29

Suggestion for Rural Computer and M- Commerce By: Naineet C. Patel Ranjeet Kumar Vimal Gautam Garde

| Date post: | 25-Dec-2015 |

| Category: |

Documents |

| Upload: | barbara-pamela-farmer |

| View: | 214 times |

| Download: | 1 times |

Suggestion for Rural Computer and M-Commerce

By: Naineet C. Patel

Ranjeet Kumar Vimal

Gautam Garde

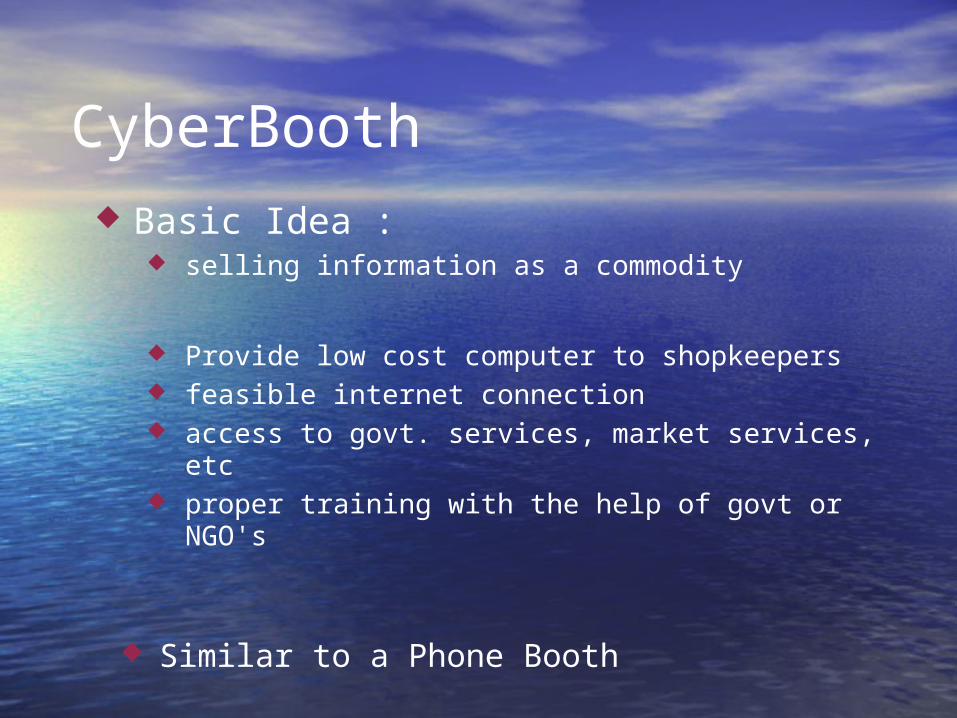

CyberBooth Basic Idea :

selling information as a commodity

Provide low cost computer to shopkeepers feasible internet connection access to govt. services, market services, etc proper training with the help of govt or NGO's

Similar to a Phone Booth

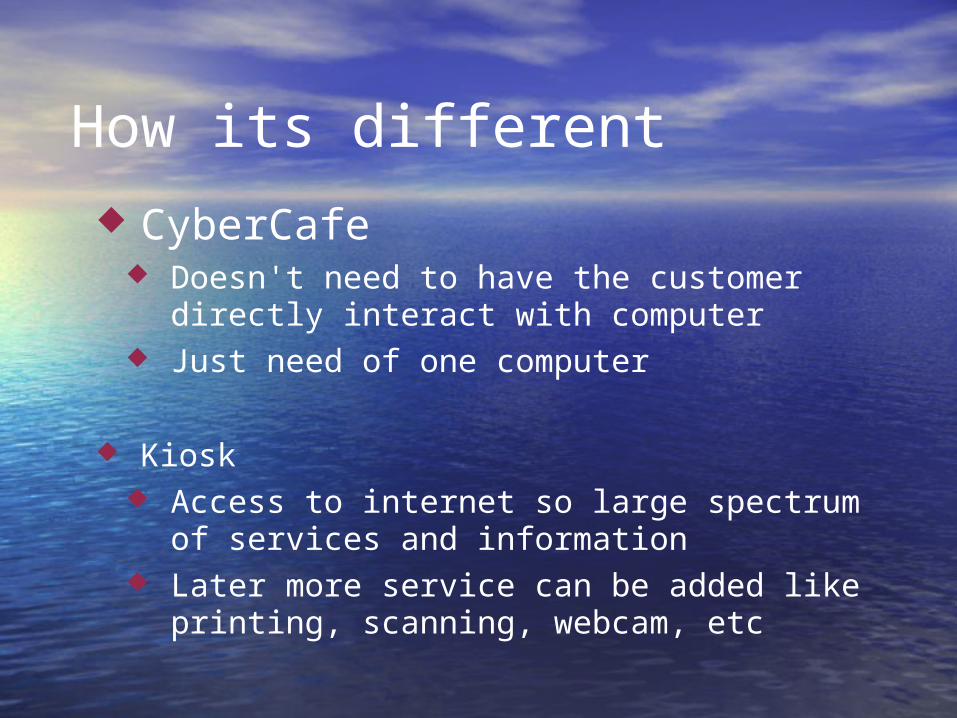

How its different CyberCafe

Doesn't need to have the customer directly interact with computer

Just need of one computer

Kiosk Access to internet so large spectrum of

services and information Later more service can be added like

printing, scanning, webcam, etc

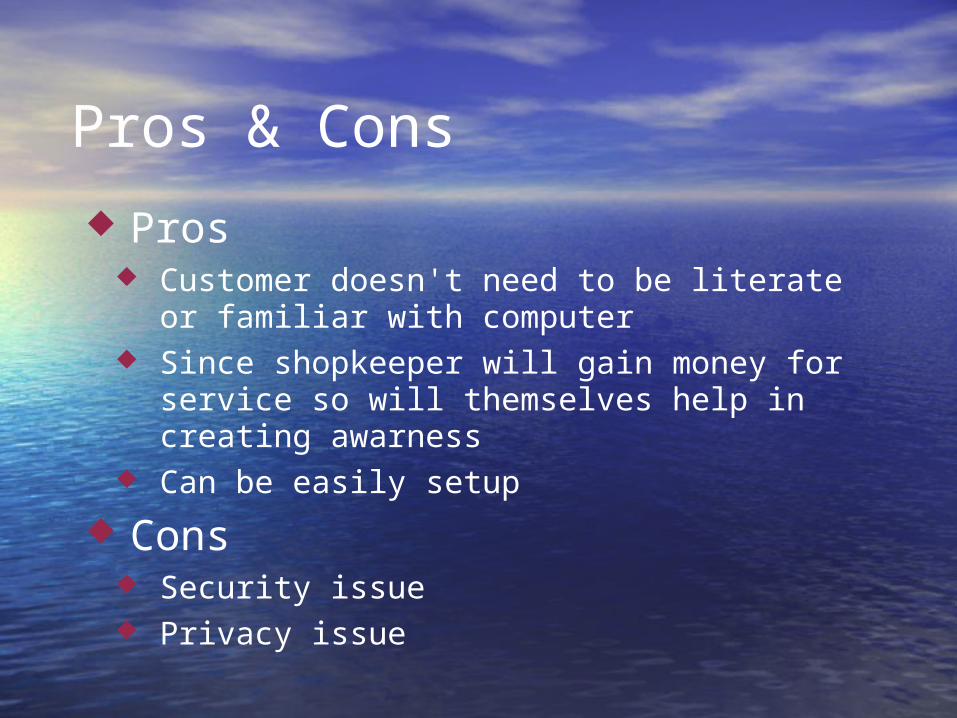

Pros & Cons

Pros Customer doesn't need to be literate or

familiar with computer Since shopkeeper will gain money for

service so will themselves help in creating awarness

Can be easily setup

Cons Security issue Privacy issue

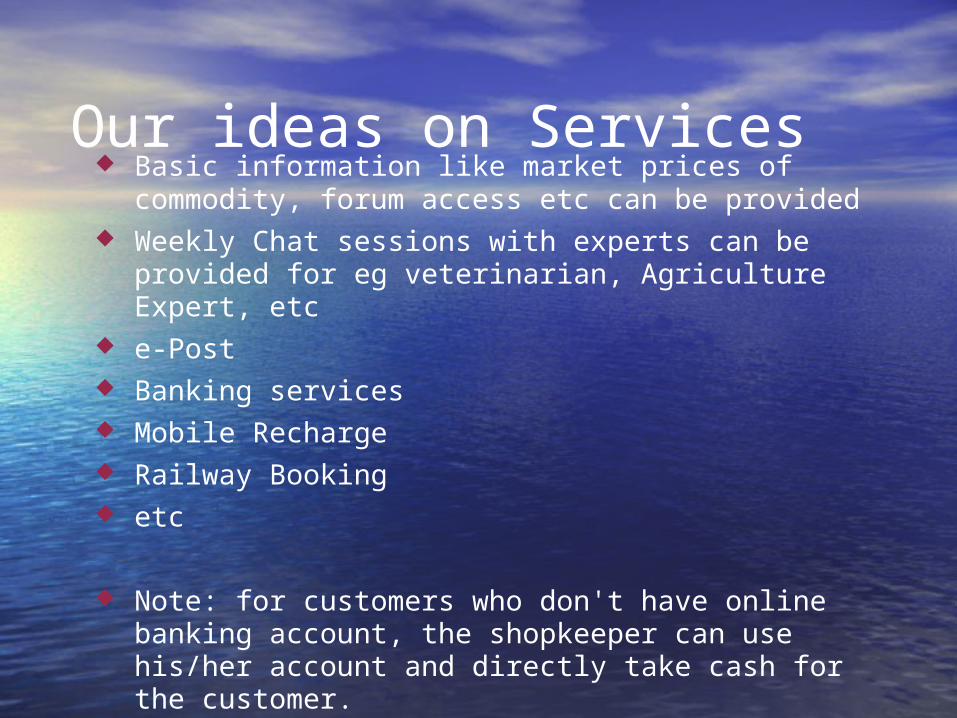

Our ideas on Services Basic information like market prices of

commodity, forum access etc can be provided Weekly Chat sessions with experts can be

provided for eg veterinarian, Agriculture Expert, etc

e-Post Banking services Mobile Recharge Railway Booking etc

Note: for customers who don't have online banking account, the shopkeeper can use his/her account and directly take cash for the customer.

Strengths Can create jobs in rural areas Useful to people who use internet once in a

while, cant afford to have a computer or monthly internet service.

Since customers just need to interact with shopkeeper he will feel more confident and and less alienated

Experts help will be easily available and readily available

Helps to save & create money eg no need to travel far away to know market prices, recharge, booking,etc

Slowly and steadily can creates awarness of IT in rural public

M-CommerceM-Commerce

Case study (work done in Case study (work done in Philippines)Philippines)

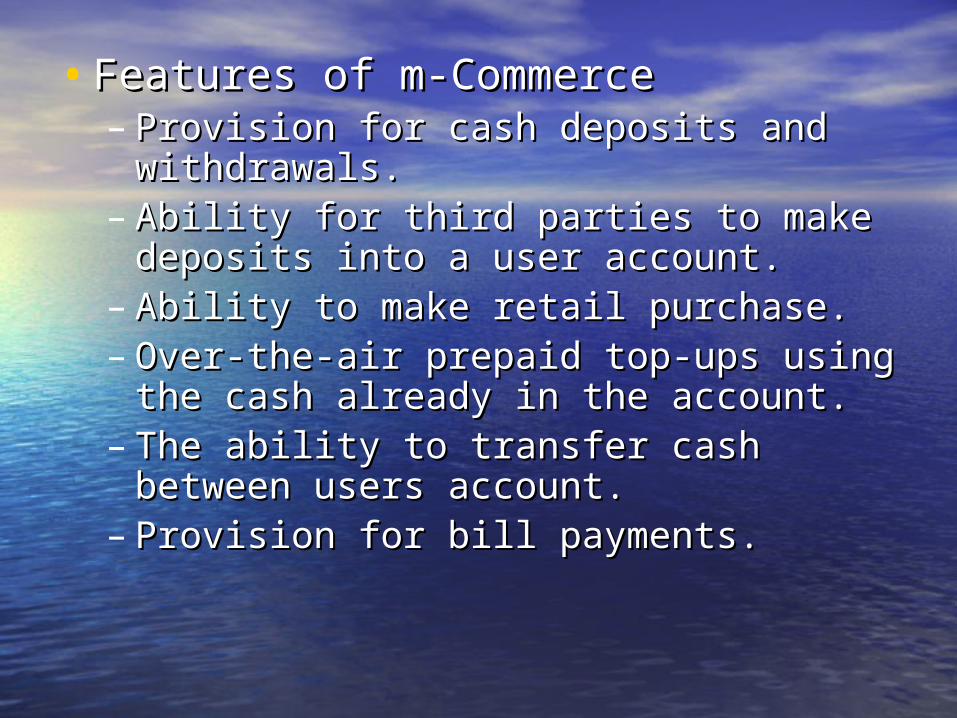

•Features of m-CommerceFeatures of m-Commerce– Provision for cash deposits and Provision for cash deposits and

withdrawals.withdrawals.– Ability for third parties to make deposits Ability for third parties to make deposits

into a user account.into a user account.– Ability to make retail purchase. Ability to make retail purchase. – Over-the-air prepaid top-ups using the Over-the-air prepaid top-ups using the

cash already in the account. cash already in the account. – The ability to transfer cash between The ability to transfer cash between

users account.users account.– Provision for bill payments.Provision for bill payments.

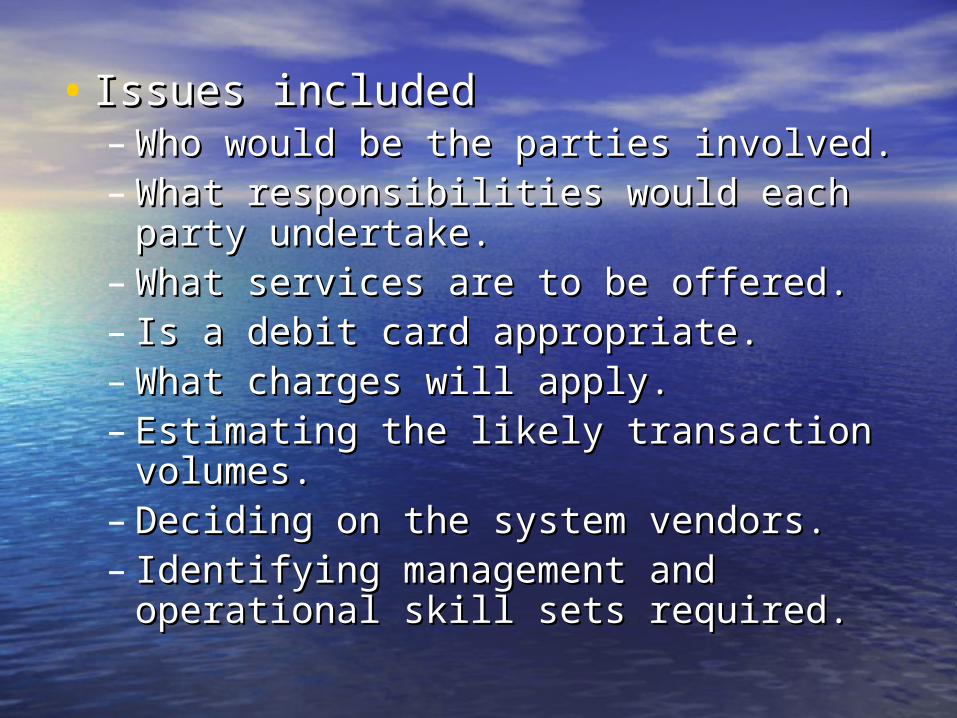

• Issues includedIssues included– Who would be the parties involved.Who would be the parties involved.– What responsibilities would each party What responsibilities would each party

undertake.undertake.– What services are to be offered.What services are to be offered.– Is a debit card appropriate. Is a debit card appropriate. – What charges will apply.What charges will apply.– Estimating the likely transaction Estimating the likely transaction

volumes.volumes.– Deciding on the system vendors.Deciding on the system vendors.– Identifying management and operational Identifying management and operational

skill sets required.skill sets required.

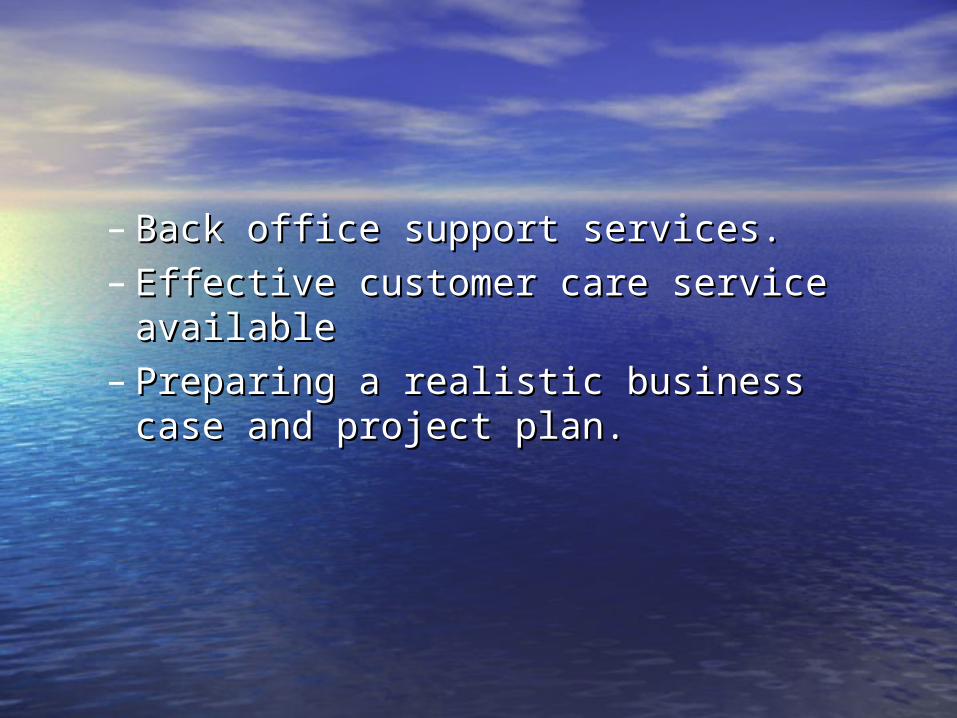

– Back office support services.Back office support services.– Effective customer care service Effective customer care service

availableavailable– Preparing a realistic business case and Preparing a realistic business case and

project plan. project plan.

Opportunities and Opportunities and ChallengesChallenges

•Customer perspectiveCustomer perspective

• Institutional perspective Institutional perspective

Customer PerspectiveCustomer Perspective

•Features:Features:– Needs meet by m-Commerce solutionsNeeds meet by m-Commerce solutions

•Accessibility:Accessibility:– Distribution of transaction pointsDistribution of transaction points

•Affordability:Affordability:– Transaction costs need to be lowTransaction costs need to be low

•Ease of use:Ease of use:– Easy to use, fast & user friendlyEasy to use, fast & user friendly

Institutional Perspective:Institutional Perspective:

•Fees and Charges:Fees and Charges:– Need for an appropriate revenue Need for an appropriate revenue

strategystrategy

•Efficiency Gains:Efficiency Gains:– Can the institution substantially increase Can the institution substantially increase

business transactions at lower cost?business transactions at lower cost?

•Controlling Development Costs:Controlling Development Costs:– Need to ensure positive returns on Need to ensure positive returns on

investmentinvestment

Institutional Perspective:Institutional Perspective:•Partnerships & Distribution Network:Partnerships & Distribution Network:

– Multiple business partnerships are Multiple business partnerships are essentialessential

– Need a wide enough network focused on Need a wide enough network focused on accessibility and ease of useaccessibility and ease of use

•Multiple Business Cases:Multiple Business Cases:– Each partner must benefit through Each partner must benefit through

reduced costs,reduced costs,– increased efficiency, or direct incomeincreased efficiency, or direct income

Agencies participated Agencies participated

•G-cash from Globe G-cash from Globe

•Smart Money Smart Money

We will discuss about G-cash We will discuss about G-cash

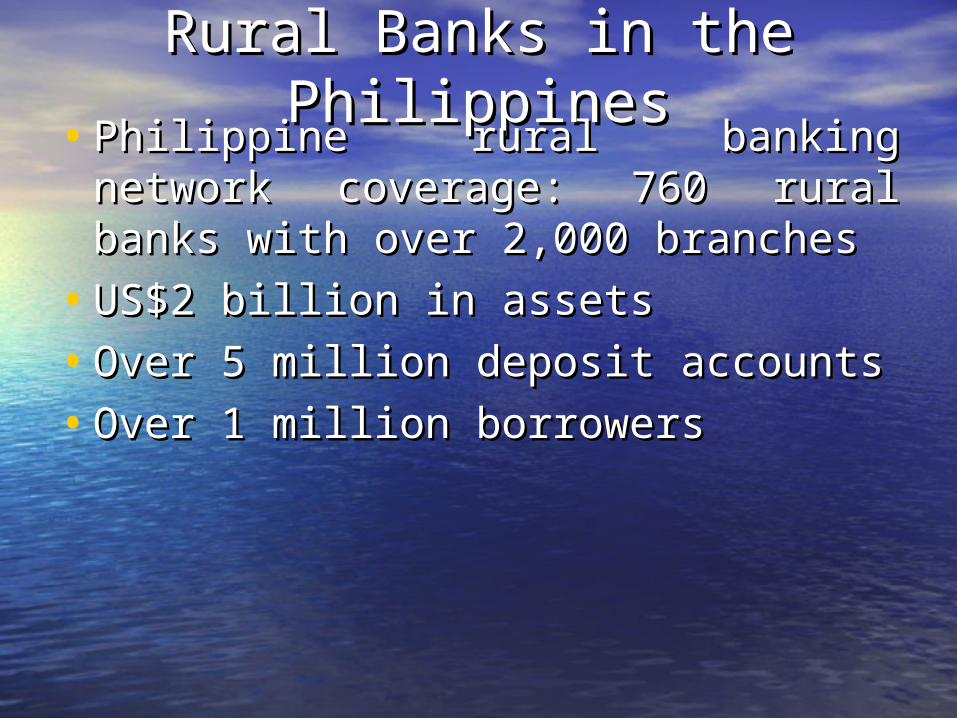

Rural Banks in the Rural Banks in the PhilippinesPhilippines•Philippine rural banking network Philippine rural banking network

coverage: 760 rural banks with over coverage: 760 rural banks with over 2,000 branches2,000 branches

•US$2 billion in assetsUS$2 billion in assets

•Over 5 million deposit accountsOver 5 million deposit accounts

•Over 1 million borrowersOver 1 million borrowers

Globe TelecomGlobe Telecom•One of the leading mobile phone One of the leading mobile phone

operators in the Philippinesoperators in the Philippines

•Over 13.5 million subscribersOver 13.5 million subscribers

•Over US$1B annual revenueOver US$1B annual revenue

•Cell phone industry processes approx. Cell phone industry processes approx. 200 million messages per day in the 200 million messages per day in the PhilippinesPhilippines

•Alliance partners include 7 mobile Alliance partners include 7 mobile operators in Asia with close to 70 million operators in Asia with close to 70 million subscriberssubscribers

•Alliance partnership involves sharing of Alliance partnership involves sharing of technology, innovation, and best technology, innovation, and best practices including marketing programs.practices including marketing programs.

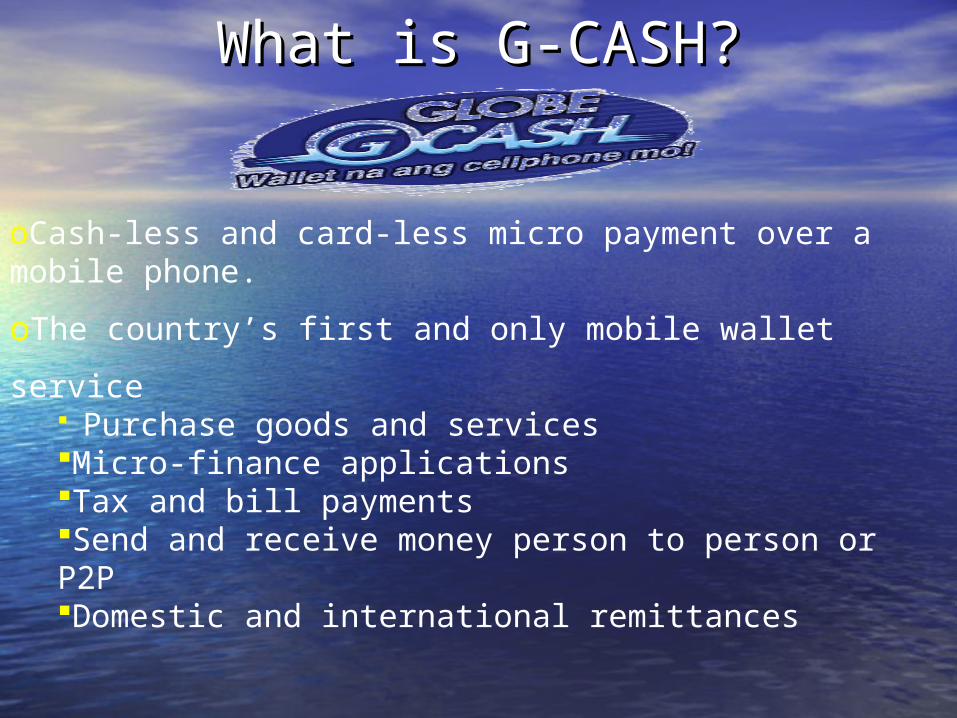

What is G-CASH?What is G-CASH?

oCash-less and card-less micro payment over a mobile phone.

oThe country’s first and only mobile wallet service Purchase goods and servicesMicro-finance applicationsTax and bill paymentsSend and receive money person to person or P2PDomestic and international remittances

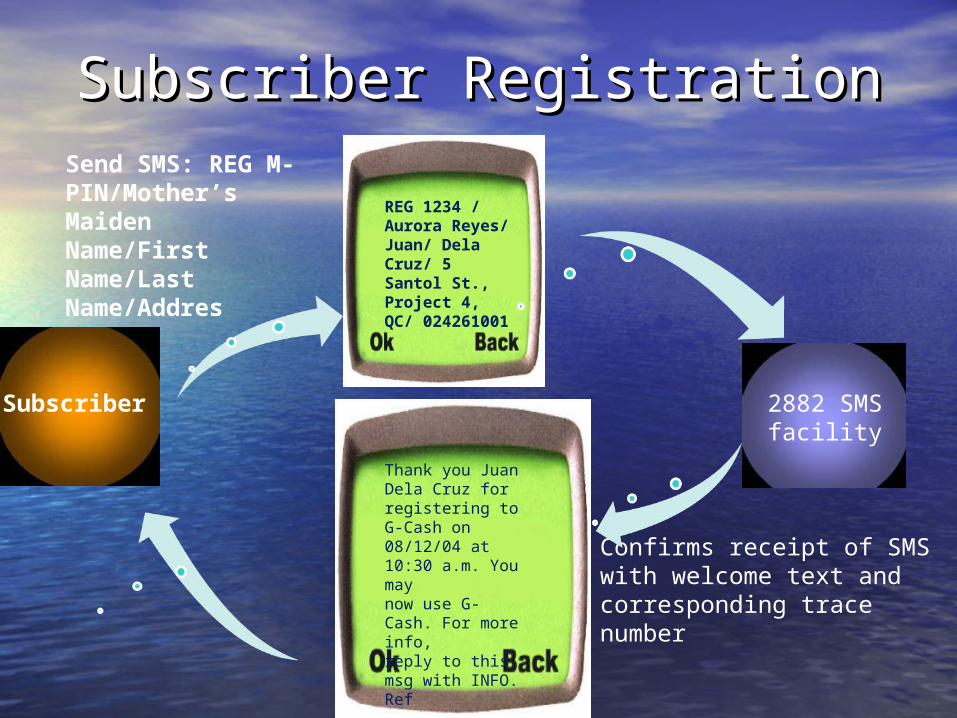

Subscriber RegistrationSubscriber Registration

Subscriber

REG 1234 / Aurora Reyes/Juan/ Dela Cruz/ 5 Santol St.,Project 4, QC/ 024261001

Thank you Juan Dela Cruz forregistering to G-Cash on08/12/04 at 10:30 a.m. You maynow use G-Cash. For more info,reply to this msg with INFO. Ref

Send SMS: REG M-PIN/Mother’s MaidenName/First Name/Last Name/Addres

Confirms receipt of SMS with welcome text and corresponding trace number

2882 SMS facility

• Recipient receives SMS advisory of G-Cash transfer• Outlet’s service unitreceives SMSacknowledgment withconfirmation number

Merchant:a)Verifies identity of customer b)Processes transaction• Collects paymenta)Sends G-Cash from outlet’s service unit to recipient’s mobile no. via P2P

Customer showsvalid Text-a-Payment ID andgives cash-inamount and

service fee

Customergoes to Outletto exchangecash for GCash

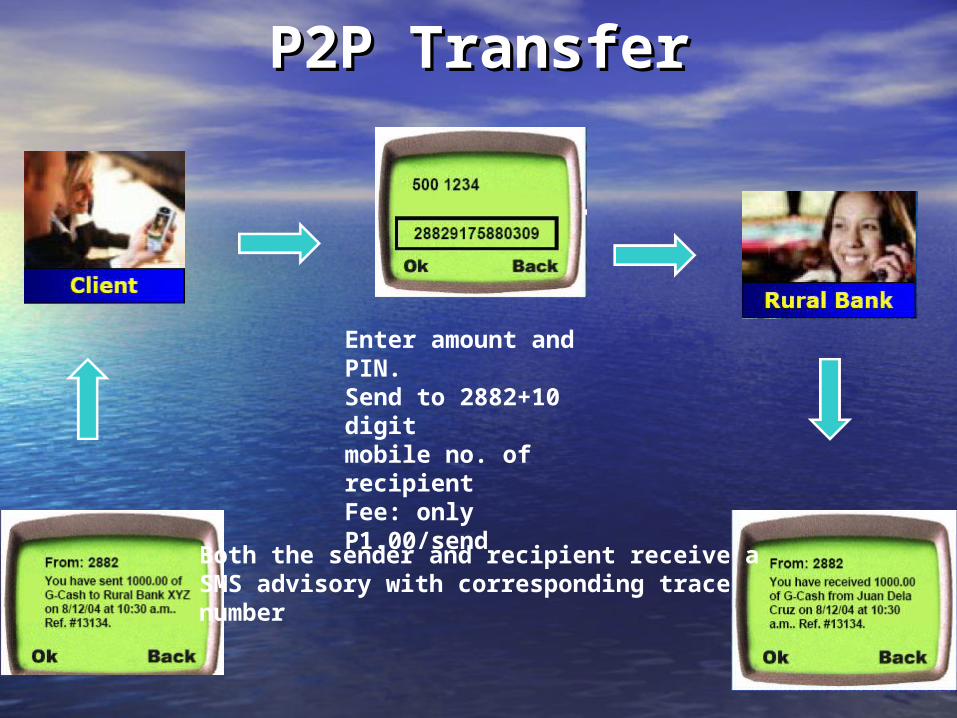

P2P TransferP2P Transfer

Enter amount and PIN.Send to 2882+10 digitmobile no. of recipientFee: only P1.00/send

Both the sender and recipient receive aSMS advisory with corresponding tracenumber

Issues To Be Considered In Issues To Be Considered In Establishing an m-CommerceEstablishing an m-Commerce

• Issues for a Network Operator.Issues for a Network Operator.

•Banking Issues.Banking Issues.

•Market Issues.Market Issues.

•Competition Issues.Competition Issues.

•Regulatory and Security IssuesRegulatory and Security Issues

•Competency.Competency.

•Transaction Management Issues.Transaction Management Issues.

•Company InfrastructureCompany Infrastructure

Issues for network operator: Issues for network operator:

• Which model to adoptWhich model to adopt – Access ModelAccess Model– Hybrid ModelHybrid Model

• Access Model Access Model – Search for banking partnerSearch for banking partner

• HybridHybrid– How far should model be developed How far should model be developed

•Banking issues:Banking issues:– How to use expanded marketHow to use expanded market– Help in reducing fraud,money launderingHelp in reducing fraud,money laundering– provide solutions for banking regulationsprovide solutions for banking regulations

•Market IssuesMarket Issues– attracting customersattracting customers

•minimum p2p airtime credit allowed was 4 minimum p2p airtime credit allowed was 4 centscents

•minimum prepaid top-up was 47 centsminimum prepaid top-up was 47 cents

– support for “sachet” purchasing support for “sachet” purchasing

•Competition IssuesCompetition Issues

•Regulatory and security IssuesRegulatory and security Issues– Liquidity,security,fraud detectionLiquidity,security,fraud detection

•TRANSACTION MANAGEMENT ISSUES:TRANSACTION MANAGEMENT ISSUES:– large no of low value transactionlarge no of low value transaction– increase in no of sms handled by existing increase in no of sms handled by existing

networksnetworks– third party transactions third party transactions – need to develop new transaction engine need to develop new transaction engine

•Robust company structure Robust company structure

Conclusion • Aim of this presentetion was to identify key

aspects of currently availble m-Commerce systems.

• for devloping economies m-Commerce is benifitial in-perticular for – Capturing unofficial cash float in the

community– eliminating need for people to carry cash in

significant amount– reducing the exposure to robbery– enabling the advancement of micro-loans to

the commnity– facilitating loan repayments– unabling payments of utility bills

•By industrial perspective– Banks

•increase in customer reach•increased cash float available to the bank

– Networks•increase in text messaging revenues•greater appeal to the market

– Retailers•added business opportunities•competitive advantage

– micro-finance institutions•ability to advance funds to remote areas •regular convenient repayments from users

m-commerce was successful in Philippines

Conditions of rural areas of Philippines and that India are quit same .There is major section people who use mobile but have to go 20-30 km to deposit/withdraw money in/from back .m-commerce can be experimented in India if some network operator comes forward to help

Thanks