EASTERN PENNSYLVANIA SOUTHERN NEW JERSEY DELAWARE Supply Reboot > The regional vacancy rate remained at 7.9 percent during the last half of 2015. > Continued grocery chain volatility impacted neighborhood and community centers throughout the region > Asking rents for top-tier centers increased, but overall rents were flat. > The inflow of new landlords has resulted in increased capital investment toward upgrading existing centers to meet evolving retailer and consumer trends. The last two quarters of 2015 were marked by an active take and give supply climate. The bankruptcy of the Great Atlantic and Pacific supermarket chain added to the surplus of vacant grocery anchors. Twenty-three Pathmark and Super Fresh stores in Pennsylvania were closed. However, Acme Markets is in the process of taking over fourteen of these locations. Multiple large scale redevelopments were moving forward. The eastern portion of the Gallery reboot in Philadelphia was underway. January 2016 demolition is scheduled for the Granite Run Mall. Boscov’s and Sears will remain open as the center is redeveloped into The Promenade at Granite Run. Demolition and redevelopment at Chesterbrook Village has started. PREIT will be demolishing the Kmart at Exton Square Mall and leasing 55,000 square feet to Whole Foods. Asking rents for new centers topped $45.00 per square foot. However, rent growth overall was dragged down by the persistent anchor vacancies. Arrows compare current period to the previous period and forecast the next period. 2015 Year End | Retail Regional Overview MARKET INDICATORS Relative to prior period PA/NJ/DE Q2 2015 PA/NJ/DE Q2 2016* VACANCY CONSTRUCTION RENTAL RATES *Projected ASKING RENTAL RATES BY CENTER TYPE Average Asking Rents Asking rents for Community, Neighborhood COMMUNITY $14.00-$29.00 and Lifestyle Centers are for the typical quoted rent NEIGHBORHOOD $12.00-$28.00 per-square-foot, triple net, and for in-line spaces. For $13.00-$22.00 Power Centers, asking POWER rents are for anchor or junior anchor positions, LIFESTYLE $25.00-$45.00 10,000 SF to 40,000 SF. RETAIL VACANCY BY CENTER TYPE 0% 5% 10% 15% Community Neighborhood Lifestyle Power 4Q 14 2Q 15 4Q 15 Research & Forecast Report

Transcript

EASTERN PENNSYLVANIA SOUTHERN NEW JERSEY DELAWARE

Supply Reboot

> The regional vacancy rate remained at 7.9 percent during the last half of 2015.

> Continued grocery chain volatility impacted neighborhood and community centers throughout the region

> Asking rents for top-tier centers increased, but overall rents were flat.

> The inflow of new landlords has resulted in increased capital investment toward upgrading existing centers to meet evolving retailer and consumer trends.

The last two quarters of 2015 were marked by an active take and give supply climate. The bankruptcy of the Great Atlantic and Pacific supermarket chain added to the surplus of vacant grocery anchors. Twenty-three Pathmark and Super Fresh stores in Pennsylvania were closed. However, Acme Markets is in the process of taking over fourteen of these locations.

Multiple large scale redevelopments were moving forward. The eastern portion of the Gallery reboot in Philadelphia was underway. January 2016 demolition is scheduled for the Granite Run Mall. Boscov’s and Sears will remain open as the center is redeveloped into The Promenade at Granite Run. Demolition and redevelopment at Chesterbrook Village has started. PREIT will be demolishing the Kmart at Exton Square Mall and leasing 55,000 square feet to Whole Foods.

Asking rents for new centers topped $45.00 per square foot. However, rent growth overall was dragged down by the persistent anchor vacancies.

Arrows compare current period to the previous period and forecast the next period.

2015 Year End | Retail

Regional Overview

MARKET INDICATORSRelative to prior period

PA/NJ/DEQ2 2015

PA/NJ/DEQ2 2016*

VACANCY

CONSTRUCTION

RENTAL RATES

*Projected

ASKING RENTAL RATES BY CENTER TYPE

Average Asking Rents Asking rents for

Community, Neighborhood

COMMUNITY $14.00-$29.00 and Lifestyle Centers are for the typical quoted rent

NEIGHBORHOOD $12.00-$28.00 per-square-foot, triple net, and for in-line spaces. For

$13.00-$22.00 Power Centers, asking POWER rents are for anchor or

junior anchor positions, LIFESTYLE $25.00-$45.00 10,000 SF to 40,000 SF.

RETAIL VACANCY BY CENTER TYPE

0%

5%

10%

15%

Community Neighborhood Lifestyle Power

4Q 14

2Q 15

4Q 15

Research & Forecast Report

2 Research & Forecast Report | 2015 Year End | Pennsylvania, New Jersey, Delaware | Colliers International

SALES ACTIVITY

PROPERTY ADDRESS LOCATION BUYER SIZE SF PRICE / SF TYPE

East Gate Square Burlington County M&J Wilkow 746,535 $252 Community Center

Voorhees Town Center Camden County Mason Asset Management 307,000 $44 Regional Mall

Penrose Plaza Shopping Center Philadelphia County Onyx Properties, etal 263,000 $95 Community Center

Southmont Plaza Lehigh Valley DDR-Blackstone 253,943 $211 Power Center

Kenhorst Plaza Berks County Paum Sales Corp. 161,449 $152 Community Center

Springfield Park Delaware County National Realty Corporation 141,141 $286 Community Center

Shops at Cedar Point Lehigh Valley DDR-Blackstone 132,395 n/a Neighborhood Center

Paulsboro Plaza Gloucester County AVPM 95,180 $13 Community Center

Mullica Hill Plaza Gloucester County Carlyle Funding 86842 $292 Neighborhood Center

Anville East Center Lebanon County PinnacleHealth 80,000 $55 Neighborhood Center

Stonybrook Shopping Center York County SJC Property Management 63,955 $57 Neighborhood Center

Powder Mill Square New Castle County Pettinaro Management 63,777 $368 Community Center

520 S. 29th Street Dauphin Cuonty AMERCO Real Estate Company 63,000 $29 Neighborhood Center

Regional Overview (continued)Acme significantly expanded its footprint in the region, filling multiple former A&P locations. Regionally-based discount retailers, supermarkets and organic-oriented stores filled vacant grocery anchor spots. Wegmans continues to expand regionally.

Landlords are more actively changing the tenant mix to provide more foot traffic by courting entertainment options like “dinner and a movie” concepts, fitness/recreation operators, as well as community service providers such as medical centers.

Private investors, particularly equity funds chasing yields, were the most active buyers in the region. PREIT continued to spinoff non-core centers including the Voorhees Town Center and the Palmer Park Mall, which was under agreement. Pettinaro Management acquired a portfolio of retail and office properties in northern Delaware from Stoltz Real Estate Partners, including Power Mill Square. There were additional major shopping centers in the Lehigh Valley under contract.

Sale prices for well-leased centers were solidly over $250 per square foot while value-add properties traded for under $100 per square foot.

Recent Transactions in Q3 and Q4 2015

LEASE ACTIVITY

PROPERTY ADDRESS LOCATION TENANT SIZE SF

Fairgrounds Square Mall Berks County Limerick Furniture 151,630

Coventry Mall Chester County Limerick Furniture 121,455

The Crossings at Conestoga Creek Lancaster County Wegmans 120,000

Lawrence Park Shopping Center Delaware County Main Line Health Center 71,932

Airport Shopping Center New Castle County Acme Markets 68,152

Cottman & Bustleton Center Philadelphia County Acme Markets 66,703

Crossroads Plaza Bucks County Acme Markets 55,537

Exton Square Mall Chester County Whole Foods 55,000

College Square New Castle County Acme Markets 55,000

Eden Square Shopping Center New Castle County Gabe's 55,000

Larkins Corner Delaware County Acme Markets 54,257

Kirkwood Plaza New Castle County Acme Markets 52,936

Warrington Crossing Bucks County Gander Mountain 52,700

Shops At Schmidts Philadelphia County Acme Markets 50,049

3901 Lancaster Pike New Castle County 7Day Farmers Market 48,662

Market Square At Chestnut Hill Philadelphia County Acme Markets 48,210

Audubon Village Shopping Center Montgomery County Keller’s Market 45,963

Colonial Commons Dauphin County HomeGoods 31,436

Carlisle Commons Carlisle Tractor Supply 30,173

Branmar Plaza New Castle County Acme Markets 30,780

Rodin Square Philadelphia County Target 55,000

3 Research & Forecast Report | 2015 Year End | Pennsylvania, New Jersey, Delaware | Colliers International

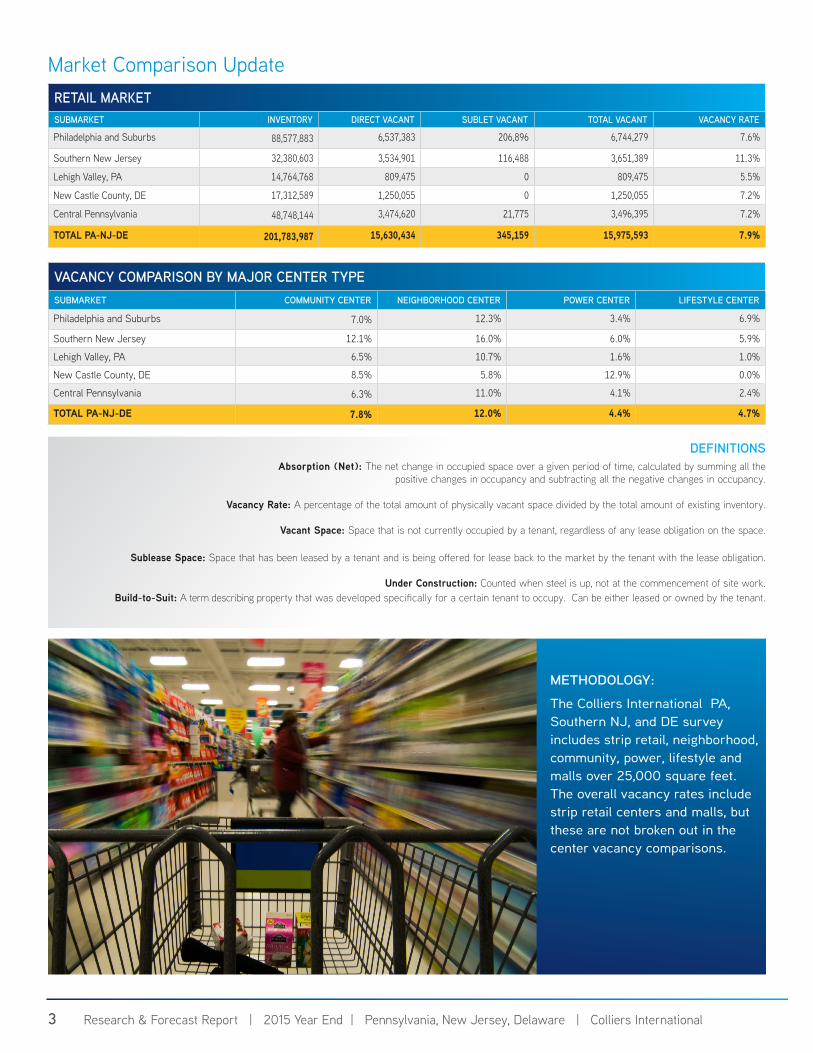

Market Comparison UpdateRETAIL MARKETSUBMARKET INVENTORY DIRECT VACANT SUBLET VACANT TOTAL VACANT VACANCY RATE

Philadelphia and Suburbs 88,577,883 6,537,383 206,896 6,744,279 7.6%

Southern New Jersey 32,380,603 3,534,901 116,488 3,651,389 11.3%

Lehigh Valley, PA 14,764,768 809,475 0 809,475 5.5%

New Castle County, DE 17,312,589 1,250,055 0 1,250,055 7.2%

Central Pennsylvania 48,748,144 3,474,620 21,775 3,496,395 7.2%

TOTAL PA-NJ-DE 201,783,987 15,630,434 345,159 15,975,593 7.9%

VACANCY COMPARISON BY MAJOR CENTER TYPESUBMARKET COMMUNITY CENTER NEIGHBORHOOD CENTER POWER CENTER LIFESTYLE CENTER

Philadelphia and Suburbs 7.0% 12.3% 3.4% 6.9%

Southern New Jersey 12.1% 16.0% 6.0% 5.9%

Lehigh Valley, PA 6.5% 10.7% 1.6% 1.0%

New Castle County, DE 8.5% 5.8% 12.9% 0.0%

Central Pennsylvania 6.3% 11.0% 4.1% 2.4%

TOTAL PA-NJ-DE 7.8% 12.0% 4.4% 4.7%

METHODOLOGY:

The Colliers International PA, Southern NJ, and DE survey includes strip retail, neighborhood, community, power, lifestyle and malls over 25,000 square feet. The overall vacancy rates include strip retail centers and malls, but these are not broken out in the center vacancy comparisons.

DEFINITIONSAbsorption (Net): The net change in occupied space over a given period of time, calculated by summing all the

positive changes in occupancy and subtracting all the negative changes in occupancy.

Vacancy Rate: A percentage of the total amount of physically vacant space divided by the total amount of existing inventory.

Vacant Space: Space that is not currently occupied by a tenant, regardless of any lease obligation on the space.

Sublease Space: Space that has been leased by a tenant and is being offered for lease back to the market by the tenant with the lease obligation.

Under Construction: Counted when steel is up, not at the commencement of site work.Build-to-Suit: A term describing property that was developed specifically for a certain tenant to occupy. Can be either leased or owned by the tenant.

4North American Research & Forecast Report | Q4 201c | Office Market Outlook | Colliers International

Colliers International Ten Penn Center1801 Market Street, Suite 550 Philadelphia, Pennsylvania, 19103+1 215 925 4600colliers.com/philadelphia

UNITED STATES:

Colliers International | Philadelphia

Philadelphia, PA (headquarters) TEL +1 215 925 4600

Allentown, PA TEL +1 610 770 3600

Conshohocken, PA TEL +1 610 684 1850

Harrisburg, PA TEL +1 717 730 3752

Wilmington, DE TEL +1 302 425 4000

Mount Laurel, NJ TEL +1 856 234 9300

peco wind pow

er

pro

duced using

FOUNDING GLOBAL PARTNER

WORLD GREEN BUILDING COUNCIL

Submarket ReviewsPhiladelphia County The vacancy in Philadelphia County increased from 7.3 percent to 8.5 percent during the last two quarters of 2015. SuperFresh and Pathmark store closings were added to Bottom Dollar vacancies from earlier in 2015.

The Gallery is currently out of the active inventory as PREIT and Macerich have commenced on the two year redevelopment project into the Fashion Outlets of Philadelphia.

The expansion of the retail footprint and strong retailer demand in Center City shows no signs of slowing.

Suburban Pennsylvania The overall vacancy rate for the four suburban counties increased from 7.3 to 7.6 percent. Delaware and Montgomery counties had a vacancy decrease, but Bucks and Chester had increased vacancy.

In addition to the major redevelopments, ground-up centers are under construction in Brookhaven, Newtown Square, Warrington and Doylestown. The next phase of King of Prussia Town Center is underway and additional stores at Brandywine Mills will join the newly opened Wegman’s. An 85,000-square-foot Cobb Theater & Cinebistro is being added to Uptown Worthington and a new Gander Mountain is being built at Warrington Crossing.

Southern New Jersey The overall vacancy rate in the three counties decreased from 11.6 percent to 11.3 percent. Burlington and Gloucester County’s vacancy decreased, but Camden County’s vacancy was flat. Camden County’s vacancy may be increasing further in 2016 as one of the two anchor department stores at Voorhees Town Center is rumored to be closing.

The Gloucester Premium Outlets opened in the third quarter. Two long-delayed redevelopment projects are moving forward. The Shoppes and Residences at Renaissance Square will be constructed on the site of the Tri-Town Plaza in early 2016. Site work has commenced on the overhaul of Paulsboro Plaza.

New Castle County, DE New Castle County’s vacancy dipped from 7.4 to 7.2 percent during the last two quarters of 2015. The first phase of the Christiana Fashion Center opened, bringing new retailers to Delaware such as Nordstrom Rack, REI, Container Store and Saks Off 5th.

The next 105,000-square-foot phase is under construction.

The new owners of the Newark Shopping Center recently completed a $10.0 million renovation to the center. Additional retail space is planned in Newark at the former Avon site.

Lehigh Valley, PA The Lehigh Valley vacancy rate trended upward over the last four quarters, mainly due to supermarket closings. Most recently, Redner’s Warehouse Markets shut the 47,900-square-foot store in Trexlertown.

However, demand has been strong at the Valley’s new shopping centers. The 570,000-square-foot Hamilton Crossings is close to being fully leased well in advance of the center’s 2Q 2016 opening. Leasing has been strong at the Madison Farms development, where ShopRite opened in the third quarter. The Westgate Mall is undergoing a major renovation, and has attracted new tenants like SkyZone trampoline park.

Central Pennsylvania The overall vacancy rate in the Central PA counties decreased from 7.6 to 7.4 percent. York and Franklin counties registered vacancy increases due to the closing of two JCPenney stores, but the other counties had improved vacancy rates.

The retail landscape continued to evolve with the expansion of existing centers and ground-up developments in the planning stages. The Kmart Shopping Center in Mechanicsburg is slated for an expansion and revamp with 40,000 square feet of retail space and facade renovations. High Real Estate Group plans to commence construction on the Wegmans’ anchored Crossings at Conestoga Creek in Lancaster County in 2016. PinnacleHealth is moving ahead with its plans to redevelop the Annville East Shopping Center into a medical complex. Other retail projects in Silver Springs, Mount Joy, and Springettsbury Townships are meeting with community opposition.

![[Conference] Building Websites that Matter - Agent Reboot Boston, Agent Reboot DC, Agent Reboot Austin](https://static.documents.pub/doc/80x56/558a27d9d8b42a98578b465c/conference-building-websites-that-matter-agent-reboot-boston-agent-reboot-dc-agent-reboot-austin.jpg)