Suhas Harinarayanan Arun Aggarwal (91-22) 6766 3404 (91-22) 6766 3440 suhas.hari@religare.in arun.aggarwal@religare.in RCML: Winner of LIPPER-STARMINE broker award for “Earnings Estimates in Midcap Research 2008” | “Honourable Mention” in Institutional Investor 2009 | Voted amongst Top 5 most improved brokerages by Asia Money Poll 2009 | RCML Research is also available on Bloomberg FTIS <GO> and Thomson First Call Initiating Coverage 02 December 2010 Financial highlights (Rs mn) FY10 FY11E FY12E FY13E Revenue 284 1,629 14,246 22,417 Growth (%) 37.9 473.5 774.7 57.4 Adj net income 62 639 5,961 7,951 Growth (%) (64.2) 937.8 832.3 33.4 FDEPS (Rs) 1.0 10.2 94.7 126.3 Growth (%) (93.2) 937.8 832.3 33.4 Profitability and return ratios (%) FY10 FY11E FY12E FY13E EBITDA margin 37.9 57.5 63.9 54.0 EBIT margin 33.8 56.6 63.7 53.9 Adj PAT margin 21.7 39.3 41.8 35.5 ROE 1.5 10.1 62.8 49.2 ROIC 0.8 5.9 50.8 93.9 ROCE 0.9 5.9 43.3 39.1 Sunteck Realty Ltd Asset-light model with high cash flow visibility We initiate coverage on Sunteck Realty (SRL) with a BUY rating and a target price of Rs 800 (implied P/BV of 2x on FY13E), offering a 23% upside. SRL is one of the best plays on Mumbai’s super-luxury segment, with 67% of its land bank located in and around the city. We like SRL for: (1) its asset-light model through JVs and joint development agreements (JDA) with landowners, resulting in low land cost of Rs 409psf and high IRRs of 50–55%; (2) its three key super-luxury residential projects in BKC-Mumbai (a commercial hub), which form 25% of our GAV (Rs 285/sh) and are likely to generate net cash of Rs 30bn+ (pre-tax) over FY11- FY13; and (3) its strong financials with a adjusted D/E ratio of 0.4x and high operating cash flow visibility of Rs 6.7bn and Rs 17.5bn in FY12 and FY13 respectively. We estimate a sales/EPS CAGR of 326%/400% over FY10-FY13. Key risks are timely execution, approval delays and an economic slowdown. Asset-light business model: SRL holds 77% of its saleable area through JV/JDAs with landowners and the balance through slum rehabilitation schemes (SRA), redevelopment projects and land buyouts. We believe the JV/JDA model helps the company build a capital-efficient business by stripping away the investment on land purchase and allowing a greater focus on value addition. It also supports efficient capacity utilisation and higher IRR (50–55%). The cost of land via JDA/JVs is Rs 48/Rs 130psf for SRL, significantly lower than that of outright land buyouts. Cash flows to strengthen: SRL is currently developing three super-luxury residential projects in Mumbai’s BKC district. These projects form 25% of our gross annual value for the company and are likely to generate cash of Rs 30bn (pre-tax) over FY11-FY13 (in comparison, the company’s current market cap is ~Rs 39bn). We expect residential absorption of 4.0msf (FY11: 0.8msf; FY12: 1.7msf; FY13: 1.5msf) including the above projects, which will aid further cash generation during FY11-FY13. Operating cash flows during FY12 and FY13 are estimated at Rs 6.7bn and Rs 17.5bn respectively, which will likely be utilised for further land acquisition. SRL’s adjusted D/E ratio of 0.4x could decline further, in our view. Improving revenue and margin profile: Since SRL follows the project completion method, a bulk of the revenue from ongoing projects is expected in FY12 and FY13. The company’s EBITDA margin is also likely to improve from 38% in FY10 to 54% in FY13 as high end luxury projects get recognised. Initiate with BUY: We value SRL at a 20% discount to NAV, translating to a target price of Rs 800. Key risks to our estimates are execution risk, rules and regulations in newer territories which may delay projects, and a slowdown in the economy. CMP TARGET RATING RISK Rs 615 Rs 800 BUY HIGH BSE NSE BLOOMBERG 512179 SUNTECK SRL IN Company data Market cap (Rs mn / US$ mn) 38,726/850 Outstanding equity shares (mn) 63 Free float (%) 16.9 Dividend yield (%) - 52-week high/low (Rs) 714 / 480 2-month average daily volume 112,665 Stock performance Returns (%) CMP 1-mth 3-mth 6-mth SRL (8.4) (1.1) 0.9 (8.4) BSE REAL 1.8 18.3 21.4 1.8 Sensex (3.1) 7.8 15.1 (3.1) Valuation matrix (x) FY10 FY11E FY12E FY13E P/E @ CMP 629.5 60.7 6.5 4.9 P/E @ Target 786.9 75.8 8.1 6.1 EV/EBITDA @ CMP 404.7 46.5 4.8 3.6

Transcript

Sunteck Realty Ltd Initiating Coverage 02 December 2010

RCML: Winner of LIPPER-STARMINE broker award for “Earnings Estimates in Midcap Research 2008” | “Honourable Mention” in Institutional Investor 2009 | Voted amongst Top 5 most improved brokerages by

Asia Money Poll 2009 | RCML Research is also available on Bloomberg FTIS <GO> and Thomson First Call

Initiating Coverage 02 December 2010

Financial highlights

(Rs mn) FY10 FY11E FY12E FY13E

Revenue 284 1,629 14,246 22,417

Growth (%) 37.9 473.5 774.7 57.4

Adj net income 62 639 5,961 7,951

Growth (%) (64.2) 937.8 832.3 33.4

FDEPS (Rs) 1.0 10.2 94.7 126.3

Growth (%) (93.2) 937.8 832.3 33.4

Profitability and return ratios

(%) FY10 FY11E FY12E FY13E

EBITDA margin 37.9 57.5 63.9 54.0

EBIT margin 33.8 56.6 63.7 53.9

Adj PAT margin 21.7 39.3 41.8 35.5

ROE 1.5 10.1 62.8 49.2

ROIC 0.8 5.9 50.8 93.9

ROCE 0.9 5.9 43.3 39.1

Sunteck Realty Ltd Asset-light model with high cash flow visibility

We initiate coverage on Sunteck Realty (SRL) with a BUY rating and a target price of Rs 800 (implied P/BV of 2x on FY13E), offering a 23% upside. SRL is one of the best plays on Mumbai’s super-luxury segment, with 67% of its land bank located in and around the city. We like SRL for: (1) its asset-light model through JVs and joint development agreements (JDA) with landowners, resulting in low land cost of Rs 409psf and high IRRs of 50–55%; (2) its three key super-luxury residential projects in BKC-Mumbai (a commercial hub), which form 25% of our GAV (Rs 285/sh) and are likely to generate net cash of Rs 30bn+ (pre-tax) over FY11-FY13; and (3) its strong financials with a adjusted D/E ratio of 0.4x and high operating cash flow visibility of Rs 6.7bn and Rs 17.5bn in FY12 and FY13 respectively. We estimate a sales/EPS CAGR of 326%/400% over FY10-FY13. Key risks are timely execution, approval delays and an economic slowdown.

Asset-light business model: SRL holds 77% of its saleable area through JV/JDAs with landowners and the balance through slum rehabilitation schemes (SRA), redevelopment projects and land buyouts. We believe the JV/JDA model helps the company build a capital-efficient business by stripping away the investment on land purchase and allowing a greater focus on value addition. It also supports efficient capacity utilisation and higher IRR (50–55%). The cost of land via JDA/JVs is Rs 48/Rs 130psf for SRL, significantly lower than that of outright land buyouts.

Cash flows to strengthen: SRL is currently developing three super-luxury residential projects in Mumbai’s BKC district. These projects form 25% of our gross annual value for the company and are likely to generate cash of Rs 30bn (pre-tax) over FY11-FY13 (in comparison, the company’s current market cap is ~Rs 39bn). We expect residential absorption of 4.0msf (FY11: 0.8msf; FY12: 1.7msf; FY13: 1.5msf) including the above projects, which will aid further cash generation during FY11-FY13. Operating cash flows during FY12 and FY13 are estimated at Rs 6.7bn and Rs 17.5bn respectively, which will likely be utilised for further land acquisition. SRL’s adjusted D/E ratio of 0.4x could decline further, in our view.

Improving revenue and margin profile: Since SRL follows the project completion method, a bulk of the revenue from ongoing projects is expected in FY12 and FY13. The company’s EBITDA margin is also likely to improve from 38% in FY10 to 54% in FY13 as high end luxury projects get recognised.

Initiate with BUY: We value SRL at a 20% discount to NAV, translating to a target price of Rs 800. Key risks to our estimates are execution risk, rules and regulations in newer territories which may delay projects, and a slowdown in the economy.

CMP TARGET RATING RISK

Rs 615 Rs 800 BUY HIGH

BSE NSE BLOOMBERG

512179 SUNTECK SRL IN

Company data

Market cap (Rs mn / US$ mn) 38,726/850

Outstanding equity shares (mn) 63

Free float (%) 16.9

Dividend yield (%) -

52-week high/low (Rs) 714 / 480

2-month average daily volume 112,665

Stock performance

Returns (%) CMP 1-mth 3-mth 6-mth

SRL (8.4) (1.1) 0.9 (8.4)

BSE REAL 1.8 18.3 21.4 1.8

Sensex (3.1) 7.8 15.1 (3.1)

Valuation matrix

(x) FY10 FY11E FY12E FY13E

P/E @ CMP 629.5 60.7 6.5 4.9

P/E @ Target 786.9 75.8 8.1 6.1

EV/EBITDA @ CMP 404.7 46.5 4.8 3.6

Sunteck Realty Ltd Initiating Coverage 02 December 2010

2

Investment rationale

Unique strategy minimises capital commitment SRL has acquired 77% of its land bank through joint ventures and joint development agreements with landowners. This model reduces the early capital commitment for the company as it is spared the heavy land acquisition costs. Moreover, apart from JV/JDAs, SRL has certain projects under slum rehabilitation and redevelopment schemes, which require lower capital commitments. The company has thus incurred a significantly lower cost (per sq ft) for these assets as compared to the direct purchase or buyout of land. Moreover, all the land acquisitions through JVs/JDAs and buyouts have been evenly spread out over earlier years (Fig-2).

Fig 1 - Model-wise land cost

Model Total area (msf)

Eco Interest (msf)

Total cost (Rs psf)

SRL cost (Rs psf)

Total (Rs psf)

SRL(Rs psf)

JV 4.4 4.4 1,268 577 285 130

JDA 20.5 13.5 1,282 641 63 48

Redevelopment 0.2 0.2 243 243 1,398 1,398

SRA 2.8 2.4 443 443 159 187

Buyout 4.1 4.1 13,218 8,149 3,186 1,964

Total 32.0 25.0 16,455 10,052

Source: Company, RCML Research

Fig 2 - Land acquisition evenly distributed

Sunteck Center Sunteck Samruddha

Signature Island

Signia Woods

Signia Poonam

Sunteck Grandeur

Sunteck Kanaka

Sunteck Crest

Signia Skys

Oman Villas

Signia Isles I

Signia Gardens

Signia Star

Sunteck Classic

Signia City (Jaipur)

Signia City (Thane)

Nagpur Ent. City

Signia Oceans

Signia City (Mulund)

Signia Pearl

Sunteck City

Signia Dadar

Signia Mahalaxmi

Sunteck Kalina

Signia Andheri (W)

In Pipeline 2

In Pipeline 3

0

2

4

6

8

10

2005 2006 2007 2008 2009 2010

New

Pro

ject

s

Year Acquired

Project Accretion

0.2 Mn sqft

1.1 Mn sqft

2.2 Mn sqft

23.1 Mn sqft

0.3 Mn sqft

5.4 Mn sqft

Signia, N. MumbaiIndia REIT Investment in S Island

Kotak REF investment in Sunteck

Debenture issued to Kotak REF-Signia Isles

CY

Source: Company

Strong cash flow from launch pipeline SRL has projects covering over 2.5msf under construction and is likely to launch a further 3.5msf in FY11. We expect residential absorption of 4msf over FY11-FY13. We believe the resultant cash flows would be utilised for self-financing of residential projects and for land acquisition. A bulk of these flows (Rs 30bn+) is likely to come from three residential properties: Signature Island and Signia Isle-I in FY11 and FY12 respectively, followed by Signia Pearl in FY13—these projects cumulatively account for 25% of our GAV (Fig-4). Moreover SRL has 0.22 msf of leased assets which contributes over Rs 150 mn pa .We expect operational cash flows of Rs 6.7 and Rs 17.5bn in FY12 and FY13 respectively.

JV/JDA model frees up capital for

further land acquisition

3 BKC projects alone could contribute

cash flows in excess of Rs 30bn by FY13

Sunteck Realty Ltd Initiating Coverage 02 December 2010

3

Fig 3 - Projects under construction

Project Location Segment Area (msf) Stake % Sold

Signature Island BKC, Mumbai Residential 0.71 87.5% 36%

Sunteck Grandeur Andheri, Mumbai Commercial 0.08 100% Not launched

Sunteck Kanaka Goa Commercial 0.12 50% Not launched

Total 2.5

Source: Company, RCML Research

Fig 4 - 3 key residential projects in BKC, Mumbai

Source: Company

MMR forms 67% of land bank; spreading wings in key cities SRL has 67% of its land bank in and around Mumbai, covering 21.6msf (in 14 of 26 projects, both ongoing and planned). Of this, it has ~7msf between Andheri and Mahalaxmi which command premium realisations. Moreover, SRL’s land cost for Mumbai is low at Rs 916psf; this together with its ability to command premium realisations (by way of strong brand equity) will bolster margins. Apart from Mumbai, SRL has forayed into Goa, Nagpur, Jaipur and Karnataka, where it has maintained its unique land acquisition strategy.

Low land cost of Rs 916psf in booming

Mumbai market

Sunteck Realty Ltd Initiating Coverage 02 December 2010

4

Fig 5 - MMR project map

Source: Company

Low-leverage business SRL’s D/E ratio for FY10 is comfortable at 0.6x. This leaves plenty of room to raise further debt in order to meet working capital needs in the event that surplus cash flows from new launches are deployed for land acquisition. Moreover, of the FY10 consolidated debt of Rs 3.9bn on its books, SRL’s share is Rs 2.4bn (Net D/E of 0.4x) (Fig-6).

Fig 6 - SRL’s share of debt

(Rs mn) Consolidated Debt Sunteck Liability

Consolidated unsecured loan 4,577 2,439

Less : Intercorporate deposits (PSRPL to SSPL) (2,222) (1,111)

Unsecured debt as on 31st Mar on balance sheet 2,356 1,328

Secured Loan

Consolidated secured loan 1610 1110

Total debt 3,966 2,438

Source: RCML Research

Strong branding supports premium realisations We believe that a strong, recognisable brand is a key differentiator in the real estate industry as this strongly influences customer buying decisions. SRL brands its high-end residential properties as Signature and Signia and commercial properties as Sunteck. Most of its projects are in JV with the Ajay Piramal group, which further creates brand recognition. We believe the quality of construction and brand recall enables the company to quote a premium in comparison to other builders (Fig-7).

Adjusted D/E is at 0.4x

Sunteck Realty Ltd Initiating Coverage 02 December 2010

5

Fig 7 - SRL commands a selling price premium to other developers

SN Project name Developer Location Sale Price(Rs psf)

A Mayfair Meridian Mayfair Housing SV Road, Andheri (W) 14,820

Raheja Plaza K Raheja Universal Andheri (W) 15,960

E Turning Point- Comm Trimurti Colonizer Bani Park 7,500

Govind Enclave-Comm Unique Dream Builders Bani Park 7,500

Signia City -Comm Sunteck Realty Bani Park 8,500

F Hirannadani Heritage Hiranandani Borivali-Mumbai 11,000

Kanakia Space Kanakia Borivali-Mumbai 10,500

Signia High Sunteck Realty Borivali-Mumbai 12,000

Source: RCML Research

Financial overview

Revenues to surge in FY13 We assume FY11/FY12/FY13 residential absorption levels of 0.8/1.7/1.5msf. Considering the recent increase in property prices, we do not assume property price rise in FY12 across various projects. The company follows the project completion method for revenue recognition, and we therefore expect substantial revenues during FY12 and FY13 (Rs 37bn) when its ongoing projects are likely to be complete.

Fig 8 - Absorption estimates

(msf) FY11E FY12E FY13E

Absorption

Residential 0.8 1.7 1.5

Commercial 0.5 0.2 0.1

Total 1.3 1.9 1.7

Source: RCML Research

Luxury Brand helps SRL garner

premium realisations

Project completion to lead the revenue

growth in FY13

Sunteck Realty Ltd Initiating Coverage 02 December 2010

6

EBITDA margin set to expand SRL’s EBITDA margin is likely to improve from 38% in FY10 to 53% in FY13 on account high-end luxury projects. In the long run, we believe the company should maintain a gross margin in the range of 55–60% led by its JV/JDA model and focus on the super-luxury segment.

Fig 9 - Margin improving going forward

38

58

64

53

76

70 68

55

30

40

50

60

70

80

FY10 FY11E FY12E FY13E

EBIDTA margin Gross margin(%)

Source: Company ,RCML Research

Strong balance sheet SRL’s balance sheet is likely to be further strengthened as its D/E ratio remains below 1x and the company generates estimated cash from operations of Rs 6.7bn and Rs 17.5bn in FY12 and FY13 respectively. This may be utilised for land acquisition.

Moreover, Sunteck’s portion of debt (excluding minority shareholder’s share) is further low (Fig 6)

Fig 10 - Cash position

FY10 FY11E FY12E FY13E

Total cash 344 339.8 6,545.2 24,328.9

Gross Debt 3966 4,866.6 4,366.6 4,866.6

Net Cash (3622) (4,526.8) 2,178.6 19,462.2

Source: RCML Research

Valuation

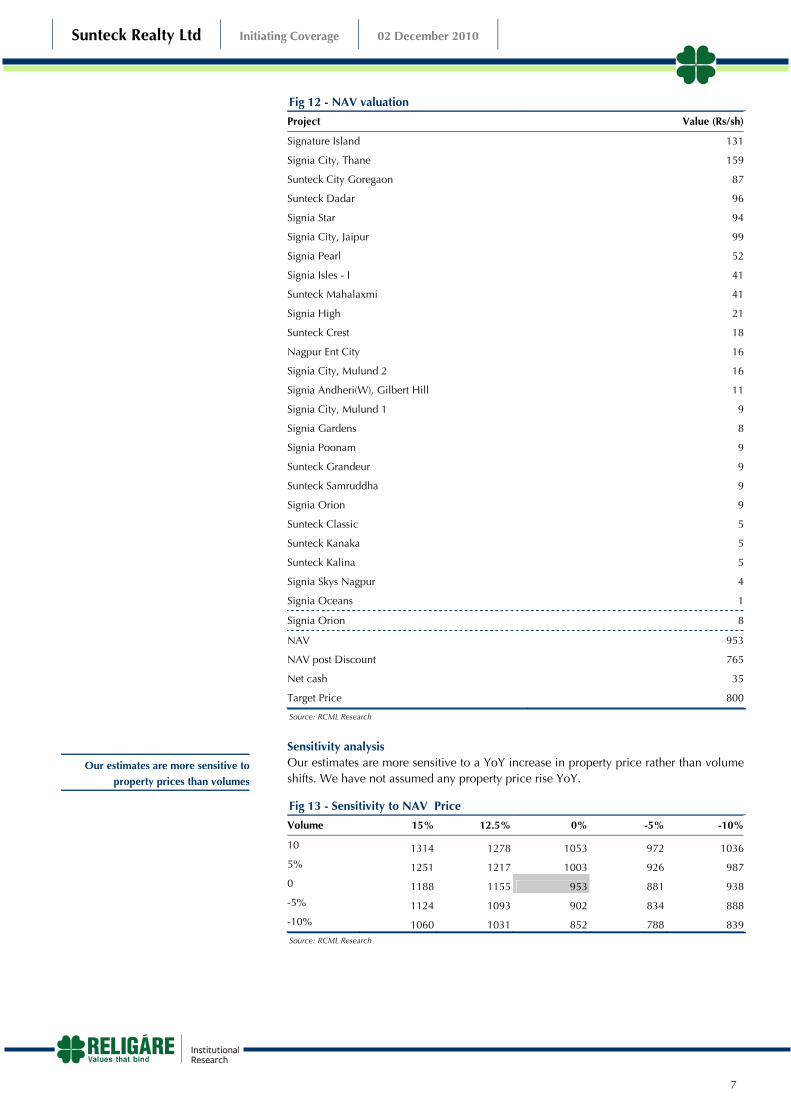

Initiate with BUY We have a target price of Rs 800 for the stock, valuing SRL’s total saleable land bank of 32msf at a 20% discount to NAV. We initiate coverage with a BUY rating given the potential 30% upside from current levels. Momentum in new launches would be a key trigger for the stock.

Fig 11 - Key assumption s

Assumption

RFR (%) 8

Beta (x) 1.2

WACC (%) 12.5

CoE (%) 14

CoD (%) 15

Source: RCML Research

EBITDA margin likely to expand from

38% in FY10 to 53% in FY13

Sales and Profit estimates

(Rs mn) FY10 FY11E FY12E FY13E

Sales 284.0 1628.7 14246.3 22131.0

EBITDA 108 937 9102 11821

EBITDA margin (%)

38% 58% 64% 53%

EPS (Rs) 1 10 95 123

Source: RCML Research

We value SRL at 20% discount to NAV

Sunteck Realty Ltd Initiating Coverage 02 December 2010

7

Fig 12 - NAV valuation

Project Value (Rs/sh)

Signature Island 131

Signia City, Thane 159

Sunteck City Goregaon 87

Sunteck Dadar 96

Signia Star 94

Signia City, Jaipur 99

Signia Pearl 52

Signia Isles - I 41

Sunteck Mahalaxmi 41

Signia High 21

Sunteck Crest 18

Nagpur Ent City 16

Signia City, Mulund 2 16

Signia Andheri(W), Gilbert Hill 11

Signia City, Mulund 1 9

Signia Gardens 8

Signia Poonam 9

Sunteck Grandeur 9

Sunteck Samruddha 9

Signia Orion 9

Sunteck Classic 5

Sunteck Kanaka 5

Sunteck Kalina 5

Signia Skys Nagpur 4

Signia Oceans 1

Signia Orion 8

NAV 953

NAV post Discount 765

Net cash 35

Target Price 800

Source: RCML Research

Sensitivity analysis Our estimates are more sensitive to a YoY increase in property price rather than volume shifts. We have not assumed any property price rise YoY.

Fig 13 - Sensitivity to NAV Price

Volume 15% 12.5% 0% -5% -10%

10 1314 1278 1053 972 1036

5% 1251 1217 1003 926 987

0 1188 1155 953 881 938

-5% 1124 1093 902 834 888

-10% 1060 1031 852 788 839Source: RCML Research

Our estimates are more sensitive to

property prices than volumes

Sunteck Realty Ltd Initiating Coverage 02 December 2010

8

Fig 14 - Cash flow

FY10 FY11E FY12E FY13E

Sales Inflow 227.69 1396.78 11826.48 24534.96

Other inflow 23.70 32.10 34.10 37.10

Outflow

Construction Costs (3753.64) (3491.35) 888.54 (6111.43)

Other (Admin Costs) (104.50) (200.13) (569.85) (269.00)

Tax payment (29.06) (58.47) (314.95) (2936.16)

Interest payments 0.00 0.00 (218.33) (243.33)

Debt payments 2780.82 900.61 (500.00) 500.00

Land purchase

Capex (1151.48) (29.76) (36.98) (44.52)

Dividend payment (11.04) (15.06) (36.84) (221.01)Change in debtors / loan and advances (3332.56) 1682.59 (4866.78) 2537.10

Investments 1334.18 131.33 0.00 0.00

Changes in Equity 4352.34 (352.92) 0.00 0.00

Total outflow 85.08 (1433.16) (5655.18) (6788.37)

Net Cash Flow 336.47 (4.29) 6205.40 17783.70

Cash at beginning of year 7.74 343.88 339.83 6545.23

Cash at end of year 343.88 339.83 6545.23 24328.87

Net Cash Flow 336.14 (4.05) 6205.40 17783.64Source: RCML Research

Key concerns

Execution the biggest risk So far, SRL has delivered only 0.22msf till FY10 whereas we expect 32msf over the next 7–8 years. Execution is thus one of the key risks to our estimates. At the same time, we note that the company has appointed prominent contractors on various projects.

Sensitive to property prices Our NAV is more sensitive to prices in comparison to volumes. Any decline in property prices may thus significantly affect our valuation.

Economic slowdown A slowdown in the economy may lead to a fall in property prices and absorption, in turn impacting SRL’s business.

Execution a key risk to our estimates

Sunteck Realty Ltd Initiating Coverage 02 December 2010

9

Company background

SRL was incorporated in 1981 but commenced real estate operations only in the year 2000. In 1985, the company was rechristened from Insul Electronic to Sunteck Realty and Infrastructure, and later to Sunteck Realty in 2007. The real estate business was founded by Kamal Khetan and Manish Khetan (promoters), who have several years of experience in the market. SRL has attracted investment from Kotak private equity fund and led to a JV with the Ajay Piramal group.

SRL is developing a number of its ongoing and planned projects jointly with the Piramal group and we believe this partnership enables it to reduce its capital commitment and forge a stronger brand image. Over the past decade, the company has acquired land in the heart of Mumbai (BKC), which is likely to add significant value in the next couple of years.

SRL’s real estate portfolio consists of 26 projects covering 32msf of saleable area across residential (18.9msf), commercial (13.2msf) and retail development. In addition, it has 219,350sq ft of prime commercial assets in the established business districts of BKC, Vile Parle and Andheri, Mumbai. The company has delivered 0.22msf so far in the commercial segment and has 2.5msf under construction.

Fig 15 - Organisation structure

Piramal Sunteck Other Projects via JVs/JDAs/Owned Land & Business Centers

Sunteck Realty

Sunteck Creast, Sion(33%)

Signia City, Mulund(50%)

Signia Isles BKC

Signia Pearl BKC

Signia City, Mulund(68%)

Signia & Sunteck City, Thane(75%)

Signia Nagpur

Signia City, Jaipur(62.5%)

Signia Oceans, New Mumbai

Madinat Al llam – Villas, Oman (50%)

Nagpur Entertainment City(55%)

Signature Island, BKC(80%)

Signia Gardens, Vile Parle (W)

Sunteck Center, Vile Parle (W)(50%)

Sunteck Grandeur, Andheri (W)

Signia High, Borivali (E)(62.5%)

Sunteck Poonam, Andheri

Sunteck Centrako, BKC

Sunteck Certainty, BKC(80%)

Signia & Sunteck Star, Ghatkoper (84.18%)

Sunteck Classic, Andheri (50%)

Sunteck Amenity & Magenta, Andheri (W)

Sunteck Kanaka, Goa(50%)

Promoters Others

34.68%65.32%

50%

50%

Sunteck, Andheri (W)Sunteck City,

GoregaonSignia Dadar

(50%)Signia Mahalaxmi

(50%)

Signia Orion,New Mumbai

Sunteck Kalina(56.5%)

FII & others institutions

@15%

Source: Company

Sunteck Realty Ltd Initiating Coverage 02 December 2010

10

Residential segment SRL has 18 residential projects covering 18.9msf, of which 2.2msf is under construction. Its properties are marketed under the brand names of Signature and Signia. The Signature brand comprises high-end, luxury residences and is aimed at high-net worth individuals. These developments are in prime city locations and have apartments sized above 6,000sq ft. Signia comprises premium and mid-level residences in select areas. Apartments under this brand are generally between 1,200sq ft and 5,000sq ft.

Fig 16 - Residential projects

Project name Location Saleable area Effective Stake

Signature Island Plot No. R1.2 & 1.3, BKC 0.71 100.00%

Signia Isles - I Plot No. R1.4, BKC 0.43 100.00%

Signia Pearl Plot No. R1.1, BKC 0.43 100.00%

Signia Star Ghatkopar 1.30 100.00%

Signia City, Jaipur Bani Park, Jaipur 4.29 100.00%

Signia Andheri(W),Gillbert Hill Andheri 0.10 100.00%

Signia Orion Airoli Sec-10 0.29 100.00%

Total 18.9

Source: company, RCML research

Commercial segment SRL has 11 commercial projects covering 13.2msf, of which 0.3msf is under construction. The company markets its properties under the brand name Sunteck. Apart from the above commercial assets, the company has 0.22msf of leased assets which contribute rent over~Rs 150mn per year.

Fig 17 - Commercial Projects – Under Construction

Project name Location Saleable area Effective Stake

Signia Star Ghatkopar 1.3 100.00%

Signia City, Jaipur Bani Park, Jaipur 4.3 100.00%

Signia City, Thane Thane 4.0 100.00%

Signia Poonam Andheri 0.1 100.00%

Sunteck Crest Sion 1.6 33.00%

Sunteck Classic Andheri 0.1 50.00%

Sunteck Granduer Andheri 0.1 100.00%

Nagpur Ent City Nagpur 1.1 55.00%

Sunteck Samruddha Hubli 0.4 26.00%

Sunteck Kanaka Goa 0.1 50.00%

Sunteck Kalina Bandra 0.1 100.00%

Total 13.2

Source: Company, RCML Research

2.2msf of residential projects under

construction

0.3msf of commercial space under

construction

Sunteck Realty Ltd Initiating Coverage 02 December 2010

11

Fig 18 - Commercial Projects – Completed

Leased Projects Location Saleable Area (msf) Effective Stake (%)

SRL was incorporated in 1981 but commenced real estate

operations only in the year 2000. In 1985, the company was

rechristened from Insul Electronic to Sunteck Realty and

Infrastructure, and later to Sunteck Realty in 2007.SRL is a Mumbai-

based realty player focussed on the super-luxury and luxury

residential segments. It has a 32msf land bank of which 67% is in

the MMR.

Shareholding pattern

(%) Mar-10 Jun-10 Sep-10

Promoters 65.3 65.3 65.3

FIIs 5.3 5.6 5.6

Banks & FIs - - -

Public 29.4 29.1 29.1

Recommendation history

Date Event Reco price Tgt price Reco

02-Dec-10 Initiating Coverage 615 800 Buy

Stock performance

590

610

630

650

670

690

710

Jul-10 Aug-10 Sep-10 Oct-10 Nov-10 Dec-10

Buy

Sunteck Realty Ltd Initiating Coverage 02 December 2010

14

Coverage Profile

By recommendation By market cap (US$)

31

9

60

0

20

40

60

80

Buy Hold Sell

(%)

69

29

20

20

40

60

80

> $1bn $200mn - $1bn < $200mn

(%)

Recommendation interpretation

Recommendation Expected absolute returns (%) over 12 months

Buy More than 15%

Hold Between 15% and –5%

Sell Less than –5%

Recommendation structure changed with effect from March 1, 2009

Expected absolute returns are based on share price at market close unless otherwise stated. Stock recommendations are based on absolute upside (downside) and have a 12-month horizon. Our target price represents the fair value of the stock based upon the analyst’s discretion. We note that future price fluctuations could lead to a temporary

mismatch between upside/downside for a stock and our recommendation.

This document is NOT addressed to or intended for distribution to retail clients (as defined by the FSA). This document is issued by Religare Capital Markets plc (“RCM”) in the UK, which is authorised and regulated by the Financial Services Authority in connection with its UK distribution. RCM is a member of the London Stock Exchange.

This material should not be construed as an offer or recommendation to buy or sell or solicitation of any offer to buy any security or other financial instrument, nor shall it, or the fact of its distribution, form the basis of, or be relied upon in connection with, any contract relating to such action or any other matter. The material in this report is based on information that we consider reliable and accurate at, and share prices are given as at close of business on, the date of this report but we do not warrant or represent (expressly or impliedly) that it is accurate, complete, not misleading or as to its fitness for the purpose intended and it should not be relied upon as such. Any opinion expressed (including estimates and forecasts) is given as of the date of this report and may be subject to change without notice.

RCM, and any of its connected or affiliated companies or their directors or employees, may have a position in any of the securities or may have provided corporate finance advice, other investment services in relation to any of the securities or related investments referred to in this document. Our asset management area, our proprietary trading desks and investing businesses may make investment decisions that are inconsistent with the recommendations or views expressed in this briefing note.

RCM accepts no liability whatsoever for any direct, indirect or consequential loss or damage of any kind arising out of the use of or reliance upon all or any of this material howsoever arising. Investors should make their own investment decisions based upon their own financial objectives and financial resources and it should be noted that investment involves risk, including the risk of capital loss.

This document is confidential and is supplied to you for information purposes only. It may not (directly or indirectly) be reproduced, further distributed to any person or published, in whole or in part, for any purpose whatsoever. Neither this document, nor any copy of it, may be taken or transmitted into the United States, Canada, Australia, Ireland, South Africa or Japan or into any jurisdiction where it would be unlawful to do so. Any failure to comply with this restriction may constitute a violation of relevant local securities laws. If you have received this document in error please telephone Nicholas Malins-Smith on +44 (0) 20 7382 4479.