Presenting a live 90‐minute webinar with interactive Q&A Structured Settlements and Deferred Attorney Fees Leveraging Structured Arrangements to Protect the Client, Facilitate Case Resolution, and Provide Tax‐Deferred Benefits for Counsel T d ’ f l f 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific TUESDAY, MARCH 1, 2011 T oday’ s faculty features: Brian Michaels, General Counsel, Brook Hollow Financial, Chicago Christopher J. Princis, Senior Vice President, Brook Hollow Financial, Chicago Robert W. Wood, Partner, Wood & Porter, San Francisco The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Transcript

Presenting a live 90‐minute webinar with interactive Q&A

Structured Settlements and Deferred Attorney FeesLeveraging Structured Arrangements to Protect the Client, Facilitate Case Resolution, and Provide Tax‐Deferred Benefits for Counsel

Brian Michaels, General Counsel, Brook Hollow Financial, Chicago

Christopher J. Princis, Senior Vice President, Brook Hollow Financial, Chicago

Robert W. Wood, Partner, Wood & Porter, San Francisco

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

For CLE purposes, please let us know how many people are listening at your location by completing each of the following steps:

• Close the notification box

• In the chat box, type (1) your company name and (2) the number of attendees at your location

• Click the blue icon beside the box to send

Tips for Optimal Quality

S d Q litSound QualityIf you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory and you are listening via your computer speakers, you may listen via the phone: dial 1-866-873-1442 and enter your PIN when prompted Otherwise please send us a chat or e mail when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

After Settlement SuccessWhat You Need to KnowWhat You Need to Know

Brian S. Michaels, Esq. General Counsel, Brook Hollow Financial

Christopher J. PrincisSenior Vice President, Brook Hollow Financial

Robert W. WoodPartner Wood & PorterPartner, Wood & Porter

5

Agenda1. Settlement Funds/468B/QSF

2. Deferred Attorney Fees

3. Structured Settlements

4. Wrap-up

6

Challenges With Multi Party SettlementsChallenges With Multi-Party Settlements

Qualified Settlement Funds (1 of 2)• Qualified Settlement Funds (“QSFs”) were ( )

established by Congress.

• Fund is established and defendant pays i t th f d t l f li bilitinto the fund, gets a release of liability and tax deduction.

• Allows plaintiff(s) to settle case andAllows plaintiff(s) to settle case and receive payment from defendant without triggering constructive receipt of the funds.

• Routinely used in class actions and mass tort cases of all sizes and comple itcomplexity.

9

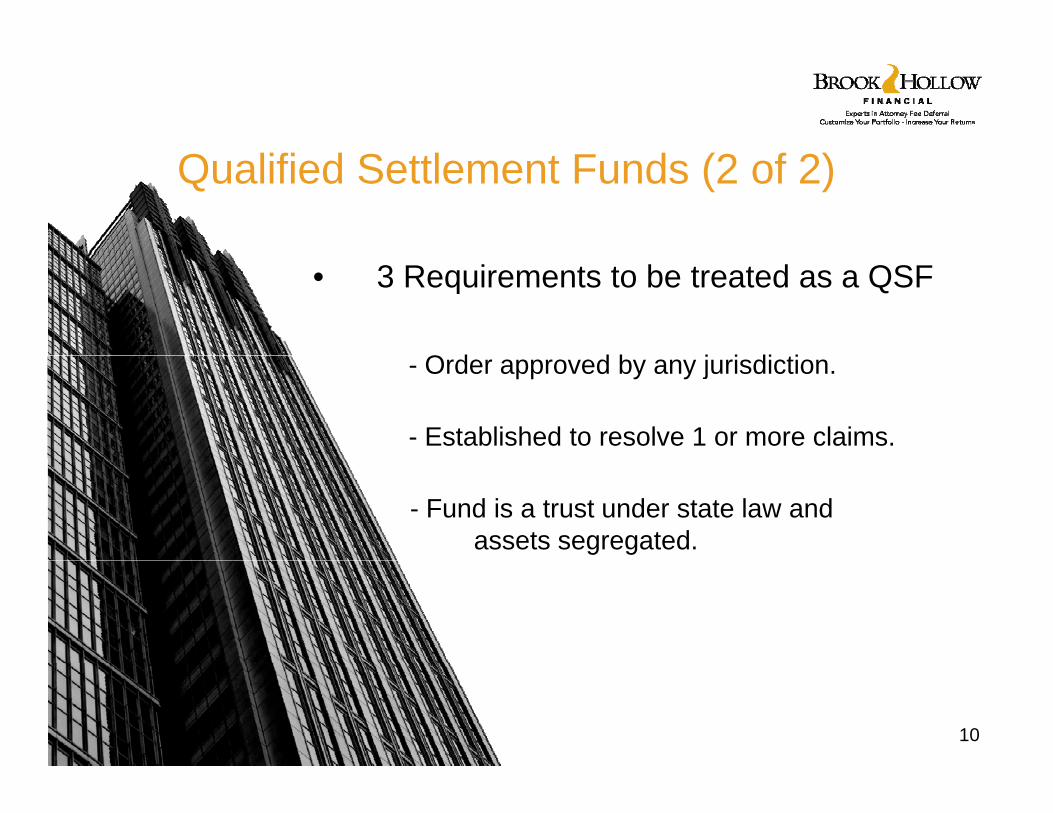

Qualified Settlement Funds (2 of 2)

• 3 Requirements to be treated as a QSF

O d d b j i di ti- Order approved by any jurisdiction.

- Established to resolve 1 or more claims.

- Fund is a trust under state law and assets segregated.

10

11

Cases Where QSFs Have Been Used

• 100’s of mass tort and class action cases

• Cook County Building50 l i tiff– 50+ plaintiffs

– Multitude of unresolved issues

• John Hancock ScaffoldingJohn Hancock Scaffolding– $78 million– 18 plaintiffs

20 d f d t• 20+ defendants, all paying at different times

12

Opportunities For Using QSFpp g• QSF by Case/Firm

L Fi t bli h QSF• Law Firm establishes own QSF – “similarly situated” cases

• QSF by Case/Multiple Firms– Each firm establishes own sub-

QSF (Avandia)

• Other

• Why?– Liens, administration, deferred

f

Other

attorney fees, structured settlements, SNTs, etc.

– Away from eyes/influence of defense– Makes everything easier

13

Deferred Attorney FFees

14

Let’s Clarify• ANY contingent fee can be

deferred (not just personal injury)

• Attorney can defer their contingent fee REGARDLESS if client chooses a structured settlement.

• Create custom portfolio with• Create custom portfolio with any investment option!

15

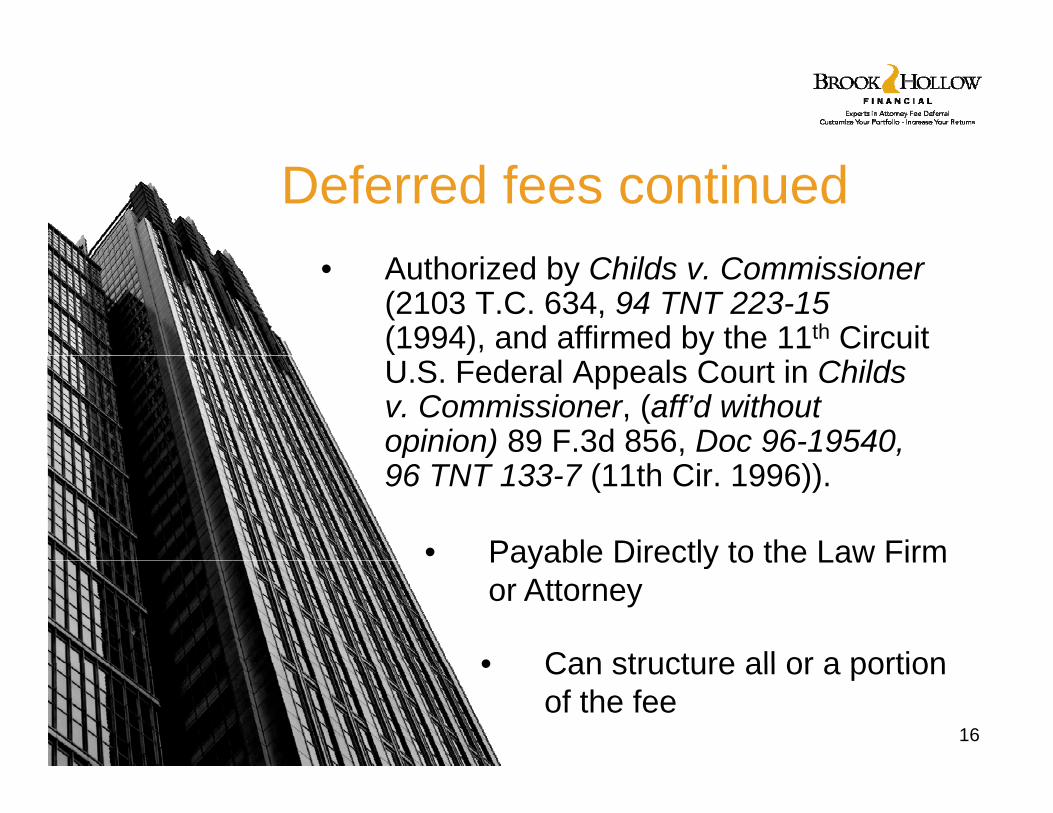

Deferred fees continued• Authorized by Childs v. Commissioner

(2103 T.C. 634, 94 TNT 223-15 (1994), and affirmed by the 11th Circuit U.S. Federal Appeals Court in Childs v. Commissioner, (aff’d without opinion) 89 F.3d 856, Doc 96-19540, p )96 TNT 133-7 (11th Cir. 1996)).

• Payable Directly to the Law FirmPayable Directly to the Law Firm or Attorney

• Can structure all or a portion• Can structure all or a portion of the fee

16

Why Structure Attorney Fees?• Income Tax Deferral. This is an excellent tool

to smooth out income from year to year and minimize problems such as the Alternative Minimum Tax and phase-outs with the very real possibility of lowering taxes actually paid.p y g y p

• Retirement Planning. 100% of income can be structured. Unlike other retirement plans there is no income limit on participation rules and no annualincome limit, on participation rules and no annual administrative costs. It has been described as an uncapped 401(K) plan.

• Overhead Expenses. Law firms have used structured attorney fees to provide for future law firm overhead expenses. By structuring a portion of current fees (or a portion of big blipsportion of current fees (or a portion of big blips in income) firms have lowered reliance on lines of credit for future operating costs.

17

Taxable Equivalent Analysis: What you have to earn to match the power of deferralWhat you have to earn to match the power of deferral

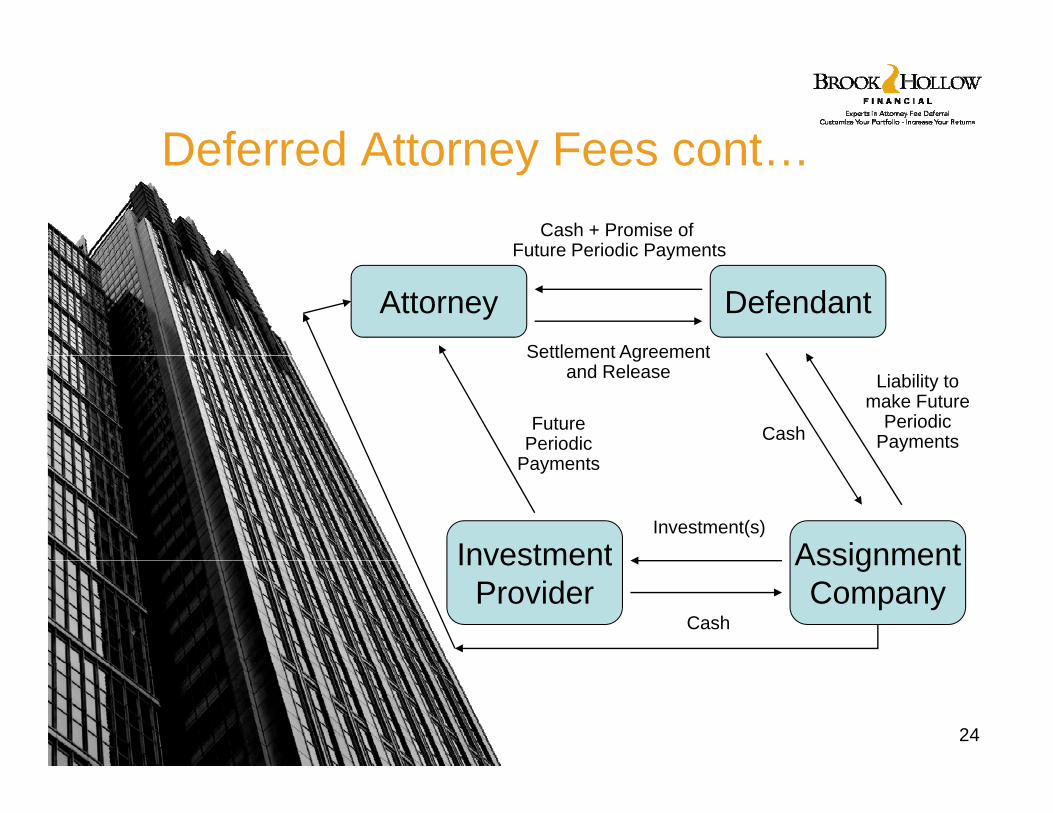

3. Parties Meet With Settlement Specialist to Determine Amount and Timing of Payments

4 Plaintiff Executes Settlement Agreement and4. Plaintiff Executes Settlement Agreement andRelease, with Attorney Fee payable in Exchange for…

5 D f d t P i t M k F t5. Defendants Promises to Make Future Periodic Payments to Attorney for fee

6. Defendant Assigns Obligation to Makeg gFuture Payments to Assignment Company

21

St t i C ti t Att FStructuring Contingent Attorney Fee: Procedural Steps

7. Defendant Transfers Cash to Assignment Company

8. Assignment Company Uses Cash to Purchaseg p yInvestments to Fund Future Payments

9. Assignment Company (or their Custodian) MakesFuture Periodic Payments to Plaintiff AttorneyFuture Periodic Payments to Plaintiff Attorney

10. Guarantee of the Performance of the Qualified Assignee is Issuedg

11. Attorney can structure their fee regardless of what client does with their settlement

22

Deferred Attorney Fees

Client Attorney

Legal Representation

y

Pay Fee in Cash +/or Promise of Future Periodic Payments

Key Point: Legal fee agreement between Client and Attorney should provide for y ppayment of contingent fee in form of lump sum and/or future periodic payments.

23

Deferred Attorney Fees contDeferred Attorney Fees cont…Cash + Promise of

Future Periodic Payments

Attorney DefendantSettlement Agreement

Future Periodic Payments

Settlement Agreementand Release

Cash

Liability to make Future

Periodic Payments

Future Periodic

P t

AssignmentInvestmentInvestment(s)

Payments

AssignmentCompany

InvestmentProvider

Cash

24

Legal and Tax HistoryLegal and Tax History

• Pre-Childs• Pre-Childs– TAMs 9134004, 9134005, 9134006– IRS said FMV of payment rights includible in

attorney’s current year taxattorney s current year tax

without opinion 89 F.3d 856, (11th Cir. 1996).• IRS has not formally acquiesced, Tax Court y q ,

bound by Childs in 11th Circuit, even so, Tax Court usually follows published guidance from another Circuit where no other published guidance existspublished guidance exists…

25

Legal History contLegal History cont.

Post-ChildsNo cases or rulings to our

knowledge since Childs

IRS has cited Childs favorablyRev. Rul. 2003-115, 2003-46 IRB 1052,Doc 2003-23359, 2003 TNT 209-15 - No constructive receipt where irrevocable electionconstructive receipt where irrevocable election and substantial limitations or restrictions

FSA 200151003 - Cites Childs, attorney has noconstructive receipt where settlement is entered into before attorney has unconditional right to receive fee PLR 200836019 - No constructivereceipt…employment settlement

26

Childs v. Commissioner• Facts

– Flows from a case where a house blew up b/c of propane gas with one person seriously injured and one death

– Plaintiff Lawyers agree to periodic payments for portion of legal feesPlaintiff Lawyers agree to periodic payments for portion of legal fees– Provided for in settlement agreement with assignment of liability to 3rd

party assignee– Assignment company purchased annuity to fund future payments– Lawyer(s) named annuitants of the annuities and estates named

beneficiaries– Annuity subject to rights of general creditor, however insurance

company guaranteed performance of the assignment company– Lawyers had no right to accelerate payments and no rights greater than

a general creditora general creditor

• Issue(s)– When are the attorney fees includible by the attorney

i hi t bl i ?in his taxable income?

• Holding– The Tax Court (affirmed by the 11th Circuit) held that( y )

the attorneys did not constructively receive the feesin the year the settlement documents were signed.

27

Childs v. Commissioner• Tax Court Holding(s):

1. HELD: The fair market values of Ps' rights to receive payments under the settlement agreements were not includable in income under sec. 83, I.R.C. in the year in which the settlement agreements were effected, since the promises to pay under the structured settlements were neither funded nor secured and thus did not meet the definition of property for purposes of sec.83.

2. HELD, FURTHER, the doctrine of constructive receiptis inapplicable, since Ps had no right to receive theattorney's fees prior to the time the agreementfixing a structured settlement was entered intofixing a structured settlement was entered into.

• 11th Circuit Holding:Affi d th T C t i d i i- Affirmed the Tax Court in a one page decision.

28

Technical Requirements of qDeferred Attorney Fee

• FORM is important with tax – do it right on the front end!

• No constructive receipt

• No IRC Section 409A

No economic benefit• No economic benefit

• Work with a highly g yqualified advisor

29

Tax Issues and/or Consequences to Attorney’s Client and Defendantto Attorney s Client and Defendant

• Client/Claimant/Plaintiff– IRC §104 case

• no taxation issues/consequences as proceeds are tax freeno taxation issues/consequences as proceeds are tax free

– Non IRC §104 case• Settlement proceeds taxable

– Structure can lower overall tax paid significantly• Attorney fees included in income of client, see

Commissioner v. Banks and Commissioner v. Banaitis, 175 S.Ct. 826; 2005 U.S. Lexis 1370 (2005)

• American Jobs Creation Act of 2004 P L 108-357American Jobs Creation Act of 2004, P.L. 108 357– Certain cases get above the line deduction, which

effectively nets out the attorney fees

» False Claims Act and Section 1862(b)(3)(A) of S i l S it A t dSocial Security Act, and

– Certain other cases do not get above the line

» A long list of laws that provide for employment claims

– Certain other cases do not get above the line deduction, but get itemized deduction subject to 2% floor (with no deduction for AMT purposes) – “gross” method 30

Tax Issues and/or Consequences to Attorney’s Client and Defendantto Attorney s Client and Defendant

• This can lead to bad tax result- see Spina v Forest Preserve District of Cook Countysee Spina v. Forest Preserve District of Cook County,

207 F. Supp.2d 764 (N.D. Ill. 2002) as reported in 2002 National Taxpayer Advocate Report to Congress at 166.

• See Adam Liptak, ‘‘Tax Bill Exceeds Award to Officerin Sex Bias Case,’’ The New York Times, Aug. 11, 2002, section 1, p. 18.Cynthia Spina v…– This is an illustrative case, this specific case

would differ after Jobs Act, however for non §104 cases that do not have Jobs Act protection, this would still be the bad tax resultwould still be the bad tax result

- Structuring attorney fees can help client byspreading out attorney fee “income” over a number of years

31

Tax Issues and/or Consequences to Attorney’s Client and Defendantto Attorney s Client and Defendant

• Defendant gets deduction, issue is when

• IRS Notice 2003-77 and Maxus Energy Corporation and gy pSubsidiaries v. United States, 31 F.3d 1135 (Fed. Cir. 1994).

– In Notice 2003-77, the Service cited Maxus Energy Corporation and Subsidiaries v. United States saying that a “taxpayer’s payment to a settlement fund effectivelytaxpayer s payment to a settlement fund effectively constitute[s] payment to the person to which the liability [is] owed [if] the claimants agree[ ] to look solely to the fund to satisfy their claims, and therefore, the taxpayer’s payment to the fund discharge[s] its liability to the claimant.” Qualified Settlement Fund (IRC Section 468B)Se e e u d ( C Sec o 68 )

– Payment by a defendant to an assignment company would be treated as a payment “to the person to which the liability is owed” under Treas. Reg. § 1.461-4(g)(1) if the payment to the assignment company extinguishes the

– Structured attorney fees typically (they should) involve a novation, therefore a defendant would be able to claim an immediate deduction upon making the lump

payment to the assignment company extinguishes the defendant’s liability to the claimant.

to claim an immediate deduction upon making the lump sum payment to the assignment company, just as if the defendant had instead paid that lump sum amount directly to the claimant

32

Tax Issues and/or Consequences to Attorney’s Client and Defendant

• Defendant’s Insurer get deduction

to Attorney s Client and Defendant

gwhen paid– Whether directly to plaintiff/claimant,

– To a QSF, or

– Structured Attorney Fee, orStructured Attorney Fee, or

– Structured Settlement

• See IRC Sections 831-832

33

Structured S ttl tSettlements

34

Why Talk About S S ?

• Must be completed at time of settlement

Structured Settlements?p

– After docs signed it is too late!

• Often offered by defense– Understand what is being offered– Resource to call to evaluate the structure

being offered

• Plaintiff/plaintiff attorney can and should have own structured settlement consultantsettlement consultant

• Understand Benefits

• Understand Limitations

35

The Settlement Industry• Approximately 600 full-time structured

settlement consultants nationwide

The Settlement Industry

• Most are primarily “defense” oriented– But, most also work with plaintiffs

• Plaintiff only brokers– Plaintiff has right to their own consultant

O l l li d lt t• Only properly licensed consultants can offer structured settlements

– Not unlicensed financial planners, brokers, etc.

• Structured settlements are specialized

• Trade Association: NationalTrade Association: National Structured Settlements Trade Association (www.nssta.org)

36

Structured Settlement

• The settlement of a claim or a lawsuit through cash payments th t d i t ll tthat are made on an installment or periodic basis

• Usually a mix of immediate cash and deferred lump sums and/or monthly payments

37

Structured Settlement Benefits• Eliminate the risk of mismanagement. According to one

recent study, approximately 90% spend all their settlement money within five years.

Structured Settlement Benefits

y y

• Provide tax advantages. Fixed annuity payments from a qualified structured settlement are tax-free to the annuitant under current IRS rules.

• Provide a steady, low-risk source of money.Structures eliminate the expense and worry of managing large sums.

Off ti th l

• Customized payments. Structures offer a

• Offer more money over time than a lump sum.Fixed annuity payments can continue for life – no matter how long the claimant lives.

p yconvenient way to meet the individual claimant’s needs and special circumstances.

• Maximize settlement benefits. In cases where the defendant has low insurance policywhere the defendant has low insurance policy limits, a structured settlement can often provide a more generous overall settlement.

38

Structured Settlement BenefitsTax-free• Structured Settlement funds are exempt from federal

d t t i t Y id th t b d

Structured Settlement Benefits

and state income taxes. You can avoid the tax burden that comes with investment earnings on a cash settlement. Over time, a structured settlement ensures significant tax savings and maximizes the value of the settlement proceeds.settlement proceeds.

No market risk• Exposure to market risks is eliminated along with the

potential for investment failures. The annuity provider absorbs any risk of market and interest rate fluctuationsabsorbs any risk of market and interest rate fluctuations, and the dollar amount of the claimant’s payments is guaranteed, year after year.

Money is available when the claimant needs it most• Annuity payments may be designed and timed to

meet the claimant’s needs now and decades from now. They are assured that funds will be there specifically for medical and educational expenses, for basic living requirements and for specializedfor basic living requirements, and for specialized healthcare needs that may arise in the future as a result of their injury.

39

Structured Settlement Benefits for MinorsSafety and Security• Brook-Hollow Financial only represents life insurance markets

Structured Settlement Benefits for Minors

y pthat have secured A++ or A+ ratings from the A.M. Best Company.

• Structured settlements are not subject to the claims of creditors.

• Structured settlements relieve the burden and expense of money management, investment decisions, and management fees.

• Structured settlements are protected by strict government regulations.

Flexible• The benefit payment streams can be designed to

meet the future financial needs of the minor.Examples include: funding a college education, lifetime guaranteed payments guaranteed lump sumlifetime guaranteed payments, guaranteed lump sum payments, and even future retirement planning.

40

Structured Settlement Benefits for MinorsEliminate the Risk of Mismanagement• Because benefits to be paid under a fixed annuity are calculated in

d th l i tiff h th it f k i th t t

Structured Settlement Benefits for Minors

advance, the plaintiffs have the security of knowing the exact amount and payment dates of their periodic payments. Structured settlements provide tax free payments. There is no tax due on the principal or earnings distributed to the plaintiff, or their beneficiaries. (IRC §104(a))

Additi l b fitAdditional benefits• Courts often insist on structures for minors because structures

guarantee the highest rate of return of any investment and the funds are set aside solely for the benefit of the minor; the structure cannot be invaded by unscrupulous individuals.be invaded by unscrupulous individuals.

• There is no need to post a bond or for annual reporting by the parent or guardian.

• It is virtually impossible for the minor to dissipate the settlement• It is virtually impossible for the minor to dissipate the settlement funds once they have attained the age of majority.

• The minor is still eligible for financial assistance in college.

• Structures provide an ongoing legacy from a parent to• Structures provide an ongoing legacy from a parent to their child.

41

Structured Settlements Are Also Useful When Dealing With Claimants Who Have Special NeedsDealing With Claimants Who Have Special Needs

• Significant, ongoing medical expenses;

• Rehabilitation or permanent care facility expenses;

• College tuition, retirement income, the down payment on a home or a mortgage payment, and;

• Replacement of monthly income, annual income or supplemental income.

• Workers compensation claims; and

• Personal injury, other than bodily injury.

42

Insurance Companies Offering p gStructured Settlements

Company Name A.M. Best Rating - SizeAll t t Lif I C A XV• Allstate Life Insurance Company A+ XV

• American General Life Insurance Company A XV• John Hancock Life Insurance Company A+ XV• Liberty Life Assurance Company of Boston A X• Metropolitan Life Insurance Company A+ XVp p y• New York Life Insurance Company A++ XV• Pacific Life and Annuity Company A+ XV• Prudential Insurance Company of America A+ XV• Symetra Life Insurance Company A XII

43

Structured Settlements Can Be Used In Tax-Free OR Taxable Recovery Cases

• Tax-free Cases– IRC Section 104IRC Section 104

• All payments ever received are free form federal income taxationtaxation

• Taxable Recovery Casesy– Payments are tax-deferred

44

Involve Structured Settlement Consultant Early

Minimal Basic Data Needed

• Case Profile Fact SheetCase Profile Fact Sheet

• Medical reports –admission/discharge summariesadmission/discharge summaries

• Plaintiff’s life care planp

• Economist’s report

45

Brian S. Michaels, Esq., General CounselDirect: 480 463 1597Direct: 480-463-1597

![TAXING STRUCTURED SETTLEMENTS - Boston Collegevhost4.bc.edu/content/dam/files/schools/law/bclawreview/pdf/51_1/... · 2010] Taxing Structured Settlements 41 are correct in their interpretation](https://static.documents.pub/doc/80x56/5b4389e17f8b9a80388bfa40/taxing-structured-settlements-boston-2010-taxing-structured-settlements-41.jpg)