Structuring Private Equity Co-Investments and Club Deals: Risks and Opportunities for Sponsors and Investors Choosing the Right Investment Structure, Negotiating Key Deal Terms, and Navigating Tax and Regulatory Ramifications Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. WEDNESDAY, APRIL 15, 2015 Presenting a live 90-minute webinar with interactive Q&A C. Spencer Johnson, III, Partner, King & Spalding, Atlanta Steven Huttler, Partner, Sadis & Goldberg, New York Alex Gelinas, Partner, Sadis & Goldberg, New York

Transcript

Structuring Private Equity Co-Investments and Club Deals: Risks and Opportunities for Sponsors and Investors Choosing the Right Investment Structure, Negotiating Key Deal Terms, and Navigating Tax and Regulatory Ramifications

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

For CLE purposes, please let us know how many people are listening at your

location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of

attendees at your location

• Click the SEND button beside the box

If you have purchased Strafford CLE processing services, you must confirm your

participation by completing and submitting an Official Record of Attendance (CLE

Form).

You may obtain your CLE form by going to the program page and selecting the

appropriate form in the PROGRAM MATERIALS box at the top right corner.

If you'd like to purchase CLE credit processing, it is available for a fee. For

additional information about CLE credit processing, go to our website or call us at

1-800-926-7926 ext. 35.

FOR LIVE EVENT ONLY

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Structuring Private Equity

Co-Investments and Club Deals:

Risks and Opportunities for

Sponsors and Investors

Choosing the Right Investment Structure, Negotiating Key

Deal Terms, and Navigating Tax and Regulatory Ramifications

April 15, 2015

Steven Huttler, Partner

Sadis & Goldberg LLP

Steven Huttler is a partner in the firm’s Financial Services and Corporate Groups. Mr. Huttler has extensive experience in corporate, finance, investment fund and securities matters, including the representation of U.S. and foreign investment funds, underwriters, and private clients in various registered public and private offerings of debt and equity securities totaling in excess of $10 billion.

As part of his investment fund practice, Mr. Huttler has served as corporate counsel to many private investment funds and partnerships based in or domiciled in the United States and in international and offshore jurisdictions such as the Cayman Islands, Bermuda, the British Virgin Islands, Ireland, Luxembourg, Isle of Man, Jersey, Guernsey, Cyprus, Mauritius, United Kingdom, Austria, Russia, India and Gibraltar. Mr. Huttler's legal practice has exposed him to diverse fund clients with an exceptionally wide range of investment programs and structures, including large mutual funds and hedge fund complexes, private equity firms, real estate partnerships and funds, venture capital funds and funds focused on specialty finance assets. He has also counseled small start-up hedge funds and financial industry entrepreneurs. His practice has included structuring and establishing start-up funds and managed accounts, and structuring investment funds to benefit from U.S. double taxation treaties. He has advised management companies and fund managers on compensation structures, restructured and reorganized funds, structured, negotiated and documented fund trades, negotiated seed, joint venture and start up agreements, and advised on a range of sophisticated transactions. He has also represented financial services providers, such as brokerage firms (including proprietary trading broker-dealers), fund administration firms and third party marketing firms in structuring their operations, reorganizations to achieve tax benefits, advising on disputes with clients, and in the development of forms for their pension, investment, trading, administration and other services to investment funds, equity, debt and option traders and other clients.

6

Alex Gelinas, Partner

Sadis & Goldberg LLP Alex Gelinas is a partner in the firm’s Tax Group. Mr. Gelinas focuses his practice on providing tax advice to investment managers of hedge funds, private equity funds and other investment funds on all aspects of their businesses, including management entity and fund formation, partnership taxation issues, compensation arrangements and ongoing investment activities and transactions. Mr. Gelinas also provides tax advice to U.S. pension funds, sovereign wealth funds and other U.S. and foreign institutional investors in connection with their investments in private equity funds, hedge funds and U.S. joint ventures. He also has extensive experience in providing tax planning advice to high-net-worth individuals and families.

and corporate finance transactions. Mr. Johnson also has significant experience with mergers and acquisition

transactions. He routinely counsels asset managers, private equity sponsors, investment banks and operating

companies in connection with these matters. His practice encompasses compliance issues involving relevant

regulatory considerations, including the Securities Act of 1933, the Investment Company Act of 1940, the Investment

Advisers Act of 1940 and today’s headline regulatory considerations, such as Dodd-Frank, the Volcker Rule, the

JOBS Act, general solicitation considerations in unregistered securities offerings and the EU Alternative Investment

Fund Managers’ Directive (AIFMD). Mr. Johnson’s practice spans a number of industries, however, the primary

focus of his practice is concentrated in real estate capital markets (including real estate investment trusts or REITs),

financial technology and payments companies, and energy private capital.

8

Overview of Presentation

I. Co-investment structures

II. Deal documents and key deal terms

III. Current trends in private equity co-investments

IV. Regulatory hurdles: broker, dealer and investment advisor regulation

V. Tax and ERISA regulatory considerations for sponsors and investors

9

Co-Investments & Club Deals

• Co-Investment ― An equity co-investment (or co-investment) is a minority

investment, made directly into an operating company, alongside a financial sponsor or other private equity investor, in a leveraged buyout, recapitalization, growth capital or other transaction

• Club Deal ― A private equity buyout or the assumption of a controlling

interest in a company that involves several different private equity firms or institutional investors

10

Co-Investment Recapitalization Structure

Fund

PoCo

Third

Party

LP

= New Investment Capital

= Existing Investments

11

Club Deal Structure

PoCo

Sponsor or

Financial

Institution

Sponsor or

Financial

Institution

Sponsor or

Financial

Institution

Target

Company

12

Capital Stack 13

Who’s Investing to bridge the gap?

• Pension Funds

― ERISA

― Non-ERISA

• Sovereign Wealth Funds

• Insurance Companies

• Private Equity Funds

• US Tax-Exempts

• US Taxable Investors and High Net Worth Platforms

14

Drivers - Private Equity Fund Structure

PE

Fund

Limited Partners

Management

Company/

Sponsor

PoCo PoCo PoCo PoCo

General

Partner

15

Drivers - Concentration

• Single Investment

16

Drivers – Really Big Deals

• How much is too much?

17

Drivers – Investment Focus

• Types of Investments

18

Drivers – Deal Access

• Deal flow

• Premium in today’s market

19

Drivers – Investor Allocations

• Help me, help you

20

Drivers – Flexibility

• Maintain investment control

• Unwilling to commit to PE funds on a long-term basis

21

Economics

How do Fund Sponsors make money?

• Management Fees

• Transaction Fees

• Carried Interest

• Other fees

Certain compensation structures provide favorable tax treatment in the U.S.

22

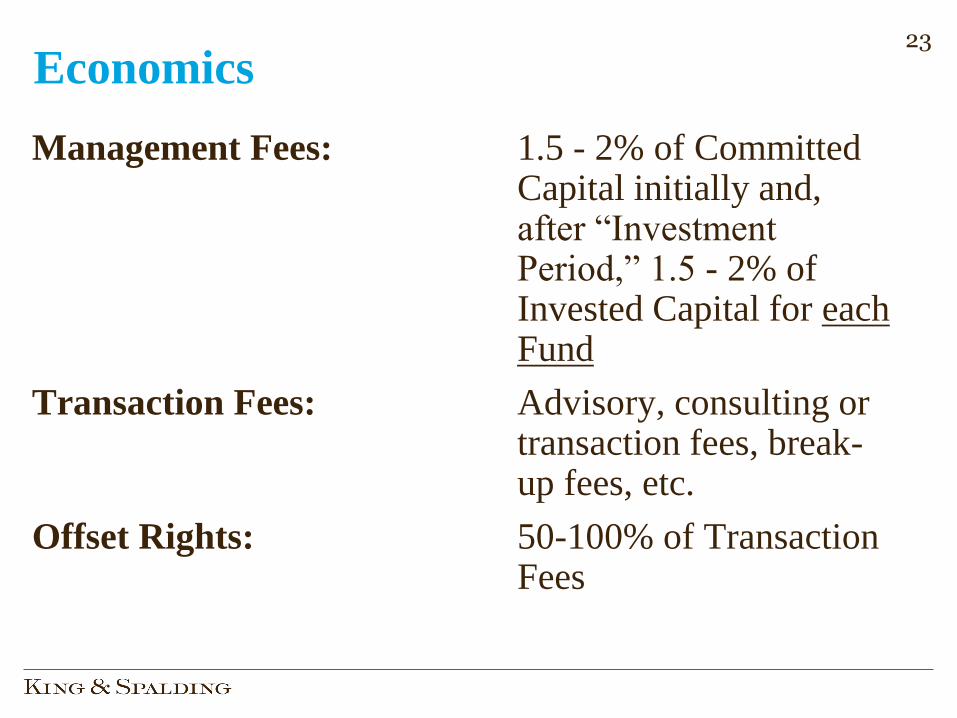

Economics

Management Fees: 1.5 - 2% of Committed Capital initially and, after “Investment Period,” 1.5 - 2% of Invested Capital for each Fund

Transaction Fees: Advisory, consulting or transaction fees, break-up fees, etc.

Offset Rights: 50-100% of Transaction Fees

23

Deal Documents

• Organizational Documents for Investment Vehicle

― Articles/bylaws

― Partnership agreement/LLC agreement

• Purchase Agreement

― Related to the purchase of the relevant interest

• Others

― Notes

― Guarantees

― Warrants

24

Deal Documents

• Organizational Documents

• Serve as the road map for the portfolio company/joint venture

• Economics

• Governance

• Capital call mechanics

• Exits

25

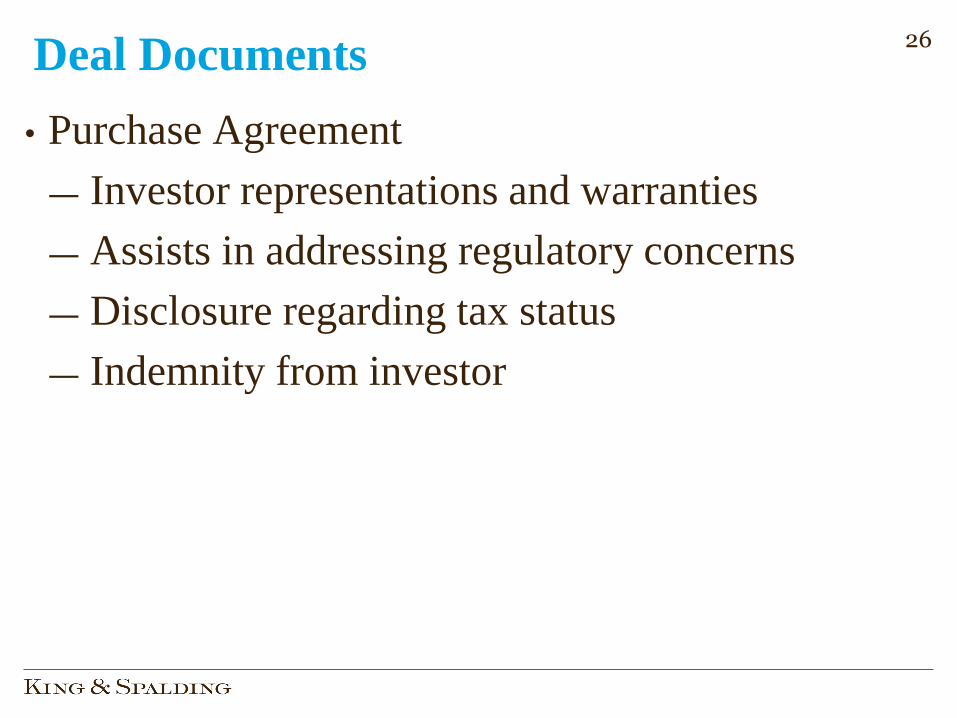

Deal Documents

• Purchase Agreement

― Investor representations and warranties

― Assists in addressing regulatory concerns

― Disclosure regarding tax status

― Indemnity from investor

26

Deal Documents

• Others

• Notes

• Convertible/exchangeable

• Guarantees

• Credit parties

• Warrant coverage

• Foot faults can result in failure to exercise

27

Trends

• Pipeline access is valuable

― Investors are negotiating for co-investment rights in connection with their fund investments

― Supply/Demand imbalance for capital versus transactions

― Sponsor favorable terms in co-investments

― Fees

― Carry

28

Trends

• Position in the capital stack

― Risk involved in the transaction

― Demand for the deal

― Preferred Equity

― Returning a stated amount to the investor

― Often coupled with warrant coverage

29

Trends

• Industries

― No bright lines for large transactions involving healthy companies

― Oil & Gas

― Increasing activity for preferred equity/mezzanine debt transactions

― Largely a function of temporary depression in market prices

― Real Estate

― What is a real estate asset?

― Large allocations driving new transactions

30

Regulatory hurdles: broker, dealer and

investment advisor regulation

31

Frequently Overlooked Regulatory Considerations

• Broker-Dealer Regulation

• Investment Adviser Regulation

32

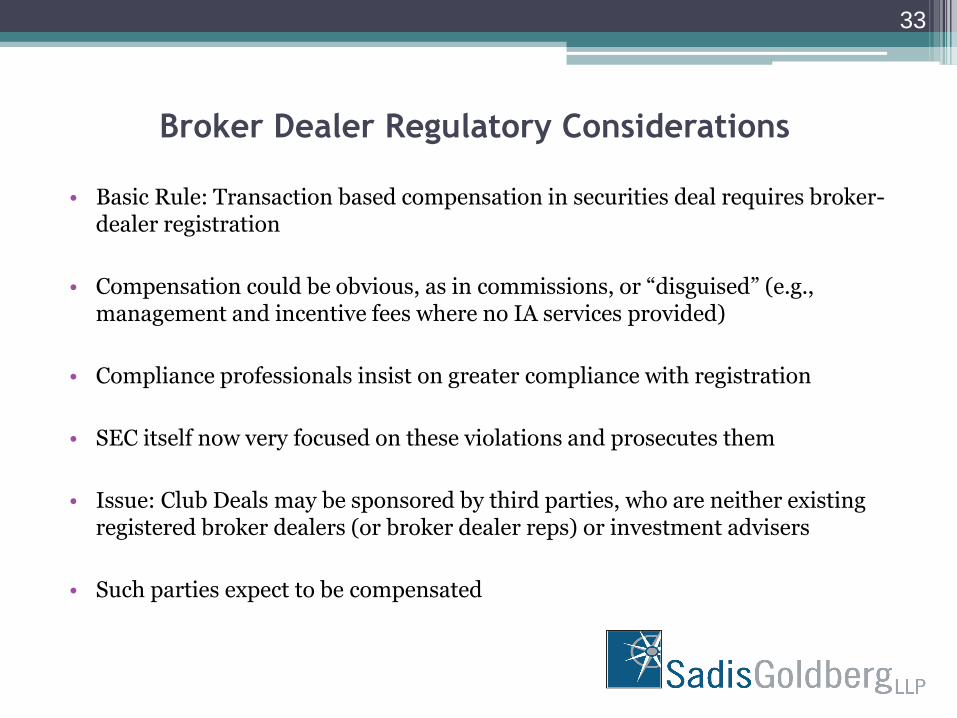

Broker Dealer Regulatory Considerations

• Basic Rule: Transaction based compensation in securities deal requires broker-dealer registration

• Compensation could be obvious, as in commissions, or “disguised” (e.g., management and incentive fees where no IA services provided)

• Compliance professionals insist on greater compliance with registration

• SEC itself now very focused on these violations and prosecutes them

• Issue: Club Deals may be sponsored by third parties, who are neither existing registered broker dealers (or broker dealer reps) or investment advisers

• Such parties expect to be compensated

33

Investment Adviser Considerations

• Many sponsors, when made aware of the broker dealer regulatory considerations, and the difficulty of meeting requirements, often turn quickly to alternatives

• Most frequent alternative: sponsor acting as investment adviser and collecting management and/or incentive fees

• However, the SEC would regard a sponsor who does not provide any investment advice as a disguised broker dealer, and the fees as disguised commissions

34

Investment Company Act

• Need for exemption under ICA

• Often overlooked because vehicle is not a “blind pool”(conventionally thought of as a fund)

• Classic Exemptions of 3(c)(1), 3(c)(5), 3(c)(7) would be most relevant

• Increased possibility of availability of 3(c)(5)

• Such increased availability may even serve as a rationale for using the whole SPA/structure

35

Tax Considerations in Structuring Private Equity Co-

Investment Transactions

The Typical Investor Participants in Private Equity Co-Investments Include:

1. US TAX-EXEMPT INVESTORS THAT ARE SUBJECT TO TAX ON UNRELATED TRADE OR BUSINESS INCOME (“UBTI”)

A. US “Fortune 500” Pension Funds

B. US University and College Endowment Funds

C. Other US Tax-Exempt Entities (Foundations, Charitable Organizations)

D. Self-Directed Retirement Plans and Individual Retirement Accounts of High Net Worth Individuals

Such tax-exempt investors would realize UBTI if they make any debt-financed investments (i.e., investments using borrowed funds made directly or by a partnership in which they are partners (including limited partners)). In addition, such tax-exempt investors would realize UBTI if they own equity interests in partnerships that are engaged in a trade or business in the US or anywhere in the world.

PREFERRED FORM OF INVESTMENT: If there is a risk of UBTI, such Tax-exempt entities typically invest through “blocker corporations “organized in “zero tax” jurisdictions like the Cayman Islands or British Virgin Islands.

36

Tax Considerations in Structuring Private Equity Co-

Investment Transactions (cont.)

2. US TAX-EXEMPT INVESTORS THAT ARE NOT SUBJECT TO THE UBTI RULES

A. Retirement Plans for State and Local Government Employees (e.g., CALPRS, CALSTRS, New York State and Local Retirement System, Florida State Employees Retirement Plan, Etc.)

PREFERRED FORM OF INVESTMENT: Such governmental employee plans are typically exempt under section 115 of the Internal Revenue Code (as governmental entities) rather than Code section 501, and are thus exempt from UBTI. Therefore, they would typically invest through pass-through entities.

2. US TAXABLE INSTITUTIONAL INVESTORS

A. Publicly Traded “C” Corporations

B. Insurance Companies

C. Private “C” Corporations

37

38

Investment Company Act

Need for exemption under ICA

Often overlooked because vehicle is not a “blind pool”(conventionally thought of as a fund)

Classic Exemptions of 3(c)(1), 3(c)(5), 3(c)(7) would be most relevant

Increased possibility of availability of 3(c)(5)

Such increased availability may even serve as a rationale for using the whole SPA/structure

Tax Considerations in Structuring Private Equity Co-

Investment Transactions (cont.)

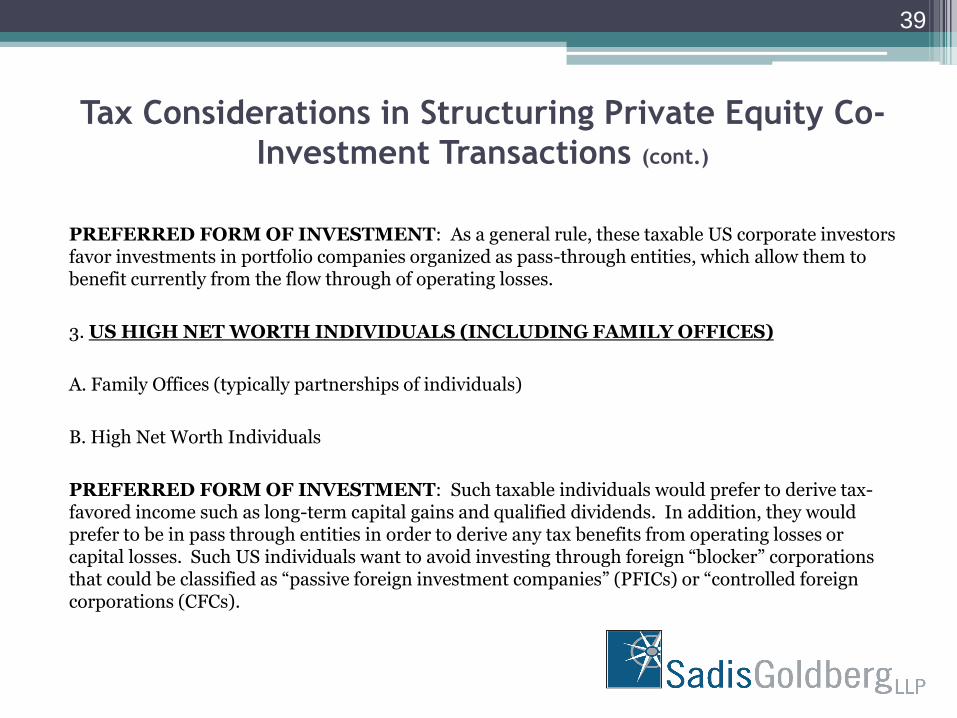

PREFERRED FORM OF INVESTMENT: As a general rule, these taxable US corporate investors favor investments in portfolio companies organized as pass-through entities, which allow them to benefit currently from the flow through of operating losses.

3. US HIGH NET WORTH INDIVIDUALS (INCLUDING FAMILY OFFICES)

A. Family Offices (typically partnerships of individuals)

B. High Net Worth Individuals

PREFERRED FORM OF INVESTMENT: Such taxable individuals would prefer to derive tax-favored income such as long-term capital gains and qualified dividends. In addition, they would prefer to be in pass through entities in order to derive any tax benefits from operating losses or capital losses. Such US individuals want to avoid investing through foreign “blocker” corporations that could be classified as “passive foreign investment companies” (PFICs) or “controlled foreign corporations (CFCs).

39

Tax Considerations in Structuring Private Equity Co-

Investment Transactions (cont.)

4. FOREIGN TAXABLE INVESTORS

A. Foreign Corporations

B. Foreign High Net Worth Individuals and Family Offices

Non-US Persons (including foreign corporations) are generally not subject US income tax on capital gains derived from investments in US securities but would be subject to US income tax on any income that is “effectively connected” with a US trade or business (“ECI”), including their share of ECI derived by a partnership in which they are a partner (including a limited partner). Thus, if the US portfolio company is organized as a partnership and is engaged in a US business, such foreign investors typically avoid ECI by investing through foreign blocker corporations organized in “zero-tax” jurisdictions.

40

Tax Considerations in Structuring Private Equity Co-

Investment Transactions (cont.)

US Withholding Taxes: The United States imposes a 30 percent withholding tax on US-source dividend and certain types of interest income (other than “portfolio interest”). US tax treaties with foreign jurisdictions in which the foreign investor may be residents typically reduce the US withholding tax on dividends to 15 percent and interest income to zero. However, the blocker corporations organized in “zero tax” jurisdictions are not eligible for the benefits of any US tax treaties

PREFERRED FORM OF INVESTMENT: Foreign taxable individuals typically invest through a blocker corporation. In addition to avoiding the ECI exposure, such individuals would also be protected from US estate tax exposure by owning the US investment through a foreign corporation.

41

Tax Considerations in Structuring Private Equity Co-

Investment Transactions (cont.)

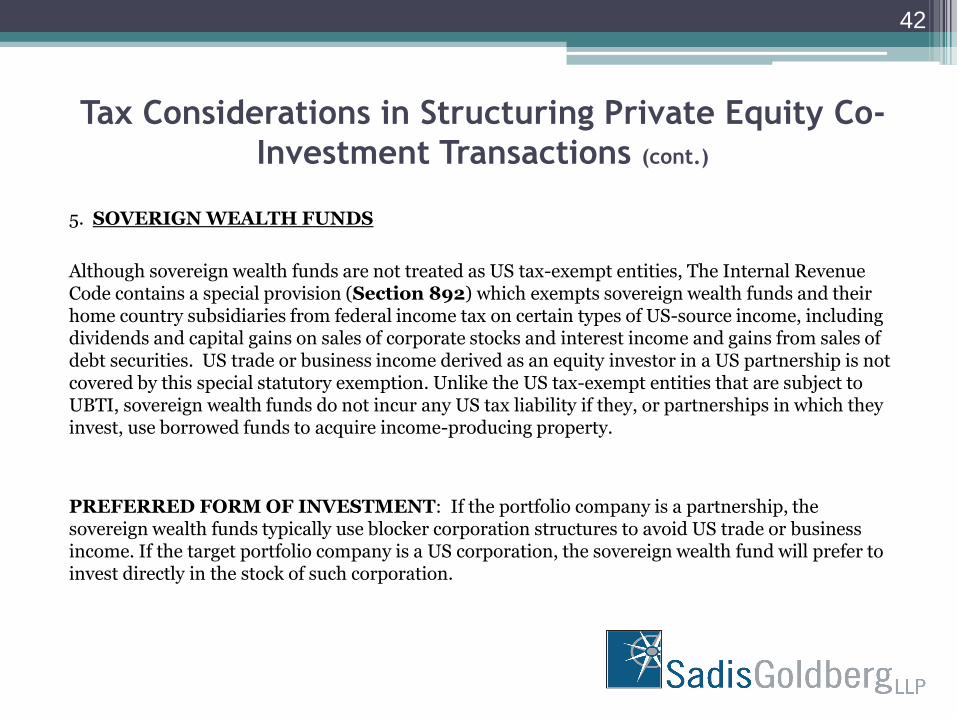

5. SOVERIGN WEALTH FUNDS

Although sovereign wealth funds are not treated as US tax-exempt entities, The Internal Revenue Code contains a special provision (Section 892) which exempts sovereign wealth funds and their home country subsidiaries from federal income tax on certain types of US-source income, including dividends and capital gains on sales of corporate stocks and interest income and gains from sales of debt securities. US trade or business income derived as an equity investor in a US partnership is not covered by this special statutory exemption. Unlike the US tax-exempt entities that are subject to UBTI, sovereign wealth funds do not incur any US tax liability if they, or partnerships in which they invest, use borrowed funds to acquire income-producing property.

PREFERRED FORM OF INVESTMENT: If the portfolio company is a partnership, the sovereign wealth funds typically use blocker corporation structures to avoid US trade or business income. If the target portfolio company is a US corporation, the sovereign wealth fund will prefer to invest directly in the stock of such corporation.

42

Diagrams of Co-Investment Structures

Direct Co-Investment in US C-Corp. Portfolio Company. In this structure, co-investors invest on a side-by-side basis with the fund directly in the portfolio company.

43

Portfolio Company (C-corp)

Fund, LP

Fund’s General Partner

All Fund Investors

Direct Co-Investors

LPs GP

Shareholder Shareholder

Diagrams of Co-Investment Structures Direct Co-Investment in foreign Holding Corporation and Pass-Through Portfolio Company. In this structure, co-investors invest on a side-by-side basis with the fund directly in the c-corp. holding company. In addition, certain co-investors (such as a fund operating partner) have a direct co-investment in the portfolio company, which is a pass-through entity (i.e., LLC).

44

Holding Company (C-corp)

Fund, LP

Fund’s General Partner

All Fund Investors

Direct Co-Investors

(Blocked)

LPs

GP

Shareholder Shareholder

Member

Direct Co-Investors (Unblocked)

Member

Portfolio Company,

LLC

Other original equity investors

ERISA Considerations Relating to Private Equity

Co-Investment Transactions

1. Plan Assets Issues; Fiduciary Status and Prohibited Transaction Issues

If the assets of an entity (e.g., a corporation, partnership or trust) are treated as plan assets of a benefit plan investor that owns an equity interest in such entity, the parties having management authority over the assets of such entity would be treated as fiduciaries under ERISA with respect to such plan investors. In addition, transactions entered into by such plan asset entities would be subject to ERISA scrutiny including complex prohibited transaction rules.

A. General Rules on Plan Assets Status

Under the ERISA plan assets regulations, the assets of an entity in which a plan has an equity interest will not be treated as plan assets if the equity interests are(1) publicly traded securities or (2) a security issued by an investment company registered under the Investment Company Act of 1940.

45

ERISA Considerations Relating to Private Equity

Co-Investment Transactions (cont.)

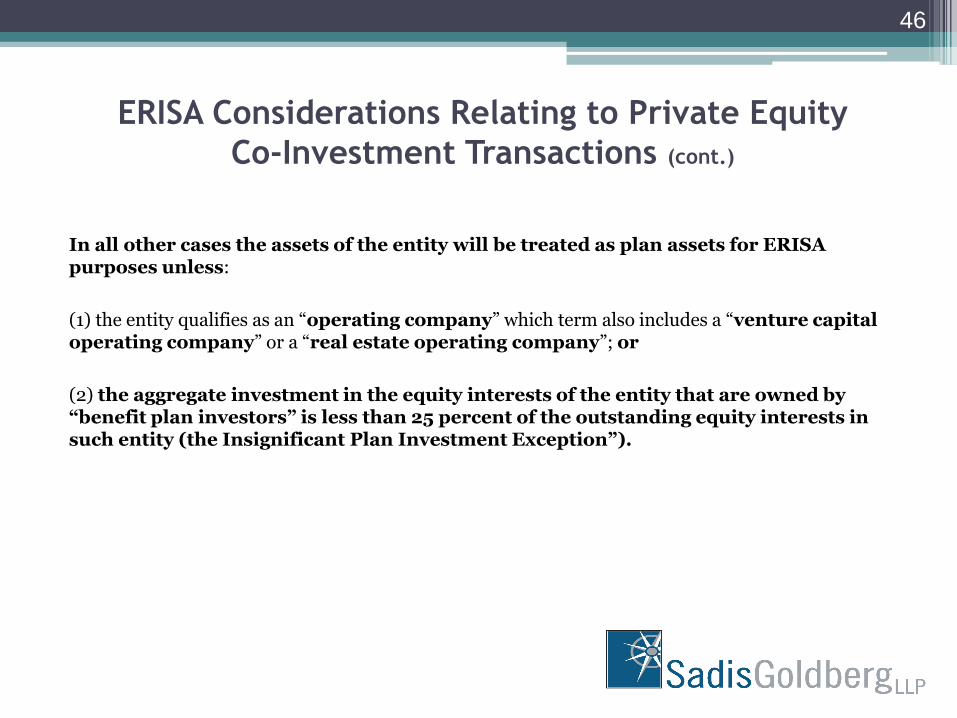

In all other cases the assets of the entity will be treated as plan assets for ERISA purposes unless:

(1) the entity qualifies as an “operating company” which term also includes a “venture capital operating company” or a “real estate operating company”; or

(2) the aggregate investment in the equity interests of the entity that are owned by “benefit plan investors” is less than 25 percent of the outstanding equity interests in such entity (the Insignificant Plan Investment Exception”).

46

ERISA Considerations Relating to Private Equity

Co-Investment Transactions (cont.)

B. Operating Company Definition

An operating company is defined as an entity that is “primarily engaged, directly or through a majority owned subsidiary or subsidiaries, in the production or sale of a product or service other than the investment of capital.”

(1) Start-up Ventures and Companies Engaged Solely in Research and Development May not Qualify under this Definition.

(2) The Venture Capital Operating Company (“VCOC”) and Real Estate Operating Company (“REOC”) Exemptions Were Added Later.

47

ERISA Considerations Relating to Private Equity

Co-Investment Transactions (cont.)

VCOC Definition

To qualify as a VCOC, the entity must satisfy two requirements: First, at least 50% of the entity’s assets (at cost) must be invested in “venture capital investments” or “derivative investments” as defined. Second, the entity must obtain and exercise “management rights” with respect to at least one of its operating company investments. The term “venture capital investment” is defined as an investment in an “operating company” in which the investing entity has obtained management rights.

REOC Definition

The REOC definition is similar to the VCOC definition. In order to be a REOC, the entity must: (1) have at least 50 percent of its assets (valued at cost) “invested in real estate that is managed or developed and with respect to which such entity has obtained the right to substantially participate directly in the management or development activities”; and (2) be directly engaged in real estate management or development activities.

48

49

If you have questions for Sadis Goldberg, please contact: