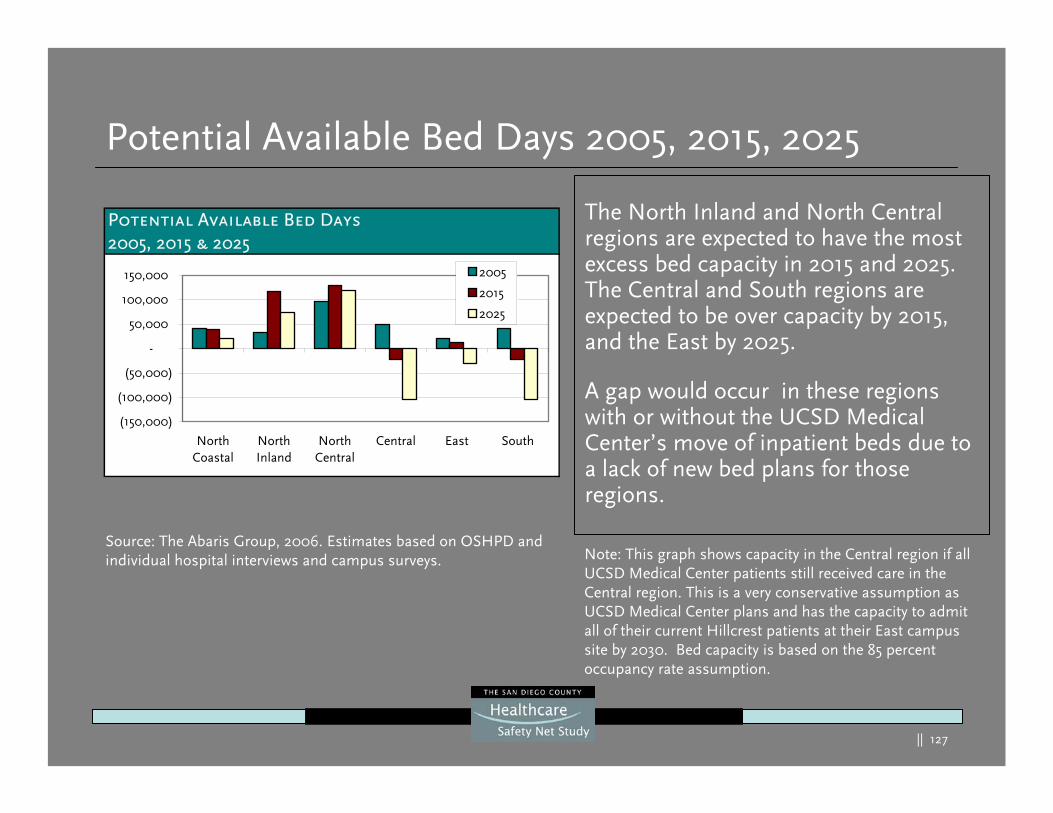

254

Study Core Report September 18, 2006

Study Core ReportSeptember 18, 2006

|| 2

Table of Contents Executive Summary……………………………….3 Capacity Forecasts……………………………80 Conclusions……………………………………166

Study Scope…………………………………………9 Methodology/Summary………………………81 Recommendations……………………………176

Safety Net Snap Shot………………………10 Community Clinics……………………………83 Appendix……………………………………………186

Current Demand………………………………29 Hospitals…………………………………………84 Methodology……………………………………187

Community Clinics……………………………32 ED Treatment Stations………………………88 Principles for the Safety Net

Hospital Utilization…………………………34 Trauma Centers………………………………91 Coordination Structure………………………191

ED Utilization…………………………… ……38 Physician/Nurse Supply……………………92 Best Practice Communities………………194

Trauma……………………………………………40 Demand Capacity Forecast UCSDMC Additional Findings……………197

County Comparisons…………………………42 Qualifiers…………………………………………96 San Diego IT Best Practice…………………207

Current Capacity………………………………47 Forecasted Payer Sources………………100 Capacity Challenges for Major

Map of Hospitals/Clinics…………………50 Gap Analysis…………………………………...109 Disasters…………………………………………210

Community Clinics………………………………51 What If?...........................................…...110 Safety Net Nationally & Statewide………218

Hospital Beds……………………………………52 Potential Hospital Closures……………...112 Immigrant Healthcare Use………………234

ED Treatment Stations…………………………57 Bed Gaps…………………………………...115 Future Trends for Healthcare…………..237

County Comparisons…………………………59 ED Treatment Station Gaps………...116

Diversion…………………………………………61 UCSDMC Inpatient Bed Move……………117

Physician/Nurse Supply……………………63 Medicare/Medi-Cal/Spending

Demand Forecasts………………………………71 Gaps…………………………………………………128

Methodology/Summary……………………72 Input From Stakeholders &

Community Clinics……………………………74 Consumers……………………………………….134

Hospital Discharges………………………….75 Characteristics of a Strong

ED Visits…………………………………………77 Healthcare Safety Net……………………142Trauma Admissions…………………………79 SWOT Analysis…………………………………148

|| 3

Executive Summary

|| 4

Executive Summary Study Overview

The San Diego County Healthcare Safety Net Study was jointly funded by The California Endowment and the County of San Diego

The study’s focus was to examine the long-term needs of the region’s healthcare safety net

As a result of this process, an estimate of the service and funding needs and gaps of the healthcare safety net, as well as the strengths, opportunities, weaknesses, and threats of meeting those needs, was developed

The Healthcare Safety Net in San Diego CountySan Diego County has an extensive network of community clinics, 19 acute care hospitals with emergency departments (EDs), and 6 trauma centers that serve the safety net

The number of uninsured and underinsured residents in San Diego County is likely to grow with some variation by region

|| 5

Executive Summary Current Demand on the Safety Net

Demand on the safety net providers has increased over the past 10 years. The number of community clinic visits, hospital discharges and ED visits have all increased steadily

While the total number of ED visits and hospital discharges has only grown modestly, the number of ED and hospital inpatient visits per hospital has increased more rapidly. Trauma center utilization (the number of trauma patient admissions per 1,000 population) has also increased at a steady rate

Current CapacityThe use of existing hospital beds has risen, which is also evidenced by the increasing number of discharges per bed and bed occupancy rate

The number of community clinics and ED stations have increased. San Diego County has the most community clinics per 100,000 residents in the state and a moderate number of ED visits per station

The actual number of physicians in the community is consistent with need but not all these physicians are available or will treat safety net patients. Nursing gaps do exist

|| 6

Executive Summary Future Demand on the Safety Net

San Diego’s population is expected to grow from 3 million to 3.7 million by 2025

Hospital discharges, community clinic visits, trauma admissions, and demand for physicians will all grow faster than the population. ED visits are projected to grow at a slightly more modest rate given San Diego County’s relatively low ED utilization rate

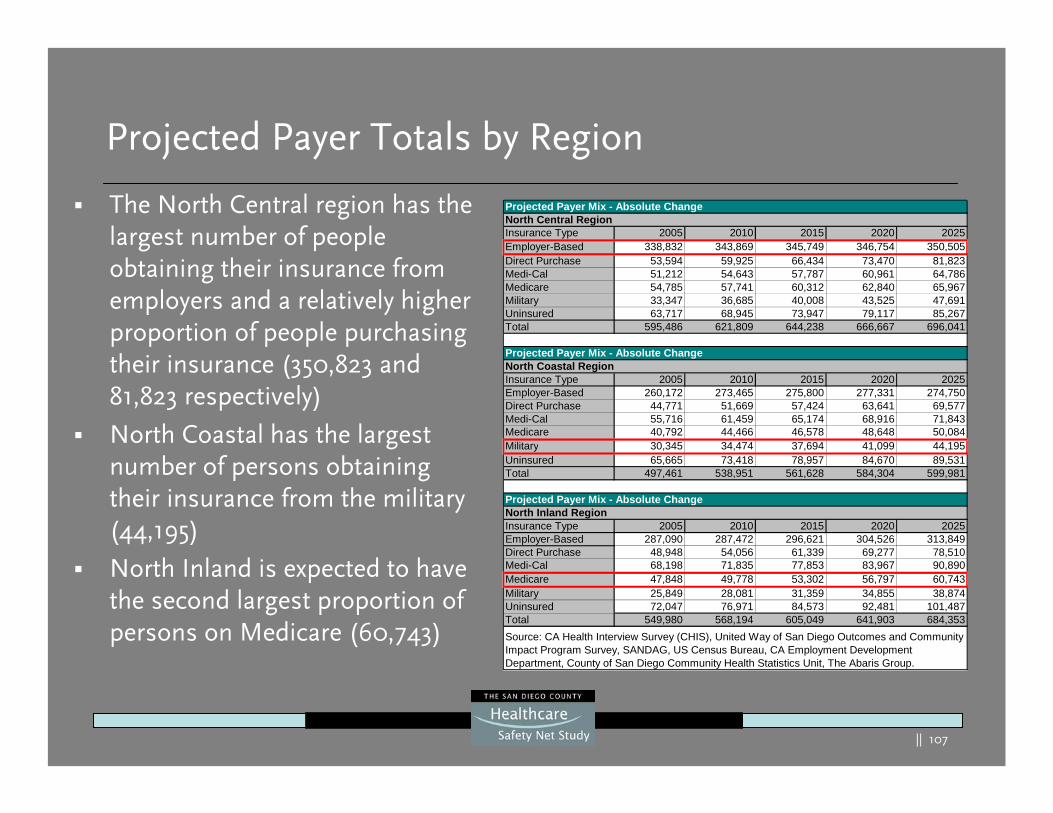

Regionally, the North Central region will see the greatest increase in discharges and ED visits growth, as this region has historically and will continue to have the most hospital inpatient capacity

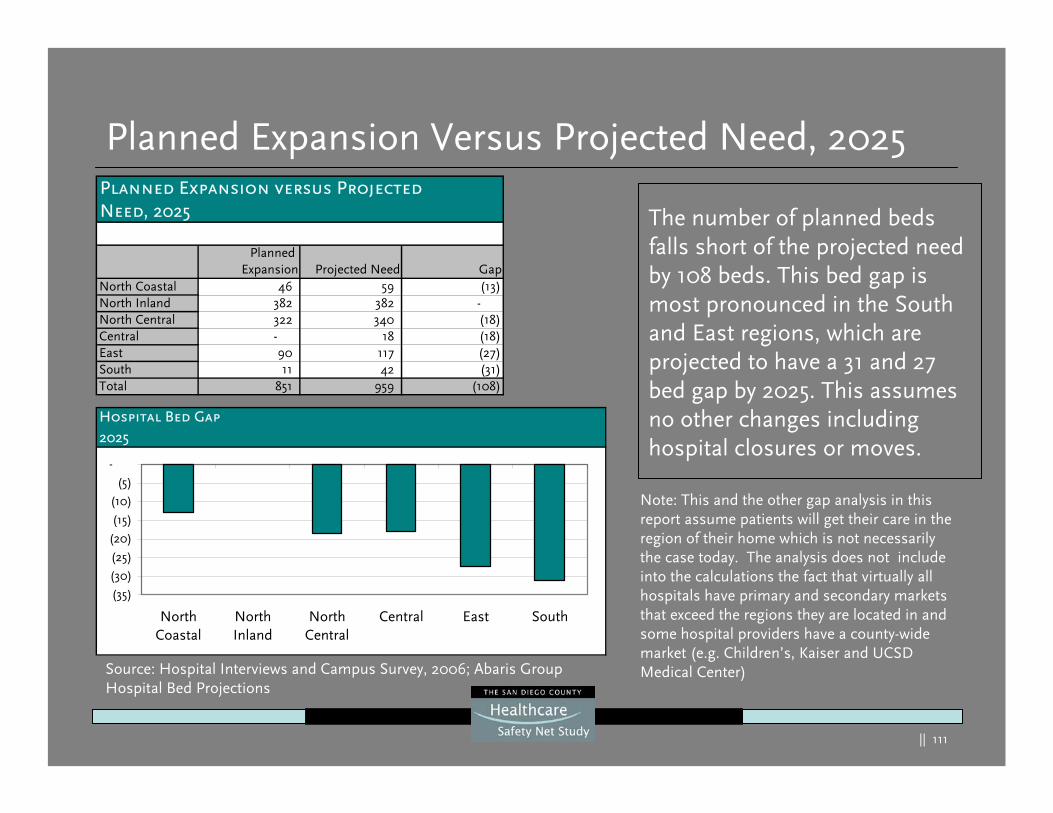

Future CapacityHospital expansion plans call for 801 beds by 2025, while the study projected the actual number of needed beds based on demand at 959

Considering historical growth in visits, the number of clinics in the community is expected to grow

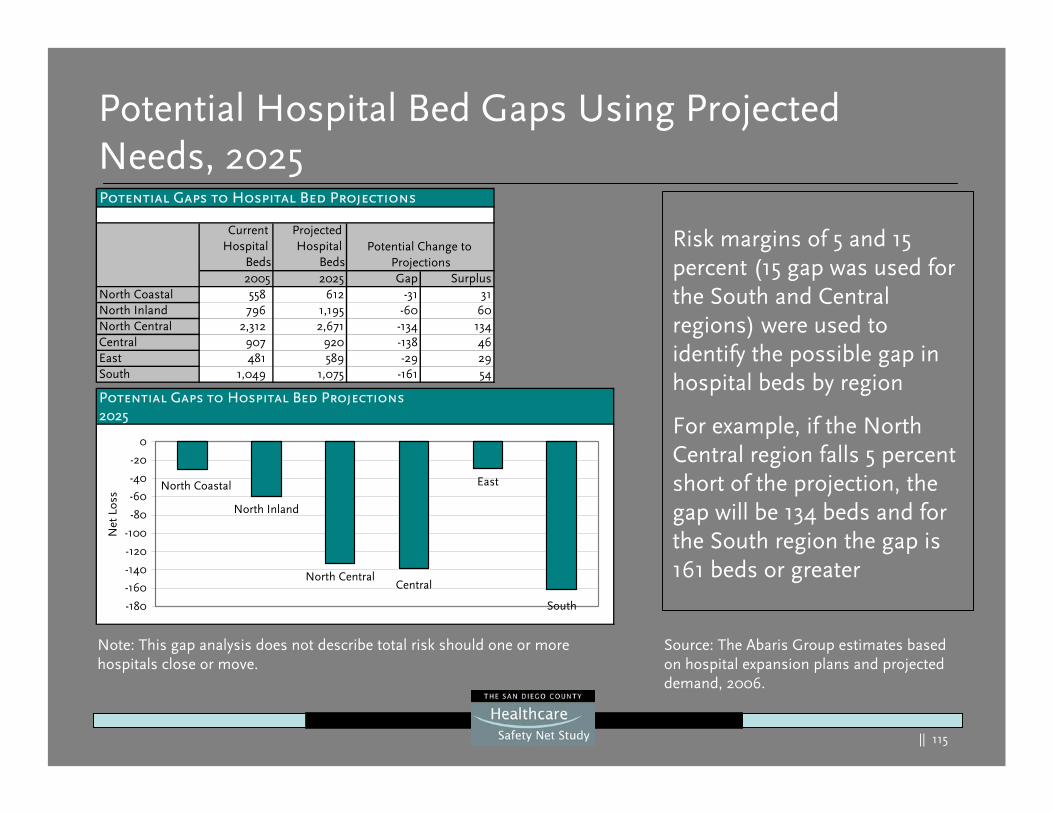

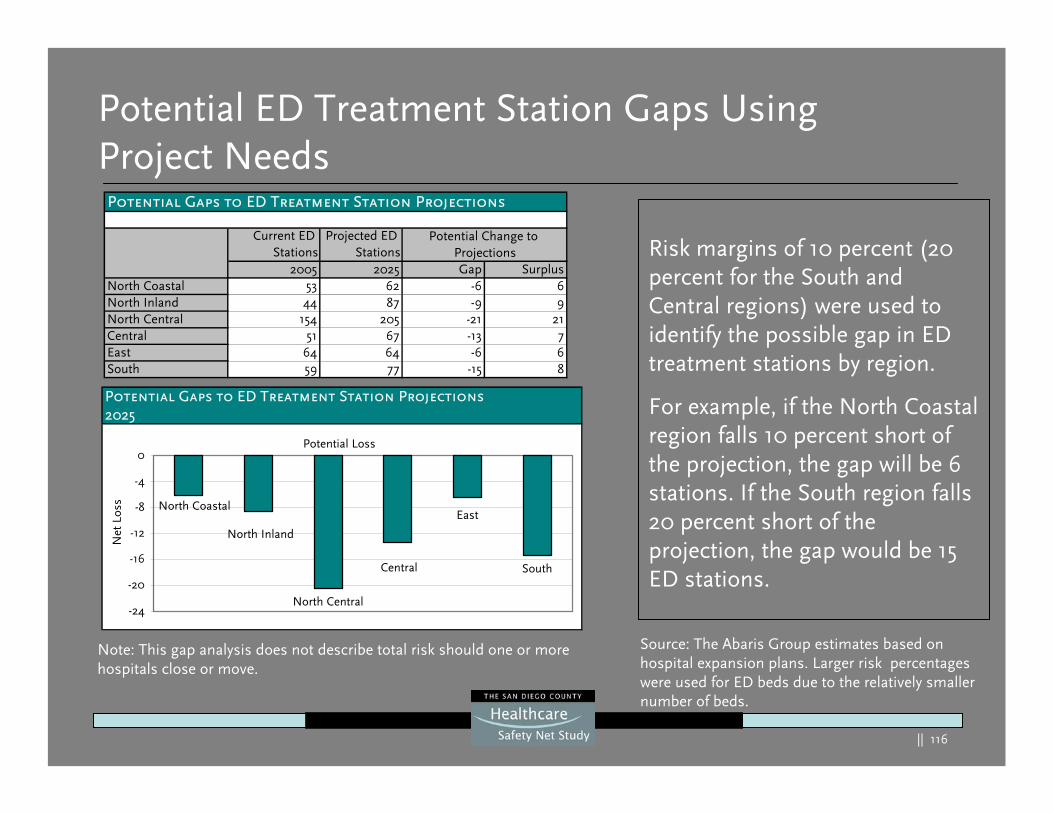

Gaps in inpatient beds and ED treatment beds were forecasted for some regions

|| 7

Executive Summary ConclusionsSeven conclusions were developed as a result of the analysis. They are, in summary:

1) San Diego County has taken a major step with the potential to rethink the delivery of healthcare

2) The community benefits from a range of resources that responds to or addresses many of the healthcare needs of the poor

3) The current capacity challenges provides an opportunity to rethink the healthcare safety net

4) UCSD Medical Center’s announced inpatient move will impact some patients and their families. However, the impact is expected to be minimized by UCSDMC’s plans to leave outpatient capacity at Hillcrest and there will be sufficient inpatient capacity attheir East campus

5) The healthcare safety net lacks a lead agency, seamless coordination and an integrated delivery system

6) This study has the potential to bolster and strengthen the safety net

7) The largest threat to the healthcare safety net in San Diego County is the potential failure to address the conclusions of this report

|| 8

Executive Summary Recommendations

The key recommendations of the report are outlined in summary below

San Diego County stakeholders should:

Develop a collaborative countywide coordination and oversight structure that uses a public/private partnership model

Explore a variety of methods to leverage and enhance funding sources for the safety net

Re-engineer and close the key access gaps identified in this report

Implement system reforms designed to improve coordination, strategic planning and best practices

|| 9Draft. Work In Progress.

Study Scope

Conduct a long-range (20 year) assessment of San Diego

County’s healthcare safety net needs including:

Hospital inpatient & outpatient

Emergency & trauma

Primary & specialty care

Physician requirements

Funding requirements

The focus should be on estimating service and funding needs and identifying strengths, weaknesses, opportunities and threats to meeting these needs.

The focus should be on estimating service and funding needs and identifying strengths, weaknesses, opportunities and threats to meeting these needs.

|| 10

Safety Net Snapshot

|| 11

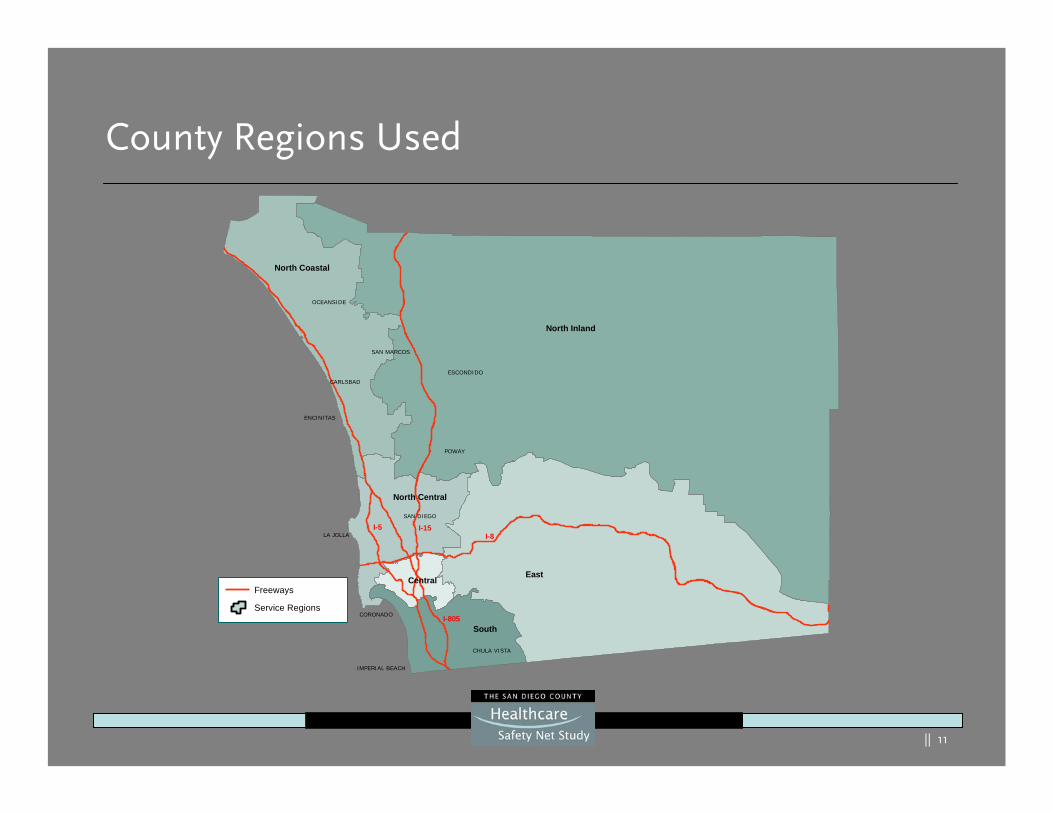

County Regions Used

North Coastal

North Inland

North Central

East

South

Central

I-15I-5I-8

I-805

SAN DIEGO

LA JOLLA

CARLSBAD

POWAY

OCEANSIDE

ENCINITAS

ESCONDIDO

CHULA VISTA

IMPERIAL BEACH

CORONADO

SAN MARCOS

®Freeways

Service Regions

|| 12

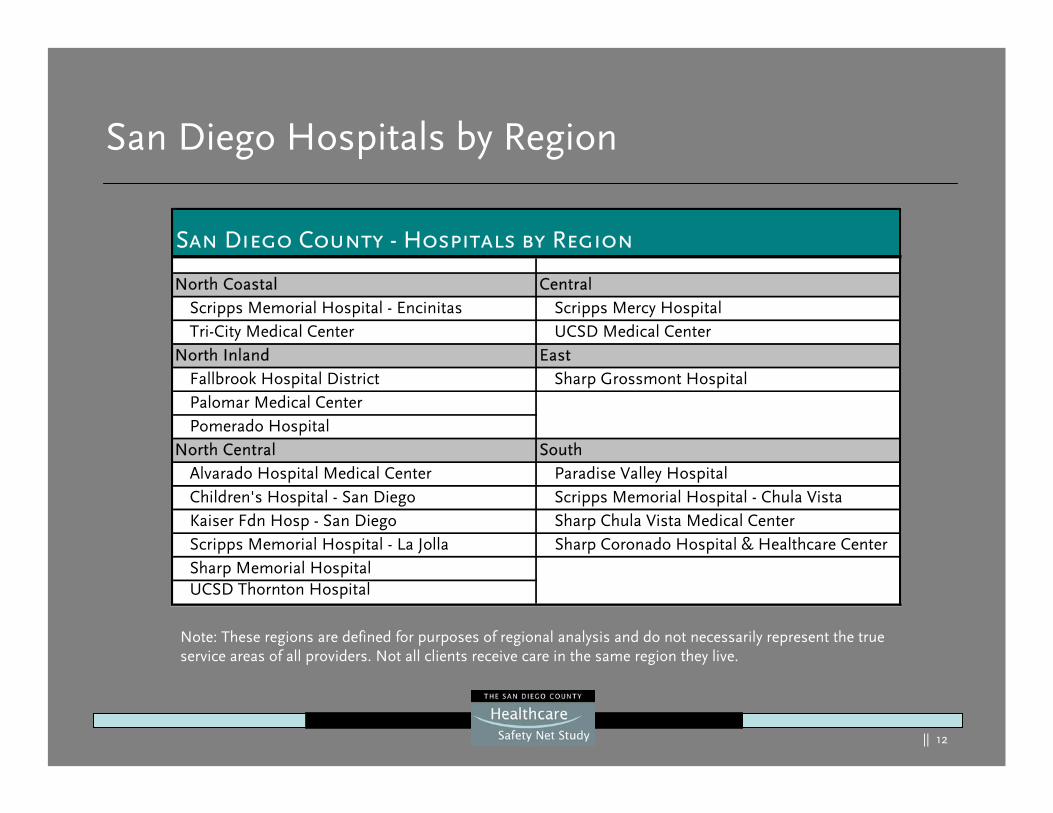

San Diego Hospitals by Region

North Coastal CentralScripps Memorial Hospital - Encinitas Scripps Mercy HospitalTri-City Medical Center UCSD Medical Center

North Inland EastFallbrook Hospital District Sharp Grossmont HospitalPalomar Medical CenterPomerado Hospital

North Central SouthAlvarado Hospital Medical Center Paradise Valley HospitalChildren's Hospital - San Diego Scripps Memorial Hospital - Chula VistaKaiser Fdn Hosp - San Diego Sharp Chula Vista Medical CenterScripps Memorial Hospital - La Jolla Sharp Coronado Hospital & Healthcare CenterSharp Memorial HospitalUCSD Thornton Hospital

San Diego County - Hospitals by Region

Note: These regions are defined for purposes of regional analysis and do not necessarily represent the true service areas of all providers. Not all clients receive care in the same region they live.

|| 13

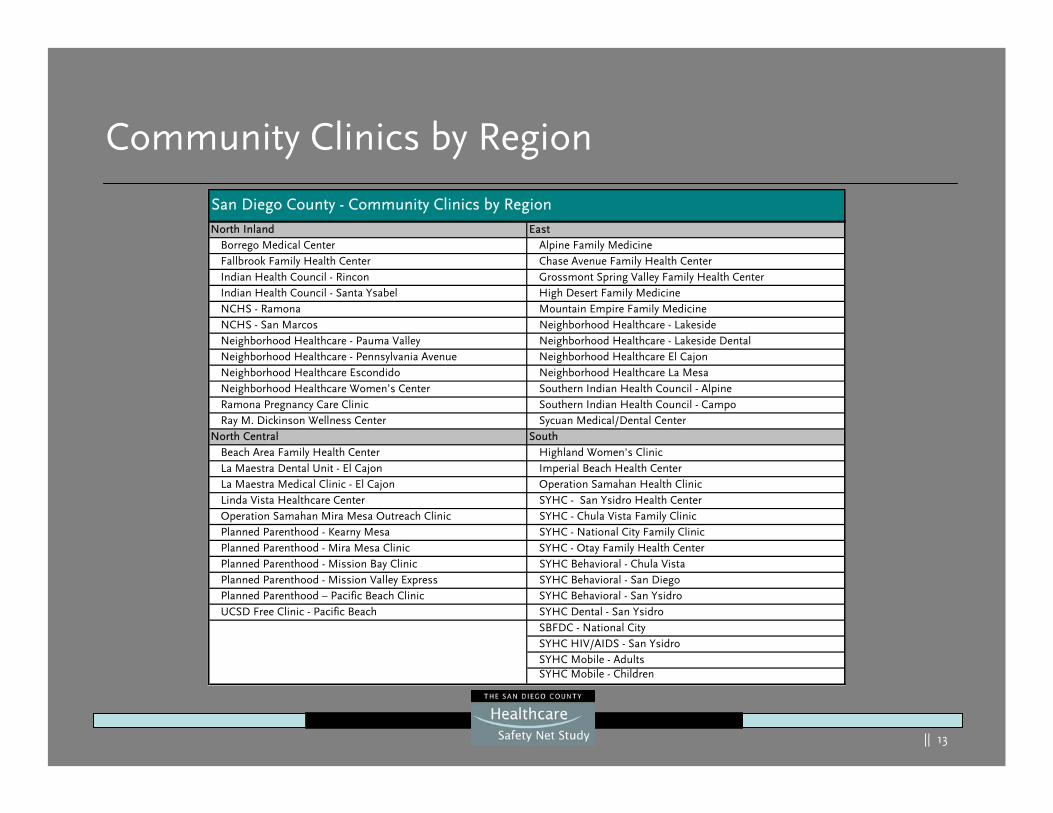

Community Clinics by Region

North Inland EastBorrego Medical Center Alpine Family MedicineFallbrook Family Health Center Chase Avenue Family Health CenterIndian Health Council - Rincon Grossmont Spring Valley Family Health CenterIndian Health Council - Santa Ysabel High Desert Family MedicineNCHS - Ramona Mountain Empire Family MedicineNCHS - San Marcos Neighborhood Healthcare - LakesideNeighborhood Healthcare - Pauma Valley Neighborhood Healthcare - Lakeside DentalNeighborhood Healthcare - Pennsylvania Avenue Neighborhood Healthcare El CajonNeighborhood Healthcare Escondido Neighborhood Healthcare La MesaNeighborhood Healthcare Women’s Center Southern Indian Health Council - AlpineRamona Pregnancy Care Clinic Southern Indian Health Council - CampoRay M. Dickinson Wellness Center Sycuan Medical/Dental Center

North Central SouthBeach Area Family Health Center Highland Women's ClinicLa Maestra Dental Unit - El Cajon Imperial Beach Health CenterLa Maestra Medical Clinic - El Cajon Operation Samahan Health ClinicLinda Vista Healthcare Center SYHC - San Ysidro Health CenterOperation Samahan Mira Mesa Outreach Clinic SYHC - Chula Vista Family ClinicPlanned Parenthood - Kearny Mesa SYHC - National City Family ClinicPlanned Parenthood - Mira Mesa Clinic SYHC - Otay Family Health CenterPlanned Parenthood - Mission Bay Clinic SYHC Behavioral - Chula VistaPlanned Parenthood - Mission Valley Express SYHC Behavioral - San DiegoPlanned Parenthood – Pacific Beach Clinic SYHC Behavioral - San YsidroUCSD Free Clinic - Pacific Beach SYHC Dental - San Ysidro

SBFDC - National CitySYHC HIV/AIDS - San YsidroSYHC Mobile - AdultsSYHC Mobile - Children

San Diego County - Community Clinics by Region

|| 14

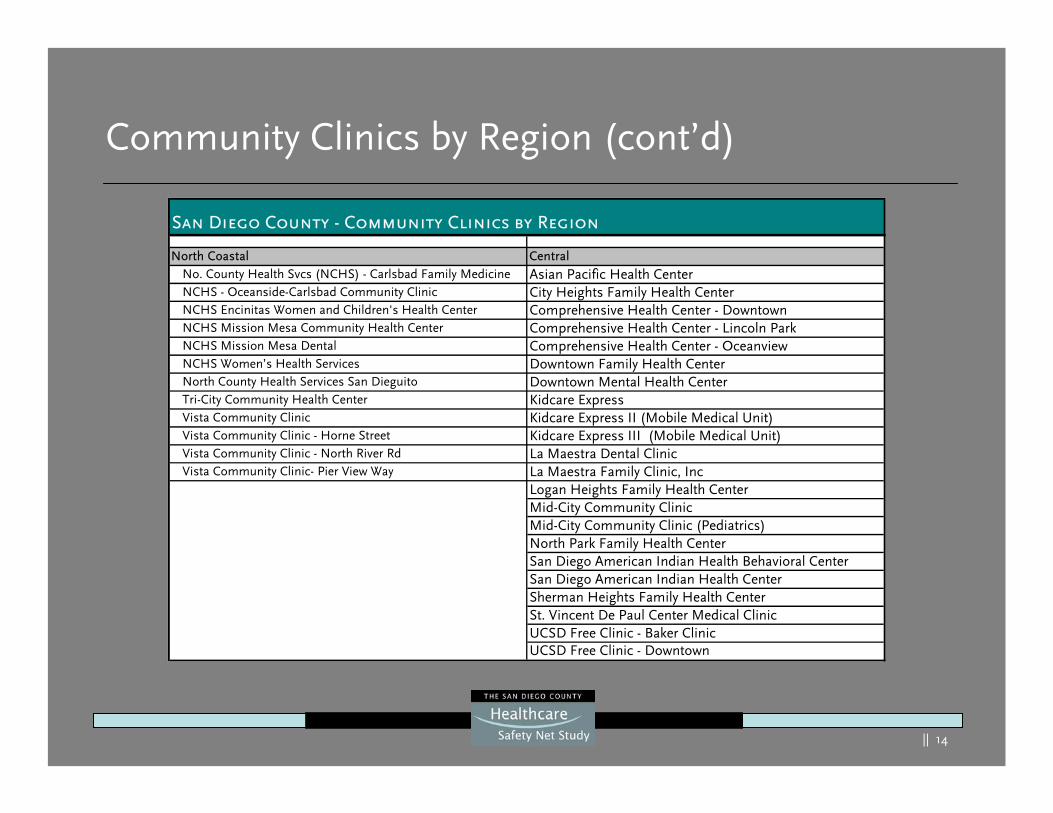

Community Clinics by Region (cont’d)

North Coastal CentralNo. County Health Svcs (NCHS) - Carlsbad Family Medicine Asian Pacific Health CenterNCHS - Oceanside-Carlsbad Community Clinic City Heights Family Health CenterNCHS Encinitas Women and Children's Health Center Comprehensive Health Center - DowntownNCHS Mission Mesa Community Health Center Comprehensive Health Center - Lincoln ParkNCHS Mission Mesa Dental Comprehensive Health Center - OceanviewNCHS Women’s Health Services Downtown Family Health CenterNorth County Health Services San Dieguito Downtown Mental Health CenterTri-City Community Health Center Kidcare ExpressVista Community Clinic Kidcare Express II (Mobile Medical Unit)Vista Community Clinic - Horne Street Kidcare Express III (Mobile Medical Unit)Vista Community Clinic - North River Rd La Maestra Dental ClinicVista Community Clinic- Pier View Way La Maestra Family Clinic, Inc

Logan Heights Family Health CenterMid-City Community ClinicMid-City Community Clinic (Pediatrics)North Park Family Health CenterSan Diego American Indian Health Behavioral CenterSan Diego American Indian Health CenterSherman Heights Family Health CenterSt. Vincent De Paul Center Medical ClinicUCSD Free Clinic - Baker ClinicUCSD Free Clinic - Downtown

San Diego County - Community Clinics by Region

|| 15

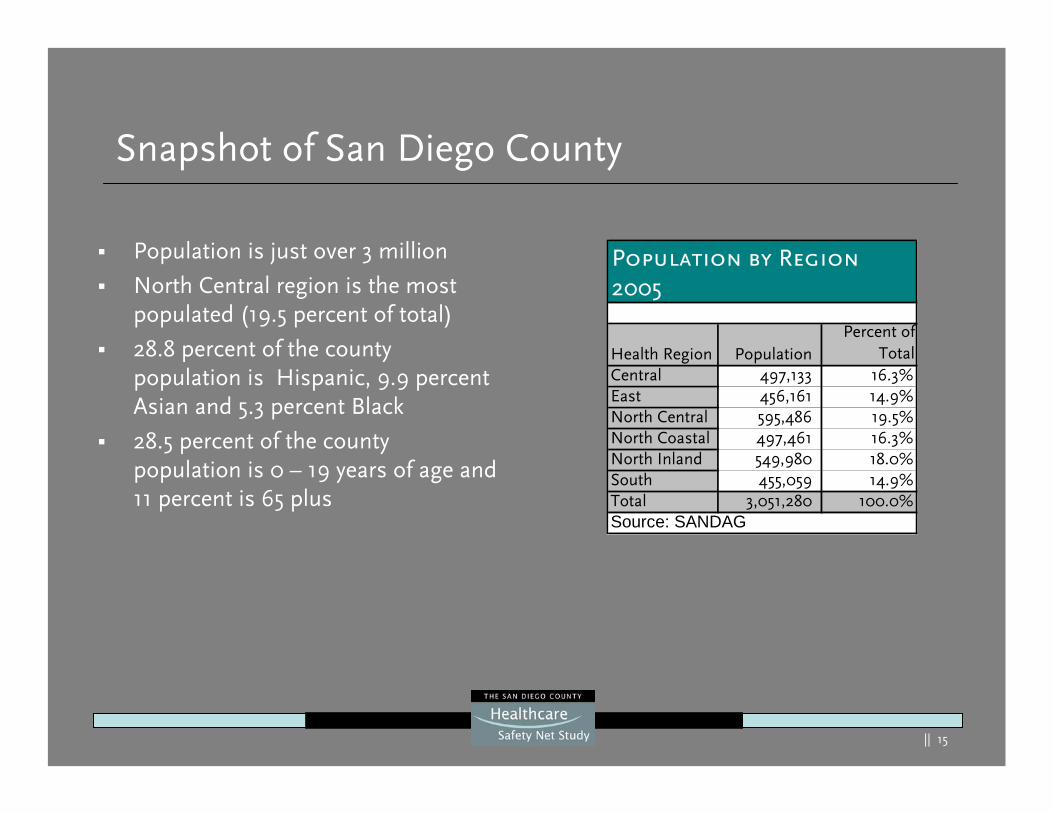

Snapshot of San Diego County

Population is just over 3 million

North Central region is the most populated (19.5 percent of total)

28.8 percent of the county population is Hispanic, 9.9 percent Asian and 5.3 percent Black

28.5 percent of the county population is 0 – 19 years of age and 11 percent is 65 plus

Health Region PopulationPercent of

TotalCentral 497,133 16.3%East 456,161 14.9%North Central 595,486 19.5%North Coastal 497,461 16.3%North Inland 549,980 18.0%South 455,059 14.9%Total 3,051,280 100.0%Source: SANDAG

Population by Region2005

|| 16

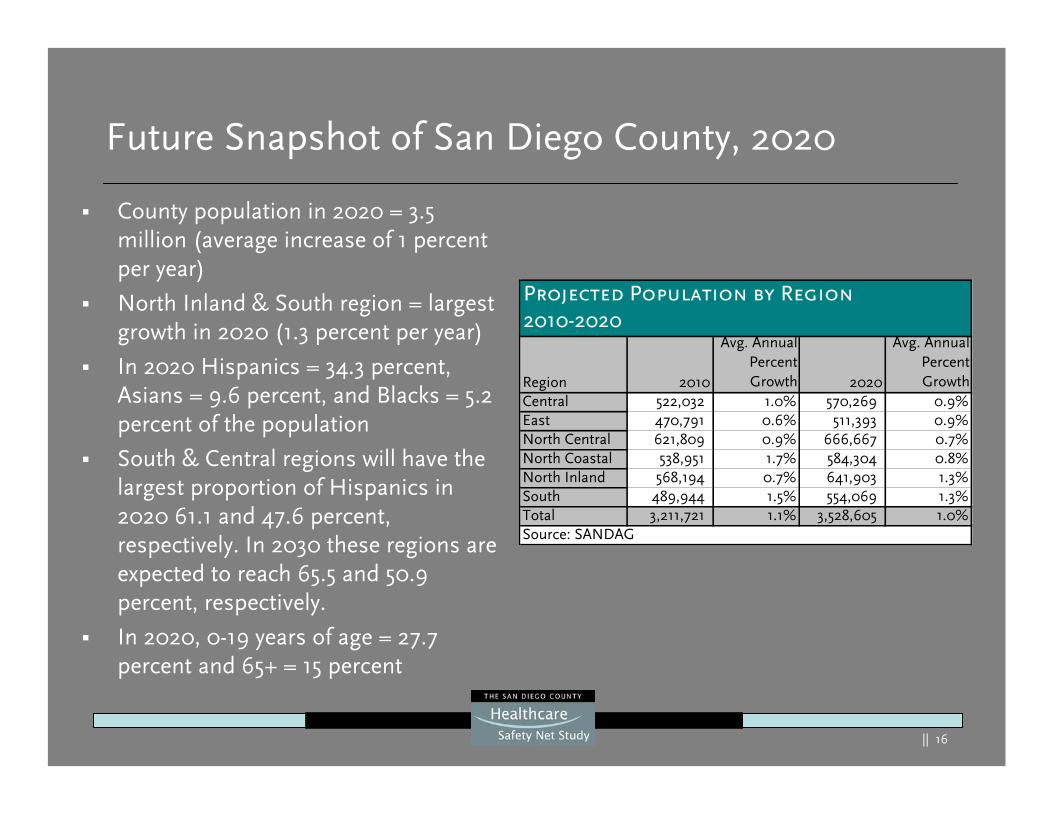

Future Snapshot of San Diego County, 2020

County population in 2020 = 3.5 million (average increase of 1 percent per year)

North Inland & South region = largest growth in 2020 (1.3 percent per year)

In 2020 Hispanics = 34.3 percent, Asians = 9.6 percent, and Blacks = 5.2 percent of the population

South & Central regions will have the largest proportion of Hispanics in 2020 61.1 and 47.6 percent, respectively. In 2030 these regions are expected to reach 65.5 and 50.9 percent, respectively.

In 2020, 0-19 years of age = 27.7 percent and 65+ = 15 percent

Region 2010

Avg. AnnualPercentGrowth 2020

Avg. AnnualPercentGrowth

Central 522,032 1.0% 570,269 0.9%East 470,791 0.6% 511,393 0.9%North Central 621,809 0.9% 666,667 0.7%North Coastal 538,951 1.7% 584,304 0.8%North Inland 568,194 0.7% 641,903 1.3%South 489,944 1.5% 554,069 1.3%Total 3,211,721 1.1% 3,528,605 1.0%Source: SANDAG

Projected Population by Region2010-2020

|| 17

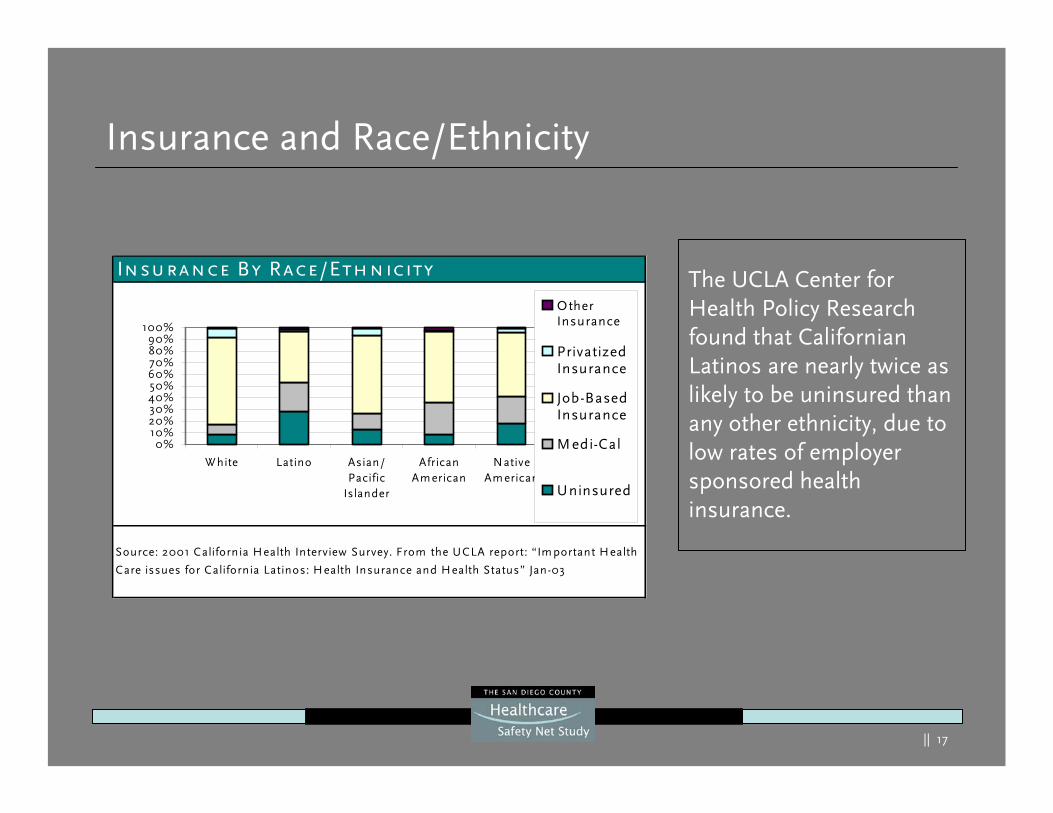

Insurance and Race/Ethnicity

The UCLA Center for Health Policy Research found that Californian Latinos are nearly twice as likely to be uninsured than any other ethnicity, due to low rates of employer sponsored health insurance.

Insurance By Race/Ethnicity

Source: 2001 California Health Interview Survey. From the UCLA report: “Im portant H ealth

Care issues for California Latinos: H ealth Insurance and Health Status” Jan-03

0%10%20%30%40%50%60%70%80%90%

100%

W hite Latino Asian/Pacific

Islander

AfricanAm erican

NativeAm erican

OtherInsurance

PrivatizedInsurance

Job-BasedInsurance

M edi-Cal

Uninsured

|| 18

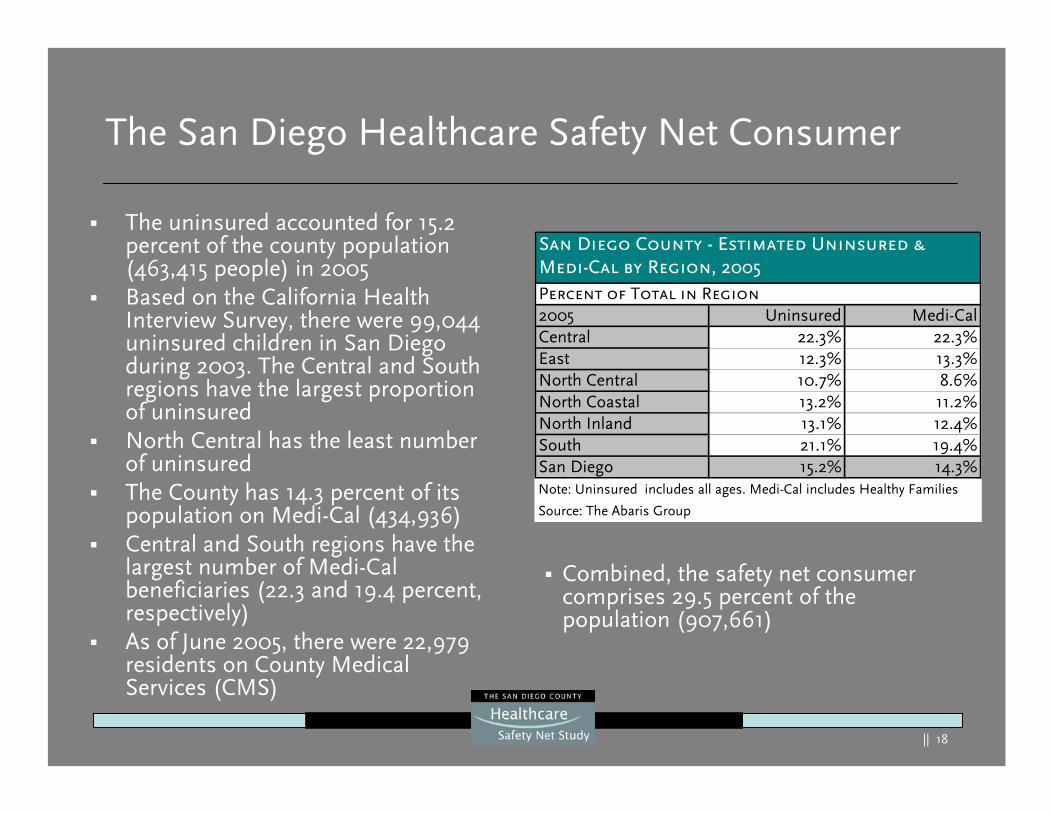

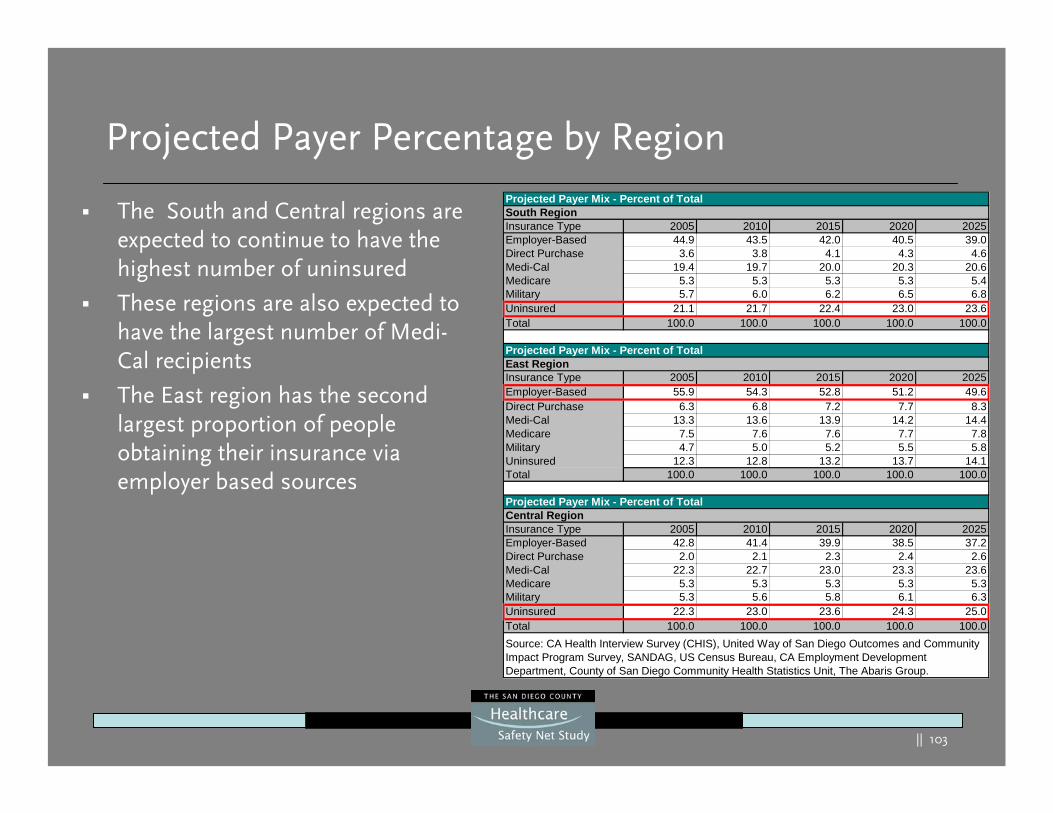

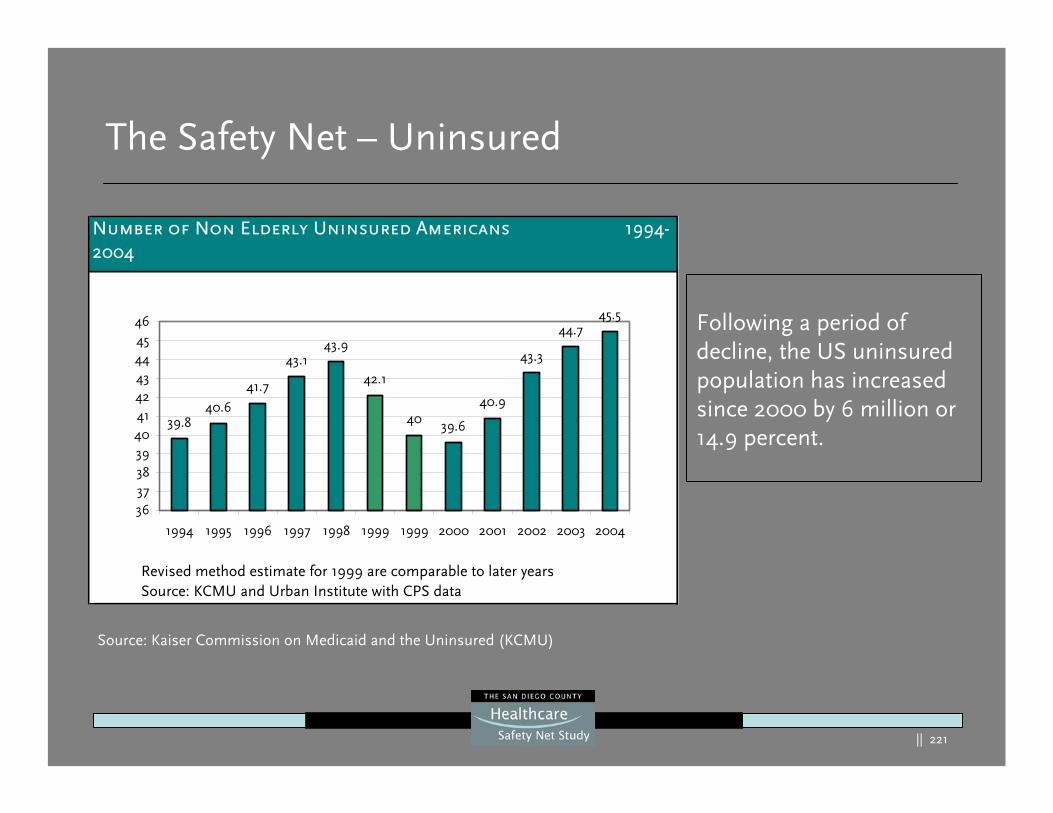

The San Diego Healthcare Safety Net Consumer

The uninsured accounted for 15.2 percent of the county population (463,415 people) in 2005Based on the California Health Interview Survey, there were 99,044 uninsured children in San Diego during 2003. The Central and South regions have the largest proportion of uninsuredNorth Central has the least number of uninsuredThe County has 14.3 percent of its population on Medi-Cal (434,936)Central and South regions have the largest number of Medi-Cal beneficiaries (22.3 and 19.4 percent, respectively)As of June 2005, there were 22,979 residents on County Medical Services (CMS)

Combined, the safety net consumer comprises 29.5 percent of the population (907,661)

Percent of Total in Region2005 Uninsured Medi-CalCentral 22.3% 22.3%East 12.3% 13.3%North Central 10.7% 8.6%North Coastal 13.2% 11.2%North Inland 13.1% 12.4%South 21.1% 19.4%San Diego 15.2% 14.3%

Source: The Abaris Group

Note: Uninsured includes all ages. Medi-Cal includes Healthy Families

San Diego County - Estimated Uninsured &Medi-Cal by Region, 2005

|| 19

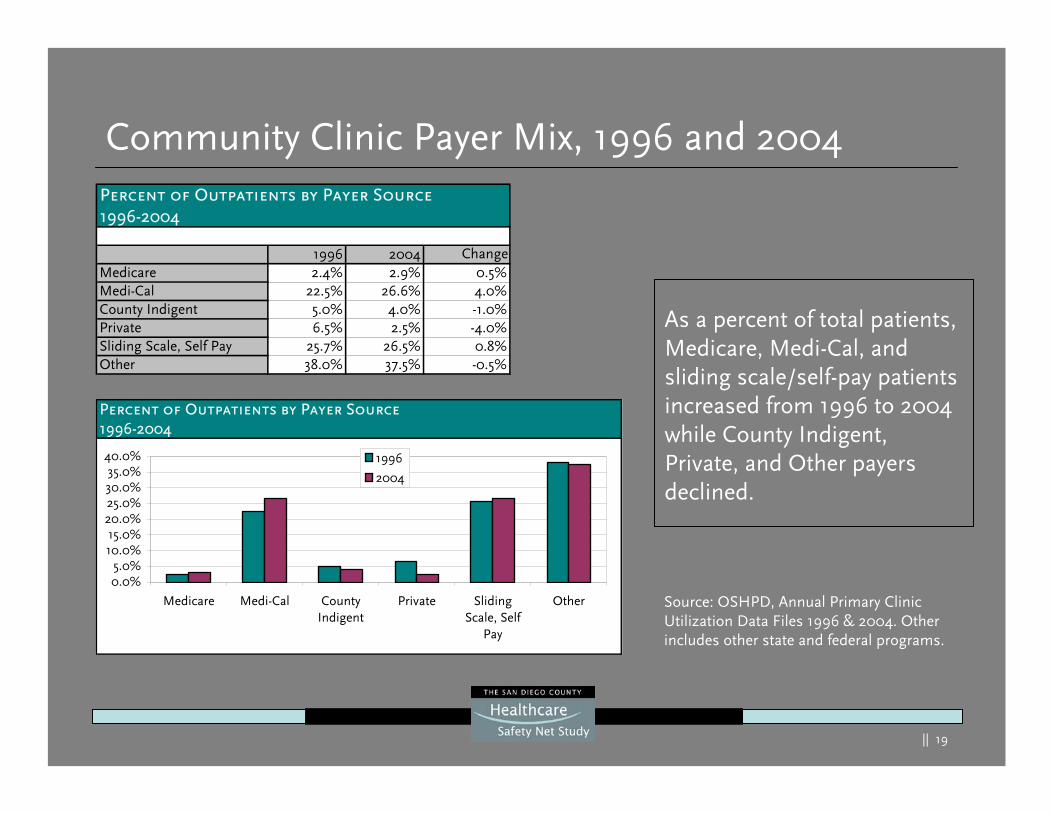

Community Clinic Payer Mix, 1996 and 2004

As a percent of total patients, Medicare, Medi-Cal, and sliding scale/self-pay patients increased from 1996 to 2004 while County Indigent, Private, and Other payers declined.

Source: OSHPD, Annual Primary Clinic Utilization Data Files 1996 & 2004. Other includes other state and federal programs.

Percent of Outpatients by Payer Source1996-2004

0.0%5.0%

10.0%15.0%

20.0%25.0%30.0%35.0%

40.0%

Medicare Medi-Cal CountyIndigent

Private SlidingScale, Self

Pay

Other

1996

2004

Percent of Outpatients by Payer Source1996-2004

1996 2004 ChangeMedicare 2.4% 2.9% 0.5%Medi-Cal 22.5% 26.6% 4.0%County Indigent 5.0% 4.0% -1.0%Private 6.5% 2.5% -4.0%Sliding Scale, Self Pay 25.7% 26.5% 0.8%Other 38.0% 37.5% -0.5%

|| 20

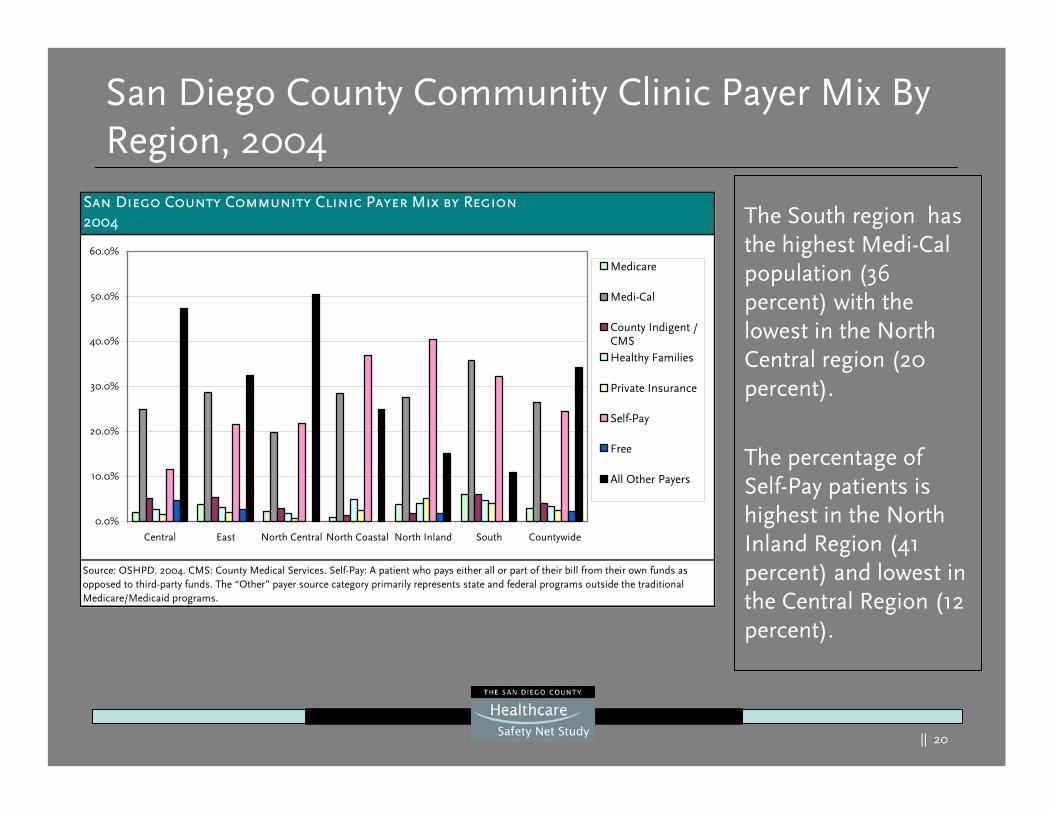

San Diego County Community Clinic Payer Mix By Region, 2004

The South region has the highest Medi-Cal population (36 percent) with the lowest in the North Central region (20 percent).

The percentage of Self-Pay patients is highest in the North Inland Region (41 percent) and lowest in the Central Region (12 percent).

San Diego County Community Clinic Payer Mix by Region2004

Source: OSHPD. 2004. CMS: County Medical Services. Self-Pay: A patient who pays either all or part of their bill from their own funds as opposed to third-party funds. The “Other” payer source category primarily represents state and federal programs outside the traditional Medicare/Medicaid programs.

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Central East North Central North Coastal North Inland South Countywide

Medicare

Medi-Cal

County Indigent /CMS Healthy Families

Private Insurance

Self-Pay

Free

All Other Payers

|| 21

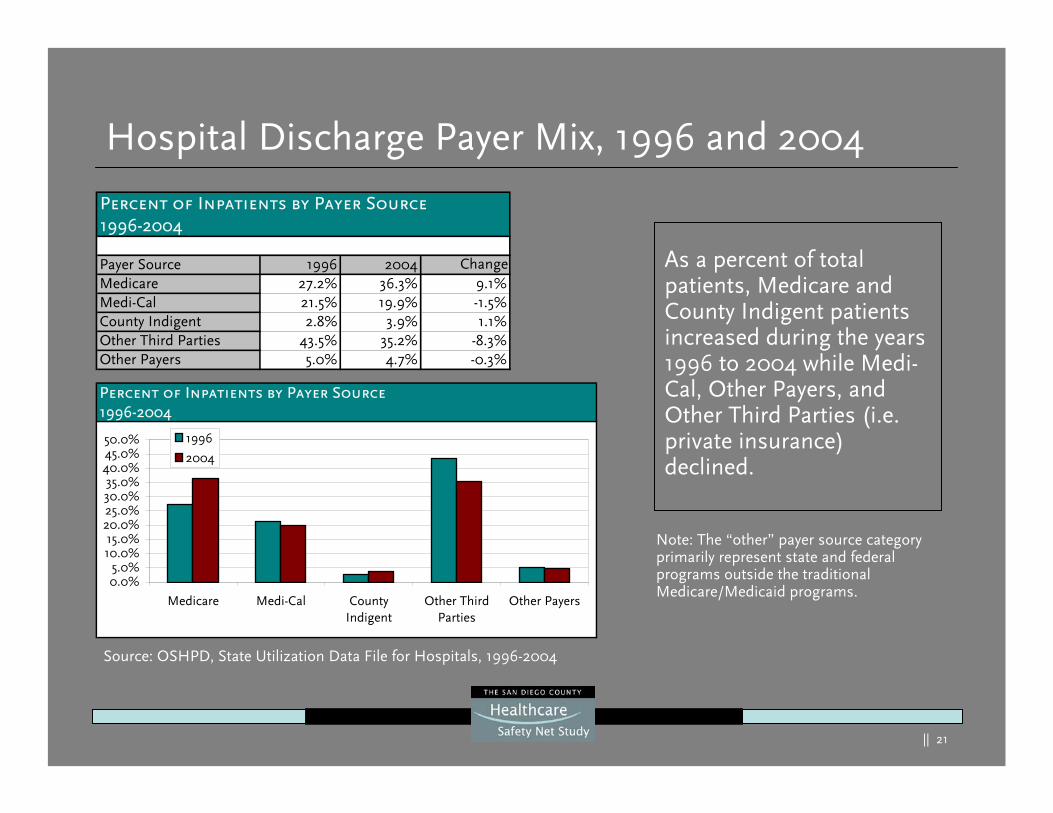

Hospital Discharge Payer Mix, 1996 and 2004

As a percent of total patients, Medicare and County Indigent patients increased during the years 1996 to 2004 while Medi-Cal, Other Payers, and Other Third Parties (i.e. private insurance) declined.

Percent of Inpatients by Payer Source1996-2004

Payer Source 1996 2004 ChangeMedicare 27.2% 36.3% 9.1%Medi-Cal 21.5% 19.9% -1.5%County Indigent 2.8% 3.9% 1.1%Other Third Parties 43.5% 35.2% -8.3%Other Payers 5.0% 4.7% -0.3%

Percent of Inpatients by Payer Source1996-2004

0.0%5.0%

10.0%15.0%

20.0%25.0%30.0%35.0%

40.0%45.0%50.0%

Medicare Medi-Cal CountyIndigent

Other ThirdParties

Other Payers

1996

2004

Source: OSHPD, State Utilization Data File for Hospitals, 1996-2004

Note: The “other” payer source category primarily represent state and federal programs outside the traditional Medicare/Medicaid programs.

|| 22

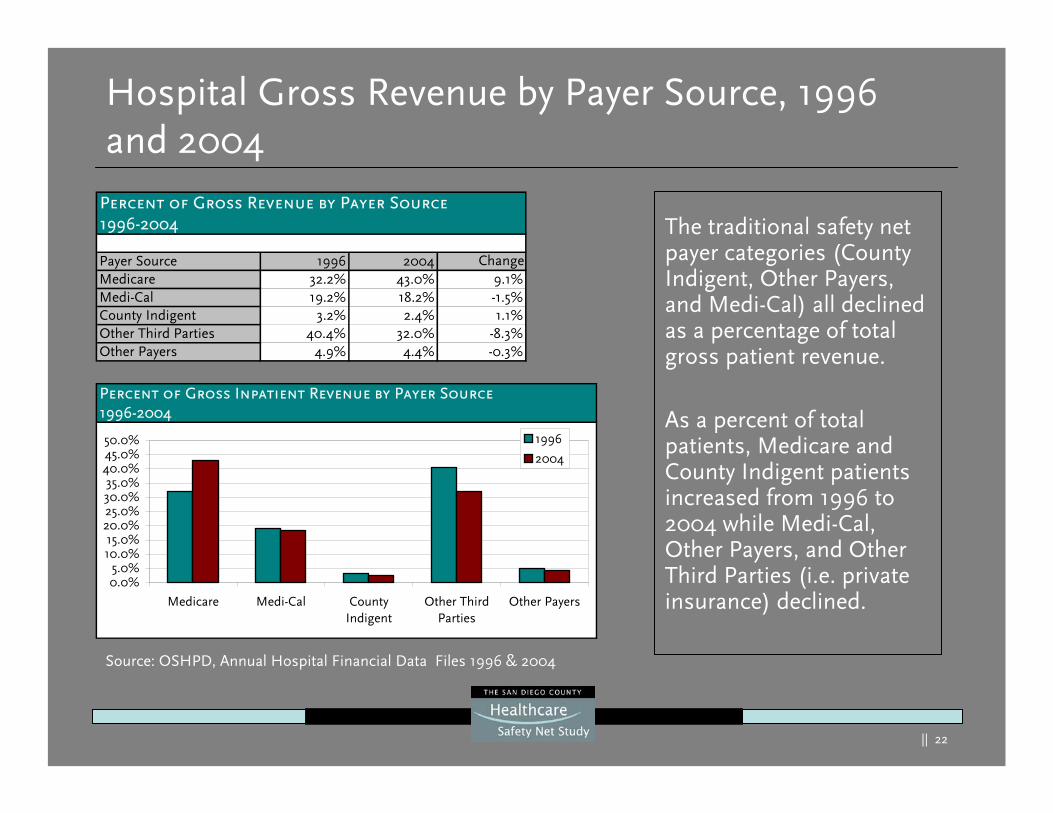

Hospital Gross Revenue by Payer Source, 1996 and 2004

The traditional safety net payer categories (County Indigent, Other Payers, and Medi-Cal) all declined as a percentage of total gross patient revenue.

As a percent of total patients, Medicare and County Indigent patients increased from 1996 to 2004 while Medi-Cal, Other Payers, and Other Third Parties (i.e. private insurance) declined.

Source: OSHPD, Annual Hospital Financial Data Files 1996 & 2004

Percent of Gross Revenue by Payer Source1996-2004

Payer Source 1996 2004 ChangeMedicare 32.2% 43.0% 9.1%Medi-Cal 19.2% 18.2% -1.5%County Indigent 3.2% 2.4% 1.1%Other Third Parties 40.4% 32.0% -8.3%Other Payers 4.9% 4.4% -0.3%

Percent of Gross Inpatient Revenue by Payer Source1996-2004

0.0%5.0%

10.0%15.0%

20.0%25.0%30.0%35.0%

40.0%45.0%50.0%

Medicare Medi-Cal CountyIndigent

Other ThirdParties

Other Payers

1996

2004

|| 23

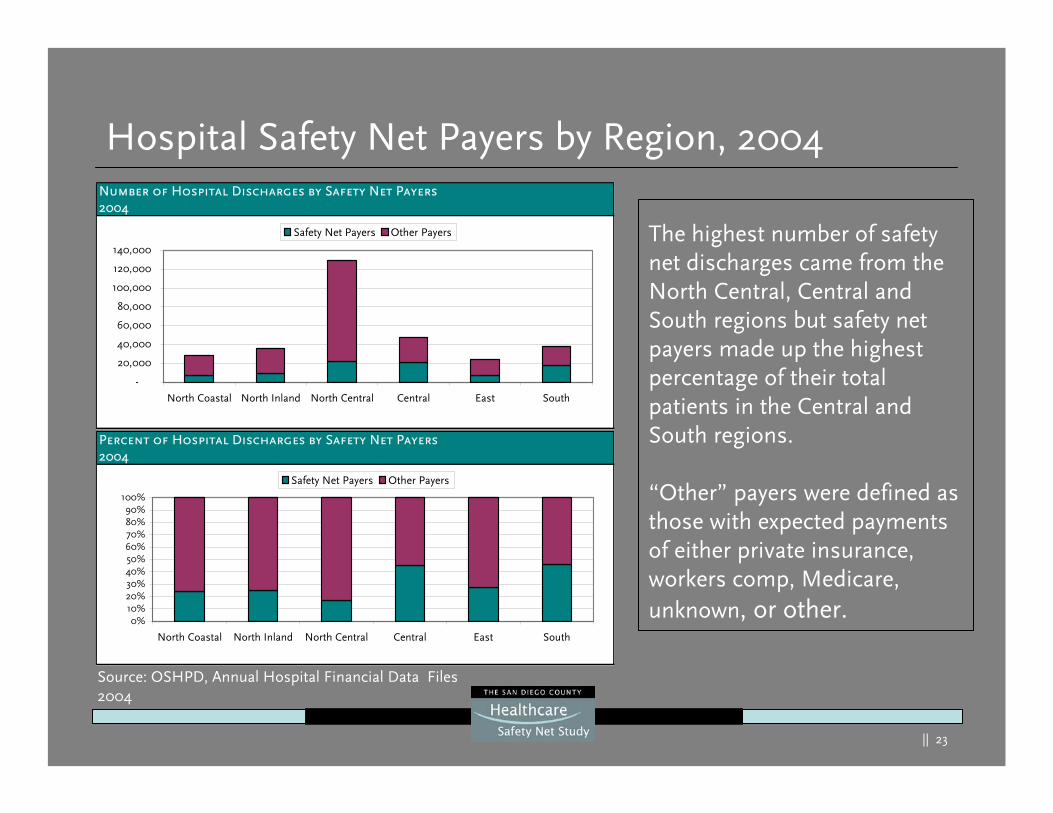

Hospital Safety Net Payers by Region, 2004

The highest number of safety net discharges came from the North Central, Central and South regions but safety net payers made up the highest percentage of their total patients in the Central and South regions.

“Other” payers were defined as those with expected payments of either private insurance, workers comp, Medicare, unknown, or other.

Percent of Hospital Discharges by Safety Net Payers2004

0%10%20%30%40%50%60%70%80%90%

100%

North Coastal North Inland North Central Central East South

Safety Net Payers Other Payers

Number of Hospital Discharges by Safety Net Payers2004

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

North Coastal North Inland North Central Central East South

Safety Net Payers Other Payers

Source: OSHPD, Annual Hospital Financial Data Files 2004

|| 24

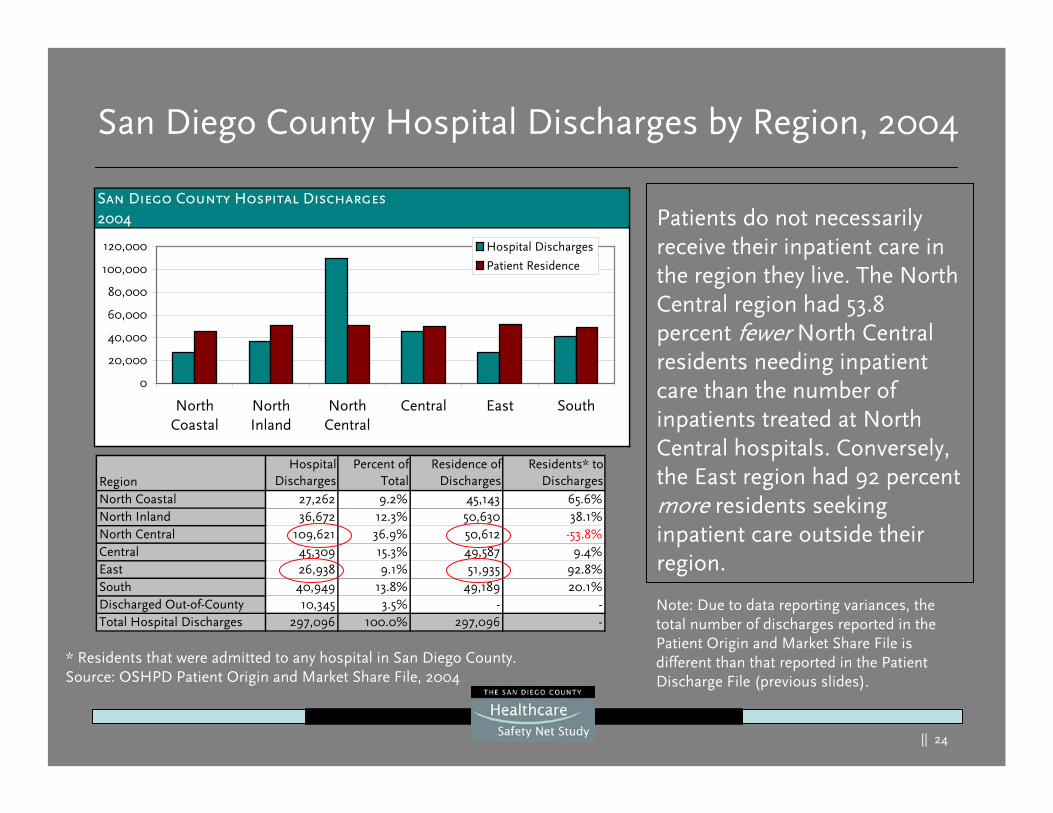

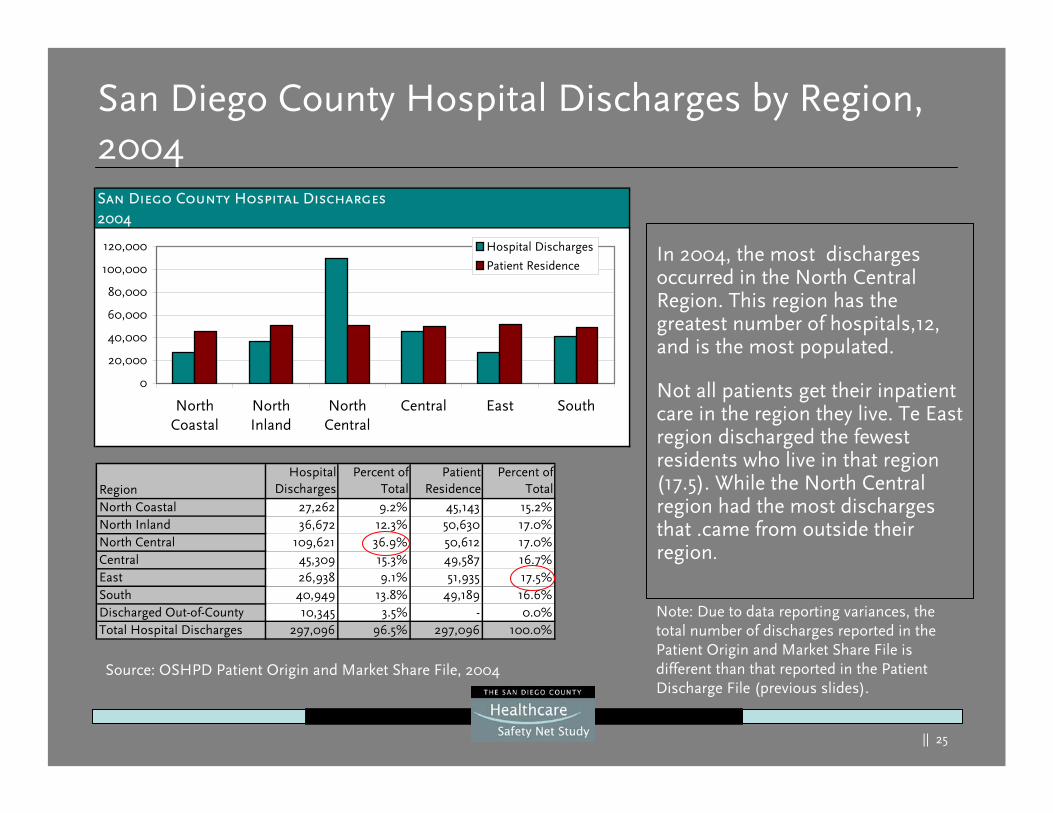

San Diego County Hospital Discharges by Region, 2004

Patients do not necessarily receive their inpatient care in the region they live. The North Central region had 53.8 percent fewer North Central residents needing inpatient care than the number of inpatients treated at North Central hospitals. Conversely, the East region had 92 percent more residents seeking inpatient care outside their region.

Note: Due to data reporting variances, the total number of discharges reported in the Patient Origin and Market Share File is different than that reported in the Patient Discharge File (previous slides).

San Diego County Hospital Discharges2004

0

20,000

40,000

60,000

80,000

100,000

120,000

NorthCoastal

NorthInland

NorthCentral

Central East South

Hospital Discharges

Patient Residence

* Residents that were admitted to any hospital in San Diego County.Source: OSHPD Patient Origin and Market Share File, 2004

RegionHospital

DischargesPercent of

TotalResidence of

DischargesResidents* to

DischargesNorth Coastal 27,262 9.2% 45,143 65.6%North Inland 36,672 12.3% 50,630 38.1%North Central 109,621 36.9% 50,612 -53.8%Central 45,309 15.3% 49,587 9.4%East 26,938 9.1% 51,935 92.8%South 40,949 13.8% 49,189 20.1%Discharged Out-of-County 10,345 3.5% - -Total Hospital Discharges 297,096 100.0% 297,096 -

|| 25

RegionHospital

DischargesPercent of

TotalPatient

ResidencePercent of

TotalNorth Coastal 27,262 9.2% 45,143 15.2%North Inland 36,672 12.3% 50,630 17.0%North Central 109,621 36.9% 50,612 17.0%Central 45,309 15.3% 49,587 16.7%East 26,938 9.1% 51,935 17.5%South 40,949 13.8% 49,189 16.6%Discharged Out-of-County 10,345 3.5% - 0.0%Total Hospital Discharges 297,096 96.5% 297,096 100.0%

San Diego County Hospital Discharges by Region, 2004

In 2004, the most discharges occurred in the North Central Region. This region has the greatest number of hospitals,12, and is the most populated.

Not all patients get their inpatient care in the region they live. Te East region discharged the fewest residents who live in that region (17.5). While the North Central region had the most discharges that .came from outside their region.

Note: Due to data reporting variances, the total number of discharges reported in the Patient Origin and Market Share File is different than that reported in the Patient Discharge File (previous slides).

San Diego County Hospital Discharges2004

0

20,000

40,000

60,000

80,000

100,000

120,000

NorthCoastal

NorthInland

NorthCentral

Central East South

Hospital Discharges

Patient Residence

Source: OSHPD Patient Origin and Market Share File, 2004

|| 26

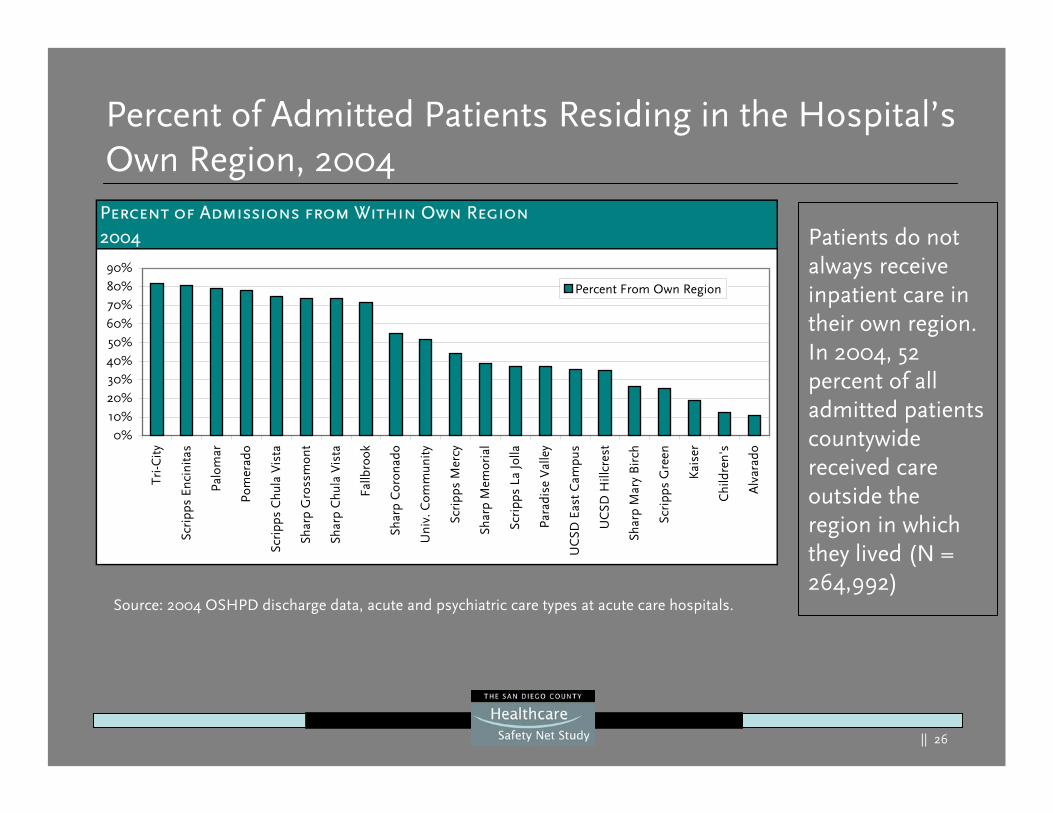

Percent of Admitted Patients Residing in the Hospital’s Own Region, 2004

Percent of Admissions from Within Own Region2004

0%10%20%30%40%50%60%70%80%90%

Tri-C

ity

Scri

pps

Enci

nita

s

Palo

mar

Pom

erad

o

Scri

pps

Chu

la V

ista

Shar

p G

ross

mon

t

Shar

p C

hula

Vis

ta

Fallb

rook

Shar

p C

oron

ado

Uni

v. C

omm

unity

Scri

pps

Mer

cy

Shar

p M

emor

ial

Scri

pps

La Jo

lla

Para

dise

Val

ley

UC

SD E

ast

Cam

pus

UC

SD H

illcr

est

Shar

p M

ary

Bir

ch

Scri

pps

Gre

en

Kai

ser

Chi

ldre

n's

Alv

arad

o

Percent From Own Region

Patients do not always receive inpatient care in their own region. In 2004, 52 percent of all admitted patients countywide received care outside the region in which they lived (N = 264,992)

Source: 2004 OSHPD discharge data, acute and psychiatric care types at acute care hospitals.

|| 27

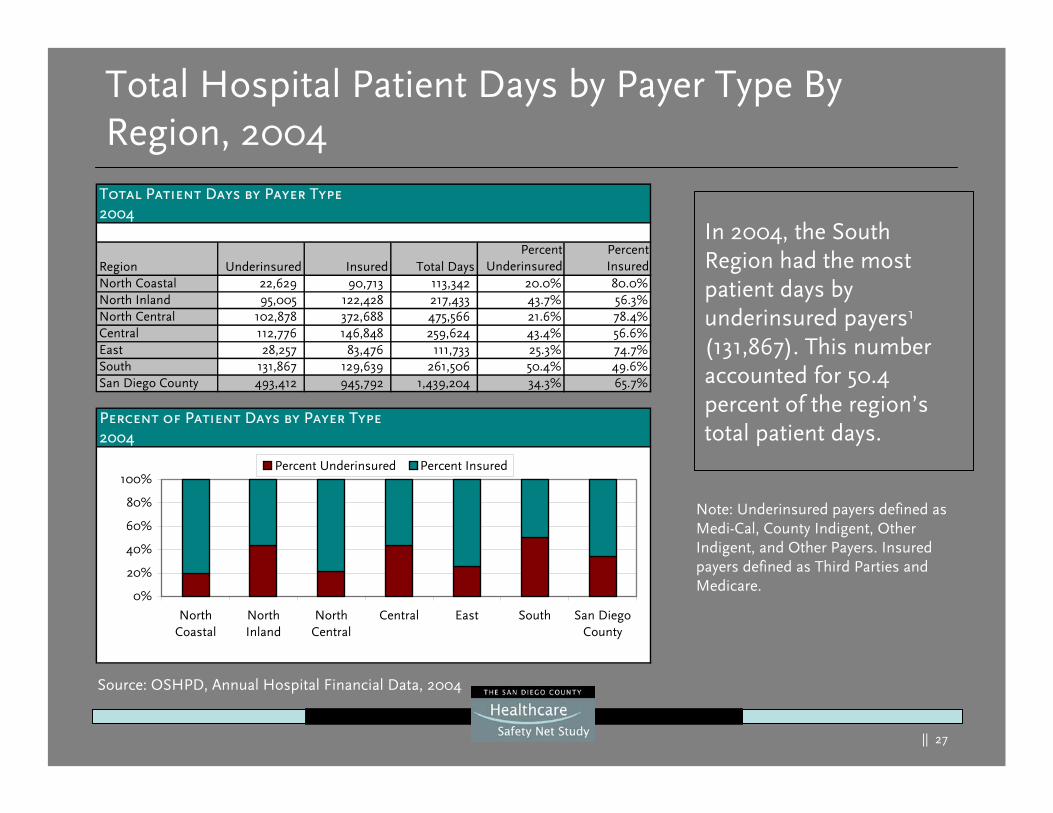

Total Hospital Patient Days by Payer Type By Region, 2004

In 2004, the South Region had the most patient days by underinsured payers1

(131,867). This number accounted for 50.4 percent of the region’s total patient days.

Total Patient Days by Payer Type2004

Region Underinsured Insured Total DaysPercent

UnderinsuredPercentInsured

North Coastal 22,629 90,713 113,342 20.0% 80.0%North Inland 95,005 122,428 217,433 43.7% 56.3%North Central 102,878 372,688 475,566 21.6% 78.4%Central 112,776 146,848 259,624 43.4% 56.6%East 28,257 83,476 111,733 25.3% 74.7%South 131,867 129,639 261,506 50.4% 49.6%San Diego County 493,412 945,792 1,439,204 34.3% 65.7%

Percent of Patient Days by Payer Type2004

0%

20%

40%

60%

80%

100%

NorthCoastal

NorthInland

NorthCentral

Central East South San DiegoCounty

Percent Underinsured Percent Insured

Source: OSHPD, Annual Hospital Financial Data, 2004

Note: Underinsured payers defined as Medi-Cal, County Indigent, Other Indigent, and Other Payers. Insured payers defined as Third Parties and Medicare.

|| 28

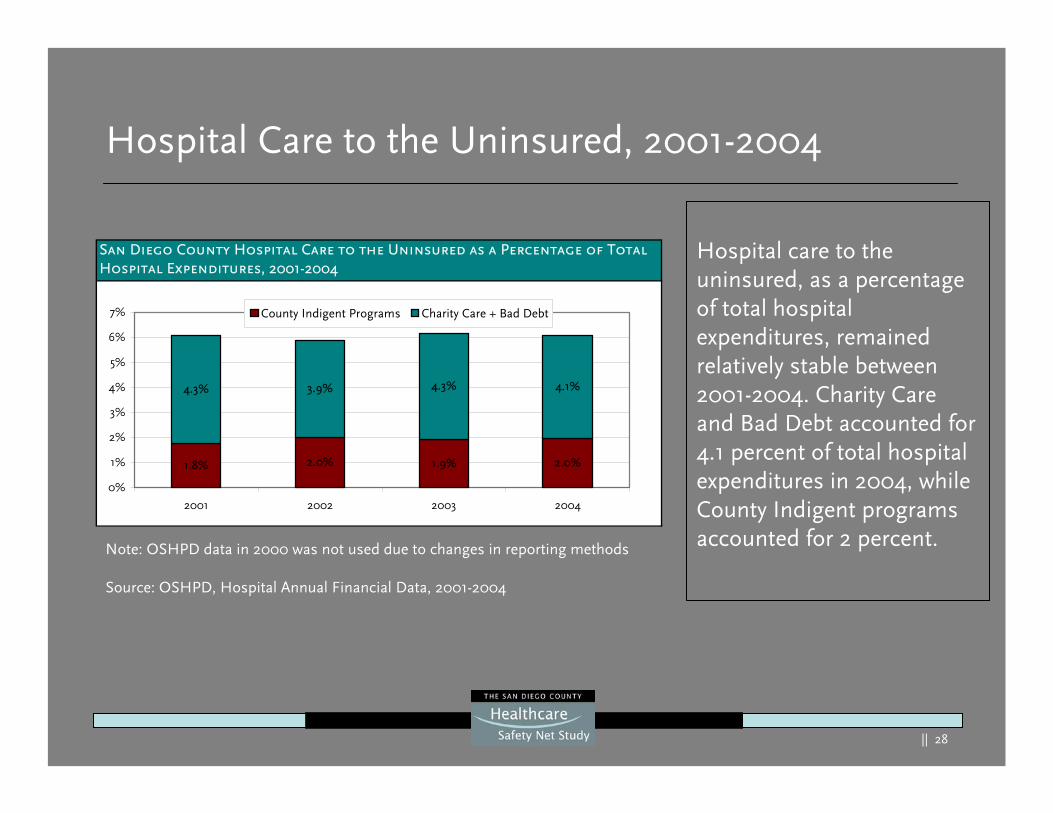

Hospital Care to the Uninsured, 2001-2004

Hospital care to the uninsured, as a percentage of total hospital expenditures, remained relatively stable between 2001-2004. Charity Care and Bad Debt accounted for 4.1 percent of total hospital expenditures in 2004, while County Indigent programs accounted for 2 percent.

San Diego County Hospital Care to the Uninsured as a Percentage of Total Hospital Expenditures, 2001-2004

1.8% 2.0% 1.9% 2.0%

4.3% 3.9% 4.3% 4.1%

0%

1%

2%

3%

4%

5%

6%

7%

2001 2002 2003 2004

County Indigent Programs Charity Care + Bad Debt

Note: OSHPD data in 2000 was not used due to changes in reporting methods

Source: OSHPD, Hospital Annual Financial Data, 2001-2004

|| 29

Current Demand

|| 30

Current Demand Summary

In San Diego County:Demand for healthcare and for the safety net consumer has continued to rise over the last several years:

– For the safety net:• Community clinics visits have increased steadily since 1996

averaging 3.3 percent growth per year• ED patient visits have continued to rise approximately 1.2 percent

per year

– For the safety net and hospitalized patients in general:• Total hospital discharges have grown modestly from 1995 to 2004

averaging 1.5 percent per year with some annual variations. However, total discharges by hospital have grown more dramatically, averaging 6.8 percent per year from 1995 to 2004

• Trauma patient admissions have risen on average 3.3 percent eachyear from 1996 to 2004

|| 31

Current Demand Summary

San Diego County has:

The second highest community clinic utilization rate (160 patients per 1,000 population) in California

A higher utilization rate for hospital discharges when compared to similar sized counties (94.7 discharges/1,000 population)

A low ED utilization rate (225 visits/1,000 population) when compared to California (275 visits/1,000 population) and the US (370 visit/1,000)

An increasing trauma utilization rate (2.9 to 3.3 from FY 1993 to 2005)

Note: Comparison counties were selected based on their relative comparative population size (Orange, population of 3,036,002; San Bernardino, population of 1,926,555; and Riverside, population of 1,849,844).

|| 32

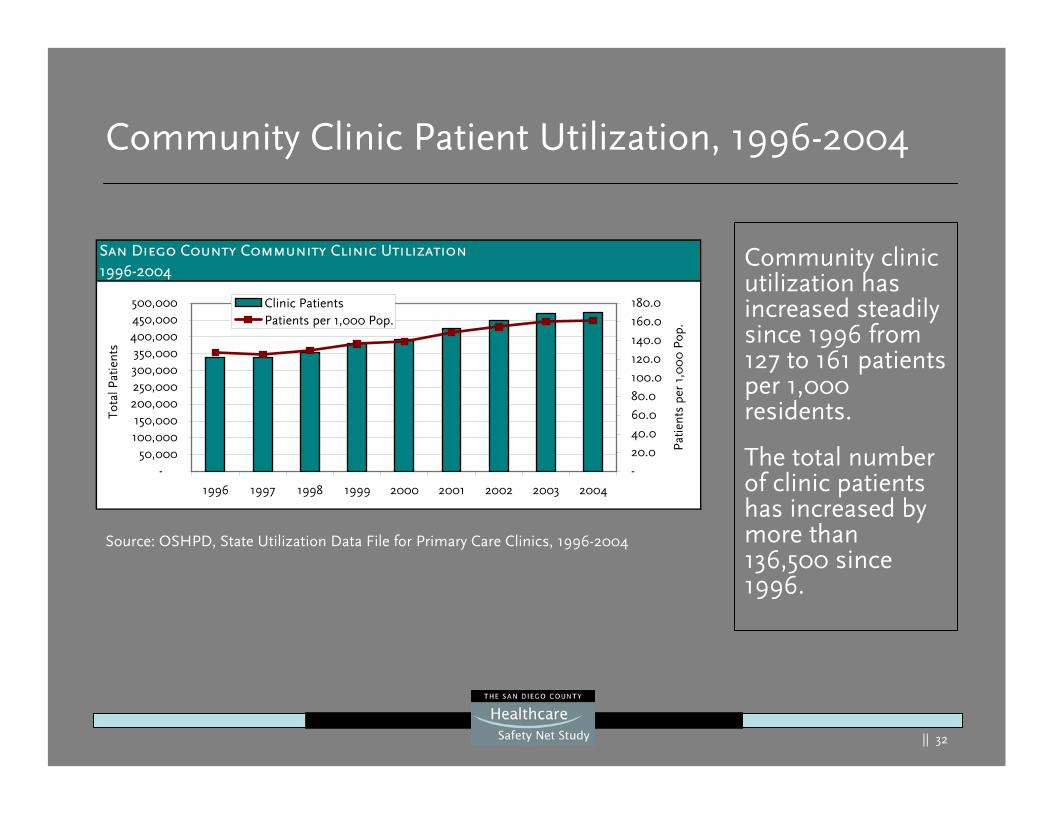

Community Clinic Patient Utilization, 1996-2004

Community clinic utilization has increased steadily since 1996 from 127 to 161 patients per 1,000 residents.

The total number of clinic patients has increased by more than 136,500 since 1996.

Source: OSHPD, State Utilization Data File for Primary Care Clinics, 1996-2004

San Diego County Community Clinic Utilization1996-2004

-50,000

100,000150,000

200,000250,000300,000350,000

400,000450,000500,000

1996 1997 1998 1999 2000 2001 2002 2003 2004

Tota

l Pat

ient

s

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

Pat

ient

s pe

r 1,

00

0 P

op.

Clinic PatientsPatients per 1,000 Pop.

|| 33

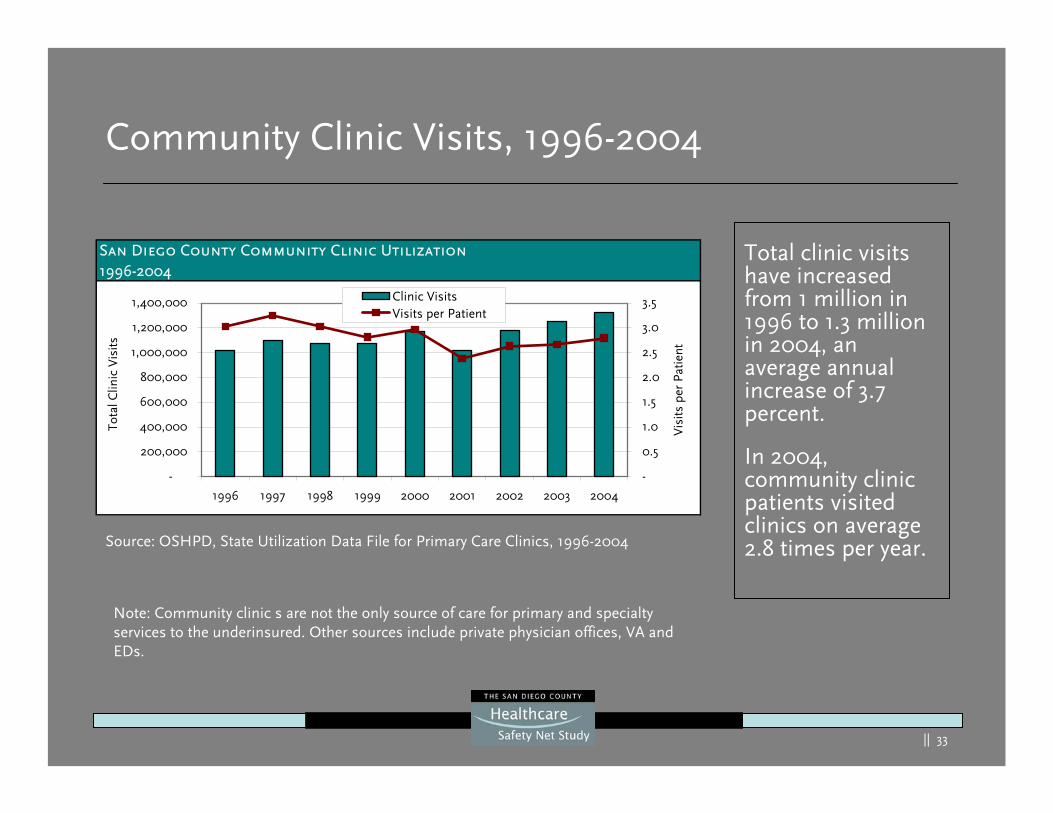

Community Clinic Visits, 1996-2004

Total clinic visits have increased from 1 million in 1996 to 1.3 million in 2004, an average annual increase of 3.7 percent.

In 2004, community clinic patients visited clinics on average 2.8 times per year.

San Diego County Community Clinic Utilization1996-2004

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1996 1997 1998 1999 2000 2001 2002 2003 2004

Tota

l Clin

ic V

isits

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Vis

its p

er P

atie

nt

Clinic VisitsVisits per Patient

Source: OSHPD, State Utilization Data File for Primary Care Clinics, 1996-2004

Note: Community clinic s are not the only source of care for primary and specialty services to the underinsured. Other sources include private physician offices, VA and EDs.

|| 34

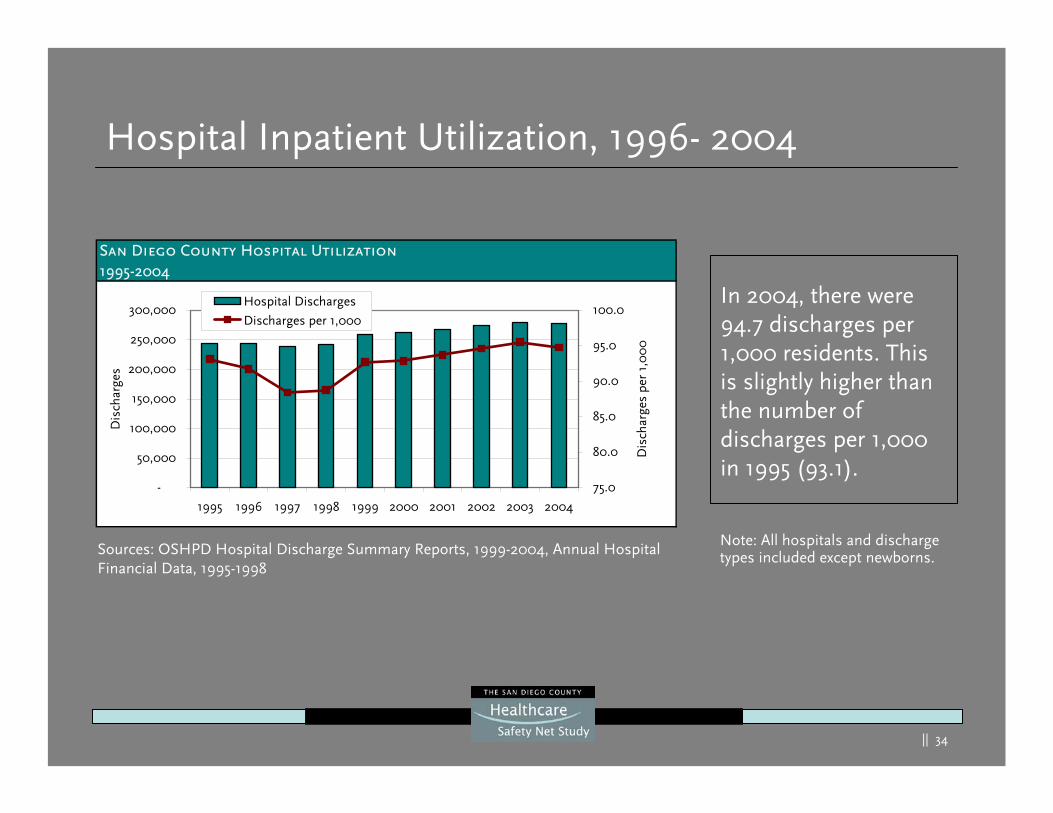

Hospital Inpatient Utilization, 1996- 2004

In 2004, there were 94.7 discharges per 1,000 residents. This is slightly higher than the number of discharges per 1,000 in 1995 (93.1).

San Diego County Hospital Utilization1995-2004

-

50,000

100,000

150,000

200,000

250,000

300,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Dis

char

ges

75.0

80.0

85.0

90.0

95.0

100.0

Dis

char

ges

per

1,0

00

Hospital Discharges

Discharges per 1,000

Sources: OSHPD Hospital Discharge Summary Reports, 1999-2004, Annual Hospital Financial Data, 1995-1998

Note: All hospitals and discharge types included except newborns.

|| 35

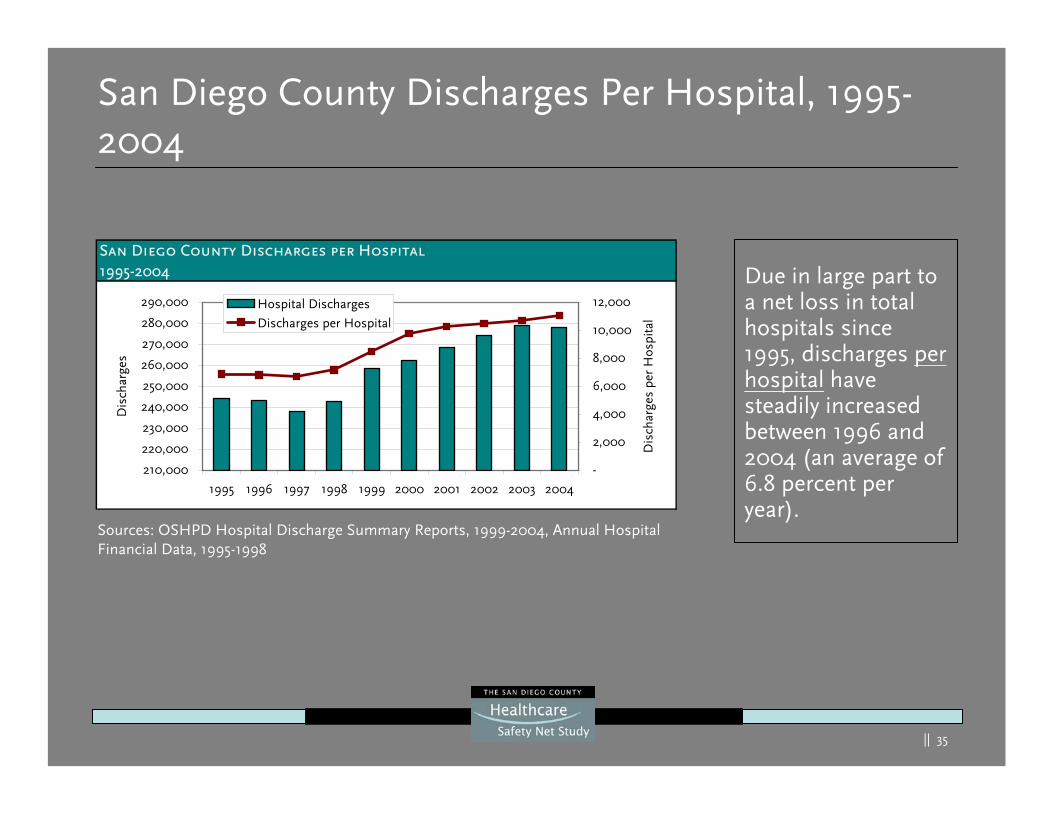

San Diego County Discharges Per Hospital, 1995-2004

Due in large part to a net loss in total hospitals since 1995, discharges per hospital have steadily increased between 1996 and 2004 (an average of 6.8 percent per year).

San Diego County Discharges per Hospital1995-2004

210,000

220,000

230,000

240,000

250,000

260,000

270,000

280,000

290,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Dis

char

ges

-

2,000

4,000

6,000

8,000

10,000

12,000

Dis

char

ges

per

Hos

pita

l

Hospital Discharges

Discharges per Hospital

Sources: OSHPD Hospital Discharge Summary Reports, 1999-2004, Annual Hospital Financial Data, 1995-1998

|| 36

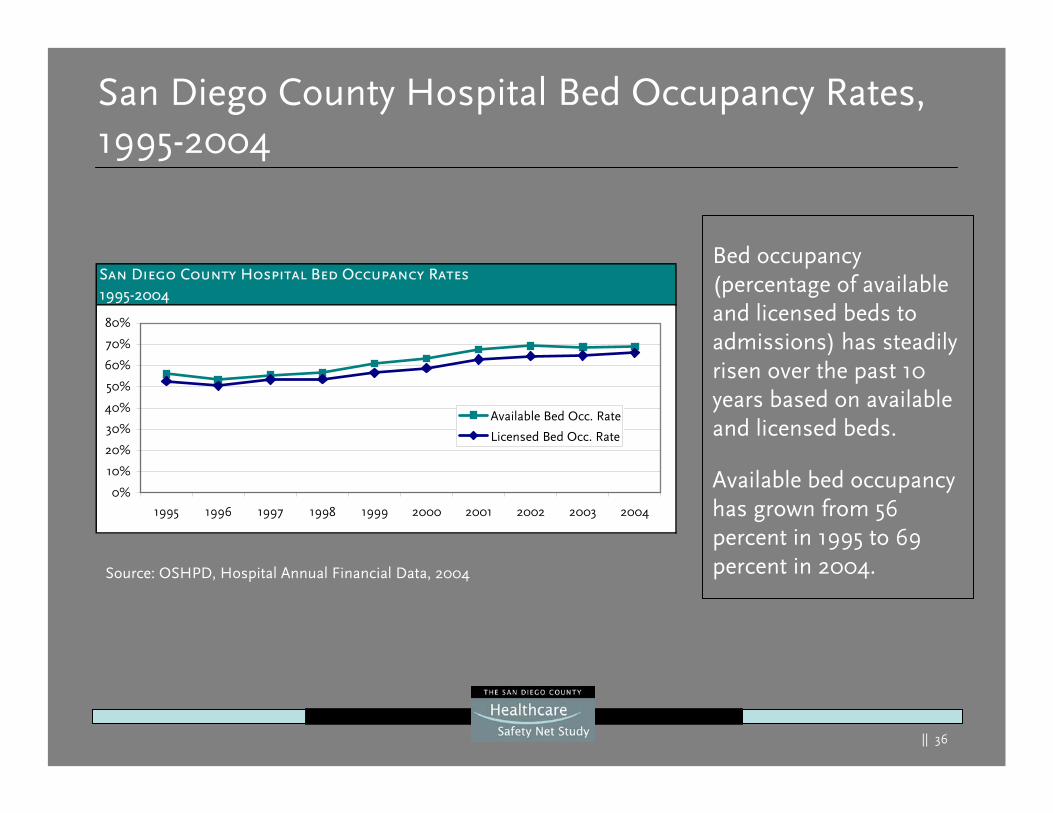

San Diego County Hospital Bed Occupancy Rates, 1995-2004

Bed occupancy (percentage of available and licensed beds to admissions) has steadily risen over the past 10 years based on available and licensed beds.

Available bed occupancy has grown from 56 percent in 1995 to 69 percent in 2004.Source: OSHPD, Hospital Annual Financial Data, 2004

San Diego County Hospital Bed Occupancy Rates1995-2004

0%

10%

20%

30%

40%

50%

60%

70%

80%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Available Bed Occ. Rate

Licensed Bed Occ. Rate

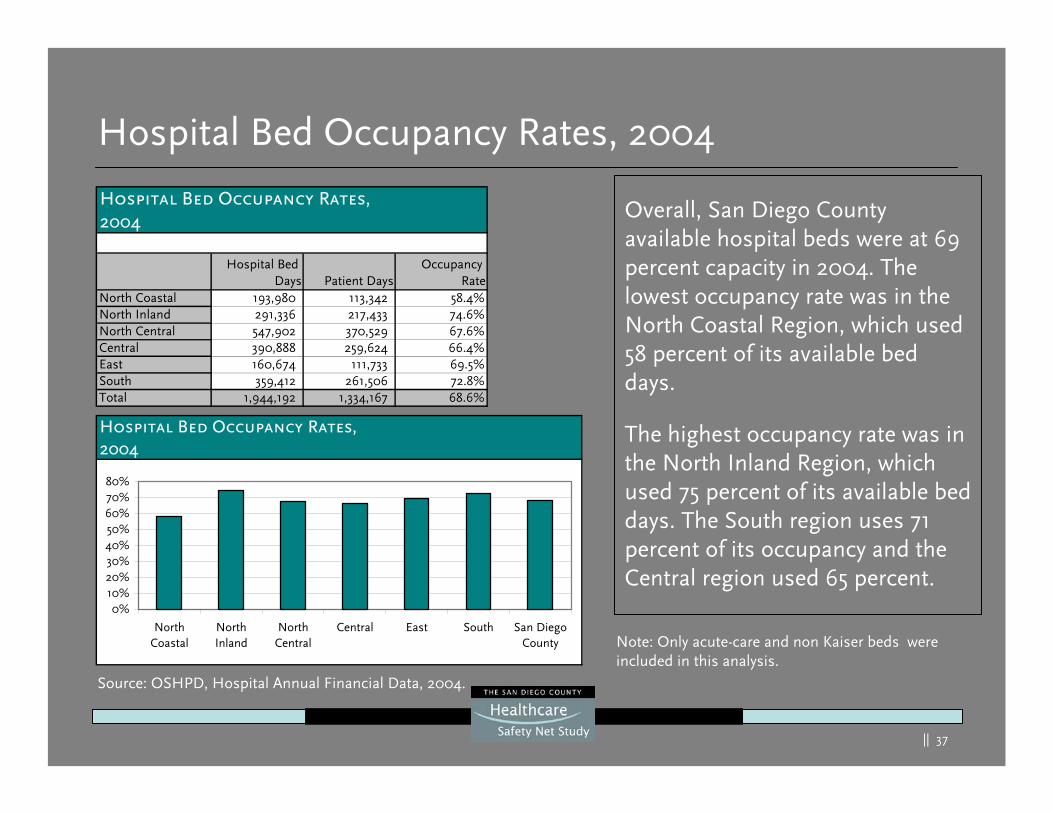

|| 37

Hospital Bed Occupancy Rates, 2004

Overall, San Diego County available hospital beds were at 69 percent capacity in 2004. The lowest occupancy rate was in the North Coastal Region, which used 58 percent of its available bed days.

The highest occupancy rate was in the North Inland Region, which used 75 percent of its available bed days. The South region uses 71 percent of its occupancy and the Central region used 65 percent.

Note: Only acute-care and non Kaiser beds were included in this analysis.

Hospital Bed Occupancy Rates,2004

Hospital Bed Days Patient Days

Occupancy Rate

North Coastal 193,980 113,342 58.4%North Inland 291,336 217,433 74.6%North Central 547,902 370,529 67.6%Central 390,888 259,624 66.4%East 160,674 111,733 69.5%South 359,412 261,506 72.8%Total 1,944,192 1,334,167 68.6%

Hospital Bed Occupancy Rates,2004

0%10%20%30%40%50%60%70%80%

NorthCoastal

NorthInland

NorthCentral

Central East South San DiegoCounty

Source: OSHPD, Hospital Annual Financial Data, 2004.

|| 38

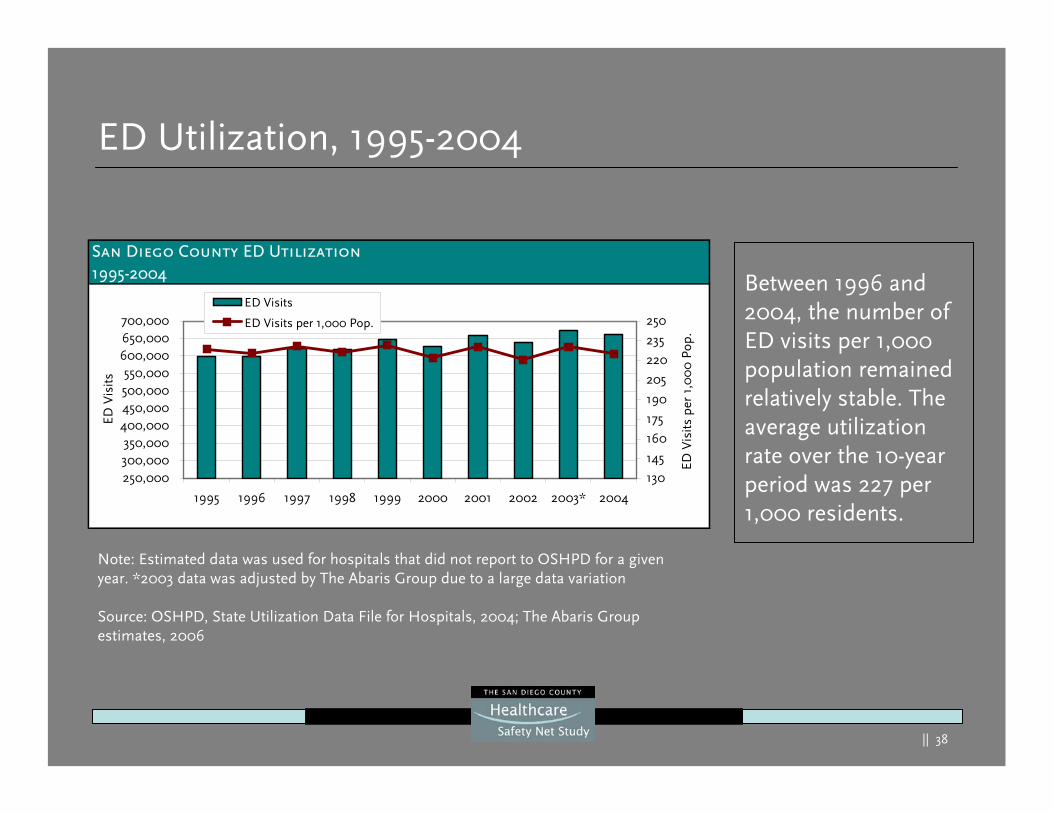

ED Utilization, 1995-2004

Between 1996 and 2004, the number of ED visits per 1,000 population remained relatively stable. The average utilization rate over the 10-year period was 227 per 1,000 residents.

Note: Estimated data was used for hospitals that did not report to OSHPD for a given year. *2003 data was adjusted by The Abaris Group due to a large data variation

Source: OSHPD, State Utilization Data File for Hospitals, 2004; The Abaris Group estimates, 2006

San Diego County ED Utilization1995-2004

250,000300,000350,000

400,000450,000500,000550,000

600,000650,000700,000

1995 1996 1997 1998 1999 2000 2001 2002 2003* 2004

ED V

isits

130

145

160

175

190

205

220

235

250

ED V

isits

per

1,0

00

Pop

.

ED Visits

ED Visits per 1,000 Pop.

|| 39

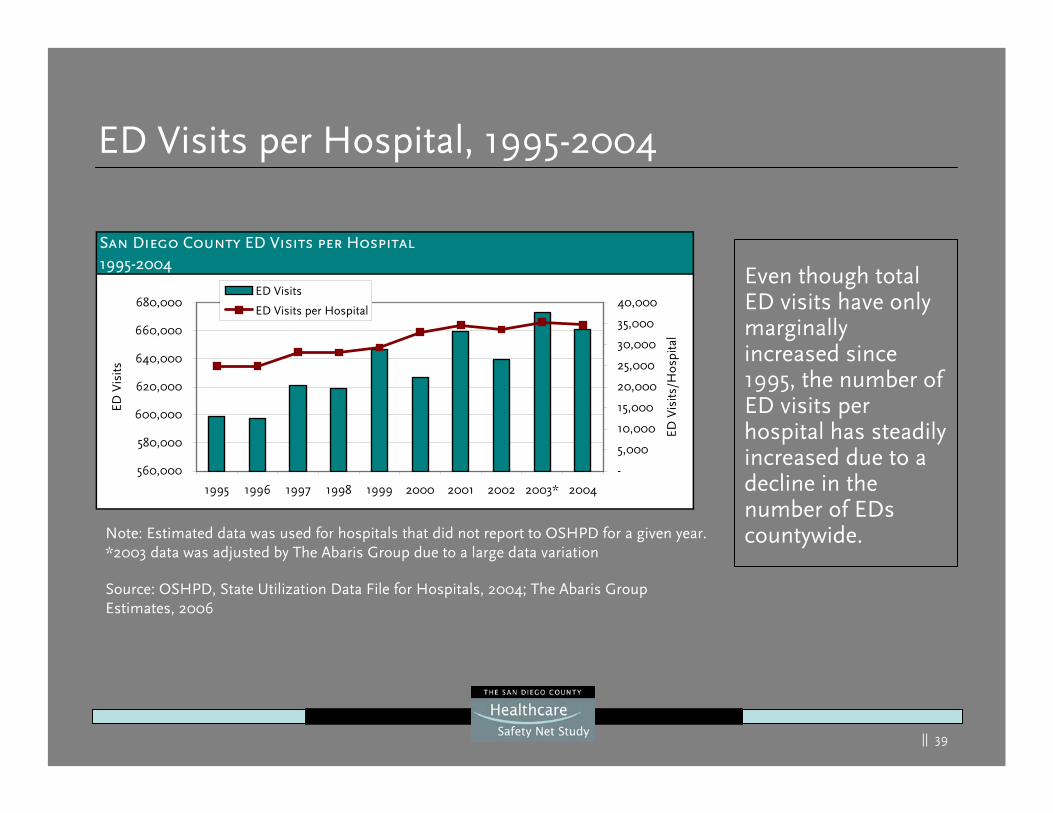

ED Visits per Hospital, 1995-2004

Even though total ED visits have only marginally increased since 1995, the number of ED visits per hospital has steadily increased due to a decline in the number of EDs countywide.Note: Estimated data was used for hospitals that did not report to OSHPD for a given year.

*2003 data was adjusted by The Abaris Group due to a large data variation

Source: OSHPD, State Utilization Data File for Hospitals, 2004; The Abaris Group Estimates, 2006

San Diego County ED Visits per Hospital1995-2004

560,000

580,000

600,000

620,000

640,000

660,000

680,000

1995 1996 1997 1998 1999 2000 2001 2002 2003* 2004

ED V

isits

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

ED V

isits

/Hos

pita

l

ED Visits

ED Visits per Hospital

|| 40

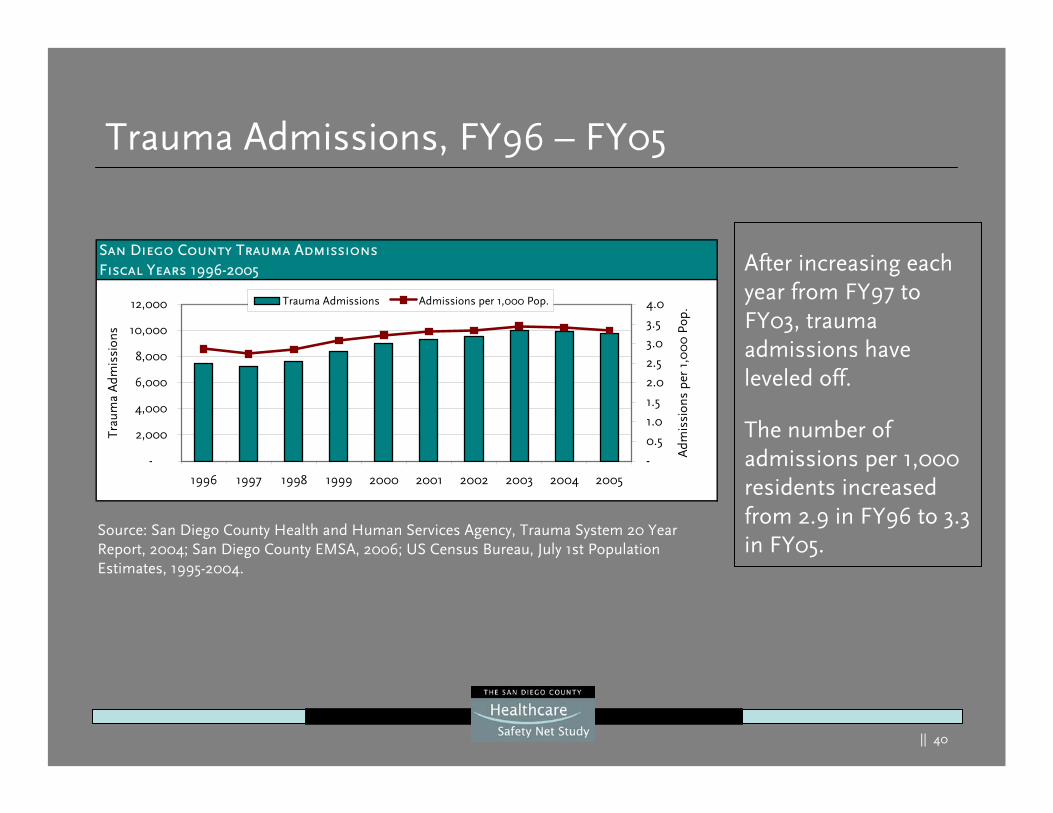

Trauma Admissions, FY96 – FY05

After increasing each year from FY97 to FY03, trauma admissions have leveled off.

The number of admissions per 1,000 residents increased from 2.9 in FY96 to 3.3 in FY05.

Source: San Diego County Health and Human Services Agency, Trauma System 20 Year Report, 2004; San Diego County EMSA, 2006; US Census Bureau, July 1st Population Estimates, 1995-2004.

San Diego County Trauma AdmissionsFiscal Years 1996-2005

-

2,000

4,000

6,000

8,000

10,000

12,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Trau

ma

Adm

issi

ons

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Adm

issi

ons

per

1,0

00

Pop

.Trauma Admissions Admissions per 1,000 Pop.

|| 41

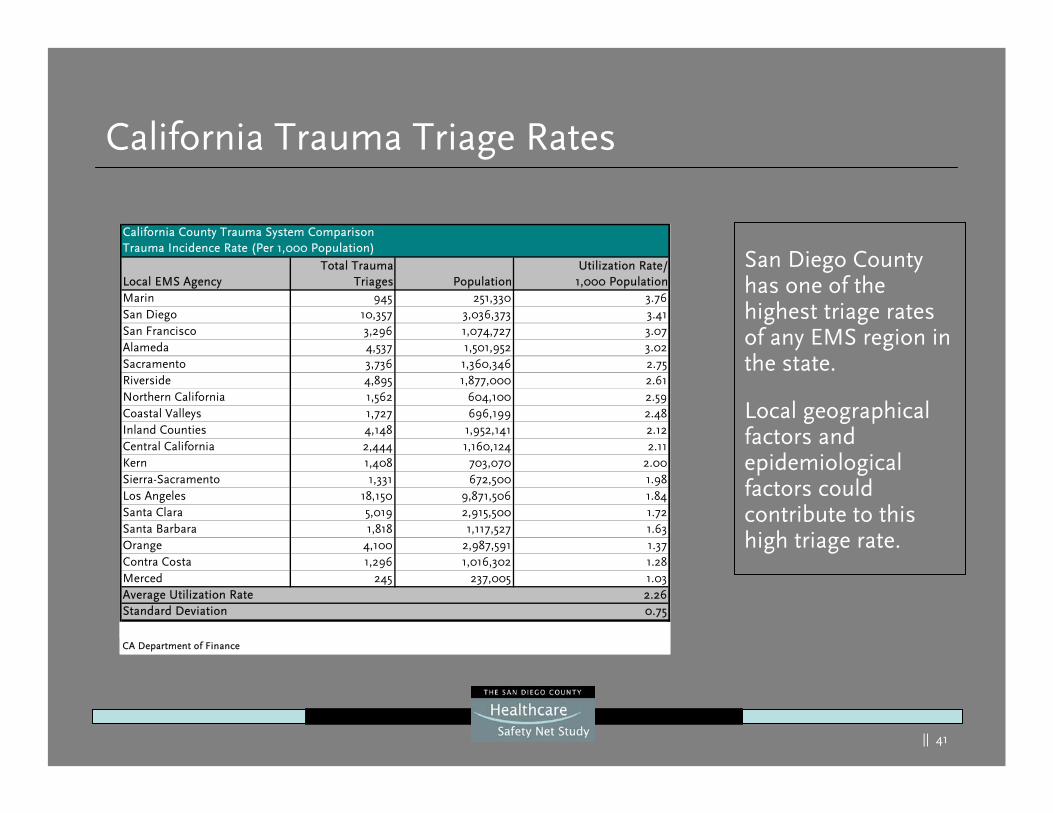

California Trauma Triage Rates

San Diego County has one of the highest triage rates of any EMS region in the state.

Local geographical factors and epidemiological factors could contribute to this high triage rate.

Marin 945 251,330 3.76San Diego 10,357 3,036,373 3.41San Francisco 3,296 1,074,727 3.07Alameda 4,537 1,501,952 3.02Sacramento 3,736 1,360,346 2.75Riverside 4,895 1,877,000 2.61Northern California 1,562 604,100 2.59Coastal Valleys 1,727 696,199 2.48Inland Counties 4,148 1,952,141 2.12Central California 2,444 1,160,124 2.11Kern 1,408 703,070 2.00Sierra-Sacramento 1,331 672,500 1.98Los Angeles 18,150 9,871,506 1.84Santa Clara 5,019 2,915,500 1.72Santa Barbara 1,818 1,117,527 1.63Orange 4,100 2,987,591 1.37Contra Costa 1,296 1,016,302 1.28Merced 245 237,005 1.03Average Utilization Rate 2.26Standard Deviation 0.75

California County Trauma System ComparisonTrauma Incidence Rate (Per 1,000 Population)

Local EMS AgencyTotal Trauma

Triages

CA Department of Finance

Source: 2005 The Abaris Group survey of Individual California local EMS agencies,

Utilization Rate/1,000 PopulationPopulation

|| 42

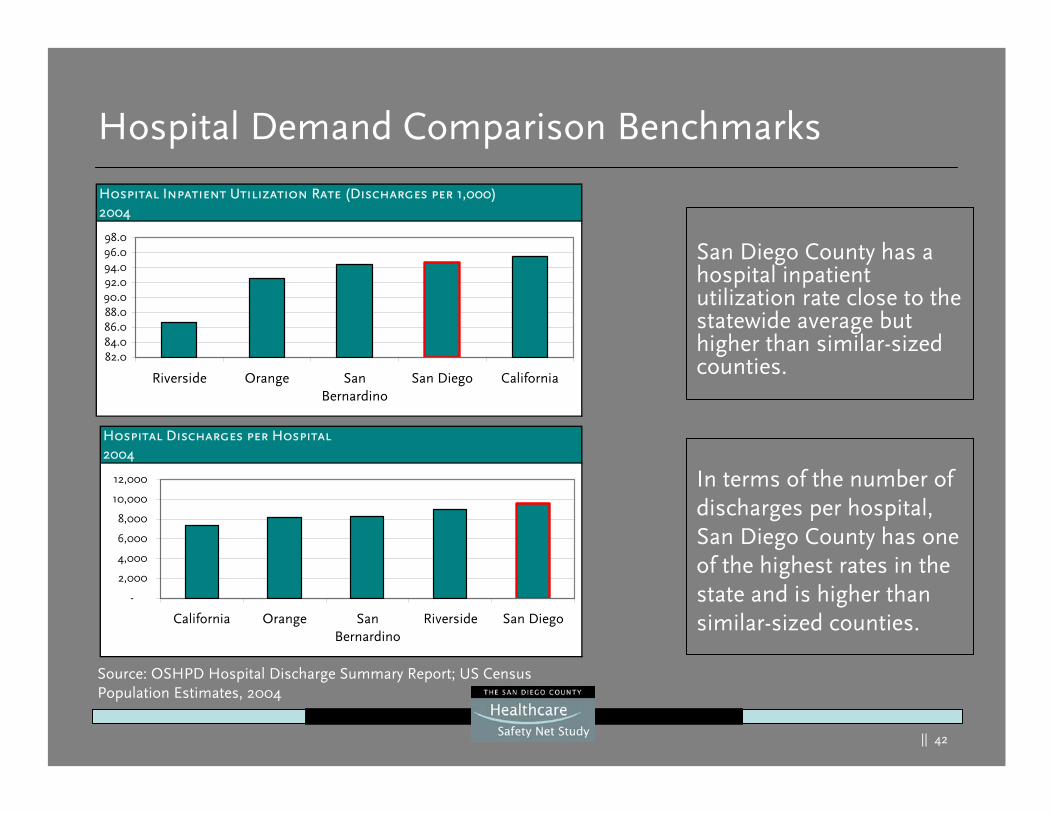

Hospital Demand Comparison Benchmarks

San Diego County has a hospital inpatient utilization rate close to the statewide average but higher than similar-sized counties.

In terms of the number of discharges per hospital, San Diego County has one of the highest rates in the state and is higher than similar-sized counties.

Source: OSHPD Hospital Discharge Summary Report; US Census Population Estimates, 2004

Hospital Inpatient Utilization Rate (Discharges per 1,000)2004

82.084.086.088.090.092.094.096.098.0

Riverside Orange SanBernardino

San Diego California

Hospital Discharges per Hospital2004

-

2,000

4,000

6,000

8,000

10,000

12,000

California Orange SanBernardino

Riverside San Diego

|| 43

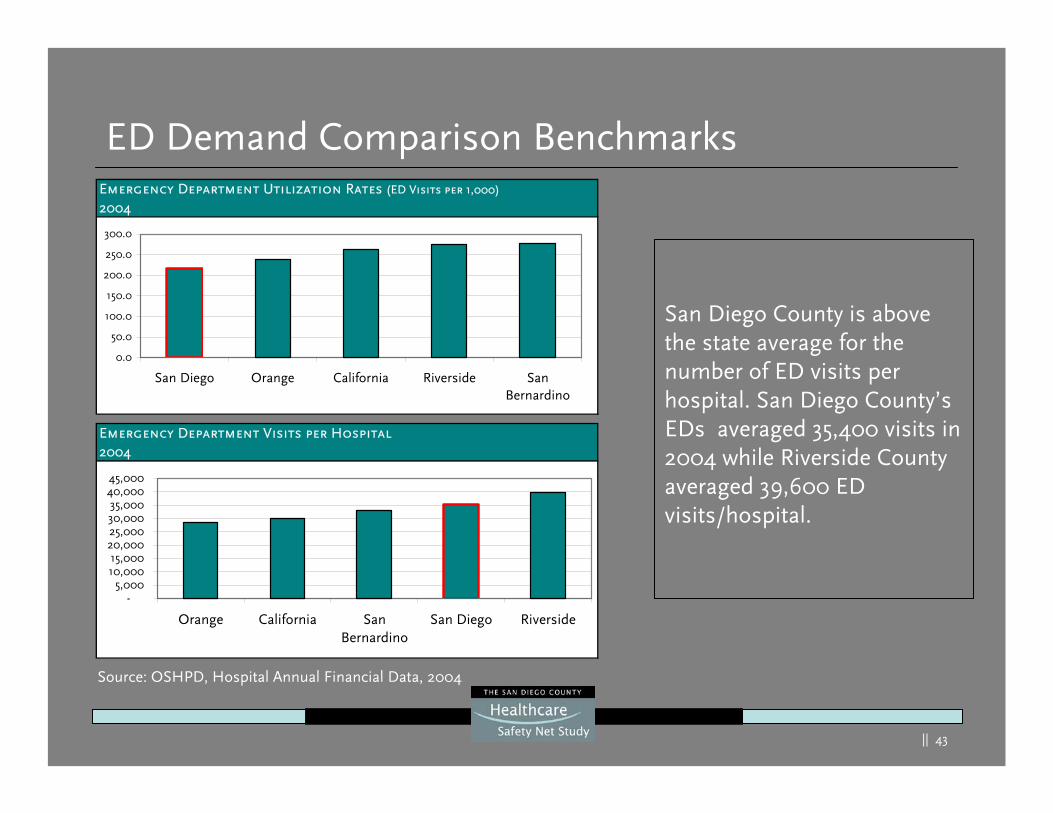

ED Demand Comparison Benchmarks

Source: OSHPD, Hospital Annual Financial Data, 2004

San Diego County is above the state average for the number of ED visits per hospital. San Diego County’s EDs averaged 35,400 visits in 2004 while Riverside County averaged 39,600 ED visits/hospital.

Emergency Department Visits per Hospital2004

-5,000

10,00015,000

20,00025,00030,00035,000

40,00045,000

Orange California SanBernardino

San Diego Riverside

Emergency Department Utilization Rates (ED Visits per 1,000)

2004

0.0

50.0

100.0

150.0

200.0

250.0

300.0

San Diego Orange California Riverside SanBernardino

|| 44

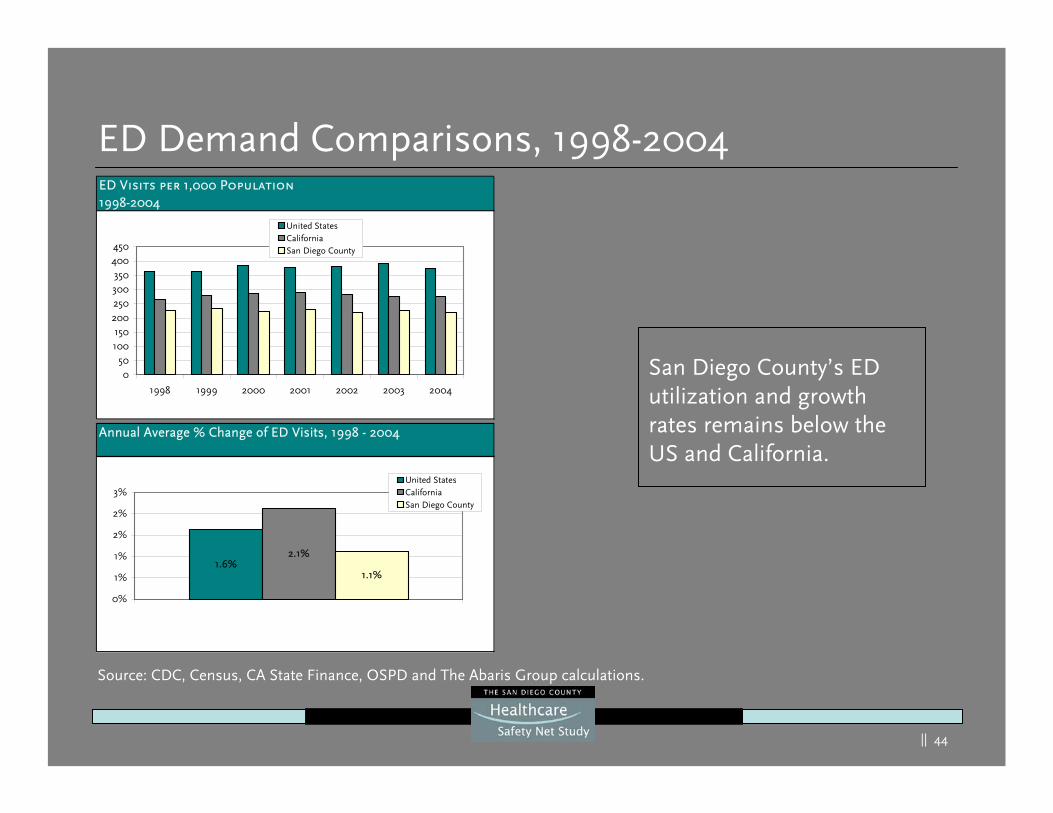

ED Demand Comparisons, 1998-2004ED Visits per 1,000 Population1998-2004

050

100150

200250300350

400450

1998 1999 2000 2001 2002 2003 2004

United StatesCaliforniaSan Diego County

Annual Average % Change of ED Visits, 1998 - 2004

1.6%2.1%

1.1%

0%

1%

1%

2%

2%

3%United StatesCaliforniaSan Diego County

San Diego County’s ED utilization and growth rates remains below the US and California.

Source: CDC, Census, CA State Finance, OSPD and The Abaris Group calculations.

|| 45

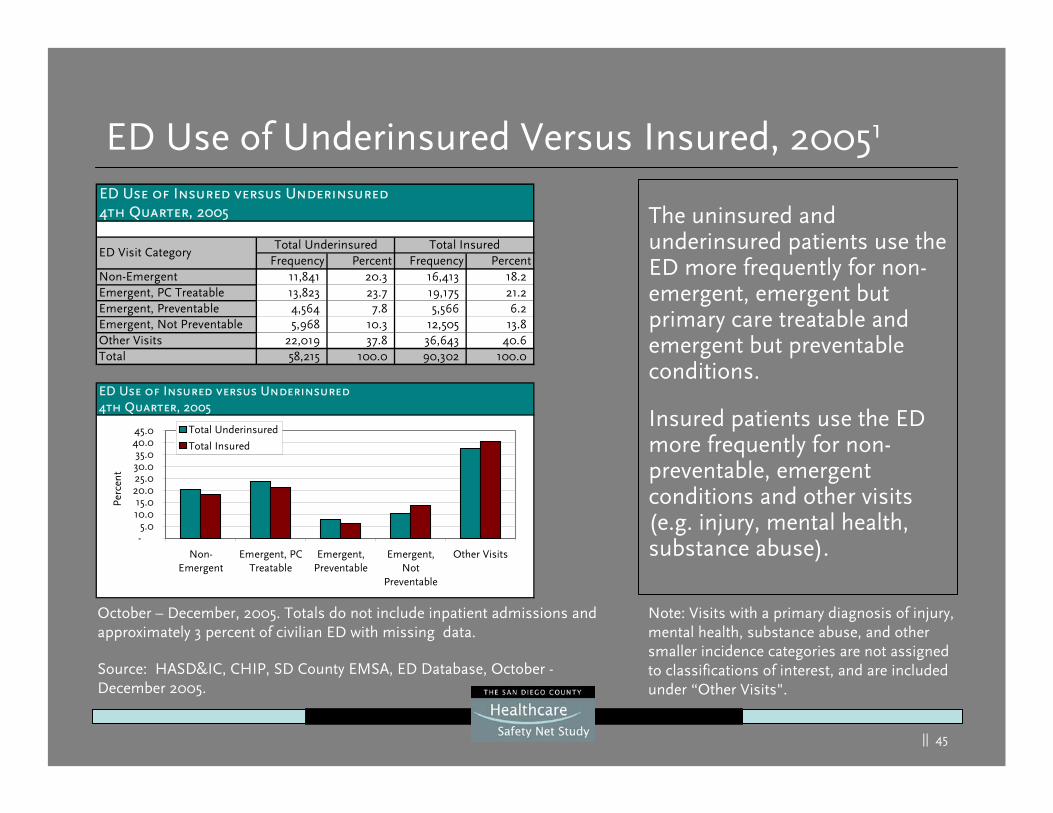

ED Use of Underinsured Versus Insured, 20051

ED Use of Insured versus Underinsured4th Quarter, 2005

Frequency Percent Frequency PercentNon-Emergent 11,841 20.3 16,413 18.2 Emergent, PC Treatable 13,823 23.7 19,175 21.2 Emergent, Preventable 4,564 7.8 5,566 6.2 Emergent, Not Preventable 5,968 10.3 12,505 13.8 Other Visits 22,019 37.8 36,643 40.6 Total 58,215 100.0 90,302 100.0

Total Underinsured Total InsuredED Visit Category

The uninsured and underinsured patients use the ED more frequently for non-emergent, emergent but primary care treatable and emergent but preventable conditions.

Insured patients use the ED more frequently for non-preventable, emergent conditions and other visits (e.g. injury, mental health, substance abuse).

Source: HASD&IC, CHIP, SD County EMSA, ED Database, October -December 2005.

October – December, 2005. Totals do not include inpatient admissions and approximately 3 percent of civilian ED with missing data.

ED Use of Insured versus Underinsured4th Quarter, 2005

-5.0

10.015.0

20.025.030.035.0

40.045.0

Non-Emergent

Emergent, PCTreatable

Emergent,Preventable

Emergent,Not

Preventable

Other Visits

Perc

ent

Total Underinsured

Total Insured

Note: Visits with a primary diagnosis of injury, mental health, substance abuse, and other smaller incidence categories are not assigned to classifications of interest, and are included under “Other Visits".

|| 46

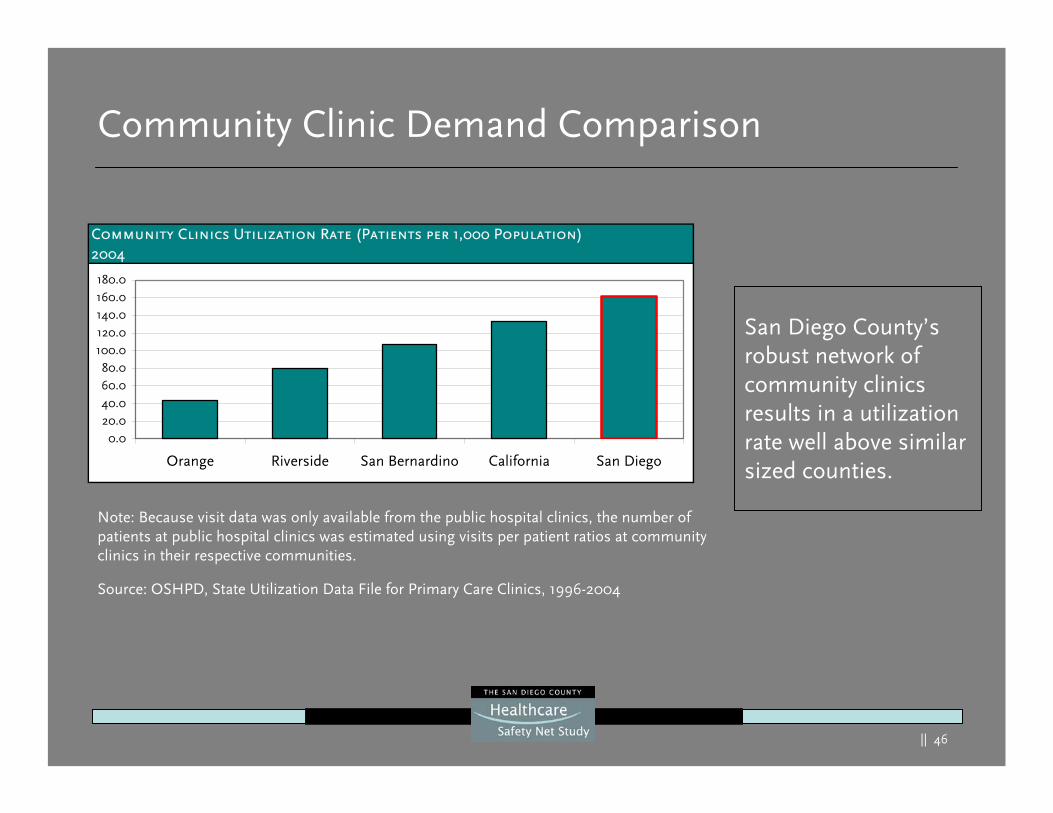

Community Clinic Demand Comparison

San Diego County’s robust network of community clinics results in a utilization rate well above similar sized counties.

Community Clinics Utilization Rate (Patients per 1,000 Population)2004

0.020.040.060.080.0

100.0120.0140.0160.0180.0

Orange Riverside San Bernardino California San Diego

Source: OSHPD, State Utilization Data File for Primary Care Clinics, 1996-2004

Note: Because visit data was only available from the public hospital clinics, the number of patients at public hospital clinics was estimated using visits per patient ratios at community clinics in their respective communities.

|| 47

Current Capacity

|| 48

Current Capacity Summary

San Diego:

Has more community clinics per 100,000 population than any othercounty in the state

Has more available hospital beds per 1,000 population than Riverside, San Bernardino and Orange Counties

Treats more patients per ED treatment station than San Bernardino and Orange Counties and has more ED bed capacity than the average for California and another comparable county, Riverside County

Has adequate physician coverage countywide with some regional and specialty gaps1

Is second to last in its nurse to population ratio compared to other California metropolitan counties

1 Not all physicians residing in San Diego County practice full time, are willing to see any or more safety net patients or make themselves available for hospital on-call services.

|| 49

Current Capacity Summary

Since 2001, San Diego County’s population has increased an average of 1.3 percent per year. Some areas of safety net capacity have also increased:

The number of community clinics has increased most years since 1996

The number of staffed hospital beds has risen since 1998

ED treatment stations have risen consistently since 2000

However, some areas of support have decreased:

Over the past 25 years, nine hospitals and one ED closed, resulting in the net total loss of 221 hospital beds and a gain of 128 ED treatment stations.

“Licensed” and “available” hospital beds have declined since 2000

|| 50

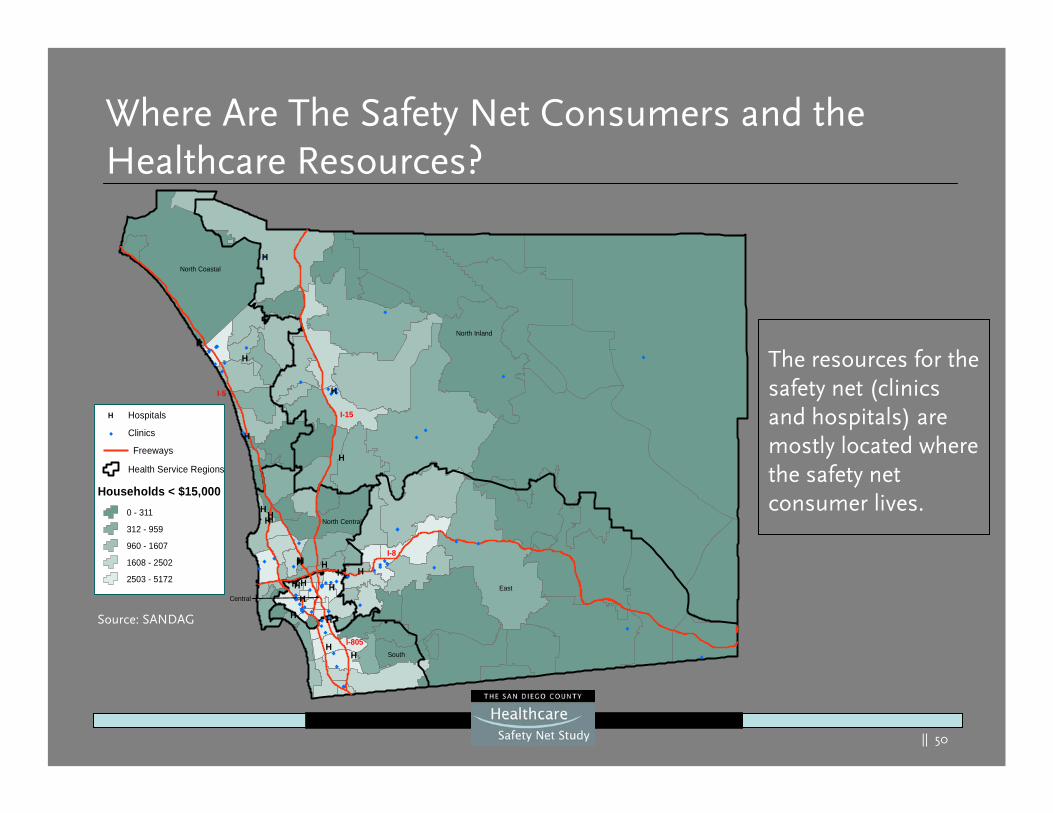

Where Are The Safety Net Consumers and the Healthcare Resources?

Source: SANDAG

H

H

H

H

H

HHHH

HHHH HHH

HHH HH

H H

HH

North Coastal

North Inland

North Central

East

South

Central

I-15

I-5

I-8

I-805

®

H Hospitals

Health Service Regions

Households < $15,000

Freeways

Clinics

0 - 311

312 - 959

960 - 1607

1608 - 2502

2503 - 5172

The resources for the safety net (clinics and hospitals) are mostly located where the safety net consumer lives.

Source: SANDAG

|| 51

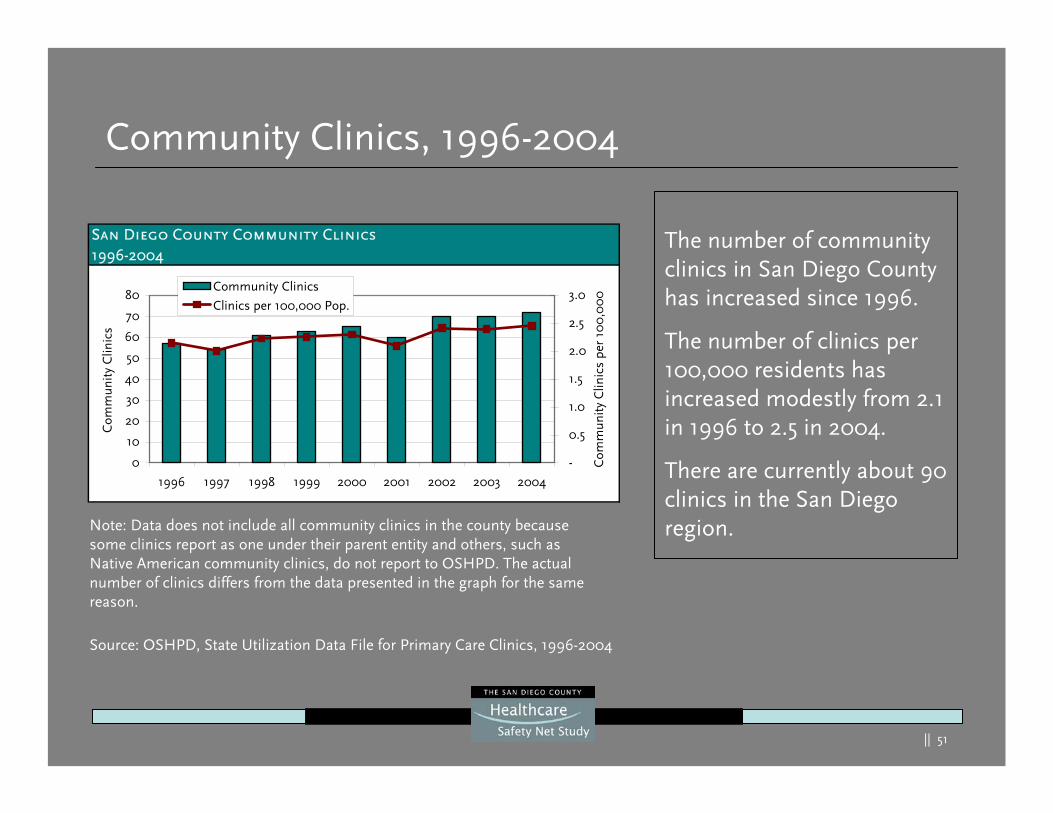

Community Clinics, 1996-2004

The number of community clinics in San Diego County has increased since 1996.

The number of clinics per 100,000 residents has increased modestly from 2.1 in 1996 to 2.5 in 2004.

There are currently about 90 clinics in the San Diego region.Note: Data does not include all community clinics in the county because

some clinics report as one under their parent entity and others, such as Native American community clinics, do not report to OSHPD. The actual number of clinics differs from the data presented in the graph for the same reason.

Source: OSHPD, State Utilization Data File for Primary Care Clinics, 1996-2004

San Diego County Community Clinics1996-2004

0

10

20

30

40

50

60

70

80

1996 1997 1998 1999 2000 2001 2002 2003 2004

Com

mun

ity

Clin

ics

-

0.5

1.0

1.5

2.0

2.5

3.0

Com

mun

ity C

linic

s pe

r 10

0,0

00

Community Clinics

Clinics per 100,000 Pop.

|| 52

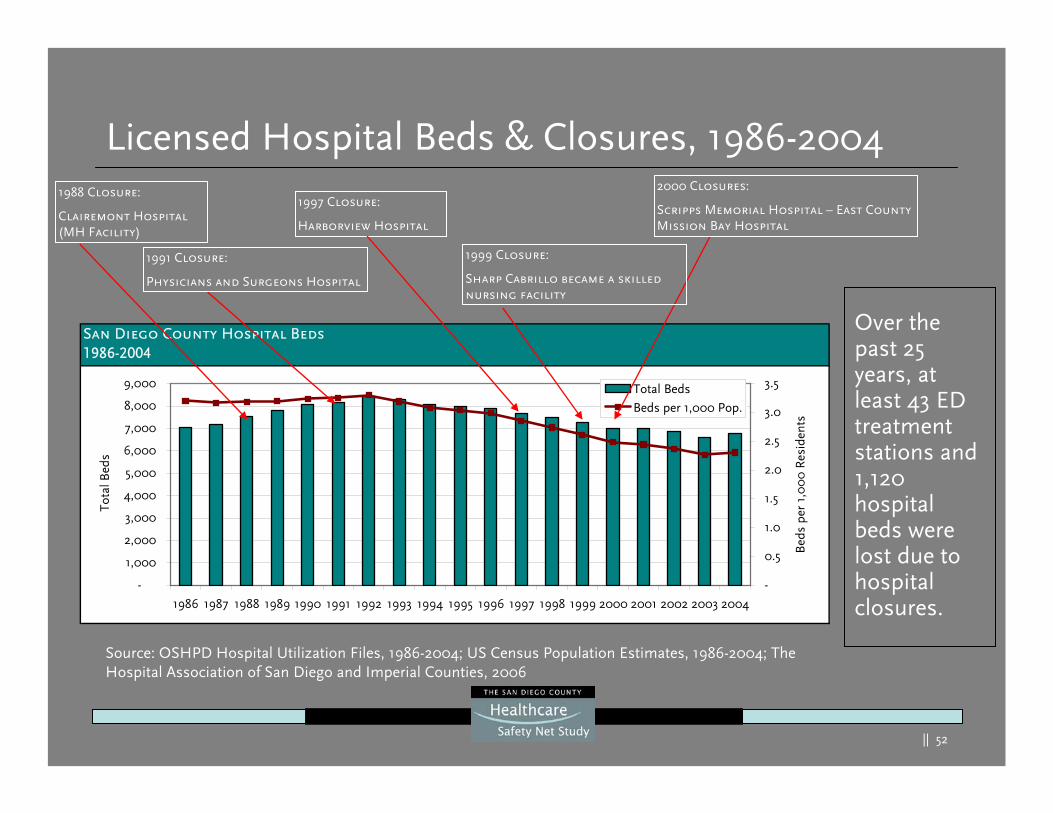

San Diego County Hospital Beds1986-2004

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Tot

al B

eds

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Bed

s pe

r 1,

00

0 R

esid

ents

Total Beds

Beds per 1,000 Pop.

Licensed Hospital Beds & Closures, 1986-20041988 Closure:

Clairemont Hospital (MH Facility)

1997 Closure:

Harborview Hospital

1991 Closure:

Physicians and Surgeons Hospital

2000 Closures:

Scripps Memorial Hospital – East CountyMission Bay Hospital

Source: OSHPD Hospital Utilization Files, 1986-2004; US Census Population Estimates, 1986-2004; The Hospital Association of San Diego and Imperial Counties, 2006

Over the past 25 years, at least 43 ED treatment stations and 1,120 hospital beds were lost due to hospital closures.

1999 Closure:

Sharp Cabrillo became a skilled nursing facility

|| 53

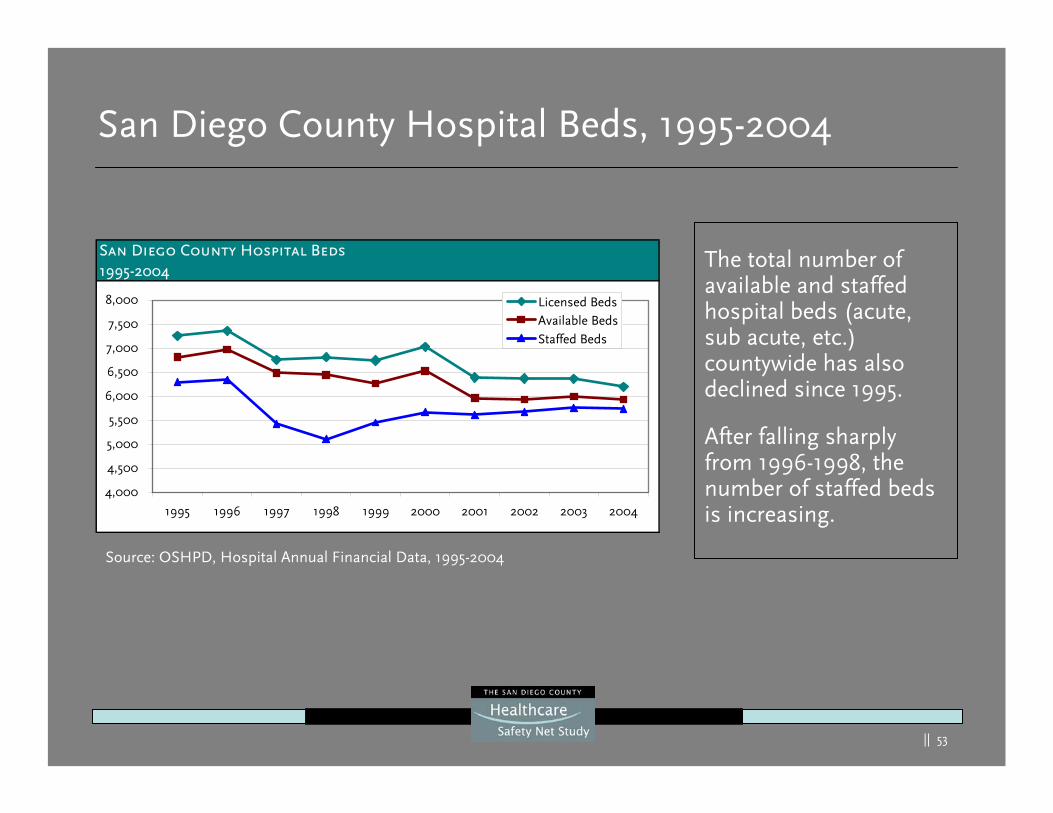

San Diego County Hospital Beds, 1995-2004

The total number of available and staffed hospital beds (acute, sub acute, etc.) countywide has also declined since 1995.

After falling sharply from 1996-1998, the number of staffed beds is increasing.

Source: OSHPD, Hospital Annual Financial Data, 1995-2004

San Diego County Hospital Beds1995-2004

4,000

4,500

5,000

5,500

6,000

6,500

7,000

7,500

8,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Licensed BedsAvailable BedsStaffed Beds

|| 54

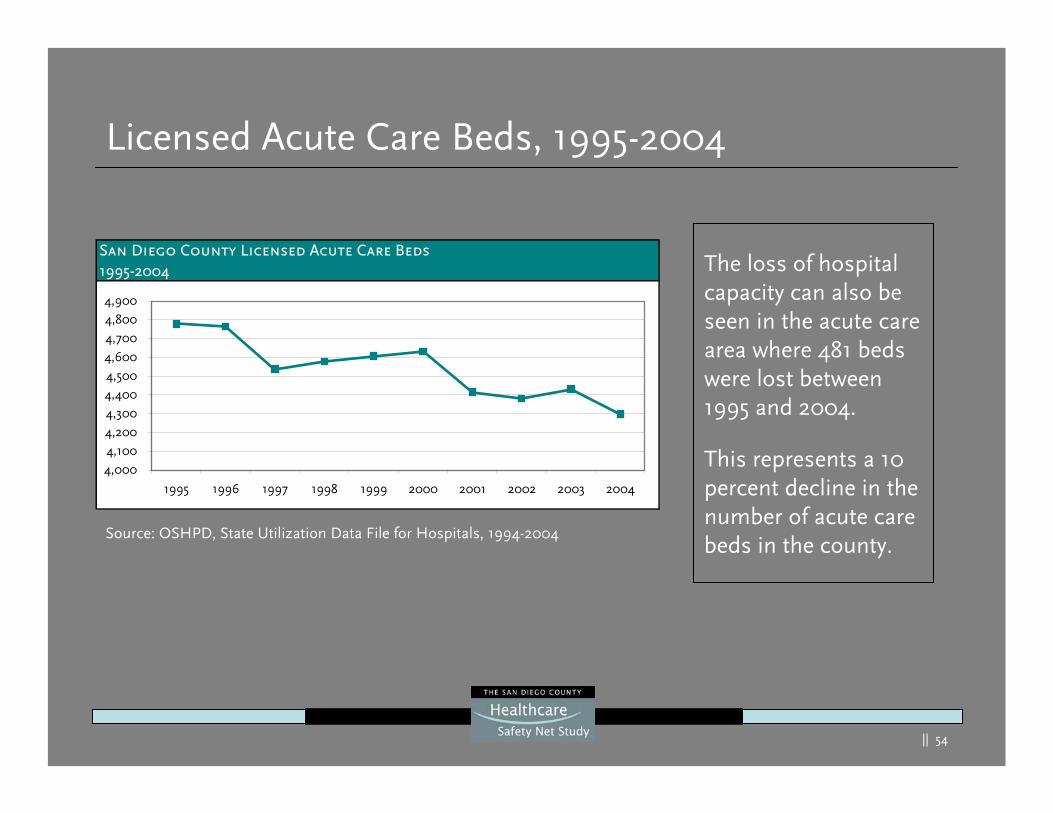

Licensed Acute Care Beds, 1995-2004

The loss of hospital capacity can also be seen in the acute care area where 481 beds were lost between 1995 and 2004.

This represents a 10 percent decline in the number of acute care beds in the county.

Source: OSHPD, State Utilization Data File for Hospitals, 1994-2004

San Diego County Licensed Acute Care Beds1995-2004

4,000

4,100

4,200

4,300

4,400

4,500

4,600

4,7004,800

4,900

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

|| 55

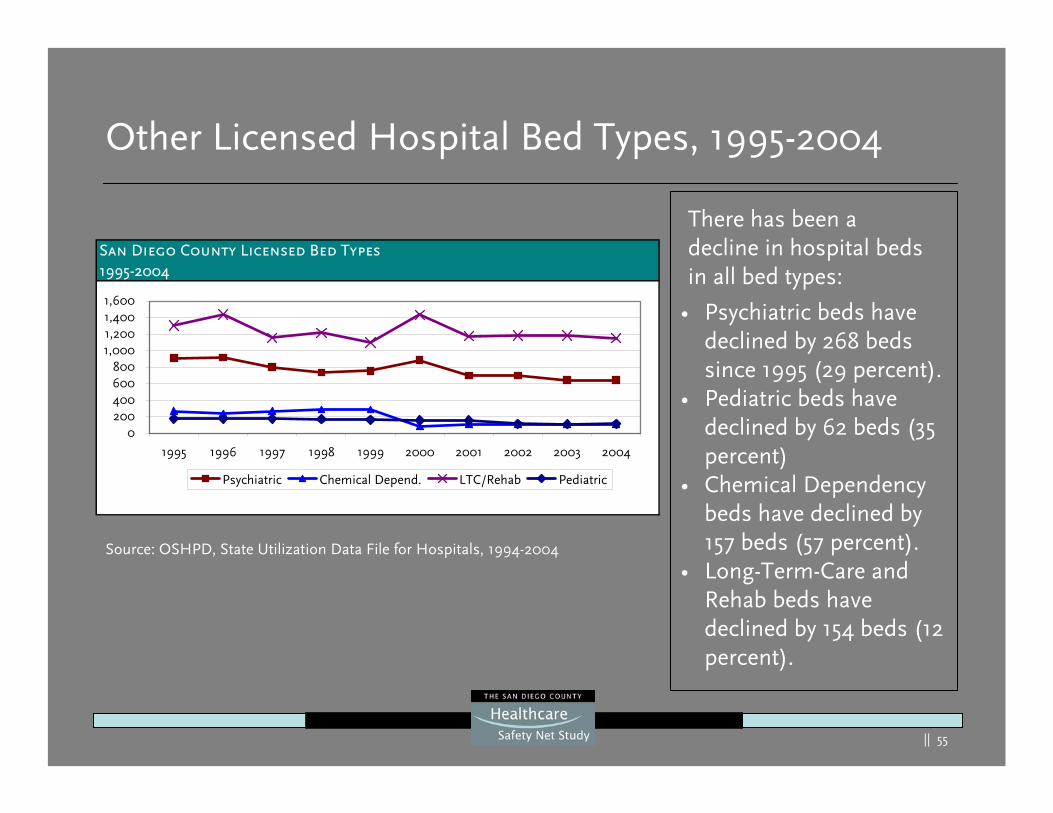

Other Licensed Hospital Bed Types, 1995-2004

Source: OSHPD, State Utilization Data File for Hospitals, 1994-2004

San Diego County Licensed Bed Types1995-2004

0200400600800

1,0001,2001,4001,600

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Psychiatric Chemical Depend. LTC/Rehab Pediatric

• Psychiatric beds have declined by 268 beds since 1995 (29 percent).

• Pediatric beds have declined by 62 beds (35 percent)

• Chemical Dependency beds have declined by 157 beds (57 percent).

• Long-Term-Care and Rehab beds have declined by 154 beds (12 percent).

There has been a decline in hospital beds in all bed types:

|| 56

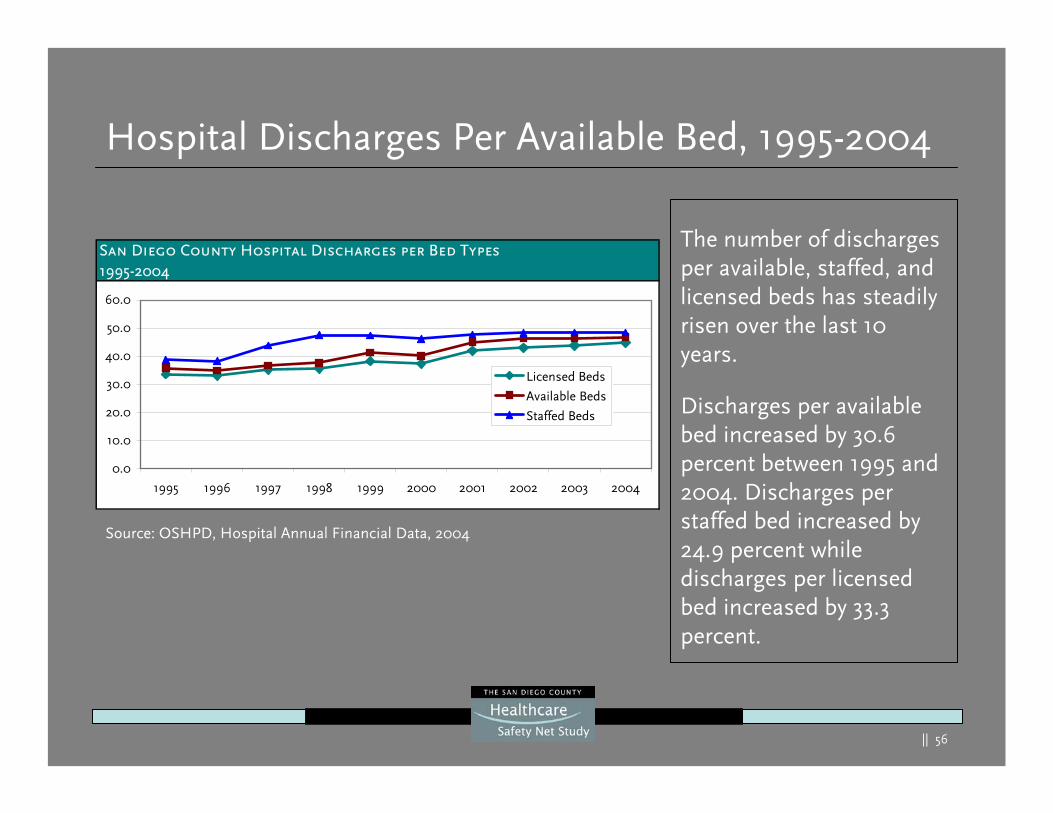

Hospital Discharges Per Available Bed, 1995-2004

The number of discharges per available, staffed, and licensed beds has steadily risen over the last 10 years.

Discharges per available bed increased by 30.6 percent between 1995 and 2004. Discharges per staffed bed increased by 24.9 percent while discharges per licensed bed increased by 33.3 percent.

Source: OSHPD, Hospital Annual Financial Data, 2004

San Diego County Hospital Discharges per Bed Types1995-2004

0.0

10.0

20.0

30.0

40.0

50.0

60.0

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Licensed Beds

Available Beds

Staffed Beds

|| 57

San Diego County ED Stations1995-2004

-50

100150

200250300350

400450

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

ED S

tatio

ns

-

5.0

10.0

15.0

20.0

25.0

Stat

ions

/Hos

pita

l

ED StationsStations per Hospital

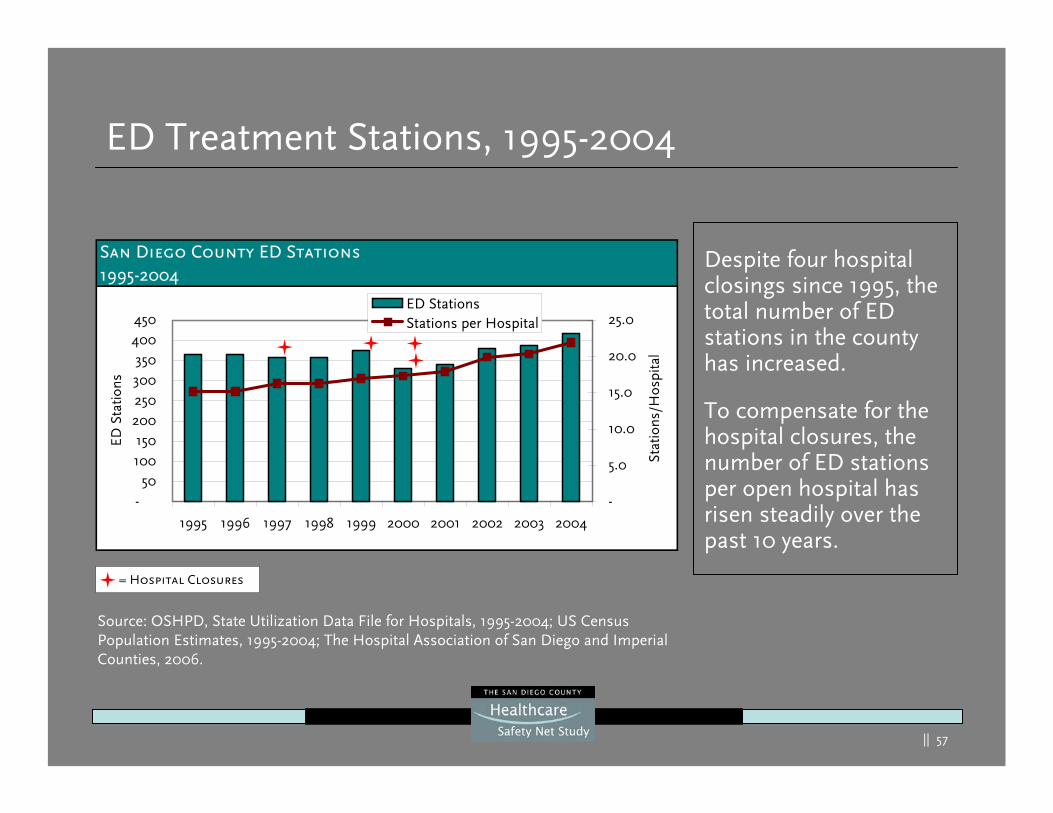

ED Treatment Stations, 1995-2004

= Hospital Closures

Source: OSHPD, State Utilization Data File for Hospitals, 1995-2004; US Census Population Estimates, 1995-2004; The Hospital Association of San Diego and Imperial Counties, 2006.

Despite four hospital closings since 1995, the total number of ED stations in the county has increased.

To compensate for the hospital closures, the number of ED stations per open hospital has risen steadily over the past 10 years.

|| 58

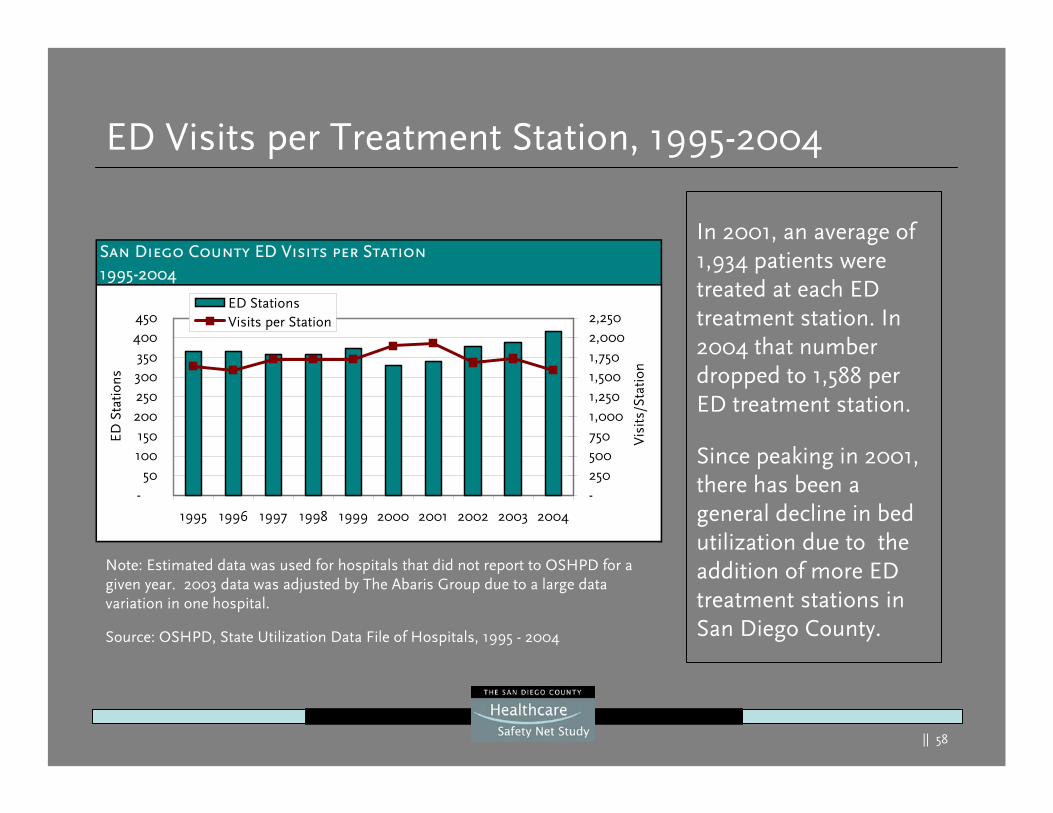

ED Visits per Treatment Station, 1995-2004

Note: Estimated data was used for hospitals that did not report to OSHPD for a given year. 2003 data was adjusted by The Abaris Group due to a large data variation in one hospital.

In 2001, an average of 1,934 patients were treated at each ED treatment station. In 2004 that number dropped to 1,588 per ED treatment station.

Since peaking in 2001, there has been a general decline in bed utilization due to the addition of more ED treatment stations in San Diego County.

San Diego County ED Visits per Station1995-2004

-50

100150

200250300350

400450

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

ED S

tatio

ns

-2505007501,0001,2501,5001,7502,0002,250

Vis

its/S

tatio

n

ED StationsVisits per Station

Source: OSHPD, State Utilization Data File of Hospitals, 1995 - 2004

|| 59

Hospital Capacity Comparison

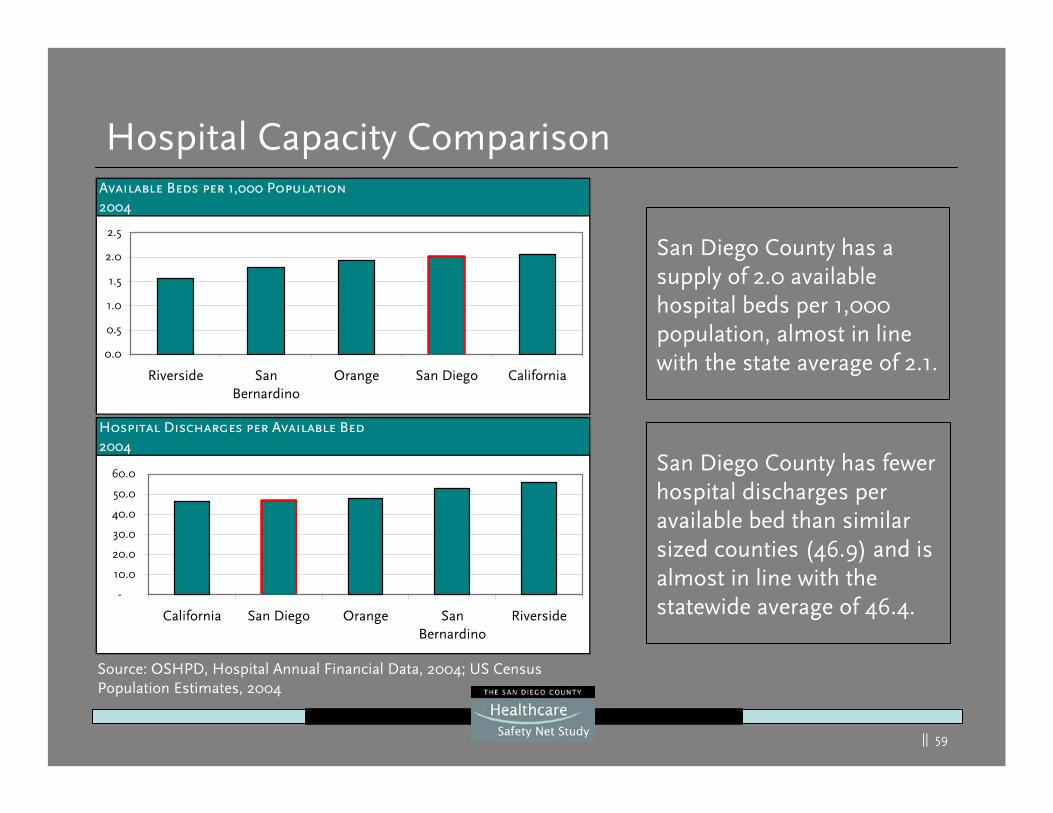

San Diego County has a supply of 2.0 available hospital beds per 1,000 population, almost in line with the state average of 2.1.

Source: OSHPD, Hospital Annual Financial Data, 2004; US Census Population Estimates, 2004

San Diego County has fewer hospital discharges per available bed than similar sized counties (46.9) and is almost in line with the statewide average of 46.4.

Available Beds per 1,000 Population2004

0.0

0.5

1.0

1.5

2.0

2.5

Riverside SanBernardino

Orange San Diego California

Hospital Discharges per Available Bed2004

-

10.0

20.0

30.0

40.0

50.0

60.0

California San Diego Orange SanBernardino

Riverside

|| 60

ED Capacity Comparison

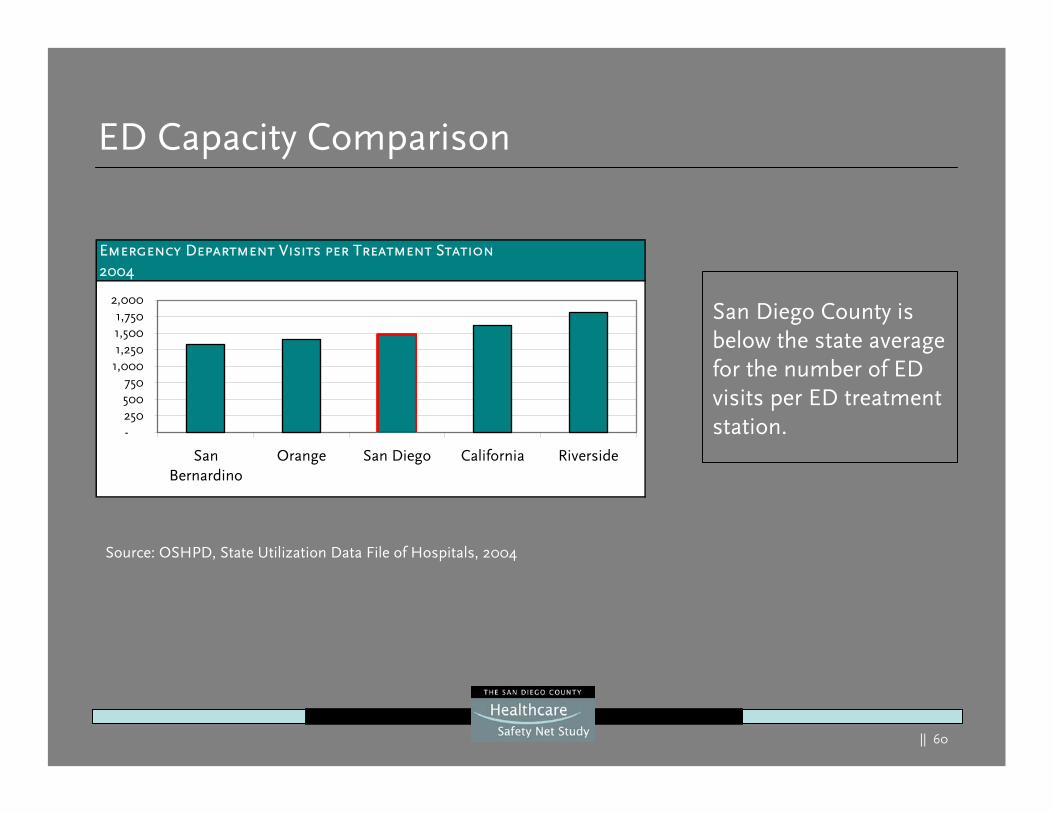

San Diego County is below the state average for the number of ED visits per ED treatment station.

Source: OSHPD, State Utilization Data File of Hospitals, 2004

Emergency Department Visits per Treatment Station2004

-250500750

1,0001,2501,5001,750

2,000

SanBernardino

Orange San Diego California Riverside

|| 61

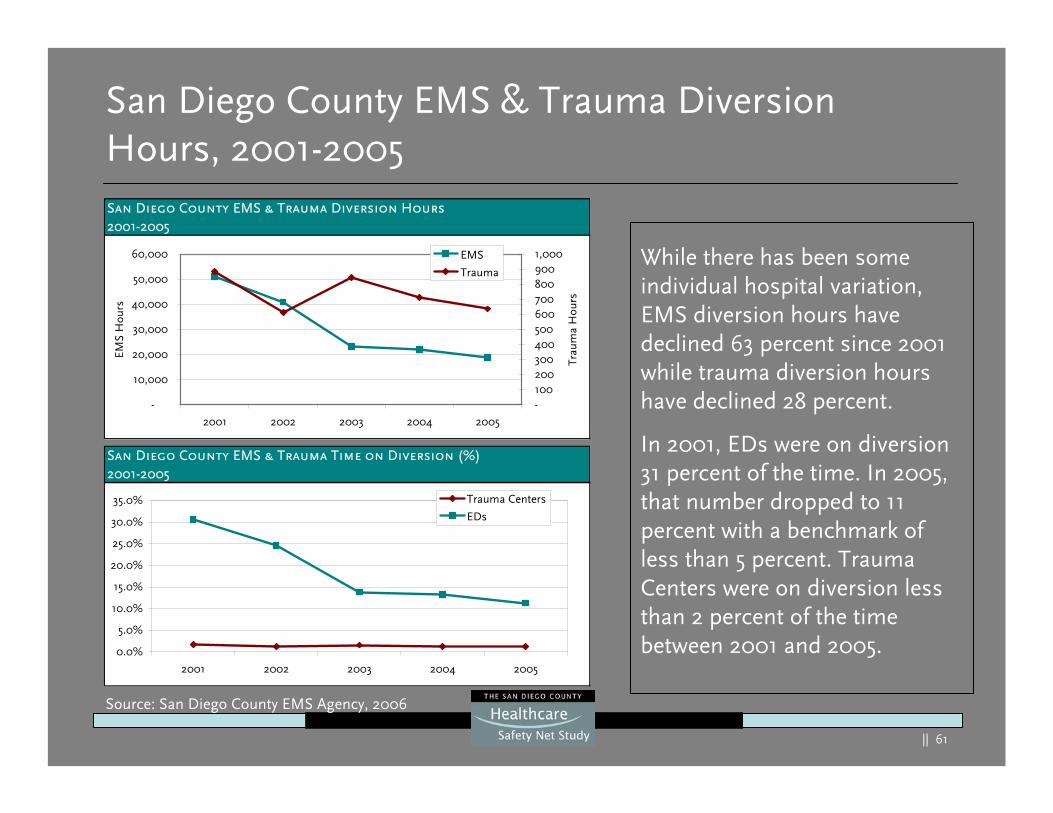

San Diego County EMS & Trauma Diversion Hours, 2001-2005

While there has been some individual hospital variation, EMS diversion hours have declined 63 percent since 2001 while trauma diversion hours have declined 28 percent.

In 2001, EDs were on diversion 31 percent of the time. In 2005, that number dropped to 11 percent with a benchmark of less than 5 percent. Trauma Centers were on diversion less than 2 percent of the time between 2001 and 2005.

Source: San Diego County EMS Agency, 2006

San Diego County EMS & Trauma Diversion Hours2001-2005

-

10,000

20,000

30,000

40,000

50,000

60,000

2001 2002 2003 2004 2005

EMS

Hou

rs

-1002003004005006007008009001,000

Trau

ma

Hou

rs

EMS

Trauma

San Diego County EMS & Trauma Time on Diversion (%)2001-2005

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

2001 2002 2003 2004 2005

Trauma Centers

EDs

|| 62

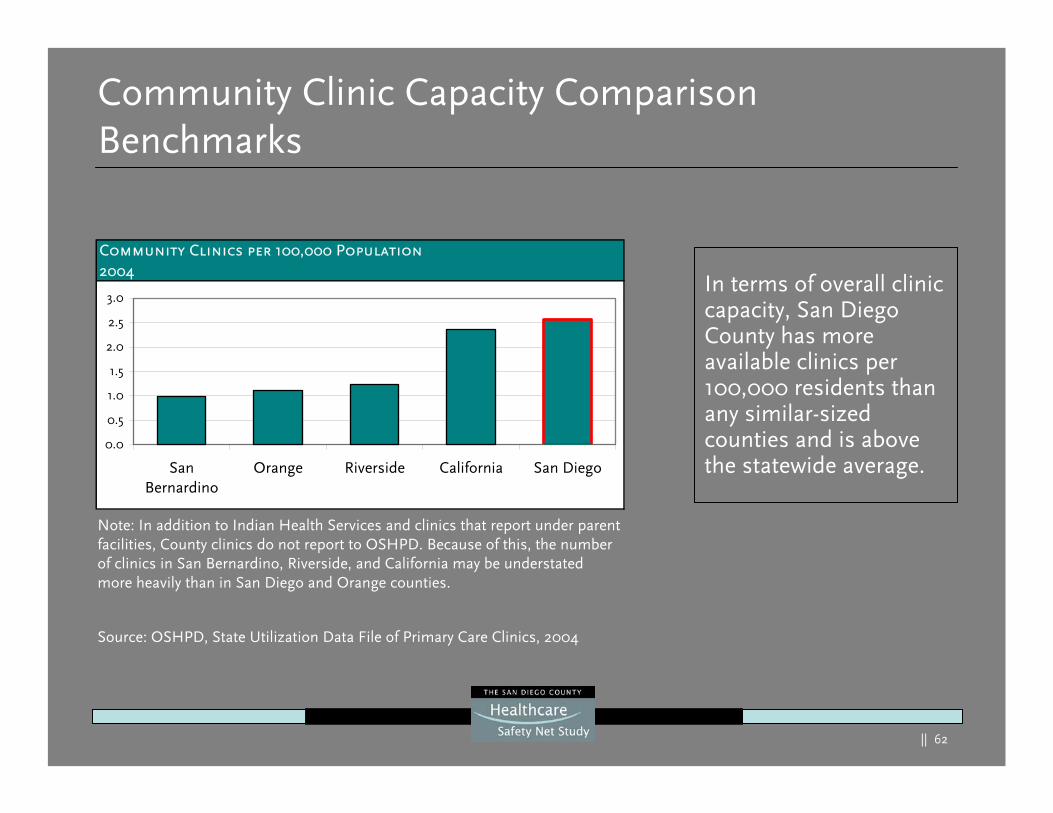

Community Clinic Capacity Comparison Benchmarks

In terms of overall clinic capacity, San Diego County has more available clinics per 100,000 residents than any similar-sized counties and is above the statewide average.

Source: OSHPD, State Utilization Data File of Primary Care Clinics, 2004

Note: In addition to Indian Health Services and clinics that report under parent facilities, County clinics do not report to OSHPD. Because of this, the number of clinics in San Bernardino, Riverside, and California may be understated more heavily than in San Diego and Orange counties.

Community Clinics per 100,000 Population2004

0.0

0.5

1.0

1.5

2.0

2.5

3.0

SanBernardino

Orange Riverside California San Diego

|| 63

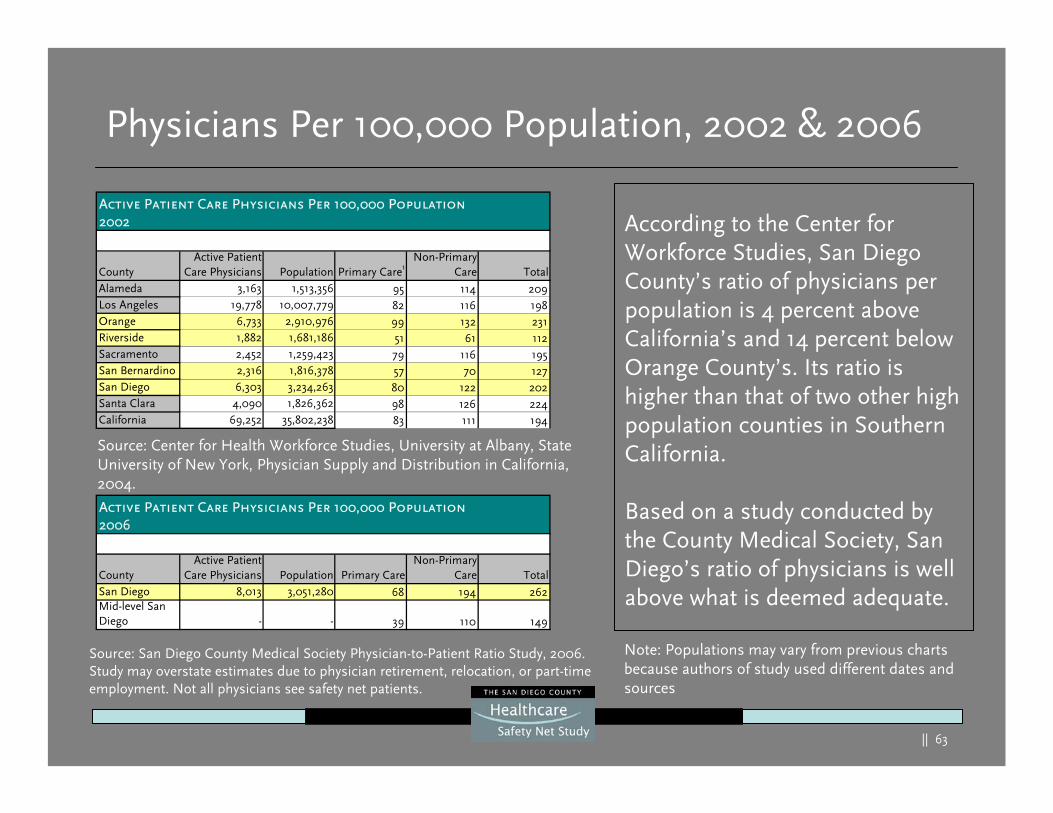

Physicians Per 100,000 Population, 2002 & 2006

According to the Center for Workforce Studies, San Diego County’s ratio of physicians per population is 4 percent above California’s and 14 percent below Orange County’s. Its ratio is higher than that of two other high population counties in Southern California.

Based on a study conducted by the County Medical Society, San Diego’s ratio of physicians is well above what is deemed adequate.

CountyActive Patient

Care Physicians Population Primary Care1Non-Primary

Care TotalAlameda 3,163 1,513,356 95 114 209Los Angeles 19,778 10,007,779 82 116 198Orange 6,733 2,910,976 99 132 231Riverside 1,882 1,681,186 51 61 112Sacramento 2,452 1,259,423 79 116 195San Bernardino 2,316 1,816,378 57 70 127San Diego 6,303 3,234,263 80 122 202Santa Clara 4,090 1,826,362 98 126 224California 69,252 35,802,238 83 111 194

Active Patient Care Physicians Per 100,000 Population2002

CountyActive Patient

Care Physicians Population Primary CareNon-Primary

Care TotalSan Diego 8,013 3,051,280 68 194 262Mid-level San Diego - - 39 110 149

Active Patient Care Physicians Per 100,000 Population2006

Source: Center for Health Workforce Studies, University at Albany, State University of New York, Physician Supply and Distribution in California, 2004.

Source: San Diego County Medical Society Physician-to-Patient Ratio Study, 2006. Study may overstate estimates due to physician retirement, relocation, or part-time employment. Not all physicians see safety net patients.

Note: Populations may vary from previous charts because authors of study used different dates and sources

|| 64

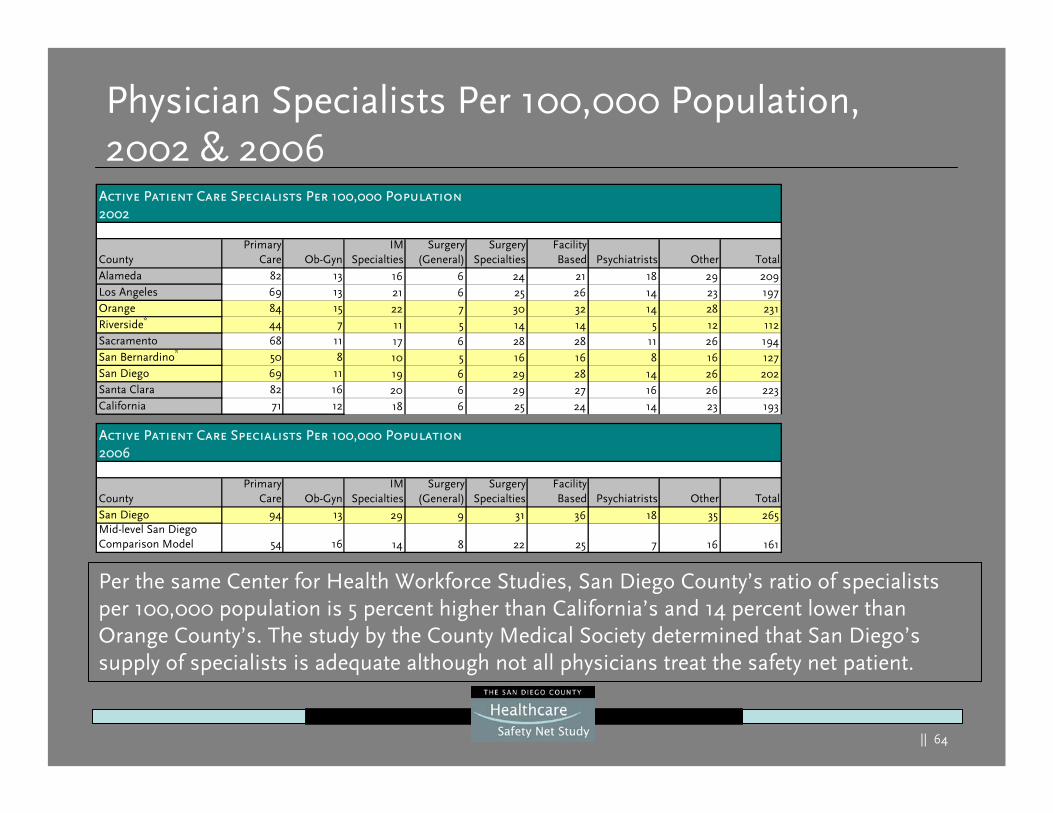

Physician Specialists Per 100,000 Population, 2002 & 2006

Per the same Center for Health Workforce Studies, San Diego County’s ratio of specialists per 100,000 population is 5 percent higher than California’s and 14 percent lower than Orange County’s. The study by the County Medical Society determined that San Diego’s supply of specialists is adequate although not all physicians treat the safety net patient.

CountyPrimary

Care Ob-GynIM

SpecialtiesSurgery

(General)Surgery

SpecialtiesFacilityBased Psychiatrists Other Total

San Diego 94 13 29 9 31 36 18 35 265Mid-level San Diego Comparison Model 54 16 14 8 22 25 7 16 161

Active Patient Care Specialists Per 100,000 Population2006

CountyPrimary

Care Ob-GynIM

SpecialtiesSurgery

(General)Surgery

SpecialtiesFacilityBased Psychiatrists Other Total

Alameda 82 13 16 6 24 21 18 29 209Los Angeles 69 13 21 6 25 26 14 23 197Orange 84 15 22 7 30 32 14 28 231Riverside* 44 7 11 5 14 14 5 12 112Sacramento 68 11 17 6 28 28 11 26 194San Bernardino* 50 8 10 5 16 16 8 16 127San Diego 69 11 19 6 29 28 14 26 202Santa Clara 82 16 20 6 29 27 16 26 223California 71 12 18 6 25 24 14 23 193

Active Patient Care Specialists Per 100,000 Population2002

|| 65

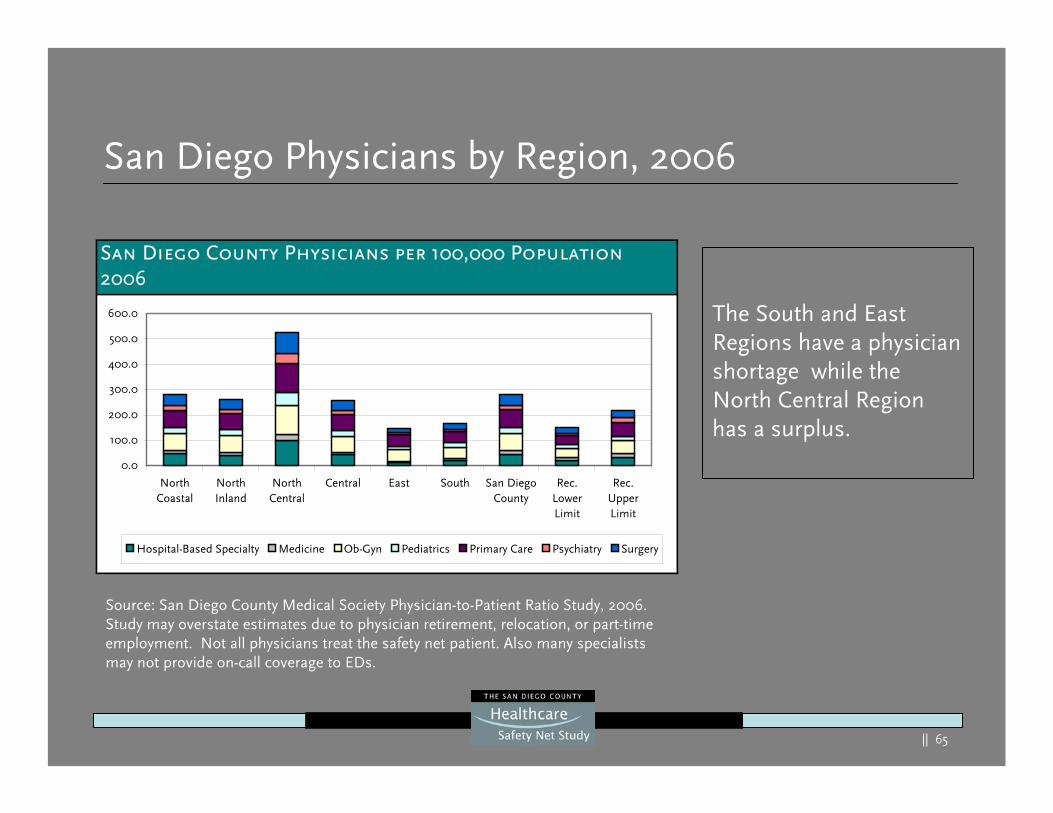

San Diego Physicians by Region, 2006

The South and East Regions have a physician shortage while the North Central Region has a surplus.

San Diego County Physicians per 100,000 Population2006

0.0

100.0

200.0

300.0

400.0

500.0

600.0

NorthCoastal

NorthInland

NorthCentral

Central East South San DiegoCounty

Rec.LowerLimit

Rec.UpperLimit

Hospital-Based Specialty Medicine Ob-Gyn Pediatrics Primary Care Psychiatry Surgery

Source: San Diego County Medical Society Physician-to-Patient Ratio Study, 2006. Study may overstate estimates due to physician retirement, relocation, or part-time employment. Not all physicians treat the safety net patient. Also many specialists may not provide on-call coverage to EDs.

|| 66

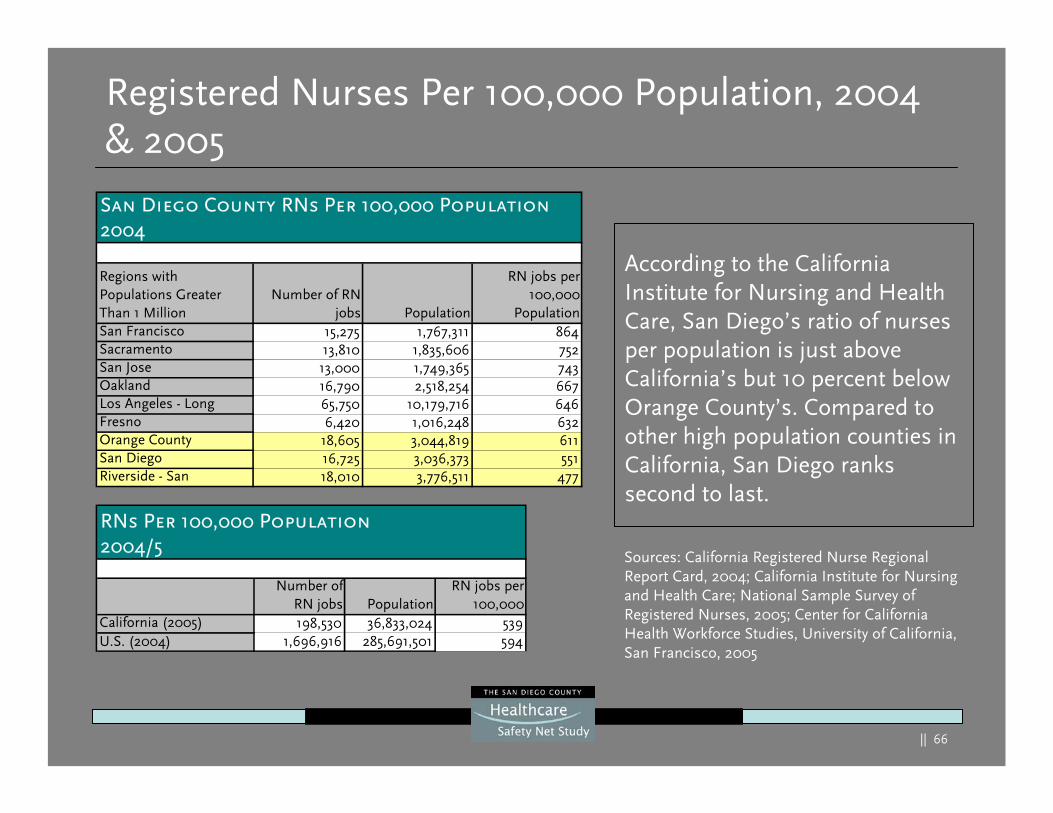

Registered Nurses Per 100,000 Population, 2004 & 2005

According to the California Institute for Nursing and Health Care, San Diego’s ratio of nurses per population is just above California’s but 10 percent below Orange County’s. Compared to other high population counties in California, San Diego ranks second to last.

Number ofRN jobs Population

RN jobs per100,000

California (2005) 198,530 36,833,024 539U.S. (2004) 1,696,916 285,691,501 594

RNs Per 100,000 Population2004/5

Regions with Populations Greater Than 1 Million

Number of RNjobs Population

RN jobs per100,000

PopulationSan Francisco 15,275 1,767,311 864Sacramento 13,810 1,835,606 752San Jose 13,000 1,749,365 743Oakland 16,790 2,518,254 667Los Angeles - Long 65,750 10,179,716 646Fresno 6,420 1,016,248 632Orange County 18,605 3,044,819 611San Diego 16,725 3,036,373 551Riverside - San 18,010 3,776,511 477

San Diego County RNs Per 100,000 Population2004

Sources: California Registered Nurse Regional Report Card, 2004; California Institute for Nursing and Health Care; National Sample Survey of Registered Nurses, 2005; Center for California Health Workforce Studies, University of California, San Francisco, 2005

|| 67

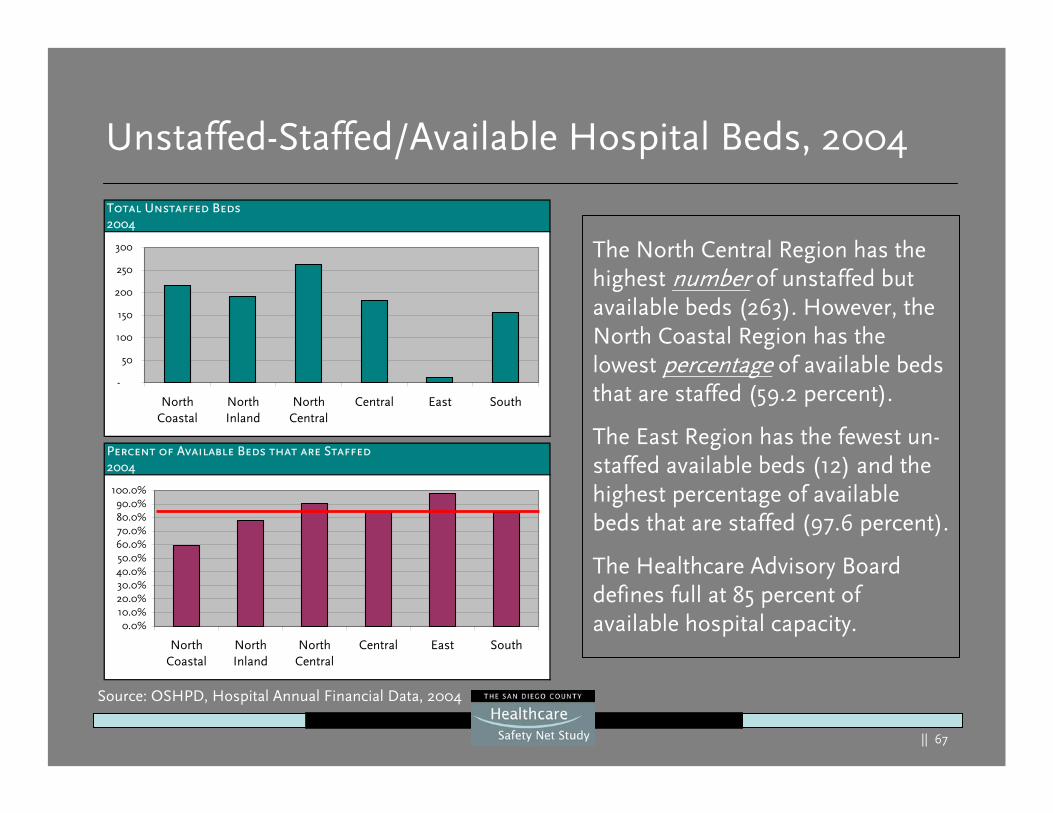

Unstaffed-Staffed/Available Hospital Beds, 2004

Total Unstaffed Beds2004

-

50

100

150

200

250

300

NorthCoastal

NorthInland

NorthCentral

Central East South

Percent of Available Beds that are Staffed2004

0.0%10.0%20.0%30.0%40.0%50.0%60.0%70.0%80.0%90.0%

100.0%

NorthCoastal

NorthInland

NorthCentral

Central East South

The North Central Region has the highest number of unstaffed but available beds (263). However, the North Coastal Region has the lowest percentage of available beds that are staffed (59.2 percent).

The East Region has the fewest un-staffed available beds (12) and the highest percentage of available beds that are staffed (97.6 percent).

The Healthcare Advisory Board defines full at 85 percent of available hospital capacity.

Source: OSHPD, Hospital Annual Financial Data, 2004

|| 68

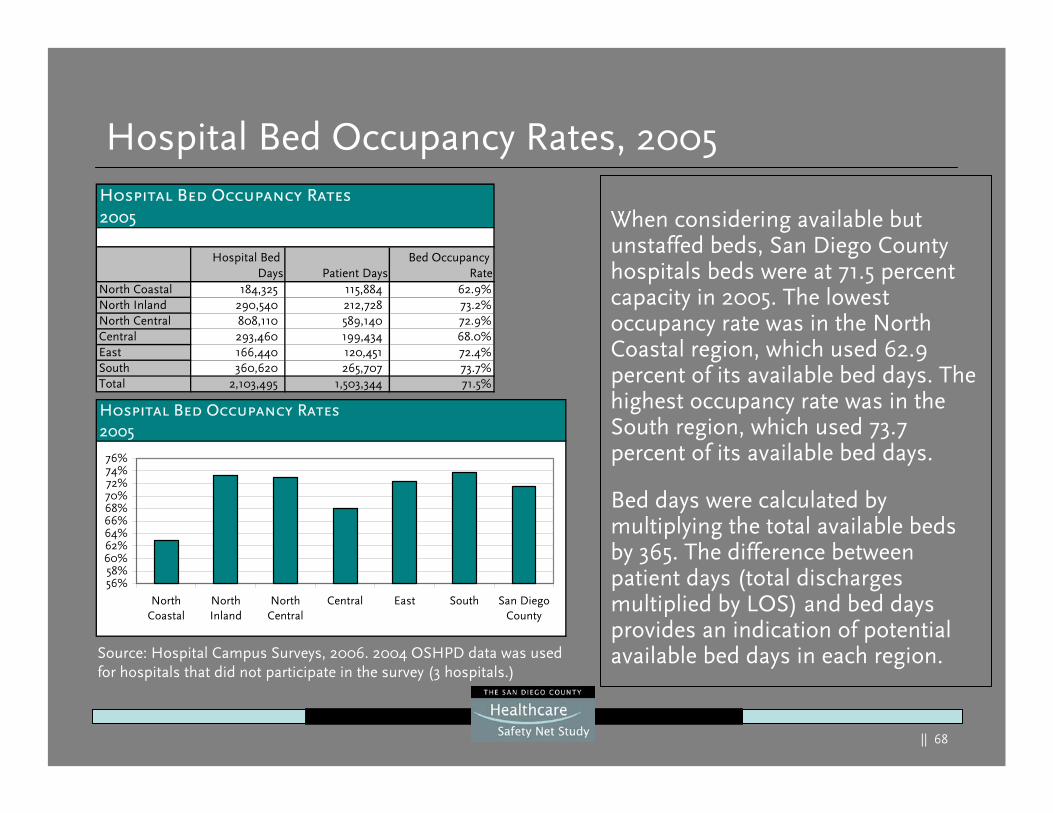

Hospital Bed Occupancy Rates, 2005

When considering available but unstaffed beds, San Diego County hospitals beds were at 71.5 percent capacity in 2005. The lowest occupancy rate was in the North Coastal region, which used 62.9 percent of its available bed days. The highest occupancy rate was in the South region, which used 73.7 percent of its available bed days.

Bed days were calculated by multiplying the total available beds by 365. The difference between patient days (total discharges multiplied by LOS) and bed days provides an indication of potential available bed days in each region.Source: Hospital Campus Surveys, 2006. 2004 OSHPD data was used

for hospitals that did not participate in the survey (3 hospitals.)

Hospital Bed Occupancy Rates2005

Hospital Bed Days Patient Days

Bed Occupancy Rate

North Coastal 184,325 115,884 62.9%North Inland 290,540 212,728 73.2%North Central 808,110 589,140 72.9%Central 293,460 199,434 68.0%East 166,440 120,451 72.4%South 360,620 265,707 73.7%Total 2,103,495 1,503,344 71.5%

Hospital Bed Occupancy Rates2005

56%58%60%62%64%66%68%70%72%74%76%

NorthCoastal

NorthInland

NorthCentral

Central East South San DiegoCounty

|| 69

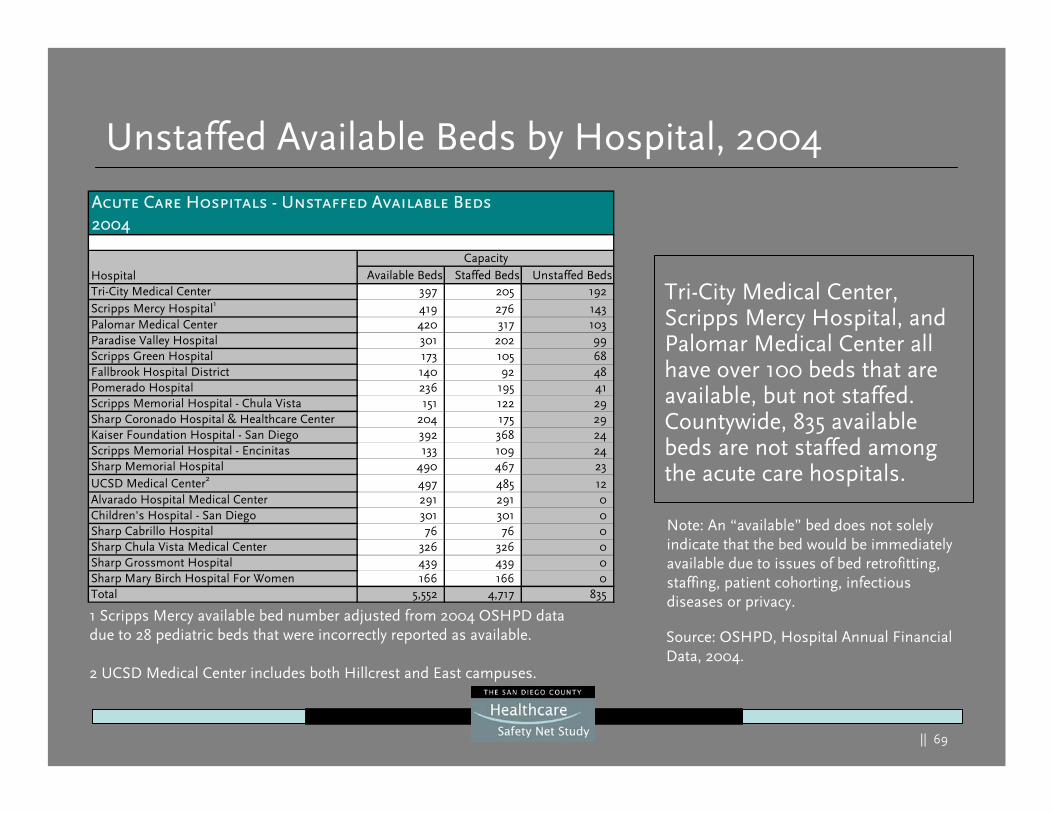

Unstaffed Available Beds by Hospital, 2004

Tri-City Medical Center, Scripps Mercy Hospital, and Palomar Medical Center all have over 100 beds that are available, but not staffed. Countywide, 835 available beds are not staffed among the acute care hospitals.

1 Scripps Mercy available bed number adjusted from 2004 OSHPD data due to 28 pediatric beds that were incorrectly reported as available.

2 UCSD Medical Center includes both Hillcrest and East campuses.

Source: OSHPD, Hospital Annual Financial Data, 2004.

Note: An “available” bed does not solely indicate that the bed would be immediately available due to issues of bed retrofitting, staffing, patient cohorting, infectious diseases or privacy.

Acute Care Hospitals - Unstaffed Available Beds2004

Hospital Available Beds Staffed Beds Unstaffed BedsTri-City Medical Center 397 205 192Scripps Mercy Hospital1 419 276 143Palomar Medical Center 420 317 103Paradise Valley Hospital 301 202 99Scripps Green Hospital 173 105 68Fallbrook Hospital District 140 92 48Pomerado Hospital 236 195 41Scripps Memorial Hospital - Chula Vista 151 122 29Sharp Coronado Hospital & Healthcare Center 204 175 29Kaiser Foundation Hospital - San Diego 392 368 24Scripps Memorial Hospital - Encinitas 133 109 24Sharp Memorial Hospital 490 467 23UCSD Medical Center2 497 485 12Alvarado Hospital Medical Center 291 291 0Children's Hospital - San Diego 301 301 0Sharp Cabrillo Hospital 76 76 0Sharp Chula Vista Medical Center 326 326 0Sharp Grossmont Hospital 439 439 0Sharp Mary Birch Hospital For Women 166 166 0Total 5,552 4,717 835

Capacity

|| 70

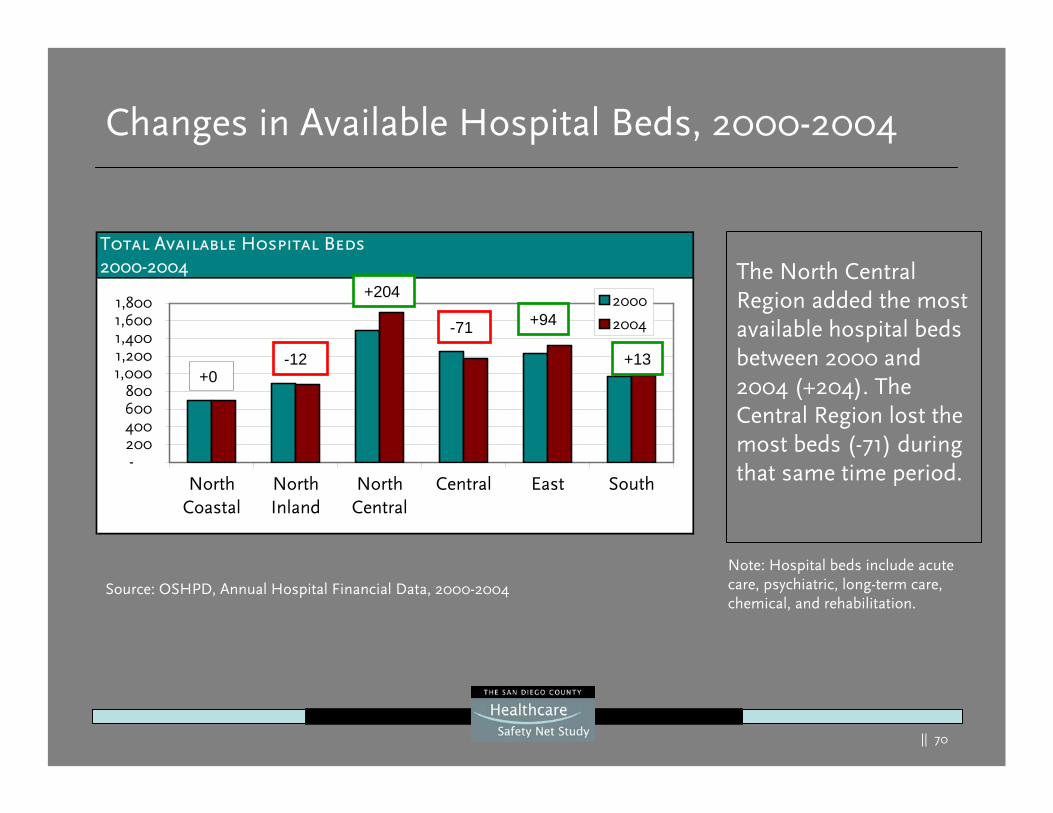

Changes in Available Hospital Beds, 2000-2004

Note: Hospital beds include acute care, psychiatric, long-term care, chemical, and rehabilitation.

Source: OSHPD, Annual Hospital Financial Data, 2000-2004

The North Central Region added the most available hospital beds between 2000 and 2004 (+204). The Central Region lost the most beds (-71) during that same time period.

Total Available Hospital Beds2000-2004

-200400600800

1,0001,2001,4001,6001,800

NorthCoastal

NorthInland

NorthCentral

Central East South

2000

2004

+0-12

+204

-71 +94

+13

|| 71

Demand Forecasts

|| 72

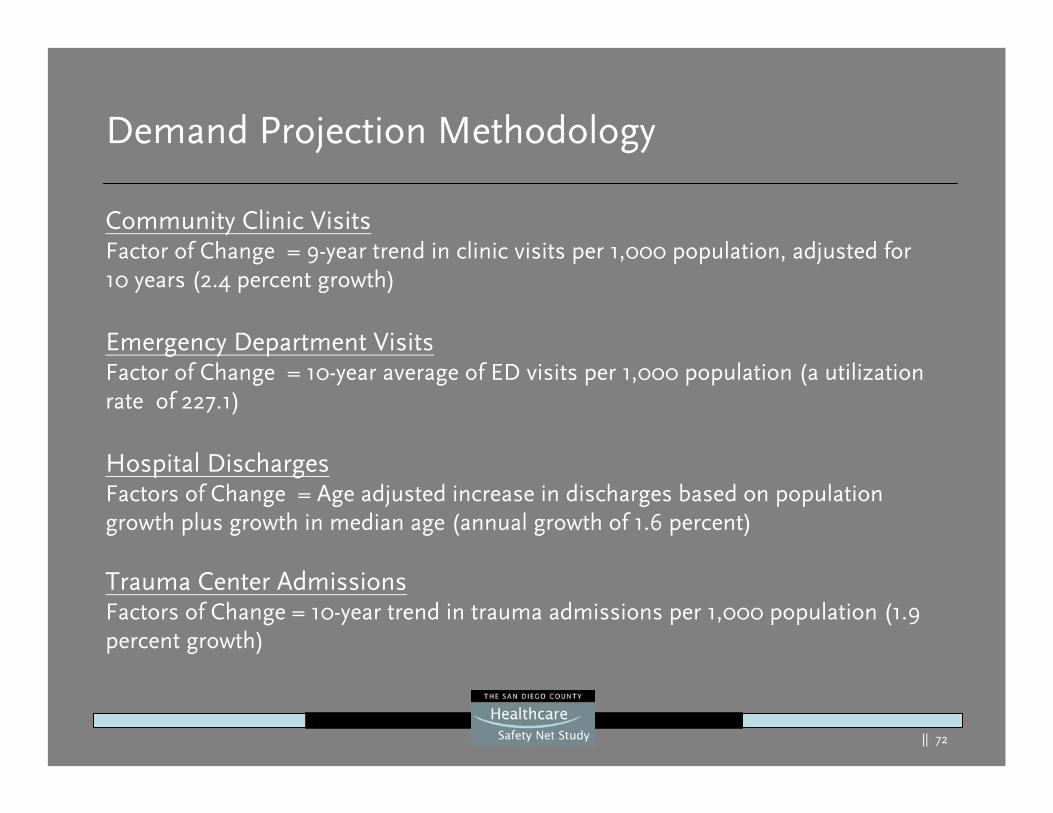

Demand Projection Methodology

Community Clinic VisitsFactor of Change = 9-year trend in clinic visits per 1,000 population, adjusted for 10 years (2.4 percent growth)

Emergency Department VisitsFactor of Change = 10-year average of ED visits per 1,000 population (a utilization rate of 227.1)

Hospital DischargesFactors of Change = Age adjusted increase in discharges based on population growth plus growth in median age (annual growth of 1.6 percent)

Trauma Center AdmissionsFactors of Change = 10-year trend in trauma admissions per 1,000 population (1.9 percent growth)

|| 73

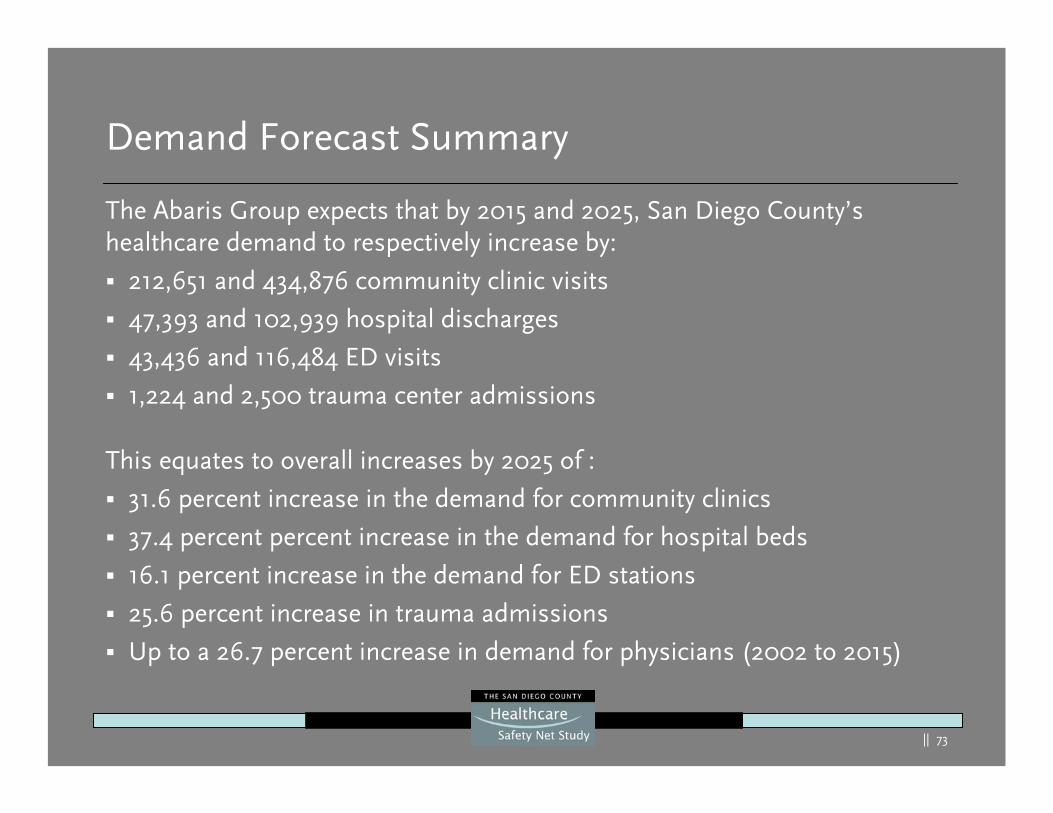

Demand Forecast Summary

The Abaris Group expects that by 2015 and 2025, San Diego County’s healthcare demand to respectively increase by:

212,651 and 434,876 community clinic visits

47,393 and 102,939 hospital discharges

43,436 and 116,484 ED visits

1,224 and 2,500 trauma center admissions

This equates to overall increases by 2025 of :

31.6 percent increase in the demand for community clinics

37.4 percent percent increase in the demand for hospital beds

16.1 percent increase in the demand for ED stations

25.6 percent increase in trauma admissions

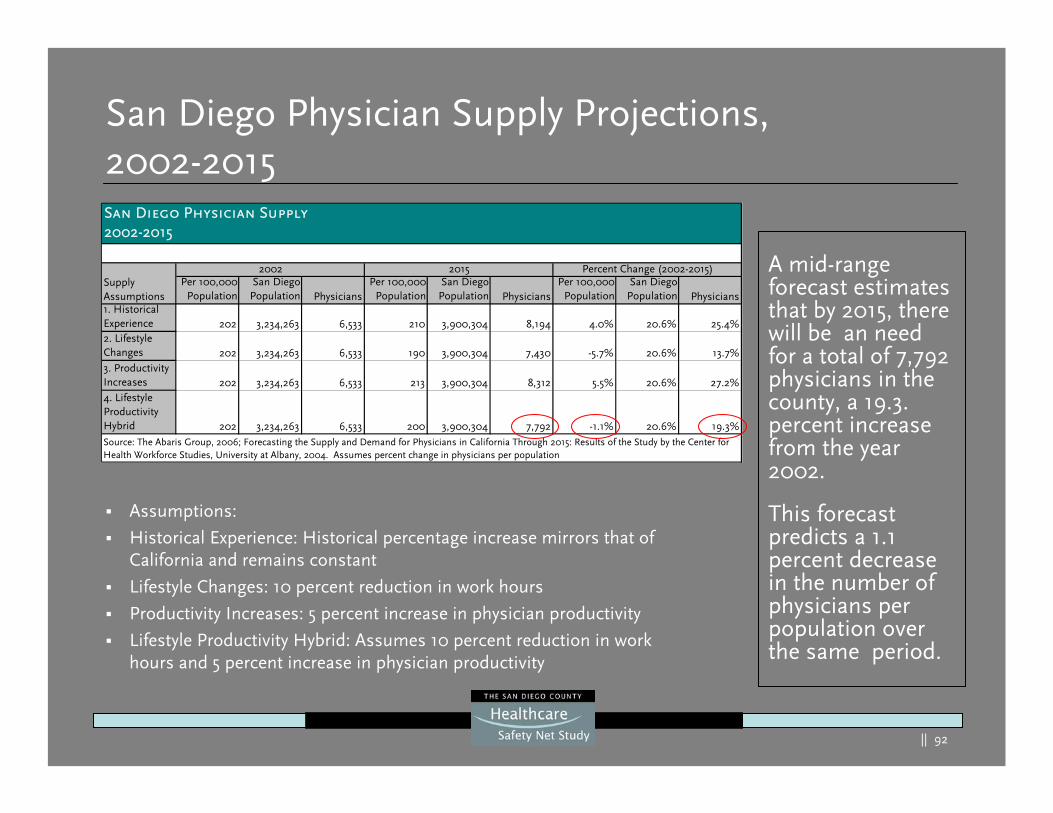

Up to a 26.7 percent increase in demand for physicians (2002 to 2015)

|| 74

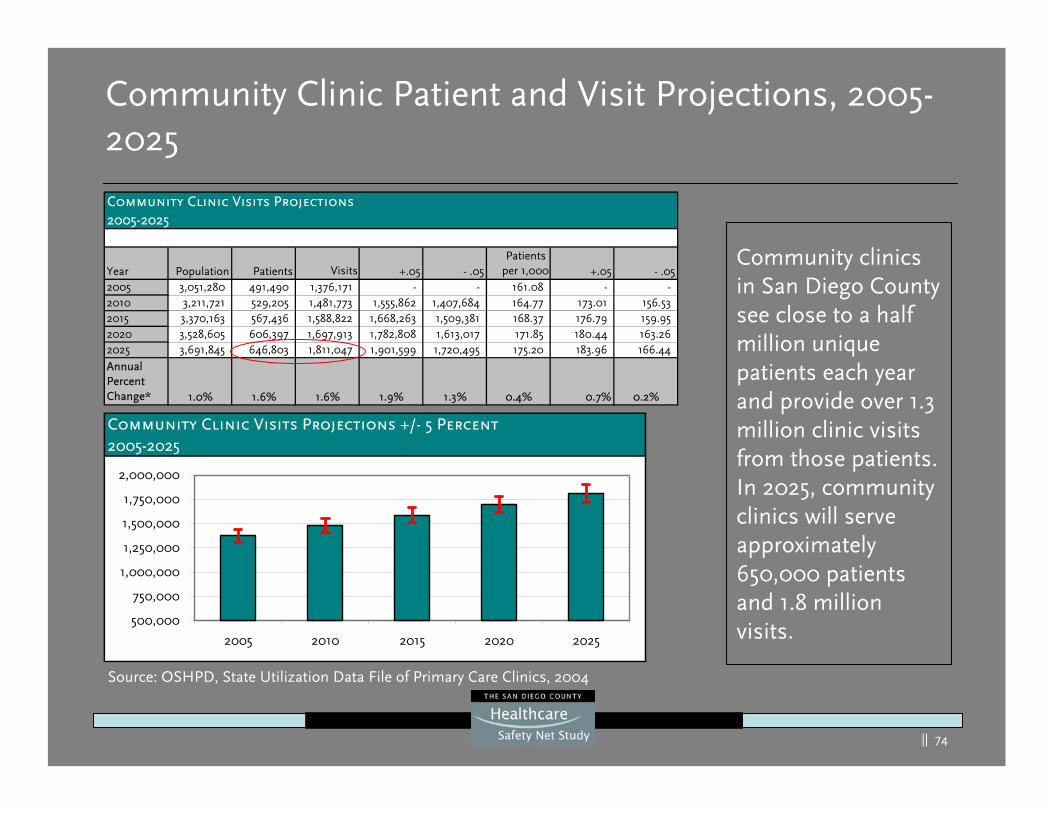

Community Clinic Visits Projections2005-2025

Year Population Patients Visits +.05 - .05Patients

per 1,000 +.05 - .052005 3,051,280 491,490 1,376,171 - - 161.08 - -2010 3,211,721 529,205 1,481,773 1,555,862 1,407,684 164.77 173.01 156.53 2015 3,370,163 567,436 1,588,822 1,668,263 1,509,381 168.37 176.79 159.95 2020 3,528,605 606,397 1,697,913 1,782,808 1,613,017 171.85 180.44 163.26 2025 3,691,845 646,803 1,811,047 1,901,599 1,720,495 175.20 183.96 166.44

Annual Percent Change* 1.0% 1.6% 1.6% 1.9% 1.3% 0.4% 0.7% 0.2%

Community Clinic Patient and Visit Projections, 2005-2025

Community Clinic Visits Projections +/- 5 Percent2005-2025

500,000

750,000

1,000,000

1,250,000

1,500,000

1,750,000

2,000,000

2005 2010 2015 2020 2025

Source: OSHPD, State Utilization Data File of Primary Care Clinics, 2004

Community clinics in San Diego County see close to a half million unique patients each year and provide over 1.3 million clinic visits from those patients. In 2025, community clinics will serve approximately 650,000 patients and 1.8 million visits.

|| 75

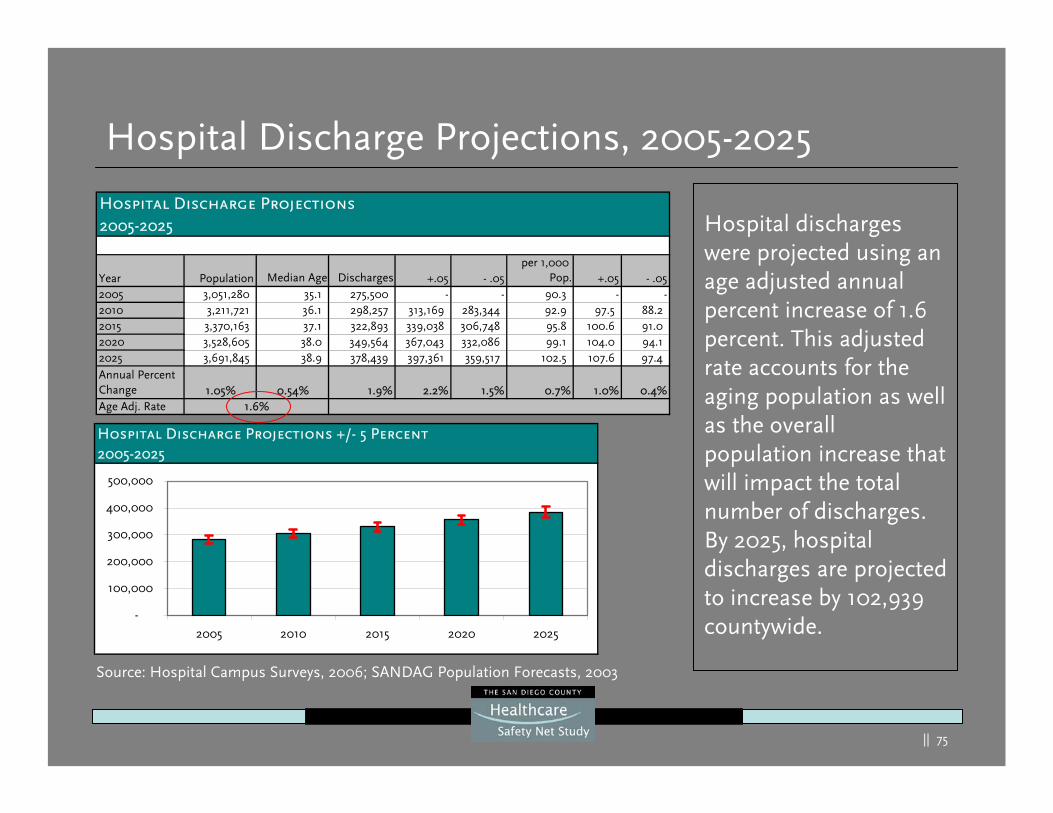

Hospital Discharge Projections2005-2025

Year Population Median Age Discharges +.05 - .05per 1,000

Pop. +.05 - .052005 3,051,280 35.1 275,500 - - 90.3 - -2010 3,211,721 36.1 298,257 313,169 283,344 92.9 97.5 88.2 2015 3,370,163 37.1 322,893 339,038 306,748 95.8 100.6 91.0 2020 3,528,605 38.0 349,564 367,043 332,086 99.1 104.0 94.1 2025 3,691,845 38.9 378,439 397,361 359,517 102.5 107.6 97.4

Annual Percent Change 1.05% 0.54% 1.9% 2.2% 1.5% 0.7% 1.0% 0.4%Age Adj. Rate 1.6%

Hospital Discharge Projections, 2005-2025

Hospital discharges were projected using an age adjusted annual percent increase of 1.6 percent. This adjusted rate accounts for the aging population as well as the overall population increase that will impact the total number of discharges. By 2025, hospital discharges are projected to increase by 102,939 countywide.

Hospital Discharge Projections +/- 5 Percent2005-2025

-

100,000

200,000

300,000

400,000

500,000

2005 2010 2015 2020 2025

Source: Hospital Campus Surveys, 2006; SANDAG Population Forecasts, 2003

|| 76

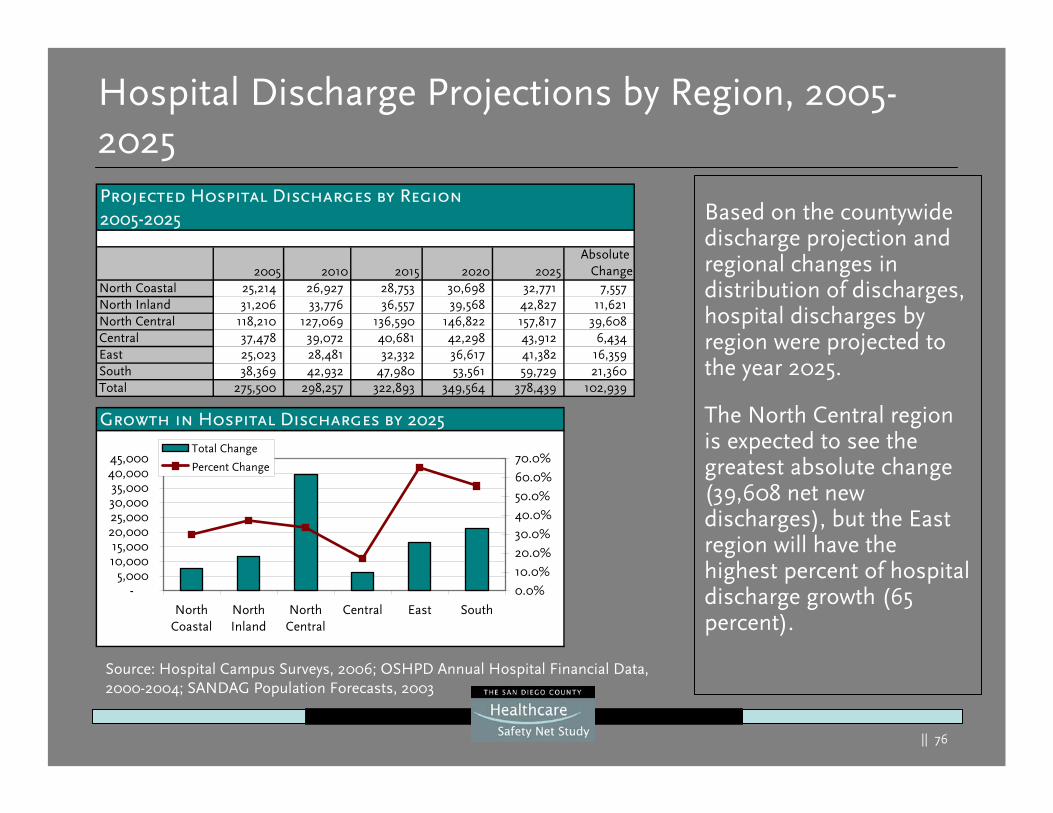

Hospital Discharge Projections by Region, 2005-2025

Based on the countywide discharge projection and regional changes in distribution of discharges, hospital discharges by region were projected to the year 2025.

The North Central region is expected to see the greatest absolute change (39,608 net new discharges), but the East region will have the highest percent of hospital discharge growth (65 percent).

Source: Hospital Campus Surveys, 2006; OSHPD Annual Hospital Financial Data, 2000-2004; SANDAG Population Forecasts, 2003

Projected Hospital Discharges by Region2005-2025

2005 2010 2015 2020 2025Absolute

ChangeNorth Coastal 25,214 26,927 28,753 30,698 32,771 7,557 North Inland 31,206 33,776 36,557 39,568 42,827 11,621 North Central 118,210 127,069 136,590 146,822 157,817 39,608 Central 37,478 39,072 40,681 42,298 43,912 6,434 East 25,023 28,481 32,332 36,617 41,382 16,359 South 38,369 42,932 47,980 53,561 59,729 21,360 Total 275,500 298,257 322,893 349,564 378,439 102,939

Growth in Hospital Discharges by 2025

-5,000

10,00015,000

20,00025,00030,00035,000

40,00045,000

NorthCoastal

NorthInland

NorthCentral

Central East South

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%Total Change

Percent Change

|| 77

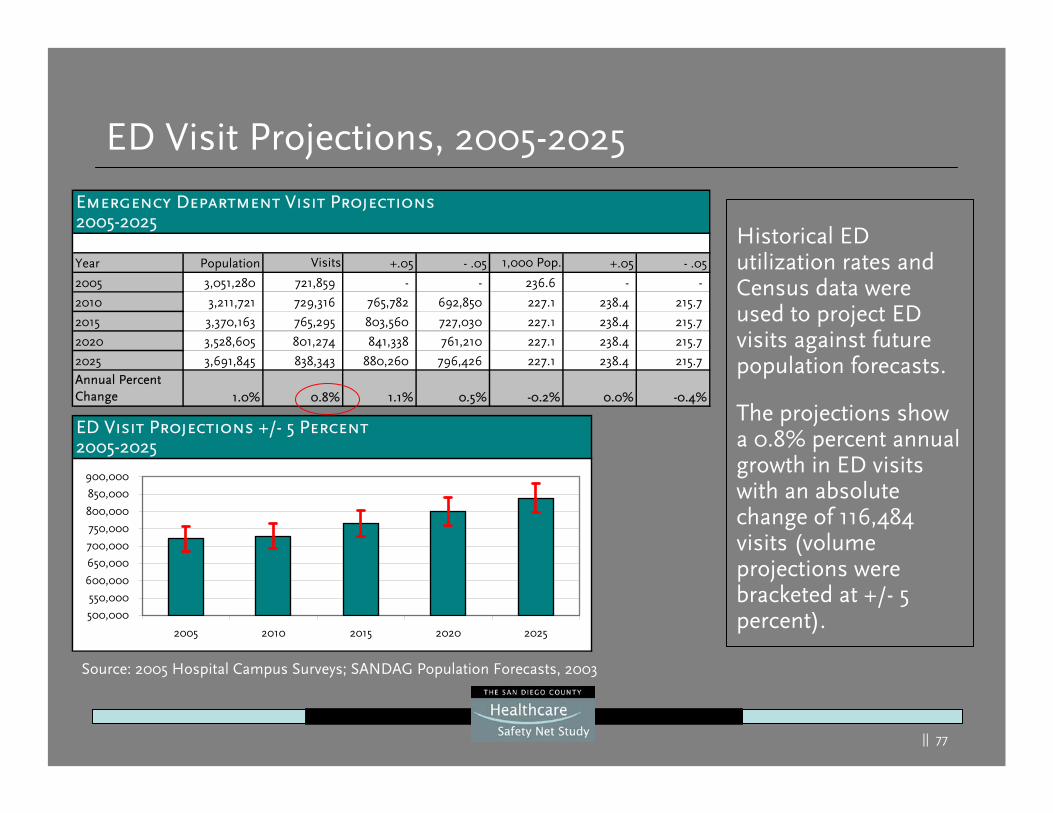

Emergency Department Visit Projections2005-2025

Year Population Visits +.05 - .05 1,000 Pop. +.05 - .05

2005 3,051,280 721,859 - - 236.6 - -

2010 3,211,721 729,316 765,782 692,850 227.1 238.4 215.7

2015 3,370,163 765,295 803,560 727,030 227.1 238.4 215.7

2020 3,528,605 801,274 841,338 761,210 227.1 238.4 215.7

2025 3,691,845 838,343 880,260 796,426 227.1 238.4 215.7 Annual Percent Change 1.0% 0.8% 1.1% 0.5% -0.2% 0.0% -0.4%

ED Visit Projections, 2005-2025

Historical ED utilization rates and Census data were used to project ED visits against future population forecasts.

The projections show a 0.8% percent annual growth in ED visits with an absolute change of 116,484 visits (volume projections were bracketed at +/- 5 percent).

Source: 2005 Hospital Campus Surveys; SANDAG Population Forecasts, 2003

ED Visit Projections +/- 5 Percent2005-2025

500,000

550,000

600,000

650,000

700,000

750,000

800,000

850,000

900,000

2005 2010 2015 2020 2025

|| 78

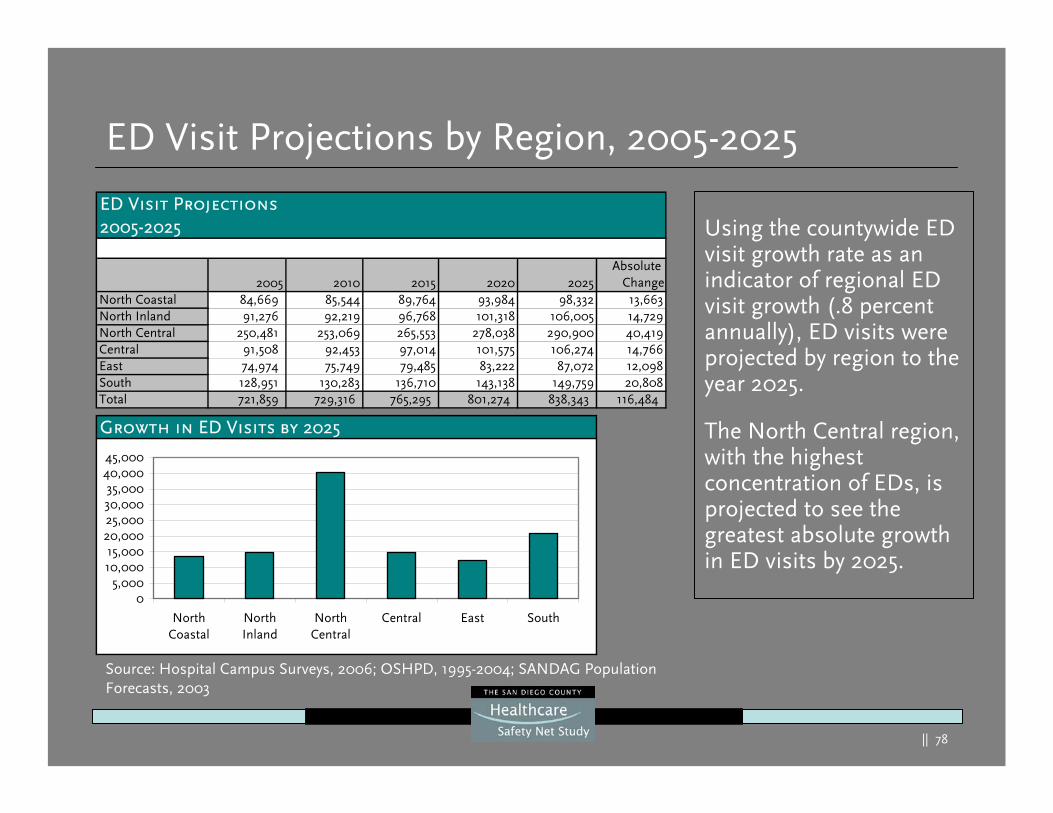

ED Visit Projections by Region, 2005-2025

Using the countywide ED visit growth rate as an indicator of regional ED visit growth (.8 percent annually), ED visits were projected by region to the year 2025.

The North Central region, with the highest concentration of EDs, is projected to see the greatest absolute growth in ED visits by 2025.

Source: Hospital Campus Surveys, 2006; OSHPD, 1995-2004; SANDAG Population Forecasts, 2003

ED Visit Projections2005-2025

2005 2010 2015 2020 2025Absolute

ChangeNorth Coastal 84,669 85,544 89,764 93,984 98,332 13,663North Inland 91,276 92,219 96,768 101,318 106,005 14,729North Central 250,481 253,069 265,553 278,038 290,900 40,419Central 91,508 92,453 97,014 101,575 106,274 14,766East 74,974 75,749 79,485 83,222 87,072 12,098South 128,951 130,283 136,710 143,138 149,759 20,808Total 721,859 729,316 765,295 801,274 838,343 116,484

Growth in ED Visits by 2025

05,000

10,00015,000

20,00025,00030,00035,000

40,00045,000

NorthCoastal

NorthInland

NorthCentral

Central East South

|| 79

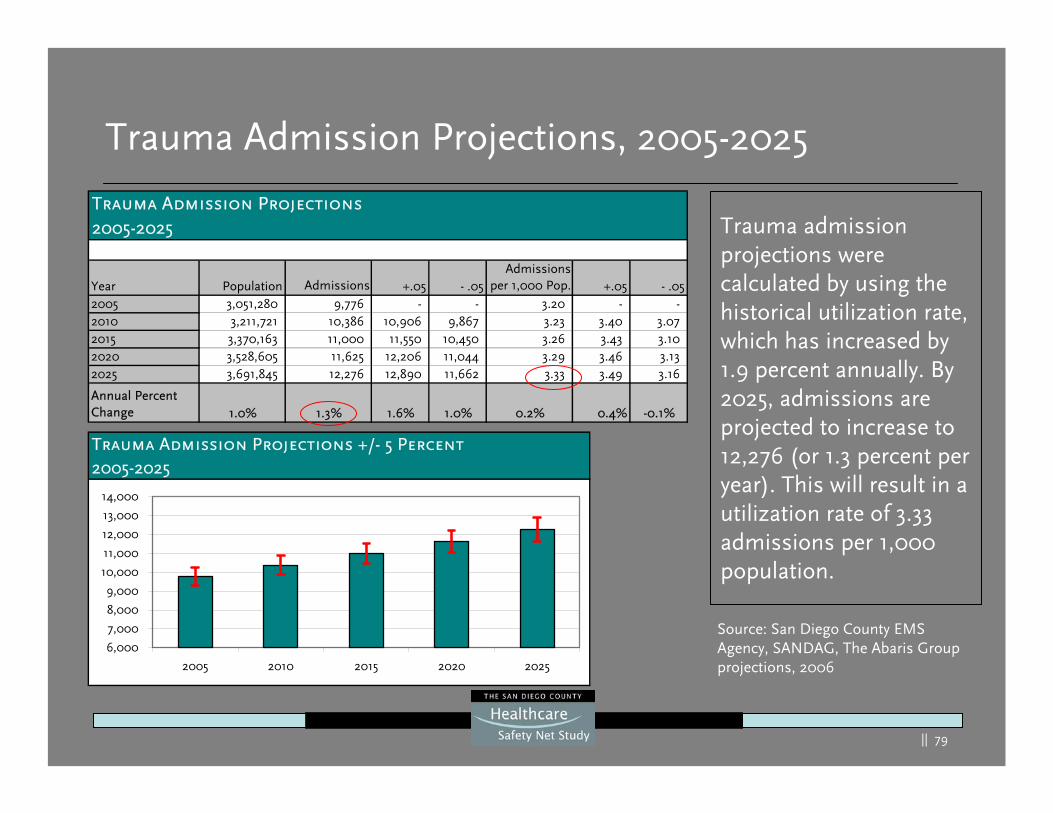

Trauma Admission Projections2005-2025

Year Population Admissions +.05 - .05Admissions

per 1,000 Pop. +.05 - .052005 3,051,280 9,776 - - 3.20 - -2010 3,211,721 10,386 10,906 9,867 3.23 3.40 3.07 2015 3,370,163 11,000 11,550 10,450 3.26 3.43 3.10 2020 3,528,605 11,625 12,206 11,044 3.29 3.46 3.13 2025 3,691,845 12,276 12,890 11,662 3.33 3.49 3.16

Annual Percent Change 1.0% 1.3% 1.6% 1.0% 0.2% 0.4% -0.1%

Trauma Admission Projections, 2005-2025

Trauma admission projections were calculated by using the historical utilization rate, which has increased by 1.9 percent annually. By 2025, admissions are projected to increase to 12,276 (or 1.3 percent per year). This will result in a utilization rate of 3.33 admissions per 1,000 population.

Trauma Admission Projections +/- 5 Percent2005-2025

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

2005 2010 2015 2020 2025

Source: San Diego County EMS Agency, SANDAG, The Abaris Group projections, 2006

|| 80

Capacity Forecasts

|| 81

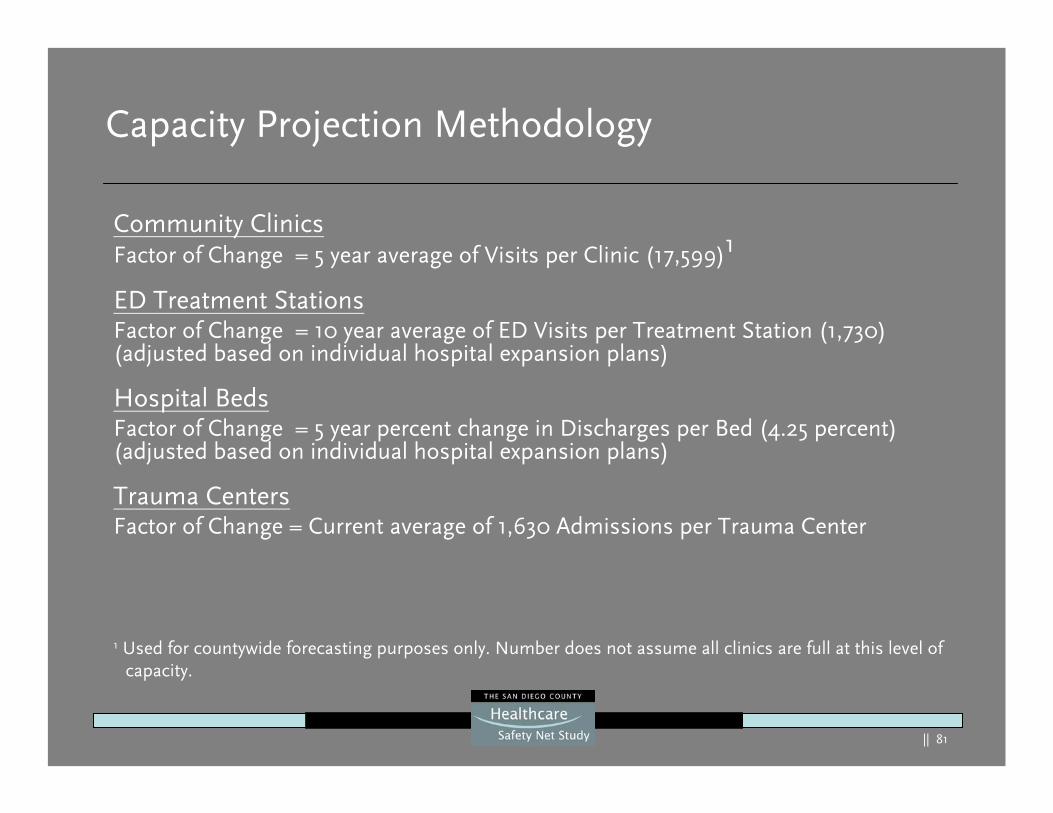

Capacity Projection Methodology

Community ClinicsFactor of Change = 5 year average of Visits per Clinic (17,599)1

ED Treatment StationsFactor of Change = 10 year average of ED Visits per Treatment Station (1,730) (adjusted based on individual hospital expansion plans)

Hospital BedsFactor of Change = 5 year percent change in Discharges per Bed (4.25 percent) (adjusted based on individual hospital expansion plans)

Trauma CentersFactor of Change = Current average of 1,630 Admissions per Trauma Center

Community ClinicsFactor of Change = 5 year average of Visits per Clinic (17,599)1

ED Treatment StationsFactor of Change = 10 year average of ED Visits per Treatment Station (1,730) (adjusted based on individual hospital expansion plans)

Hospital BedsFactor of Change = 5 year percent change in Discharges per Bed (4.25 percent) (adjusted based on individual hospital expansion plans)

Trauma CentersFactor of Change = Current average of 1,630 Admissions per Trauma Center

1 Used for countywide forecasting purposes only. Number does not assume all clinics are full at this level of capacity.

|| 82

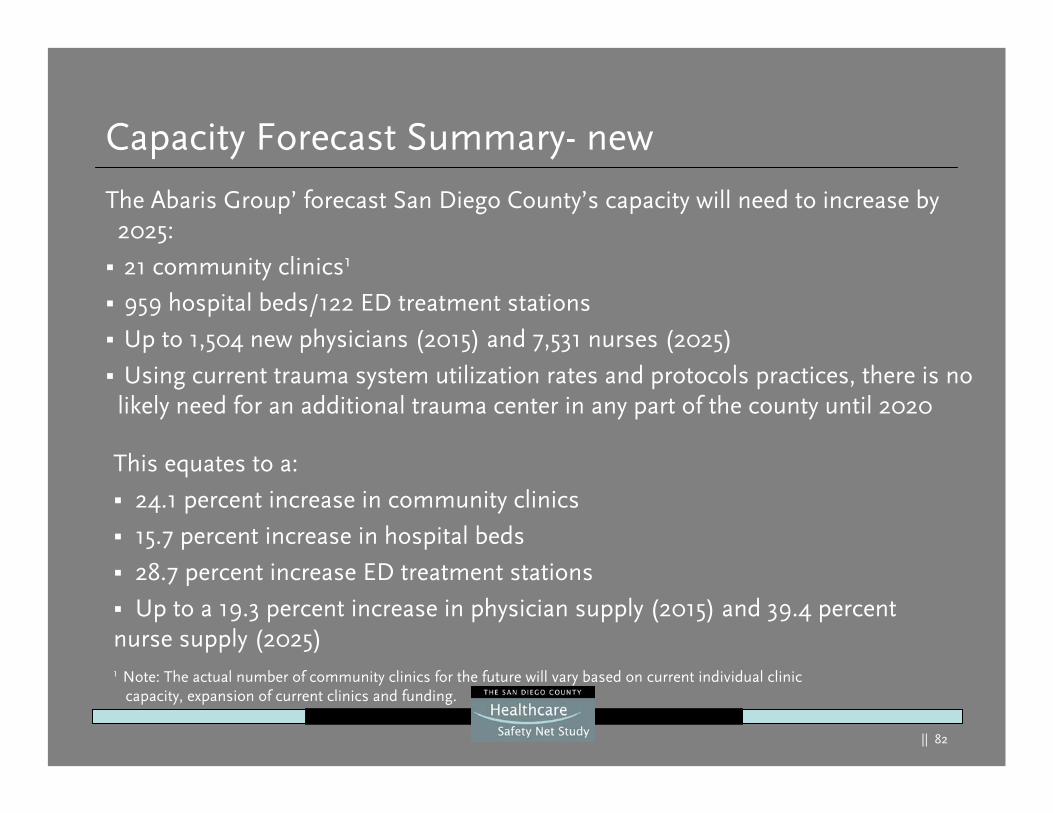

Capacity Forecast Summary- new

The Abaris Group’ forecast San Diego County’s capacity will need to increase by 2025:

21 community clinics1

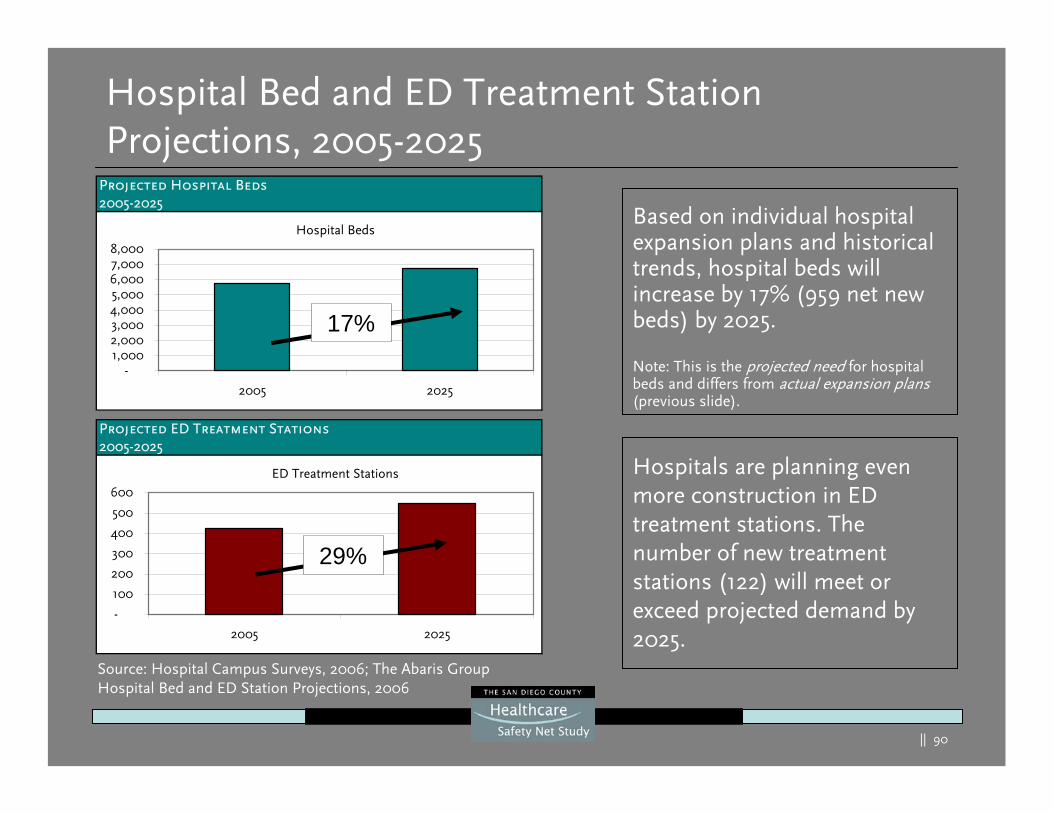

959 hospital beds/122 ED treatment stations

Up to 1,504 new physicians (2015) and 7,531 nurses (2025)

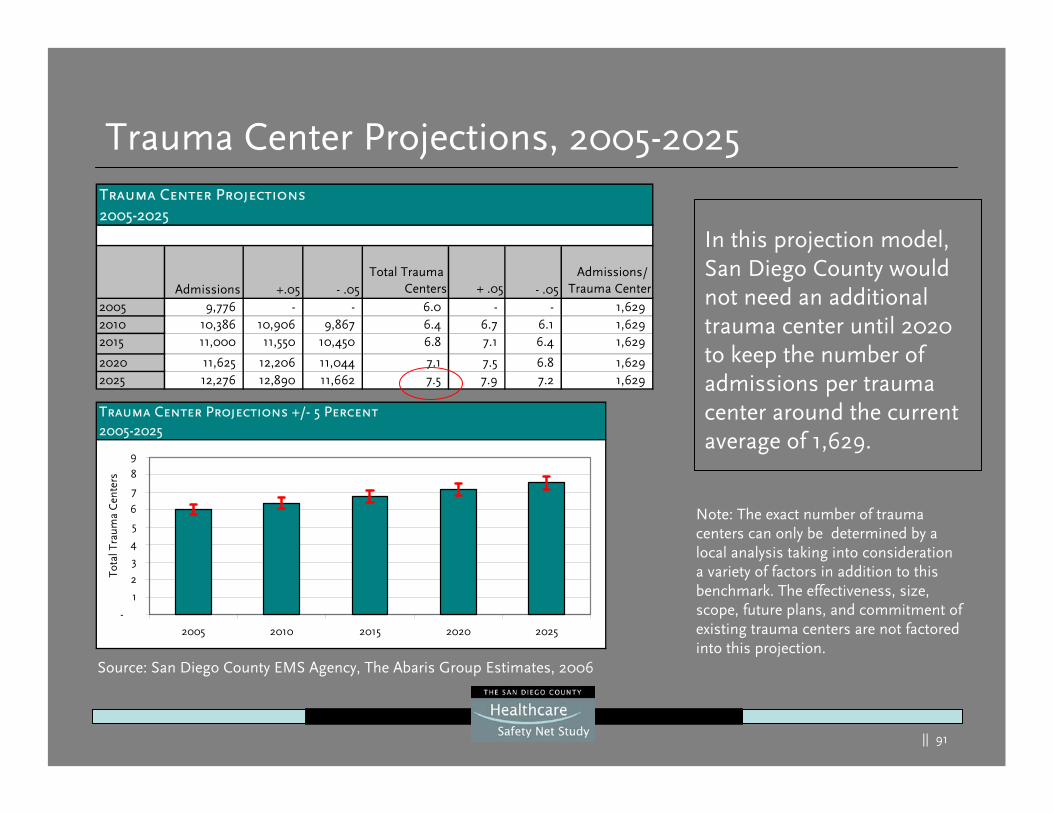

Using current trauma system utilization rates and protocols practices, there is no likely need for an additional trauma center in any part of the county until 2020

This equates to a:

24.1 percent increase in community clinics

15.7 percent increase in hospital beds

28.7 percent increase ED treatment stations

Up to a 19.3 percent increase in physician supply (2015) and 39.4 percent nurse supply (2025)1 Note: The actual number of community clinics for the future will vary based on current individual clinic

capacity, expansion of current clinics and funding.

|| 83

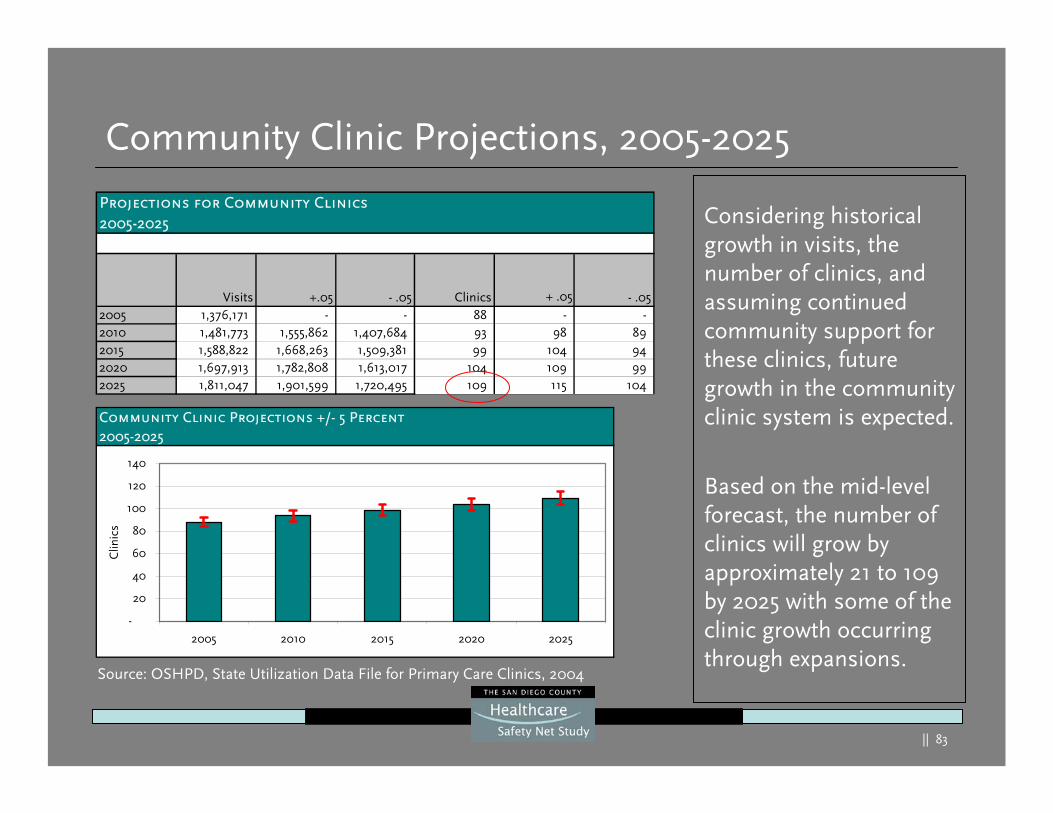

Projections for Community Clinics2005-2025

Visits +.05 - .05 Clinics + .05 - .052005 1,376,171 - - 88 - -2010 1,481,773 1,555,862 1,407,684 93 98 89 2015 1,588,822 1,668,263 1,509,381 99 104 94 2020 1,697,913 1,782,808 1,613,017 104 109 99 2025 1,811,047 1,901,599 1,720,495 109 115 104

Community Clinic Projections, 2005-2025

Considering historical growth in visits, the number of clinics, and assuming continued community support for these clinics, future growth in the community clinic system is expected.

Based on the mid-level forecast, the number of clinics will grow by approximately 21 to 109 by 2025 with some of the clinic growth occurring through expansions.

Community Clinic Projections +/- 5 Percent2005-2025

-

20

40

60

80

100

120

140

2005 2010 2015 2020 2025

Clin

ics

Source: OSHPD, State Utilization Data File for Primary Care Clinics, 2004

|| 84

Hospital Expansion Plans

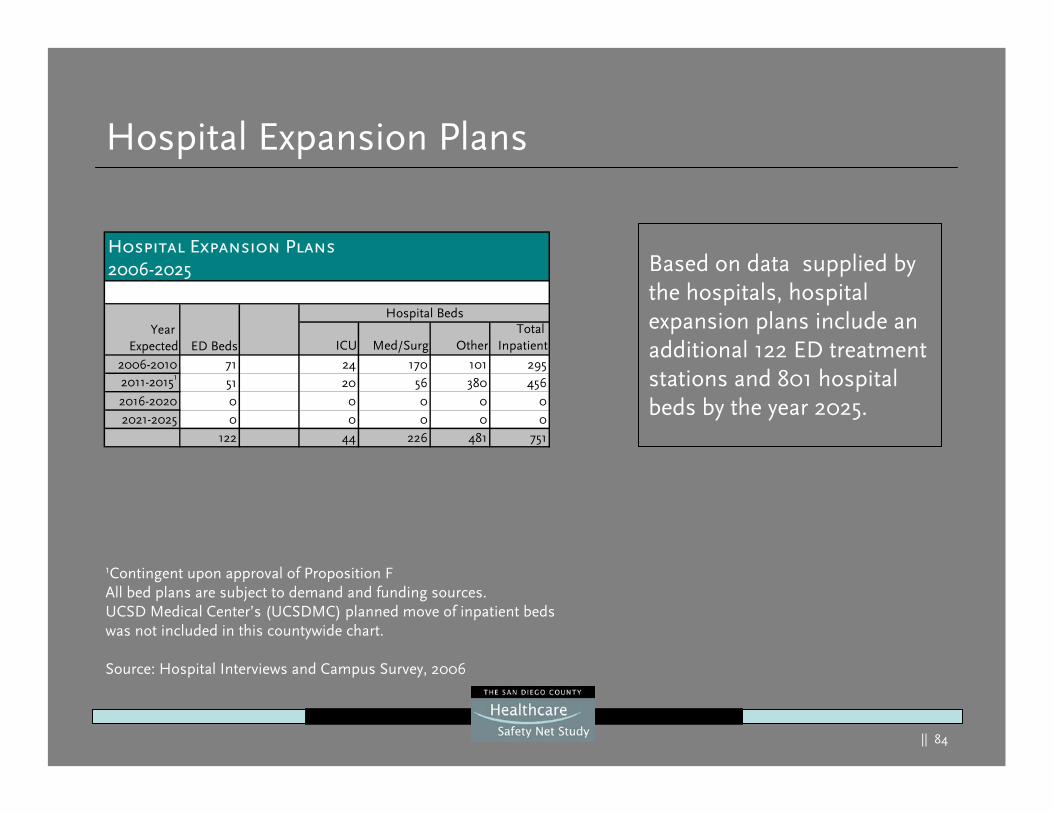

Based on data supplied by the hospitals, hospital expansion plans include an additional 122 ED treatment stations and 801 hospital beds by the year 2025.

Based on data supplied by the hospitals, hospital expansion plans include an additional 122 ED treatment stations and 801 hospital beds by the year 2025.

1Contingent upon approval of Proposition FAll bed plans are subject to demand and funding sources. UCSD Medical Center’s (UCSDMC) planned move of inpatient beds was not included in this countywide chart.

Source: Hospital Interviews and Campus Survey, 2006

ICU Med/Surg OtherTotal

Inpatient

2006-2010 71 24 170 101 2952011-20151 51 20 56 380 4562016-2020 0 0 0 0 02021-2025 0 0 0 0 0

122 44 226 481 751

Hospital Expansion Plans2006-2025

Hospital Beds

ED BedsYear

Expected

|| 85

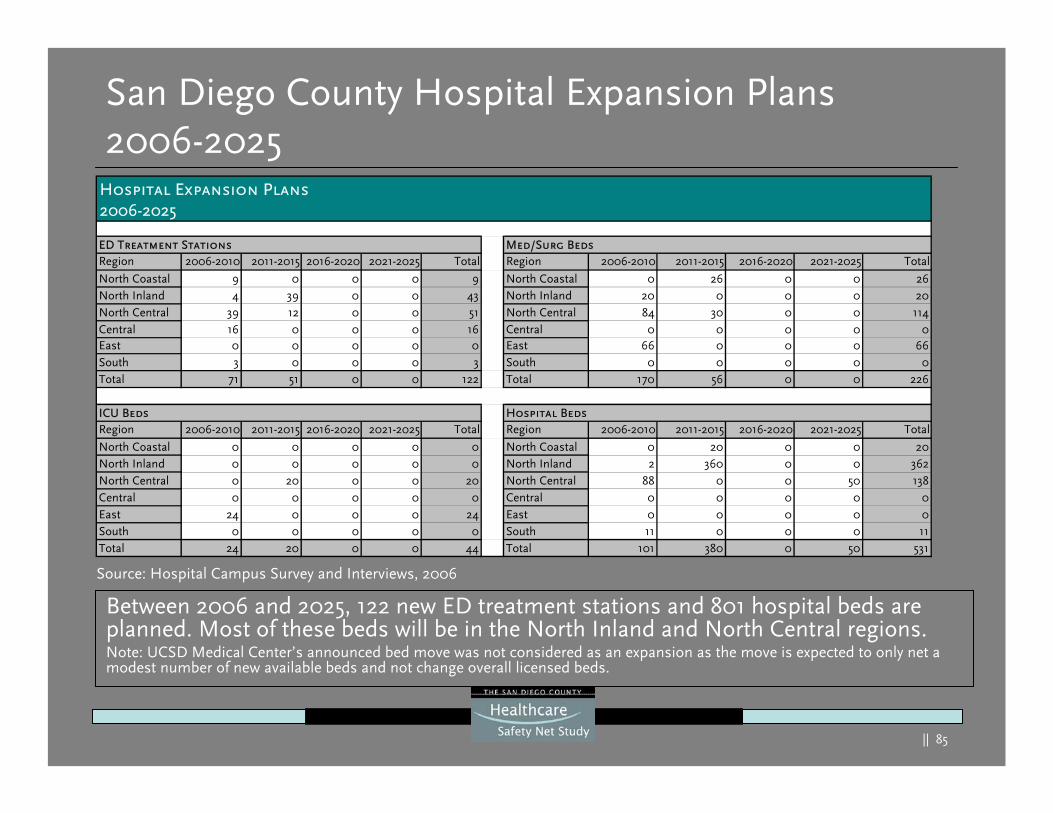

San Diego County Hospital Expansion Plans2006-2025

Between 2006 and 2025, 122 new ED treatment stations and 801 hospital beds are planned. Most of these beds will be in the North Inland and North Central regions.Note: UCSD Medical Center’s announced bed move was not considered as an expansion as the move is expected to only net a modest number of new available beds and not change overall licensed beds.

Between 2006 and 2025, 122 new ED treatment stations and 801 hospital beds are planned. Most of these beds will be in the North Inland and North Central regions.Note: UCSD Medical Center’s announced bed move was not considered as an expansion as the move is expected to only net a modest number of new available beds and not change overall licensed beds.

Region 2006-2010 2011-2015 2016-2020 2021-2025 Total Region 2006-2010 2011-2015 2016-2020 2021-2025 Total

North Coastal 9 0 0 0 9 North Coastal 0 26 0 0 26North Inland 4 39 0 0 43 North Inland 20 0 0 0 20North Central 39 12 0 0 51 North Central 84 30 0 0 114Central 16 0 0 0 16 Central 0 0 0 0 0East 0 0 0 0 0 East 66 0 0 0 66South 3 0 0 0 3 South 0 0 0 0 0Total 71 51 0 0 122 Total 170 56 0 0 226

Region 2006-2010 2011-2015 2016-2020 2021-2025 Total Region 2006-2010 2011-2015 2016-2020 2021-2025 Total

North Coastal 0 0 0 0 0 North Coastal 0 20 0 0 20North Inland 0 0 0 0 0 North Inland 2 360 0 0 362North Central 0 20 0 0 20 North Central 88 0 0 50 138Central 0 0 0 0 0 Central 0 0 0 0 0East 24 0 0 0 24 East 0 0 0 0 0South 0 0 0 0 0 South 11 0 0 0 11Total 24 20 0 0 44 Total 101 380 0 50 531

Hospital Expansion Plans2006-2025

ED Treatment Stations

ICU Beds Hospital Beds

Med/Surg Beds

Source: Hospital Campus Survey and Interviews, 2006

|| 86

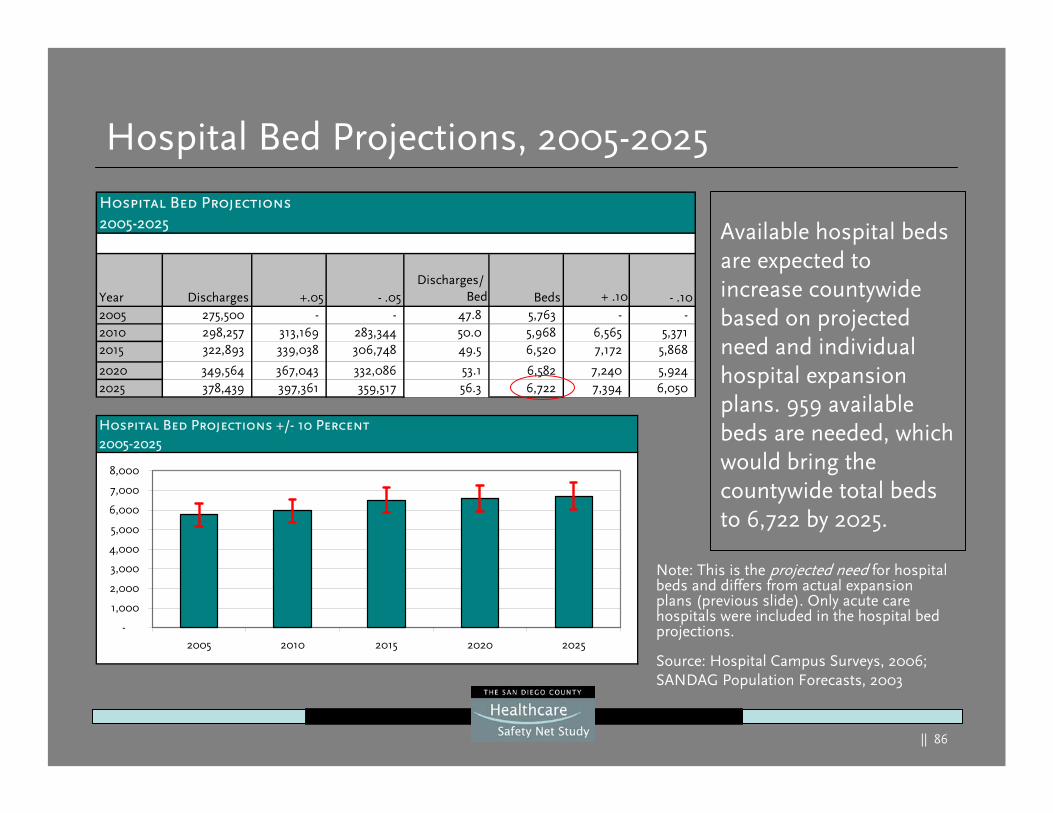

Hospital Bed Projections2005-2025

Year Discharges +.05 - .05Discharges/

Bed Beds + .10 - .102005 275,500 - - 47.8 5,763 - -2010 298,257 313,169 283,344 50.0 5,968 6,565 5,371 2015 322,893 339,038 306,748 49.5 6,520 7,172 5,868

2020 349,564 367,043 332,086 53.1 6,582 7,240 5,924 2025 378,439 397,361 359,517 56.3 6,722 7,394 6,050

Hospital Bed Projections, 2005-2025

Available hospital beds are expected to increase countywide based on projected need and individual hospital expansion plans. 959 available beds are needed, which would bring the countywide total beds to 6,722 by 2025.

Source: Hospital Campus Surveys, 2006; SANDAG Population Forecasts, 2003

Note: This is the projected need for hospital beds and differs from actual expansion plans (previous slide). Only acute care hospitals were included in the hospital bed projections.

Hospital Bed Projections +/- 10 Percent2005-2025

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2005 2010 2015 2020 2025

|| 87

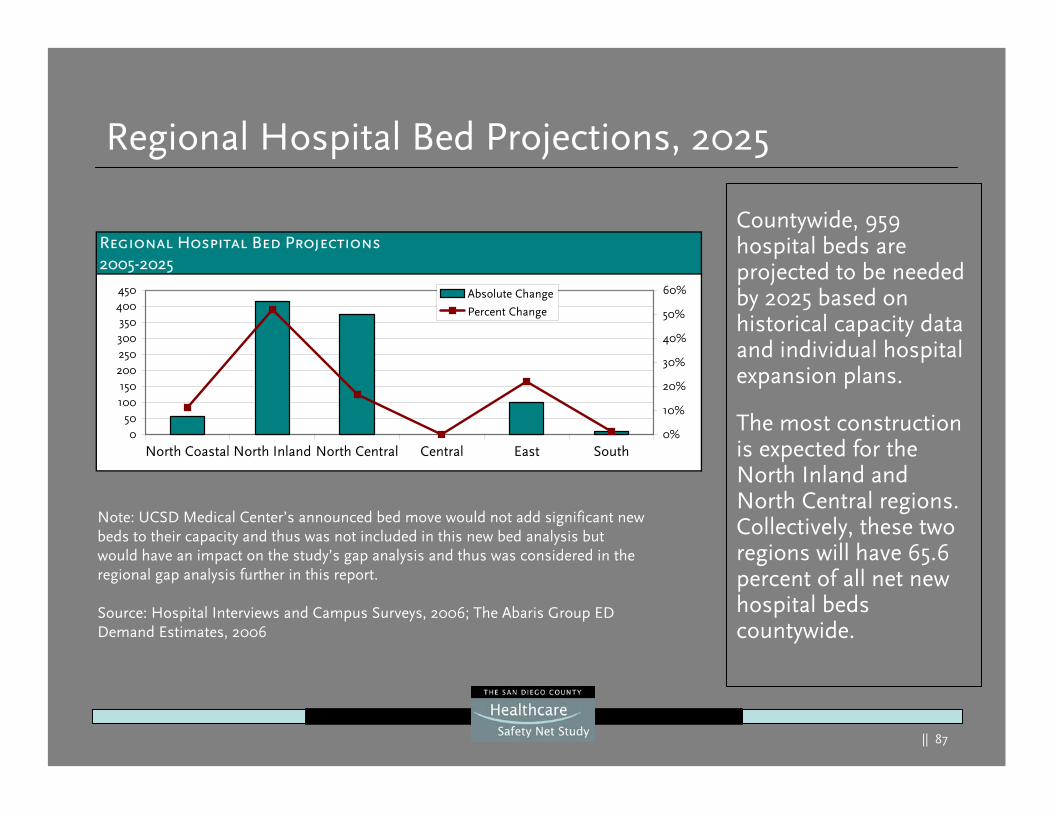

Regional Hospital Bed Projections, 2025

Countywide, 959 hospital beds are projected to be needed by 2025 based on historical capacity data and individual hospital expansion plans.

The most construction is expected for the North Inland and North Central regions. Collectively, these two regions will have 65.6 percent of all net new hospital beds countywide.

Note: UCSD Medical Center’s announced bed move would not add significant new beds to their capacity and thus was not included in this new bed analysis but would have an impact on the study’s gap analysis and thus was considered in the regional gap analysis further in this report.

Source: Hospital Interviews and Campus Surveys, 2006; The Abaris Group ED Demand Estimates, 2006

Regional Hospital Bed Projections2005-2025

050

100150

200250300350

400450

North Coastal North Inland North Central Central East South0%

10%

20%

30%

40%

50%

60%Absolute Change

Percent Change

|| 88

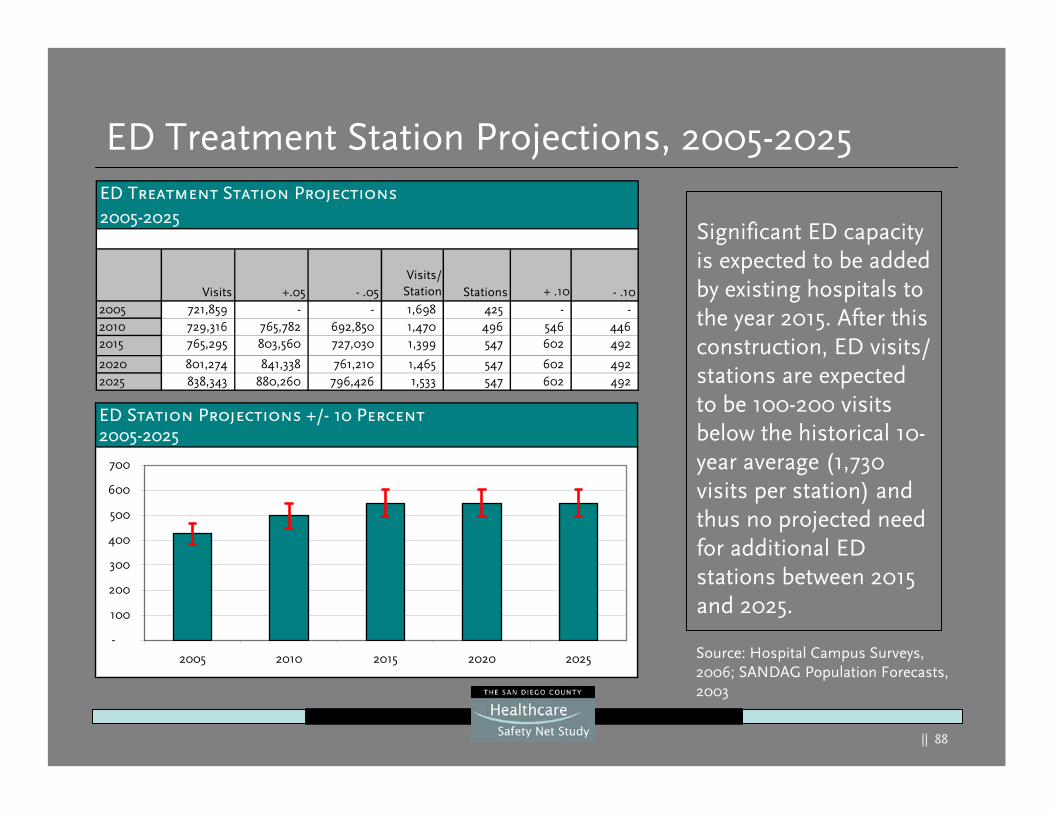

ED Treatment Station Projections, 2005-2025

Significant ED capacity is expected to be added by existing hospitals to the year 2015. After this construction, ED visits/ stations are expected to be 100-200 visits below the historical 10-year average (1,730 visits per station) and thus no projected need for additional ED stations between 2015 and 2025.