47

Syndicate Capital Briefing 23/01/2017 © Lloyd’s

Syndicate Capital Briefing23/01/2017

© Lloyd’s

222

Agenda Capital reviews 2016

Lloyd’s capital review process

Looking forward – March and beyond

Capital results for 2017 YoA

Questions

© Lloyd’s

333

Capital reviews 2016 – How did it go?

© Lloyd’s

444

New Lloyd’s Actuary

Richard Rodriguez started in March 2016

No July submission of LCR

Following feedback from the market

Major model change

Reviewed through the year

More changes next year

© Lloyd’s

Year of transition

555

Capital reviews 2016 – Objectives

© Lloyd’s

666

Successful transition to one submission format

Major model change submissions

Link with SCR reviews

Key review period: September to November

CPG aims to:

offer a joined up review process with clear points of contact

ensure CEOs of MAs are clear on Lloyd’s view throughout

use “virtual teams” (MRC lead team on capital)

provide written feedback at specified points during the review

ensure consistency with PRA Guidance; risk margin and contract boundaries adjustment

initiate early awareness and approval of model development through major model change submissions

© Lloyd’s

What were the key objectives for 2017 YOA?

777

Generally positive feedback Peter Montanaro (CPG Chair) has written to all MAs

Great buy in from the market on the process

No major changes to the quantitative requirements

Value of early engagement

More efficient and effective process

© Lloyd’s

Overall it went well…

888

Many resubmissions this year More information to look at in the same timeframe

Major model change applications through the year Not always time/resource efficient

RI contract boundary adjustment was done on old/new basis 2018 YoA only on new basis

Heavy burden on MAs and centre

Reviewing process for 2018 YoA Same objectives

© Lloyd’s

Room for improvement?

999

The reviews sit alongside the SAG process:Similar to last year

Standards Assurance Group (SAG) assesses agents’ regulatory compliance

Capital and Planning Group (CPG) oversees Lloyd’s capital setting and syndicate business planning processes

CPG will make decision on prudential measures based on SAG input:

Capital loadings

Business plan restrictions

© Lloyd’s

Agent contact

RISK

ASSURANCE

FUNCTION

technical

review

TEAMS

Oversight and

decision making

Review work & agent

interaction

SAG

Terms of Reference:

• “Assess MA compliance with Lloyd's Standards”

• “Assess compliance with SII internal model tests and standards”

• “Authorise the use of syndicate internal models for capital setting & provide input to CPG”

• “Authorise syndicate major model changes”

CPG

Terms of Reference:

• “Approve all Business plans & Syndicate capital requirements”

• “Approve any Franchise Guideline dispensations”

MRC

Technical

Committee

101010

Additional Features of the review process

Second pair of eyes, SCR review for each syndicate was peer reviewed by another actuary

MRC technical committee, every peer reviewed CPG paper was discussed in detail by a panel of actuaries before CPG discussion

This ensured consistency in SCR/validation reviews

© Lloyd’s

Agent contact

RISK

ASSURANCE

FUNCTION

technical

review

TEAMS

Oversight and

decision making

Review work & agent

interaction

SAG

Terms of Reference:

• “Assess MA compliance with Lloyd's Standards”

• “Assess compliance with SII internal model tests and standards”

• “Authorise the use of syndicate internal models for capital setting & provide input to CPG”

• “Authorise syndicate major model changes”

CPG

Terms of Reference:

• “Approve all Business plans & Syndicate capital requirements”

• “Approve any Franchise Guideline dispensations”

MRC

Technical

Committee

111111

Where are we on validation?

Validation reports used to aid capital reviews

MAs faced challenge in validating the final number, due to time constraints

Validation reports followed a good structure

Board report covered key findings

Technical report/appendices covered

Feedback has now been sent to the market

© Lloyd’s

121212

Common validation issues

One year risk: Validation has improved, but not yet adequate in some cases

Quantitative tests can be included

Sensitivity tests

Scenario tests

Reverse stress tests

Alternatives considered

Comparison with Standard Formula

Qualitative assessment adds value too

More importantly, One year SCR often not highlighted in the Board report

© Lloyd’s

131313

Common validation issues

Reverse stress tests: Inconsistency in the test definition and design

Challenges are:

Quantifying ORSA scenarios

Determining return period for the combined scenarios

Selection of the collar of simulations around expert’s return period

Uses are:

Validation of the final distribution

Consideration of all the underlying dependencies

© Lloyd’s

141414

Common issues - Dependency

Parameterisation

Correlation coefficient/drivers/dependency structure

Expert judgement unavoidable

Rationale should be explained clearly

Validation

Expert judgements are often justified, not validated

Purpose of different validation tests Sensitivity/stress tests…how bad can it get?

Scenario test…when will it fail?

Reverse stress test…how does all the dependency structures work together?

Alternative assumptions…should be modelled, explanation not enough

Joint exceedance probabilities…explain the outcome

Input v output correlation…consider dampening effect in output correlation matrix

Difficulty in applying dependencies where distributions sparse (e.g. RI credit risk defaults)

© Lloyd’s

151515

Common issues - Dependency

Possible alternatives

Aggregate data, model and compare…this may not necessarily pick up tail dependency

Backtest…group data for similar pairs to increase data points

Compare dependency at the tail and also the body of distribution

Explain association through clarification of drivers

Diversification benefits – are pre / post diversification contributions consistent with the intended dependency structure?

Example: Consider what parts (percentiles) of the stand-alone distributions contribute to the combined 99.5th (or other) percentile

May indicate where the key considerations for correlations are (i.e. is it in extreme tail or other parts of the distribution )

Clearly this might be affected by the way the dependency structure has been modelled

Consider what dependency you expect to see at different parts of the distribution to inform the decision on appropriate copula

Might be interesting to see how this changes if different copulas are used…

© Lloyd’s

161616

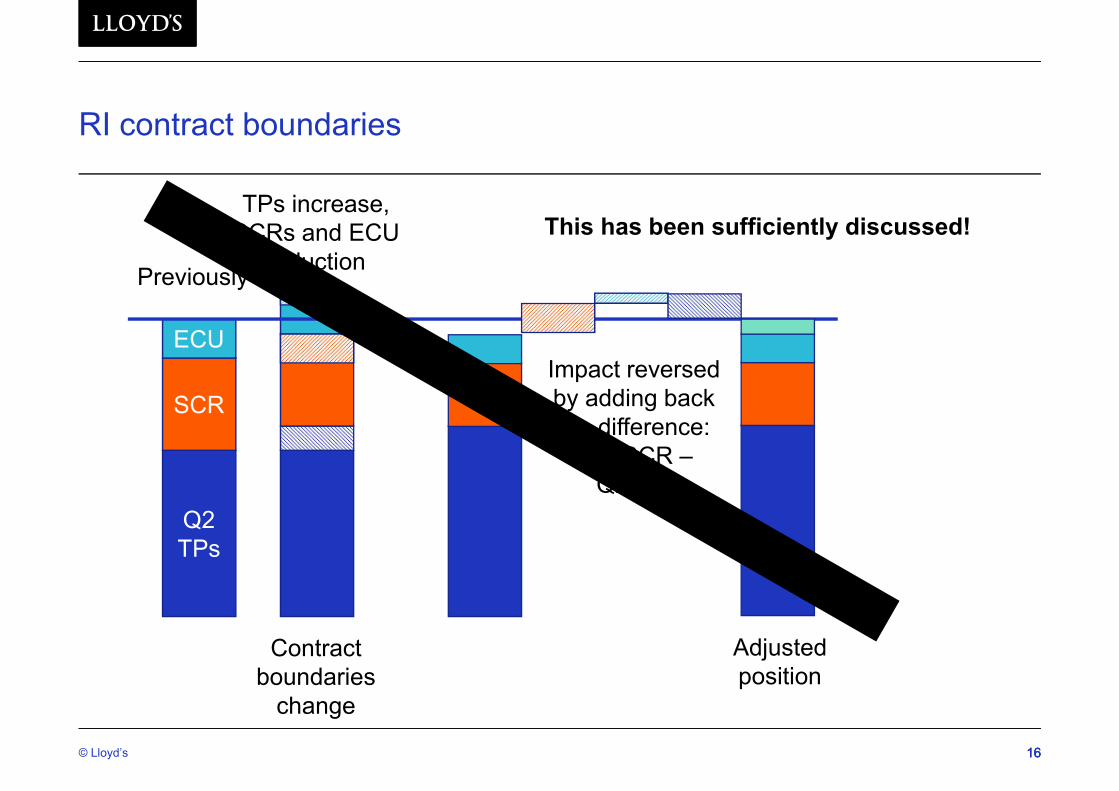

RI contract boundaries

© Lloyd’s

Q2 TPs

SCR

ECU

Previously

Contract boundaries

change

TPs increase, SCRs and ECU

reduction

Impact reversed by adding back the difference:

1.35SCR –Q2TPs

Adjusted position

This has been sufficiently discussed!

171717

Lloyd’s process

© Lloyd’s

181818

Lloyd’s review process

Analysis of Change

© Lloyd’s

EXAMPLE…

191919© Lloyd’s

2016 Sep 2016 Mar Significant movements between 2016 Sep and 2016 Mar

LCR edition 1 5 £ change % change

Exposure and Risk Margin

Premium 1 [Note 1] 75.9 85.7 -9.8 -11%Premium 2 [Note 2] 92.6 84.2 8.4 10%Reserves 1 [Note 3] 185.6 209.1 -23.5 -11%Reserves 2 [Note 4] 173.4 185.6 -12.2 -7%Premium 1 + 1/2 * Reserves 1 168.7 190.3 -21.6 -11%Premium 2 + 1/2 * Reserves 2 179.3 177.0 2.3 1%Risk margin (RM) 19.8 25.7 -5.9 -23%1:200 gross claims less 1:200 net claims [Note 5] 114.0 124.6 -10.6 -9%Available assets [Note 6] 278.4 303.8 -25.4 -8%

SCR

Mean -15.7 -12.5 -3.2 26% SCR (submitted) 62.4 58.9 3.5 6%Undiversified 75.1 74.3 0.8 1%Diversification credit (£) 12.7 15.4 -2.7 -18%Diversification credit (%) 16.9% 20.7% 0.0 -18%Loading [Note 7] 0.0 0.0 0.0SCR (agreed) 62.4 58.9 3.5 6%SCR (agreed) + RM 82.2 84.6 -2.4 -3%Mean vs. Premium 1 + 1/2 * Reserves 1 -9.3% -6.6% 42% Mean vs. exposure has increased by more than 5%SCR (agreed) + RM vs. Premium 1 + 1/2 * Reserves 1 48.7% 44.5% 10% 1:200 has increased by more than 5%SCR (agreed) + RM vs. Premium 2 + 1/2 * Reserves 2 45.8% 47.8% -4%

Insurance risk

Mean -11.2 -9.6 -1.6 17% The 1:200 has decreased but the mean profit has not1:200 48.8 57.3 -8.5 -15%1:200 undiversified 54.9 71.2 -16.3 -23%Diversification credit (£) 6.1 13.9 -7.8 -56%Diversification credit (%) 11.1% 19.5% -43% 1:200 + RM 68.6 83.0 -14.4 -17%Mean vs. Premium 1 + 1/2 * Reserves 1 -6.6% -5.0% 32% Mean vs. exposure has increased by more than 5%1:200 + RM vs. Premium 1 + 1/2 Reserves 1 40.7% 43.6% -7% 1:200 has decreased by more than 5%1:200 + RM vs. Premium 2 + 1/2 Reserves 2 38.3% 46.9% -18%

Premium risk

Mean -4.9 -6.3 1.4 -22%

1:200 48.2 32.9 15.3 47%

Mean vs. Premium 1 -6.5% -7.4% -12% Mean vs. exposure has decreased by more than 5%1:200 vs. Premium 1 63.5% 38.4% 65% 1:200 has increased by more than 5%1:200 vs. Premium 2 52.1% 39.1% 33%

Reserve risk

Mean -19.8 -25.7 5.9 -23% 1:200 24.4 19.5 4.9 25%1:200 + Risk margin 44.2 45.2 -1.0 -2%Mean vs. Reserves 1 -10.7% -12.3% -13% Mean vs. exposure has decreased by more than 5%1:200 vs. Reserves 1 13.1% 9.3% 41%1:200 + RM vs. Reserves 1 23.8% 21.6% 10% 1:200 has increased by more than 5%1:200 + RM vs. Reserves 2 25.5% 24.4% 5%

2016 Sep vs. 2016 Mar

A. EXPOSURE & RISK MARGIN

B. ULTIMATE RISK

202020

Mean 50th 75th 90th 95th 99.5th

A 50.0 29.0 Y 58% 39% 60% 75% 85% 92%

B 12.0 9.0 Y 75% 57% 65% 74% 79% 95%

C 1.4 0.9 N 63% 36% 78% 149% 227% 436%

D 77.0 56.0 N 73% 64% 75% 86% 93% 114%

E 4.0 1.0 Y 25% 26% 32% 45% 48% 55%

F 23.0 11.3 Y 49% 54% 66% 77% 85% 106%

G 2.9 1.6 Y 55% 65% 75% 78% 81% 85%

H 1.1 0.9 N 82% 72% 92% 113% 126% 165%

I 15.0 11.5 N 77% 87% 95% 120% 132% 177%

J 8.0 4.3 Y 54% 73% 83% 93% 100% 118%

K 9.9 7.3 Y 74% 78% 89% 102% 113% 189%

L 0.9 0.3 Y 28% 58% 68% 79% 88% 124%

All other

Total 205.2 133.1 65% 74% 88% 91% 99% 103%

Class Name Net PremiumMean Net

Claims

CAT

Exposed

ULRs including Catastrophe

Supplementary Questionnaire

© Lloyd’s

212121

Lloyd’s review process

Analysis of Change

Supplementary Questionnaire

Documentation

Validation report

Discussion with the agent

Challenges

Documentation – often incomplete

Sign posting – risk of missing out on key details

Documentation structure - pack doesn’t need to be updated annually, but details are still required

© Lloyd’s

222222

What happens in March & beyond?

© Lloyd’s

232323

Specific re-submissions in March

For a number of agents the CPG or SAG feedback was to require a resubmission in March

either a material point to resolve; or

agent proposed as work not complete

not every case was where a capital loading applied

we are currently working with agents on these

For everyone else MB Y5013 applies:

If circumstances change, leading to a material change in SBF and/or uSCR, by the end of February 2017, then a resubmission of relevant returns must be made

by 02 March 2017.

© Lloyd’s

242424

High level principles of the March reassessments

Highlights of SCR Re-assessments:

Resubmissions for material (greater than 10%) movements excluding FX/risk

in the SCR to ultimate. Also resubmit the revised one-year SCR

For any SAG related issues you may wish to make a resubmission – this is

fine but please contact us if planning on doing this

Resubmissions must be made at the year-end exchange rates (US$:GBP rate

was 1.24), see MB Y5053 for all currencies

LCRs should be re-submitted by 1pm, 2 March 2017

Where no resubmission is required and the current SCR is still valid, agents

should confirm this to Lloyd’s via QMC form 990

© Lloyd’s

Remember: We will adjust ECAs for year end exchange rates, movements in risk margins and RI CB changes for mid-year CiL

252525

Our mutual interest

Similar review process

Business as usual/live SII environment

Less time spent reviewing/addressing feedback

Fewer model changes or CPG loadings

Revised major model change process

Guidance amended to ensure an efficient process

Feedback from January workshop to be considered

No major changes in LCR submission planned

© Lloyd’s

262626

A way forward?

Deep dive reviews

To allow better understanding of agent model

Faster and more efficient review in September

More quantitative information on case-by-case basis

Syndicate capability oversight team to allow better engagement

No relaxation of regulatory requirement planned

BAU validation – 3 year plan for deep dive validation

Commerciality of the market will continue be the focus

Model drift

Lloyd’s Internal Model (LIM)

Syndicate specific information

LIM validation

© Lloyd’s

272727

Capital Results for 2017 YOA

© Lloyd’s

282828

Capital vs. exposure has increased

© Lloyd’s

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Economic Capital Assessment vs Gross Premium

Notes:For Active Syndicates ONLYGP: Gross Written Premium net of Special Purpose Arrangement premium.ECA: Excludes the reserve margin credits allowed in 2010/2011/2012.2009 / 2015/ 2016 YOA: GGP & ECA is as at mid-year coming into line (CIL)

Year of Account

ECA as a Percentage of

GP

292929

…and CPG loadings have increased

© Lloyd’s

YoA YoA

281

218

255

282

219

119

92

143

0

50

100

150

200

250

300

2010 2011 2012 2013 2014 2015 2016 2017

£m Ultimate Loading

23

12

17

33

26

19

17

21

-

5

10

15

20

25

30

35

2010 2011 2012 2013 2014 2015 2016 2017

No. of Syndicates

303030

Drivers of the movements

Review process: revised SCRs based on feedback on

Soft market/lower profitability

FX rate

Vendor model updates

Exposure change/other:

Mostly RI contract boundary change and changes to plan or RI (FX excluded)

CPG loadings/ULR loading:

Operational risk loadings relating to risk management and non modelling issues

Premium and reserve risk issues

ULR difference with plan

Other (late plan changes, model validation, etc.)

© Lloyd’s

313131

Detailed results

© Lloyd’s

323232

Results for 2017 YOA: user beware

LCR risks vs. exposure: an update from last year

Based on November 2016 CiL and November 2017 CiL data

Keep in mind the caveats / limitations

this is a partial selection of metrics

the exposure measures are not optimal

gaps/jumps may occur near the percentiles shown

excludes new syndicates

means are volume weighted

© Lloyd’s

333333

Results for 2017 YOA: user beware

Remember:

distance from the market mean is not a validation test

Common theme for 2017 YoA vs. 2016 YoA:

means / lower percentiles mostly stable

upper percentiles have increased for most cases

© Lloyd’s

343434

Ultimate SCR vs. net premium

© Lloyd’s

Ult SCR: F309

Net PI: F313 table 1 col D row 1

353535

Ultimate SCR vs. exposure (net premium + ½ net reserves)

© Lloyd’s

Ult SCR: F309

Exposure: Net PI + 0.5*Net Reserves

363636

Premium risk vs. net premium

© Lloyd’s

Ult premium risk (pre diversification): F309

Net PI: F313 table 1 col D row 1

373737

Reserve risk + risk margin vs. reserves

© Lloyd’s

Reserve risk (pre Diversification) F309

Risk margin: F312 col P total

Net Reserves: F312 cols H+I-J Total less Proposed YOA

383838

Market risk vs. available assets

© Lloyd’s

Market risk (pre Diversification): F309

Available assets: F312 col Q Total less Proposed YOA + F313 table 1 col D row 1

393939

RI credit risk vs. 1:200 recoveries

© Lloyd’s

RI credit risk (pre Diversification): F309

1:200 Recoveries (approximated): F311 table 1 col G row 4 less row 3

404040

Operational risk vs. net premium

© Lloyd’s

Operational risk (pre Diversification): F309

Net PI: F313 table 1 col D row 1

414141

SCR(1) vs. SCR(U) + RM

© Lloyd’s

Ult SCR and one year SCR: F309

Risk margin: F312 col P total

424242

0%

20%

40%

60%

80%

100%

120%

140%

On

e y

ea

r S

CR

/ (

Ult

ima

te S

CR

+ r

isk

ma

rgin

)

Syndicates

Market average

SCR(1) vs. SCR(U) + RM

© Lloyd’s

Expect morescrutiny here

434343

SCR(1) vs. SCR(U) + RM

© Lloyd’s

Note that the sample of syndicates for this graph is the submitted LCR, so excludes any syndicates based on the Lloyd’s syndicate benchmark model.

0%

20%

40%

60%

80%

100%

120%

140%

On

e y

ea

r S

CR

/ (

Ult

ima

te S

CR

+ r

isk

ma

rgin

)

Syndicates

Market average

2017 YoA

2016 YoA

444444

One year emergence

Greater scrutiny continued in 2016

CPG loadings: £178m one year vs. £143m ultimate (approx)

RI contract boundaries did not impact one year SCR

PRA continues to give close scrutiny

Lloyd’s approach on emergence patterns:

Mechanical approaches (high or low) not advisable

Provide justification if <70% or >90%

This is a challenging area…and an important one

© Lloyd’s

454545

Questions

© Lloyd’s

464646

This information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. It is the responsibility of any person publishing or communicating the contents of this document or communication, or any part thereof, to ensure compliance with all applicable legal and regulatory requirements.

The content of this presentation does not represent a prospectus or invitation in connection with any solicitation of capital. Nor does it constitute an offer to sell securities or insurance, a solicitation or an offer to buy securities or insurance, or a distribution of securities in the United States or to a U.S. person, or in any other jurisdiction where it is contrary to local law. Such persons should inform themselves about and observe any applicable legal requirement.

© Lloyd’s