CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission of McKinsey & Company is strictly prohibited Structural shifts shaping the future of Asset Management April 26 th , 2010 Discussion document

Transcript

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

Structural shifts shaping the future of Asset Management

April 26th, 2010

Discussion document

|McKinsey & Company 1

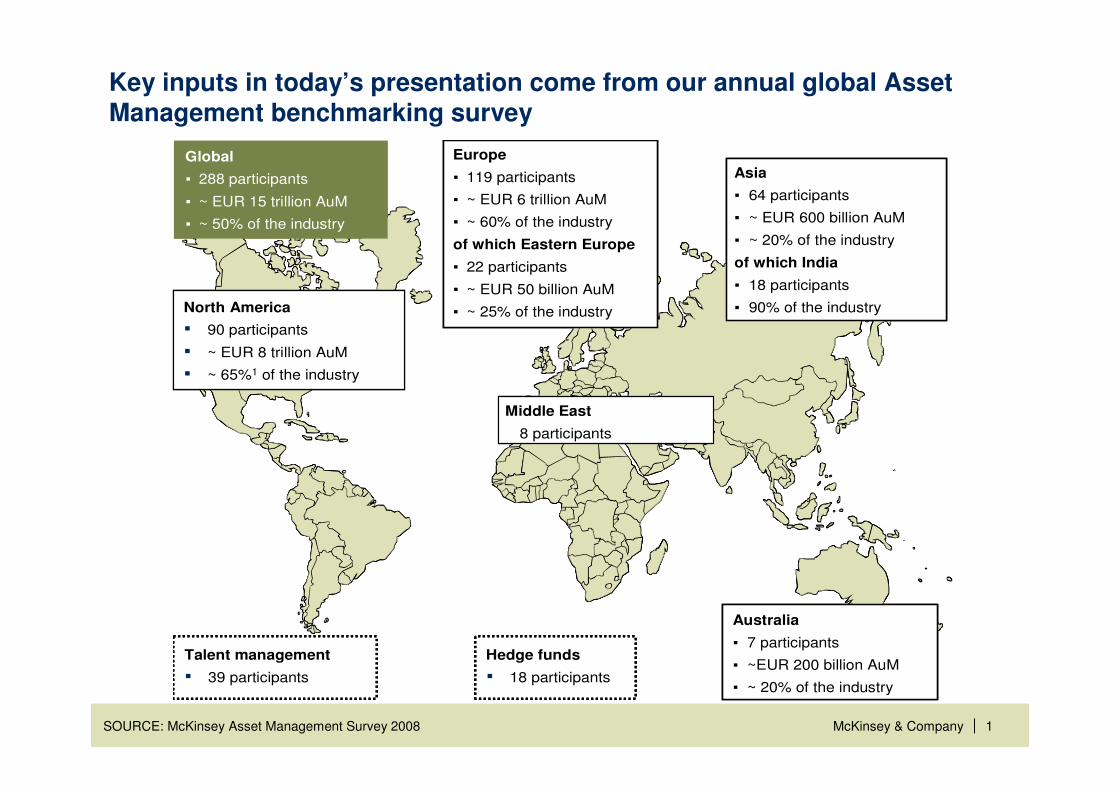

Key inputs in today’s presentation come from our annual global Asset Management benchmarking survey

SOURCE: McKinsey Asset Management Survey 2008

Australia

▪ 7 participants

▪ ~EUR 200 billion AuM

▪ ~ 20% of the industry

Middle East

▪ 8 participants

Europe

▪ 119 participants

▪ ~ EUR 6 trillion AuM

▪ ~ 60% of the industry

of which Eastern Europe

▪ 22 participants

▪ ~ EUR 50 billion AuM

▪ ~ 25% of the industry

Asia

▪ 64 participants

▪ ~ EUR 600 billion AuM

▪ ~ 20% of the industry

of which India

▪ 18 participants

▪ 90% of the industry

Global

▪ 288 participants

▪ ~ EUR 15 trillion AuM

▪ ~ 50% of the industry

North America

▪ 90 participants

▪ ~ EUR 8 trillion AuM

▪ ~ 65%1 of the industry

Talent management

▪ 39 participants

Hedge funds

▪ 18 participants

Australia

▪ 7 participants

▪ ~EUR 200 billion AuM

▪ ~ 20% of the industry

Middle East

▪ 8 participants

Europe

▪ 119 participants

▪ ~ EUR 6 trillion AuM

▪ ~ 60% of the industry

of which Eastern Europe

▪ 22 participants

▪ ~ EUR 50 billion AuM

▪ ~ 25% of the industry

Asia

▪ 64 participants

▪ ~ EUR 600 billion AuM

▪ ~ 20% of the industry

of which India

▪ 18 participants

▪ 90% of the industry

Global

▪ 288 participants

▪ ~ EUR 15 trillion AuM

▪ ~ 50% of the industry

North America

▪ 90 participants

▪ ~ EUR 8 trillion AuM

▪ ~ 65%1 of the industry

North America

▪ 90 participants

▪ ~ EUR 8 trillion AuM

▪ ~ 65%1 of the industry

Talent management

▪ 39 participants

Hedge funds

▪ 18 participants

Talent management

▪ 39 participants

Talent management

▪ 39 participants

Hedge funds

▪ 18 participants

Hedge funds

▪ 18 participants

|McKinsey & Company 2

Key messages

2009 marked a decade low in AM margins

Excellence in business management, not just investment management, is now required for firms to build a robust operating model

Looking ahead, despite a lot of uncertainty, the asset management market can be an opportunity-rich environment for firms that can capitalize on 5 structural shifts

1

2

3

|McKinsey & Company 3

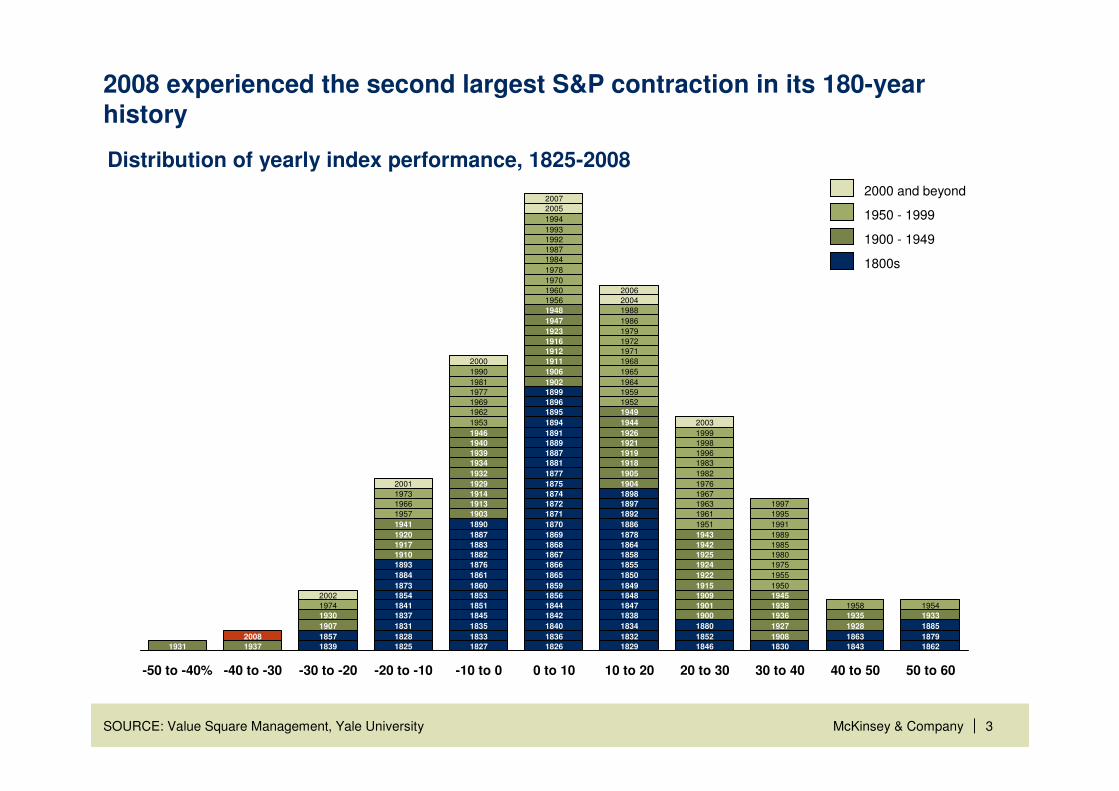

2008 experienced the second largest S&P contraction in its 180-year history

-50 to -40%

2008

1937

-40 to -30

2002

1974

1930

1907

1857

1839

-30 to -20

2001

1973

1966

1957

1941

1920

1917

1910

1893

1884

1873

1854

1841

1837

1831

1828

1825

-20 to -10

2000

1990

1981

1977

1969

1962

1953

1946

1940

1939

1934

1932

1929

1914

1913

1903

1890

1887

1883

1882

1876

1861

1860

1853

1851

1845

1835

1833

1827

-10 to 0

2007

2005

1994

1993

1992

1987

1984

1978

1970

1960

1956

1948

1947

1923

1916

1912

1911

1906

1902

1899

1896

1895

1894

1891

1889

1887

1881

1877

1875

1874

1872

1871

1870

1869

1868

1867

1866

1865

1859

1856

1844

1842

1840

1836

1826

0 to 10

2006

2004

1988

1986

1979

1972

1971

1968

1965

1964

1959

1952

1949

1944

1926

1921

1919

1918

1905

1904

1898

1897

1892

1886

1878

1864

1858

1855

1850

1849

1848

1847

1838

1834

1832

1829

10 to 20

2003

1999

1998

1996

1983

1982

1976

1967

1963

1961

1951

1943

1942

1925

1924

1922

1915

1909

1901

1900

1880

1852

1846

20 to 30

1997

1995

1991

1989

1985

1980

1975

1955

1950

1945

1931

1938

1936

1927

1908

1830

30 to 40

1958

1935

1928

1863

1843

40 to 50

1954

1933

1885

1879

1862

50 to 60

2000 and beyond

1950 - 1999

1900 - 1949

1800s

Distribution of yearly index performance, 1825-2008

SOURCE: Value Square Management, Yale University

|McKinsey & Company 4

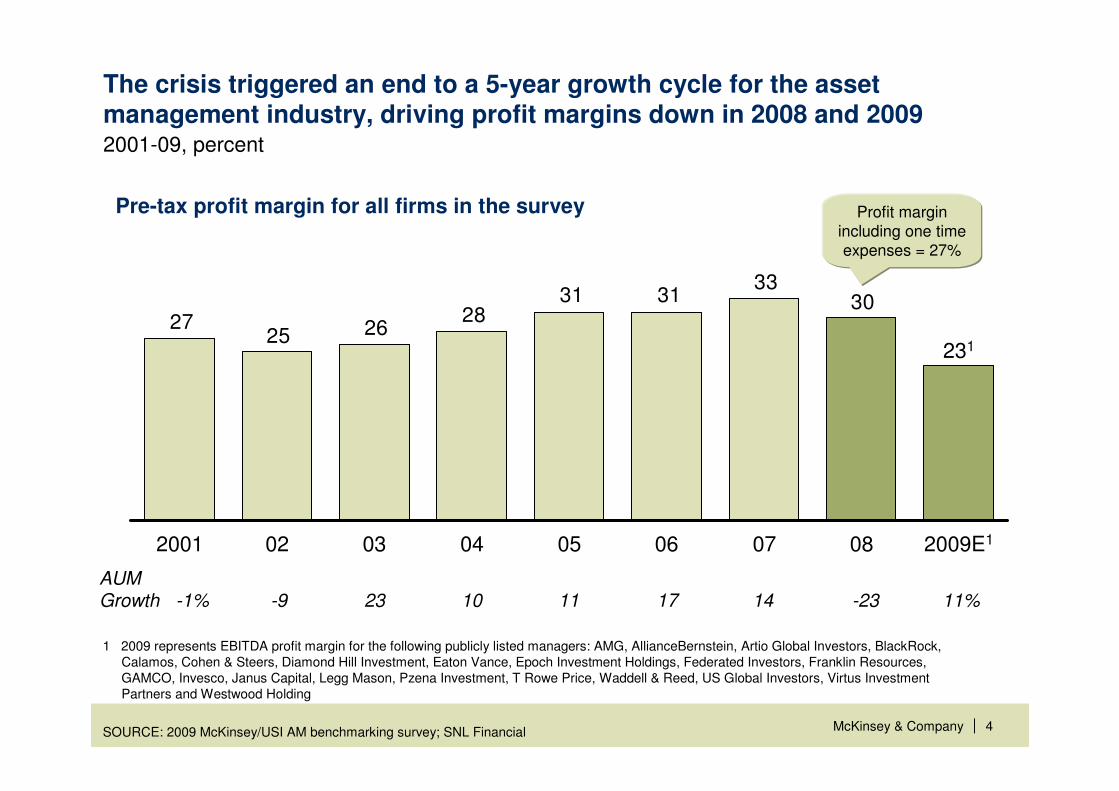

The crisis triggered an end to a 5-year growth cycle for the asset management industry, driving profit margins down in 2008 and 2009

Pre-tax profit margin for all firms in the survey

2001-09, percent

3033

313128

262527

2009E1

231

080706050403022001

1 2009 represents EBITDA profit margin for the following publicly listed managers: AMG, AllianceBernstein, Artio Global Investors, BlackRock, Calamos, Cohen & Steers, Diamond Hill Investment, Eaton Vance, Epoch Investment Holdings, Federated Investors, Franklin Resources, GAMCO, Invesco, Janus Capital, Legg Mason, Pzena Investment, T Rowe Price, Waddell & Reed, US Global Investors, Virtus Investment Partners and Westwood Holding

SOURCE: 2009 McKinsey/USI AM benchmarking survey; SNL Financial

Profit margin including one time expenses = 27%

11%AUM Growth -1% -9 23 10 11 17 14 -23

|McKinsey & Company 5

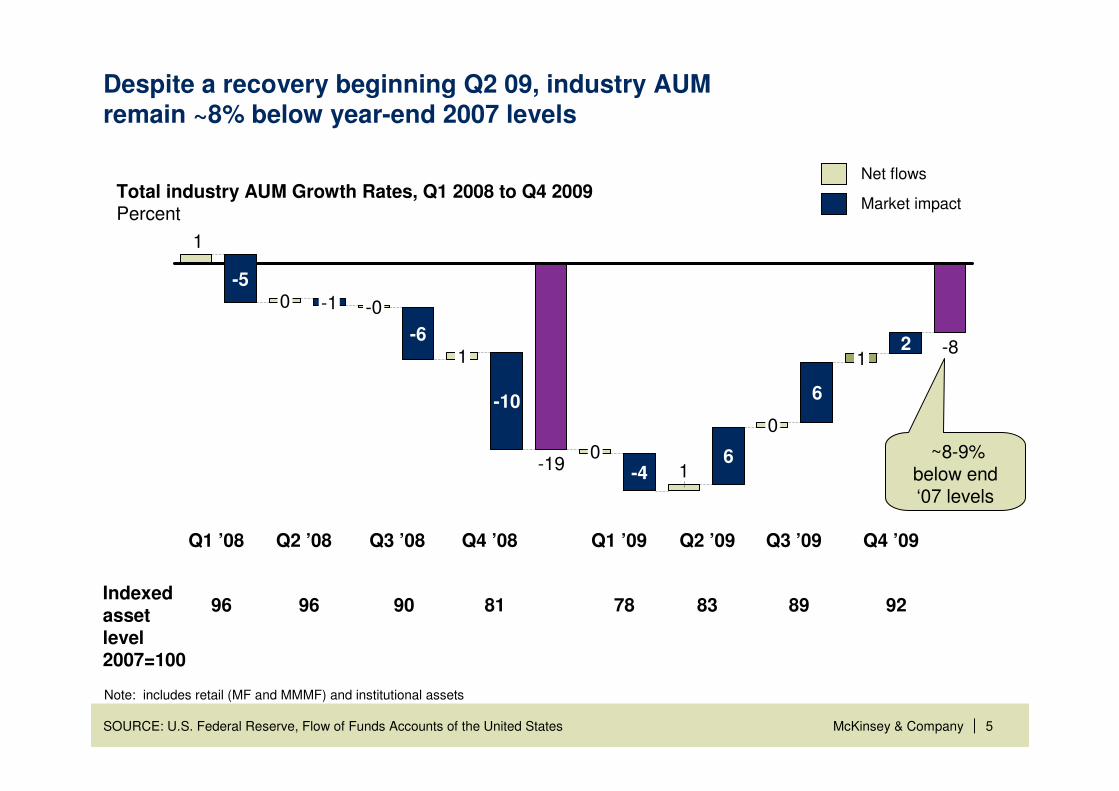

Despite a recovery beginning Q2 09, industry AUM remain ~8% below year-end 2007 levels

SOURCE: U.S. Federal Reserve, Flow of Funds Accounts of the United States

1

2

6

0

61-4

0-19

-0-10-5

1-8

1

-6

-10

Total industry AUM Growth Rates, Q1 2008 to Q4 2009Percent

Net flows

Market impact

Indexed asset level 2007=100

Q1 ’08

96

Q2 ’08

96

Q3 ’08

90

Q4 ’08

81

Q1 ’09

78

Q2 ’09

83

Q3 ’09

89

~8-9% below end ‘07 levels

Q4 ’09

92

Note: includes retail (MF and MMMF) and institutional assets

|McKinsey & Company 6

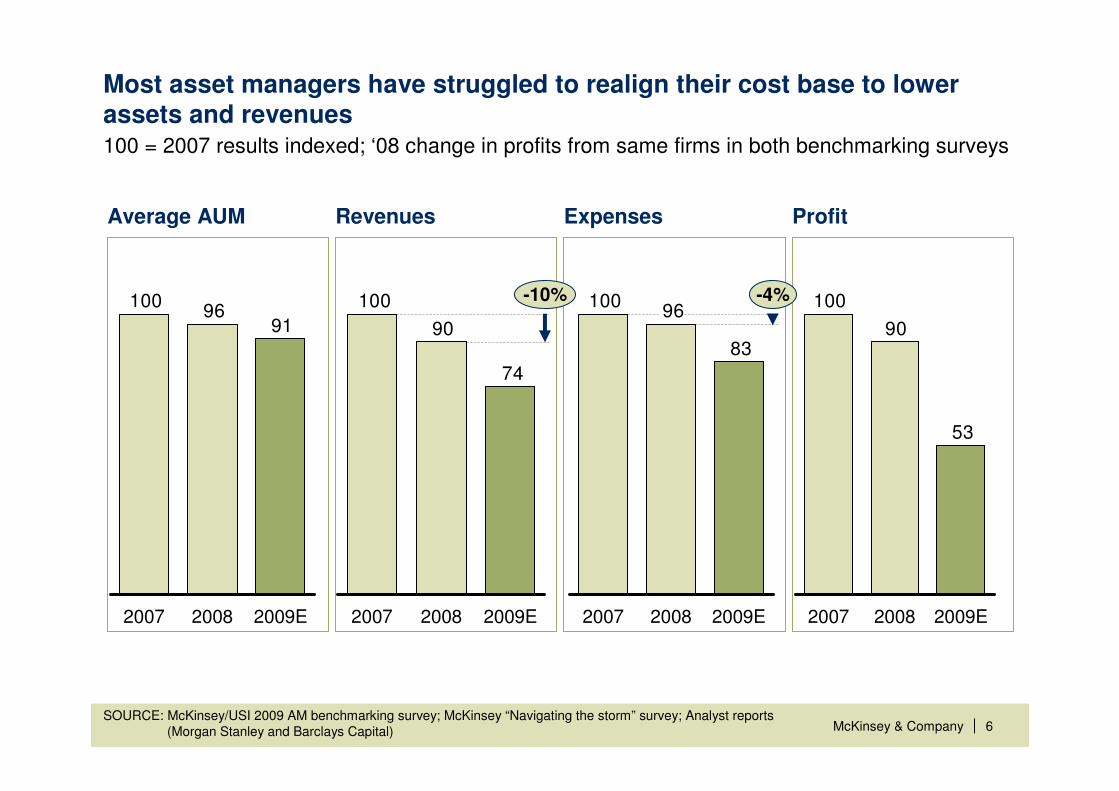

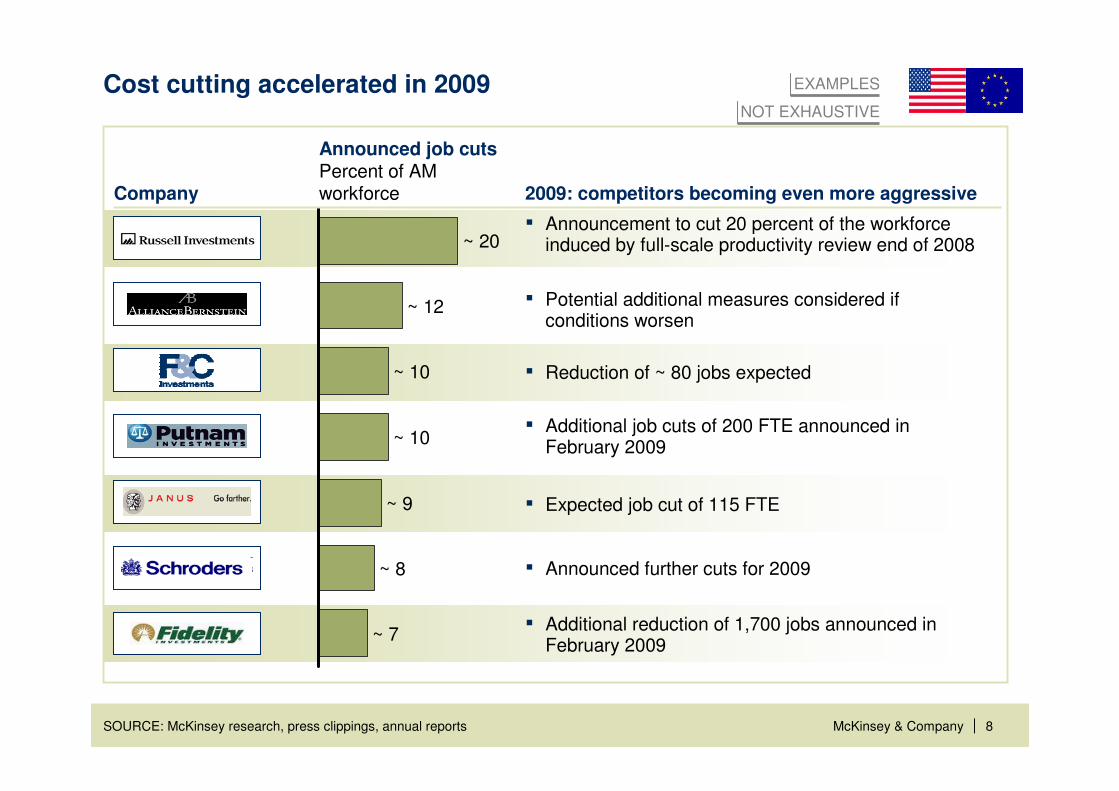

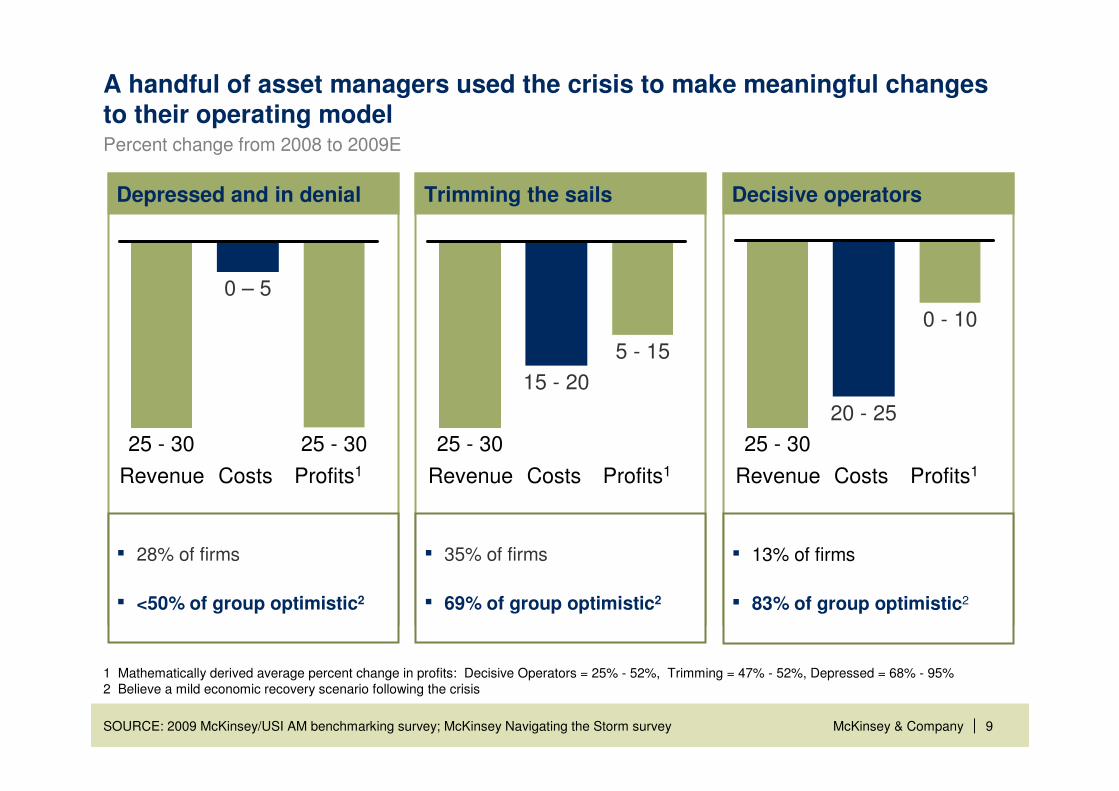

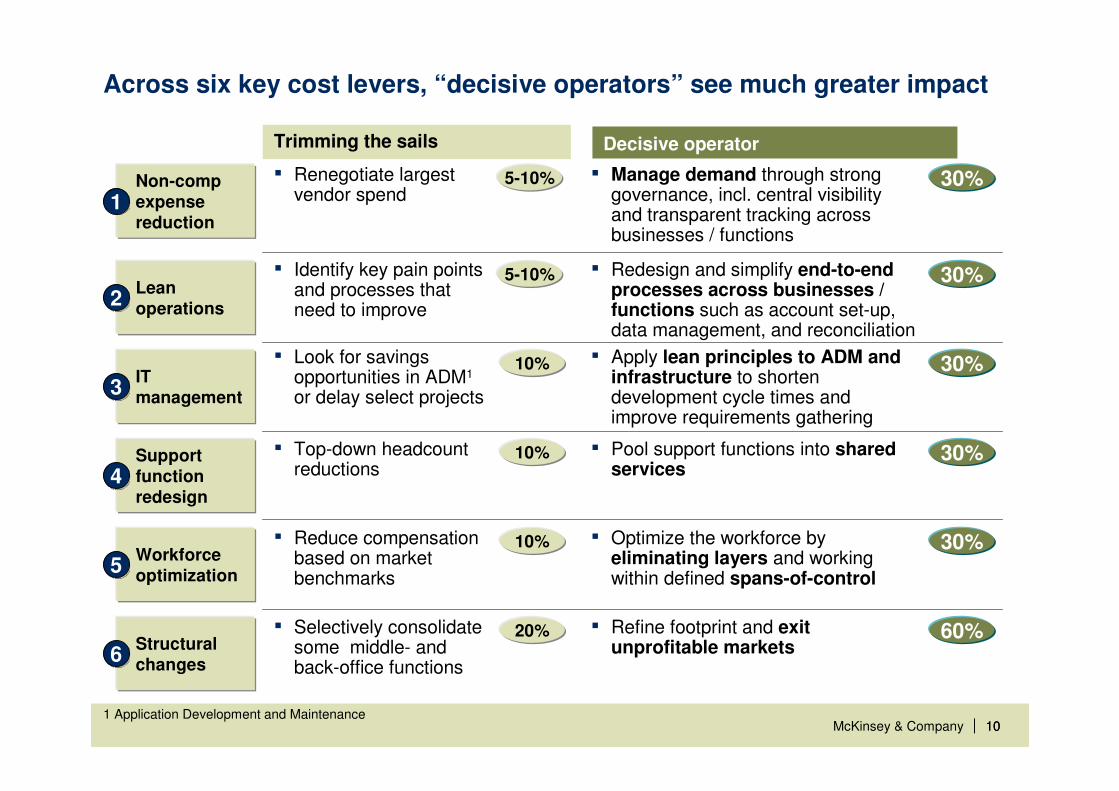

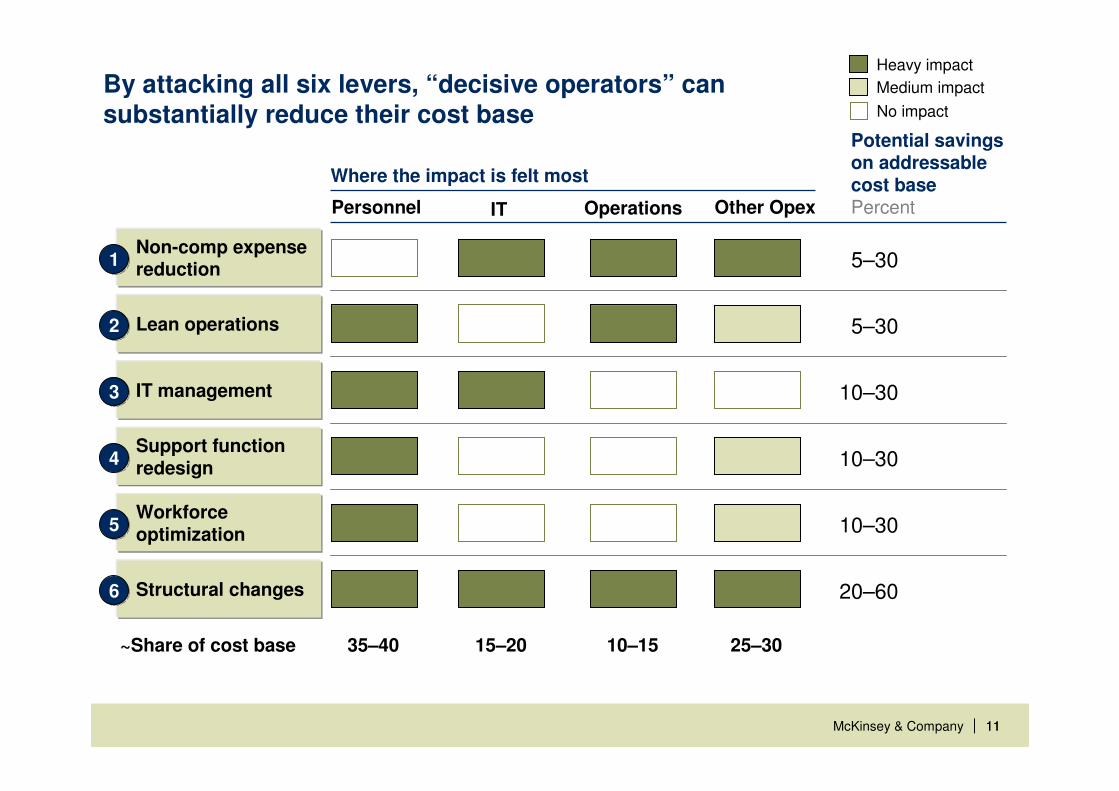

Most asset managers have struggled to realign their cost base to lower assets and revenues

SOURCE: McKinsey/USI 2009 AM benchmarking survey; McKinsey “Navigating the storm” survey; Analyst reports (Morgan Stanley and Barclays Capital)

Average AUM Revenues Expenses Profit

9196

100

2009E20082007

74

90

100

2009E20082007

-10%

83

96100

2009E20082007

-4%

53

90

100

2009E20082007

100 = 2007 results indexed; ‘08 change in profits from same firms in both benchmarking surveys

|McKinsey & Company 7

Key messages

2009 marked a decade low in AM margins

Excellence in business management, not just investment management, is now required for firms to build a robust operating model

Looking ahead, despite a lot of uncertainty, the asset management market can be an opportunity-rich environment for firms that can capitalize on 5 structural shifts

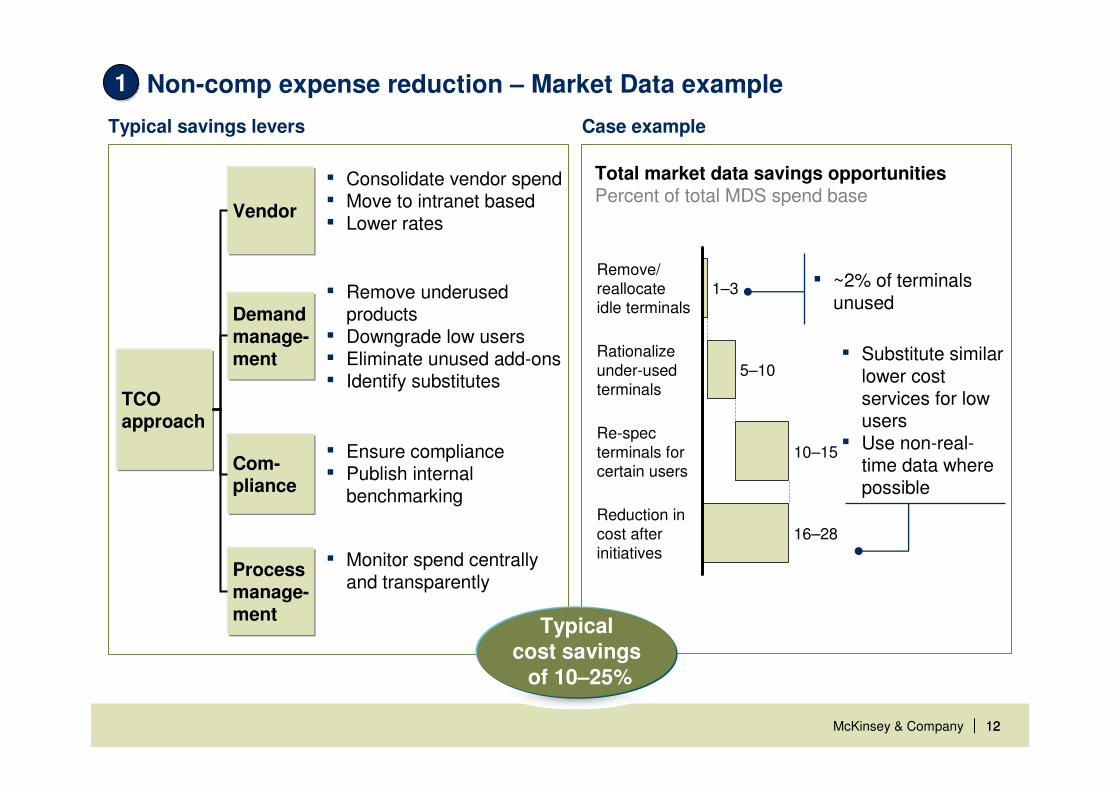

Total market data savings opportunitiesPercent of total MDS spend base

▪ ~2% of terminals unused

▪ Substitute similar lower cost services for low users

▪ Use non-real-time data where possible

Typical cost savings

of 10–25%

|McKinsey & Company 1313

Product development

▪ Install lean requirements definition process with a set of go / no-go points between Ops & Technology and the product groups before product launch

Investment management

▪ Improve cycle time of innovation and pre-trade investment ideas

▪ Implement cost, quality and service metrics to manage vendor performance

Asset management operations

▪ Implement common workflows to simplify process and reduce waste

Fund administration

▪ Optimize staff locations to load balance and segment complexity by asset type

Client Service▪ Consolidate redundant functional units (e.g., transfer

agency processing groups)

Lean techniques across the value chain22

|McKinsey & Company 1414

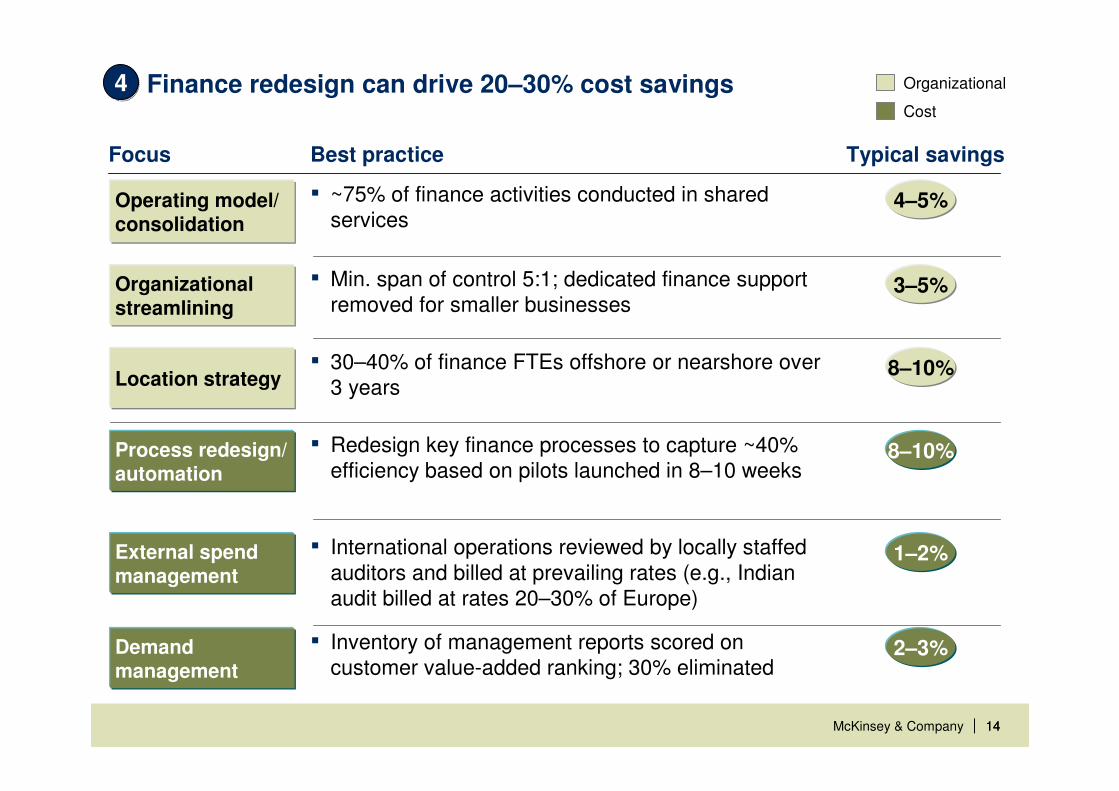

Finance redesign can drive 20–30% cost savings

1–2%

44 Organizational

Best practice Typical savingsFocus

4–5%Operating model/ consolidation

▪ ~75% of finance activities conducted in shared services

Organizational streamlining

▪ Min. span of control 5:1; dedicated finance support removed for smaller businesses

3–5%

Location strategy▪ 30–40% of finance FTEs offshore or nearshore over

3 years8–10%

Cost

Process redesign/ automation

▪ Redesign key finance processes to capture ~40% efficiency based on pilots launched in 8–10 weeks

8–10%

External spend management

▪ International operations reviewed by locally staffed auditors and billed at prevailing rates (e.g., Indian audit billed at rates 20–30% of Europe)

Demand management

▪ Inventory of management reports scored on customer value-added ranking; 30% eliminated

2–3%

|McKinsey & Company 1515

Workforce optimization – Spans and Layers

Optimizing Spans and Layers

▪ Reduce compensation costs by 10–20%

▪ Improve speed and agility

▪ Help create a stronger performance culture with clear accountability

▪ Clarify career paths and increase employee satisfaction and retention

Typical Spans and Layers process

▪ Align on targets by area and toolkit

▪ Identify areas with low spans of control

▪ Identifying areas to delayer management

▪ Evaluate tradeoffs and select the desired end state

▪ Develop scorecards to monitor progress

8Layers

AfterBefore

11Layers

5Span

8Span

55

|McKinsey & Company 1616 SOURCE: McKinsey Quarterly Performance Transformation Survey, July 2008

There are several success factors for sustained cost cutting efforts

Percent of respondents (total respondents = 2,994)

What would you change next time in your transformation?

▪ Better planning and preparation (e.g., be ready to integrate with organization, create a clear roadmap)

▪ Allocate more resources from the startUse disciplined program governance

5

▪ Focus more effort on creating a culture of change (ensure peopleresistant to change are engaged)

▪ Gain more buy-in and personal leadership from the CEO

Take a holistic approach

3

▪ Spend more time engaging the workforce

▪ Gain earlier ‘success stories’ to demonstrate the impact and potential

Focus on business unit ownership

4

▪ Spend more time developing and communicating a ‘change story’

▪ Have stronger alignment of the top management teamAlign the senior team

2

▪ Set a higher aspiration

Set high aspirations

1

▪ Set clearer targets

Response rank(1 = most popular)

9

1

5

3

7

2

8

6

10

4

|McKinsey & Company 17

Key messages

2009 marked a decade low in AM margins

Excellence in business management, not just investment management, is now required for firms to build a robust operating model

Looking ahead, despite a lot of uncertainty, the asset management market can be an opportunity-rich environment for firms that can capitalize on 5 structural shifts

1

2

3

|McKinsey & Company 18

There are a number of opportunities created by structural shifts that have and will continue to shape the future of asset management

1The industry is becoming increasingly concentrated and dominated by bank-owned players in Canada and “pure plays” in the US due to faster organic growth and acquisitions

|McKinsey & Company 19

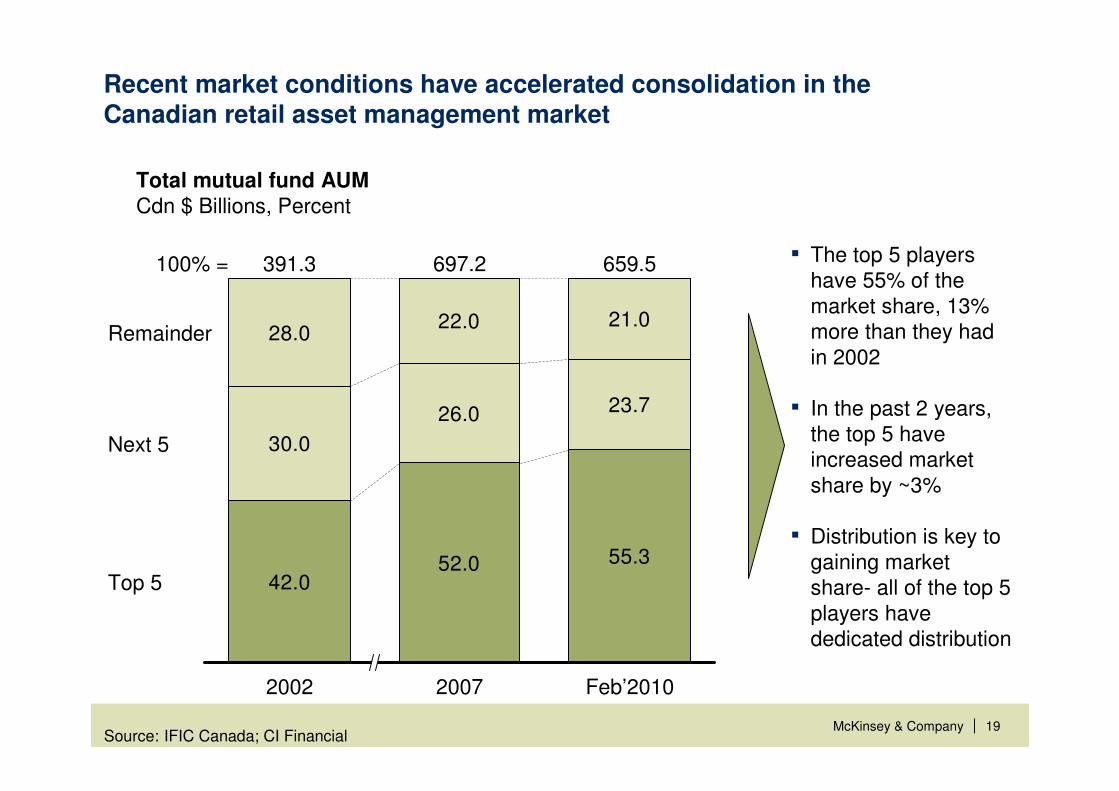

Recent market conditions have accelerated consolidation in the Canadian retail asset management market

Total mutual fund AUM Cdn $ Billions, Percent

Source: IFIC Canada; CI Financial

42.052.0 55.3

30.0

26.0 23.7

28.022.0 21.0

2002

391.3100% =

Top 5

Next 5

Remainder

Feb’2010

659.5

2007

697.2 ▪ The top 5 players have 55% of the market share, 13% more than they had in 2002

▪ In the past 2 years, the top 5 have increased market share by ~3%

▪ Distribution is key to gaining market share- all of the top 5 players have dedicated distribution

|McKinsey & Company 20SOURCE: Institutional Investor; SNL Financial; McKinsey

36 3951

63

3538

32

2398

20 15 17 13

11

1998

17

2003

1

27

2007

1

21

20081

Insurance andOther-owned

Broker-owned

Bank-owned

Independent

100% =

Asset share of top 50 US Asset Managers by OwnershipPercent, $ Trillions

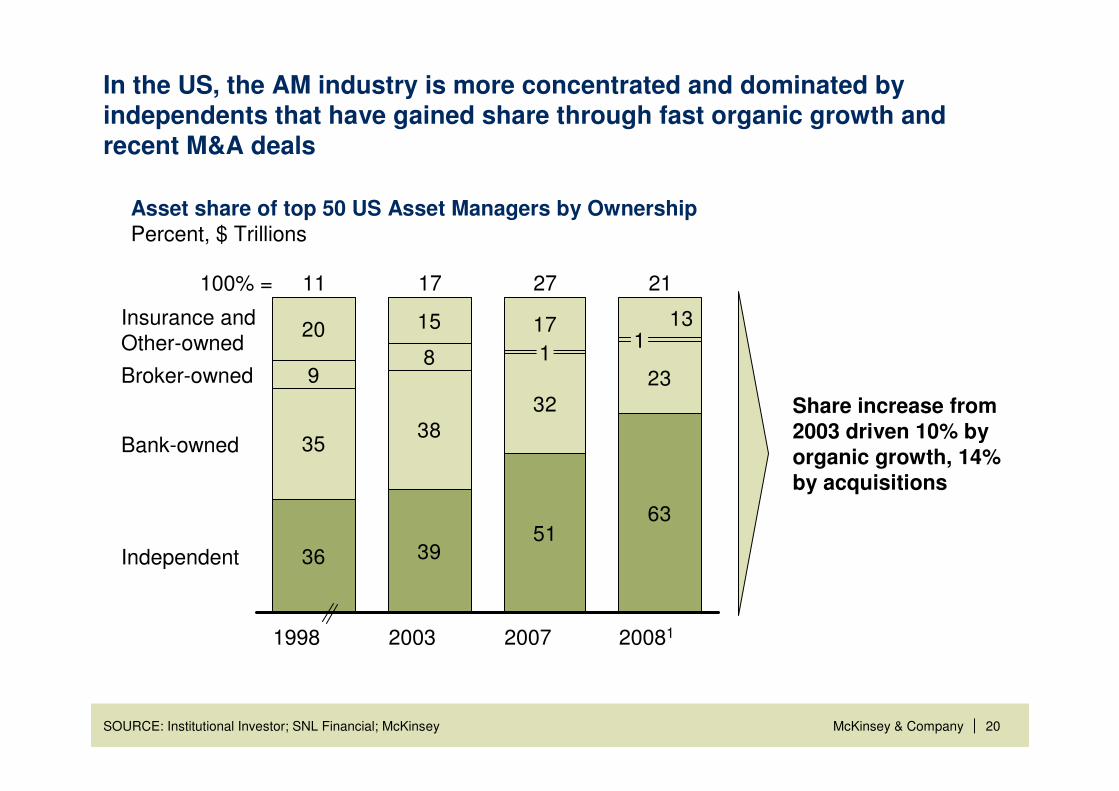

In the US, the AM industry is more concentrated and dominated byindependents that have gained share through fast organic growth and recent M&A deals

Share increase from 2003 driven 10% by organic growth, 14% by acquisitions

|McKinsey & Company 21

There are a number of opportunities created by the structural shifts that have and will continue to shape the future of asset management

2Secular shifts in allocations and investor expectations will enable those managers who can adapt to capture share and offset impact of deteriorating revenue mix

1The industry is becoming increasingly concentrated and dominated by bank-owned players in Canada and “pure plays” in the US due to faster organic growth and acquisitions

|McKinsey & Company 22

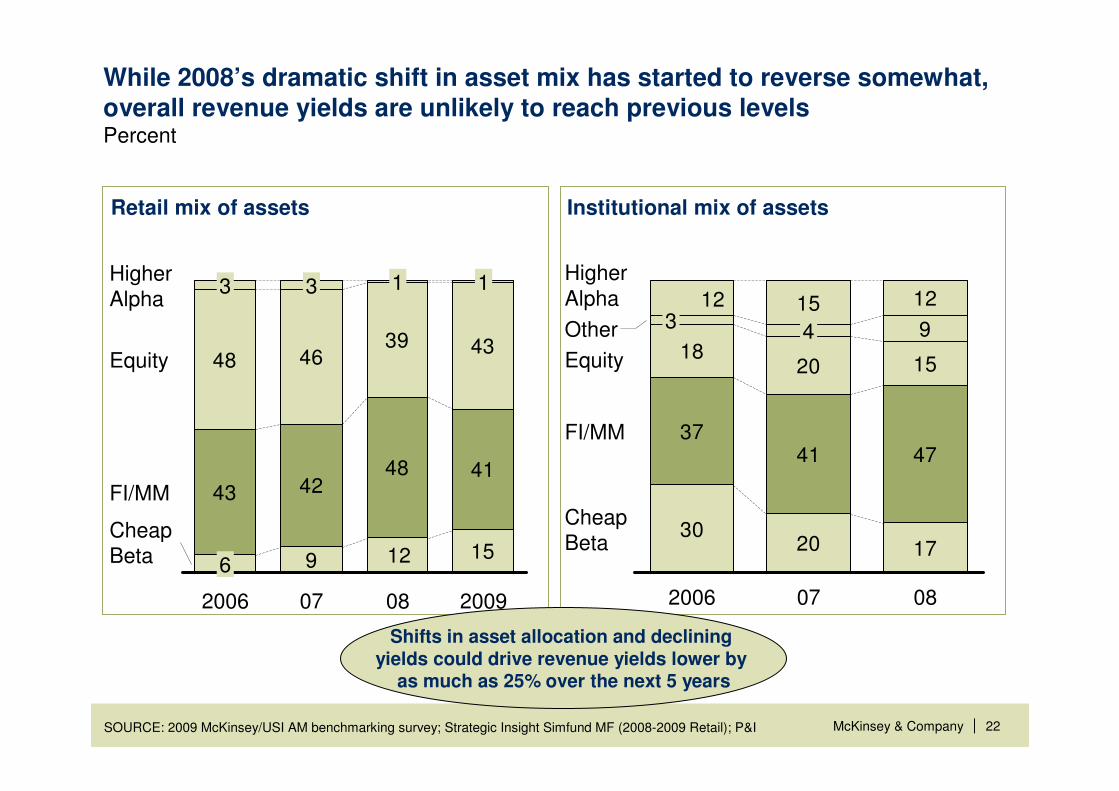

Retail mix of assets

9 1512

41484243

43394648

Cheap Beta

FI/MM

Equity

Higher Alpha

2009

1

08

1

07

3

2006

6

3

Institutional mix of assets

3020 17

3741 47

1820 15

15 12

9

123

Cheap Beta

FI/MM

Equity

Other

Higher Alpha

0807

4

2006

While 2008’s dramatic shift in asset mix has started to reverse somewhat, overall revenue yields are unlikely to reach previous levelsPercent

Shifts in asset allocation and declining yields could drive revenue yields lower by

as much as 25% over the next 5 years

|McKinsey & Company 23

Net revenue yields in retail and institutional AM have declined from their peakBps

Retail net revenues/AUM Institutional net revenues/AUM

3941423735363433

’09E1

341

’080706050403022001

434645

4851

545359

’09E1

351

080706050403022001

1 2009 based on publicly listed players only, Retail = Eaton Vance, Federated Investors, Franklin Templeton, Invesco, Janus, T Rowe Price, US Global Investors and Waddell & Reed; Institutional = Affiliated Managers Group, AllianceBernstein, Artio Global Investors, Calamos, Pzena, and Virtus Investment Partners

SOURCE: 2009 McKinsey/USI AM benchmarking survey; SNL Financial

Decline due to lower revenue yields and changing asset and product mix

|McKinsey & Company 24

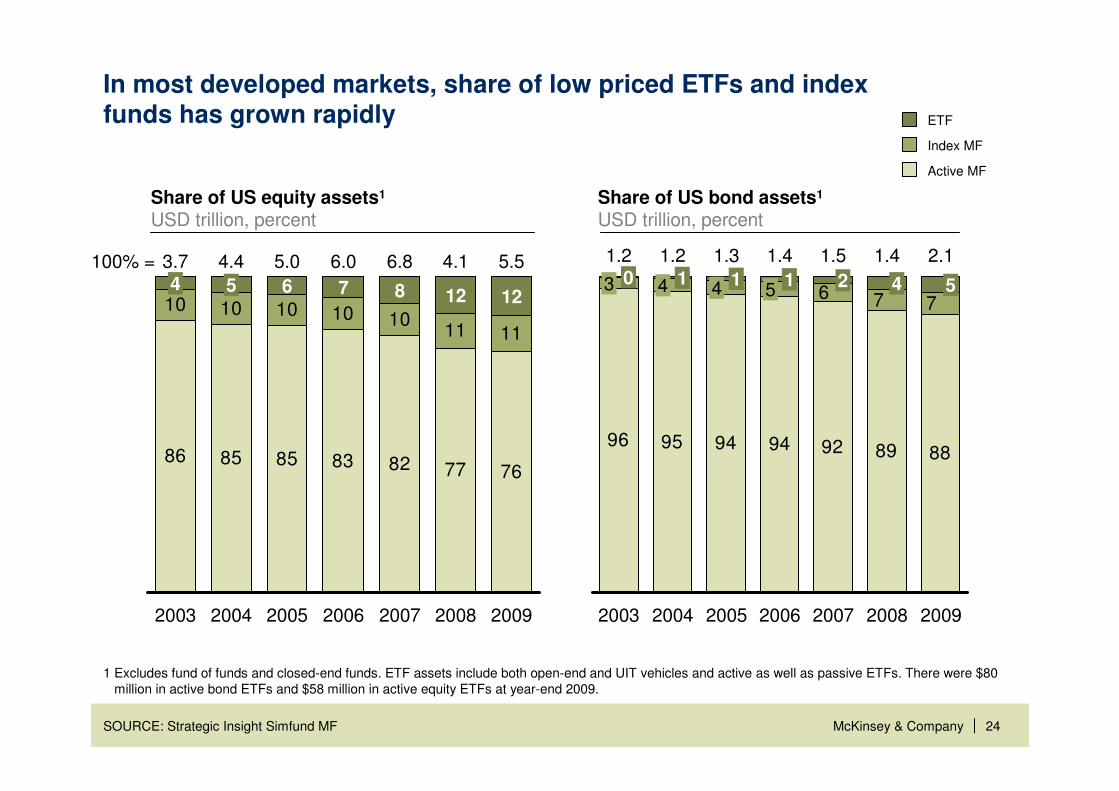

In most developed markets, share of low priced ETFs and index funds has grown rapidly

1 Excludes fund of funds and closed-end funds. ETF assets include both open-end and UIT vehicles and active as well as passive ETFs. There were $80 million in active bond ETFs and $58 million in active equity ETFs at year-end 2009.

SOURCE: Strategic Insight Simfund MF

76778283858586

111110101010108

2006

6.0 6.8

2007

124

3.7

2003

5

4.4

2004

4.1

2009

7

2005

100% = 5.0 5.5

12

2008

6

Index MF

Active MF

ETF

Share of US equity assets1

USD trillion, percent

96 95 94 94 92 89 88

7761 4

20072005

1.3 1.5

4 21

2004 2006

1.41.2

54 1

2003

1.2

3 0 5

2008 2009

1.4 2.1

Share of US bond assets1

USD trillion, percent

|McKinsey & Company 25

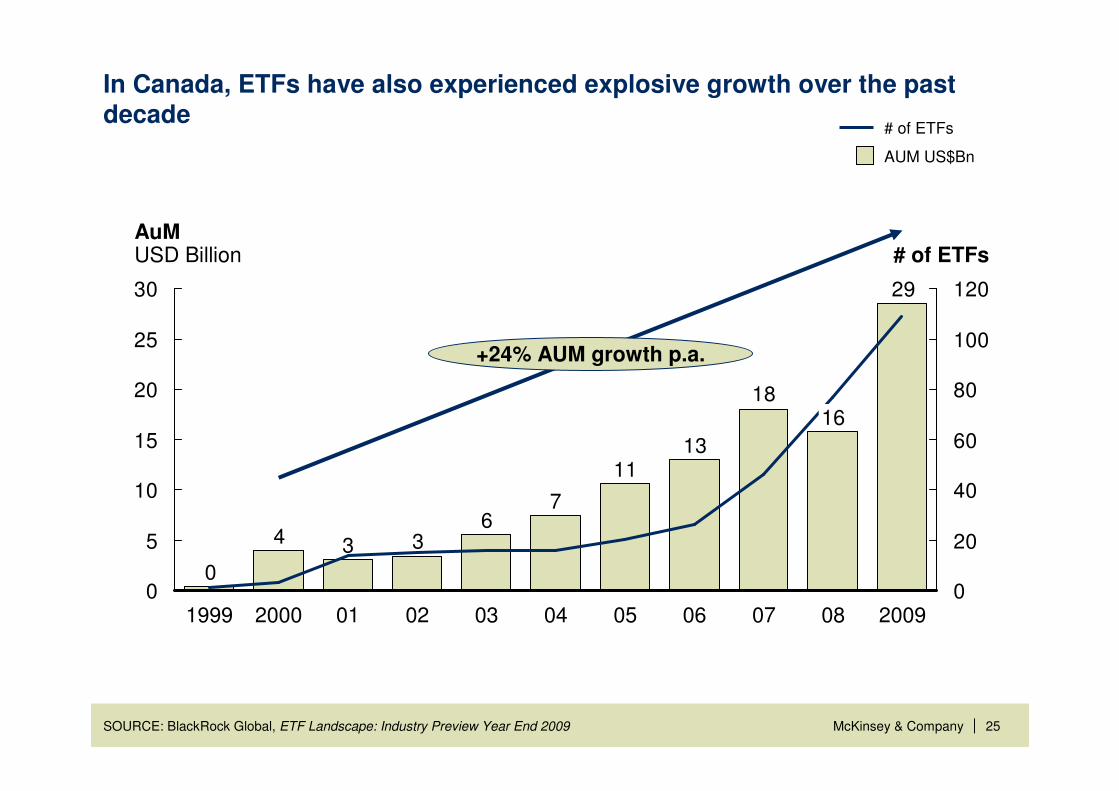

In Canada, ETFs have also experienced explosive growth over the past decade

SOURCE: BlackRock Global, ETF Landscape: Industry Preview Year End 2009

29

18

1311

76

334

00

5

10

15

20

25

30

0

20

40

60

80

100

120

# of ETFsAuM USD Billion

+24% AUM growth p.a.

200908

16

0706050403020120001999

AUM US$Bn

# of ETFs

|McKinsey & Company 26

There are a number of opportunities created by the structural shifts that have and will continue to shape the future of asset management

Proven resilience of qualified funds and a reinvigorated push towards open architecture demands a targeted DC strategy

3

2Secular shifts in allocations and investor expectations will enable those managers who can adapt to capture share and offset impact of deteriorating revenue mix

1The industry is becoming increasingly concentrated and dominated by bank-owned players in Canada and “pure plays” in the US due to faster organic growth and acquisitions

|McKinsey & Company 27

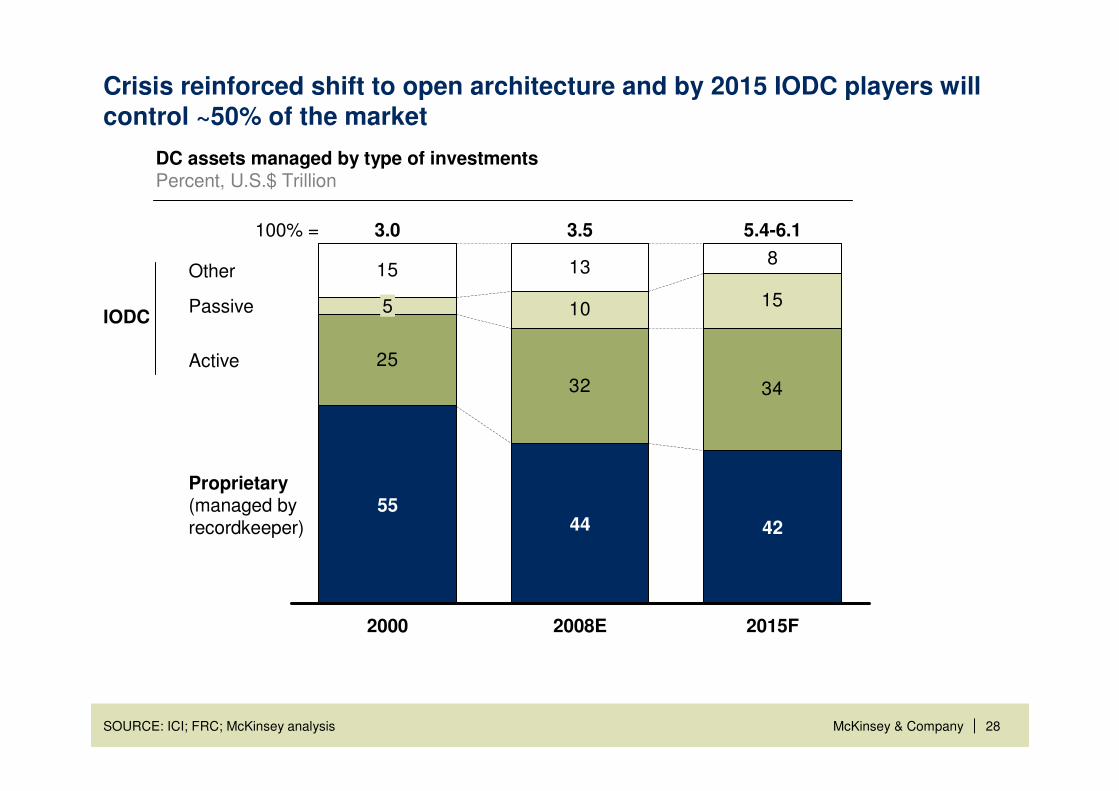

DC assets likely to return to ‘07 levels by 2011 and approach $6 T by 2015

SOURCE: ICI; American Benefits Council; Vanguard; J.P. Morgan Asset Management

2.7

2015F assetsRollovers / Withdrawals

2.4

Market appreciation

Contributions2009E assets

4.2

0.5-1.8

DC assets$ Trillions

~5.4-6.1

Estimated DC net flows$ Billions

19

45

69

86

89

2014

2013

2012

2011

2010

2007 assets

4.5 CAGR 4-6%

Cumulative net flows: ~$300 B

|McKinsey & Company 28SOURCE: ICI; FRC; McKinsey analysis

25

32 34

10 15

15 13 8

5.4-6.1

42

2008E

3.5

44

2000

3.0

55

5

2015F

100% =

Proprietary(managed by recordkeeper)

Active

Passive

Other

DC assets managed by type of investmentsPercent, U.S.$ Trillion

IODC

Crisis reinforced shift to open architecture and by 2015 IODC players will control ~50% of the market

|McKinsey & Company 29

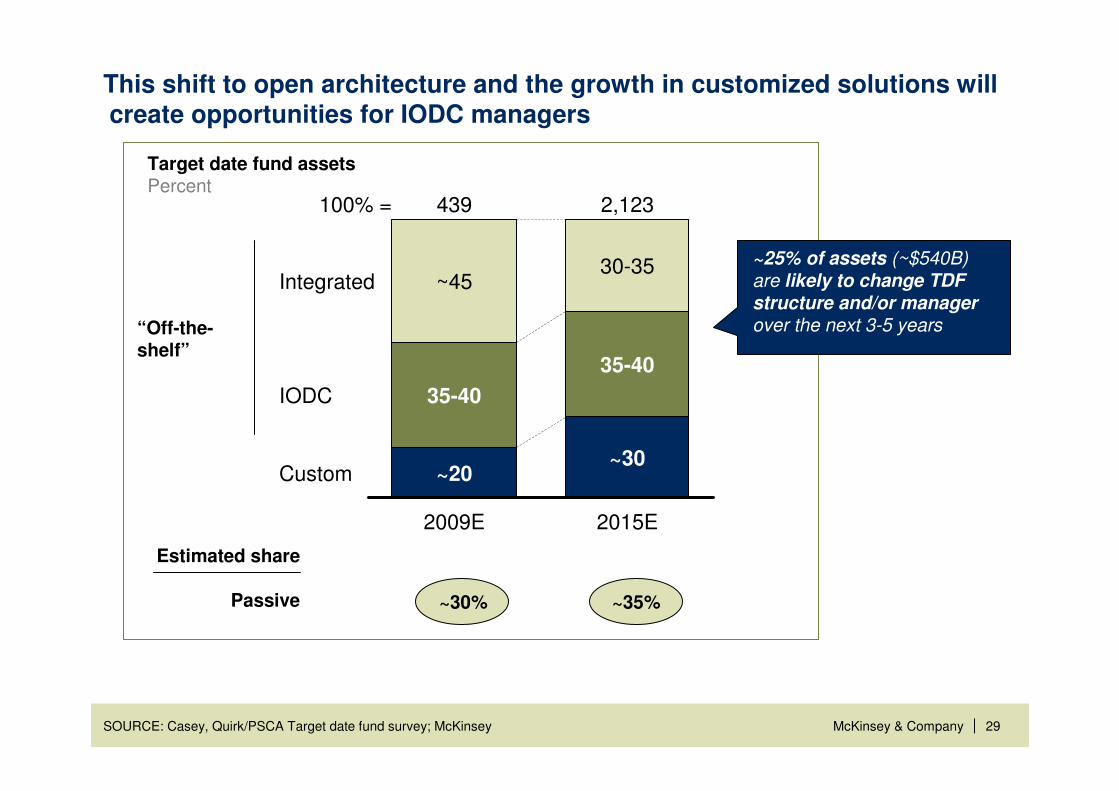

This shift to open architecture and the growth in customized solutions will create opportunities for IODC managers

SOURCE: Casey, Quirk/PSCA Target date fund survey; McKinsey

Passive

~25% of assets (~$540B) are likely to change TDF

structure and/or manager

over the next 3-5 years

Target date fund assetsPercent

Estimated share

“Off-the-shelf”

~30% ~35%

30-35

2015E

439100% =

~30

35-40

Integrated

35-40

2009E

~20

2,123

Custom

IODC

~45

|McKinsey & Company 30

There are a number of opportunities created by the structural shifts that have and will continue to shape the future of asset management

Emerging markets and Sovereign (Wealth) Funds will continue to represent one of the largest sources of global assets over the next five years

4

Proven resilience of qualified funds and a reinvigorated push towards open architecture demands a targeted DC strategy

3

2Secular shifts in allocations and investor expectations will enable those managers who can adapt to capture share and offset impact of deteriorating revenue mix

1The industry is becoming increasingly concentrated and dominated by bank-owned players in Canada and “pure plays” in the US due to faster organic growth and acquisitions

|McKinsey & Company 31

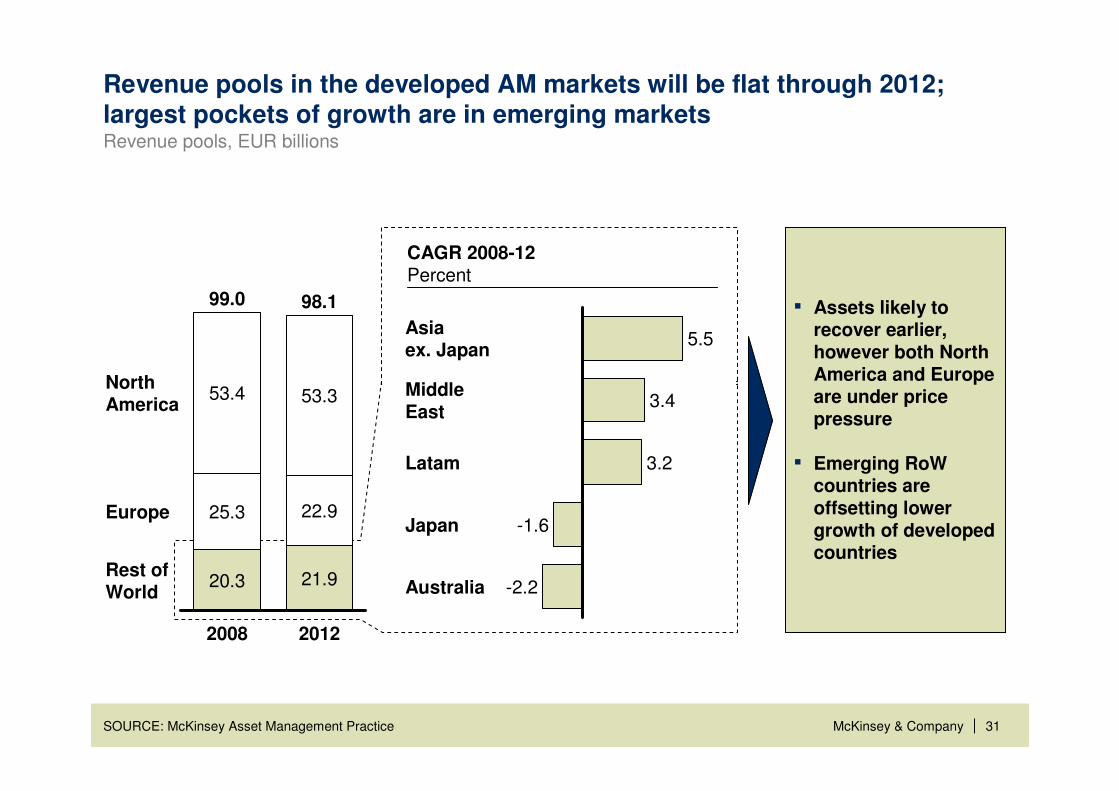

Revenue pools in the developed AM markets will be flat through 2012; largest pockets of growth are in emerging marketsRevenue pools, EUR billions

Europe 22.9

98.1

2012

21.9

North America

99.0

20.3

25.3

53.3

2008

53.4

Rest of World

CAGR 2008-12Percent

Australia

-1.6

Latam 3.2

-2.2

Japan

MiddleEast

3.4

Asiaex. Japan

5.5

▪ Assets likely to recover earlier, however both North America and Europe are under price pressure

▪ Emerging RoW countries are offsetting lower growth of developed countries

SOURCE: McKinsey Asset Management Practice

|McKinsey & Company 32

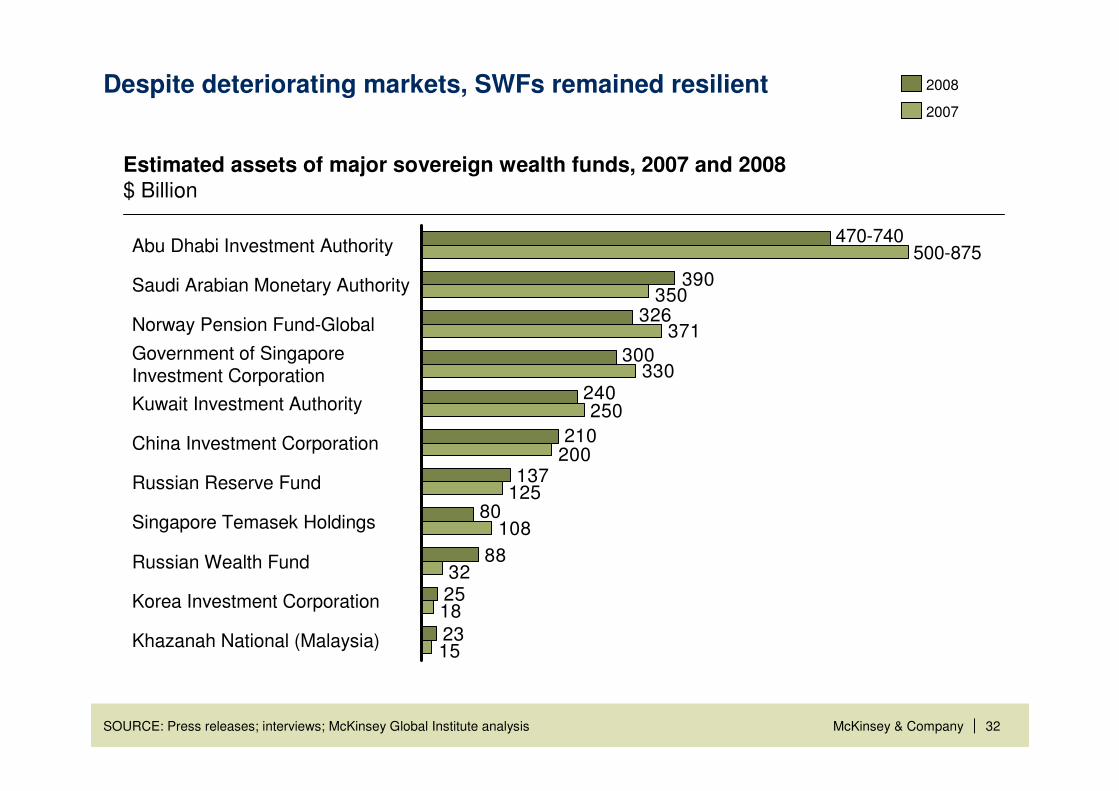

Despite deteriorating markets, SWFs remained resilient

23

25

88

80

137

210

240

300

326

390

15

18

32

108

125

200

250

330

371

350

470-740500-875Abu Dhabi Investment Authority

Saudi Arabian Monetary Authority

Norway Pension Fund-Global

Government of SingaporeInvestment Corporation

Kuwait Investment Authority

China Investment Corporation

Russian Reserve Fund

Singapore Temasek Holdings

Russian Wealth Fund

Korea Investment Corporation

Khazanah National (Malaysia)

2008

2007

Estimated assets of major sovereign wealth funds, 2007 and 2008 $ Billion

SOURCE: Press releases; interviews; McKinsey Global Institute analysis

|McKinsey & Company 33

3.0

4.8

3.8

5.8

2013E

Emerging markets

Other

2009

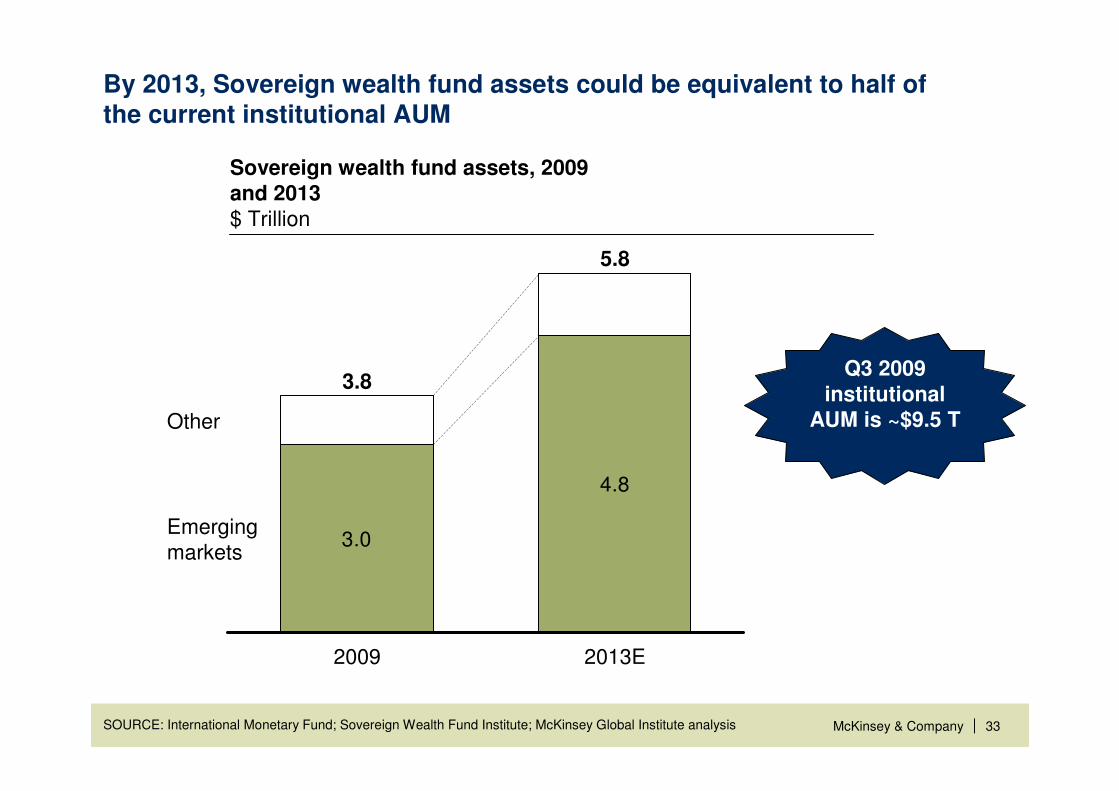

By 2013, Sovereign wealth fund assets could be equivalent to half of the current institutional AUM

Sovereign wealth fund assets, 2009 and 2013$ Trillion

SOURCE: International Monetary Fund; Sovereign Wealth Fund Institute; McKinsey Global Institute analysis

Q3 2009 institutional

AUM is ~$9.5 T

|McKinsey & Company 34

There are a number of opportunities created by the structural shifts that have and will continue to shape the future of asset management

Alternative asset classes will continue to gain market share as investors continue to seek diversification and uncorrelated returns – however, at reduced fees and with increased transparency around reporting and performance

5

Emerging markets and Sovereign (Wealth) Funds will continue to represent one of the largest sources of global assets over the next five years

4

Proven resilience of qualified funds and a reinvigorated push towards open architecture demands a targeted DC strategy

3

2Secular shifts in allocations and investor expectations will enable those managers who can adapt to capture share and offset impact of deteriorating revenue mix

1The industry is becoming increasingly concentrated and dominated by bank-owned players in Canada and “pure plays” in the US due to faster organic growth and acquisitions

|McKinsey & Company 35

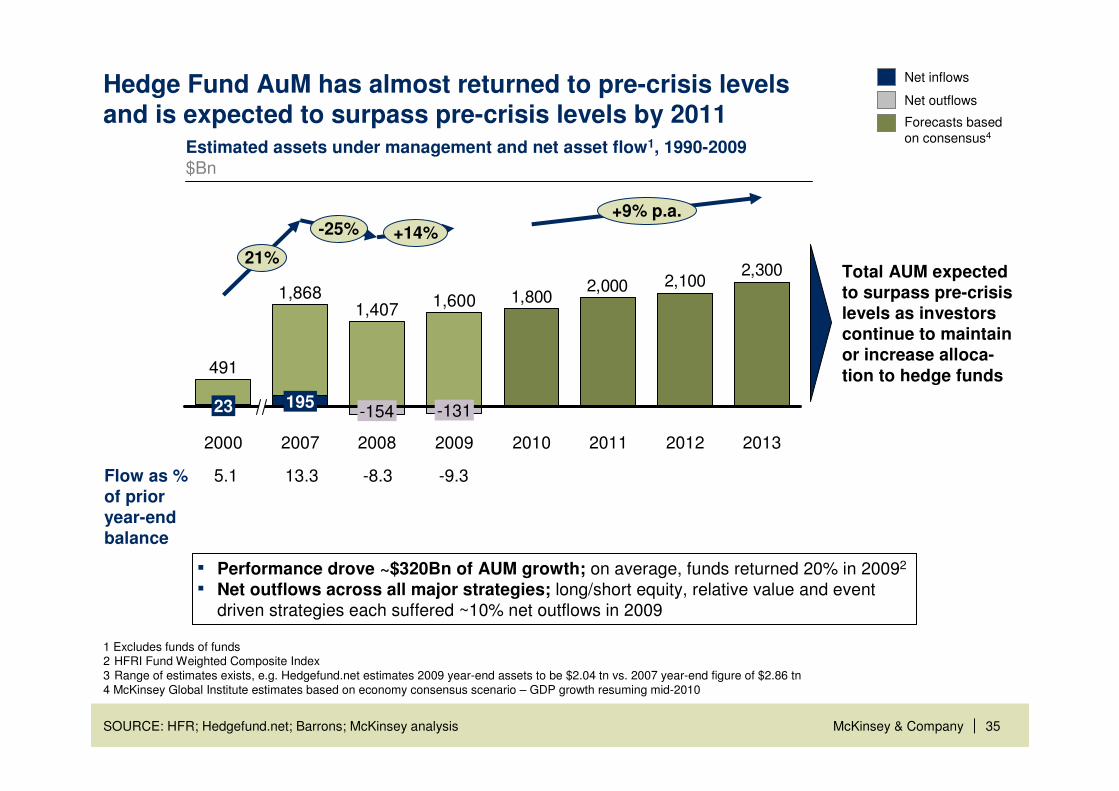

Hedge Fund AuM has almost returned to pre-crisis levels and is expected to surpass pre-crisis levels by 2011

Estimated assets under management and net asset flow1, 1990-2009$Bn

2,3002,1002,000

1,800

+9% p.a.

+14%

21%

-25%

20132012201120102009

1,600

-131

2008

1,407

-154

2007

1,868

195

2000

491

23

1 Excludes funds of funds2 HFRI Fund Weighted Composite Index3 Range of estimates exists, e.g. Hedgefund.net estimates 2009 year-end assets to be $2.04 tn vs. 2007 year-end figure of $2.86 tn4 McKinsey Global Institute estimates based on economy consensus scenario – GDP growth resuming mid-2010

Flow as % of prior year-end balance

5.1 13.3 -8.3 -9.3

▪ Performance drove ~$320Bn of AUM growth; on average, funds returned 20% in 20092

▪ Net outflows across all major strategies; long/short equity, relative value and event driven strategies each suffered ~10% net outflows in 2009

Total AUM expected to surpass pre-crisis levels as investors continue to maintain or increase alloca-tion to hedge funds

Net inflows

Net outflows

Forecasts based on consensus4

|McKinsey & Company 36

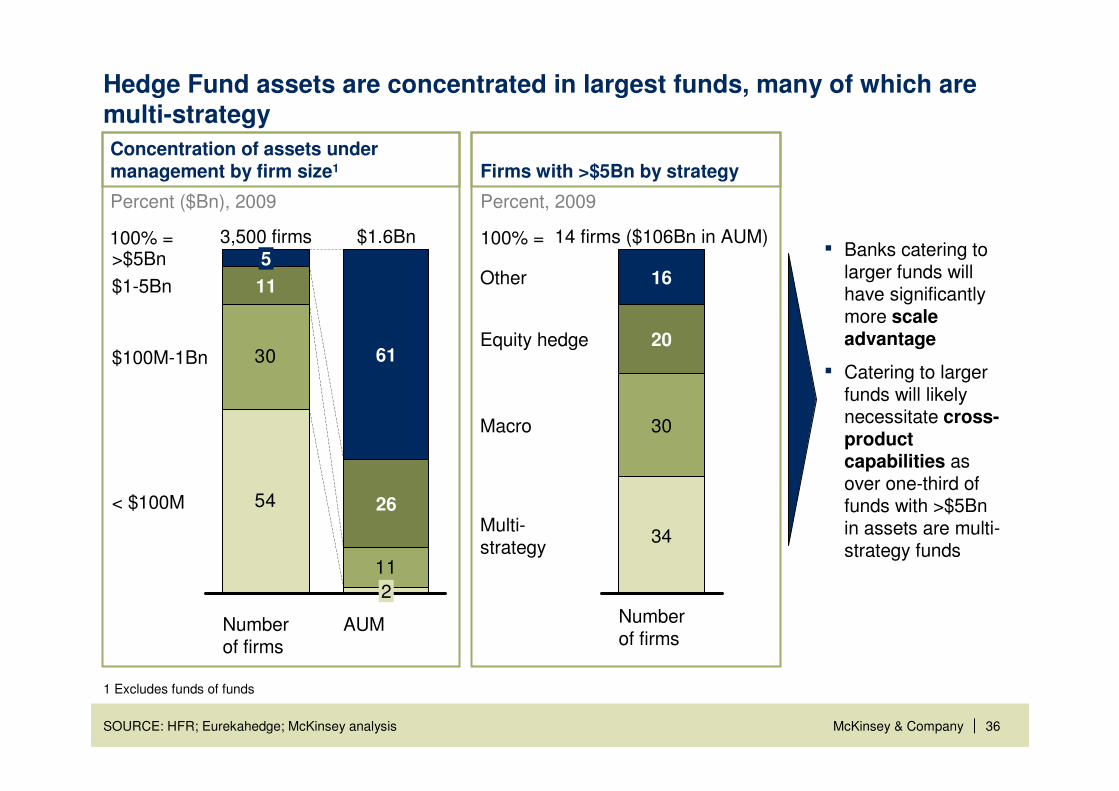

Hedge Fund assets are concentrated in largest funds, many of which are multi-strategy

SOURCE: HFR; Eurekahedge; McKinsey analysis

1 Excludes funds of funds

▪ Banks catering to larger funds will have significantly more scale advantage

▪ Catering to larger funds will likely necessitate cross-product capabilities as over one-third of funds with >$5Bnin assets are multi-strategy funds

30

11

54< $100M

$100M-1Bn

$1-5Bn

>$5Bn

AUM

$1.6Bn

2

26

61

Number of firms

3,500 firms

11

5

Concentration of assets under management by firm size1 Firms with >$5Bn by strategy

100% = 100% =

Multi-strategy

Macro

Equity hedge

Other

Number of firms

20

30

16

14 firms ($106Bn in AUM)

34

Percent, 2009 Percent ($Bn), 2009

|McKinsey & Company 37

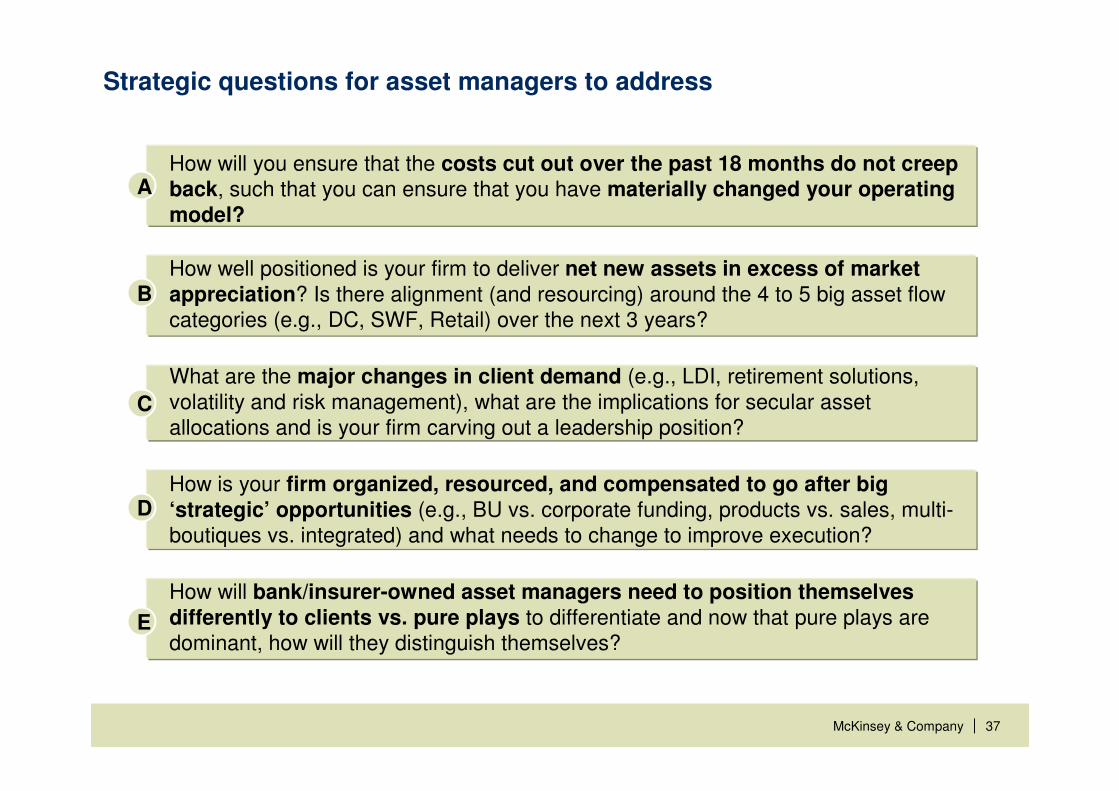

E

Strategic questions for asset managers to address

D

C

B

AHow will you ensure that the costs cut out over the past 18 months do not creep back, such that you can ensure that you have materially changed your operating model?

How well positioned is your firm to deliver net new assets in excess of market appreciation? Is there alignment (and resourcing) around the 4 to 5 big asset flow categories (e.g., DC, SWF, Retail) over the next 3 years?

What are the major changes in client demand (e.g., LDI, retirement solutions, volatility and risk management), what are the implications for secular asset allocations and is your firm carving out a leadership position?

How is your firm organized, resourced, and compensated to go after big ‘strategic’ opportunities (e.g., BU vs. corporate funding, products vs. sales, multi-boutiques vs. integrated) and what needs to change to improve execution?

How will bank/insurer-owned asset managers need to position themselves differently to clients vs. pure plays to differentiate and now that pure plays are dominant, how will they distinguish themselves?

|McKinsey & Company 38

Appendix

|McKinsey & Company 39

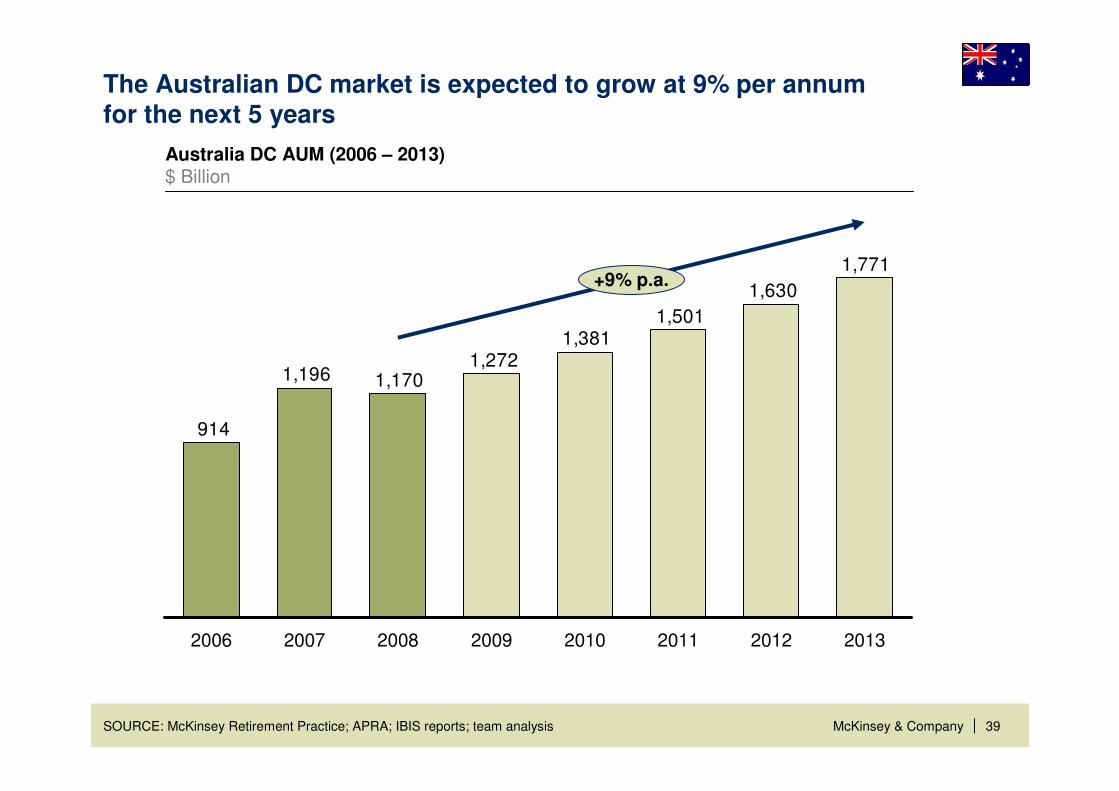

The Australian DC market is expected to grow at 9% per annumfor the next 5 years

SOURCE: McKinsey Retirement Practice; APRA; IBIS reports; team analysis

Australia DC AUM (2006 – 2013) $ Billion

1,771

1,630

1,5011,381

1,2721,1701,196

914

2006 2007 20092008 2010

+9% p.a.

20132011 2012

|McKinsey & Company 40

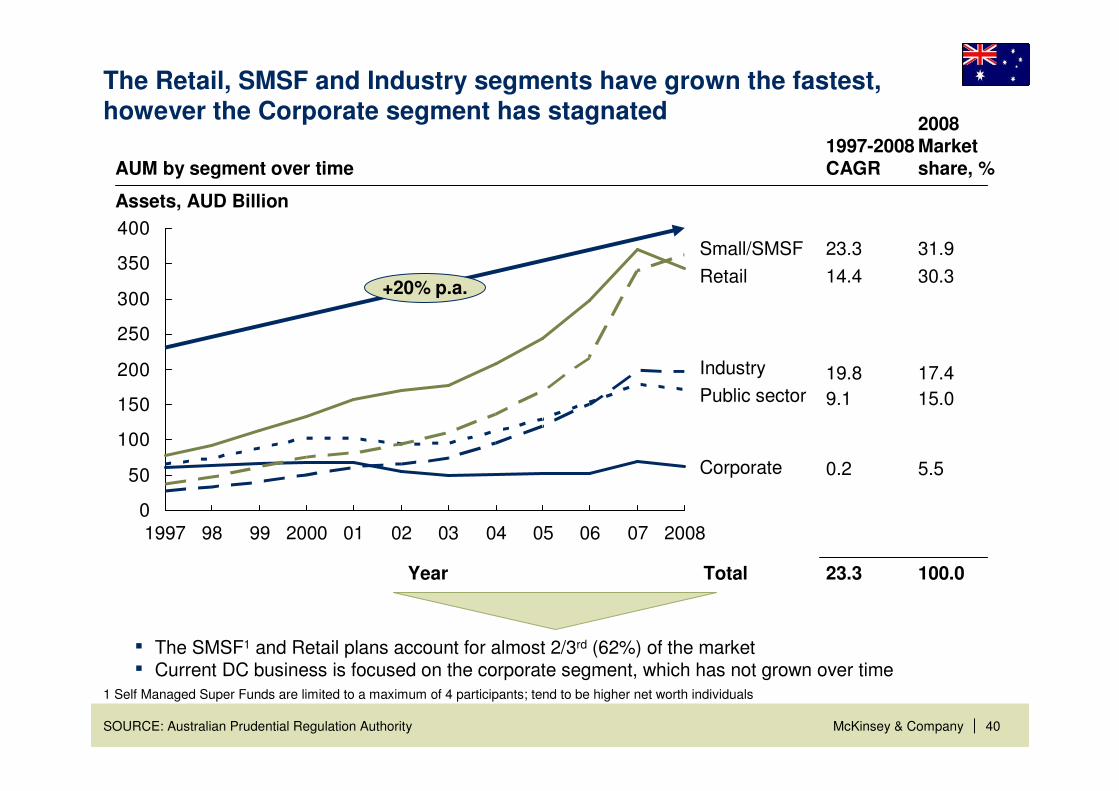

The Retail, SMSF and Industry segments have grown the fastest, however the Corporate segment has stagnated

SOURCE: Australian Prudential Regulation Authority

0

50

100

150

200

250

300

350

400

1997 98 99 2000

Corporate

0504030201 06

Industry

Public sector

Retail

Small/SMSF

07 2008

+20% p.a.

1997-2008CAGR

23.3

14.4

19.8

9.1

0.2

23.3Total

AUM by segment over time

Assets, AUD Billion

Year

▪ The SMSF1 and Retail plans account for almost 2/3rd (62%) of the market▪ Current DC business is focused on the corporate segment, which has not grown over time

1 Self Managed Super Funds are limited to a maximum of 4 participants; tend to be higher net worth individuals