28

Finn Casey Winnie Chin Jonathan Faulk Schuyler O’Reilly AMN Healthcare Services Inc. Strategic Discussion Materials April 1 st , 2016

| Date post: | 22-Jan-2018 |

| Category: |

Economy & Finance |

| Upload: | schuyler-oreilly |

| View: | 166 times |

| Download: | 0 times |

Finn Casey

Winnie Chin

Jonathan Faulk

Schuyler O’Reilly

AMN Healthcare Services Inc. Strategic Discussion Materials

April 1st, 2016

Our Team

Finn Casey

• Indiana University, Kelley School of Business, 2019

• Majors: Finance & Accounting

• Naperville, IL

Winnie Chin

• Indiana University, Kelley School of Business, 2019

• Majors: Accounting, Business Analytics, Finance

• Taipei, Taiwan

Jonathan Faulk

• Indiana University, Kelley School of Business, 2019

• Majors: Finance & Economic Consulting

• Fort Lauderdale, FL

Schuyler O’Reilly

• Indiana University, Kelley School of Business, 2019

• Majors: Finance & Accounting

• Fishers, IN

2

Table of Contents

3

I. Executive Summary 4

II. Company Overviews 6

III. Industry Overview 9

IV. Strategic Opportunities 11

V. Valuation Analysis 15

VI. Pro Forma Capital Structure 22

VII. Appendix 25

Executive SummarySECTION I

4

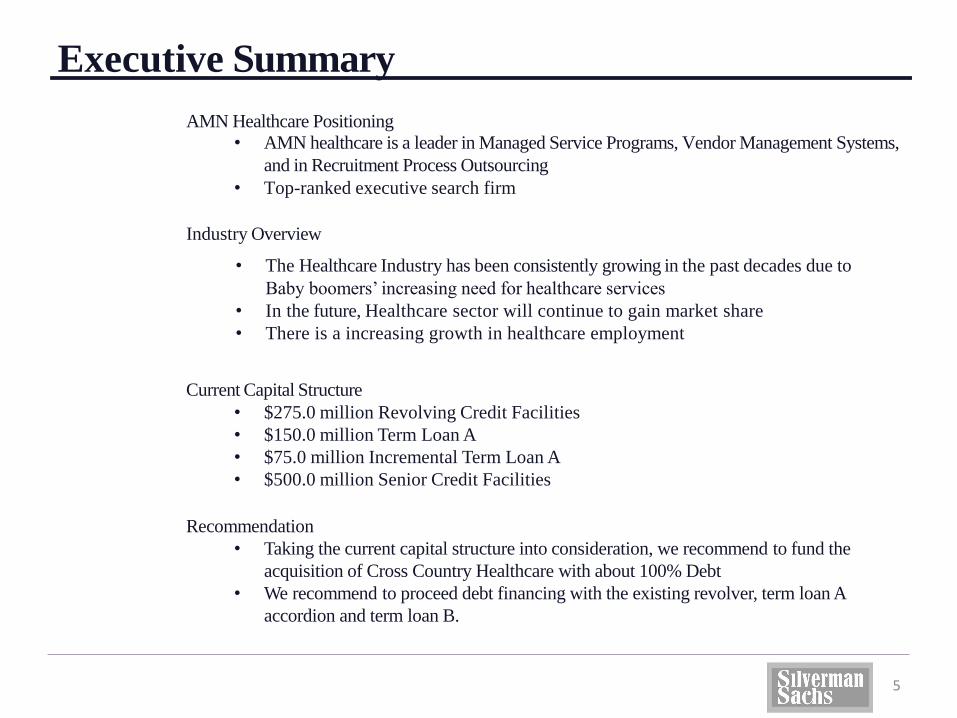

Executive Summary

5

AMN Healthcare Positioning

• AMN healthcare is a leader in Managed Service Programs, Vendor Management Systems,

and in Recruitment Process Outsourcing

• Top-ranked executive search firm

Industry Overview

• The Healthcare Industry has been consistently growing in the past decades due to

Baby boomers’ increasing need for healthcare services

• In the future, Healthcare sector will continue to gain market share

• There is a increasing growth in healthcare employment

Current Capital Structure

• $275.0 million Revolving Credit Facilities

• $150.0 million Term Loan A

• $75.0 million Incremental Term Loan A

• $500.0 million Senior Credit Facilities

Recommendation

• Taking the current capital structure into consideration, we recommend to fund the

acquisition of Cross Country Healthcare with about 100% Debt

• We recommend to proceed debt financing with the existing revolver, term loan A

accordion and term loan B.

Company OverviewSECTION II

6

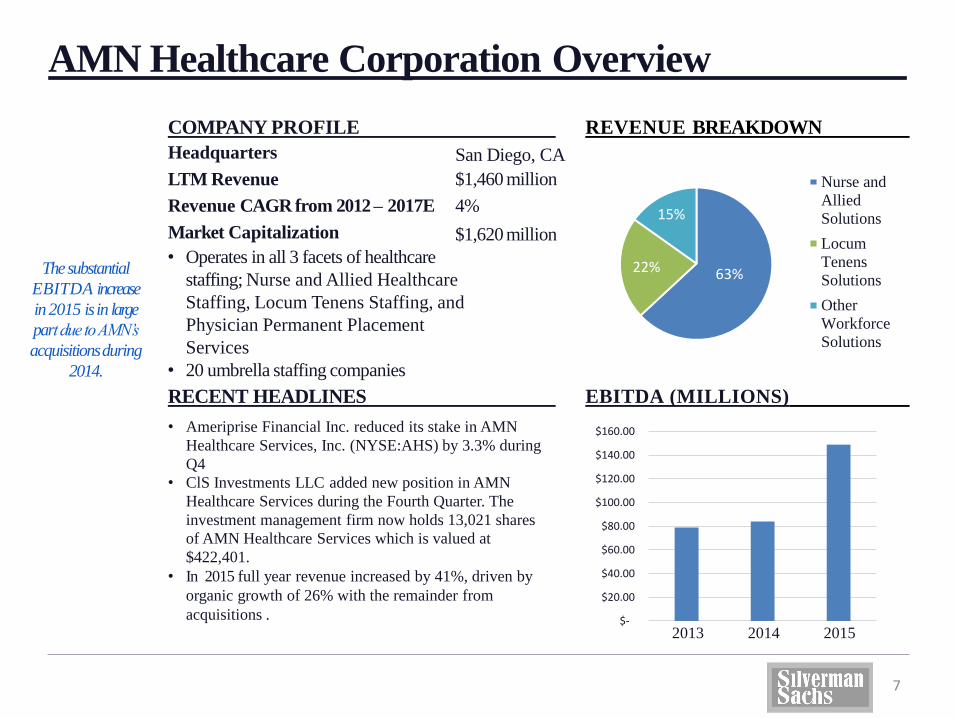

COMPANY PROFILE

Headquarters

LTM Revenue

Revenue CAGR from 2012 – 2017E

Market Capitalization

San Diego, CA

$1,460 million

4%

$1,620 million

AMN Healthcare Corporation Overview

• Operates in all 3 facets of healthcare

staffing; Nurse and Allied Healthcare

Staffing, Locum Tenens Staffing, and

Physician Permanent Placement

Services

• 20 umbrella staffing companies

The substantial

EBITDA increase

in 2015 is in large

part due to AMN’s

acquisitions during

2014.

• Ameriprise Financial Inc. reduced its stake in AMN

Healthcare Services, Inc. (NYSE:AHS) by 3.3% during

Q4

• ClS Investments LLC added new position in AMN

Healthcare Services during the Fourth Quarter. The

investment management firm now holds 13,021 shares

of AMN Healthcare Services which is valued at

$422,401.

• In 2015 full year revenue increased by 41%, driven by

organic growth of 26% with the remainder from

acquisitions .

REVENUE BREAKDOWN

7

RECENT HEADLINES EBITDA (MILLIONS)

63%22%

15%

Nurse and

Allied

Solutions

Locum

Tenens

Solutions

Other

Workforce

Solutions

$-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$160.00

2013 2014 2015

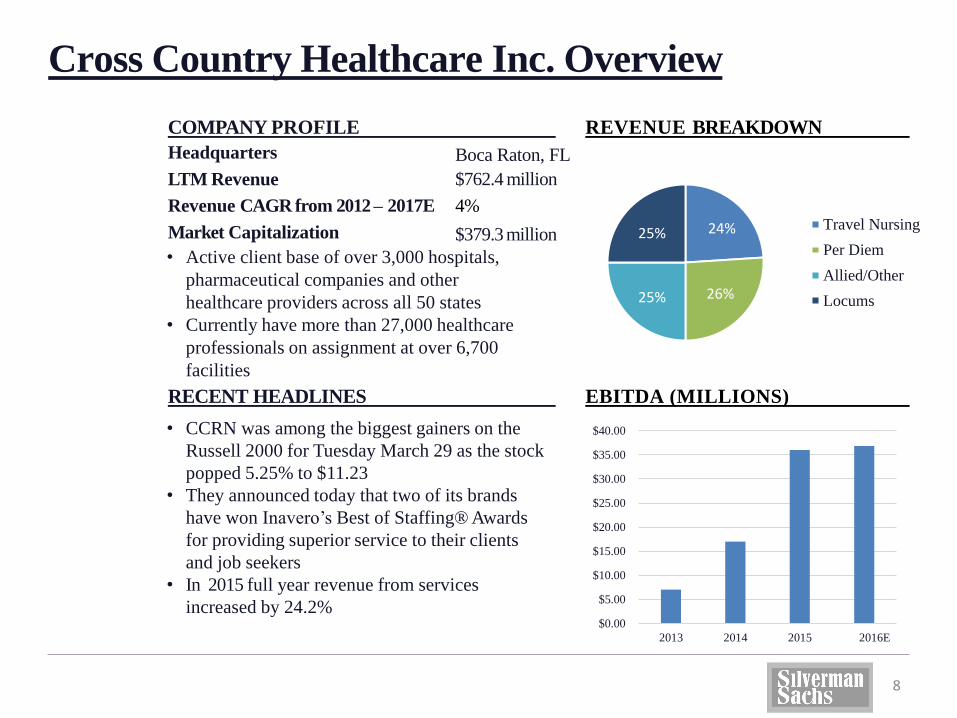

COMPANY PROFILE

Headquarters

LTM Revenue

Revenue CAGR from 2012 – 2017E

Market Capitalization

Boca Raton, FL

$762.4 million

4%

$379.3 million

Cross Country Healthcare Inc. Overview

• CCRN was among the biggest gainers on the

Russell 2000 for Tuesday March 29 as the stock

popped 5.25% to $11.23

• They announced today that two of its brands

have won Inavero’s Best of Staffing® Awards

for providing superior service to their clients

and job seekers

• In 2015 full year revenue from services

increased by 24.2%

REVENUE BREAKDOWN

8

RECENT HEADLINES EBITDA (MILLIONS)

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

2013 2014 2015 2016E

• Active client base of over 3,000 hospitals,

pharmaceutical companies and other

healthcare providers across all 50 states

• Currently have more than 27,000 healthcare

professionals on assignment at over 6,700

facilities

24%

26%25%

25%Travel Nursing

Per Diem

Allied/Other

Locums

Industry OverviewSECTION III

9

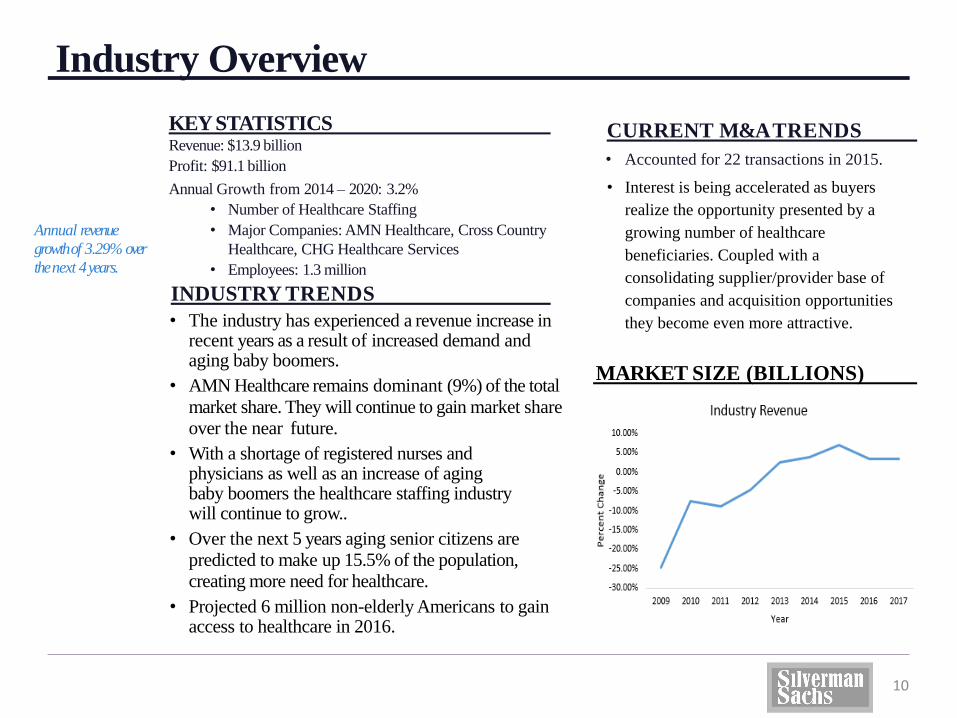

KEYSTATISTICSRevenue: $13.9 billion

Profit: $91.1 billion

Annual Growth from 2014 – 2020: 3.2%

• Number of Healthcare Staffing

• Major Companies: AMN Healthcare, Cross Country

Healthcare, CHG Healthcare Services

• Employees: 1.3 million

Industry Overview

CURRENT M&ATRENDS

• Accounted for 22 transactions in 2015.

• Interest is being accelerated as buyers

realize the opportunity presented by a

growing number of healthcare

beneficiaries. Coupled with a

consolidating supplier/provider base of

companies and acquisition opportunities

they become even more attractive.

INDUSTRY TRENDS

• The industry has experienced a revenue increase in recent years as a result of increased demand and aging baby boomers.

• AMN Healthcare remains dominant (9%) of the total

market share. They will continue to gain market share

over the near future.

• With a shortage of registered nurses and physicians as well as an increase of aging baby boomers the healthcare staffing industry will continue to grow..

• Over the next 5 years aging senior citizens are

predicted to make up 15.5% of the population,

creating more need for healthcare.

• Projected 6 million non-elderly Americans to gain access to healthcare in 2016.

Annual revenue

growth of 3.29% over

the next 4years.

10

MARKET SIZE (BILLIONS)

Strategic OpportunitiesSECTION IV

11

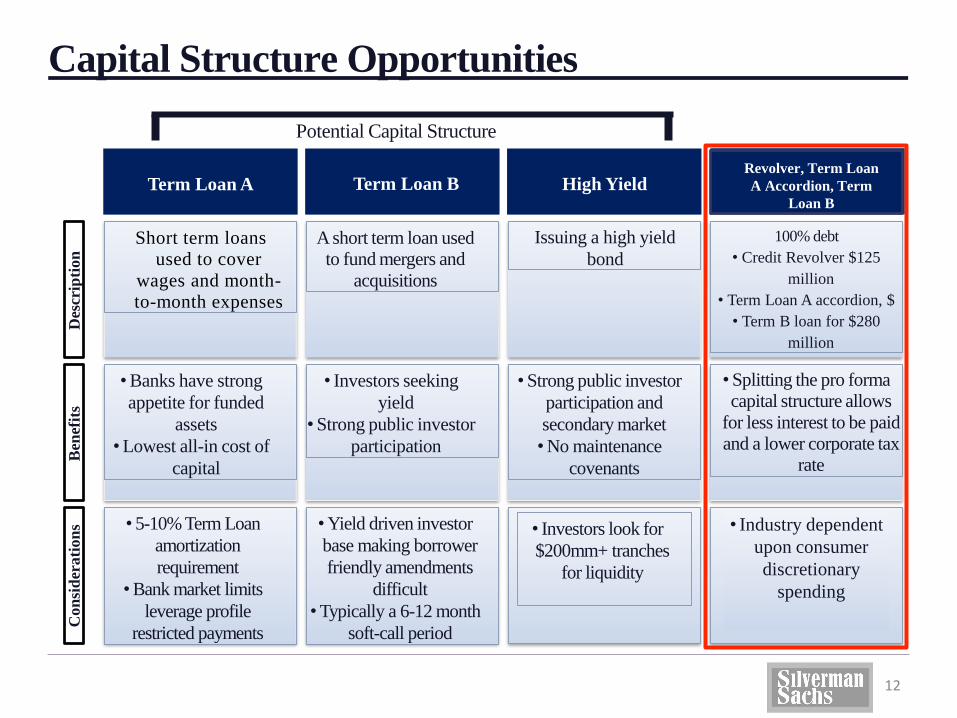

Capital Structure OpportunitiesD

escr

ipti

on

Ben

efit

sC

on

sid

erati

on

s

100% debt

• Credit Revolver $125

million

• Term Loan A accordion, $

• Term B loan for $280

million

•Splitting the pro forma

capital structure allows

for less interest to be paid

and a lower corporate tax

rate

• Industry dependent

upon consumer

discretionary

spending

Short term loans

used to cover

wages and month-

to-month expenses

•Banks have strong

appetite for funded

assets

•Lowest all-in cost of

capital

• 5-10% Term Loan

amortization

requirement

•Bank market limits

leverage profile

restricted payments

A short term loan used

to fund mergers and

acquisitions

• Investors seeking

yield

•Strong public investor

participation

•Yield driven investor

base making borrower

friendly amendments

difficult

•Typically a 6-12 month

soft-call period

Issuing a high yield

bond

•Strong public investor

participation and

secondary market

•No maintenance

covenants

• Investors look for

$200mm+ tranches

for liquidity

Potential Capital Structure

12

Term Loan A Term Loan B High YieldRevolver, Term Loan

A Accordion, Term

Loan B

Geographic

Diversity

Acquisition

Opportunities

Company

Growth

13

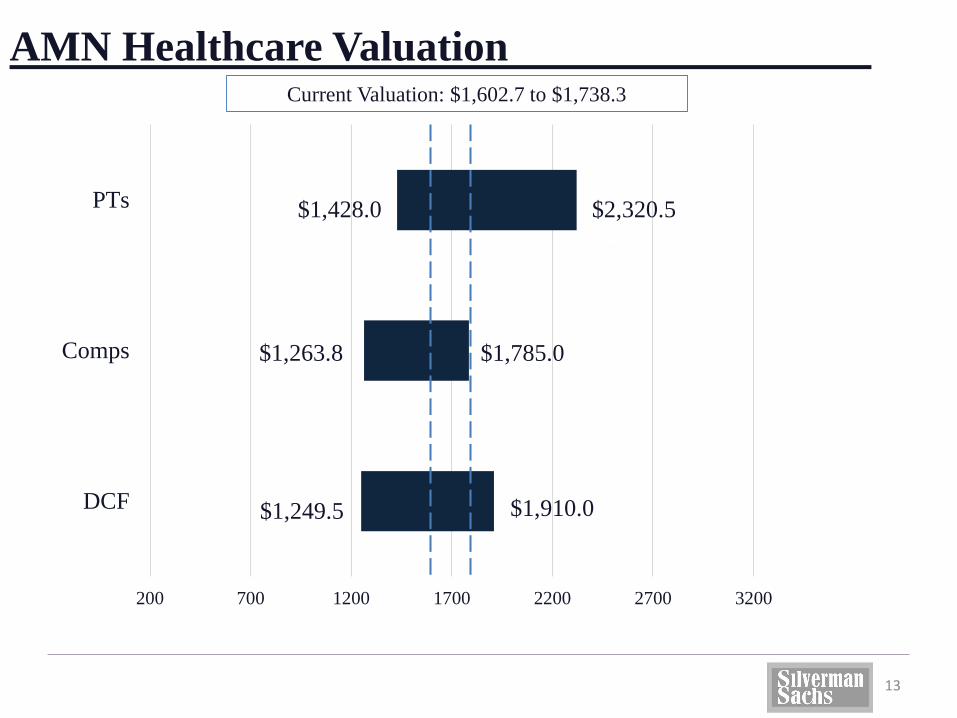

200 700 1200 1700 2200 2700 3200

DCF

Comps

PTs

AMN Healthcare Valuation

$1,249.5

$1,263.8

$1,428.0

$1,910.0

$1,785.0

$2,320.5

Current Valuation: $1,602.7 to $1,738.3

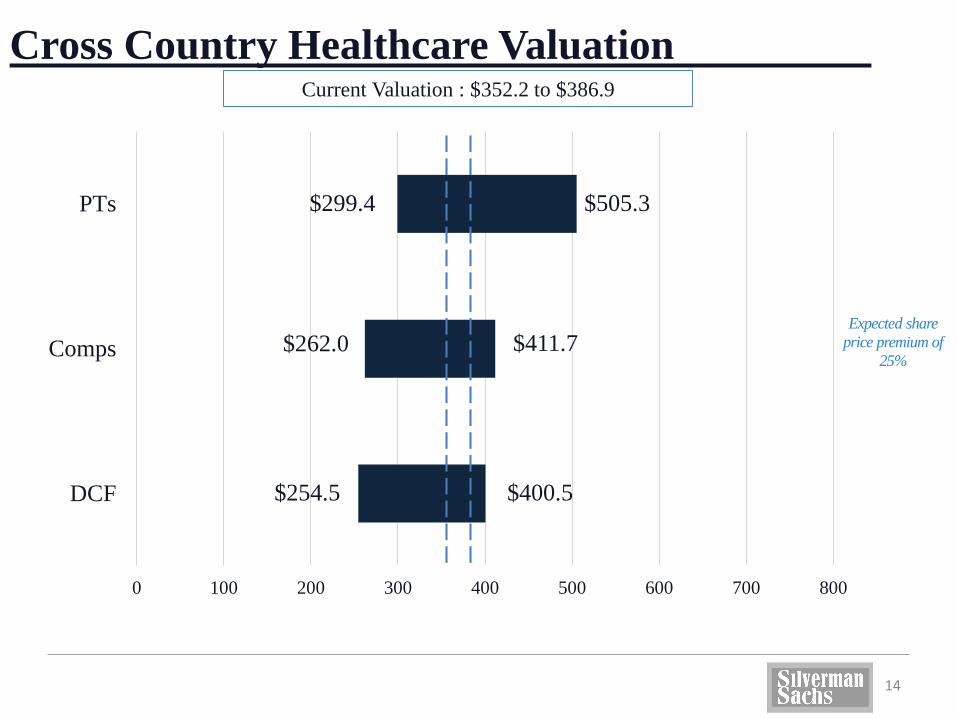

0 100 200 300 400 500 600 700 800

DCF

Comps

PTs

Cross Country Healthcare Valuation

$299.4

$262.0

$505.3

$254.5

$411.7

$400.5

Current Valuation : $352.2 to $386.9

14

Expected share

price premium of

25%

Valuation AnalysisSECTION V

15

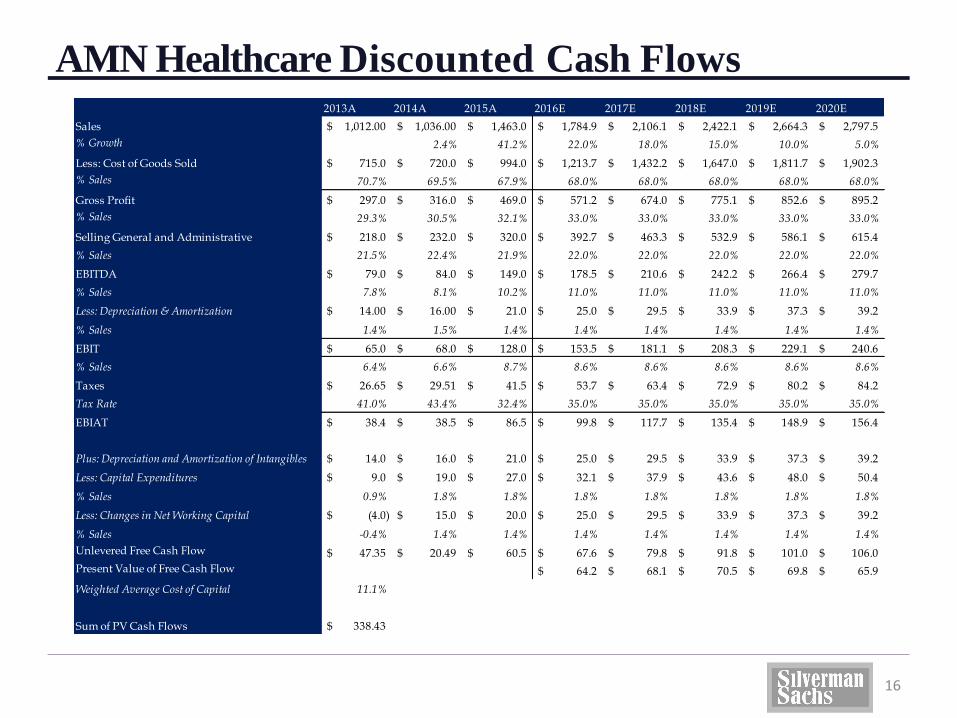

AMN Healthcare Discounted Cash Flows

16

2013A 2014A 2015A 2016E 2017E 2018E 2019E 2020E

Sales 1,012.00$ 1,036.00$ 1,463.0$ 1,784.9$ 2,106.1$ 2,422.1$ 2,664.3$ 2,797.5$

% Growth 2.4% 41.2% 22.0% 18.0% 15.0% 10.0% 5.0%

Less: Cost of Goods Sold 715.0$ 720.0$ 994.0$ 1,213.7$ 1,432.2$ 1,647.0$ 1,811.7$ 1,902.3$

% Sales 70.7% 69.5% 67.9% 68.0% 68.0% 68.0% 68.0% 68.0%

Gross Profit 297.0$ 316.0$ 469.0$ 571.2$ 674.0$ 775.1$ 852.6$ 895.2$

% Sales 29.3% 30.5% 32.1% 33.0% 33.0% 33.0% 33.0% 33.0%

Selling General and Administrative 218.0$ 232.0$ 320.0$ 392.7$ 463.3$ 532.9$ 586.1$ 615.4$

% Sales 21.5% 22.4% 21.9% 22.0% 22.0% 22.0% 22.0% 22.0%

EBITDA 79.0$ 84.0$ 149.0$ 178.5$ 210.6$ 242.2$ 266.4$ 279.7$

% Sales 7.8% 8.1% 10.2% 11.0% 11.0% 11.0% 11.0% 11.0%

Less: Depreciation & Amortization 14.00$ 16.00$ 21.0$ 25.0$ 29.5$ 33.9$ 37.3$ 39.2$

% Sales 1.4% 1.5% 1.4% 1.4% 1.4% 1.4% 1.4% 1.4%

EBIT 65.0$ 68.0$ 128.0$ 153.5$ 181.1$ 208.3$ 229.1$ 240.6$

% Sales 6.4% 6.6% 8.7% 8.6% 8.6% 8.6% 8.6% 8.6%

Taxes 26.65$ 29.51$ 41.5$ 53.7$ 63.4$ 72.9$ 80.2$ 84.2$

Tax Rate 41.0% 43.4% 32.4% 35.0% 35.0% 35.0% 35.0% 35.0%

EBIAT 38.4$ 38.5$ 86.5$ 99.8$ 117.7$ 135.4$ 148.9$ 156.4$

Plus: Depreciation and Amortization of Intangibles 14.0$ 16.0$ 21.0$ 25.0$ 29.5$ 33.9$ 37.3$ 39.2$

Less: Capital Expenditures 9.0$ 19.0$ 27.0$ 32.1$ 37.9$ 43.6$ 48.0$ 50.4$

% Sales 0.9% 1.8% 1.8% 1.8% 1.8% 1.8% 1.8% 1.8%

Less: Changes in Net Working Capital (4.0)$ 15.0$ 20.0$ 25.0$ 29.5$ 33.9$ 37.3$ 39.2$

% Sales -0.4% 1.4% 1.4% 1.4% 1.4% 1.4% 1.4% 1.4%

Unlevered Free Cash Flow 47.35$ 20.49$ 60.5$ 67.6$ 79.8$ 91.8$ 101.0$ 106.0$

Present Value of Free Cash Flow 64.2$ 68.1$ 70.5$ 69.8$ 65.9$

Weighted Average Cost of Capital 11.1%

Sum of PV Cash Flows 338.43$

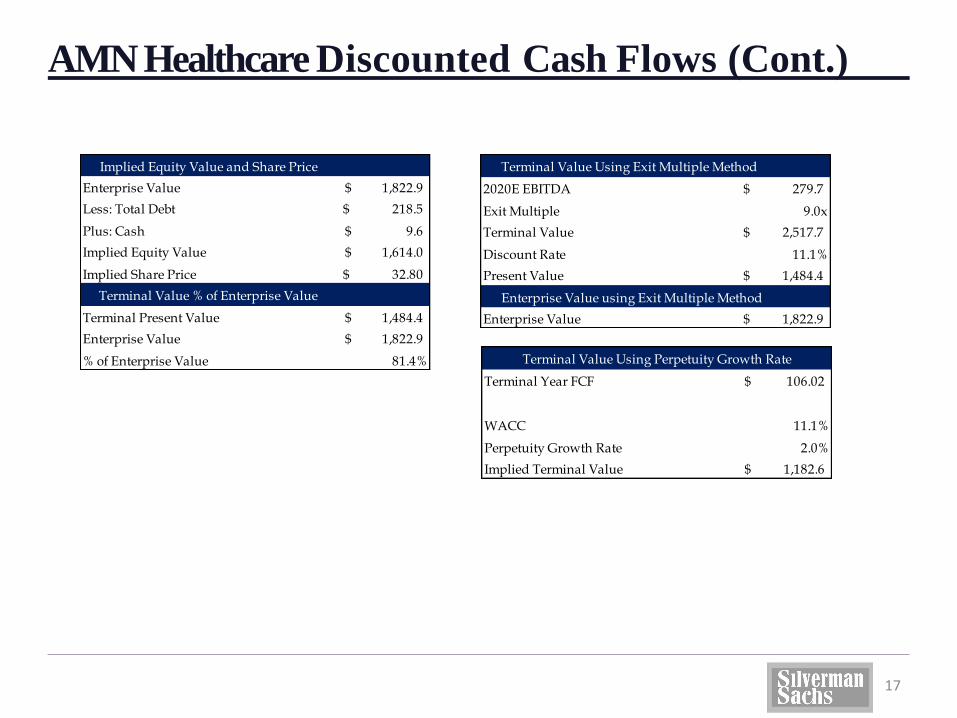

AMN Healthcare Discounted Cash Flows (Cont.)

17

Implied Equity Value and Share Price

Enterprise Value 1,822.9$

Less: Total Debt 218.5$

Plus: Cash 9.6$

Implied Equity Value 1,614.0$

Implied Share Price 32.80$

Terminal Value % of Enterprise Value

Terminal Present Value 1,484.4$

Enterprise Value 1,822.9$

% of Enterprise Value 81.4%

Terminal Value Using Exit Multiple Method

2020E EBITDA 279.7$

Exit Multiple 9.0x

Terminal Value 2,517.7$

Discount Rate 11.1%

Present Value 1,484.4$

Enterprise Value using Exit Multiple Method

Enterprise Value 1,822.9$

Terminal Year FCF 106.02$

WACC 11.1%

Perpetuity Growth Rate 2.0%

Implied Terminal Value 1,182.6$

Terminal Value Using Perpetuity Growth Rate

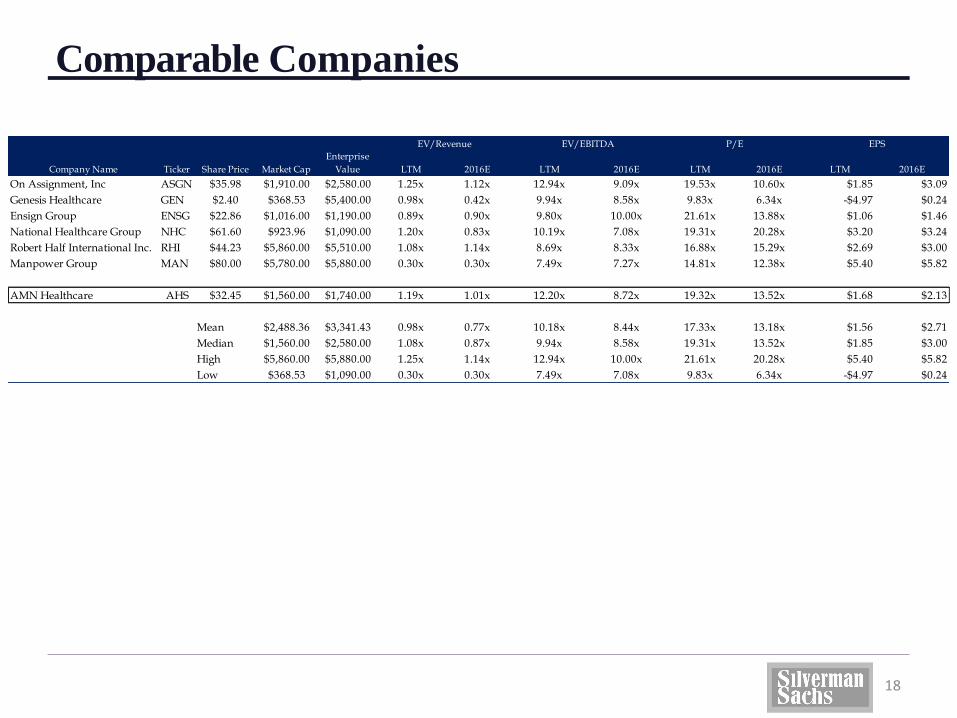

Comparable Companies

18

Company Name Ticker Share Price Market Cap

Enterprise

Value LTM 2016E LTM 2016E LTM 2016E LTM 2016E

On Assignment, Inc ASGN $35.98 $1,910.00 $2,580.00 1.25x 1.12x 12.94x 9.09x 19.53x 10.60x $1.85 $3.09

Genesis Healthcare GEN $2.40 $368.53 $5,400.00 0.98x 0.42x 9.94x 8.58x 9.83x 6.34x -$4.97 $0.24

Ensign Group ENSG $22.86 $1,016.00 $1,190.00 0.89x 0.90x 9.80x 10.00x 21.61x 13.88x $1.06 $1.46

National Healthcare Group NHC $61.60 $923.96 $1,090.00 1.20x 0.83x 10.19x 7.08x 19.31x 20.28x $3.20 $3.24

Robert Half International Inc. RHI $44.23 $5,860.00 $5,510.00 1.08x 1.14x 8.69x 8.33x 16.88x 15.29x $2.69 $3.00

Manpower Group MAN $80.00 $5,780.00 $5,880.00 0.30x 0.30x 7.49x 7.27x 14.81x 12.38x $5.40 $5.82

AMN Healthcare AHS $32.45 $1,560.00 $1,740.00 1.19x 1.01x 12.20x 8.72x 19.32x 13.52x $1.68 $2.13

Mean $2,488.36 $3,341.43 0.98x 0.77x 10.18x 8.44x 17.33x 13.18x $1.56 $2.71

Median $1,560.00 $2,580.00 1.08x 0.87x 9.94x 8.58x 19.31x 13.52x $1.85 $3.00

High $5,860.00 $5,880.00 1.25x 1.14x 12.94x 10.00x 21.61x 20.28x $5.40 $5.82

Low $368.53 $1,090.00 0.30x 0.30x 7.49x 7.08x 9.83x 6.34x -$4.97 $0.24

EV/Revenue EV/EBITDA P/E EPS

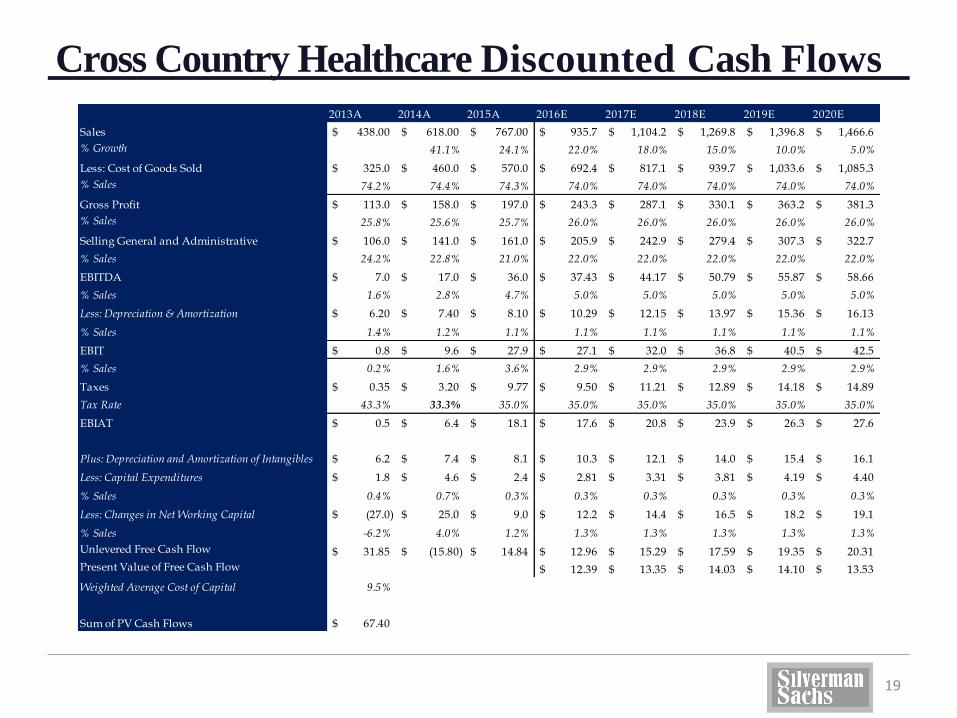

Cross Country Healthcare Discounted Cash Flows

2 0 1 3 A

19

2 0 1 4 A 2 0 1 5 A 2 0 1 6 E 2 0 1 7 E 2 0 1 8 E 2 0 1 9 E 2 0 2 0 E

2013A 2014A 2015A 2016E 2017E 2018E 2019E 2020E

Sales 438.00$ 618.00$ 767.00$ 935.7$ 1,104.2$ 1,269.8$ 1,396.8$ 1,466.6$

% Growth 41.1% 24.1% 22.0% 18.0% 15.0% 10.0% 5.0%

Less: Cost of Goods Sold 325.0$ 460.0$ 570.0$ 692.4$ 817.1$ 939.7$ 1,033.6$ 1,085.3$

% Sales 74.2% 74.4% 74.3% 74.0% 74.0% 74.0% 74.0% 74.0%

Gross Profit 113.0$ 158.0$ 197.0$ 243.3$ 287.1$ 330.1$ 363.2$ 381.3$

% Sales 25.8% 25.6% 25.7% 26.0% 26.0% 26.0% 26.0% 26.0%

Selling General and Administrative 106.0$ 141.0$ 161.0$ 205.9$ 242.9$ 279.4$ 307.3$ 322.7$

% Sales 24.2% 22.8% 21.0% 22.0% 22.0% 22.0% 22.0% 22.0%

EBITDA 7.0$ 17.0$ 36.0$ 37.43$ 44.17$ 50.79$ 55.87$ 58.66$

% Sales 1.6% 2.8% 4.7% 5.0% 5.0% 5.0% 5.0% 5.0%

Less: Depreciation & Amortization 6.20$ 7.40$ 8.10$ 10.29$ 12.15$ 13.97$ 15.36$ 16.13$

% Sales 1.4% 1.2% 1.1% 1.1% 1.1% 1.1% 1.1% 1.1%

EBIT 0.8$ 9.6$ 27.9$ 27.1$ 32.0$ 36.8$ 40.5$ 42.5$

% Sales 0.2% 1.6% 3.6% 2.9% 2.9% 2.9% 2.9% 2.9%

Taxes 0.35$ 3.20$ 9.77$ 9.50$ 11.21$ 12.89$ 14.18$ 14.89$

Tax Rate 43.3% 33.3% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0%

EBIAT 0.5$ 6.4$ 18.1$ 17.6$ 20.8$ 23.9$ 26.3$ 27.6$

Plus: Depreciation and Amortization of Intangibles 6.2$ 7.4$ 8.1$ 10.3$ 12.1$ 14.0$ 15.4$ 16.1$

Less: Capital Expenditures 1.8$ 4.6$ 2.4$ 2.81$ 3.31$ 3.81$ 4.19$ 4.40$

% Sales 0.4% 0.7% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3%

Less: Changes in Net Working Capital (27.0)$ 25.0$ 9.0$ 12.2$ 14.4$ 16.5$ 18.2$ 19.1$

% Sales -6.2% 4.0% 1.2% 1.3% 1.3% 1.3% 1.3% 1.3%

Unlevered Free Cash Flow 31.85$ (15.80)$ 14.84$ 12.96$ 15.29$ 17.59$ 19.35$ 20.31$

Present Value of Free Cash Flow 12.39$ 13.35$ 14.03$ 14.10$ 13.53$

Weighted Average Cost of Capital 9.5%

Sum of PV Cash Flows 67.40$

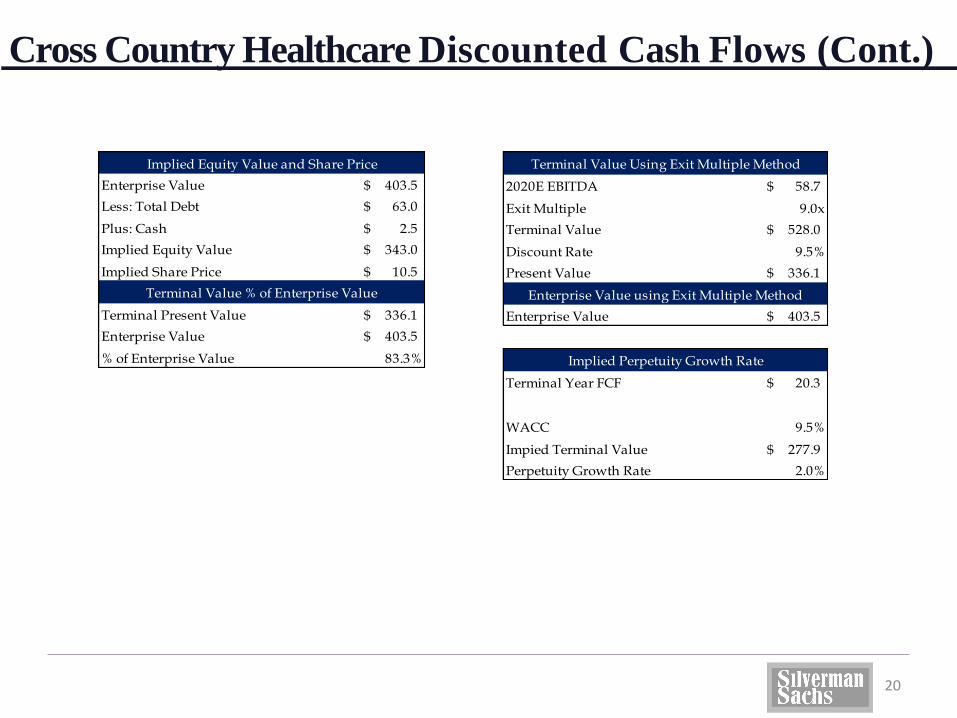

Cross Country Healthcare Discounted Cash Flows (Cont.)

20

Enterprise Value 403.5$

Less: Total Debt 63.0$

Plus: Cash 2.5$

Implied Equity Value 343.0$

Implied Share Price 10.5$

Terminal Present Value 336.1$

Enterprise Value 403.5$

% of Enterprise Value 83.3%

Terminal Value % of Enterprise Value

Implied Equity Value and Share Price

2020E EBITDA 58.7$

Exit Multiple 9.0x

Terminal Value 528.0$

Discount Rate 9.5%

Present Value 336.1$

Enterprise Value 403.5$

Terminal Value Using Exit Multiple Method

Enterprise Value using Exit Multiple Method

Terminal Year FCF 20.3$

WACC 9.5%

Impied Terminal Value 277.9$

Perpetuity Growth Rate 2.0%

Implied Perpetuity Growth Rate

Cross Country Healthcare Comparable Companies

Company Name Ticker Share Price Market Cap

Enterprise

Value LTM 2016E LTM 2016E LTM 2016E LTM 2016E

Team Health Holdings TMH $41.60 $3,060.00 $5,350.00 1.49x 1.15x 14.77x 10.65x 37.13x 14.45x $1.12 $2.87

Lifepoint Hospitals LPNT $68.78 $2,970.00 $5,420.00 1.00x 0.86x 8.10x 7.11x 17.42x 15.53x $3.95 $3.76

Robert Half International Inc. RHI $44.23 $5,860.00 $5,510.00 1.08x 1.14x 8.69x 8.33x 16.88x 15.29x $2.69 $3.00

On Assignment, Inc ASGN $35.98 $1,910.00 $2,580.00 1.25x 1.12x 12.94x 9.09x 19.53x 10.60x $1.85 $3.09

Cross Country Healthcare CCRN $11.23 $366.21 $394.99 0.52x 0.57x 20.87x 21.36x 36.09 18.32x -$0.31 $0.64

Mean $2,833.24 $3,851.00 1.07x 0.93x 13.07x 11.31x 25.41x 14.84x $1.86 $2.67

Median $2,970.00 $5,350.00 1.08x 1.00x 12.94x 9.09x 19.53x 15.29x $1.85 $3.00

High $5,860.00 $5,510.00 1.49x 1.15x 20.87x 21.36x 37.13x 18.32x $3.95 $3.76

Low $366.21 $394.99 0.52x 0.57x 8.10x 7.11x 16.88x 10.60x -$0.31 $0.64

EV/Revenue EV/EBITDA P/E EPS

21

Pro Forma Capital StructureSECTION VI

22

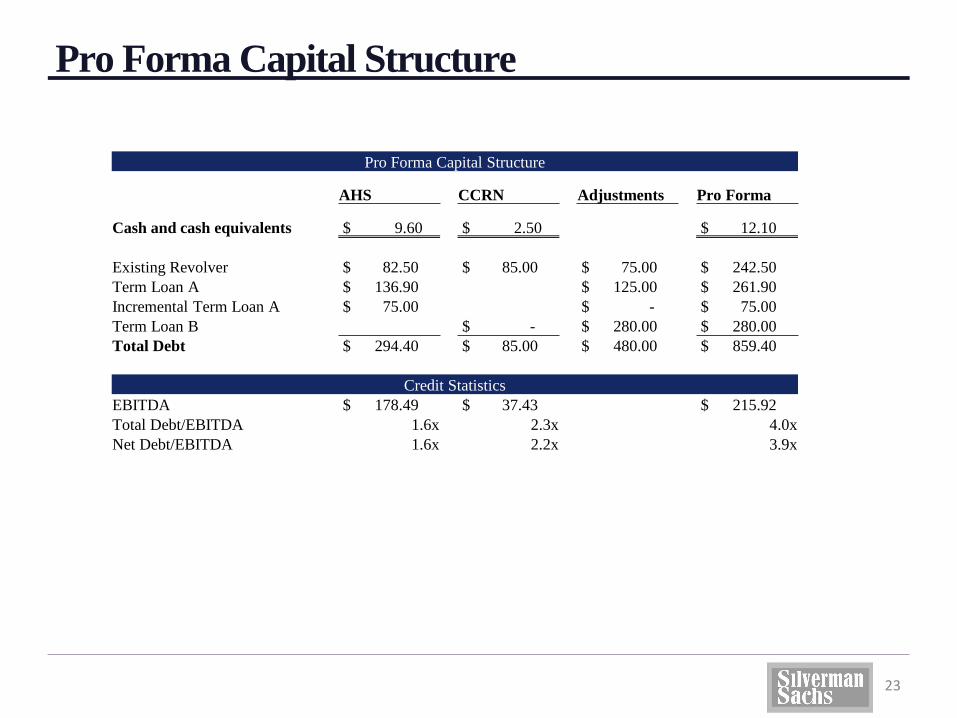

Pro Forma Capital Structure

23

Pro Forma Capital Structure

AHS CCRN Adjustments Pro Forma

Cash and cash equivalents $ 9.60 $ 2.50 $ 12.10

Existing Revolver $ 82.50 $ 85.00 $ 75.00 $ 242.50

Term Loan A $ 136.90 $ 125.00 $ 261.90

Incremental Term Loan A $ 75.00 $ - $ 75.00

Term Loan B $ - $ 280.00 $ 280.00

Total Debt $ 294.40 $ 85.00 $ 480.00 $ 859.40

Credit Statistics

EBITDA $ 178.49 $ 37.43 $ 215.92

Total Debt/EBITDA 1.6x 2.3x 4.0x

Net Debt/EBITDA 1.6x 2.2x 3.9x

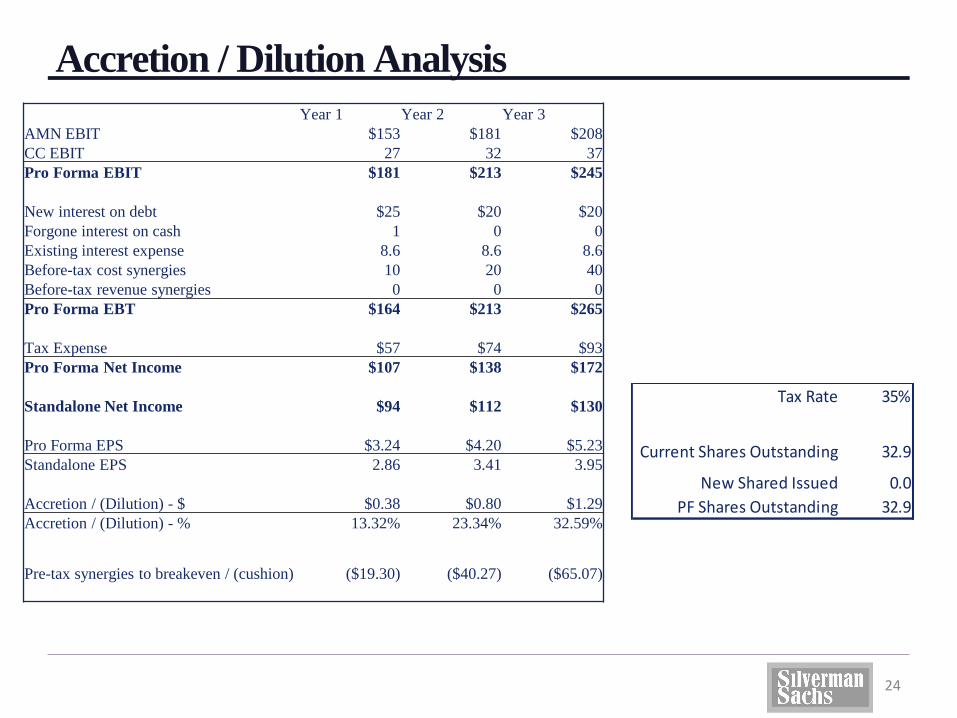

Accretion / Dilution Analysis

24

Year 1 Year 2 Year 3

AMN EBIT $153 $181 $208

CC EBIT 27 32 37

Pro Forma EBIT $181 $213 $245

New interest on debt $25 $20 $20

Forgone interest on cash 1 0 0

Existing interest expense 8.6 8.6 8.6

Before-tax cost synergies 10 20 40

Before-tax revenue synergies 0 0 0

Pro Forma EBT $164 $213 $265

Tax Expense $57 $74 $93

Pro Forma Net Income $107 $138 $172

Standalone Net Income $94 $112 $130

Pro Forma EPS $3.24 $4.20 $5.23

Standalone EPS 2.86 3.41 3.95

Accretion / (Dilution) - $ $0.38 $0.80 $1.29

Accretion / (Dilution) - % 13.32% 23.34% 32.59%

Pre-tax synergies to breakeven / (cushion) ($19.30) ($40.27) ($65.07)

Tax Rate 35%

Current Shares Outstanding 32.9

New Shared Issued 0.0

PF Shares Outstanding 32.9

AppendixSECTION VII

25

26

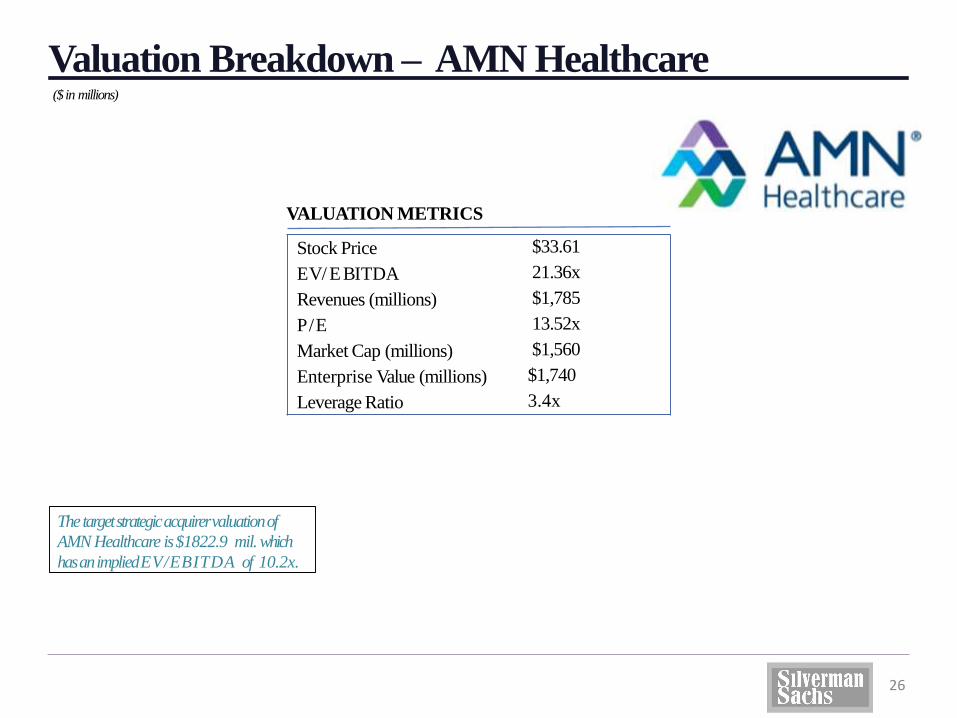

Valuation Breakdown – AMN Healthcare($ in millions)

The target strategic acquirer valuation of

AMN Healthcare is $1822.9 mil. which

has an implied EV/EBITDA of 10.2x.

Stock Price

EV/ EBITDA

Revenues (millions)

P/E

Market Cap (millions)

Enterprise Value (millions)

Leverage Ratio

$33.61

21.36x

$1,785

13.52x

$1,560

$1,740

3.4x

VALUATION METRICS

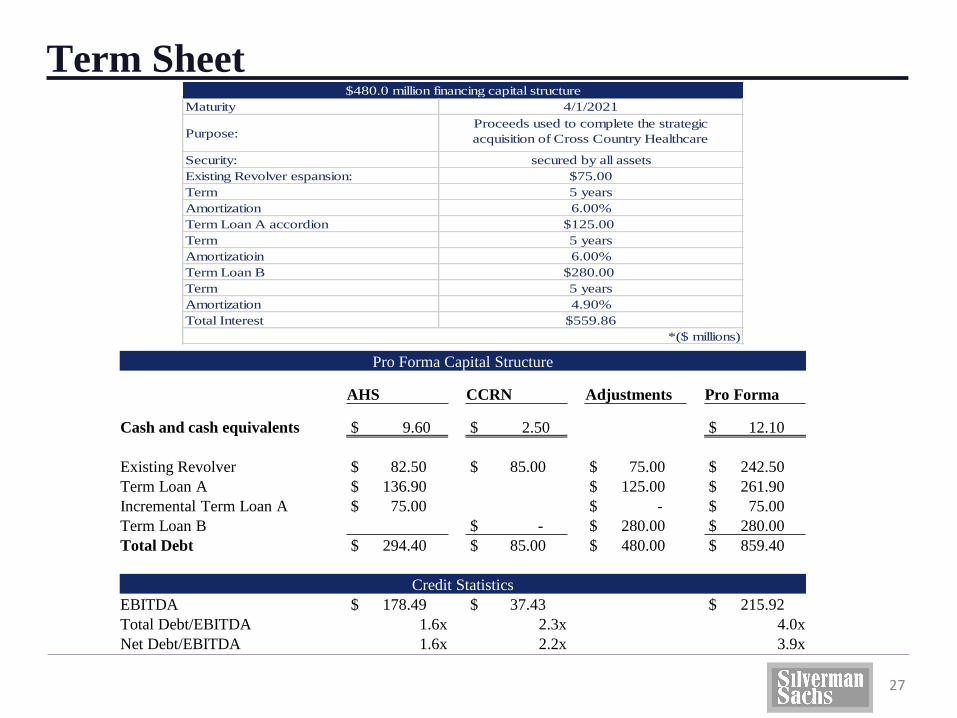

Term Sheet

27

Pro Forma Capital Structure

AHS CCRN Adjustments Pro Forma

Cash and cash equivalents $ 9.60 $ 2.50 $ 12.10

Existing Revolver $ 82.50 $ 85.00 $ 75.00 $ 242.50

Term Loan A $ 136.90 $ 125.00 $ 261.90

Incremental Term Loan A $ 75.00 $ - $ 75.00

Term Loan B $ - $ 280.00 $ 280.00

Total Debt $ 294.40 $ 85.00 $ 480.00 $ 859.40

Credit Statistics

EBITDA $ 178.49 $ 37.43 $ 215.92

Total Debt/EBITDA 1.6x 2.3x 4.0x

Net Debt/EBITDA 1.6x 2.2x 3.9x

Maturity

Purpose:

Security:

Existing Revolver espansion:

Term

Amortization

Term Loan A accordion

Term

Amortizatioin

Term Loan B

Term

Amortization

Total Interest

4.90%

$559.86

*($ millions)

6.00%

$125.00

5 years

6.00%

$280.00

5 years

Proceeds used to complete the strategic

acquisition of Cross Country Healthcare

$480.0 million financing capital structure

4/1/2021

secured by all assets

$75.00

5 years

Why Silverman Sachs

Previous Success

• 95% deal success rate

Quality

• Small deal team size contributes to a high level of quality and team synergy

Specialties

• Healthcare industry experts

• Specialize in mergers & acquisitions

28