4

The Meaning and Scope of the Acte Clair Doctrine in the ECJ’s Direct Tax Case Law Cécile Brokelind - Lund University Department of Business Law School of Economics and Management

| Date post: | 30-Dec-2015 |

| Category: |

Documents |

| Upload: | leroy-kane |

| View: | 32 times |

| Download: | 2 times |

The Meaning and Scope of the Acte Clair Doctrine in the ECJ’s

Direct Tax Case Law

Cécile Brokelind - Lund University

Department of Business Law

School of Economics and Management

2

L U N D U N I V E R S I T Y

SWEDISH CASES

• Free movement of capital

• Difficulties with the leave to appeal procedure

• Clear reliance on the Bachmann defense and the Futura Territoriality

Principle in cases not referred

Too few cases? 52 preliminary rulings sent as of 1995 in total (Finland 38, Austria 261)

8 preliminary rulings in income tax law (1995-2007)

6 from Supreme Administrative Court (5 from SRN) one pending 2 from lower courts

Cases referred Types of cases referred

3

L U N D U N I V E R S I T Y

SWEDISH CASES

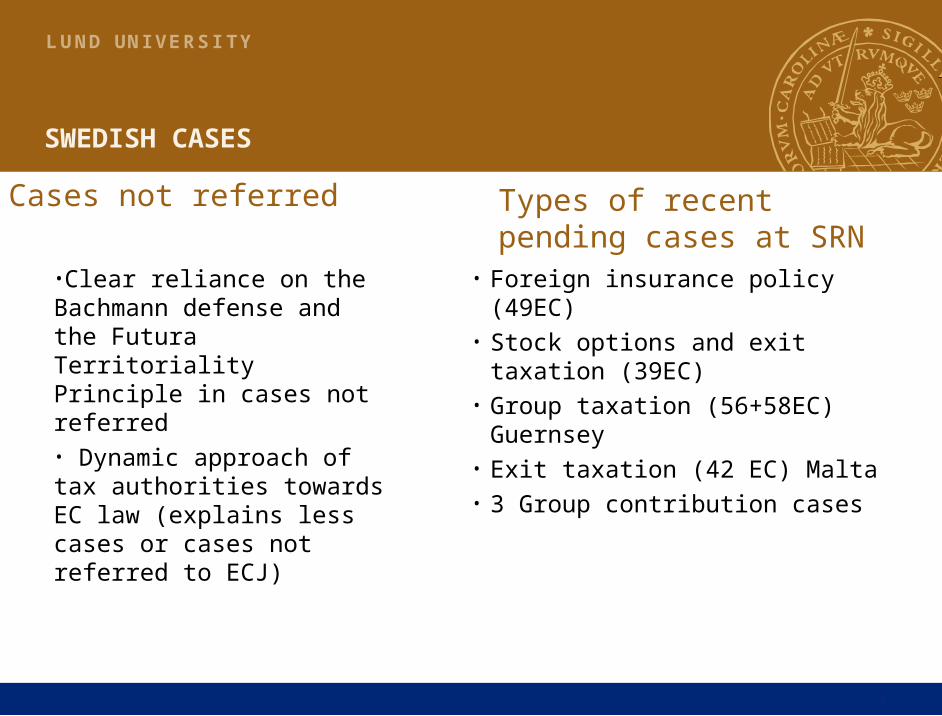

• Foreign insurance policy (49EC)• Stock options and exit taxation

(39EC)• Group taxation (56+58EC) Guernsey• Exit taxation (42 EC) Malta• 3 Group contribution cases

•Clear reliance on the Bachmann defense and the Futura Territoriality Principle in cases not referred• Dynamic approach of tax authorities towards EC law (explains less cases or cases not referred to ECJ)

Cases not referred Types of recent pending cases at SRN

4

L U N D U N I V E R S I T Y

Earlier case law

22/10Not145

17/8Ref 47Ref38Ref 43

18/10 Ref 86

29/10BODLUND

4/7 Söderberg

4/7 Mogren

29/10Gambro

17/9Ref 84

22/10Elenius

Safir28/4/96

Xab & Yab18/11/99

X & Y21/11/02

Skandia26/6/03

30/3 Örfelt

11/3lasteyrie

Wallentin 1//7

7/6ref66

95-99 00 01 03 0418/10Comm/SW234

05

14/2 not7

27/4 Littorin

20/9 Bergen

29/9 Traneus

06

Bouanich16/1

24/3Cylinda

4/4CFC

30/5Lindex

1/11Europress

6/7Y.Rocher

1/04Comm/SW CG

02

8/7 Exit

4/5Ref 21

3/2Tauson

29/6not135

C-101/05.

C-101/05.

15/6Ref 53

30/5Palazzini

16/5Mogren

29/3Merger invest