111

Study Guide Business Law 2 By Mike Wilson, Esq.

| Date post: | 27-May-2018 |

| Category: |

Documents |

| Upload: | phungquynh |

| View: | 213 times |

| Download: | 0 times |

Study Guide

Business Law 2By

Mike Wilson, Esq.

About the Author

Mike Wilson is a freelance writer and college instructor who hashad wide legal and educational experience.

He graduated with his bachelor of arts degree in English from theUniversity of Kentucky in 1976, and three years later received hisjuris doctorate from the same school. He has been a partner in a law firm and a solo practitioner and has worked in general and family mediation. He has also been a full-time instructor in Paralegal Studies at Sullivan College in Kentucky. He was given the “Teacher of the Year” award in 1997.

Mr. Wilson has had a number of papers published on law-relatedtopics in both scholarly and popular journals.

Copyright © 2015 by Penn Foster, Inc.

All rights reserved. No part of the material protected by this copyright may bereproduced or utilized in any form or by any means, electronic or mechanical,including photocopying, recording, or by any information storage and retrieval system, without permission in writing from the copyright owner.

Requests for permission to make copies of any part of the work should be mailed to Copyright Permissions, Penn Foster, 925 Oak Street, Scranton,Pennsylvania 18515.

Printed in the United States of America

All terms mentioned in this text that are known to be trademarks or service marks have been appropriately capitalized. Use of a term in this text should not beregarded as affecting the validity of any trademark or service mark.

INSTRUCTIONS TO STUDENTS 1

LESSON ASSIGNMENTS 5

LESSON 1: PROPERTY 7

LESSON 2: SALES AND CONSUMER PROTECTION 21

LESSON 3: NEGOTIABLE INSTRUMENTS 37

LESSON 4: INSURANCE, SECURED TRANSACTIONS, AND BANKRUPTCY 47

LESSON 5: TORTS AND CRIMES 59

GRADED PROJECT 67

SELF-CHECK ANSWERS 73

iii

Co

nt

en

ts

Co

nt

en

ts

INTRODUCTIONWelcome to Business Law 2, the second of two courses onthe legal environment of business. This course will completethe exploration of the legal aspects of business that youbegan with Business Law 1. In addition, this course offers a good overall picture of the American legal system and how it affects business on a daily basis.

This study guide, based on your textbook, Business Law withUCC Applications, is divided into five lessons. This studyguide provides your assignments for each lesson, self-checksand their answers, and your exams. Each lesson has severalassignments. To ensure you understand the material alongthe way, self-checks follow each assignment. The answers foreach self-check are at the back of this study guide.

OBJECTIVES When you complete this course, you’ll be able to

� Explain laws pertaining to ownership and transfer ofproperty

� Describe the general principles involved in wills, trusts,and estates

� Discuss the formation of sales and lease contracts andthe legal issues arising from those types of contracts

� Explain the purpose and types of negotiable instrumentsand the role they play in business

� Explain the rights of secured and unsecured creditorsand the consequences of bankruptcy

� Define risk management and discuss the purpose of dif-ferent types of insurance, including life, property,automobile, and health

� Discuss the principles of torts, the different types oftorts, and criminal law as it relates to business

1

Ins

tru

ctio

ns

Ins

tru

ctio

ns

Instructions to Students2

YOUR TEXTBOOKYour textbook for this course, Business Law with UCCApplications, Thirteenth Edition, by Gordon W. Brown and Paul A. Sukys, offers a solid introduction to the basicprinciples of business law. The study guide will help youunderstand the material, but your exams are based on yourtextbook and will test your understanding of the materialcovered in the textbook.

Your textbook’s table of contents in brief begins on page xviiand lists all the chapters and topics covered by the textbook.A more detailed table of contents appears on page xix.

At the end of each chapter, the textbook offers a summary of the material covered, a list of key terms, questions forreview and discussion, and cases for analysis. Each chapteralso contains a quick quiz with answers at the end of the chapter. A glossary appears at the end of the textbook. The appendices at the back of your textbook provide the U.S. Constitution and excerpts from the UniformCommercial Code.

Each chapter offers cases selected to illustrate the legal principles covered in the textbook. Some cases are fictional,but many are summaries from actual cases, affording you theopportunity to review real scenarios that pertain to the mate-rial covered in this course. When reading the case summaries, remember that they involve individuals and busi-nesses facing real problems. The rule of law affects all peopleas they engage in the activities of their daily lives, whetherdirectly or indirectly.

Although the assignments and self-checks may seem like alot to digest at first, don’t worry. The purpose of having several different types of questions is to expose you to morematerial, so when you take your exams, you’ll be prepared.

COURSE MATERIALS This course includes the following materials:

1. Your textbook, Business Law with UCC Applications,which contains the assigned readings, including casesummaries and helpful review questions

2. This study guide, which includes

� A list of lesson assignments

� Introductions to your lessons with discussion of themost crucial portions of the textbook, including,when relevant, new developments in business law

� Self-checks after each assignment and answers tothe self-checks

A STUDY PLAN Think of this study guide as a blueprint for your course.Read it carefully. Use the following procedures to receive themaximum benefit from your studies:

1. Read the lesson introduction in the study guide to get anoverview of what you’ll learn from the textbook, as wellas objectives.

2. Read the instructions for the assignment in the studyguide. First read the assignment in your study guide.Then read the assigned pages in your textbook to graspthe content in your textbook.

3. After you’ve finished each assignment, answer the questions provided in the self-check exercise in yourstudy guide. This will serve as a review of the materialcovered in the assignment. Then check your answerswith those given in the back of the study guide. If youmiss any questions, review the material covering thosequestions. The self-checks are designed to reveal weakpoints that you need to review. Don’t send your answersto the school.

Instructions to Students 3

4. Complete the online textbook chapter quizzes, as well asthe Quick Quizzes that appear throughout each textbookchapter that are assigned at the end of each readingassignment in your study guide. The link to the onlinetextbook chapter quiz is given at the end of each assign-ment. Answers to the Quick Quizzes are at the end ofeach textbook chapter, and feedback will be provided toyou after you take each online textbook chapter quiz.

5. After you’ve completed the self-check and the quizzes, goto the next assignment, following the procedure outlinedin steps 2–4.

6. Complete the first exam. After you take your exam, youcan move on to the next lesson.

7. Follow this procedure for all five lessons.

At any time, you can e-mail your instructor for assistance orinformation regarding the materials.

Now you’re ready to begin Lesson 1. Good luck!

Instructions to Students4

Remember to check your student portal regularly. Your instructor may

post additional resources that you can access to enhance your learn-

ing experience.

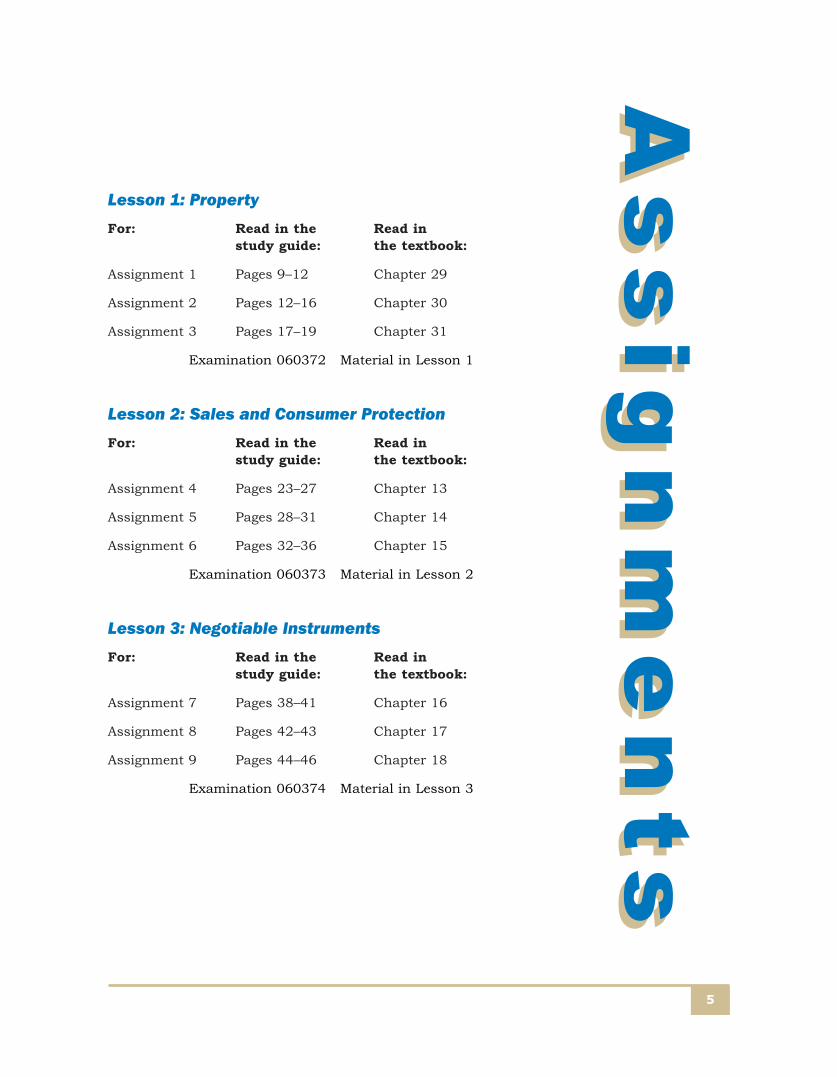

Lesson 1: PropertyFor: Read in the Read in study guide: the textbook:

Assignment 1 Pages 9–12 Chapter 29

Assignment 2 Pages 12–16 Chapter 30

Assignment 3 Pages 17–19 Chapter 31

Examination 060372 Material in Lesson 1

Lesson 2: Sales and Consumer ProtectionFor: Read in the Read in study guide: the textbook:

Assignment 4 Pages 23–27 Chapter 13

Assignment 5 Pages 28–31 Chapter 14

Assignment 6 Pages 32–36 Chapter 15

Examination 060373 Material in Lesson 2

Lesson 3: Negotiable InstrumentsFor: Read in the Read in study guide: the textbook:

Assignment 7 Pages 38–41 Chapter 16

Assignment 8 Pages 42–43 Chapter 17

Assignment 9 Pages 44–46 Chapter 18

Examination 060374 Material in Lesson 3

5

As

sig

nm

en

tsA

ss

ign

me

nts

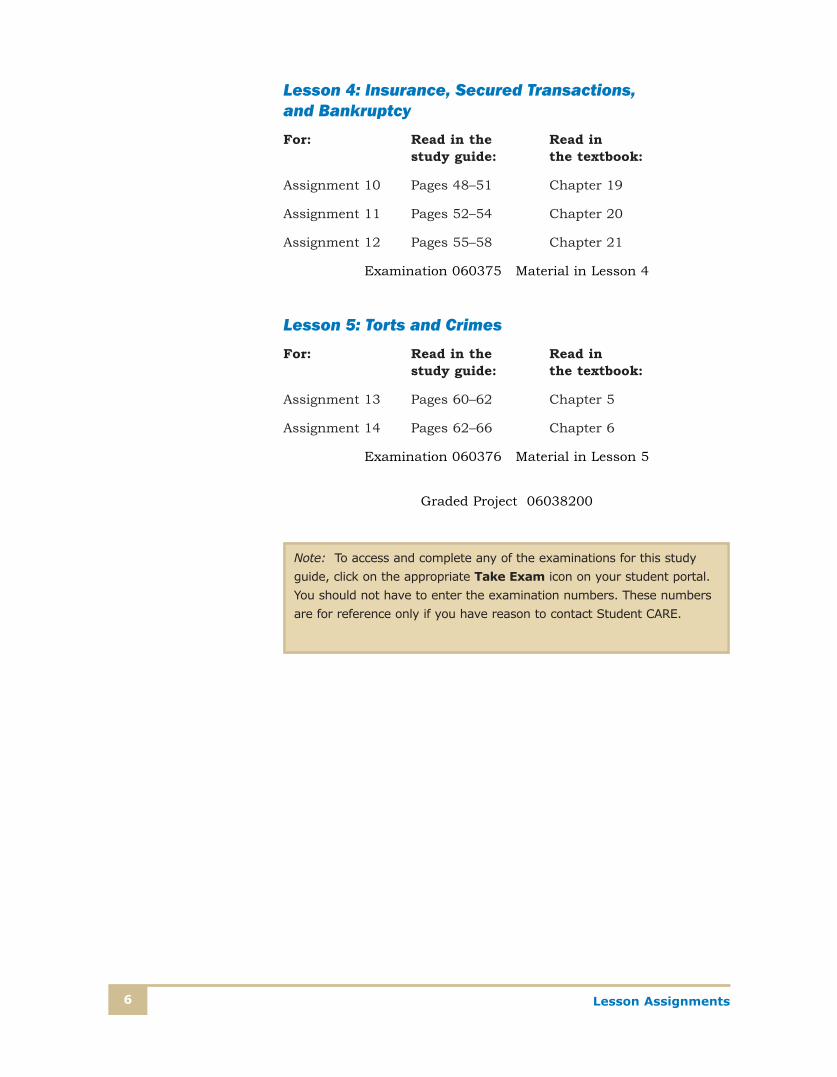

Lesson 4: Insurance, Secured Transactions, and BankruptcyFor: Read in the Read in study guide: the textbook:

Assignment 10 Pages 48–51 Chapter 19

Assignment 11 Pages 52–54 Chapter 20

Assignment 12 Pages 55–58 Chapter 21

Examination 060375 Material in Lesson 4

Lesson 5: Torts and CrimesFor: Read in the Read in study guide: the textbook:

Assignment 13 Pages 60–62 Chapter 5

Assignment 14 Pages 62–66 Chapter 6

Examination 060376 Material in Lesson 5

Graded Project 06038200

Lesson Assignments6

Note: To access and complete any of the examinations for this study

guide, click on the appropriate Take Exam icon on your student portal.

You should not have to enter the examination numbers. These numbers

are for reference only if you have reason to contact Student CARE.

7

Le

ss

on

1L

es

so

n 1

Property

INTRODUCTIONLesson 1 introduces you to the law of property. You’ll learnthat law divides property into two types: real property andpersonal property. You’ll study the law as it pertains to eachtype of property. You’ll also study bailment, which is the tem-porary transfer of personal property to another. You’ll learnabout landlord-tenant law. Finally, you’ll study the law thatgoverns the transfer of property on death and law concerningtrusts.

OBJECTIVESWhen you complete this lesson, you’ll be able to

� Explain ownership of personal property

� Describe the law concerning property that has been lost,misplaced, or abandoned

� Discuss laws related to stolen and gifted personal property

� Describe intangible personal property, such as patents,copyrights, trademarks, and trade secrets

� Define bailment and describe types of bailment and howeach type differs in terms of legal duties created

� Discuss special bailment situations involving innkeepers,carriers, and warehousers

� Discuss real property and the main types of estates inreal property

� Explain how the law on real property treats trees andvegetation, air rights, subterranean rights, water rights,and fixtures

� Define and give examples of easements

Business Law 28

� Explain different types of co-ownership, including jointtenancy, tenancy in common, tenancy by the entirety,community property, and tenancy in partnership

� Explain the methods by which title to real property isacquired, including the differences in acquiring propertyby deed, reason of death, or adverse possession

� Discuss how zoning laws affect property rights

� Explain eminent domain and its use by government toacquire real property for a public purpose

� Define the relationship between a landlord and a tenant,and describe a landlord’s duties and a tenant’s duties

� Differentiate among leasing, licensing, and lodging

� Explain the features of different types of leasehold interests, including tenancy at will, tenancy for years,periodic tenancy, and tenancy at sufferance

� Discuss common terms appearing in a lease agreementand the process of eviction

� Explain probate law and how it may relate to business

� Discuss advance directives and what happens to property when a person dies without a will

� Explain laws that pertain to wills, laws that protect the interest of spouses or children in the estates of decedents, how wills are executed and changed, andgrounds for contesting a will

� Discuss problems arising when people die simultane-ously and what’s involved in settling an estate

� Discuss the law of trusts and common types of trusts

Lesson 1 9

ASSIGNMENT 1Read this introduction to Assignment 1. Then read Chapter 29of your textbook.

Chapter 29 introduces you to personal property and the dif-ferent ways to own personal property. When an individualowns property, that property is owned in severalty. Whenmore than one person owns property, that property is ownedin cotenancy. Cotenants can own as tenants in common or asjoint tenants (also called tenants with right of survivorship).Joint tenants are distinguished from tenants in common inthat when one joint tenant dies, his or her share passes tothe survivor automatically.

Nine states recognize a form of ownership called communityproperty, in which property (except a gift or inheritance)acquired by either spouse during the marriage belongs toboth spouses equally. Spouses may bequeath their share ofcommunity property by will to whomever they choose, but ifthey die without a will, the property passes by survivorship tothe surviving spouse.

There are special rules for lost and abandoned property.Someone who finds lost property becomes the owner aftermaking reasonable but unsuccessful efforts to find the origi-nal owner. When property is stolen, a thief doesn’t therebyacquire title and is incapable of transferring title to anyone.Abandoned property, if proven abandoned by clear and con-vincing evidence, belongs to whoever finds it. The right toabandoned shipwrecks outside the boundaries of a state isgoverned by the law of finds or the law of salvage. If an abandoned shipwreck is found in the submerged land of anystate, the Abandoned Shipwreck Act of 1987 applies ratherthan the law of finds or the law of salvage.

Personal property can be gifted. The donor is the person making the gift, and the donee is the person receiving thegift. The gift is complete if the donor intended to make a giftand delivered the gift, and the donee accepted the gift.

The Uniform Transfers to Minors Act establishes proceduresto protect the rights of minors who are donees. Minors areassured that gifts to them will be either used for their benefit

Business Law 210

or turned over to them when they become adults. The IRShas special kiddie tax rules that determine how much of theincome is taxed to the child and how much to the parent.

Intellectual property is a kind of intangible property. Patentsgive inventors exclusive rights, for a time, to processes,machines, chemical formulas, and articles of manufacture.Copyrights protect the work of authors, artists, musicians,and software designers from unauthorized reproduction,republication, or sale. The owner of a trademark can registerthat trademark and thereby protect the exclusive right to usethat trademark. However, companies may lose trademarkprotection if the trademark becomes a popular generic termby use of a large segment of the public.

Bailment involves transfer of possession of personal propertytemporarily with the intent that it be returned later. Thebailor is the person transferring possession. The bailee is the person temporarily receiving possession. Bailments aredistinguished by whom they benefit. Bailment could benefitonly the bailor—for example, asking a friend to mail you apackage as a favor. Bailment could benefit only the bailee—for example, your neighbor borrowing your wheelbarrow.Mutual-benefit bailments benefit both parties—for example,leaving your clothes at the dry cleaners (you benefit fromhaving your clothes cleaned, and the cleaner benefits byreceiving payment for the service).

Traditionally the type of care a bailee had to exercise withregard to the property transferred depended on the type ofbailment. If the bailment benefited only the bailee, great carewas required. If it benefited only the bailor, slight care wasrequired. If it benefited both, ordinary care was required.Today, many jurisdictions simply apply a reasonable carestandard to all types of bailments.

Ordinarily, a plaintiff claiming property damage caused bynegligence has the burden to prove negligence. However,when property in the possession of a bailee is damaged, theburden of proof is shifted to the bailee to prove that he or shewasn’t negligent.

Lesson 1 11

Certain types of bailees have special additional duties. Undercommon law, innkeepers have a duty to provide accommoda-tions if they’re available and serve as insurers for theirguests’ property. Innkeepers must use reasonable care inprotecting guests from harm, must respect guests’ privacy,and must not discriminate based on race, creed, color, sex, or ethnicity, pursuant to the Civil Rights Act of 1964.Innkeepers may, however, turn away those whose presencemight endanger the other guests.

Common carriers also are a special type of bailee. With cer-tain exceptions, common carriers, whether negligent or not,are insurers of all goods accepted for shipment. They’re notresponsible for acts of god, acts of public enemies, acts ofpublic authorities, acts of the shipper, or damages caused bythe inherent nature of the item being shipped.

Warehousers are also a type of bailee. A public warehouse isa warehouse that any member of the public may pay to storegoods in. A private warehouse is a warehouse not open to thepublic. Warehousers must use reasonable care and are liablefor damage caused by failure to exercise reasonable care.

Warehousers who aren’t paid have a lien on goods stored inthe warehouse and may retain possession of them until paid.The lien covers the storage charge and other charges, such as transportation, insurance, and expenses incurred to pre-serve the goods. The lien is lost if the warehouser voluntarilygives up possession of the goods or wrongfully fails to deliverpossession.

Review and ApplicationWhen you finish reading the chapter,

� Answer the Quick Quiz questions on pages 638 and 649.Check your answers on page 652. These quizzes will notbe scored so don’t send them to the school; they’re foryou to gauge your progress. If there are any questionsyou don’t understand, refer back to the textbook andreread the assignment.

Business Law 212

� Complete the online textbook chapter quiz athttp://highered.mheducation.com/sites/0073524956/student_view0/chapter29/chapter_quiz.html. Feedback onyour answers will be provided once you finish the quizand click the Submit Answers button.

� Take a moment to complete Self-Check 1. You can checkyour answers by turning to the back of this study guide.If you have trouble with any of the material, review thosesections in your text.

ASSIGNMENT 2Read this introduction to Assignment 2. Then read Chapter 30of your textbook.

Chapter 30 introduces you to real property. Real property island and things permanently attached to land. Real propertyincludes things on the surface, such as buildings, fences,and trees; things below the surface, such as minerals; andthe airspace above the surface. Landowners own the airspaceas high as they can effectively possess or reasonably control.

Self-Check 1At the end of each section of Business Law 2, you’ll be asked to pause and check

your understanding of what you’ve just read by completing a “Self-Check” exercise.

Answering these questions will help you review what you’ve studied so far. Please

complete Self-Check 1 now.

Answer the “Questions for Review and Discussion” on page 650 of your textbook.

Check your answers with those on page 73.

Lesson 1 13

Trees are a kind of vegetation, but not all vegetation is realproperty. Trees, shrubs, vineyards, and perennial crops aretreated as real property, but annual crops are personal property.

Fixtures are items that were formerly personal property butthat have become attached to real property. Whether an itemis a fixture depends on various factors a court will consider.Those factors include whether the item has been temporarilyor permanently installed, whether the item has been adaptedto the intended use of the real property, and the intent of theparty at the time the item was attached to the real property.

Easements are rights to use property for a limited purpose—for example, an easement for ingress and egress, whichmeans a right to cross someone else’s property to go into and come out of your own property. An easement can be created by grant (expressly conveying the easement to some-one), reservation (retaining an easement right in property one has outconveyed), or implication (implied under the circumstances).

In law, estate is used in various ways. One use of estate is todescribe the degree of ownership of real property. A leaseholdestate gives one the right to occupy property as a tenan. Afreehold estate is a greater degree of ownership and consistsprimarily of two types: a life estate, which is the right to ownfor life, and a fee simple, which is an absolute and unlimitedownership. Fee simple estates pass on death to whoevertakes the decedent’s estate.

Dower for widows and curtesy for widowers are common-lawrights to a life estate in one-third of the real estate owned bythe spouse during the marriage. Many states have eliminatedor modified dower and curtesy rights.

Tenancy by the entirety may be held only by a husband and awife. On the death of one, his or her interest passes to thesurviving spouse. A tenancy in partnership is another type ofownership that exists in some states.

Ownership of real property may be acquired in three ways.First, ownership may be acquired by deed. The conveyancemay be a sale or a gift. Different types of deeds can be distin-guished by the extent that title is warranted by the grantor.

Business Law 214

These types include general warranty deeds, special warrantydeeds, bargain-and-sale deeds, and quitclaim deeds. Second,ownership may be acquired by reason of death, and the propertymay pass by will or by descent in the case of intestacy. Third,ownership may be acquired by adverse possession, which occurswhen a nonowner, for a period set by applicable state statutes,continuously, openly, and without permission of the owner pos-sesses property. After the requisite period has run, the possessorbecomes the new owner.

Zoning is governmental regulation of the use of property.Properties are classified or zoned into various categories, andonly certain types of use are permitted in each zone. If one hasestablished a use that was permitted at the time, but due tochanges in zoning is no longer permitted, the use is called a non-conforming use and the owner may continue such use. A varianceis permission granted by zoning authorities to engage in a usenot normally permitted under applicable zoning ordinances.

Eminent domain is the power government has to take privateproperty for a public purpose. An example would be taking landto build a road or a public park. The government must pay fairvalue for the land it takes.

A leasehold is an interest in real estate, but the landlord-tenant relationship also is a contract in which the owner of thereal estate allows the tenant to have possession for a period inexchange for consideration. To create the relationship, five thingsare necessary: (1) consent of the landlord to the occupancy, (2)transfer of possession and control to the tenant in subordinationto the landlord’s rights, (3) a landlord’s right to return of theproperty at the end of the lease, which is called a reversion, (4)creation of an ownership interest in the tenant called a leasehold,and (5) satisfaction of all the other elements necessary to create acontract (mutual assent, competent parties, consideration andlawful purpose).

A license gives permission to someone to perform acts on prop-erty that would otherwise be trespass but doesn’t confer apossessory estate and is usually not transferable. It doesn’trequire consideration and need not delineate the space to beoccupied or used. In contrast, a lease gives exclusive possession,describes the property leased, states the term of the lease andrent to be paid, and, in some cases, may have to

Lesson 1 15

be in writing. A lease also is different from lodging. A lodger is atype of licensee with the right to use property but not to possessit.

There are four types of tenancy. A tenancy for years is an estatefor a fixed time period—it may be less than a year. A periodic ten-ancy is a fixed-period tenancy that continues for successiveperiods until one of the parties chooses to terminate the arrange-ment. A tenancy at will is a tenancy for which no term has beenfixed. Tenancy at sufferance is a way of describing someone whowrongfully remains in possession after his or her tenancy expires.

To create a lease, the parties must define the bounds of the prop-erty being leased, identify the term of the lease, and agree on adefinite rent.

A tenant may transfer the right to occupy property by assignmentor by sublease. Assignment is a transfer of the tenant’s rightsunder the lease. A sublease is a new lease between the tenant andthe sublessee. If the transfer of the right to occupy property is forless than the remainder of the term, or there’s any sort of rever-sion right retained by the tenant, the arrangement will be treatedas a sublease. Leases may require that the landlord’s approval beobtained before assignment or subleasing may occur.

When dwellings are rented, most states imply a warranty by thelandlord that the property is habitable.

Landlords have certain duties under leases. These duties includea duty to refrain from violating laws against discrimination, to make repairs necessary to maintain the habit-ability of the premises, and to deliver peaceful possession or quietenjoyment. Landlords may not commingle security deposits andmust return the balance of any security deposit to the tenant atthe end of the lease.

Tenants also have duties, including paying the rent; complyingwith any conditions and covenants in the lease, such as keepingthe property clean; not committing waste, which is damaging theproperty being rented; and returning to the landlord all fixtures(other than trade fixtures) added by the tenant during the term ofthe lease.

Landlords are responsible for harm caused by defects in commonareas if the landlord was negligent. Tenants are responsible forharm caused by defects in areas controlled by the tenant.

Business Law 216

Landlords have the right to evict tenants who violate theterms of the lease. Some states permit landlords to enterwrongfully held premises and retake possession if it can bedone peacefully. The common law name for a lawsuit broughtto evict is ejectment. Unlawful detainer is a legal proceedingwith the same purpose but accomplishes its objective morequickly. Strict notice requirements apply.

Review and ApplicationWhen you finish reading the chapter,

� Answer the Quick Quiz questions on pages 658, 661,666, 671, and 674. Check your answers on page 677.These quizzes will not be scored so don’t send them tothe school; they’re for you to gauge your progress. Ifthere are any questions you don’t understand, refer backto the textbook and reread the assignment.

� Complete the online textbook chapter quiz athttp://highered.mheducation.com/sites/0073524956/student_view0/chapter30/chapter_quiz.html. Feedback onyour answers will be provided once you finish the quizand click the Submit Answers button.

� Take a moment to complete Self-Check 2. You can checkyour answers by turning to the back of this study guide.If you have trouble with any of the material, review thosesections in your text.

Self-Check 2Answer the “Questions for Review and Discussion” on page 676 of your textbook.

Check your answers with those on page 75.

Lesson 1 17

ASSIGNMENT 3Read this introduction to Assignment 3. Then read Chapter 31of your textbook.

Chapter 31 introduces you to will, trusts, and estates. Thetext will explain probate law and how it may relate to busi-ness. Probate is the court supervised administration of adecedent’s estate. Each state’s law is different on the proce-dures involved, so you’ll need to check your state’s law whenaddressing probate matters. A decedent’s property is distrib-uted according to the instructions in the decedent’s will, or ifthere’s no will, according to the law of intestate succession.

Probate is relevant to business entities in a variety of ways.All businesses are owned by people in one way or another,and their interest in a business—whether sole proprietorship,partnership, or stock in a corporation—passes on death tosomeone. In addition, businesses who are creditors may haveclaims against estates for business-related debts. Also, thedeath of a partner dissolves a partnership, absent an agree-ment to the contrary, and the deceased partner’s estate hasthe right to be paid the value of the partner’s share or havethe partnership liquidated and be paid from the net proceeds.

Advance medical directives are written instructions for futuremedical care in the event the patient becomes unable to givesuch instructions. The most common use of advance medicaldirectives is a living will, which expresses a person’s wishesregarding whether he or she, if in a terminal condition or per-sistent vegetative state, wishes to be allowed to die a naturaldeath rather than being kept alive by artificial means.Another way to accomplish these purposes is to execute ahealth care proxy, which authorizes another person to makemedical decisions in the event of incapacity.

A durable power of attorney is a power of attorney that’s notaffected by the disability of the principal.

A will, also called a last will and testament, is a documentthat governs transfer of one’s property at death. A personwho dies with a will is testate, a person who dies without awill dies intestate. A person who makes a will is a testator.Any competent adult may make a will. Competency to make a

Business Law 218

will requires that the testator generally knows the nature andextent of the property he or she owns, knows who would bethe natural recipients of the estate, is free from delusionsthat might influence the terms of the will, and intends tomake a will.

State laws differ on the formal requirements for executing awill, but in general, it must be in writing, signed by the testa-tor, and witnessed in the testator’s presence by the numberof witnesses required under state law.

State laws create various types of protection for the familywhen a decedent dies. These include family allowances, thehomestead exemption, exempt property, dower and courtesy,and the right of a surviving spouse to elect against the willand take a forced share of the estate. These devices aredescribed in your text.

In general, children may be omitted from a will. Omitted children must prove they were mistakenly rather than inten-tionally omitted to receive a share of the estate. To avoidconfusion about whether the omission was a mistake, a testator should state specifically that a child is being omittedintentionally. To the extent children have rights in an estate,adopted children are treated the same as children of thebody.

Sometimes people make wills and change their minds. Willsmay be revoked by burning, tearing, canceling, or obliteratingthe will with intent to revoke. They also may be revoked byexecuting another will. In some states, marriage, divorce, orannulment may revoke a will in whole or in part.

When people die owning assets, their estate must be pro-bated. Heirs are notified, and an executor or administrator is appointed to settle the estate. Settling the estate involvescollecting the assets, paying debts, paying taxes, and distrib-uting what remains according to the will or the law ofintestate succession if the person dies without a will.

A trust divides ownership between a trustee, who holds legaltitle, and a beneficiary, who holds equitable or beneficial title.This allows the trustee to control the property for the benefitof the beneficiary.

Lesson 1 19

Review and ApplicationWhen you finish reading the chapter,

� Answer the Quick Quiz questions on pages 680, 689,692, and 694. Check your answers on page 697. Thesequizzes will not be scored so don’t send them to theschool; they’re for you to gauge your progress. If thereare any questions you don’t understand, refer back tothe textbook and reread the assignment.

� Complete the online textbook chapter quiz athttp://highered.mheducation.com/sites/0073524956/student_view0/chapter31/chapter_quiz.html. Feedback onyour answers will be provided once you finish the quizand click the Submit Answers button.

� Take a moment to complete Self-Check 3. You can checkyour answers by turning to the back of this study guide.If you have trouble with any of the material, review thosesections in your text.

Then review the material you’ve learned in this study guideand the assigned pages in your textbook for Assignments 1–3. When you’re sure that you completely understand theinformation presented in those assignments, complete yourmultiple-choice examination for Lesson 1.

Self-Check 3 Answer the “Questions for Review and Discussion” on pages 695–696 of your textbook.

Check your answers with those on page 78.

Business Law 220

NOTES

21

Le

ss

on

2L

es

so

n 2

Sales and ConsumerProtection

INTRODUCTIONLesson 2 introduces you to sales and consumer protection.Much of contract and property law provides the legal supportfor commercial activity, and a significant portion of commer-cial activity involves sale or lease of goods. In this lesson,you’ll learn that the Uniform Commercial Code (UCC) pro-vides statutory law that governs the sale and lease of goods.Warranties are representations regarding the quality or performance of a product. You’ll study laws applicable towarranties.

Products can cause injury to persons who buy them or usethem. Products also can injure innocent bystanders. You’llstudy the law pertaining to product liability.

Consumers can be harmed in commercial transactions. You’ll learn about laws designed to protect consumers.

OBJECTIVESWhen you complete this lesson, you’ll be able to

� Explain the basic principles governing the sale and leaseof goods

� Discuss how the law treats contracts created for sale ofgoods and services

� Discuss the special rules that apply to sales contractsand how those rules may differ from common law con-tract rules

� Discuss UCC writing requirements for sales contractsand how they may differ from common law rules

� Explain void and voidable title

Business Law 222

� Discuss the relationship of passage of title and risk of loss

� Discuss the rules for risk of loss when the goods are delivered

� Explain the law concerning sales with right of return

� Explain how the UCC defines the obligations of sellerand buyer

� Describe tender of delivery, the rules concerning it, andhow it affects the duties of the parties

� Identify the rights of buyers when the goods that aredelivered are nonconforming

� Explain the seller’s right to cure an improper tender

� Discuss breach of contract under the UCC, includinganticipatory breach, and identify remedies availableunder the UCC for breach

� Explain the difference between express and implied warranties

� Identify the three automatic implied warranties underthe UCC

� Discuss and differentiate the three theories of productliability: warranty, negligence, and strict liability

� Discuss protections afforded consumers against unfair ordeceptive acts or practices

� Explain the role of the Federal Trade Commission in con-sumer protection

� Discuss the main features of the Consumer ProductSafety Act and the Consumer Leasing Act

� Describe important consumer-protection provisions thatappear in other federal laws

Lesson 2 23

ASSIGNMENT 4Read this introduction to Assignment 4. Then read Chapter 13of your textbook.

Chapter 13 introduces you to the law on sale and lease ofgoods. The UCC governs the law of contracts for sale andlease of goods. The law applies to transactions between indi-viduals, between businesses, and between consumers andbusinesses. In some cases, there may be special rules fortransactions between merchants.

In general, goods are movable, tangible property. Examplesare cars, clothes, and furniture. Laws concerning sale ofgoods for the most part apply to future goods as well, such as minerals in the group that will be mined, fish in the sea,or timber yet to be cut.

Contracts for sale of goods can involve a sale of goodspresently or it may contemplate sale of goods in the future.Both types of contracts are contracts for sale covered by the UCC.

Sometimes contracts contemplate both sale of goods and provision of services. When that’s the case, a court will lookat which element dominates the contract to classify it as acontract for sale of goods or a contract for services.

The UCC has special rules that apply to sale of goods that, in some cases, may differ from the common law that governsother contracts. Many of these rules are intended to make it easier to create contracts without following common lawcontract rules strictly. Examples of special rules in the UCCapplicable to sale of goods include the following:

� No consideration is necessary to modify a contract forthe sale of goods. Under the common law, additional ornew consideration is required to modify a contract.

� The UCC imposes a duty on the parties to act and dealwith each other in good faith and fairly.

� The UCC expressly permits course of dealing and usageof trade to be considered when interpreting the terms ofa contract.

Business Law 224

� Sales contracts can be created in any matter that showsthe parties reached an agreement.

� Under common law, contracts couldn’t be created unlessthe material terms were agreed on. Under the UCC, con-tracts can be created even if all terms aren’t stated, if theparties intend to contract. Thus, for example, a contractcould be created even though the price or time for deliv-ery wasn’t discussed. The UCC has rules used to supplythe missing terms. For example, if the price isn’t stated,it will be a “reasonable” price at the time of delivery.

� Unless otherwise specified in the offer, acceptance can bein any manner sufficient to show agreement, includingshipment of the goods.

� Under common law, to create an option contract, consideration had to be given in exchange for holding the offer open. Under the UCC, a written promise by amerchant to hold an offer open is binding without anyconsideration.

� Output contracts obligate sale and purchase not of a definite number but in terms of output produced.Requirement contracts similarly define quantity in termsof need rather than a definite number. Such contractsweren’t permitted under common law because the termswere too indefinite. However, output and requirementcontracts are allowed under the UCC as long as the parties deal in good faith and according to reasonableexpectations.

� Under common law, acceptance had to be a “mirrorimage” of the offer, neither varying nor adding to theterms of the offer. Under the UCC, the presence of minordifferences in the acceptance doesn’t make the accept-ance ineffective. However the different terms don’tbecome part of the contract unless both parties are mer-chants, the differences aren’t material, and no objectionis made within a reasonable time.

The statute of frauds is a list of contracts that have to be inwriting to be enforceable. The UCC law on sale of goods hasits own writing requirement. Contracts for sale of goods for

Lesson 2 25

$500 or more, or lease of goods for $1,000 or more, must bein writing to be enforceable. Like with the statute of frauds,the writing must be signed by the party against whomenforcement is sought. However, the requirements of thewriting are less stringent than under the common law, andthere are exceptions to the writing requirements. For exam-ple, if both parties are merchants and one of the partiesreceives written confirmation and doesn’t object to it in writ-ing within 10 days, the contract is enforceable against theparty who didn’t object to the confirmation. You’ll want tonote the other exceptions discussed in your textbook.

Title is the right to ownership of goods. A bill of sale is a written evidence of transfer of such ownership from one person to another. However, a bill of sale doesn’t prove thatthe possessor has good title. What if the goods were stolen or obtained by fraud and then transferred to an innocentpurchaser? Does the innocent purchaser have good title?This depends on whether the transferor’s title was void orvoidable.

Void title isn’t title, has never been title, and can never betitle. Voidable title means the title may be voided if one of the parties acts to void it.

If goods are stolen, title is void. The innocent purchaser cansue the person who sold the stolen item to him or her, butthe true owner is entitled to return of the item. Voidable titlecan arise when property is obtained by fraud, misrepresenta-tion, mutual mistake, undue influence, or duress. Voidabletitle means title can be voided if the injured party acts to voidit. Title acquired from a person lacking capacity, such as aminor or mentally impaired person, is also voidable. Voidabletitle is valid title until it’s voided.

When goods are entrusted to a merchant who in turn sellsthem in the ordinary course of business to someone whodoesn’t know about the real owner’s rights, the originalowner loses title. The owner can sue the merchant if sale waswrongful, but the purchaser has good title. This rule allowscustomers to have confidence that what they buy will belongto them. An exception to the rule is stolen property.

Business Law 226

If goods are lost, damaged, stolen, or destroyed between thetime delivery begins and delivery is completed, who bears theloss? The UCC addresses this question. Except when goodsare to be picked up by the buyer, and a few other situations,risk of loss passes when title passes. Thus, one needs toknow when title passes from seller to buyer.

A shipment contract is one in which the seller delivers thegoods via a common carrier. In a shipment contract, title andrisk pass when the goods are given to a common carrier fordelivery. If the terms of shipment don’t specify a shippingpoint or destination, it’s assumed to be a shipment contract.

In a destination contract, the seller’s obligation is to deliverthe goods to a destination. Title and risk pass when the sellertenders the goods at the place of destination.

Where delivery isn’t required and buyer picks up the goods,title passes to the buyer when the contract is made, but riskof loss passes when the buyer receives the goods. If the sellerisn’t a merchant, the risk passes when seller tenders thegoods to the buyer.

Some types of goods are sold with documents of title thatauthorize the buyer to pick up the goods at a warehouse. Insuch cases, receipt of the document of title is the event thatcauses title and risk to pass.

These are default rules, and in general, the parties canexpressly agree on when risk and title pass. However, if theagreement allows the seller to retain title after the goods areshipped, title passes to buyer at shipment, and the seller istreated as having a security interest in the goods rather thanhaving title.

Sales that permit conforming goods to be returned are “saleson approval” when the goods are for the buyer’s use, and riskand title don’t pass until buyer approves the goods. If thereturn is permitted and the goods are for resale, these are“sales or return” and title and risk pass at the time of saleand if returned are returned at buyer’s risk and expense.

Buyers may insure goods from the moment the contract ismade and the goods are identified to the contract, eventhough title has yet to pass.

Lesson 2 27

Review and ApplicationWhen you finish reading the chapter,

� Answer the Quick Quiz questions on pages 279, 283,288, 293, and 294. Check your answers on page 297.These quizzes will not be scored so don’t send them tothe school; they’re for you to gauge your progress. Ifthere are any questions you don’t understand, refer backto the textbook and reread the assignment.

� Complete the online textbook chapter quiz athttp://highered.mheducation.com/sites/0073524956/student_view0/chapter13/chapter_quiz.html. Feedback onyour answers will be provided once you finish the quizand click the Submit Answers button.

� Take a moment to complete Self-Check 4. You can checkyour answers by turning to the back of this study guide.If you have trouble with any of the material, review thosesections in your text.

Self-Check 4 Answer the “Questions for Review and Discussion” on page 296 of your textbook.

Check your answers with those on page 81.

Business Law 228

ASSIGNMENT 5Read this introduction to Assignment 5. Then read Chapter 14of your textbook.

Chapter 14 concerns performance and breach of the obliga-tions under a sales contract. The UCC defines the obligationsof parties to a sales contract in a very simple manner: Theseller is obligated to tender conforming goods, and the buyeris obligated to accept and pay for them. Conforming goodsmeans that the goods conform to the requirements of thesales contract.

To tender performance is to attempt or offer to do what one is obligated to do under the sales contract. The seller mustmake tender of delivery, and the buyer must make tender ofpayment. If one party fails to make tender, that party can’tbring suit, even if the other party is in breach.

Tender of delivery requires that conforming goods be at the buyer’s disposition. Delivery must be at a reasonabletime, and the seller must be given notice of delivery. If it’s a shipment contract, tender of delivery is accomplished bydelivering the goods to a common carrier and contracting to have them transported to the buyer. If delivery is made by transporting the goods to a warehouse where the buyerwill pick them up, the seller must deliver to the buyer any documents necessary to claim the goods or obtainacknowledgment from the warehouse of the buyer’s right to claim them.

Tender of payment may be made in any manner that’s cus-tomary, such as a check, provided that buyer may demandlegal tender if the buyer gives the seller a reasonable time toobtain it.

A buyer has a duty to accept the goods but has an interven-ing right to inspect them before accepting or paying. Anexception exists for goods shipped cash on delivery (c.o.d.)or when the contract provides for payment against a docu-ment of title.

If the goods are nonconforming, the buyer may reject them oraccept them, or the buyer may accept any commercial unit or units and reject the other units. Rejection must occur

Lesson 2 29

within a reasonable time after delivery or tender. If goods are rejected, the buyer must notify the seller and identify the defect in what was tendered and give the seller a chance to correct the problem. The seller has a right to correct the problem if the time for performance hasn’t expired. This rightexists until the contract time has expired.

The buyer must hold rejected goods long enough to give theseller a chance to remove them. If the seller gives no instruc-tions about what to do with the goods, the buyer may storethem, ship them back to the seller, or resell them, all to theseller’s account. If the buyer is a merchant, there are additionalduties: the buyer must follow seller’s reasonable instructionsregarding disposition of the goods; if there are no instructions,the buyer has a duty to make reasonable attempts to sell thegoods if they’re perishable or likely to decline in value quickly.

Acceptance occurs when the buyer signifies that the goods areconforming, signifies a willingness to accept the goods thoughnot conforming, fails to reject them within a reasonable time, oracts with regard to the goods in a way that’s inconsistent withthe seller’s ownership.

The UCC provides a number of remedies for the seller when thebuyer breaches: withhold delivery of goods, stop delivery ofgoods in transit, resell the goods, sue for damages (differencebetween market price and contract price or the profit sellerwould have made had the contract been performed), sue for incidental damages that result indirectly from the breach, suefor the price under the contract, or cancel the contract.

The UCC also provides remedies for the buyer when the sellerbreaches: cover (purchase the same goods from someone else)and sue for the difference between the contract price and the cost of the cover, sue for damages (difference between con-tract price and market price) and incidental and consequentialdamages, keep the goods and seek an adjustment in the price,or sue for specific performance if money damages are inade-quate, such as when the goods are unique, rare, or speciallymanufactured.

Warranty is another name for a guarantee. It’s a representationof fact on which the contract is based. Often the warranty concerns the quality of a product. The words warranty and

Business Law 230

guarantee don’t have to be used. What matters is whether theseller has made a statement of fact or promise concerning theproduct.

Express warranties can arise from express statements of factor promise by a description of the goods or by use of a sam-ple or model. The federal Magnuson-Moss Warranty Act isdesigned to prevent deceptive warranty practices and provideconsumers with information about warranties on the prod-ucts they purchase. Under the act, when a written warrantyis given, it must be made available to the consumer beforethe consumer purchases, must state the terms and condi-tions in simple, understandable language, and must statewhether it’s a full warranty or a limited warranty.

A full warranty is one under which the product will berepaired or replaced without charge within a reasonable timeif it proves to be defective. A limited warranty is any warrantythat’s not a full warranty.

In addition to express warranties that a seller may make,there are three automatic implied warranties under the UCC. The first is warranty of title. Under the implied war-ranty of title, the seller warrants that the seller is transferringgood title, free of all claims. The second is warranty of merchantability. Warranty of merchantability applies to mer-chants selling goods and means the goods are of ordinaryquality and would pass without objection in the trade underthe contract description, be of fair average quality if fungiblegoods, be fit for the normal purposes for which such goodsare used, be of even kind quality and quantity, be properlypackaged, and conform to any representations about thegoods made on the packaging. The third is warranty of fit-ness for a particular purpose. This arises during negotiationsbetween buyer and seller if buyer makes known a purposeand relies upon seller’s knowledge to choose the product.

Implied warranties of merchantability don’t apply to obviousdefects that would be discovered on examination if the buyerhas the opportunity to examine. Implied warranties also may be disclaimed. To disclaim merchantability, the word merchantability must be used, and if in writing, the dis-claimer must be conspicuous. To disclaim fitness for a

Lesson 2 31

particular purpose, the disclaimer must be written and con-spicuous. Phrases like as is and with all its faults are alsoused to make disclaimers.

If warranties are breached, the buyer must give notice withina reasonable time after the defect was discovered or shouldhave been discovered, or the buyer may lose the right to suefor damages.

Review and ApplicationWhen you finish reading the chapter,

� Answer the Quick Quiz questions on pages 303, 309,and 314. Check your answers on page 316. Thesequizzes will not be scored so don’t send them to theschool; they’re for you to gauge your progress. If thereare any questions you don’t understand, refer back tothe textbook and reread the assignment.

� Complete the online textbook chapter quiz athttp://highered.mheducation.com/sites/0073524956/student_view0/chapter14/chapter_quiz.html. Feedback onyour answers will be provided once you finish the quizand click the Submit Answers button.

� Take a moment to complete Self-Check 5. You can checkyour answers by turning to the back of this study guide.If you have trouble with any of the material, review thosesections in your text.

Self-Check 5Answer the “Questions for Review and Discussion” on page 315 of your textbook.

Check your answers with those on page 82.

Business Law 232

ASSIGNMENT 6Read this introduction to Assignment 6. Then read Chapter 15of your textbook.

Chapter 15 concerns product liability and consumer protection. In addition to suing under the theory of breach of warranty, a person harmed by a product may sue in tortunder negligence theory or under strict liability. Negligencetheory requires proof that the manufacturer failed to exercisereasonable care. This may be difficult to prove sometimes as the consumer or user has no first-hand knowledge of howthe product was made. Under strict liability, the injured partymust prove that the product was sold in an unreasonablydangerous condition that proximately caused the injury.

Consumer protection laws apply to transactions betweenbusinesses and consumers. The Federal Trade Commission(FTC) Act prohibits unfair or deceptive practices in or affect-ing commerce. Unfair and deceptive practices can include

� Fraudulent misstatements that deceive

� False statements about the construction, durability, reliability, safety, strength, condition, or life expectancyof a product

� Failing to disclose facts that would cause a buyer not topurchase

Examples of unfair or deceptive acts include fraudulent mispresentations, bait-and-switch, odometer tampering, andsending unordered merchandize. Regarding the latter, therecipient may treat it as a gift or dispose of it however theychoose.

The FTC created a Used Car Rule that requires a buyer’sguide be posted on the window of the car disclosing the following:

� That the car is sold as is, with limited warranties only, or with full warranty

� The length of any express warranty, the systems covered,and the percentage of repair costs the buyer must pay

� A warning not to rely on spoken promises

Lesson 2 33

� A suggestion that consumers ask to have the vehicleinspected by their own mechanic

� A list of the 14 major systems of an automobile andsome of the principal defects that occur in these systems

Another rule created by the FTC is the Cooling-Off Rule,which applies to sales of goods or services of more than $25that occur away from the seller’s regular place of business,such as at the consumer’s home. Under this rule, the buyerhas three days to cancel the sale and must be given twocopies of a cancellation form, one of which can be sent to theseller to cancel the deal.

The FTC’s Negative Option Rule requires sellers of subscrip-tions, such as magazines or CD clubs, to tell subscribers:

� How many selections they must buy, if any

� How and when they can cancel membership

� How to notify the seller that they don’t want a selection

� When to return the negative option form to cancel shipment of a selection

� When they get credit for return of a selection

� How postage and handling costs are charged

� How often they’ll receive announcements and forms

The FTC’s Mail, Telephone, Internet, or Fax Rule requires sell-ers to ship orders within the time promised in advertisementsor, if none, within 30 days of receipt of the order. If there’s adelay, an option notice must be sent giving the option toaccept the delay or cancel the order.

The FTC’s Telemarketing Sales Rule does the following:

� Prohibits calling if the consumer hasn’t asked to becalled

� Restricts calling time to between 8:00 A.M. and 9:00 P.M.

� Requires telemarketers to disclose that it’s a sales call,the seller’s name, and what’s being sold before makingtheir pitch

Business Law 234

� Requires the consumer to be told, if it’s a prize promo-tion, that no purchase or payment is necessary to enteror win

� Prohibits misrepresentations

� Requires disclosure of total cost of product

� Prohibits withdrawal of money from consumer’s checkingaccount without express, verifiable authorization fromthe consumer

� Requires that certain services (credit repair, “recoveryroom,” and advance-fee loans) be performed before thecustomer is required to pay

The FTC’s 900-Telephone Number Rule requires that callersbe warned of the cost and given a chance to hang up beforecharges begin, that telephone companies block service to 900numbers if requested by the customer, and that customersbe sent annual pay-per-call disclosures. It also bars phonecompanies from disconnecting phone service to customerswho refuse to pay for 900-number calls.

The Can Spam Act requires unsolicited commercial e-mail betruthful and not use misleading subject lines or incorrectreturn addresses. E-mail containing pornography must bespecifically labeled in the subject line. Spammers are prohib-ited from harvesting e-mail addresses from chat rooms orother sites without permission. The FTC is authorized toestablish a Do-Not-E-mail Registry.

The FTC has Antislamming Rules to protect consumers whosetelephone service was changed without permission. The con-sumer need not pay for service up to 30 days after beingslammed. After that, you must pay for services to yourauthorized company at the authorized company’s rate ratherthan at the slammer’s rate.

The Consumer Product Safety Act protects consumers fromunreasonable risk of injury from hazardous products. The actapplies both to products made in America and imported thatare intended for personal use, consumption, or enjoyment.The Consumer Product Safety Commission has the power to

Lesson 2 35

create standards and rules and to enforce those rules withsanctions. The commission can seek injunctions, can banhazardous products, and can impose fines.

The Consumer Leasing Act requires disclosure of informationthat allows the buyer to compare the cost of leasing with thecost of buying.

The Truth-in-Lending Act requires creditors to disclose financecharges and the annual percentage rate (the true cost of thedebt when charges in addition to interest are factored in)before loaning to customers. Credit card holders aren’tresponsible for charges made on lost, stolen, or possibly misused cards after notifying the card company, and exposure for unauthorized charges is limited to $50.

The Equal Credit Opportunity Act prohibits denying creditbased on gender, marital status, color, race, religion, nationalorigin, ethnicity, age, or receipt of public assistance.

The Fair Debt Collection Practices Act prohibits debt collectorsfrom engaging in deceptive or abusive practices. Among theprohibited practices are overcharging, harassment, and dis-closing information about the debt to third parties.

Review and ApplicationWhen you finish reading the chapter,

� Answer the Quick Quiz questions on pages 323, 329,and 333. Check your answers on page 335. Thesequizzes will not be scored so don’t send them to theschool; they’re for you to gauge your progress. If thereare any questions you don’t understand, refer back tothe textbook and reread the assignment.

� Complete the online textbook chapter quiz athttp://highered.mheducation.com/sites/0073524956/student_view0/chapter15/chapter_quiz.html. Feedback onyour answers will be provided once you finish the quizand click the Submit Answers button.

Business Law 236

� Take a moment to complete Self-Check 6. You can checkyour answers by turning to the back of this study guide.If you have trouble with any of the material, review thosesections in your text.

Then review the material you’ve learned in this study guideand the assigned pages in your textbook for Assignments 4–6. When you’re sure that you completely understand theinformation presented in those assignments, complete yourmultiple-choice examination for Lesson 2.

Self-Check 6Answer questions in “Questions for Review and Discussion” on page 334 of your textbook.

Check your answers with those on page 85.

Negotiable Instruments

INTRODUCTIONNegotiable instruments are written documents that contain apromise or an order to pay money. In this lesson, you’ll learnabout the different types of negotiable instruments and therules governing them. You’ll learn how negotiable instru-ments are transferred. You’ll study the special protectionsafforded holders in due course. You’ll also study the lawsthat govern the relationships between banks and their depositors.

OBJECTIVESWhen you complete this lesson, you’ll be able to

� Identify the purpose of and parties to negotiable instruments

� Explain types of promise instruments and order instruments and the differences in their features

� State the requirements for a writing to constitute a negotiable instrument

� Explain how negotiable instruments are transferred andthe difference between assignment and negotiation

� Explain how instruments are negotiated by endorsementand the different types of endorsement

� Discuss the obligations of those who endorse a negotiable instrument

� Discuss the issues raised when there are multiple payees, unauthorized endorsements, and forged endorsements

� Define the term holder in due course and explain why itmatters

37

Le

ss

on

3L

es

so

n 3

Business Law 238

� Discuss personal defenses that can’t be asserted againsta holder in due course

� Discuss real defenses that can be asserted against allholders

� Explain the liability of makers, acceptors, drawers, andendorsers

� Discuss the duties that banks have to depositors andthat depositors have to banks

� Explain how electronic banking works

� Describe the process of bank deposits and collections

ASSIGNMENT 7Read this introduction to Assignment 7. Then read Chapter 16of your textbook.

Chapter 16 introduces you to the purpose and types of negotiable instruments.

The purpose of negotiable instruments is to facilitate trans-fers of money and borrowing of money.

Promissory notes and certificates of deposit are two types ofnegotiable instruments that contain a promise to pay money.The parties to a note are the maker and the payee. A demandnote is payable whenever the payee chooses to demand pay-ment. A time note is payable at some defined future date.Installment notes are payable in a series of installments atspecified times.

Drafts and checks are negotiable instruments that contain anorder to pay money. The parties to a draft are the drawer,drawee, and payee. A check drawn on a checking account isa kind of draft. Using the example of a check drawn on abank, the person writing the check is the drawer, the personto whom the check is made payable is the payee, and thebank on which the check is drawn is the drawee. Draweesare liable on drafts only when they accept them.

The UCC doesn’t require that a preprinted form be used towrite checks and allows for any writing to serve as a check ifit otherwise meets the requirements of the UCC.

Lesson 3 39

A bank draft is a check drawn by one bank on another bankin which it has funds on deposit. Such accounts may be usedto facilitate a customer’s business transactions in distantplaces. A cashier’s check is drawn by the bank on itself. Acertified check is a check guaranteed by the bank at therequest of either the depositor or the holder. The UCC doesn’trequire banks to certify checks. A money order is a type ofdraft that may be purchased from banks, post offices, orother companies as a substitute for a check.

A bearer is a person who possesses a negotiable instrumentpayable to “bearer,” “cash,” or an instrument that has beenendorsed in blank. A holder is a person in possession of aninstrument issued or endorsed to that person’s order or tothe bearer. A holder in due course is one who’s treated favor-ably and immune from certain defenses.

Negotiable instruments are used daily by millions of peopleand are highly trusted. When an instrument is transferred bynegotiation, the person receiving the instrument is providedwith more protection than might have been available to theperson from whom it was received. In some instances, thetransferee may be able to recover money using the instru-ment when the person transferring it couldn’t have done so.

Negotiable instruments may be assigned or transferred.Assignment occurs when the instrument is transferred with-out proper endorsement or otherwise in a form that’s notnegotiable. An assignee has only the rights of the assignorand is subject to all defenses existing against the assignor.

Negotiation occurs when the transfer makes the transferee aholder. A holder has greater rights than an assignee.Negotiation is accomplished by endorsement with the intentto transfer ownership.

Different types of endorsements include the following:

� A blank endorsement, which is a signature alone, inwhich the holder of such an instrument can recover itsface value by delivery alone, even if the holder isn’t theperson who made the endorsement

� A special endorsement, which is made by writing “pay tothe order of” or “pay to” followed by the name of the per-son to whom it’s transferred, and then followed by theendorser’s signature

Business Law 240

� A restrictive endorsement, which limits the subsequentuse of an instrument, such as endorsing “for depositonly”

� A qualified endorsement, which limits the liability of theendorser

Certain warranties are automatically made by a person whoreceives consideration for an instrument (for example, uses acheck to pay for goods or cashes a check at a bank):

� The endorser has the right to enforce the instrument(has good title).

� All signatures are genuine or authorized.

� The instrument hasn’t been materially altered.

� No defense of any party is good against the endorser.

� He or she has no knowledge of bankruptcy of the maker,acceptor, or drawer of an unaccepted instrument.

Unless the endorsement provides otherwise, an endorseragrees to pay any subsequent holder the face amount of theinstrument.

If an instrument is payable to one person and another person, it must be endorsed by both. If it’s payable to oneperson or another person, the endorsement by either is sufficient.

The tort of conversion is committed when an instrument ispaid on a forged endorsement. A forged endorsement isn’teffective as the signature of the person whose name is signedunless

� It’s ratified

� The person signing is an impostor and impersonates theperson whose name is signed

� The maker intends the payee to have no interest or thepayee is a fictitious person

� An agent pads the payroll by supplying the employerwith fictitious names

Lesson 3 41

Review and ApplicationWhen you finish reading the chapter,

� Answer the Quick Quiz questions on pages 351 and 358.Check your answers on page 361. These quizzes will notbe scored so don’t send them to the school; they’re foryou to gauge your progress. If there are any questionsyou don’t understand, refer back to the textbook andreread the assignment.

� Complete the online textbook chapter quiz athttp://highered.mheducation.com/sites/0073524956/student_view0/chapter16/chapter_quiz.html. Feedback onyour answers will be provided once you finish the quizand click the Submit Answers button.

� Take a moment to complete Self-Check 7. You can checkyour answers by turning to the back of this study guide.If you have trouble with any of the material, review thosesections in your text.

Self-Check 7Answer the “Questions for Review and Discussion” on pages 359–360 of your textbook.

Check your answers with those on page 87.

Business Law 242

ASSIGNMENT 8Read this introduction to Assignment 8. Then read Chapter 17of your textbook.

Chapter 17 discusses defenses that can be asserted toenforcing negotiable instruments and differentiates betweenthe liabilities of holders and the liabilities of holders in duecourse.

A holder in due course takes the instrument for value, in good faith, and without notice of any defenses. A holder whoreceives an instrument from a holder in due course acquiresthe rights of a holder in due course even though he or shemight not otherwise qualify as a holder in due course. This iscalled a shelter provision and is designed to permit holders indue course to transfer all of their rights to others. The shelterprovision doesn’t apply to a holder who has committed fraudor an illegal act.

Personal defenses are sometimes called limited defensesbecause they can’t be used against a holder in due course.The most common personal defenses are breach of theunderlying contract for which the instrument was considera-tion, lack or failure of consideration (the underlying contractis unenforceable due to lack of consideration), fraud in theinducement, lack of delivery (the holder obtains possession insome manner other than voluntary delivery), and payment.

The FTC has adopted a “holder in due course rule” thatallows consumers obligated under credit contracts to assertpersonal defenses against holders in due course, such as afinance company that might purchase the credit obligation.

Real defenses may be asserted against all holders, includingholders in due course. Real defenses include minority, lack ofcapacity, illegality, duress, fraud as to the nature of thetransaction, bankruptcy, unauthorized signature, and alteration.

The term presentment means a holder’s demand to pay oraccept an instrument. Presentment may be made by anycommercially reasonable means. The term dishonor refers torefusal to pay when an instrument is due or to accept whenproperly presented. Dishonor also occurs when presentmentis excused and the instrument is past due and unpaid.

Lesson 3 43

The obligations of makers, acceptors, and endorsers are different. Makers of notes and acceptors of drafts must paywithout reservation. Endorsers, on the other hand, must payonly if a properly presented instrument is dishonored andnotice of the dishonor is given to the drawee or party obli-gated to pay the instrument. Notice of dishonor may be givenby any reasonable means. Nonbank holders must give noticeof dishonor to the drawer and endorsers within 30 days following the dishonor

Review and ApplicationWhen you finish reading the chapter,

� Answer the Quick Quiz questions on pages 366, 369,371, and 373. Check your answers on page 375. Thesequizzes will not be scored so don’t send them to theschool; they’re for you to gauge your progress. If thereare any questions you don’t understand, refer back tothe textbook and reread the assignment.

� Complete the online textbook chapter quiz athttp://highered.mheducation.com/sites/0073524956/student_view0/chapter17/chapter_quiz.html. Feedback onyour answers will be provided once you finish the quizand click the Submit Answers button.

� Take a moment to complete Self-Check 8. You can checkyour answers by turning to the back of this study guide.If you have trouble with any of the material, review thosesections in your text.

Self-Check 8Answer the “Questions for Review and Discussion” on page 374 of your textbook.

Check your answers with those on page 88.

Business Law 244

ASSIGNMENT 9Read this introduction to Assignment 9. Then read Chapter 18 ofyour textbook.

Chapter 18 describes rules governing bank deposits and collections. Banks and their depositors have contractual relationships both of debtor and creditor and of agent and prin-cipal. The bank becomes a debtor when the customer depositsmoney. The bank acts as an agent when honoring drafts drawnby the customer on the account.

Banks must honor checks if there are sufficient funds in thecustomer’s account, unless the check is stale, which means it’spresented for payment more than six months after its date. Ifthe bank fails to honor a check due to a mistake by the bank,the bank is liable for actual damages caused by the dishonor.However, unless the check is certified, the bank has no liabilityto the holder of the check.

A bank continues to have authority to honor checks of a customer who’s deceased or becomes incompetent until itreceives notice of the death or incompetence. Even with notice,banks may honor or certify checks for 10 days after the deathof the drawer.

If a bank pays an altered amount of a check to a holder, it maydeduct from the account only the amount of the check as it wasoriginally written. If the bank honors a forged check, it’sresponsible to the depositor. However, the UCC imposes a dutyon depositors to examine their bank statements and canceledchecks promptly and to report forged or altered checks or theymay lose the right to hold the bank responsible for these losses.

Banks haven’t always made deposited funds available with thesame timeliness. As a result, the Competitive Banking Act wasadopted. Pursuant to regulations issued by authority of this act,the following rules apply:

� Funds from checks drawn on the U.S. Treasury or anystate or local government, and funds from any bank draft,cashier’s check, or postal money order must be made avail-able on the next business day (with some exceptions).

� Funds from checks drawn on banks within the sameFederal Reserve district must be available within two busi-ness days.

Lesson 3 45

� Funds from checks drawn on banks outside the bank’sFederal Reserve district must be available within five businessdays.

In many states, writing a check on an account that one knows hasinsufficient funds to cover the check is larceny.

A written stop-payment order is binding for six months unlessrenewed in writing. An oral stop-payment order is binding for 14days.

The FDIC insures deposits for up to $100,000 and joint accountsfor up to an additional $100,000.

Electronic banking is a very important feature of modern life. Manypeople use automated teller machines (ATMs) to deposit or with-draw money using an ATM card with a personal identificationnumber. Debit cards can be used to purchase goods and servicesby subtracting money electronically from a bank account. Somebanks permit payment by e-check, in which funds are electroni-cally transferred from a customer’s checking account. Businessesthat deal with large sums of money can avoid loss of interest andachieve other advantages by using electronic fund transfers.

ATM customers are entitled to a written receipt documenting theirtransaction, and the transactions must appear on bank statementssent to the customer. A consumer’s liability for unauthorized useof an ATM card is limited to $50 if notice of loss or theft is given tothe bank within two business days. After that, liability increases to$500 and becomes unlimited if notice isn’t given within 60 days.

A depository bank is the first bank to which an item is transferredfor collection. A payor bank is a bank by which an item is payable,including a drawee bank. In some circumstances, the same bankcould be both.

The process of collection of a check is as follows. The depositorybank acts as the customer’s agent for collection of the money fromthe payor bank. The check is sent to the payor bank, and if hon-ored, the amount is deducted from the drawer’s account. If thecheck is dishonored, it will be returned to the payee and creditswill be revoked.

The Check 21 Act allows use of a substitute check—a paper repro-duction of the original that can be processed. Customers don’thave an absolute right to see the original canceled check, only theright to return of a substitute check. The use of a substitute checkfacilitates electronic check processing.

Business Law 246

Review and ApplicationWhen you finish reading the chapter,

� Answer the Quick Quiz questions on pages 384, 387,and 391. Check your answers on page 394. Thesequizzes will not be scored so don’t send them to theschool; they’re for you to gauge your progress. If thereare any questions you don’t understand, refer back tothe textbook and reread the assignment.

� Complete the online textbook chapter quiz athttp://highered.mheducation.com/sites/0073524956/student_view0/chapter18/chapter_quiz.html. Feedback onyour answers will be provided once you finish the quizand click the Submit Answers button.

� Take a moment to complete Self-Check 9. You can checkyour answers by turning to the back of this study guide.If you have trouble with any of the material, review thosesections in your text.

Then review the material you’ve learned in this study guideand the assigned pages in your textbook for Assignments 7–9. When you’re sure that you completely understand theinformation presented in those assignments, complete yourmultiple-choice examination for Lesson 3.

Self-Check 9Answer the “Questions for Review and Discussion” on pages 392–393 of your textbook.

Check your answers with those on page 89.

Insurance, SecuredTransactions, andBankruptcy

INTRODUCTIONLesson 4 addresses the role that insurance, secured transactions, and bankruptcy play in business law.

OBJECTIVESWhen you complete this lesson, you’ll be able to

� Explain the purpose of insurance and binders

� Identify parties to an insurance contract

� Explain insurable interest and why it matters

� Define subrogation and explain how it occurs

� Discuss the features of life insurance, property insur-ance, health insurance, and an insurance application

� Discuss issues concerning premiums and lapse of coverage

� Describe grounds for cancellation of a policy by theinsurer

� Discuss how security interests are created in real property using mortgages

� Explain the different types of mortgages

� Define the rights and duties of mortgagors and mort-gagees, especially when there are multiple mortgages

� Explain how security interests are created in personalproperty