Page 1

Swiss Software Industry Survey 2019

THOMAS HURNI, CORINNA RUTSCHI, AND JENS DIBBERN INSTITUTE OF INFORMATION SYSTEMS - INFORMATION ENGINEERING

A Study of the University of Bern on behalf of ICTswitzerland

November 2019

Current State, Emerging Trends, and Long-term developments

in the Swiss Software Industry

Page 2

Principal:

ICTswitzerland

Aarbergergasse 30

CH - 3011 Bern

Authors:

Corinna Rutschi

Dr. Thomas Hurni

Prof. Dr. Jens Dibbern

University of Bern

Institute of Information Systems

Department of Information Engineering

Engehaldenstrasse 8

CH - 3012 Bern

www.iwi.unibe.ch

Substantial and methodological partners:

ICTswitzerland

Dr. Pascal Sieber & Partners AG

Institut für Wirtschaftsstudien Basel

Tran Engineering

Promotional partners:

inside-it.ch

topsoft

SWICO

Alp ICT

Editorial support:

Nicolas Mayr von Baldegg

Stephanie Elliott

Maximilian Walser

Gowthaman Udayakumar

Jessica Zurbriggen

Anna Filippova

Louis Felder

Picture Credits:

Cover: Pexels.com; 4: Pexels.com; 6: Pexels.com; 13: Pexels.com; 16: Pexels.com; 27: Pexels.com

Bern, November 2019

Note regarding use :

No use of this publication may be made for resale

or any other commercial purpose whatsoever.

Additional remarks:

The report reflects the view of the authors which

does not necessarily correspond with the views of

the principal or of the support group.

Page 3

Swiss Software Industry Survey 2019 3

Preface

The fifth edition of the Swiss Software Industry Survey (SSIS), the

most extensive study of its kind in Switzerland, provides you with

comprehensive information about the current state, emerging

trends, and long-term developments of the Swiss software industry.

As in previous years, our goal was to be as close as possible to the

Swiss software industry and the people who shape it. To this end,

we conducted a workshop with representatives of the Swiss soft-

ware industry and used their feedback to optimize our question-

naire. The highly valuable feedback from this workshop, however,

not only helped us to optimize the SSIS as a whole but also served

as valuable input for the design of this year’s two special topics. The

first of these two special topics focuses on the productivity of the

Swiss software industry, thus on a central aspect in an increasingly

competitive environment. Here we show what measures Swiss soft-

ware companies are taking to increase their productivity. Besides,

we illustrate what changes Swiss software companies expect to see

in the sources of their revenues over the next three years. The sec-

ond special topic focuses on public tenders. Here we show the rea-

sons why Swiss software companies participate in public tenders or

explicitly refrain from doing so. We also illustrate the importance of

public tenders for individual subindustries and the major regions of

Switzerland.

This year, we again improved our SSIS benchmarking website to

provide a unique service to our participants. The SSIS benchmarking

website has become central to our value proposition, as it delivers

actionable information for participating companies. As an additional

incentive, we were able to offer participating companies, which

shared all key figures with us, a voucher for a free job advertise-

ment on ictjobs.ch. We thank our partner inside-it.ch for this oppor-

tunity.

The SSIS would not be possible without the long-term support of

our partners, in particular, ICTswitzerland, the principal of the

study, and Sieber & Partners. We want to thank ICTswitzerland,

Sieber & Partners, and all other partners for their continued sup-

port.

Finally, we would like to thank Thomas Huber for his many years of

commitment to the SSIS. Thomas Huber was appointed Assistant

Professor at the ESSEC Business School in Paris. Corinna Rutschi

joined the SSIS team this year and therewith completes our team.

We hope you enjoy reading this report!

Corinna Rutschi

Dr. Thomas Hurni

Prof. Jens Dibbern

Editorial

Corinna Rutschi

Dr. Thomas Hurni

Prof. Dr. Jens Dibbern

Page 4

Swiss Software Industry Survey 2019 4

Preface

5 Executive Summary

6 Revenue, Profitability & Future Growth

13 Sources of Revenue

16 Internationalization & Sourcing

20 Productivity

24 Public Tenders

27 About the SSIS 2019

Page 5

Swiss Software Industry Survey 2019 5

The EBIT margin of the Swiss software industry improved by 1.5 percentage points compared to the previ-

ous year and now amounts to 8.2%.This growing EBIT margin is reflected in the increase in revenues per

employee from CHF 221’098.4 in 2017 to CHF 225’498.9 in 2018. These positive developments result in a

more optimistic outlook for 2019 and 2020: For this year, a growth in revenues of 9.5% and an increase in

the number of employees of 11.6% are expected.

Growing EBIT Margins and Revenues per Employee

Executive Summary

2018 was a successful year for the Swiss software industry. The industry-wide revenue per employee rose from CHF

221’098.4 in 2017 to CHF 225’498.9 in 2018 and the industry-wide EBIT margin from 6.7% in 2017 to 8.2% in 2018. Due

to these positive developments, Swiss software companies are more optimistic about the future. Both the expected

growth of revenues (i.e., 9.5% in 2019 and 11.3% in 2020) and employees (i.e., 11.6% for 2019 and 14.9% for 2020) is

higher than in the previous year. Also, software companies are trying to become more productive through process opti-

mization and employee development.

Executive Summary

Swiss software companies expect cloud solutions to gain in importance by 2021. The share of cloud solu-

tions in industry sales is expected to rise from 7.5% today to 11.5% in 2021. According to expectations,

this increase will be at the expense of the development of custom software. Here a reduction of 5.2 per-

centage points in the share of industry revenue is expected by 2021. This development indicates that the

industry will increasingly focus on more scalable products and services.

Shift Towards Cloud

Swiss software companies find themselves in an increasingly international competitive environment. To

survive in this environment, they invest in productivity-enhancing measures. By far the most important

measures concern existing processes that are optimized, agilitized, automatized and/or digitalized. Be-

sides, Swiss software companies also invest heavily in the development of their workforce and infrastruc-

ture, in adapting their product and service portfolios, and in improving their knowledge management.

Productivity: Do Things Better

The Swiss software industry generates about 17% of its revenue from contracts awarded in compliance

with WTO rules. Such contracts are particularly relevant for software companies from the Espace Mittel-

land and for consulting companies. The most important reason why Swiss software companies explicitly

refrain from participating in WTO-compliant tenders is the high cost in relation to the expected return.

The most important reason for participation is the attractiveness of such contracts.

Public Tenders

Page 6

Swiss Software Industry Survey 2019 6

Revenue, Profitability & Future Growth

Spotlight on

Page 7

Swiss Software Industry Survey 2019 7

Distribution of Participating Companies

Figure 1: Number of companies per subindustry as percentage of total responses

Source: SSIS 2019

Spotlight on Revenue, Profitability and Future Growth

As in previous years, custom software manufacturers

and standard software manufacturers dominate our

sample. Both subindustries account for about one third

of the answers. Consulting companies (12.4%), software

integrators (8.5%), and technology and service provid-

ers (6.4%) follow at some distance (see Figure 1).

To make valid statements about the Swiss software in-

dustry as a whole, we post-stratified our sample. This

statistical procedure compares our sample with the

software industry as a whole by taking into account offi-

cial statistics on regions, subindustries, company sizes,

and revenues. If this procedure finds that individual

participating companies are under-represented in our

sample, then it assigns them higher weights to adjust

for biases. The advantage of this procedure is that state-

ments about the industry as a whole become more reli-

able. Moreover, the SSIS 2019 is backward compatible

as we have applied the same statistical procedure to the

samples of the SSIS in 2017 and 2018. The figures in this

report are therefore comparable to those in the previ-

ous two reports.

Figure 2 shows that consulting companies are the main

contributors to industry revenue (43.3%), followed by

manufacturers of custom software (24.4%) and stand-

ard software (24.0%). Together, these three sub-

industries account for more than 90.0% of the industry

revenue.

Given that software companies usually operate in a

wide variety of fields, i.e., consulting companies do not

only ‘consult’ but also create revenue through other

activities such as custom software development or soft-

ware integration. Figure 3 considers this diversity by

showing the revenues by activity. Here, consulting

(22.6%), standard (23.5%) and custom software manu-

facturing (32.2%) contribute most significantly to the

industry revenue. Interestingly, Figure 3 shows that

across all companies, more than 50.0% of the industry

revenue is created through the development of soft-

ware (standard and custom).

Sample, Projection Method, and Industry Revenue

N = 484

Standard software manufacturer (including SaaS)

33.1%

Custom software manufacturer29.3%

Consulting12.4%

Software integrator

8.5%

Technology and service providers6.4%

Other

10.3%

Page 8

Swiss Software Industry Survey 2019 8

Distribution of Revenue per Subindustry

Figure 2: Revenue per subindustry as percentage of industry revenue

Spotlight on Revenue, Profitability and Future Growth

Distribution of Revenue per Activity

Figure 3: Revenue per field of activity as percentage of industry revenue

Source: SSIS 2019 N = 191

Source: SSIS 2019 N = 191

Consulting43.3%

Custom software manufacturer24.4%

Standard software manufacturer (including SaaS)

24.0%

Software integrator2.0%

Technology and service providers1.6%

Other4.6%

Custom software manufacturing32.2%

Standard software manufacturing (including SaaS)

23.5%

Consulting22.6%

Software integration10.6%

Providing software-related mainteneance services3.8%

Other7.2%

Page 9

Swiss Software Industry Survey 2019 9

Spotlight on Revenue, Profitability and Future Growth

Revenue per Employee

Figure 4: Average revenue per employee

Source: SSIS 2019 N = 190

Figure 4 shows the revenue per employee in 2018 com-

pared to 2017. Overall, the revenue per employee in-

creased slightly to CHF 225’498.9 in 2018 compared to

CHF 221’098.4 in 2017. As in previous years, manufac-

turers of custom software generated the lowest reve-

nue per employee (CHF 189’246.3), followed by tech-

nology and service providers (CHF 239’221.1), con-

sulting companies (CHF 241’173.9), standard software

manufacturers (CHF 248’156.3), and software integra-

tors (CHF 252’597.4).

Figure 5 shows the distribution of employees. It mirrors

the distribution of revenues, i.e., consulting companies

(33.6%), custom software manufacturers (31.5%), and

standard software manufacturers (25.5%) account for

more than 90.0% of the industry’s employees.

Higher Revenues per Employee

Distribution of Employees

Figure 5: Number of employees per subindustry as percentage of total employees

Source: SSIS 2019 N = 191

Consulting

33.6%

Custom software manufacturer31.5%

Standard software manufacturer

(including SaaS)

25.5%

Software integrator2.6%

Technology and service providers1.9%

Other

4.9%

CH

F 1

81

’86

3.8

CH

F 2

31

’48

4.4

CH

F 2

38

’61

5.1

CH

F 2

55

’21

1.0

CH

F 2

64

’26

5.1

CH

F 2

21

’09

8.4

CH

F 1

89

’24

6.3

CH

F 2

48

’15

6.3

CHF

241’

173.

9

CH

F 2

52

’59

7.4

CH

F 2

39

’22

1.1

CH

F 2

25

’49

8.9

CHF -

CHF 50’000.0

CHF 100’000.0

CHF 150’000.0

CHF 200’000.0

CHF 250’000.0

CHF 300’000.0

Custom softwaremanufacturer

Standard softwaremanufacturer

(including SaaS)

Consulting Softwareintegrator

Technology andservice providers

Software Industry

2017 2018

Page 10

Swiss Software Industry Survey 2019 10

Spotlight on Spotlight on Revenue, Profitability and Future Growth

Figure 6 shows the EBIT margins of the subindustries

with an industry-wide increase from 6.7% in 2017 to

8.2% in 2018. This upward trend applies to all subindus-

tries, with the exception of standard software manufac-

turers, which generated a lower margin (from 9.1% in

2017 to 4.8% in 2018).

Figure 7 shows the EBIT margins by activities. This figure

reflects broadly the same pattern as Figure 6: compared

to the previous year, profitability has increased overall.

Again, this increase is shown in almost all activities, ex-

cept for standard software manufacturing and software

integration, which have both decreased in profitability.

Increasing EBIT Margins

EBIT Margins in the Swiss Software Industry

Figure 6: EBIT margins by subindustries

Source: SSIS 2019 N = 171

EBIT Margins per Activity

Figure 7: EBIT margins per activity

Source: SSIS 2019 N = 171

5.5%

9.1%

6.7%7.5%

5.3%

6.7%

7.8%

4.6%

10.1%9.4%

6.8%

8.2%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Custom softwaremanufacturer

Standard softwaremanufacturer

(including SaaS)

Consulting Software integrator Technology andservice providers

Software Industry

2017 2018

6.1%

8.0%

5.9%

8.5%

5.0%

6.7%

8.4%

4.4%

11.3%

7.7%6.6%

8.2%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Custom softwaremanufacturing

Standard softwaremanufacturing(including SaaS)

Consulting Software integration Technology andservice provision

Software Industry

2017 2018

Page 11

Swiss Software Industry Survey 2019 11

Expected Growth in Revenue

Figure 8: Expected year-over-year revenue growth for 2019 and 2020

Spotlight on Revenue, Profitability and Future Growth

Source: SSIS 2019 N = 189

Research and Development Investments

Figure 9: R&D investments in 2017 and 2018 as percentage of revenue

Figure 8 shows the positive revenue expectations of the

Swiss software industry. Compared to the moderate

expectations of the previous year, Swiss software com-

panies now expect a growth of 9.5% in 2019 and even

11.3% in the following year. In 2019, standard software

manufacturers expect the highest revenue growth

(10.8%), followed by software integrators (10.4%), con-

sulting firms (10.1%), custom software manufacturers

(8.9%), and technology and service providers (8.0%).

Overall, this leads to the assumption that the Swiss soft-

ware industry is optimistic about the future.

Optimistic Growth Expectations

Across all subindustries, Swiss software companies have

invested less of their revenues in research and develop-

ment (see Figure 9) compared to the previous year.

R&D expenses thus fell to the level of 2016.

As in prior years, manufacturers of standard software

have invested the most in R&D (13.8%), while all other

subindustries invested less than 6.0%. More specifically,

manufacturers of custom software spent 5.4%, con-

sulting firms 5.1%, technology and service providers

4.5%, and software integrators 3.9% of their revenues in

R&D.

Lower R&D Investments

Source: SSIS 2019 N = 177

8.9%10.8% 10.1% 10.4%

8.0% 9.5%12.1%

14.7%

9.4%

19.7%

9.6%11.3%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Custom softwaremanufacturer

Standard softwaremanufacturer

(including SaaS)

Consulting Software integrator Technology andservice providers

Software Industry

2019 2020

12.6%

25.3%

4.0%7.0% 5.8%

11.3%

5.4%

13.8%

5.1% 3.9% 4.5%7.1%

0.0%5.0%

10.0%15.0%20.0%25.0%30.0%

Custom softwaremanufacturer

Standard softwaremanufacturer

(including SaaS)

Consulting Software integrator Technology andservice providers

Software Industry

2017 2018

Page 12

Swiss Software Industry Survey 2019 12

Spotlight on Revenue, Profitability and Future Growth

Employee Growth Prospects

Figure 10: Expected year over year growth of workforce for 2019 and 2020

Source: SSIS 2019 N = 191

Figure 10 shows the employee growth expectations of

the Swiss software industry. Interestingly, the overall

employee growth expectations (11.6% for 2019 and

14.9% for 2020) reflect the revenue growth expecta-

tions (9.9% for 2019 and 11.3% for 2020), i.e., high in-

creases in expected revenue mirror similarly high in-

creases in the workforce.

For 2019, the Swiss software industry expects to hire

11.6% additional employees, and 13.6% in 2020.

No subindustry plans to reduce their workforce in the

upcoming two years. In 2019, manufacturers of custom

software plan the steepest increases in their workforce

(15.7%), followed by technology and service providers

(12.7%), consulting companies (11.9%), software inte-

grators (11.3%), and standard software manufacturers

(7.3%). In 2020, software integrators (20.0%) and con-

sulting companies (19.9%) plan the steepest increases in

their workforce. However, given the small number of

responses within these subindustries, these high values

are not as robust as those for the industry as a whole.

Besides, technology and service providers expect an

increase of 14.5%, custom software manufacturers of

13.5% and standard software manufacturers of 9.8% in

their workforce.

Expected Employee Growth Reflects Expected Revenue Growth

Expected employee growth of

in 2019

11.6%

15.7%

7.3%

11.9%11.3%

12.7%11.6%

13.5%

9.8%

19.9% 20.0%

14.5% 14.9%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Custom softwaremanufacturer

Standard softwaremanufacturer

(including SaaS)

Consulting Software integrator Technology andservice providers

Software Industry

2019 2020

Page 13

Swiss Software Industry Survey 2019 13

Sources of Revenue Spotlight on

Page 14

Swiss Software Industry Survey 2019 14

Spotlight on Sources of Revenue

Sources of Revenue

Figure 11: Revenue from different revenue sources as percentage of industry revenue

Source: SSIS 2019 N = 178

Figure 11 shows the sources of revenue of Swiss soft-

ware companies in 2018. With a share of 39.2%, the

most crucial source of revenue for Swiss software com-

panies in 2018 was the development of custom-made

software, followed by maintenance and support

(16.7%). Together, with the revenues from the two cus-

tomization categories (i.e., customization of self-

developed standard software (7.1%) and third-party

standard software (5.6%)), the development of custom-

made software and maintenance and support account

for almost three-fourths of the revenue. This underlines

the importance of custom software solutions in Switzer-

land. At the same time, it is evident that the Swiss soft-

ware industry offers only a minimal range of scalable

standard software and incurs license fees for it (8.9%).

Interestingly, revenues from cloud solutions (7.5%) be-

came more critical compared to 2017 (5.0%).

If we now look at the revenue sources of standard and

individual software manufacturers separately, the pic-

ture is quite different. For manufacturers of standard

software (see Figure 12), maintenance and support

(37.8%), royalties from own software licenses (27.5%),

and customization of self-developed standard software

(14.1%) account for more than three-fourths of the rev-

enue. Revenues from cloud solutions grew in im-

portance since 2017 and now account for 13.8%

(compared to 6.2% in 2017).

For custom software manufacturers (see Figure 13), the

development of custom software is the largest source of

revenue (59.1%). Together with revenues from mainte-

nance and support (11.2%), the development of custom

software accounts for almost three fourths.

Sources of Revenue

From the industry revenue

are generated through cloud solutions

7.5%

Development of custom-made software39.2%

Maintenance and support16.7%

Royalties (own software licenses)8.9%

Cloud solutions

7.5%

Customization (self-developed standard software)

7.1%

Customization (3rd-party s tandard software)

5.6%

Embedded software2.0%

Royalties (resale)

1.7%

Other11.2%

Page 15

Swiss Software Industry Survey 2019 15

Sources of Revenue for Manufacturers of Standard Software

Figure 12: Revenue from different revenue sources as percentage of standard software manufacturer revenue

Spotlight on Sources of Revenue

Sources of Revenue for Manufacturers of Custom Software

Figure 13: Revenue from different revenue sources as percentage of custom software manufacturer revenue

Source: SSIS 2019 N = 51

Source: SSIS 2019 N = 61

Maintenance and support37.8%

Royalties (own software licenses)27.5%

Customization (self-developed s tandard software)

14.1%

Cloud solutions13.8%

Development of custom-made software2.1%

Customization (3rd-party s tandard software)1.5%

Royalties (resale)0.8%

Embedded software

0.3% Other

1.9%

Development of custom-made software

59.1%

Maintenance and support11.2%

Customization (self-developed standard software)

10.0%

Royalties (own software licenses)8.0%

Customization (3rd-party

s tandard software)4.8%

Cloud solutions

1.9%

Royalties (resale)0.4%

Embedded software0.2%

Other4.4%

Page 16

Swiss Software Industry Survey 2019 16

Internationalization & Sourcing

Spotlight on

Page 17

Swiss Software Industry Survey 2019 17

Degree of Internationalization and Target Markets

Figure 14: Distribution of international revenue

Source: SSIS 2019

Spotlight on Internationalization & Sourcing

N = 188

Figure 14 shows the degree of internationalization and

the target markets in 2018. Compared to 2017, the per-

centage of revenue Swiss software companies genera-

ted abroad decreased to 14.0%. This is a sharp de-

crease of 11.0 percentage points compared to 2017.

Like in prior years, Germany remains the most im-

portant export market (26.9%). Compared to 2017,

however, this is a decrease of 9.8 percentage points and

thus one possible explanation for the overall decline.

The second most important international market in

2018 was Luxembourg, with 19.8%, followed by North

America (9.8%), the United Kingdom (7.2%), and the

neighbouring countries France (6.0%) and Italy (5.3%).

Figure 15 shows the employee growth prospects ab-

road. With 10.6% for 2019 and 13.5% for 2020, these

growth prospects are lower than the growth prospects

in Switzerland (11.6% for 2019 and 14.9% for 2020).

Increasing Internationalization of Swiss Software Companies

Growth of Headcounts Abroad

Figure 15: Percentage of growth in headcounts of employees in Switzerland and abroad

Source: SSIS 2019 N = 48

10.6%

13.5%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

2019 2020

Switzerland

86.0%

Germany26.9%

Luxembourg19.8%

North

America9.8%

United Kingdom7.2%

France

6.0%Ita ly5.3%

Asia4.8%

Other European countries

12.9%

Rest of the World7.3%

Page 18

Swiss Software Industry Survey 2019 18

Spotlight on Sources of Revenue

Outsourcing Yes—No

Figure 16: Percentage of companies that outsource by subindustries

Source: SSIS 2019 N = 260

Sourcing, the development, improvement, and opera-

tion of IT products and/or services through external

service providers and/or own subsidiaries, remains vital

for Swiss software companies. Figure 16 shows the pro-

pensity to source products or services from external

service providers, own subsidiaries, or both external

service providers and own subsidiaries in 2018.

Our results show that the propensity to outsource is the

highest among consulting firms (54.8%), followed by

software integrators (45.8%), custom software manu-

facturers (40.5%), technology and service providers

(30.8%), and standard software manufacturers (30.6%).

Interestingly, the propensity to source services and/or

products from own subsidiaries is the highest among

standard software manufacturers (10.6%). So while

standard software manufacturers are comparably reluc-

tant to source from external service providers, they are

relatively often doing so from their subsidiaries. The

second-highest propensity to source services and/or

products from own subsidiaries had technology and

service providers (7.7%), followed by custom software

manufacturers (6.3%), software integrators (4.2%), and

consulting companies (3.2%).

When it comes to sourcing from both external service

providers and own subsidiaries, software integrators

had the highest propensity (16.7%), followed by tech-

nology and service providers (15.4%), consulting compa-

nies (12.9%), standard software manufacturers (10.6%),

and custom software manufacturers (7.6%).

Outsourcing in the Swiss Software Industry

Among consulting companies

do source products and/or services from external service providers

54.8%

40.5%30.6%

54.8%45.8%

30.8%38.1%

6.3%

10.6%

3.2%

4.2%

7.7%

6.5%

7.6%10.6%

12.9%

16.7%

15.4%12.3%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Custom softwaremanufacturer

Standard softwaremanufacturer

(including SaaS)

Consulting Software integrator Technology andservice providers

Software industry

External Service Provider Own Subsidiary Both External Service Provider and Own Subsidiary

Page 19

Swiss Software Industry Survey 2019 19

Spotlight on Internationalization & Sourcing

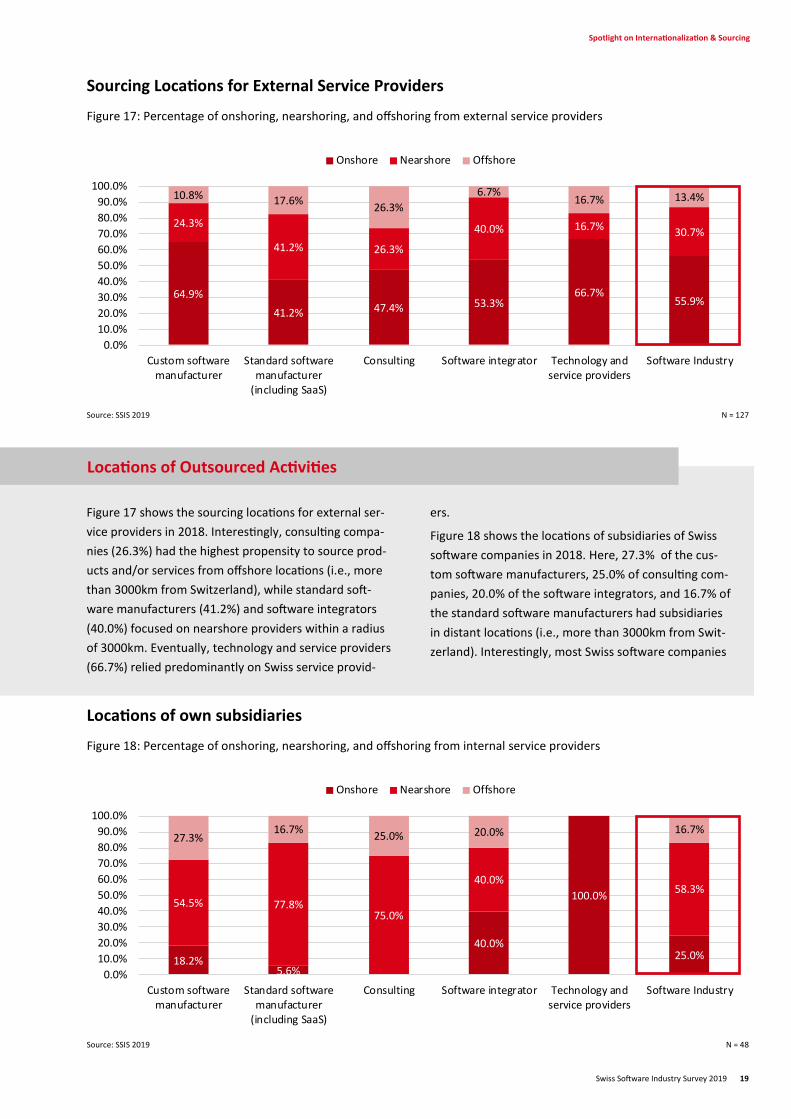

Sourcing Locations for External Service Providers

Figure 17: Percentage of onshoring, nearshoring, and offshoring from external service providers

Source: SSIS 2019 N = 127

Locations of own subsidiaries

Figure 18: Percentage of onshoring, nearshoring, and offshoring from internal service providers

Source: SSIS 2019 N = 48

Figure 17 shows the sourcing locations for external ser-

vice providers in 2018. Interestingly, consulting compa-

nies (26.3%) had the highest propensity to source prod-

ucts and/or services from offshore locations (i.e., more

than 3000km from Switzerland), while standard soft-

ware manufacturers (41.2%) and software integrators

(40.0%) focused on nearshore providers within a radius

of 3000km. Eventually, technology and service providers

(66.7%) relied predominantly on Swiss service provid-

ers.

Figure 18 shows the locations of subsidiaries of Swiss

software companies in 2018. Here, 27.3% of the cus-

tom software manufacturers, 25.0% of consulting com-

panies, 20.0% of the software integrators, and 16.7% of

the standard software manufacturers had subsidiaries

in distant locations (i.e., more than 3000km from Swit-

zerland). Interestingly, most Swiss software companies

Locations of Outsourced Activities

64.9%

41.2% 47.4% 53.3%66.7%

55.9%

24.3%

41.2% 26.3%

40.0% 16.7% 30.7%

10.8% 17.6%26.3%

6.7%16.7% 13.4%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Custom softwaremanufacturer

Standard softwaremanufacturer

(including SaaS)

Consulting Software integrator Technology andservice providers

Software Industry

Onshore Nearshore Offshore

18.2%5.6%

40.0%

100.0%

25.0%

54.5% 77.8%75.0%

40.0%58.3%

27.3%16.7%

25.0% 20.0% 16.7%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Custom softwaremanufacturer

Standard softwaremanufacturer

(including SaaS)

Consulting Software integrator Technology andservice providers

Software Industry

Onshore Nearshore Offshore

Page 20

Swiss Software Industry Survey 2019 20

Productivity Spotlight on

Page 21

Swiss Software Industry Survey 2019 21

Spotlight on Productivity

Source: SSIS 2019

Figure 19 shows the measures taken by Swiss software

companies in 2018 to enhance their productivity. Most

of the enhancement measures concerned existing pro-

cesses, including the optimization, agilization, automa-

tion, and digitalization of business processes. Swiss soft-

ware companies have also invested heavily in upskilling

their staff through trainings and new employees,

streamlining their product and service portfolios

through standardizations and cloud solutions, using the

latest technologies, improving their knowledge manage-

ment, and promoting employee loyalty.

Figure 20 shows the measures Swiss Software compa-

nies consider efficient to enhance productivity.

Productivity-enhancing measures in the Swiss software industry

Named Measures to Enhance Productivity

Figure 19: Measures to increase productivity in proportion to their naming

Source: SSIS 2019 N =

Page 22

Swiss Software Industry Survey 2019 22

Spotlight on Internationalization & Sourcing

Effectiveness of Productivity-Enhancing Measures

Figure 20: Which productivity-enhancing measures do Swiss software companies consider efficient?

Source: SSIS 2019 N = 200

Shifts in Sources of Revenue until 2021

Figure 21: Revenue sources in 2018 compared to revenue sources in 2021

Source: SSIS 2019 N = 178

Figure 21 shows the revenue sources in 2018 compared

with the revenue sources expected by Swiss software

companies in 2021. Interestingly, Swiss software com-

panies expect a significant shift in revenues from the

development of custom-made software (from 39.2% in

2018 to 34.0% in 2021) to cloud solutions (from 7.5% in

2018 to 11.5% in 2021), and maintenance and support

(from 16.7% in 2018 to 18.7% in 2021).

Figure 22 shows the same diagram for standard soft-

ware manufacturers. Here, revenues from cloud solu-

tions increase from 13.8% to 21.4% while, revenues

from royalties decrease from 27.5% to 23.1% .

Figure 23 shows the same diagram for custom software

manufacturers. Here, revenues from cloud solutions

increase from 1.9% to 7.1%, while revenues from cus-

tom-made software decrease from 59.1% to 49.8%.

Expected Changes in the Sources of Their Revenues

-80.0% -60.0% -40.0% -20.0% 0.0% 20.0% 40.0% 60.0% 80.0% 100.0%

Training existing employees

Simplifying of internal processes

Standardizing of internal processes

Reusing existing components

Automating of internal processes

Hiring more productive employees

Sourcing activites

39

.2%

16

.7%

7.5

%

8.9

%

7.1

%

5.6%

2.0

%

1.7

%

11.2

%

34

.0%

18

.7%

11

.5%

8.5%

7.0

%

5.7

%

1.9

%

1.9%

10.9

%

0.0%5.0%

10.0%15.0%20.0%25.0%30.0%35.0%40.0%45.0%

De

ve

lop

me

nt

of

cust

om-m

ade

soft

war

e

Mai

nten

ance

and

sup

po

rt

Clo

ud

so

luti

on

s

Ro

yalt

ies

(ow

nso

ftw

are

licen

ses)

Cust

om

izat

ion

(sel

f-d

ev

elo

pe

d s

tan

da

rdso

ftw

are

)

Cu

sto

miz

atio

n (3

rd-

pa

rty

sta

nd

ard

soft

wa

re)

Emb

edde

d s

oftw

are

Ro

yalt

ies

(res

ale)

Oth

er

2018 2021

Page 23

Swiss Software Industry Survey 2019 23

Shifts in Sources of Revenue until 2021 for Standard Software Manufacturers

Figure 22: Revenue sources of standard software manufacturers in 2018 compared to revenue sources in 2021

Spotlight on Sources of Revenue

Shifts in Sources of Revenue until 2021 for Custom Software Manufacturers

Figure 23: Revenue sources of custom software manufacturers in 2018 compared to revenue sources in 2021

Source: SSIS 2019 N = 51

Source: SSIS 2019 N = 61

37

.8%

27

.5%

13.8

%

14

.1%

1.5

%

0.8

%

2.1

%

0.3

%

1.9

%

35.1

%

23.1

%

21

.4%

12

.6%

2.3

%

1.3%

1.3%

1.0

%

1.8

%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Ma

inte

na

nce

an

d s

up

po

rt

Ro

yalt

ies

(ow

n s

oft

wa

relic

ense

s)

Clou

d so

luti

ons

Cust

om

izat

ion

(sel

f-de

velo

ped

stan

da

rd s

oft

wa

re)

Cu

sto

miz

ati

on

(3

rd-p

art

yst

and

ard

so

ftw

are)

Ro

yalt

ies

(res

ale)

Dev

elo

pm

ent

of c

ust

om-m

ade

soft

war

e

Emb

edde

d s

oftw

are

Oth

er

2018 20215

9.1

%

11.2

%

10.0

%

8.0

%

4.8%

1.9

%

0.4

%

0.2

% 4.4%

49

.8%

11.3

%

10.5

%

10

.2%

5.1

%

7.1%

0.9%

0.2

% 4.8

%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Dev

elop

men

t of

cus

tom

-mad

eso

ftw

are

Ma

inte

na

nce

an

d s

up

po

rt

Cust

om

izat

ion

(sel

f-de

velo

ped

stan

da

rd s

oft

wa

re)

Ro

yalt

ies

(ow

n s

oft

wa

relic

ense

s)

Cu

sto

miz

ati

on

(3rd

-pa

rty

stan

dar

d s

oft

war

e)

Clo

ud

so

luti

on

s

Ro

yalt

ies

(re

sale

)

Emb

edde

d s

oftw

are

Oth

er

2018 2021

Page 24

Swiss Software Industry Survey 2019 24

Public Tenders Spotlight on

Page 25

Swiss Software Industry Survey 2019 25

Spotlight on Internationalization & Sourcing

Reasons for Participating in WTO Tenders

Figure 24: Reasons for participation in WTO tenders in proportion to their naming

Source: SSIS 2019 N = 70

Reasons Against Participation in WTO Tenders

Figure 25: Reasons against participation in WTO tenders in proportion to their naming

Source: SSIS 2019 N = 145

Figure 24 shows the reasons why Swiss software com-

panies participate in public tenders. Here, the most im-

portant reason for participation is the exploitation of

opportunities through attractive public projects, large

projects, new markets, or new customers. The second

most important reason was the specific orientation on

the public sector, followed by the ability to use free

capabilities and capacities, and to increase sales.

Figure 25 shows the reasons why Swiss software com-

panies do not participate in public tenders. The most

important reason for non-participation is the time and

effort small companies can hardly bear, the lack of ca-

pacity, and the low success rate. The second most im-

portant reason was a different orientation or simply a

lack of awareness.

WTO Tenders and the Swiss Software Industry Survey

Page 26

Swiss Software Industry Survey 2019 26

Spotlight on Internationalization & Sourcing

WTO-Compliant Revenues in the Subindustries

Figure 26: Percentage of revenues in 2018 in the individual subindustries from contracts awarded under WTO rules

Source: SSIS 2019 N = 72

WTO-Compliant Revenues in the Major Regions of Switzerland

Figure 27: Percentage of revenues in 2018 in the major regions of Switzerland from contracts awarded under WTO rules

Source: SSIS 2019 N = 72

Figure 26 shows the percentage of revenues in 2018 of

Swiss software companies from contracts awarded un-

der WTO rules. On average Swiss software companies

generate among 16.7% of the revenues form contracts

awarded under WTO. This source of revenue is most

important for consulting companies (22.2%) and soft-

ware integrators (18.1%).

Figure 27 shows the percentage of revenues in 2018 in

the major regions of Switzerland from contracts award-

ed under WTO rules. Revenues form contracts awarded

under WTO rules are most important for the Espace

Mittelland (31.9%), followed by Zurich (16.6%), eastern

Switzerland (15.7%), northern Switzerland (8.9%), and

the lake Geneva region (0.9%).

Revenues from Contracts Awarded in Accordance with WTO Rules

10.6% 7.8%22.2% 18.1%

6.5% 9.8% 16.7%

89.4% 92.2%77.8% 81.9%

93.5% 90.2% 83.3%

0.0%10.0%20.0%30.0%40.0%50.0%60.0%70.0%80.0%90.0%

100.0%

Custom softwaremanufacturer

Standardsoftware

manufacturer(including SaaS)

Consulting Softwareintegrator

Technology andservice providers

Other SoftwareIndustry

Revenues in 2018 from contracts awarded in accordance with WTO rules Other Revenues in 2018

31.9%16.6% 15.9% 15.7% 8.9% 0.9%

68.1%83.4% 84.1% 84.3% 91.1%

99.1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Espace Mittelland Zurich Eastern Switzerland Central Switzerland NorthwesternSwitzerland

Lake Geneva Region

Revenues in 2018 from contracts awarded in accordance with WTO rules Other Revenues in 2018

Page 27

Swiss Software Industry Survey 2019 27

About the SSIS Method and Official Statistics

Page 28

Swiss Software Industry Survey 2019 28

Geographical Distribution of the Participants in 2019

Figure 28: Participating companies per canton

The SSIS and Official Statistics

This year we conducted the Swiss Software Industry

Survey (SSIS) for the fifth time. With the fifth iteration,

the SSIS managed to defend its pole position in terms of

size, geographical reach, and methodological rigor:

Reach of the survey: The Swiss software industry sur-

vey aims to represent the entire Swiss software indus-

try—rather than only a couple of large companies.

Therefore, the SSIS…

Builds on an extended and refined high-quality

contact database with approximately 5’000 vali-

dated Swiss software companies

Covers all Swiss language regions

Covers 20 cantons (see Figure 28)

Builds on a large sample size with 591 partici-

pants, 271 complete responses, and 191 post-

stratified data points on revenue and profitability

Rigor of the survey: To meet highest research stand-

ards...

… we developed, refined, and assessed new con-

structs by following state-of-the-art procedures

for construct development

… we relied on the extrapolation method devel-

oped for last year’s SSIS, which builds on state-of

-the-art econometrical procedures (post-

stratification by region, subindustries, company

size, and revenue)

Additional benefits for participating companies: All

participants of the survey can compare their own per-

formance against other companies using our bench-

marking website. In addition, companies which partici-

pate regularly can now benchmark their performance

over time (www.softwareindustrysurvey.ch).

About the SSIS in 2019

Source: SSIS 2019

1

83

Responses

Page 29

Swiss Software Industry Survey 2019 29

Official Statistics - Employees and Added Value

Table 1: Distribution of Added Value in 2017 and distribution of Full-Time Equivalents in 2016 by industry

Source: BESTA , Added Value 2016, FTEs 2016

The SSIS and Official Statistics

Added Value FTEs

Energy Supply, Water Supply, Waste Management 1.6% 1.1%

Construction 5.5% 8.5%

Manufacturing 19.1% 16.0%

Trade, Repair of Motor Vehicles & Motorcycles 14.3% 13.5%

Accommodation and Food Service Activities 1.7% 4.9%

IT and Other Information Services (NOGA 62, 63) 2.4% 2.4%

Financial Service Activities & Insurance 9.4% 3.9%

Public Administration 10.8% 4.3%

Education 0.6% 6.0%

Human Health & Social Work Activites 8.2% 13.1%

Transportation, Storage, Information & Communication 6.1% 6.7%

Real Estate, Professional, Scientific, Technical & Administrative Activities 18.1% 15.7%

Other Sectors 2.2% 3.9%

Total 100% 100%

Data about the Swiss software industry is provided as

part of official statistics nested in the broad categories

of “Computer programming, consultancy and related

activities” and “Information service activities” (NOGA

codes 62 & 63).

The respective data on added value (i.e., revenue) and

number of employees from Swiss Statistics emphasize

the major importance of the Helvetic Information Tech-

nology and Information Services sector. With more than

20 billion Swiss francs it adds roughly 2.4% to the Swiss

GDP (see Table 1) and employs almost 2.4% of all job-

holders in Switzerland (see Table 1), and is one of the

strongest growing sectors. Figures 29 and 30 show the

official employee statistics.

Official statistics provide reliable information about the

size and growth of the overall IT sector. However, they

do not draw a very detailed picture about the Swiss

software industry.

Therefore, the SSIS positions itself as a complementary

study that enriches official statistics. Compatibility with

official statistics is ensured by focusing on two NOGA

codes (62, 63). Yet, we provide a richer picture of what

is going on within these codes. Specifically, the report

enables the following additional insights:

Trend analysis of key performance indicators

incl. EBIT, R&D expenditure, employee growth,

and revenue growth

Indicators on profitability and R&D investments

Analyses along practically relevant categories

(standard vs. custom software, maintenance vs.

testing, etc.).

The SSIS as Complement to Official Statistics

Page 30

Swiss Software Industry Survey 2019 30

Employees in the Swiss ICT Sector

Figure 29: Number of FTEs in NOGA 62 & 63 from 1991-2018

Spotlight on Sources of Revenue

Part-Time Employees in the Swiss ICT Sector

Figure 30: Number of FTEs and Part-Time Employees in NOGA 62 & 63 from 1991 - 2018

Source: BESTA 2019

Source: BESTA 2019

0.00

10'000.00

20'000.00

30'000.00

40'000.00

50'000.00

60'000.00

70'000.00

80'000.00

90'000.00

100'000.00

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Full

Tim

e Eq

uiv

ale

nts

Total (in FTE)

Full-time Employees (absolute numbers)

Part-time Employees (absolute numbers)

Total Male Employees (FTE)

Total Female Employees (FTE)

-

10'000.00

20'000.00

30'000.00

40'000.00

50'000.00

60'000.00

70'000.00

80'000.00

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Full

Tim

e Eq

uiv

ale

nts

Male Full-time Employees

Female Full-time Employees

Male Part-time Employees

Female Part-time Employees