48

Summary of Last Lecture: • Capital Rationing • IRR and NPV interpretation with limited capital

| Date post: | 24-Dec-2015 |

| Category: |

Documents |

| Upload: | sherilyn-montgomery |

| View: | 237 times |

| Download: | 0 times |

Summary of Last Lecture:

• Capital Rationing• IRR and NPV interpretation with limited

capital

BONDS AND CLASSIFICATION OF BONDS

Learning Objectives:

• After going through this lecture, you would be able to have an understanding of the following topic

• Bonds• Classifications of bonds

Learning Objectives:

• Up to lecture no 11, we have discussed the investment decisions and capital budgeting as it relates to real assets and properties. Now, we discuss about the securities.

Difference between Real Assets & Securities

• Real assets are physical property such as Land, Machinery, equipments and Building etc. Where as securities basically, are legal contractual piece of paper.

Kinds of securities:

• We have discussed about two types of securities.

• Direct claim securities:• Stocks (Shares):• It is defined as equity paper representing

ownership, shareholding. Appears on Liabilities side of Balance Sheet

Kinds of securities:

• Bonds:• It is a debt paper representing loan or

borrowing. These are long term debt instruments.

Classification of bonds on Balance sheet:

• One should be very careful regarding the classifications of bonds on the balance sheet. Because, when you are Issuing Bonds (i.e. borrowing money) then the Value of Bonds appears under Liabilities side (as Long Term Debt) of Balance Sheet.

Classification of bonds on Balance sheet:

• If you are Investing (or buying) Bonds of other companies then their Value appears under Assets side (as Marketable Securities) of Balance Sheet.

Classification of bonds on Balance sheet:

• The Important thing to remember is that the stocks represent the ownership and bonds represent the debt. Both are the direct claim securities.

Classification of bonds on Balance sheet:

When a company or investor rising funds he have two possible options available to him.

• 1) Equity• 2) Debt

Textile Weaving Factory Case Study:

• A Textile Weaving Factory uses thread to make cotton fabric and then sells cotton fabric to earn cash receipts. It needs Rs.1 million to make a Capital Investment in looms and machinery. It has two options he can raise money through

• 1. Equity, OR• 2. Debt

Textile Weaving Factory Case Study:

• Lets suppose that company decide to take Rs. 1 million in the form of debt It can raise money for a period of 1 year by Debt Financing by Issuing a 1 year Mortgage Bond whereby it pays the Lender (i.e. Investor or Bondholder) 15% p.a Coupon Interest Rate.

Textile Weaving Factory Case Study:

• You decided to divide 1 million in to 1 thousand parts and each one of these parts in the form of paper that has a face or par value of Rs 1,000.Each Bond paper worth Rs 1,000 and the total number of bonds is 1,000.Each bond paper carries the face value which is printed on it and also carries coupon interest rate.

Textile Weaving Factory Case Study:

• Suppose that coupon interest rate on this bond is 15% it means that this company would pay 15% of the face value to the lender. It is income for the lender (Bond holder). The Bond also has the limited life.

Textile Weaving Factory Case Study:

• In this case we suppose that management need money for the period of two years. The company pays the coupon rate to the bond holder for two years and also returns the principle to the lender after two years at maturity date.

Textile Weaving Factory Case Study:

• The Lender’s (or Bond Holder’s or Investor’s) money is protected because the Mortgage Bond is Backed (or Secured) by Real Property such as the land, factory building, and machinery.

Textile Weaving Factory Case Study:

• Upon Maturity, after 1 year, the Bond Issuer will return the Par or Face Value (or Principal Amount of Rs 1 million) to the Lender.

Textile Weaving Factory Case Study:

• Now, we discuss different concepts which are common in different bonds. There are certain advantages and disadvantages of raising money either through equity or through bonds.

Textile Weaving Factory Case Study:

• Why to raise money through a Debt (ie. Bond) rather than through Equity (i.e. Shares or Stocks)?

Textile Weaving Factory Case Study:

• If the Company raises money using Bonds, then it will have to pay a fixed amount of interest (or mark-up) regularly for a limited amount of time. You do not share the profits of the company. But there as legal risk attached to the failure to pay interest can force company to close down.

Textile Weaving Factory Case Study:

• If the Company raises money using Equity, then it is forced to bring in new shareholders who can interfere in the management and will get a share of the net profits (or dividends) for as long as the company is in operation! The amount of dividends can vary.

Value of the Bond:

• The Value of the Bond can be calculated from the Cash Flows attached to the Bond. Bonds are direct claim securities. The bond holder will receive the coupon interest rate and he will also receive his principle amount at the time of maturity. Where are these cash flows come from?

Value of the Bond:

• How the company is able to pay interest to the bond holder. The company is making cash from operations. Those Cash Flows depend on the Cash Flows from the Real Business i.e. the textile factory’s cash flows from sale of fabric.

Value of the Bond:

• Bond value is coming from the fabric sale. This is why the Bond is called a Direct Claim Security whose value depends on the value of some underlying real asset.

Characteristics of bonds:

• In Pakistan, the bonds take on the form of Term Finance Certificates (TFC’s).These are traded on three stock exchanges of Pakistan.

Characteristics of bonds:

• It is quite common to trade bonds in the stock markets. In Pakistan, the Par Value (or Face Value) of each TFC is generally Rs 1,000 but it can be different. The Life of a Bond is generally limited (or finite) i.e. 6 months, 1 year, 3 years, 5 years…..

Characteristics of bonds:

• The bonds can be issued by any one (Public, Private) who is in need of money. For example, Defense saving certificates, Treasury bills, T Bills (short term bonds) & FIB (Long term bonds) are also classifieds as the bonds.

Characteristics of bonds:

• Face value is the amount which is mentioned on the bond paper. Par value is fixed but the bonds are traded in the markets. As the financial health (cash flows and income) of the company changes with time, the Market Value (or Price) of the Bond changes (even though it’s Par Value is fixed).

Characteristics of bonds:

• Market Prices also change depending on the Supply-Demand for the Bond (or TFC) and Investors’ Perception. Major reason is the change in interest rate effect the bond price we will discuss it in detail in upcoming lectures.

Characteristics of bonds:

• In case of Textile Company this company issued a bond at the fixed coupon interest rate is 15 % of par value. This rate is fixed and should be paid by the company. Non payment of this would default and result in the closing of the company.

Characteristics of bonds:

• However, the market interest rate keeps moving and it changes on daily basis. We have discussed the factors that caused the changes in interest rate in the previous lectures.

Bonds: Definition

• Bond is a type of Direct Claim Security (a legal contractual paper) whose value is secured by Real Assets owned by the Issuer. Bond is issued by the Issuer (or Borrower) to the Bondholder (or Lender or Investor or Financier) in exchange for the cash. Borrowers and lenders can be individual persons or companies or governments.

Bonds: Definition

• Examples: Term Finance Certificate (TFC issued by Public Listed Industrial Companies), Defense Saving Certificate (DSC issued by Government), T-Bill (issued by Government).

Bonds: Definition

• Bond is a Legal Contractual Paper Certificate that represents Long Term Debt (or Long-term Promissory Note).Bond paper contains legal & numerical points.

Bonds: Numerical Features

• Maturity or Tenure or Life: Measured in years. On the Maturity Date when the bond expires, the Issuer returns all the money (Principal/par and Interest/coupon) to the Investor (thereby terminating or Redeeming the bond) ie. 6 months, 1 year, 3 years, 5 years, 10 years, …

Bonds: Numerical Features

• Par Value or Face Value: Principal Amount (generally printed on the bond paper) returned at maturity ie. Rs 1,000 or Rs. 10,000. Contrast this to Market Value (or Actual Price based on Supply/Demand) and Intrinsic or Fair Value (estimated using Bond Pricing or Present Value Formula).

Bonds: Numerical Features

• Coupon Interest Rate: percentage of Par Value paid out as interest irrespective of changes in Market Value ie. 5 % pa, 10 % pa, 15% pa, … etc. Coupon Receipt = Coupon Rate x Par Value. Coupon Receipts can be paid out monthly, quarterly, six-monthly, annually…etc. Contrast to Market Interest Rate (macro-economic).

Bonds: Characteristics & Legal Points

• Indenture”: Long Legal Agreement between the Issuer (or Borrower) and the Bond Trustee (generally a bank of financial institution that acts as the representative for all Bondholders).

• Basically protects Bondholders from mismanagement by the bond issuer, default, other security holders, etc.

Bonds: Characteristics & Legal Points

• Claims on Assets & Income: Bondholders have the First Claim on Assets in case the company closes down (Before Shareholders). The Financial Charges due to Bond Holders must be paid out from the Income before any Net Income can be distributed to Stockholders in the form of Dividends (see P/L Statement).

Bonds: Characteristics & Legal Points

• Claims on Assets & Income: If Issuer (or Borrower) does not pay the interest to the Bondholder (i.e. Default), then the firm can be legally declared Insolvent, Bankrupt, and forced to close down.

Bonds: Characteristics & Legal Points

• If Issuer (or Borrower) does not pay the interest to the Bondholder (i.e. Default), then the firm can be legally declared Insolvent, Bankrupt, and forced to close down.

Bonds: Characteristics & Legal Points

• Security: Mortgage Bonds are backed by real property (ie. Land, building,, machinery, inventory) whose value is generally higher than that of the value of the bonds issued.

Bonds: Characteristics & Legal Points

• Debentures and Subordinated Bonds are not secured by real property but they are backed by personal and corporate guarantees and their security and value is tied to the anticipated future cash in-flows of the business.

Bond Ratings & Risk

• Bonds are rated by various Rating Agencies:• Internationally: Moody’s, S&P.• In Pakistan: Pacra, VIS.

Bond Ratings & Risk

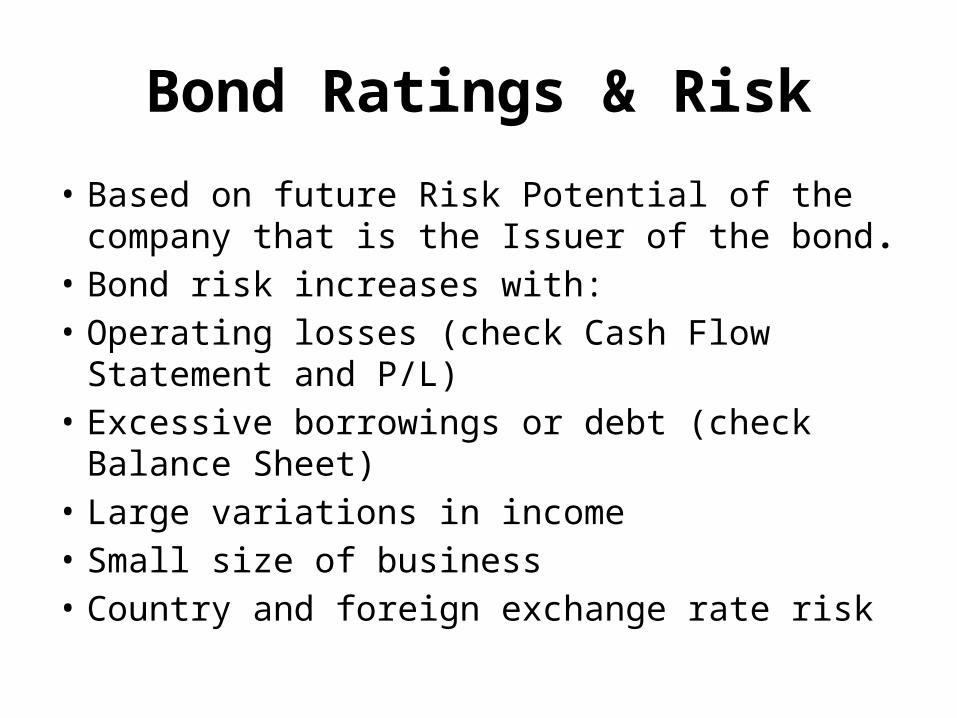

• Based on future Risk Potential of the company that is the Issuer of the bond.

• Bond risk increases with:• Operating losses (check Cash Flow Statement and

P/L)• Excessive borrowings or debt (check Balance Sheet)• Large variations in income• Small size of business• Country and foreign exchange rate risk

Bond Ratings & Risk

• International Bond Rating Scale (starting from the best or least risky): AAA, AA, A, BBB, BB, B, CCC, CC, C, D. Also + is better and - is worse. So A+ is better than A. A- is worse than A.

Summary:

• Bonds• Classifications of bonds