22

Superior Value Creation Denver Gold Forum 2016 Neal Froneman Chief Executive Officer 19 September 2016

Superior Value

Creation

Denver Gold Forum 2016

Neal Froneman

Chief Executive Officer

19 September 2016

Disclaimer

The information in this presentation may include forward-looking statements, which are based on current expectations and

projections about future events. These statements may include, without limitation, any statements preceded by, followed by or

including words such as “target,” “expect,” “may,” “anticipate,” “estimate,” “will,” and other words and terms of similar

meaning or the negative thereof. These forward-looking statements, as well as those included in any other material discussed

at the meeting, are subject to risks, uncertainties and assumptions, including, among other things, the development of

Sibanye’s business, general economic conditions and actions of regulators. In light of these risks, uncertainties and

assumptions, the events in the forward-looking statements may not occur. No representation or warranty is made that any

forward-looking statement will come to pass and no reliance should be placed on any forward-looking statement. No one

undertakes to publicly update or revise any such forward-looking statement.

2

What differentiates Sibanye

• Significant free cash generation

• Industry leading returns to shareholders

• South African focussed

• Focused on delivering superior value to all stakeholders

3Uniquely positioned in industry

Corporate overview

4A FTSE/JSE Top 40 precious metals company

Shares in issueShares in ADR form

923 902 469189 073 910

Market cap R53.5bn (US$3.8bn)

Listings • JSE Limited share code: SGL • New York Stock Exchange ADR

programme share code: SBGL

Debt1 R5.3bn (US$478m) of R10.1bn term and revolving facility

Major Sibanye Gold shareholders*

Gold One Limited 20.07%

Public Investment Corporation 8,99%

Old Mutual Plc 4.91%

Van Eck Associates Corporation 4.73%

Contact details

Libanon Business Park

1 Hospital Road (off Cedar Avenue)

Libanon, Westonaria, 1779

South Africa

Neal Froneman

CEO

Tel: +27 11 278 9600

e-mail: [email protected]

James Wellsted

Investor Relations

Tel: +27 11 278 9600

e-mail: [email protected]

1 At 30 June 2016, except market cap at 5 September 2016

20%

24%

33%

5%

3%

2%

13%

China

South Africa

USA

Luxembourg

United Kingdom

Ireland

Others

* Source: J.P.Morgan Cazenove, July 2016

Shareholder geographic distribution*

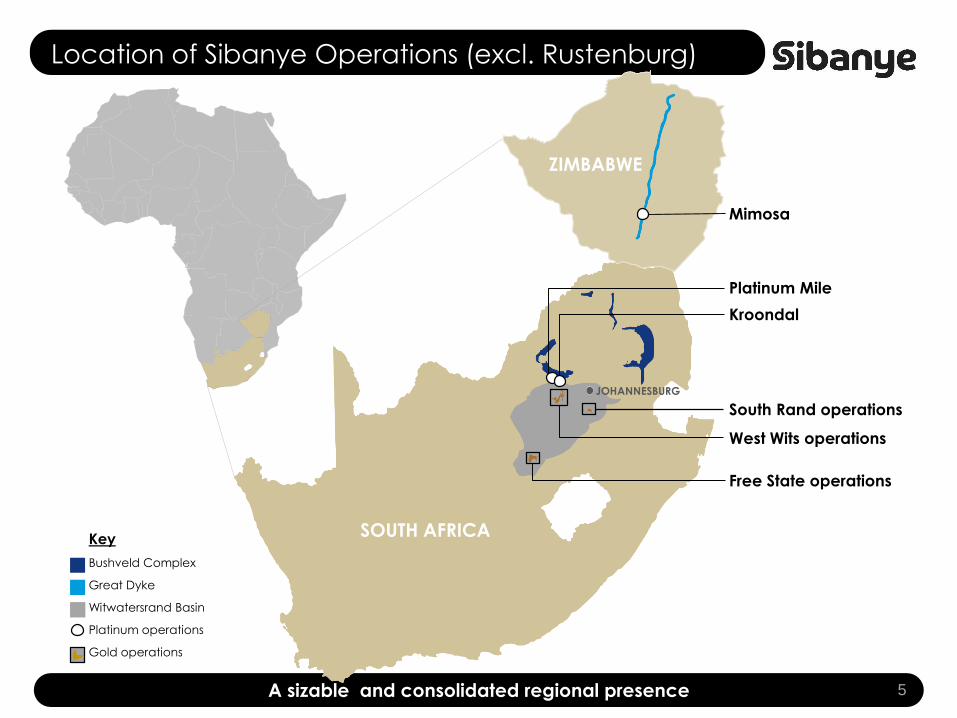

Location of Sibanye Operations (excl. Rustenburg)

5A sizable and consolidated regional presence

Mimosa

Platinum Mile

Kroondal

SOUTH AFRICA

ZIMBABWE

JOHANNESBURG

Free State operations

West Wits operations

South Rand operations

Key

Bushveld Complex

Great Dyke

Witwatersrand Basin

Platinum operations

Gold operations

Source: Bloomberg, Companies’ disclosures, Broker reports

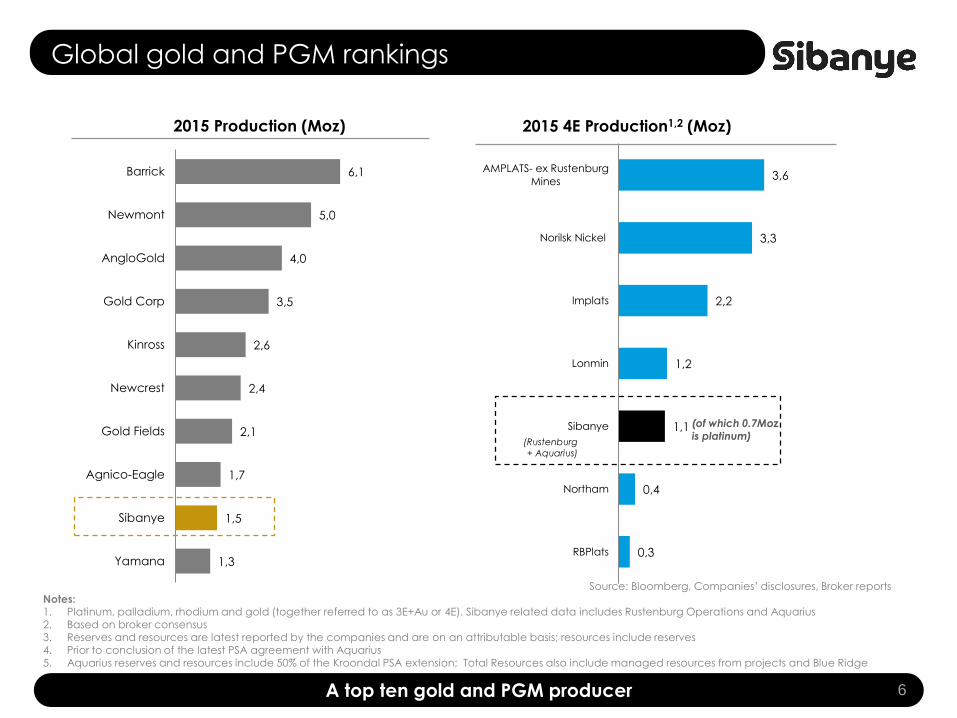

Notes:1. Platinum, palladium, rhodium and gold (together referred to as 3E+Au or 4E). Sibanye related data includes Rustenburg Operations and Aquarius2. Based on broker consensus3. Reserves and resources are latest reported by the companies and are on an attributable basis; resources include reserves4. Prior to conclusion of the latest PSA agreement with Aquarius5. Aquarius reserves and resources include 50% of the Kroondal PSA extension; Total Resources also include managed resources from projects and Blue Ridge

1,3

1,5

1,7

2,1

2,4

2,6

3,5

4,0

5,0

6,1

Yamana

Sibanye

Agnico-Eagle

Gold Fields

Newcrest

Kinross

Gold Corp

AngloGold

Newmont

Barrick

2015 Production (Moz)

Global gold and PGM rankings

6A top ten gold and PGM producer

0,3

0,4

1,1

1,2

2,2

3,3

3,6

RBPlats

Northam

Sibanye

Lonmin

Implats

Norilsk Nickel

AMPLATS- ex Rustenburg

Mines

(Rustenburg

+ Aquarius)

2015 4E Production1,2 (Moz)

(of which 0.7Mozis platinum)

H1 2016 results highlights*

• Gold production 5% higher to 23,229kg (746,800oz)

• AISC of R448,922/kg increased by 3% - below SA inflation (US$908/oz, 20%

lower)

• Record attributable PGM (4E) production of 92,773oz for the June quarter

• Operating profit 128% higher at R5.4bn (US$350m)

• H1 2016 interim dividend of R785m (US$53m) vs R919m(US$72m) total dividend

in 2015

*for the six months ended 30 June 2016 relative to six months ended 30 June 2015

Solid operational performance

23%

32%

36%

15%

20%

25%

30%

35%

40%

0

2 000

4 000

6 000

H1 2015 H2 2015 H1 2016

%

R m

illio

n

Sibanye operating profit and margin

Gold operating profit (Rm) Platinum operating profit (Rm) Group operating margin (%)

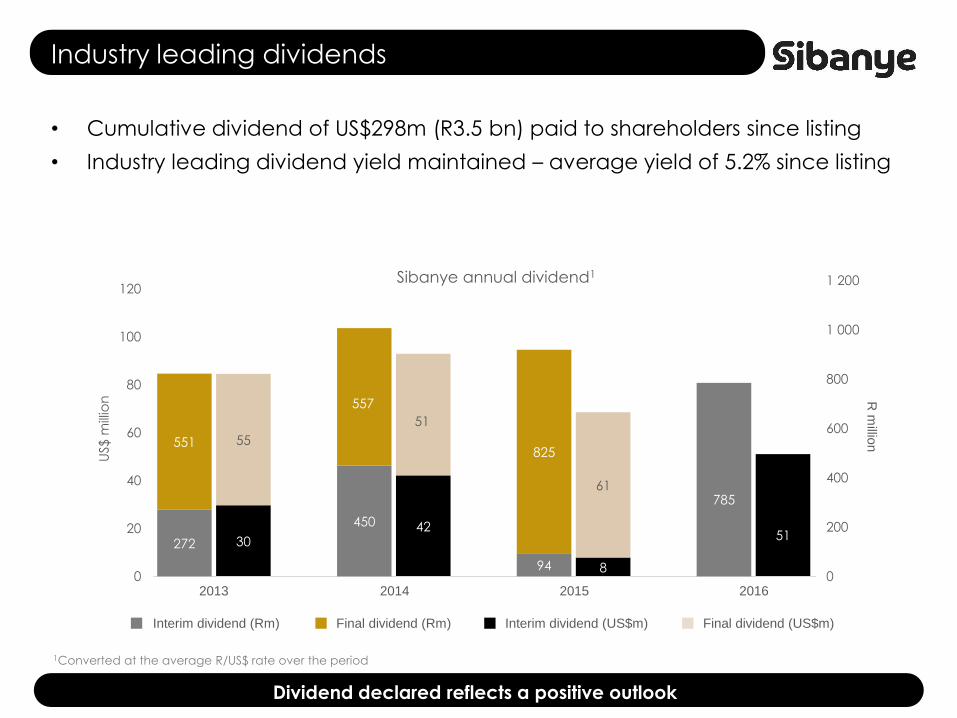

• Cumulative dividend of US$298m (R3.5 bn) paid to shareholders since listing

• Industry leading dividend yield maintained – average yield of 5.2% since listing

Industry leading dividends

Dividend declared reflects a positive outlook

1Converted at the average R/US$ rate over the period

3042

8

51

55

51

61

0

20

40

60

80

100

120

2013 2014 2015 2016

US$ m

illio

n

Sibanye annual dividend1

272

450

94

785

551

557

825

0

200

400

600

800

1 000

1 200

R m

illion

2013 2014 2015 2016

Interim dividend (Rm) Final dividend (Rm) Interim dividend (US$m) Final dividend (US$m)

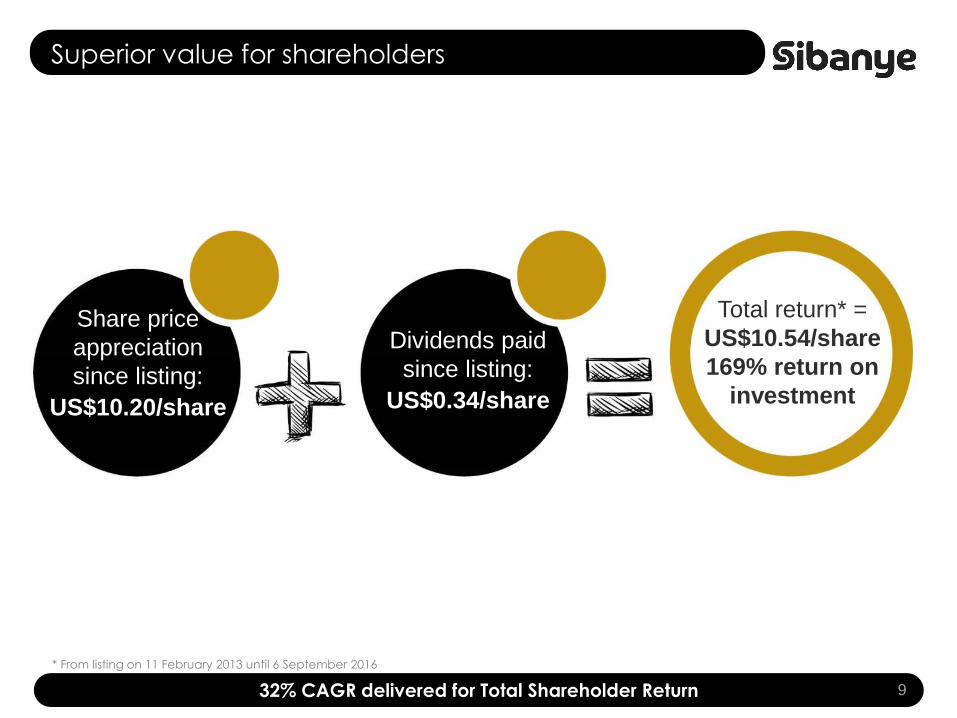

Superior value for shareholders

932% CAGR delivered for Total Shareholder Return

* From listing on 11 February 2013 until 6 September 2016

Share price

appreciation

since listing:

US$10.20/share

Dividends paid

since listing:

US$0.34/share

Total return* =

US$10.54/share

169% return on

investment

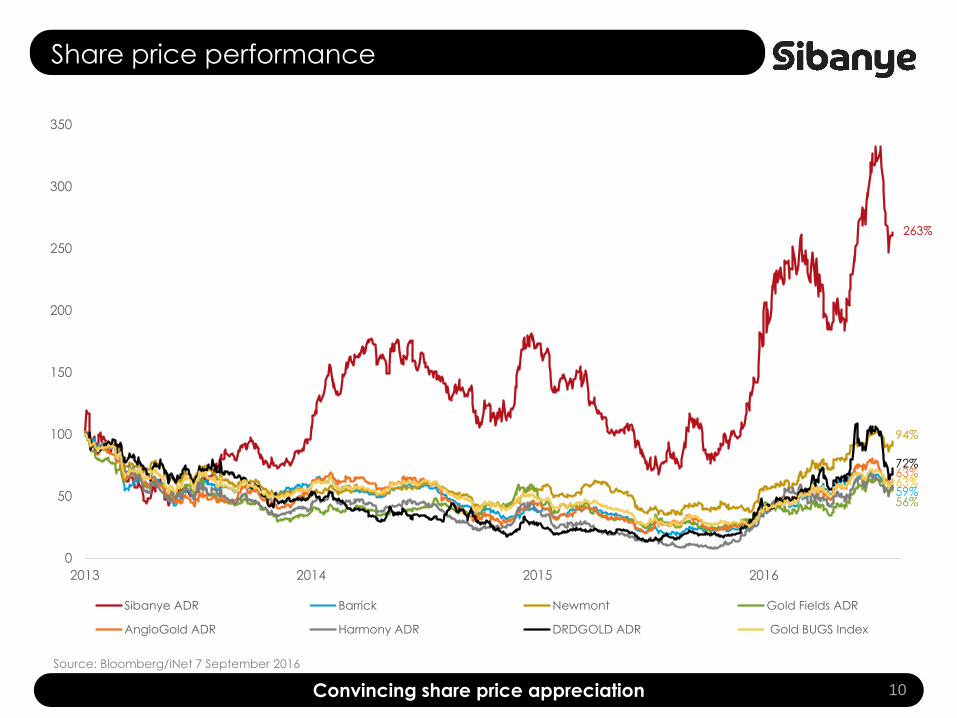

Share price performance

0

50

100

150

200

250

300

350

2013 2014 2015 2016

Sibanye ADR Barrick Newmont Gold Fields ADR

AngloGold ADR Harmony ADR DRDGOLD ADR Gold BUGS Index

10

Source: Bloomberg/iNet 7 September 2016

263%

94%

72%

63%63%

56%59%

Convincing share price appreciation

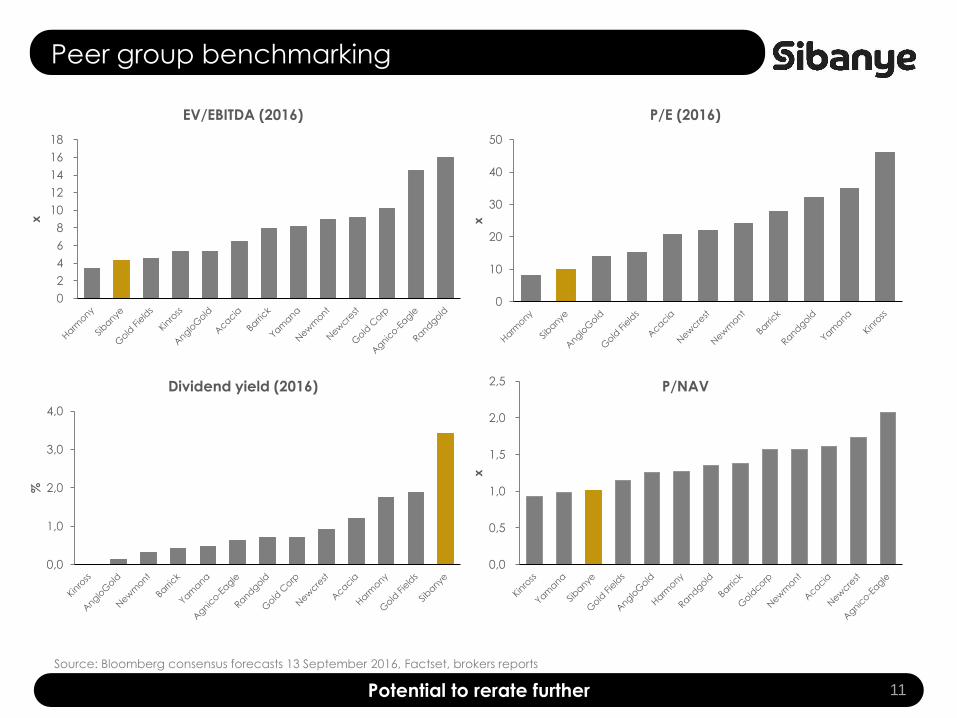

Peer group benchmarking

11Potential to rerate further

Source: Bloomberg consensus forecasts 13 September 2016, Factset, brokers reports

0,0

0,5

1,0

1,5

2,0

2,5

x

P/NAV

0

2

4

6

8

10

12

14

16

18

x

EV/EBITDA (2016)

0

10

20

30

40

50

x

P/E (2016)

0,0

1,0

2,0

3,0

4,0

%

Dividend yield (2016)

Value focus

• Continue to drive operational excellence on existing asset base

– a proven operating model

– robust cash flow

– strong balance sheet

• Investing in organic growth

– R3.6bn approved in mid 2015 (gold price R450,000/kg) for organic growth

projects

– Significant leverage at a R600,000/kg gold price:

• NPV of approximately R7bn

• IRRs between 20% and 30%

12Well-positioned to realise further value

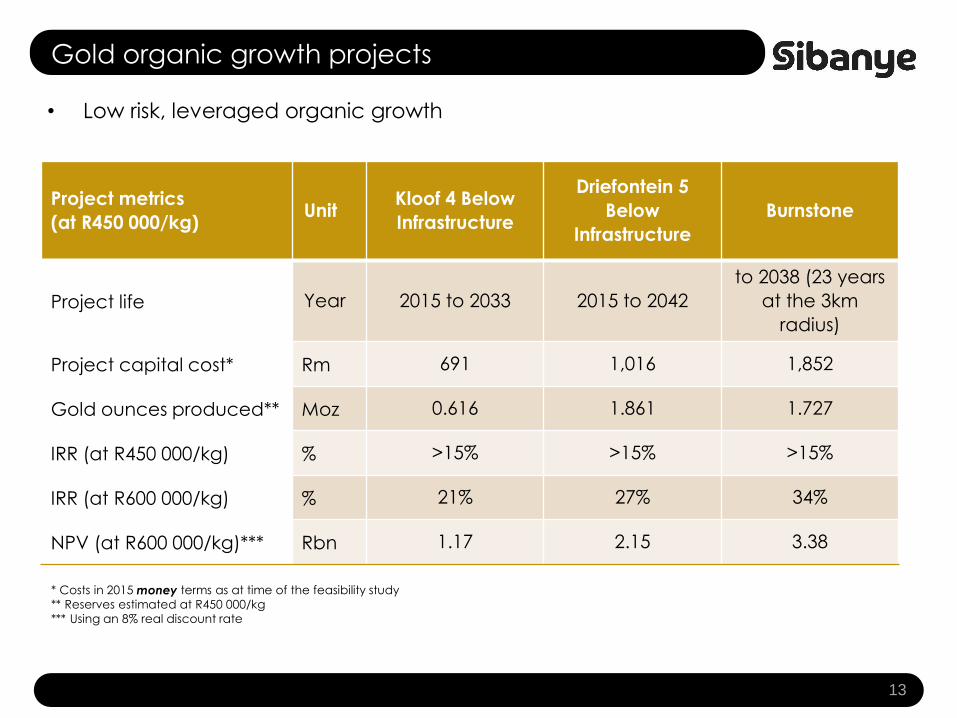

Gold organic growth projects

• Low risk, leveraged organic growth

13

Project metrics

(at R450 000/kg)Unit

Kloof 4 Below

Infrastructure

Driefontein 5

Below

Infrastructure

Burnstone

Project life Year 2015 to 2033 2015 to 2042

to 2038 (23 years

at the 3km

radius)

Project capital cost* Rm 691 1,016 1,852

Gold ounces produced** Moz 0.616 1.861 1.727

IRR (at R450 000/kg) % >15% >15% >15%

IRR (at R600 000/kg) % 21% 27% 34%

NPV (at R600 000/kg)*** Rbn 1.17 2.15 3.38

* Costs in 2015 money terms as at time of the feasibility study

** Reserves estimated at R450 000/kg

*** Using an 8% real discount rate

LoM reserve production profiles

14Extending the operating life

0

10 000

20 000

30 000

40 000

50 000

60 000

kg

Pre-feasibilities studies

undertaken

De Bron

Beisa

Pending capital approval

WRTRP

Projects in development

Burnstone

Below infrastructure projects

Kloof

Driefontein

Surface reserves in LoM

Kloof

Driefontein

Cooke

Beatrix

Underground reserves in LoM

Kloof

Driefontein

Cooke

Beatrix

Note: Project profile is based on pre-feasibility and feasibility studies as at December 2015

Based on Reserves declared as at 31 December 2015

Assumptions: Gold price: R430,000/kg, Uranium R1,455/lb (real 2015 terms)

Gold Fields plan

31,000kg (1Moz)

Precious metals strategy - Platinum a logical first step

• Many operational similarities with gold mining

• Long-term PGM supply and demand fundamentals remain robust

• Low PGM prices and escalating costs (labour, utilities) have put balance sheets

under strain

• Opportunity to leverage Sibanye’s successful operating model and hard rock,

tabular, labour intensive mining competency to realise further value

• Innovative approach to structuring transactions and projects

• The SA PGM sector offers a number of consolidation opportunities

15

Consolidation benefits

• Planning and ore body extraction optimised by breaking down farm boundaries

• Improved capacity utilisation and rationalisation of infrastructure

• Remove duplicated/unnecessary overhead structures and costs

• Rationalise replicated support services

• Optimise capital allocation

• Flexibility to close loss making production

• Enhance financial capacity

– Access to capital markets improved

– Cost of capital reduced

Consolidation is logical and necessary 16

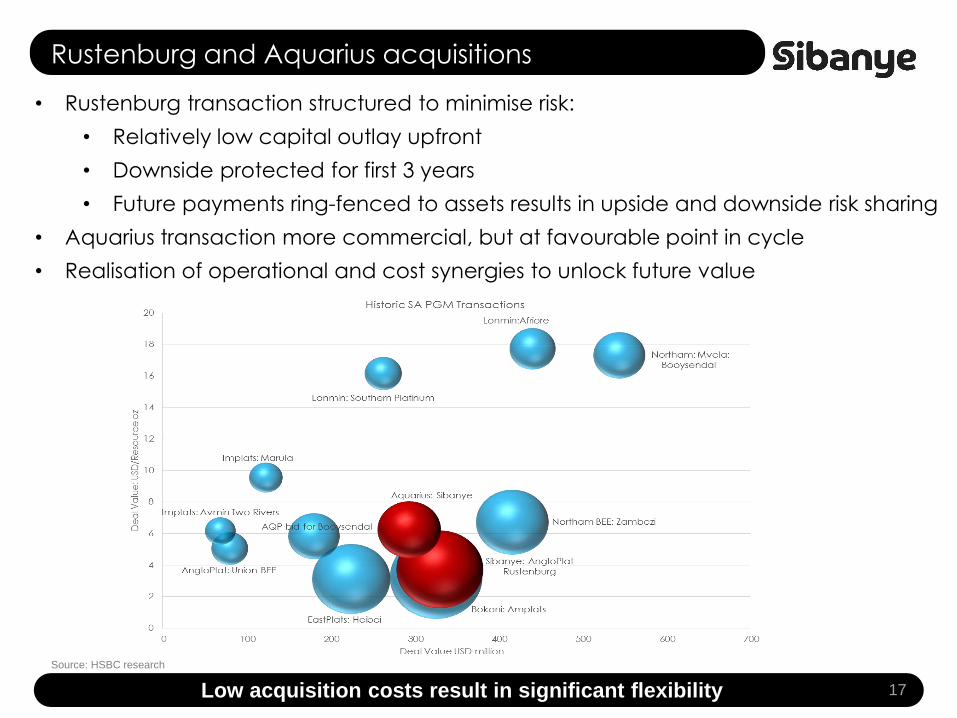

Rustenburg and Aquarius acquisitions

Low acquisition costs result in significant flexibility

Source: HSBC research

• Rustenburg transaction structured to minimise risk:

• Relatively low capital outlay upfront

• Downside protected for first 3 years

• Future payments ring-fenced to assets results in upside and downside risk sharing

• Aquarius transaction more commercial, but at favourable point in cycle

• Realisation of operational and cost synergies to unlock future value

17

Operating synergies

• Removal of mine boundaries results in

optimised mine plans and underground infrastructure

• Optimising plant utilisation and surface ore flow

Direct cost savings at operations

• Best practice operational

benchmarking

• Economies of scale benefits

Operating and separate synergies targeted

Driving value creation through realisation of regional and operating synergies 18

Shared services and central cost savings

• Bathopele/Kroondal shared services optimised

• Rustenburg and Kroondal training

• Regional, central and shared services

• Corporate overheads reduced

Turk #

(undeveloped)

School

of MinesRustenburg Operations

Care and maintenance

Aquarius

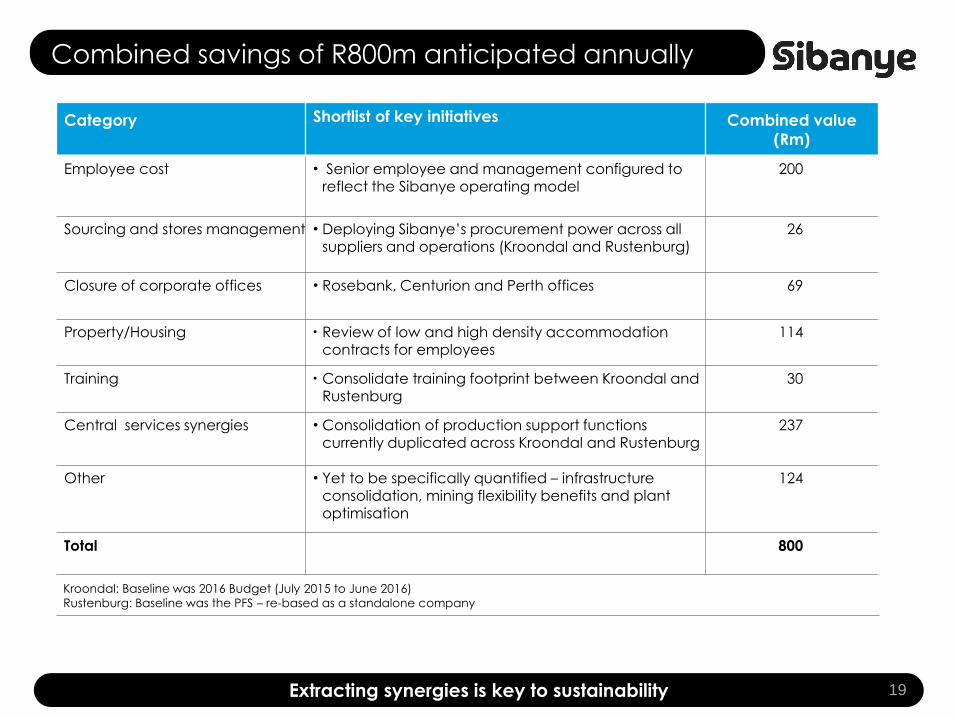

Combined savings of R800m anticipated annually

Extracting synergies is key to sustainability 19

Category Shortlist of key initiatives Combined value

(Rm)

Employee cost • Senior employee and management configured to reflect the Sibanye operating model

200

Sourcing and stores management • Deploying Sibanye’s procurement power across all suppliers and operations (Kroondal and Rustenburg)

26

Closure of corporate offices • Rosebank, Centurion and Perth offices 69

Property/Housing • Review of low and high density accommodation contracts for employees

114

Training • Consolidate training footprint between Kroondal and Rustenburg

30

Central services synergies • Consolidation of production support functions currently duplicated across Kroondal and Rustenburg

237

Other • Yet to be specifically quantified – infrastructure consolidation, mining flexibility benefits and plant optimisation

124

Total 800

Kroondal: Baseline was 2016 Budget (July 2015 to June 2016)

Rustenburg: Baseline was the PFS – re-based as a standalone company

F2016 outlook*

20A very solid outlook

Gold Division

• Gold production : 50 000 kg (1.6Moz)

• Total cash cost: R355 000/kg (US$760/oz)

• All-in sustaining cost: R425 000/kg

(US$910/oz)

• Capital expenditure: R3.9bn (US$270m)

* Assuming average exchange rate of R14:50/US$ for F2016

Platinum Division (excl. Rustenburg)

• PGM production: 260 000oz (4E)

• Average cash operating cost: R10 600/oz

(US$735/oz)

• Capital expenditure: R225m (US$15m)

• Rustenburg acquisition on track for

completion in Dec 2016 quarter

• A secure and prosperous future

Conclusion

• Sibanye is committed to creating superior value for ALL stakeholders

• Gold division is generating substantial cash flows

• Platinum acquisitions will realise significant value in the medium term

• Robust financial position and strong balance sheet at an opportune

point in the commodity cycle

• Industry-leading dividend yield investment thesis remains

the cornerstone building block

21A secure and prosperous future

Questions

![ORDER - justice.gov.za · Neutral citation: Black Sash Trust v Minister of Social Development and Others [2017] ZACC 8 Coram: Mogoeng CJ, Nkabinde ADCJ, Cameron J, Froneman J, Jafta](https://static.documents.pub/doc/80x56/5b6e2bb37f8b9a962a8dc83c/order-neutral-citation-black-sash-trust-v-minister-of-social-development.jpg)