14

Expomin 2018 Supply Chain Seminar, April 24 Daniel Torreblanca

Expomin 2018Supply Chain Seminar, April 24

Daniel Torreblanca

Who we are?

Our products in society

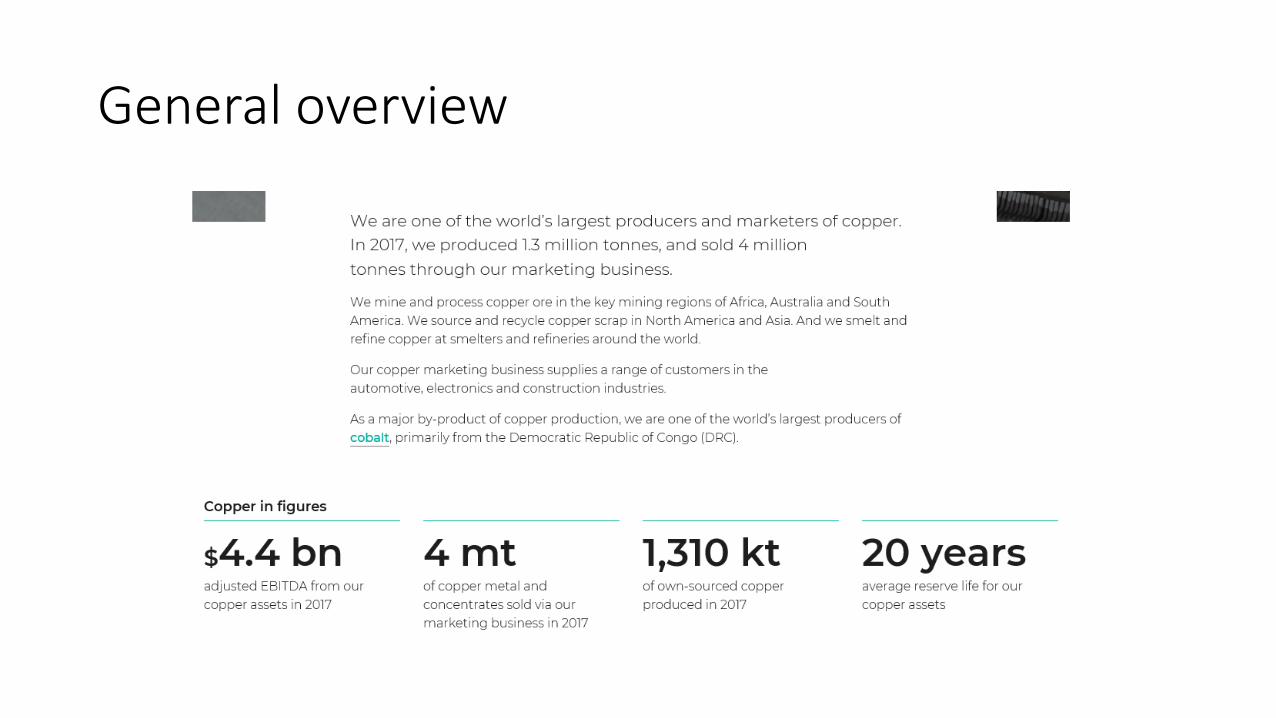

3

172,695

8,694

2,172

177,351

10,268

3,930

Revenue Adjusted EBITDA Adjusted EBIT

Glencore at a glance

• Glencore is one of the world’s largest global diversified natural resources companies and a major producer and marketer of more than 90 commodities. The Group’s operations comprise around 150 mining and metallurgical sites, oil production assets and agricultural facilities.

• With a strong footprint in both established and emerging regions for natural resources, Glencore’s industrial and marketing activities are supported by a global network of more than 90 offices located in over 50 countries.

• Glencore’s customers are industrial consumers, such as those in the automotive, steel, power generation, oil and food processing sectors. We also provide financing, logistics and other services to producers and consumers of commodities. Glencore’s companies employ around 143,000 people, including contractors.

• Glencore is proud to be member of the Voluntary Principles on Security and Human Rights and the International Council on Mining and Metals. We are active participant in the Extractive Industries transparency Initiative.

4

Key facts and figures

Key competitive strengths

• Scale and commodity diversity

• Unique business model, fully-integrated along the supply chain

• Ability to respond to changing industry dynamics

• Core competence in commodity marketing, logistics, risk management and financing

• Leading industrial asset portfolio of diversified operations with strong growth prospects

• Diversified position across multiple commodities, suppliers and customers

• World-class management team, entrepreneurial culture and track record of value creation

Key financials

($M)

Metals and minerals Energy products Agriculture

• Copper

• Zinc/Lead

• Aluminium

• Ferroalloys

• Nickel

• Iron Ore

• Coal

• Oil

Grains

Oils/Oilseeds

Sugar

Cotton

2015 2016

Glencore at a glance

5

Key facts and figures

Key competitive strengths

• Scale and commodity diversity

• Unique business model, fully-integrated along the supply chain

• Ability to respond to changing industry dynamics

• Core competence in commodity marketing, logistics, risk management and financing

• Leading industrial asset portfolio of diversified operations with strong growth prospects

• Diversified position across multiple commodities, suppliers and customers

• World-class management team, entrepreneurial culture and track record of value creation

Metals and minerals Energy products Agriculture

• Copper

• Zinc/Lead

• Aluminium

• Ferroalloys

• Nickel

• Iron Ore

• Coal

• Oil

Grains

Oils/Oilseeds

Sugar

Cotton

Exploration

Mining / producing

Processing / refining

Logistics

Marketing & trading

Traditionalminers Traders

Exploration

Mining / producing

Processing / refining

Logistics

Marketing & trading

• Quick response to market conditions. Cu Price cycle obligated us to react being focused in our cash flow, investment studied in deep, working capital revision permanently.

Where we operate

6

General overview

Cu Operations in South America

• Peru:• Antapaccay,

Guillermo Freire

• Antamina (JV - 33.75%)Enrique Alania

• Argentina:• La Alumbrera

Pablo Dramis

• El PachonRaul Mentz

Cu Operations in South America

• Chile:Lomas Bayas (II Region)

Manuel Alcaino

Altonorte (Smelter, II Region) Alvaro Baeza

Minera Altos de Punitaqui (IV region)Omar Carmi

Collahuasi (I region, JV – 44%)Roberto Quijada/Alvaro Alarcon

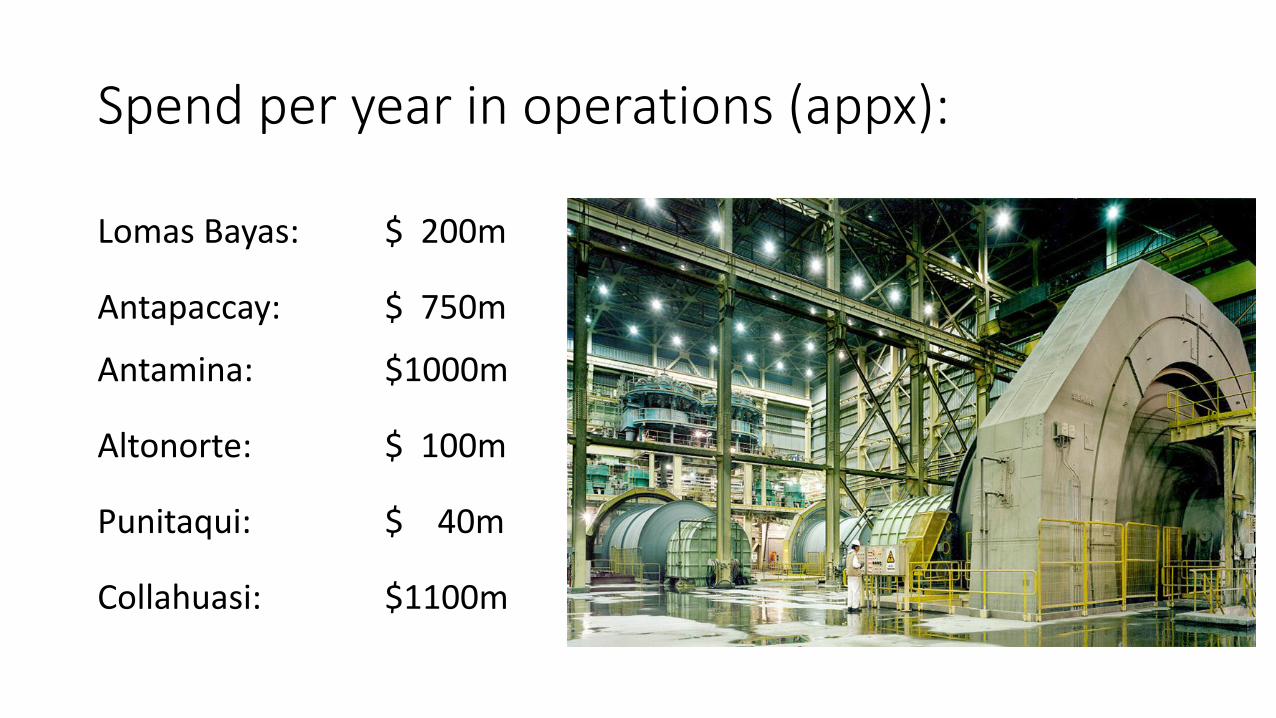

Spend per year in operations (appx):

Lomas Bayas: $ 200m

Antapaccay: $ 750m

Antamina: $1000m

Altonorte: $ 100m

Punitaqui: $ 40m

Collahuasi: $1100m

Projects, innovation and development• No approved major expansion projects in SA – Cu Operations

• El Pachon – under review.• Coroccohuayco – under review.• Alumbrera UG – under review.

• Low CAPEX projects:• New warehouse at Lomas Bayas• New bays for truck shop at Lomas Bayas• Clean and control yards at Antapaccay• Developing Emerging Markets opportunities• Bar codes/RFDI for warehouses

• We invite suppliers to present solutions that have an impact on reducing our costs• Test for most relevant proposals• Willing to share benefits• Solutions can be exported to other regions (Africa and Australia)

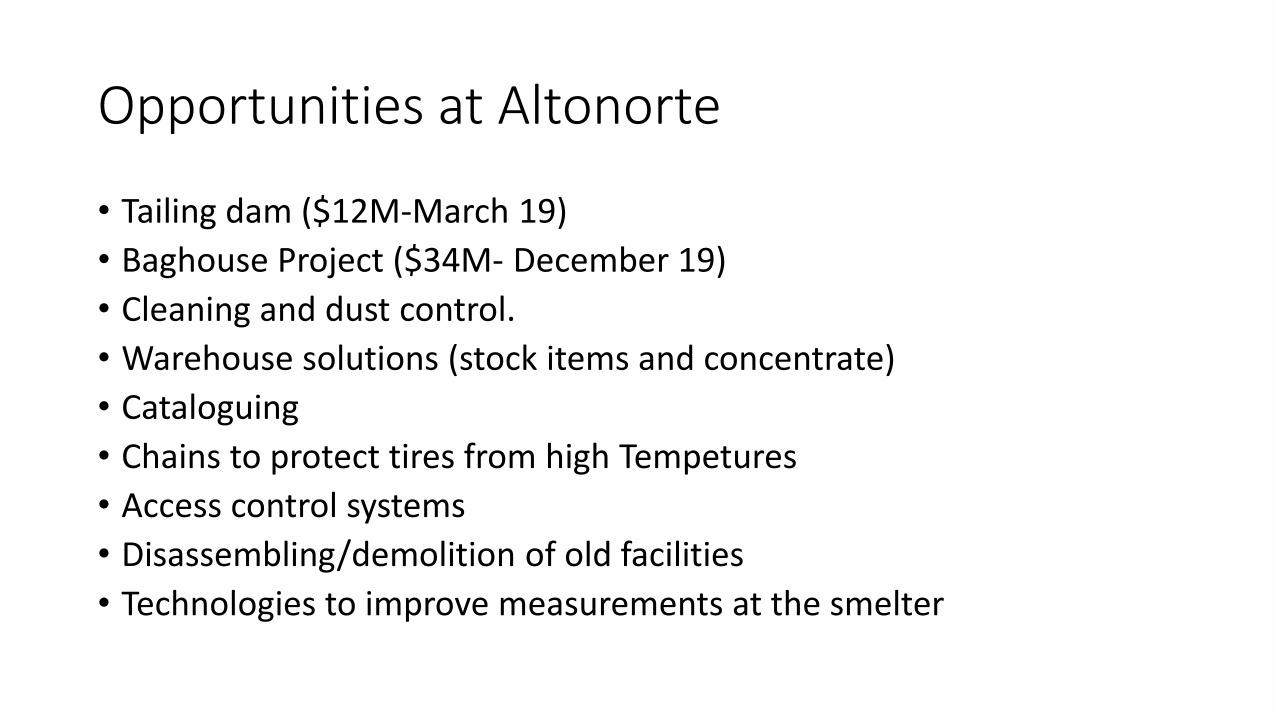

Opportunities at Altonorte

• Tailing dam ($12M-March 19)

• Baghouse Project ($34M- December 19)

• Cleaning and dust control.

• Warehouse solutions (stock items and concentrate)

• Cataloguing

• Chains to protect tires from high Tempetures

• Access control systems

• Disassembling/demolition of old facilities

• Technologies to improve measurements at the smelter

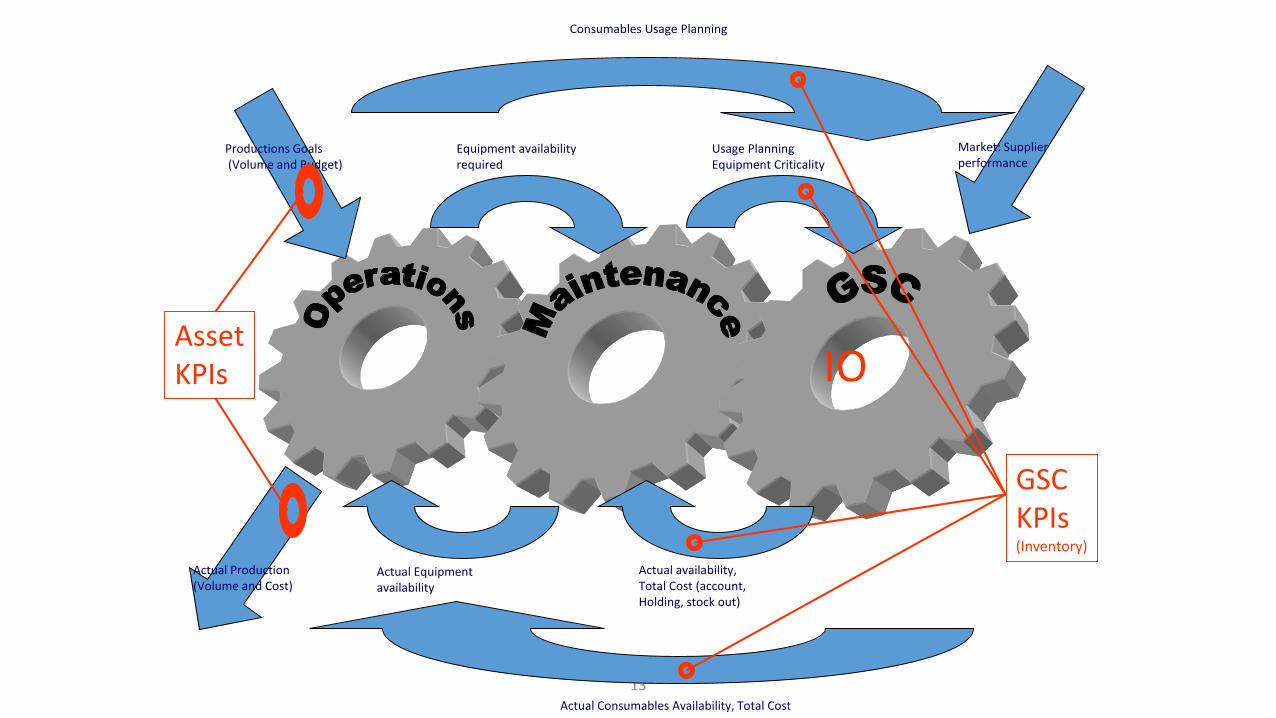

13

Productions Goals (Volume and Budget)

Equipment availabilityrequired

Usage PlanningEquipment Criticality

Market: Supplier performance

Actual availability,Total Cost (account, Holding, stock out)

Actual Equipment availability

Actual Production(Volume and Cost)

AssetKPIs IO

Consumables Usage Planning

Actual Consumables Availability, Total Cost

GSCKPIs (Inventory)