14

When and How to Use Syndication to Issue Domestic Public Debt? Baudouin Richard Gemloc Peer Group Dialogue September 23, 2010

When and How to Use Syndication

to Issue Domestic Public Debt?

Baudouin Richard

Gemloc Peer Group Dialogue

September 23, 2010

2

• Current practice

• Rationale for using syndication for domestic currency

denominated issues

• Factors contributing to successful syndications

• Conclusion

Outline

3

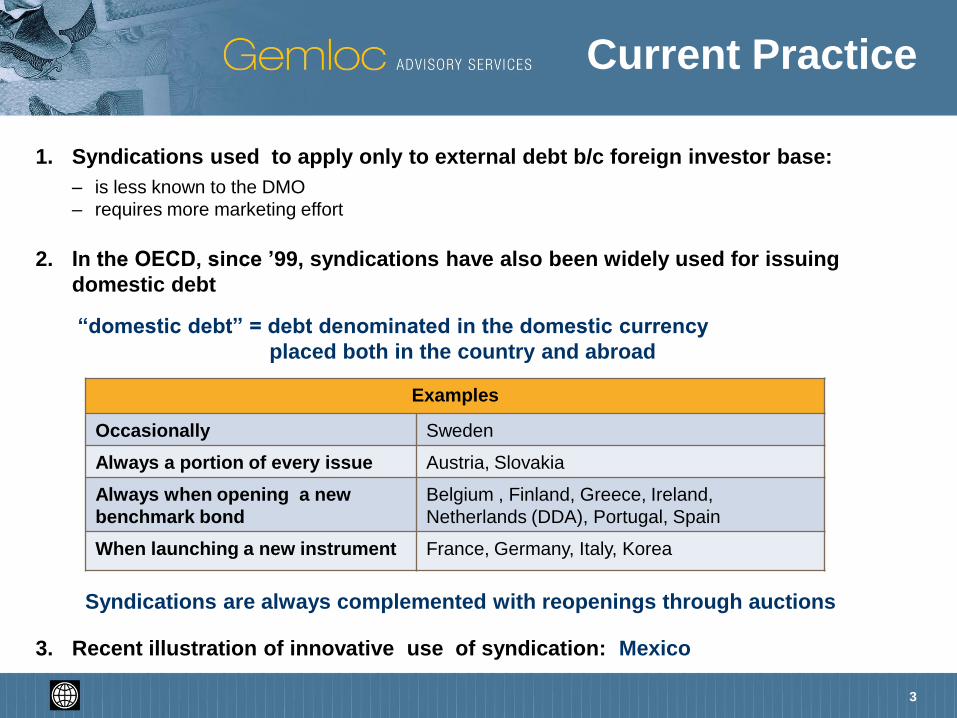

1. Syndications used to apply only to external debt b/c foreign investor base:

– is less known to the DMO

– requires more marketing effort

2. In the OECD, since ’99, syndications have also been widely used for issuing

domestic debt

“domestic debt” = debt denominated in the domestic currency

placed both in the country and abroad

3. Recent illustration of innovative use of syndication: Mexico

Current Practice

Examples

Occasionally Sweden

Always a portion of every issue Austria, Slovakia

Always when opening a new

benchmark bond

Belgium , Finland, Greece, Ireland,

Netherlands (DDA), Portugal, Spain

When launching a new instrument France, Germany, Italy, Korea

Syndications are always complemented with reopenings through auctions

4

Syndication:

• Achieves four things which an auction cannot do:

– Larger size

– Flexible timing

– Diversification of investor base

– Firm secondary market prices

• Has two ancillary benefits:

– DMO Marketing

– Strong PD motivation to perform

Rationale for

Domestic Market

5

A syndication allows to place larger amounts than does an auction

1. Investors are more attracted by syndications than by auctions

– Easier price discovery (book building)

– Lower risk of winner’s curse (uniform price)

– Better liquidity (larger size; balanced distribution)

– Expectation of (small) capital gain (firm secondary market prices)

2. PDs are more motivated to find buyers for the securities

– Commission

– League table

3. A syndication can be done when the timing is right

– (next slide)

Larger Size

6

A syndication can be done out of the auction issuance calendar

• When market conditions are right

• On a date chosen by the DMO at its discretion

Flexible Timing

7

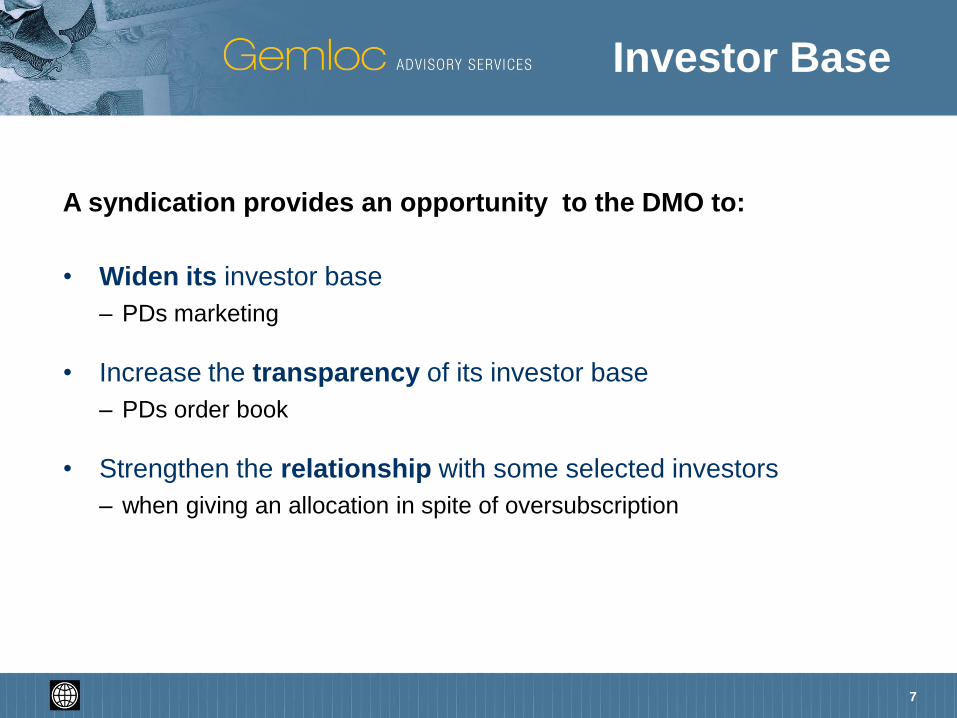

A syndication provides an opportunity to the DMO to:

• Widen its investor base

– PDs marketing

• Increase the transparency of its investor base

– PDs order book

• Strengthen the relationship with some selected investors

– when giving an allocation in spite of oversubscription

Investor Base

8

A syndication offers 2 opportunities for secondary market prices:

1. The appointment of lead managers makes a few designated PDs

specifically responsible for ensuring that prices stay firm during a

certain period.

– The ideal outcome is when an issue’s yield decreases 1 or 2 bps after

launch. When investors expect this to happen, their capital gain is not an

opportunity cost for the DMO.

2. The allocation of orders allows to strike the right balance amongst

holders of the security between traders and buy and hold investors.

Firm Secondary

Market Prices

9

1. Syndications are an opportunity to do road shows

– “Deal related road shows”

– Opportunity to advertise the country’s fundamentals and debt market

2. Syndications are widely reported in the press

– Opportunity to demonstrate the DMO’s expertise and professionalism

DMO Marketing

10

This applies when the DMO informs its PDs that :

1. The best performing PDs will be appointed as lead managers, all

other things being equal

– assuming equal degree of expertise in managing syndications

2. Membership to the syndicate is reserved for PDs

Strengthening

PDs’ Motivation

11

• Selection of lead managers

– Complimentary strengths

– Not too many

• Commissions

– DMO should pay going market rate

• Structure of the syndication

– Pot system for lead managers

– Strategic reserve for co-managers

– Full transparency to the DMO of PDs’ order book

• Investor Base

– DMO should play an active role in: o directing PDs where to look for orders

o allocating orders

Factors Contributing to

Successful Syndications

12

Syndications can be a powerful issuance instrument

Usual arguments for the use of syndication in emerging markets:

• Diversified investor base– Ability to attract either foreign investors or a varied group of domestic

investors that may not participate in regular auctions (e.g., pension funds,

mutual funds), or both

• Greater liquidity– Ability to place larger volumes of medium and long term bonds faster

• Improved price discovery– Ability to achieve price formation in markets where secondary market prices

are unreliable. Placing first tranche through a syndication gives participants a

clearer idea of how to price an issue in subsequent auctions.

Conclusion

Selected topics for discussion:

• Are syndications always valid for EMEs?

• Are there minimum prerequisites that need

to be considered?

13

Topics for

Discussion