17

Subsea Market and Strategy Christophe Armengol Vice President, Subsea Strategy and Market Analysis March 30, 2010

Subsea Marketand Strategy

Christophe ArmengolVice President, Subsea Strategy and Market AnalysisMarch 30, 2010

2

Subsea market: Overview

►Significant slowdown in 2009, but Technip maintained its leading and resilient position

►Subsea market activity should pick up going forward

►Key driver of activity will be complex and deepwater projects

3

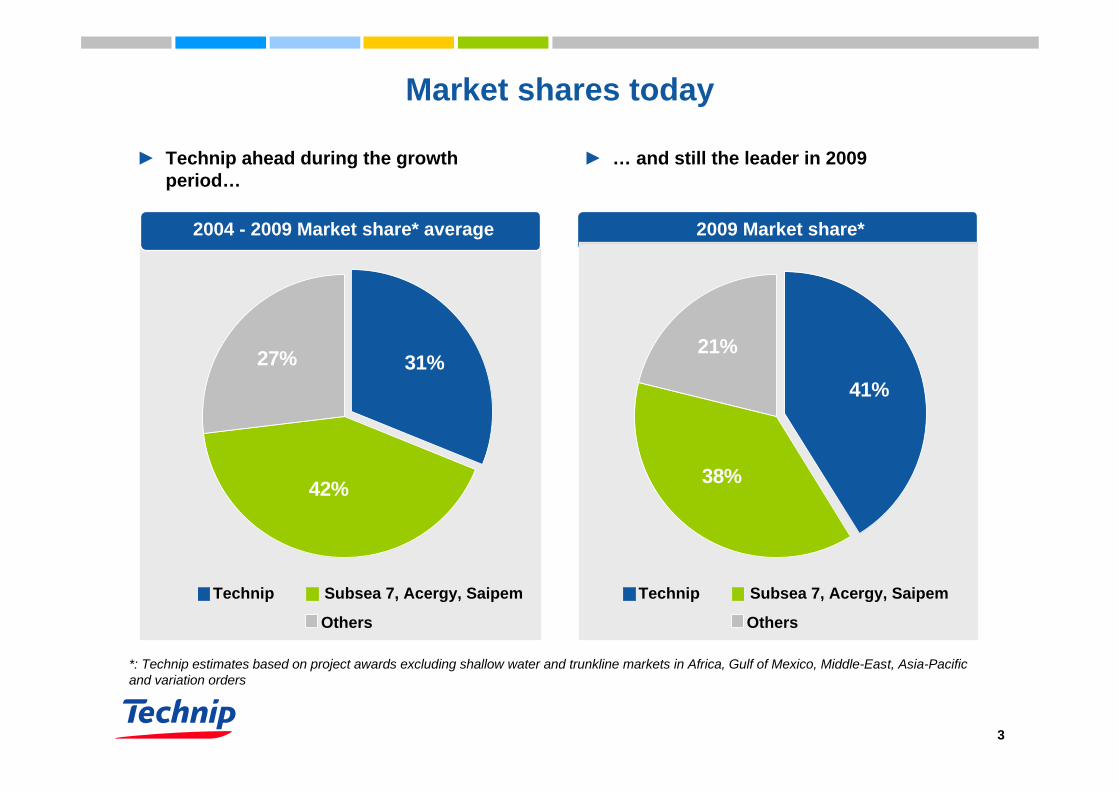

31%27%

42%

2009 Market share*

Market shares today

*: Technip estimates based on project awards excluding shallow water and trunkline markets in Africa, Gulf of Mexico, Middle-East, Asia-Pacific and variation orders

2004 - 2009 Market share* average

► Technip ahead during the growth period…

► … and still the leader in 2009

Technip Subsea 7, Acergy, Saipem

Others

41%

21%

38%

Technip Subsea 7, Acergy, Saipem

Others

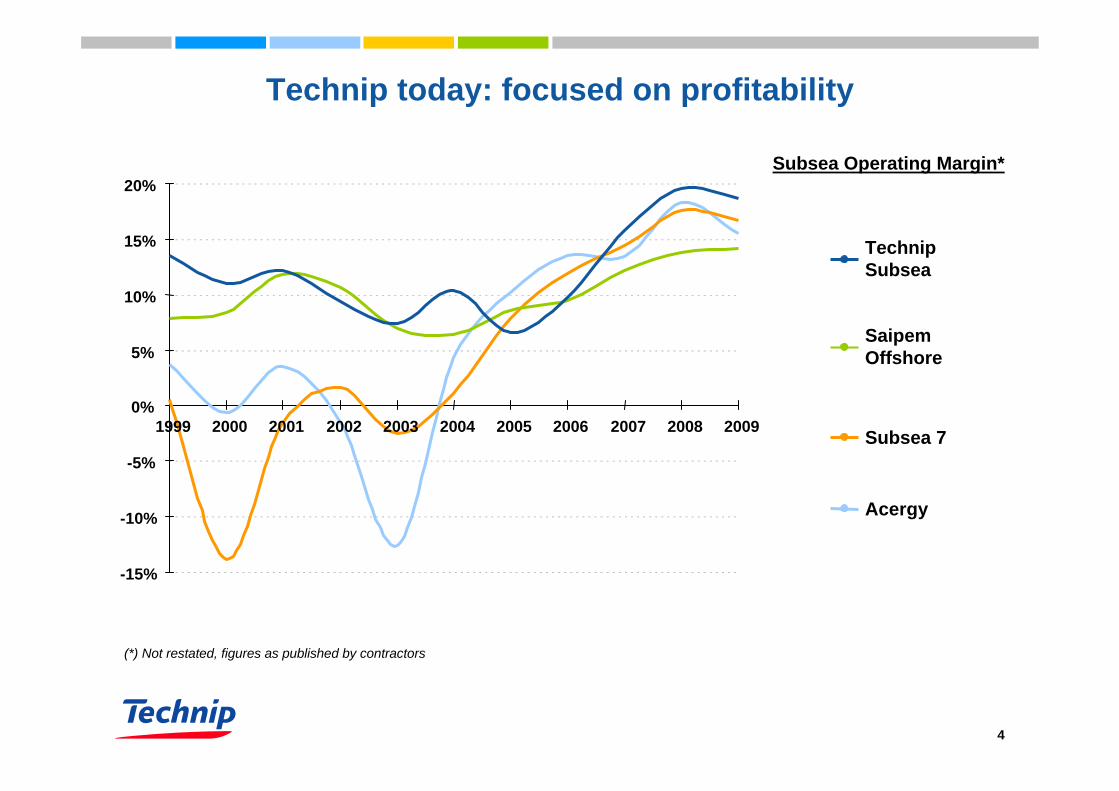

4

TechnipSubsea

Acergy

Subsea 7

SaipemOffshore

Subsea Operating Margin*

Technip today: focused on profitability

(*) Not restated, figures as published by contractors

-15%

-10%

-5%

0%

5%

10%

15%

20%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

5

Subsea tree awards picking upPositive signs for FPS* awards

Source: Technip

Looking ahead: Major oil companies announced an increase in Final Investment Decisions

Source: Quest Offshore

Floater solution still to be definedOTHER FLOATERS (FPU/Spar/TLP, Semi, FLNG)FPSO (new built & converted)

(*) Floating Production System

0

200

400

600

800

1,000

1,200

2000 2002 2004 2006 2008 2010 2012 2014

59 awards

88 awards

0

10

20

30

40

2006 2007 2008 2009 2010F 2011F 2012F

► Leading indicators show a positive trend:

6

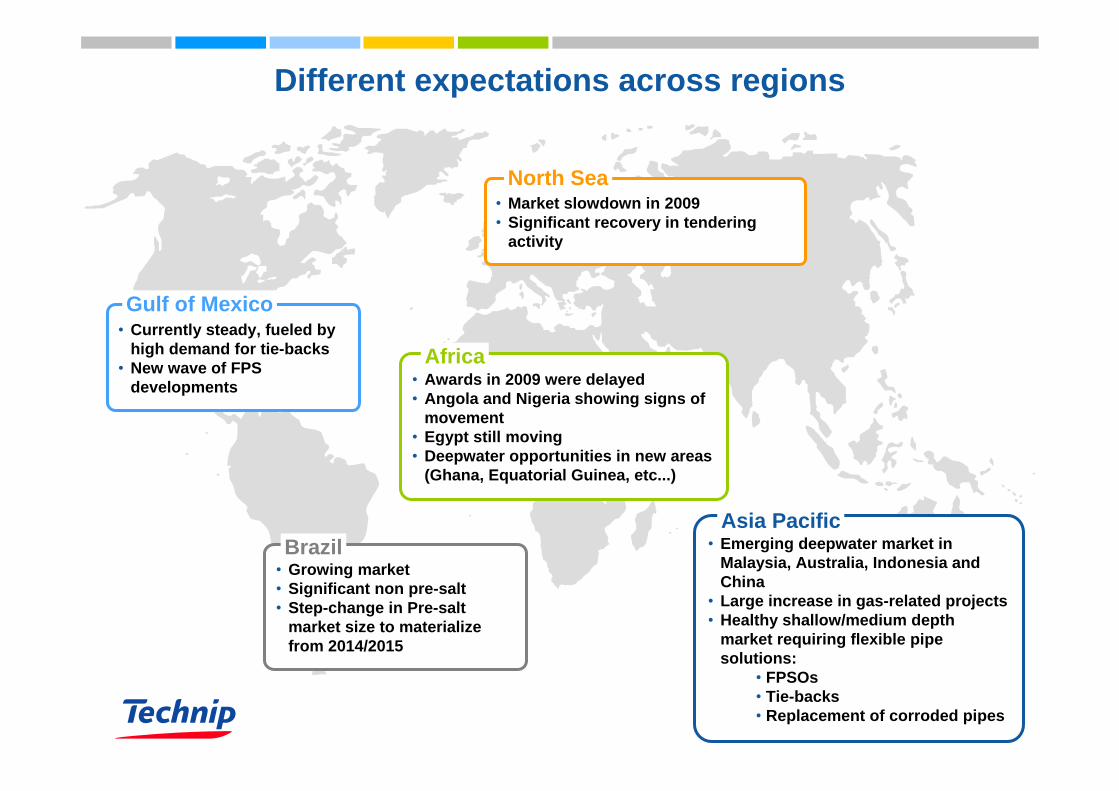

• Growing market• Significant non pre-salt• Step-change in Pre-salt

market size to materialize from 2014/2015

Brazil

• Currently steady, fueled by high demand for tie-backs

• New wave of FPS developments

Gulf of Mexico

• Market slowdown in 2009• Significant recovery in tendering

activity

North Sea

• Awards in 2009 were delayed• Angola and Nigeria showing signs of

movement• Egypt still moving• Deepwater opportunities in new areas

(Ghana, Equatorial Guinea, etc...)

Africa

• Emerging deepwater market in Malaysia, Australia, Indonesia and China

• Large increase in gas-related projects• Healthy shallow/medium depth

market requiring flexible pipe solutions:

• FPSOs• Tie-backs• Replacement of corroded pipes

Asia Pacific

Different expectations across regions

7

Pipeline (Flexible & Rigid) installed in water deeper than 1,000 meters*

Breakdown 2008 - 2015

Future growth areas: Subsea market growth drivers►Asia Pacific & India

► Emerging area for ultra deepwater projects

Pipeline installed (in km)

+60%

Sou

rces

: Tec

hnip

, Inf

ield

Gulf of Mexico

Asia Pacific India

Brazil

Africa

0

4,000

8,000

12,000

16,000

2000 - 2007 2008 - 2015

14%

21%

25%

40%

*Excluding Pre-Salt effect

88

Brazil is leading growth in deep and ultra deepwater

Water Depth >1,000 meters

*Excluding Pre-Salt effect

Deepwater flexible market* expected to represent 60%of the market over 2010 - 2012

Sources: Technip

2010 - 2012

16%

84%

Rest of WorldBrazil

0%

20%

40%

60%

80%

100%

2010 - 2012<150 150 - <500 500 - <1,000 1,000 - <1,500 >1,500Water Depth in meters:

<1,000m

>1,000m

Worldwide Flexible Market

9

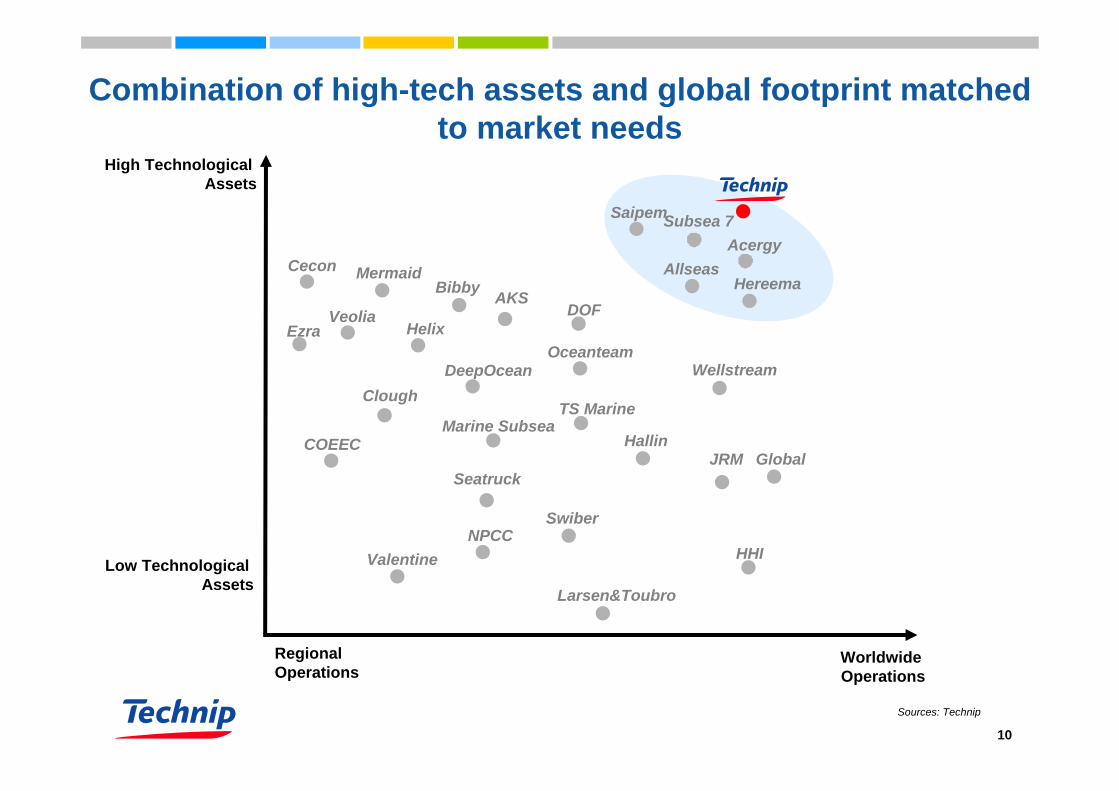

►High tech global assets

►Vertically integrated business

►Worldwide organisation for seamless project execution

►Strategic position in faster growing emerging markets

►Leadership in subsea technologies

Technip: Unmatched capability to design and execute successful projects

10

Marine Subsea

AcergySubsea 7

Bibby

Clough

Helix

DeepOcean

JRM Global

NPCC

COEEC

HHI

Seatruck

AllseasHereema

Worldwide Operations

Regional Operations

Oceanteam

TS Marine

Cecon Mermaid

Ezra

Hallin

AKSDOF

Wellstream

Larsen&Toubro

Swiber

Veolia

Valentine

High Technological Assets

Low Technological Assets

Combination of high-tech assets and global footprint matched to market needs

Saipem

Sources: Technip

11

Manufacture & Fabricate

• Flexibles pipes Umbilicals

• Manufacturing plants on all continents

Le Trait (France), Vitoria (Brazil), AsiaFlex (Malaysia)

Spoolbases: Evanton (UK), Orkanger (Norway), Mobile (USA), Dande (Angola)

Logistic bases: Vitoria, Angra Porto (Brazil)

Umbilicals: Newcastle (UK), Houston (USA), Lobito (Angola)

Install & Monitor

• Vessels designed to install our pipes

• Vertical Laying system

• Monitoring

Unmatched vertically integrated business to optimize design & execution

R&D

• New prototypes

• Proprietary technology

• R&D Centers close to production sites

World-class R&D facilities

Le Trait (France)

Aberdeen (UK)

Newcastle (UK)

Rio & Vitoria (Brazil)

Design & Project Management

• Optimized solutions

• ”A la carte”engineering

• Dedicated teams around the world

Strategic locationsParisAberdeenOsloHoustonKuala LumpurPerthRio de Janeiro

1 2

34

12

Example: Cascade & Chinook

12

Houston

St John’s Paris

Rio de Janeiro

Cascade & Chinook

AberdeenPori

Le Trait

Multi vessel installation (Incl. Deep Blue / Deep Pioneer)

Fabrication of the flexible pipes at Le Trait

Worldwide organization for seamless project execution

World record depth for Hybrid Free Standing Riser in 2,500m -2,640m of water

Installation ongoing - on schedule

Coordinated Engineering teams from Offshore & Subsea divisions

13

Southern Hemisphere

Technip Subsea revenues (in €m)

Northern Hemisphere

Strategic position in faster growing emerging markets

Sources: Technip

1,257

33%

52%

48%

67%

2,866

2002 2009

14

26%29%

45%

Strategic Capital Expenditure (2007 - 2011) Development Strategy

Generic -Non

Attributable

• Manufacturing plants

• Human resources

• Marine Assets

• Spoolbases and Logistic Bases

Strategic position in faster growing emerging markets

Investments

Southern Hemisphere

Northern Hemisphere

Sources: Technip

15

►Ultra deepwater:• Weight of pipelines (flexible, rigid, umbilicals)• Alternative installation methods• Hybrid System Riser

►More challenging reservoirs• Flow assurance• High Pressure/High Temperature• Corrosive Fluids

►Operational and Riser Integrity Management

Growing R&D investments expand leadershipin subsea technologies

16

Subsea market: Conclusion

►Significant slowdown in 2009, but Technip maintained its leading and resilient position

►Subsea market activity should pick up going forward

►Key driver of activity will be complex and deepwater projects

Thank you

Christophe ArmengolVice President, Subsea Strategy and Market AnalysisMarch 30, 2010