43

Supplier Country and Partner Country Features © Professor Daniel F. Spulber

| Date post: | 14-Dec-2015 |

| Category: |

Documents |

| Upload: | annette-choyce |

| View: | 222 times |

| Download: | 1 times |

Supplier Country and Partner Country Features

© Professor Daniel F. Spulber

2

Japan’s domestic production and exports of cars– The turning point

VERs (early 80s -1995), High Yen (70s to 90s)

3

Toyota’s Activities in the US from 1957 till Today

4

Toyota’s Activities in the US in Numbers

5

Toyota’s Foreign Direct Investment in the US

6

Toyota’s Locations in the US

7

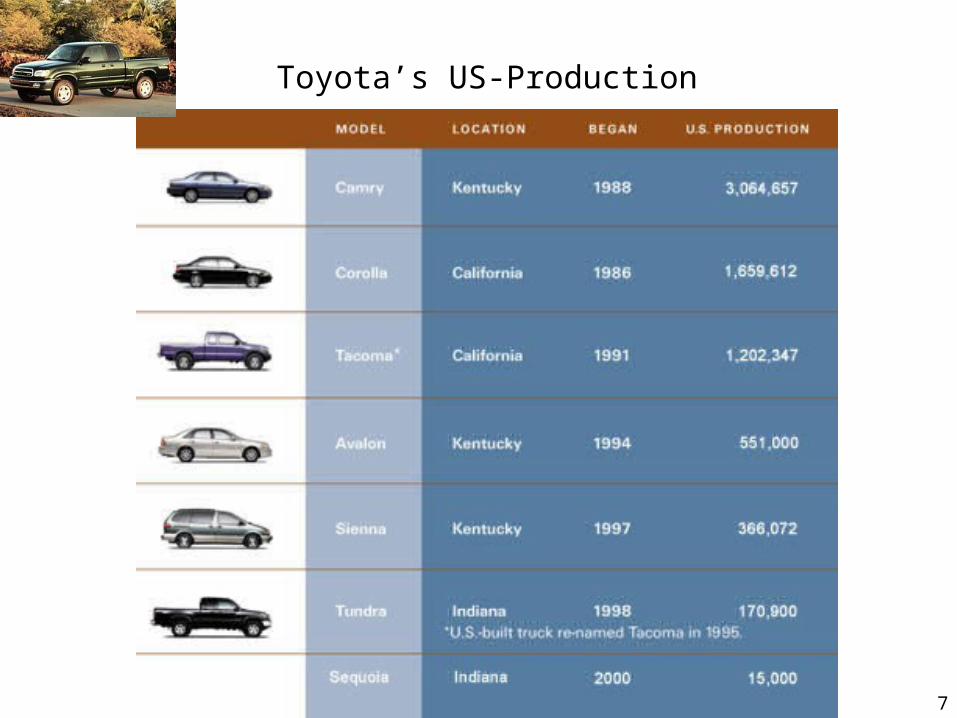

Toyota’s US-Production

8

Toyota

• 1980 11 production facilities in 9 countries

• 1990 20 production in 14 countries

• 2003 42 production facilities in 21 countries

• Production facilities in Asia, Africa, China, North America, and South America, and plans for Russia

• Plans to double overseas production to 6 million vehiclesWSJ, 11/2/04, p. A3

9

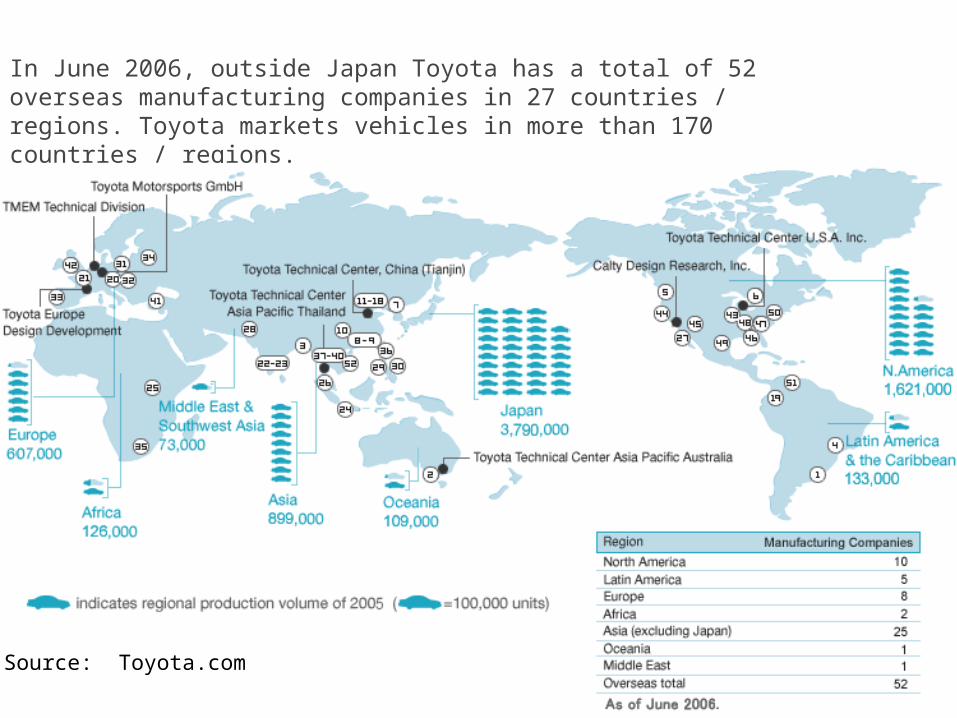

In June 2006, outside Japan Toyota has a total of 52 overseas manufacturing companies in 27 countries / regions. Toyota markets vehicles in more than 170 countries / regions.

Source: Toyota.com

10

Choose supplier countries for competitive advantage

• Worker wages and productivity • Technology • Finance capital• Factor supplies• Supplier industry• Political, legal, regulatory climate• Operating costs/risks

Supplier country features – Production and procurement

Why did Toyota choose to produce in the US in comparison to Japan or Mexico?

11

Supplier country features – Production and procurement

Choose supplier countries for competitive advantage

• Get close to customers

• Can produce and procure in or near customer countries to improve distribution

12

Choose partners for competitive advantage• Complementary products

Video game player and video games Andy Grove: “Complementors”

• Complementary technology

• Complementary capabilities

Partner country features – Demand-side and supply-side complements

13

Choose partner countries for competitive advantage

• Proximity to customer markets• Partners provide knowledge of customers• Partners provide access to human capital• Political, legal, regulatory climate

important for types of agreements• Contracts, JVs, formal and informal

alliances

Partner countries – Demand-side andsupply-side complements

14

Sony-Samsung JV: S-LCD Tang-Jeong, Korea

Seventh-generation technology plant: Capacity 90,000 panels/month

Eighth-generation LCD plant projected capacity 50,000 panels a month (2.2 x 2.5m) 2007Cost: $1.9 bn Each firm will invest half.

Complementary technologies

Television (Sony)Flat panel design

(Samsung)

15

TCS is India's largest IT outsourcing firm (majority partner) Microsoft – US JV to be based in Beijing, China

To provide IT outsourcing services and solutions to U.S., Europe, and the Asia Pacific region, and China.

Three Chinese firms are partners: Beijing Zhongguancun Software Park Development Co., Uniware Co., and Tianjin Huayuan Software Park Construction and Development Co.

The Chinese firms operate national software development parks in China.

Partner countriesJoint venture: Tata Consultancy Services (TCS) – Microsoft

16

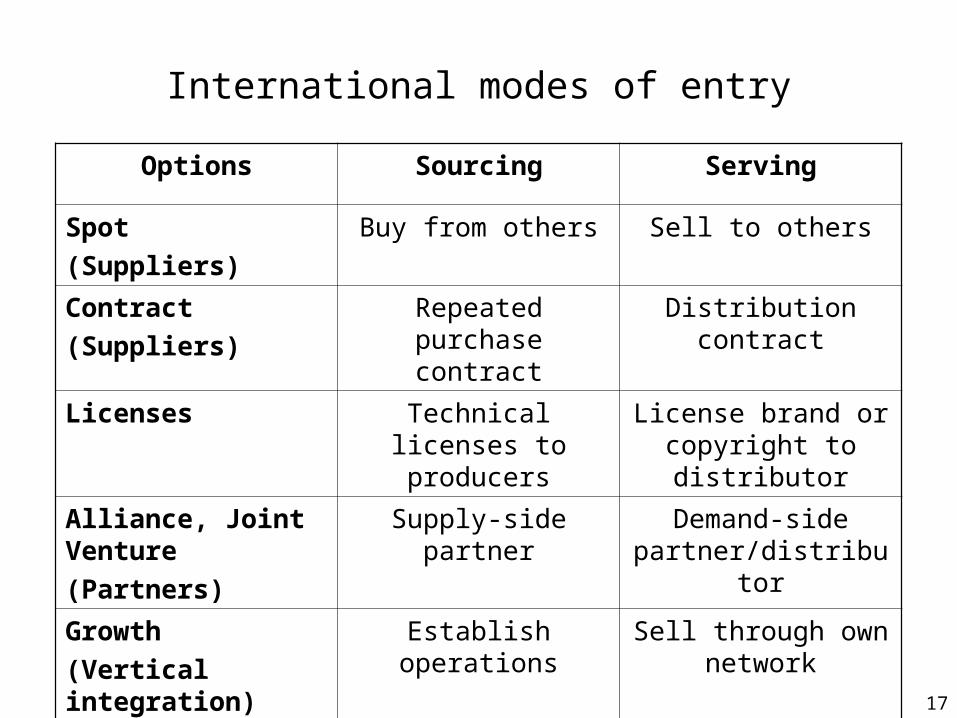

International modes of entry

• Modes of entry are alternatives ways to produce and purchase products in supplier countries

• Modes of entry are also ways to sell and distribute in a target customer country

• Ownership of facilities in multiple countries makes the business a multinational corporation (MNC)

• International businesses tend to be vertically integrated but this is likely to change

17

International modes of entry

Options Sourcing Serving

Spot(Suppliers)

Buy from others Sell to others

Contract(Suppliers)

Repeated purchase contract

Distribution contract

Licenses Technical licenses to producers

License brand or copyright to distributor

Alliance, Joint Venture(Partners)

Supply-side partner

Demand-side partner/distributor

Growth(Vertical integration)

Establish operations

Sell through own network

M&A(Vertical integration)

Merge with supplier

Merge with distributor.

18

MIX and MATCH

Modes of entry can differ:

• Across supplier and partner countries

• Across customer countries

• Between production and distribution sides

Example: GAP owns stores but outsources production

19

International modes of entry and strategy

Advantages of vertical integration:

Greater internal coordination across international operations

Avoiding market transaction costs

Internal technology transfer

Avoid double marginalization

20

International modes of entry and strategy

Disadvantages of vertical integration:

Operating costs/risks in supplier country

Less flexibility, greater organizational costs

Less market responsiveness

Lose benefits of focus on core competencies and outsourcing

21

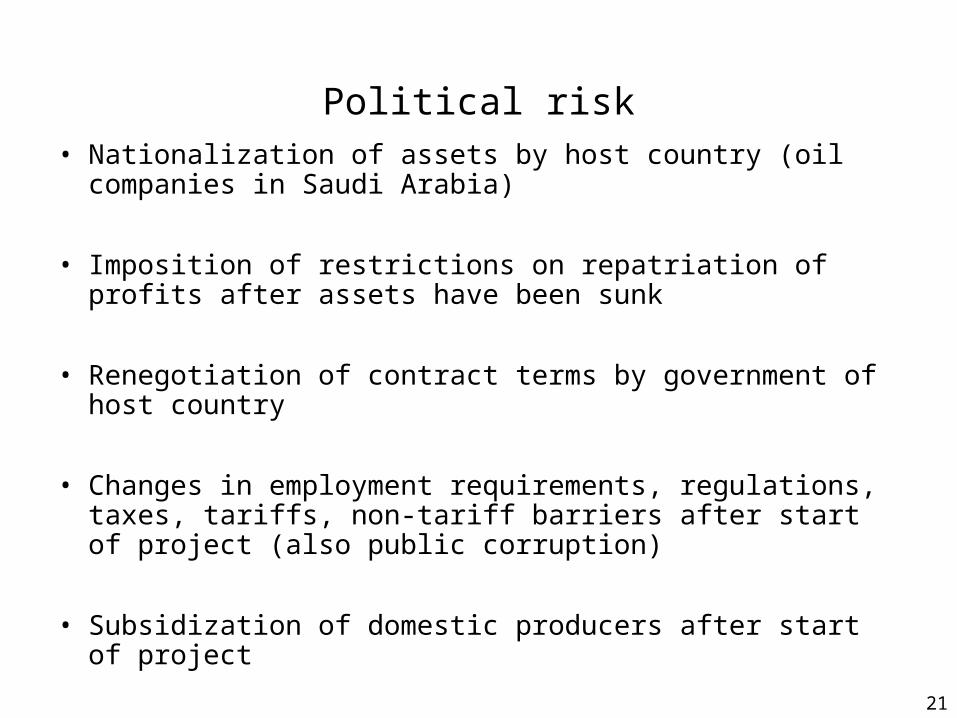

Political risk• Nationalization of assets by host country (oil companies in

Saudi Arabia)

• Imposition of restrictions on repatriation of profits after assets have been sunk

• Renegotiation of contract terms by government of host country

• Changes in employment requirements, regulations, taxes, tariffs, non-tariff barriers after start of project (also public corruption)

• Subsidization of domestic producers after start of project

22

Reducing political risk• Forecast potential changes in the policies of the host country –

include domestic politics of host country and international relations

• Understand objectives of host government – tax revenues, local control of investment, political control, employment, attracting investment, attracting technology

• Understand public policy limits on market power, employment practices, environmental activities

• Understand public policy differences toward international business operating abroad versus domestic business

23

Contract risk: Suppliers and partners• Renegotiation of contract terms by supplier or partner in the

host country

• Renegotiation of contracts by foreign suppliers and partners often protected by government policy, legal system, or absence of business reputation effects

• Local supplier or partner does not honor contract (low-quality production) or defaults on payments

• Supplier or partner acts after investments have been sunk – hold-up problem

24

Reducing Contract Risk

• Long-term relationships with repeated exchange increase incentives for local supplier or partner to perform

• Being part of a business network creates performance incentives for local supplier or partner

• Use of trusted intermediaries in forming and maintaining business relationship

• Evaluate legal and regulatory climate in host country

25

Trade-off between political and contract risks

• Entry without local supplier or partner avoids some contract risks by going it alone – but increases political risk

• Entry without local supplier or partner allows greater vertical integration and control

• Sharing business with local supplier or partner reduces capital at risk and gains allies but increases contract risk

• Sharing business with local supplier or partner reduces control and loses some benefits of vertical integration

26

Overview and Take-Away Points

• Manager should carefully consider features of supplier countries and partner countries in production and procurement decisions

• Adjust mode of entry depending on features of supplier countries and partner countries

• Mode of entry is critical for global competitive advantage

27

Case study

The global market for petroleum

Choosing supplier and partner countries

28

Gusher in Spindletop, Texas, 1902. Photo by Trost, courtesy of the Texas Energy Museum, Beaumont, Texas

Petroleum starts asa local phenomenon

29

Petroleum becomes a global market

30

Largest oil companies by production: Exxon Mobil (USA)British Petroleum Amoco (UK)Royal Dutch Shell (UK/Neth)Chevron Texaco (USA) Yukos (Russia)Total Fina Elf (France)Lukoil (Russia)ConocoPhillips (USA)Surgutneftegas (Russia)ENI (Italy)

31

International oil markets

• Total proved reserves

1.025 trillion bbl (1 January 2002)

• Total production

75.34 million bbl/day (2001 est.)

Note: 1,025,000/75 = 13,666 days = 37 years

• Oil and gas together supply 60% of world energy needs (API, 2004)

• US imports over 56% of its petroleum consumption

World of Petroleum by C.D. Masters, D.H. Root, and R.M. Turner, World map of petroleum basins showing estimated quantities of conventional crude oil future

resources in six different categories. Future quantities include identified reserves plus undiscovered resources.

Recoverable Crude Oil Futures (in billions of barrels)

0.1 0.1 to 1 1 to 10 10 to 20 20 to 100 > 100

Eckert VI Projection U. S. Geological Survey, C. Masters & R. M. Turner 1994

33

34

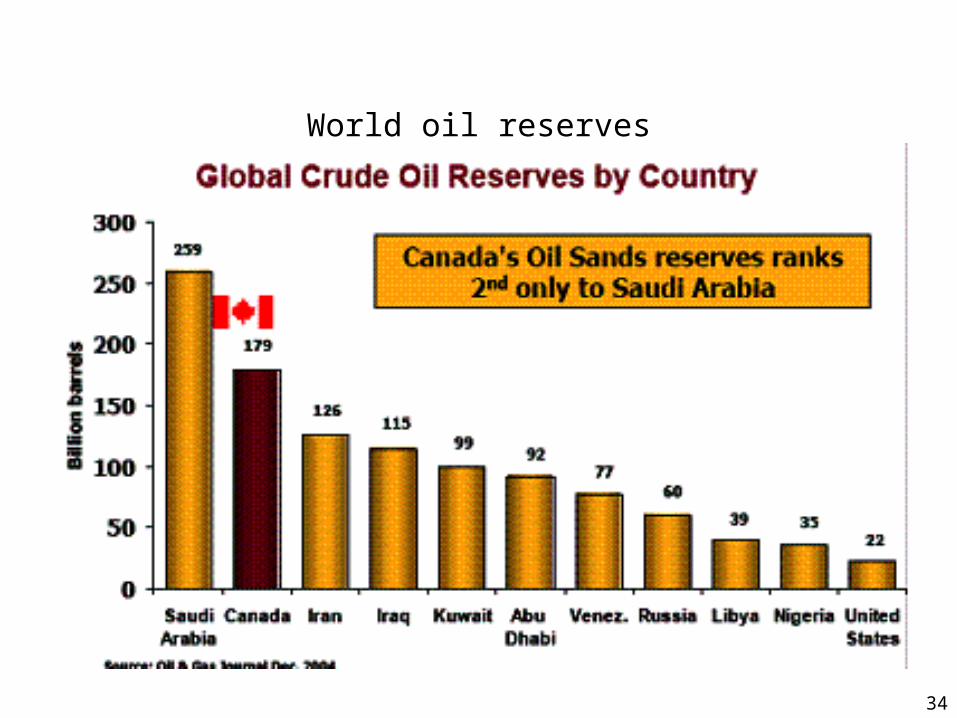

World oil reserves

35

Extraction costs

• In 1897 the first offshore oil well was drilled at the end of a wharf, 300 feet out into the ocean in Summerland , CA .

• Using floating platforms, wells have been drilled in 10,000 deep water

• Increasing depth as prices of oil risehttp://www.eia.doe.gov/kids/energyfacts/sources/non-renewable/offshore.html

36

World oil reserves

0

5

10

15

20

25

Cost of extraction

$/per barrel

CRUDE OIL DEEP OIL HEAVY OIL

Type of oil supply

37

Oil has political dimensions that can increase costs

38

Source: American Petroleum Institute Prices adjusted for inflation (2006 = 100).

39

Source: American Petroleum Institute. Prices adjusted for inflation (2006 = 100).

40

OPEC

• Eleven countries: Algeria, Indonesia, Iran, Iraq, Kuwait, Libya, Nigeria, Qatar, Saudi Arabia, the United Arab Emirates and Venezuela

• Supplies about 40 per cent of the world's oil output

• Has more than three-quarters of the world's total proven crude oil reserves.

41

42

43

What the future holds

• Sustained higher crude prices eventually• Greater aggregate demand due to

economic growth• More discoveries and more new reserves

as crude prices increase• Long-term usage of petroleum• Greater efficiency due to higher prices• Many new energy alternatives and

technologies coming on line