligible new entrants from the new entrant re-

serve (cf. chapter 4.6).

The compilation of all sources for demand and supply enables an integrated projection

for the balance of demand and supply from 2012 to 2020 (chapter 4.7).

4.2 Baseline emission trends for the EU ETS from 2012 to 2030

The emission reduction effort within the EU ETS results from the difference of the

emission levels in a baseline trend and the cap. The baseline scenario is the counter-

factual scenario of what would occur in a regulatory environment without a price on

greenhouse gas emissions. Key determinants for the baseline emission trend in the

sectors regulated by the EU ETS are:

the demographic and economic trends as essential driving forces;

the energy and investment costs as significant factors influencing energy supply

and demand patterns; and

Öko-Institut (Institute for Applied Ecology) Strengthening the EU ETS

- 27 -

the general regulatory framework and complementary instruments to the EU

ETS, especially separate support schemes for renewable energies and energy

efficiency.

The cap definition for the EU ETS from 2013 onwards was based on an integrated

analysis for the 2008 climate and energy package of the European Union (Capros et al.

2008) which reflected both the overarching greenhouse gas emission reduction targets

for the EU as well as the plans to increase the share of renewable energy sources in

the energy mix and particularly in the power sector.

Figure 3 Comparison of GDP projections for ETS-relevant modelling exercises for

the European Union, 2005-2030

80%

90%

100%

110%

120%

130%

140%

150%

160%

170%

180%

2000 2005 2010 2015 2020 2025 2030 2035

20

05

= 1

00

%

EU Energy & Climate Package analysis (2008)

EU Energy Roadmap 2050 analysis (2011)

1.8...2% GDP growth from 2014

1.5% GDP growth from 2014

Historical data

-14%

-13%

-19%

-17%

Source: Eurostat, European Commission, calculations by Öko-Institut

However, some of the assumptions for the integrated modelling exercise carried out in

2008 no longer reflect the real trends for some key determinants of the baseline sce-

nario.

First of all, the short-, medium- and long-term economic outlook for the EU-27 has

changed significantly since 2008. Figure 3 indicates a range of projections for the de-

velopment of the gross domestic product (GDP), the key indicator for economic activi-

ties in a country or region.

For the modelling exercises on the EU energy and climate package in 2008 the

assumption for GDP growth from 2005 to 2030 amounted to an increase of ap-

prox. 43 % by 2020 and 71 % by 2030;

Strengthening the EU ETS Öko-Institut (Institute for Applied Ecology)

- 28 -

For the numerical analysis on the EU Energy Roadmap 2050 in 2011 (CEC

2011d) the modelling assumption was a total GDP growth from 2005 to 2020 of

approx. 28 % by 2020 and 52 % by 2030;

With respect to the most recent developments and trends two additional vari-

ants were analysed, the return to an annual of growth of 1.8 to 2.0 % during the

next two decades and a rather slow economic growth of about 1.5 % annually,

which results in a total GDP growth of approx. 17 to 21 % by 2020 and 38 to

48 % by 2030.

As a result, the total economic activity represented by GDP will be 14 to 17 % lower by

2020 and 13 to 19 % lower by 2030 than assumed in the analysis for the 2008 EU en-

ergy and climate package and thus for the cap of the EU ETS. Such changes for one of

the major driving forces for the baseline emission trend must result in a major change

of the emission reduction effort built into the cap of the EU ETS.

Furthermore, the massive support of renewable energy sources (RES) in the frame-

work of the 2008 EU energy and climate package could have a major impact on the

respective emission reduction efforts to be delivered by the EU ETS. For renewable

energy the following dimensions must be considered:

In terms of the EU ETS the EU-wide target for the expansion of renewable en-

ergies will mainly have an effect on the power generation from renewable ener-

gy sources; the share of renewables in the heat and transport market is of much

less or of no significance for the installations regulated by the EU ETS.

When the modelling for the 2008 EU energy and climate package was conduct-

ed, the analysis was based on certain assumptions for the power generation

from renewable energy sources. Subsequently and within the framework of the

EU Directive on Renewable Energies (EU 2009c) the Member States developed

National Renewable Energy Action Plans (NREAP) which include sectoral tar-

gets and projections for the different sectors. The deployment trends and tar-

gets for the renewable energies are not necessarily consistent with the underly-

ing assumptions of the 2008 modelling exercises.

Last but not least, the historical data for the development of renewable energies

in the power sector must not necessarily fit into the projections in terms of levels

and structures of RES deployment.

In order to make the data comparable for the purpose of the analysis presented in this

paper, the power generation from different renewable energy sources was transformed

into avoided CO2 emissions based on the following assumptions6:

Power generation from solar energy was assumed to substitute natural gas-

fired power plants;

6 These assumptions are in line with our own modelling exercises as well as the respective

literature (ISI 2005+2009).

Öko-Institut (Institute for Applied Ecology) Strengthening the EU ETS

- 29 -

Power generation from hydro, biomass, geothermal heat and ocean energy was

assumed to substitute hard coal-fired power plants; and

Power generation from wind energy was assumed to substitute a mix of hard

coal-fired plants (75 %) and natural gas-fired power plants (25 %).

Figure 4 Comparison of CO2 emission abatement contributions from renewable

energy sources in the power sector for the EU, 2005-2020

0

200

400

600

800

1,000

1,200

1,400

2005 2010 2015 2020 Integratedpackage

Baseline Integratedpackage

Baseline

Historical data NREAP (2011) 2020 projection (2008) 2030 projection (2008)

mln

t C

O2

Geothermal

Solar & ocean

Wind

Biomass

Hydro

Source: Eurostat, European Commission, calculations by Öko-Institut

Figure 4 provides an overview of the RES deployment trends in the EU power sector

from the three data sources mentioned above:

The data indicate that the trend of historical data is all in all consistent with the

projections submitted by the Member States in the National Renewable Energy

Action Plans (NREAP) in 2011 (EEA 2011).

The 2008 modelling for the EU energy and climate package and its integrated

targets for greenhouse gas emission reduction, the revision of the EU ETS and

the deployment of renewable energy sources for 2020 indicate that the effects

of an increased support for renewable energy sources are significant in terms of

CO2 emission abatement.7

7 For the modelling of the “Integrated package” projection a broad range of policies and

measures was considered while the “Baseline” modelling describes a projection in absence of these new policies and measures at EU level. The “Integrated package” projection refers to the CSE scenario in the documentation of the modelling exercise (Capros et al. 2008) and the “Baseline” projection refers to the respective baseline case.

Strengthening the EU ETS Öko-Institut (Institute for Applied Ecology)

- 30 -

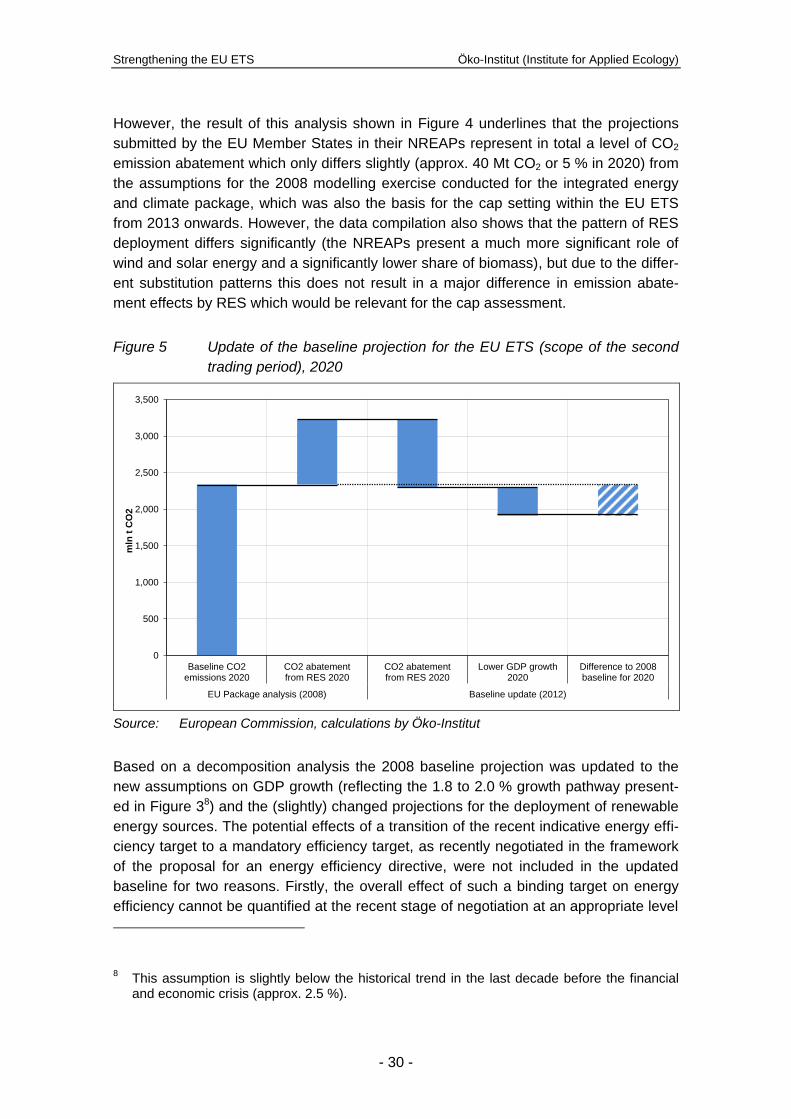

However, the result of this analysis shown in Figure 4 underlines that the projections

submitted by the EU Member States in their NREAPs represent in total a level of CO2

emission abatement which only differs slightly (approx. 40 Mt CO2 or 5 % in 2020) from

the assumptions for the 2008 modelling exercise conducted for the integrated energy

and climate package, which was also the basis for the cap setting within the EU ETS

from 2013 onwards. However, the data compilation also shows that the pattern of RES

deployment differs significantly (the NREAPs present a much more significant role of

wind and solar energy and a significantly lower share of biomass), but due to the differ-

ent substitution patterns this does not result in a major difference in emission abate-

ment effects by RES which would be relevant for the cap assessment.

Figure 5 Update of the baseline projection for the EU ETS (scope of the second

trading period), 2020

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Baseline CO2emissions 2020

CO2 abatementfrom RES 2020

CO2 abatementfrom RES 2020

Lower GDP growth2020

Difference to 2008baseline for 2020

EU Package analysis (2008) Baseline update (2012)

mln

t C

O2

Source: European Commission, calculations by Öko-Institut

Based on a decomposition analysis the 2008 baseline projection was updated to the

new assumptions on GDP growth (reflecting the 1.8 to 2.0 % growth pathway present-

ed in Figure 38) and the (slightly) changed projections for the deployment of renewable

energy sources. The potential effects of a transition of the recent indicative energy effi-

ciency target to a mandatory efficiency target, as recently negotiated in the framework

of the proposal for an energy efficiency directive, were not included in the updated

baseline for two reasons. Firstly, the overall effect of such a binding target on energy

efficiency cannot be quantified at the recent stage of negotiation at an appropriate level

8 This assumption is slightly below the historical trend in the last decade before the financial

and economic crisis (approx. 2.5 %).

Öko-Institut (Institute for Applied Ecology) Strengthening the EU ETS

- 31 -

of uncertainty. Secondly, and more importantly, it is rather impossible at the current

stage to translate the emerging additional energy efficiency efforts in additional green-

house gas emission abatement for the sources regulated by the EU ETS, especially

the electricity generation sector.

Therefore, the updated baseline assumes no further changes in energy and carbon

intensity (with the exception of the respective effects of renewable energies) and repre-

sents a difference to the originally used baseline of about 425 Mt CO2 for 2020 which

results essentially from the lower GDP growth assumptions and is significant with re-

spect to an assessment of the EU ETS cap.

Furthermore, the projection for the emissions from aviation was updated, considering

the different system boundaries of the aviation sector in energy balances and emission

inventories on the one hand and the scope of the EU ETS with respect to aviation. The

updated projection is based on the average emissions from 2004 to 2006 (220 Mt

CO2), which form the basis for the aviation-specific part of the cap in the EU ETS. The

projection for the emissions from aviation is based on this 2005 emission level and the

growth rates for the final energy use by aviation from the modelling exercise for the EU

Energy Roadmap 2050, which represents the most recent EU-wide trends for aviation

(CEC 2011d).

Figure 6 Comparison of historical CO2 emissions data and baseline projections

for the EU ETS (scope of the second period and aviation), 2005-2030

0

500

1,000

1,500

2,000

2,500

3,000

Baseline2008

Historicaldata

Historicaldata

Historicaldata

Baseline2008

Update2012

Baseline2008

Update2012

2005 2010 2011 2020 2030

mln

t C

O2

Aviation

Stationary ETS sectors (3rd period scope)

Source: European Commission, calculations by Öko-Institut

Figure 6 summarizes the historical data and the updated baseline projections for the

sectors regulated by the EU ETS for the scope of the second trading period as well as

the aviation sector which falls in the scope of the EU ETS since 2012. For the station-

Strengthening the EU ETS Öko-Institut (Institute for Applied Ecology)

- 32 -

ary part of the EU ETS the counterfactual (reflecting the updated GDP growth assump-

tions as well as the updated emission abatement from RES) is an emissions trend

which increases slightly over time but remains more or less at emission levels which

were observed during the last few years. The difference to the baseline trends used for

the definition of the cap from 2013 onwards amounts to 385 Mt CO2 in 2020 and 365

Mt CO2 in 2030 which equals a 16 % reduction. This significant reduction of the base-

line levels is partly compensated by an increased baseline assumption for the aviation

sector (+67 Mt CO2 in 2020 and +38 Mt CO2 in 2030). However, with respect to the fact

that the cap for aviation was derived separately and is based on data which have no

direct link to the 2008 modelling of the baseline, the offsetting effects of the increased

aviation baseline are not relevant for the assessment of the 2008 baseline assump-

tions.

Last but not least, emissions from new sectors will fall under the scope of the EU ETS

in 2013 (e.g. N2O from industrial gases, PFC from Aluminium and others). The starting

point for specifying the respective increase of the cap is 107 million EUA in 2013, which

reflects the fact that the UK, the Netherlands, Austria, Italy and Norway already opted

in their nitric acid and adipic acid production during the second trading period of the EU

ETS.

According to Article 9a (2) of the revised EU ETS Directive Member States had to notify

verified emissions of new installations entering the EU ETS from 2013 to determine the

increase of the cap. For non-CO2 gases Member States were allowed to “notify a lower

amount of emissions according to the reduction potential of those installations” (Article

9a (2)). Unfortunately there is no information available on the extent to which Member

States took the reduction potential into account when the cap increase for nitric acid

and adipic acid production was determined.

Recently implemented or announced JI projects for the abatement of N2O within the EU

have resulted in impressive emission reductions which are part of the baseline because

they were mainly triggered by non-ETS policies. Therefore, it can be expected that

emissions from nitric acid and adipic acid production will be drastically reduced in the

third trading period of the EU ETS. In 2008 N2O emissions from nitric acid and adipic

acid production was 33 million tons of carbon dioxide equivalent (t CO2e) in the EU-27

without installations opted in by the Netherlands and Austria (ETC/ACC 2010). Based

on data from ETC/ACC (2010) the emission reduction could be as high as 30 million t

CO2e in the years from 2013 onwards compared to emissions in the year 2008. If

Member States have taken this reduction potential into account, there will be no sur-

plus from installations entering the EU ETS from 2013 onwards. If Member States have

not taken this reduction potential into account, the annual surplus could be 30 million

EUA. It is assumed that half of the reduction potential was taken into account. Thus

emissions are estimated at a level of 91 million EUA for the years 2013 to 2020 (de-

ducting 15 million EUA from the level of 107 million EUA mentioned above).

Öko-Institut (Institute for Applied Ecology) Strengthening the EU ETS

- 33 -

Table 5 Updated baseline emission trends for the EU ETS sectors, 2005-2030

2005 2010 2011 2012 2013 2014 2015 2020 2025 2030

Stationary ETS II scope 2,230 1,939 1,903 1,892 1,886 1,898 1,912 1,954 1,954 1,954

Stationary ETS III scope - - - - 91 91 91 91 91 91

Aviation 221 - - 239 245 251 257 285 295 293

Total - - - - 2,222 2,240 2,260 2,330 2,340 2,338

mln t CO2e

Note: Due to the different scope of the EU ETS (stationary sources, aviation) no totals are given for the years before 2013. Source: Calculations by Öko-Institut

Table 5 summarizes the updated baseline emission trends for the different scopes of

the EU ETS. The total emissions in the baseline increase by 50 million t CO2 for sta-

tionary installations and by 54 million in the aviation sector by 2020 compared to the

current emission level (2011/2012). For 2030 the baseline emissions are almost con-

stant compared to the 2020 levels.

4.3 Free allocation from 2012 to 2020

As a starting point it is assumed that the free allocation for the year 2012 will be equal

to the free allocation in the year 2011. Thus free allocation would be 2,001 million t CO2

in the year 2012.

Table 6 Amount of free allocation, 2008-2020

Total

2008 2009 2010 2011 2012 2013 2014 2015 2020 2008-2020

Stationary ETS II scope 1,961 1,976 1,998 2,001 2,001 820 799 778 639 15,839

Stationary ETS III scope 77 77 77 72 607