REPORT T. Rowe Price INSIGHTS ON INVESTING AND FINANCIAL TOPICS Send us your comments, questions, and ideas: [email protected]Moderating risk Prospects for shiſting economic and financial conditions following the U.S. presidential election—including expectations for modestly higher inflation and interest rates and a possible redirection of U.S. trade policies—led the T. Rowe Price Asset Allocation Committee to make several tactical changes to its diversified multi-asset portfolios as 2016 ended. ese moves were designed to position for 2017 markets that may be more volatile than previously anticipated, particularly due to economic and policy risks that could prove challenging for non-U.S. dollar assets. We lowered the risk profile of our portfolios by reducing allocations to emerging market equities, thereby lessening risks related to foreign currencies and a potential U.S. shiſt toward more protectionist trade policies. A more expansionary U.S. fiscal policy could push inflation higher and increase the Fed’s tightening pace, leading to additional U.S. dollar appreciation and potential capital outflows from emerging markets. More broadly, we also have lowered our overweight to international equities versus U.S. stocks to neutral. However, expectations for somewhat faster U.S. growth and a generally supportive global economic environment should benefit credit-sensitive fixed income The Outlook for 2017: Some Caution in Order sectors, such as high yield bonds. e reflationary implications of looser U.S. fiscal policy also should increase the relative attractiveness of assets that offer some built-in protection against higher interest rates and rising inflation, such as floating rate bank loans and Treasury inflation protected securities. Stocks versus bonds Against this background, we remain neutral on stocks relative to bonds. Equity valuations are above historical averages and profit margins are declining—although earnings growth is showing signs of improvement aſter several negative quarters. Within fixed income, rising U.S. interest rates are a potential headwind as low yields provide only a modest buffer against rising rates (although we still expect the pace of Fed tightening to be gradual). Other asset allocation positions at the beginning of 2017 include: favoring global equities over real assets equities, U.S. growth stocks over U.S. value stocks, non-U.S. value stocks over non-U.S. growth stocks, high yield bonds over U.S. investment-grade bonds, and an underweight to non-U.S. dollar bonds. e committee’s tactical portfolio positions are relative to its long-term strategic neutral allocations across asset allocation portfolios. ■ Diversification cannot assure a profit or protect against loss in a declining market. BY CHARLES SHRIVER, PORTFOLIO MANAGER FOR THE GLOBAL ALLOCATION, BALANCED, SPECTRUM, AND PERSONAL STRATEGY FUNDS ISSUE NO. 131 WINTER 2017 2 Global Economics: Growth and Uncertainty 4 Global Equities: Earnings Growth Key 6 U.S. Equities: Good Outlook but Risks 8 EM Equities: Pockets of Growth 9 Global Fixed Income: Politics Dominate 12 EM Bonds: Favor USD Sovereigns 13 New Fund: Beyond Core Sectors 14 Personal Finance: Rebalancing and Volatility 16 Last Word: Women and Retirement QUARTERLY PERFORMANCE UPDATE 17 Equity Market Review Fixed Income Market Review Fund Performance Tables

Transcript

REPORTT. Rowe Price

I N S I G H T S O N I N V E S T I N G A N D F I N A N C I A L T O P I C S

Moderating risk Prospects for shifting economic and financial conditions following the U.S. presidential election—including expectations for modestly higher inflation and interest rates and a possible redirection of U.S. trade policies—led the T. Rowe Price Asset Allocation Committee to make several tactical changes to its diversified multi-asset portfolios as 2016 ended.

These moves were designed to position for 2017 markets that may be more volatile than previously anticipated, particularly due to economic and policy risks that could prove challenging for non-U.S. dollar assets.

We lowered the risk profile of our portfolios by reducing allocations to emerging market equities, thereby lessening risks related to foreign currencies and a potential U.S. shift toward more protectionist trade policies.

A more expansionary U.S. fiscal policy could push inflation higher and increase the Fed’s tightening pace, leading to additional U.S. dollar appreciation and potential capital outflows from emerging markets. More broadly, we also have lowered our overweight to international equities versus U.S. stocks to neutral.

However, expectations for somewhat faster U.S. growth and a generally supportive global economic environment should benefit credit-sensitive fixed income

The Outlook for 2017: Some Caution in Order

sectors, such as high yield bonds. The reflationary implications of looser U.S. fiscal policy also should increase the relative attractiveness of assets that offer some built-in protection against higher interest rates and rising inflation, such as floating rate bank loans and Treasury inflation protected securities.

Stocks versus bondsAgainst this background, we remain neutral on stocks relative to bonds. Equity valuations are above historical averages and profit margins are declining—although earnings growth is showing signs of improvement after several negative quarters.

Within fixed income, rising U.S. interest rates are a potential headwind as low yields provide only a modest buffer against rising rates (although we still expect the pace of Fed tightening to be gradual).

Other asset allocation positions at the beginning of 2017 include: favoring global equities over real assets equities, U.S. growth stocks over U.S. value stocks, non-U.S. value stocks over non-U.S. growth stocks, high yield bonds over U.S. investment-grade bonds, and an underweight to non-U.S. dollar bonds.

The committee’s tactical portfolio positions are relative to its long-term strategic neutral allocations across asset allocation portfolios. ■

Diversification cannot assure a profit or protect against loss in a declining market.

BY CHARLES SHRIVER, PORTFOLIO MANAGER FOR THE GLOBAL ALLOCATION, BALANCED, SPECTRUM, AND PERSONAL STRATEGY FUNDS

ISSUE NO. 131 WINTER 2017

2 Global Economics: Growth and Uncertainty

4 Global Equities: Earnings Growth Key

6 U.S. Equities: Good Outlook but Risks

8 EM Equities: Pockets of Growth

9 Global Fixed Income: Politics Dominate

12 EM Bonds: Favor USD Sovereigns

13 New Fund: Beyond Core Sectors

14 Personal Finance: Rebalancing and Volatility

16 Last Word: Women and Retirement

QUARTERLY PERFORMANCE UPDATE

17 Equity Market Review

Fixed Income Market Review

Fund Performance Tables

2

ISSUE NO. 131 WINTER 2017

UncertaintiesThe pace of global economic growth has accelerated meaningfully since its trough in the spring of 2016. The improvement in the momentum of global growth has been relatively broad-based and driven by looser global financial conditions and the delayed impact of Chinese stimulus measures taken early in 2016. Additionally, growth has benefited from a slowing in the pace of inventory liquidation and the stabilization in commodity prices.

As the impact of stimulus in both China and the developed world fades in early 2017, we expect global growth to slow a bit from its peak in late 2016. The global economic outlook also has grown more uncertain due to the rising wave of populism in developed markets, which may lead to stronger growth through greater fiscal support in some regions while threatening progress in others.

As economic conditions have improved, uncertainty about the future stance of global monetary policy has increased. The assumption that the Fed will restrict itself to two or three interest rate increases in 2017 has been challenged by the prospect of increased fiscal stimulus under the incoming Trump

administration. A wave of stimulus accompanied the first years of the Obama, Bush II, and Reagan administrations. But, in each case, fiscal expansion came against a background of substantial slack in the U.S. economy. How inflation will respond to stimulus when the economy is near full employment is unclear, as is the Fed’s likely reaction.

Financial markets also are adjusting to the reality that the European Central Bank (ECB) has started to implement a less accommodative monetary policy stance. There is no evidence that core inflation in Europe is rising significantly, but rising energy prices mean that headline inflation is poised to bounce in early 2017. As announced in the December meeting of the ECB’s monetary policy committee, the process of normalization has taken the form of a slowing of the pace of quantitative easing (QE). The question about further tapering of the QE program is likely to provoke fierce debate among ECB policymakers.

Asian economies have a similarly indeterminate policy outlook. In September 2016, the Bank of Japan made a substantial change to its monetary program, announcing that it would adjust its QE purchases in order to target stable and positive longer-term yields. The new program remains unproven, but it may help the bank control the appreciation of the yen, which has weighed heavily on the Japanese economy.

Meanwhile, China is wrestling with rising corporate debt loads, especially for state-sponsored firms, and the need to manage an increasing stock of nonperforming loans in its banking system. The fiscal spigots that helped stabilize the economy early in 2016 are likely to remain open as the top leadership in the Politburo Standing Committee undergoes a transition. The other major emerging markets appear to be continuing to go through a relatively orderly deleveraging process as they digest the lending boom that developed on the back of the very loose monetary policy stance in the developed economies.

PopulismLate 2016 saw the headwinds of emerging market deleveraging—which have been evident for some time—joined by the crosswinds of developed market populism. Britain’s decision to

GLOBAL ECONOMICS

Growth Higher but so Are Uncertainties About Global Monetary PoliciesThe crosswinds of developed market populism could have a major impact on global growth.

BY ALAN LEVENSON, CHIEF U.S. ECONOMIST, AND NIKOLAJ SCHMIDT, CHIEF INTERNATIONAL ECONOMIST

KEY POINTSρ Global growth has picked up meaningfully since its

trough in early 2016, but the boost from stimulus is likely to fade a bit in 2017.

ρ Central bank policy has become harder to predict now that growth has picked up, and higher oil prices are likely to cause a bounce in headline inflation.

ρ China’s political transition is likely to keep the fiscal spigots open, but other major emerging markets appear to be going through an orderly deleveraging process.

ρ A populist wave in developed markets has further complicated the global outlook, increasing the possibility that growth will be either much slower or faster than envisioned in our base-case scenario.

The assumption that the Fed will restrict itself to two or three interest rate increases in 2017 has been challenged by the prospect of increased fiscal stimulus under the incoming Trump administration.

3T R O W E P R I C E . C O M

Figure 1 Global Economy Picked Up in Early 2016Composite Purchasing Managers’ Indices

Sources: IHS Markit, J.P. Morgan, and Haver Analytics.

Com

posi

te P

urch

asin

g M

anag

ers’

In

dex

Leve

ls

48

50

52

54

56

58

11/16

6/16

12/15

6/15

12/14

6/14

12/13

6/13

12/12

6/12

12/11

6/11

Emerging MarketsDeveloped MarketsGlobal

leave the European Union (EU) and Donald J. Trump’s election as U.S. president both reflected a broader pattern of disaffection in developed economies, fed by widening inequality and a growing sense that the benefits of economic growth are not trickling down to the middle class. The uneven distribution of the wealth and income generated by globalization is pushing voters to search for new champions.

How far this populist wave will travel in 2017, particularly in Europe, remains unclear, but it could have major impacts on global growth. Although Austria’s far-right Freedom Party was unable to take the presidency in a runoff in early December 2016, electoral gains seem likely in 2017 for similar parties in France, Italy, Germany, Greece, and the Netherlands. An uncertain political environment is likely to encourage corporate managers and investors to defer irreversible decisions.

Concerns also have deepened about the possibility of a so-called hard Brexit. Whether British Prime Minister Theresa May will be able to follow through with her promise to begin the formal process of withdrawal from the EU by the end of March is unclear, as the roles of the High Court and Parliament are still not fully settled. Ms. May and her political circle have sent conflicting signals over their willingness to sacrifice access to the customs union and the single European market in order to maintain control over immigration.

A hard Brexit would have a widespread impact, but we would expect it to weigh most immediately and forcefully on the British pound. The Bank of England might respond with lower rates and an extension of its QE program in order to protect the economy—even as the weaker pound has raised inflationary pressures in the UK.

Trump’s electionU.S. populism is taking a different form and will have disparate effects on the U.S. economy. Central elements of Mr. Trump’s economic plan include a pro-growth tax plan; a new modern regulatory framework, including an unleashed energy sector; and an “America-first” trade policy. Swift action is conceivable in some areas.

Reforming and simplifying the personal and business tax codes could boost growth even before taking into account any reduction in effective tax rates. Improvements in regulatory frameworks also could increase economic dynamism, and cutting taxes, along with deregulation, likely would support the economy.

In contrast, a trade agenda emphasizing tariffs or penalties for U.S. multinational firms producing abroad would be a headwind for growth, disrupting supply chains and raising the prices of imported goods. More aggressive immigration enforcement also could have a negative economic impact, creating labor shortages in industries and states with high concentrations of unlawful immigrants, which would raise U.S. wage costs and depress economic growth.

The U.S. Congress may not share Mr. Trump’s willingness to risk trade wars, but it is worth noting that under the Trade Act of 1974, the president has the executive authority to withdraw from trade agreements and to impose import tariffs of up to 15% for up to 150 days, without consulting Congress.

The prospects for fiscal stimulus and deregulation on the one hand and heightened trade frictions on the other have increased the risk of extreme, or “tail,” outcomes for the U.S. economy in 2017. While the political whirlwind of 2016 has not changed our base-case scenario of a U.S. growth rate of roughly 2%, we believe that investors should be prepared for the possibility that growth will be significantly faster or slower—a caution that also applies to the overall global economy. ■

While the political whirlwind of 2016 has not changed our base-case scenario of a U.S. growth rate of roughly 2%, we believe that investors should be prepared for the possibility that growth will be significantly faster or slower—a caution that also applies to the overall global economy.

4

ISSUE NO. 131 WINTER 2017

KEY POINTSρ Earnings prospects are improving in both developed

and emerging equity markets, although recent political referendums and elections could create market uncertainty.

ρ Expectations for somewhat faster global growth could continue to drive a rotation from defensive to cyclical and financial stocks.

ρ Equity investors appear to believe that the Trump administration will pursue more aggressive fiscal stimulus. However, policy details are unclear.

ρ A gradual rise in U.S. interest rates should not threaten global equity markets. The recovery in emerging equities appears strong enough to withstand moderate U.S. dollar appreciation.

GLOBAL EQUITIES

Earnings Growth, not Politics, Is Central to the 2017 Equity OutlookThe global consumer, health care, and technology sectors appear poised for earnings acceleration in 2017.

BY ROB SHARPS, CO-HEAD OF GLOBAL EQUITY, AND CHRIS ALDERSON, CO-HEAD OF GLOBAL EQUITY

Improved foundationsWhile Donald J. Trump’s election as U.S. president has captured the attention of analysts and investors worldwide, we believe global equity performance in 2017 is more likely to hinge on the prospects for a broad earnings recovery from the currency and commodity-related downturn of the past two years.

The foundations for an improved global earnings environment in 2017 appear to be in place:

ρ Forward earnings forecasts for the energy and materials sectors have turned sharply positive, reversing the drag on broader earnings from those two sectors over the past two years.

ρ Key emerging market currencies have stabilized and inflation pressures are lessening, allowing emerging markets central banks to ease monetary policy to spur growth. Nascent economic recoveries are underway in several major emerging markets (such as Brazil and Russia) hard hit by commodity price declines.

ρ Aggressive quantitative easing by the European Central Bank (ECB) and the Bank of Japan (BoJ) has reduced the risk of broad price deflation, reducing the headwinds to earnings.

ρ The global consumer, health care, and technology sectors—which continued to grow through the commodity-related profits recession—also appear poised for earnings acceleration in 2017.

ρ Major U.S. and Japanese companies continue to commit cash to share buyback programs, enabling earnings per share (EPS) to grow faster than both net earnings and revenue.

Durable recoveryDespite the post-U.S. election bond market sell-off, developed world yields remain quite low by historical standards. Past rate cycles suggest that when yields rise from relatively low levels—below 5% on the 10-year Treasury note—the impact on equities can be benign as investors also begin to anticipate faster economic and earnings growth.

Moreover, while market expectations for interest rates hikes by the U.S. Federal Reserve also have risen, we believe the Fed will continue to tighten slowly and incrementally.

These scenarios suggest an environment in 2017 in which rising interest rates and rising equity markets can peacefully coexist as long as economic growth is positive and inflationary pressures remain moderate, which is still our base case. Globally, the ECB and BoJ both are likely to remain accommodative, while many emerging market central banks will look to ease policy—although they may be wary of the risk of faster U.S. dollar appreciation.

Within the context of expected earnings acceleration, equities appear fairly valued to us by most measures in most markets and relatively attractive in Japan and the emerging markets. (See Figure 1.) Here again, historically low developed market bond yields should remain supportive of valuations.

Regional outlooksU.S. equities have generally outperformed other developed markets since the end of the 2008–2009 global financial crisis and emerging markets equities since early 2013. We expect this trend to persist into 2017, but with the U.S. advantage narrowing:

ρ United States: The third quarter of 2016 saw modestly positive year-over-year EPS gains for the S&P 500 companies, ending the string of EPS declines that started in the second quarter of 2015. We expect earnings momentum to accelerate in 2017, with EPS growth in the mid- to high-single digits possible.

ρ Developed Europe: Europe’s economic recovery appears on track, sustained by export demand, a return to growth in key peripheral countries, and the ECB. However, the political risks to monetary union can’t be dismissed.

ρ Japan: Earnings held up surprisingly well in 2016, despite yen appreciation. An acceleration in global growth should

be supportive in 2017. We also are impressed by the governance reforms that are making Japanese firms more mindful of shareholder value. Dividend payouts and share buybacks have risen sharply, and that likely will continue.

ρ China: The rebalancing from investment and exports to consumption and services appears on track. And with almost $3.5 trillion in foreign exchange reserves, Beijing should be able to prevent destabilizing yuan depreciation. Domestic credit imbalances, while substantial, appear manageable. However, confidence in China’s equity markets remains fragile.

ρ Other emerging markets: Key commodity-producing economies, such as Russia and Brazil, are in recovery, while India could see economic growth of 7% or more in 2017. Given this momentum, we do not expect higher U.S. interest rates or U.S. dollar appreciation to derail the emerging markets recovery.

“Trump rotation”Mr. Trump’s victory suggests that economic growth and inflation could move higher in the United States and across the globe, as he is widely expected to propose major tax cuts and increases in federal infrastructure spending. However, key policy details remain uncertain.

Initially, the election results gave a strong push to a trend already visible before the election: a shift away from defensive utility, telecommunications, and consumer growth stocks and toward more cyclical industries. However, investors are still trying to assess the potential impact of Mr. Trump’s program on specific sectors:

ρ Financials: Higher interest rates and a steeper yield curve are positive for net lending margins. Mr. Trump has

promised to roll back some financial regulations imposed after the 2008–2009 financial crisis. Some analysts believe the Department of Labor may delay or revise rules imposing stricter fiduciary standards on brokers and advisors who sell financial products to retirement accounts.

ρ Health care: Voters in California rejected a ballot initiative that would have required the state to negotiate for lower drug prices. Mr. Trump’s promise to repeal the Affordable Care Act could be negative for hospitals, device manufacturers, and other providers that benefited from increased health spending under the act.

ρ Technology: Many large technology companies sold off following the U.S. election as investors became more mindful of tech valuations. However, the rotation toward cyclicals already has brought tech valuations more in line with the broad market.

ρ Industrials: Higher federal infrastructure spending could boost demand for heavy equipment and other industrial goods. But possible tariffs or other trade barriers, as well as the potential for U.S. dollar appreciation if Mr. Trump’s fiscal program is seen as inflationary, could squeeze operating margins for U.S.-based manufacturers.

ρ Energy: Mr. Trump has said he wants to open up more federal land to exploration and withdraw from the Paris Climate Agreement, measures widely backed by energy producers. However, if his proposals eventually boost oil, gas, and coal production, they could contribute to global oversupply, putting downward pressure on prices and profits.

Restrained expectationsDeveloped market economies continue to struggle with growth, as evidenced by recent referendums and elections, raising expectations of fiscal stimulus in many countries.

But global equity markets appear poised for an earnings recovery in 2017, led by a return to growth in the sectors and regions hardest hit by the steep declines in energy and commodity prices. Faster U.S. growth, improved operating results in Europe, and an easing of deflationary pressures in Japan also should support a cyclical upturn.

However, investors should keep expectations in check. Large deficits and debt burdens appear to leave only limited room for fiscal stimulus in most developed economies, including the United States. While some emerging economies have room for fiscal stimulus, most are still focused on reforms that reduce public spending. Under these circumstances, we are cautious about pursuing the “Trump rotation” too aggressively, especially among lower-quality cyclical stocks. ■

All investments are subject to market risk, including the potential loss of principal. Non-U.S. securities are subject to the unique risks of international investing, including currency fluctuation. Past performance cannot guarantee future results.

6

ISSUE NO. 131 WINTER 2017

FundamentalsU.S. equity investors entered the year with even more uncertainty than usual. But as indicated by the postelection market rally, the fundamental environment for equity investing could remain favorable.

President-elect Donald J. Trump’s plans to reduce taxes, moderate regulations, and increase infrastructure investment are all potentially supportive of stronger economic growth and better corporate earnings, particularly for such sectors as industrials, financials, and health care.

However, it’s far from certain how successful the Republican leadership will be in enacting and implementing these policies. How long it would take for these steps to have a positive impact, if at all, also is not clear.

Key risks include possible renegotiation of key trade agreements, resulting in higher tariffs or other trade frictions. Also, if federal spending increases and tax cuts are not offset by spending cuts or a revitalized economy, concerns about inflation, rising deficits, and ballooning national debt will move to the forefront.

A bearish scenario ultimately could come about if, after several years, the government has not stimulated much growth in the economy—at the costs of growing trade tensions, more federal borrowing, higher deficits, and sharply rising interest rates.

However, we don’t expect that outcome, and overall there are reasons for an optimistic market outlook. If the Republican-led

government can execute its initiatives skillfully, there is a reasonable chance for acceptable and perhaps even above-average U.S. equity returns over the next 18 to 36 months.

As 2017 opened, U.S. stock valuations, on average, were reasonable by almost any measure. Growth stocks were selling at a lower-than-average premium to cyclical, value-oriented stocks, particularly among the larger companies.

Interest rates should continue to move higher over the next couple of years, with short-term rates perhaps reaching 2% and longer-term rates around 5%. History has shown that rising rates did not derail the case for equities if accompanied by an improving economy. In periods of rising rates since the early 1990s, as long as the 10-year Treasury yield remained below 5%, the market still performed reasonably well. (See Figure 1.)

Meanwhile, the S&P 500 Index’s dividend yield remains attractive relative to current interest rate levels, even with the sharp rise in rates following the election.

Corporate earnings, which had contracted for five consecutive quarters through June 2016, should continue a recovery that started in the third quarter of 2016—particularly if there is corporate tax reform and infrastructure investment expands.

Wall Street estimates call for a 11.9% gain in S&P 500 earnings in 2017 and 5.6% growth in revenue as the energy sector becomes less of a drag. Now, energy companies are slowly recovering and are likely to improve their margins and profitability.

Nevertheless, investors should keep in mind that, even with tax cuts, less regulation, and more infrastructure spending, expectations for cyclical improvement in the economy could be too optimistic.

Period*Treasury Starting

Yield

Treasury Ending Yield

Yield Increase

Annualized S&P 500 Return

9/30/93– 11/30/94 5.40% 7.91% 251 bps** -1.00%

12/31/95–8/31/96 5.58 6.96 138 8.90

9/30/98–1/31/00 4.44 6.68 224 26.70

5/31/03–6/30/06 3.37 5.15 178 9.40

12/31/08– 12/31/09 2.25 3.85 160 23.50

7/31/12–12/31/13 1.51 3.04 153 22.90

Figure 1 Stocks Usually Have Gained With Rising Rates10-Year Treasury Yields and S&P 500 Performance

*Periods of rising rates since the early 1990s. **A basis point (bps) is 1/100th of 1%. Past performance cannot guarantee future results. Source: Strategas Reseach Partners.

U.S. EQUITIES

Favorable Outlook for Equities Tempered by Policy UncertaintiesFocus on all-season growth companies with durable earnings and free cash flow growth.

BY LARRY PUGLIA, MANAGER OF THE BLUE CHIP GROWTH FUND

KEY POINTSρ President-elect Donald J. Trump’s plans to cut taxes, lessen

regulations, and promote infrastructure investment could boost U.S. corporate earnings and the economy.

ρ The fundamental backdrop for U.S. equity investing should remain favorable.

ρ Potential protectionist policies and higher federal deficits, along with geopolitical tensions, pose key risks.

7T R O W E P R I C E . C O M

Sector opportunities

We believe the best opportunities for earnings growth are in the large-cap growth area, particularly in these sectors:

ρ Within health care, certain biotechnology companies are innovating and have had rapid revenue growth. There also are attractive opportunities among medical device companies and managed care companies.

ρ In the technology sector, we remain optimistic about such dominant firms as Google, Facebook, and Microsoft. Select companies generating sustainable or recurring service revenue are attractively valued, while those participating in the growth of cloud computing and social networking should achieve strong secular growth. Companies manufacturing semiconductors used in autonomous driving and touchless payments could see brisk growth. ρ Several technology companies had setbacks after the election given the view that the Trump administration could hurt the sector with harmful trade and immigration policies, supply chain disruptions, and possibly antitrust actions. However, we don’t consider this the most likely outcome. ρ The financials sector has improved on expectations for less regulation and a steepening yield curve (longer-term rates increasing more relative to short-term rates, which boosts bank profits). Those factors could drive earnings improvements.

ρ Strong consumer discretionary stocks should continue compounding good earnings and likely would benefit if tax cuts put more money in people’s pockets.

Given U.S. political uncertainties, investors should focus on the time-tested process of investing in companies with durable earnings and free cash flow growth—and not be too swayed by postelection expectations.

Many of these high-quality companies have low levels of debt and tend to pay high tax rates, so they would benefit from corporate tax reform. In these times, owning all-season growth companies that can do well in most environments makes sense.

Of course, investors also should be mindful of the risks. In addition to those from possible unfavorable policy outcomes, concerns over lackluster global growth and possible economic dislocation from Brexit still loom, as well as myriad geopolitical tensions. If the surge in the dollar persists, it could have a negative effect on U.S. competitiveness and growth and undermine profits for multinational companies, which derive a significant portion of their revenue from abroad.

Last, this bull market, which began in March 2009, has surpassed the average bull market in return and duration. Market strength over the past few years tempers the amount of potential appreciation. (See Figure 2.)

So investors should maintain a healthy dose of skepticism not seen in the postelection rally and have modest expectations. At the same time, an improving earnings trend, pockets of strong growth opportunities, and possibly better economic performance could produce another good year for U.S. equity investors. ■

All investments are subject to market risk, including the potential loss of principal. As of Dec. 31, 2016, Facebook and Microsoft made up 8.1% of the Blue Chip Growth Fund; it did not own shares of Google.

Figure 2 The Current U.S. Bull Market Versus HistoryThe U.S. bull market—as measured by the S&P 500 Index of large-cap stocks from March 9, 2009, through the end of 2016—has persisted longer than the average U.S. bull market going back to the 1930s and delivered better-than-average returns. Excluding the current bull market, U.S. bull markets since the 1930s have averaged a duration of 57 months and returns of 164.5%.

Source: Strategas Research Partners.

Bull Market Duration in Months20 40 60 80 100 120

0

100

200

300

400

500%

1966–19681970–1973

1942–1946

2002–2007

1982–1987

1932–1937

1962–19661957–1961

1974–1980

1949–19562009–Present94 months, 231% return

Average

1990–2000

1987–1990

Cum

ulativ

e Bu

ll Mar

ket R

etur

ns (I

ndex

Pric

e)

8

ISSUE NO. 131 WINTER 2017

EM EQUITIES

Better Growth and Earnings Spell Good Outlook for Emerging MarketsBut U.S. political uncertainties and rising rates pose potential headwinds for EM stocks.

BY GONZALO PÁNGARO, MANAGER OF THE EMERGING MARKETS STOCK FUND

Stabilized growthEmerging markets (EM) stocks enjoyed strong performance in 2016 with better economic growth and improving corporate earnings. In the near term, however, market volatility may continue given several top-down concerns, particularly U.S. political uncertainties.

Overall, the outlook for emerging markets equities in 2017 remains good. Economic growth relative to developed markets has stabilized. And the EM growth premium is again expanding as the larger economies of Brazil and Russia, which have been suffering tough recessions, are now showing signs of turnarounds.

Meanwhile, Asia’s economies are robust. India is a great example of a country making hard reforms now to maintain its future prospects.

China’s economy, however, continues to slow. But a growth slowdown should not be confused with a growth crisis, in our view. China ultimately has the ability and willingness to apply policy action that will prevent its economic and debt dynamics from becoming disorderly.

Corporate earningsBeyond China, economic growth for emerging markets as a whole is again advancing—a healthier environment for corporate earnings.

Last year marked a turnaround in earnings for emerging markets after a number of years in the doldrums. Some of this was helped by the revival in commodities, but we also have increasingly seen many more examples of self-help within companies focusing on cost control, capital expenditure efficiency, and improved returns.

Margins in most emerging countries remain below historical averages, but better growth and more disciplined cost management can help them recover, and there already are tentative signs of this. Importantly, for the first time in five years, productivity is increasing at a faster pace than real wages in some key markets.

Overall, emerging markets valuations still look attractive. They remain at a discount relative to developed markets, particularly on a price-to-book basis. Valuations on a price-to-earnings basis are a bit more varied, with some sectors, such as consumer staples and health care, slightly above their long-term averages.

What to watchOne of the main headwinds facing emerging markets investors in 2017 is the potential impact of the Trump administration’s policies. Mr. Trump’s election immediately caused volatility in emerging market equities. If he follows through on his protectionist rhetoric, trade could be damaged.

Most likely the administration will pursue a pro-growth agenda that will include lower taxes, reduced regulation, and infrastructure spending. These measures could pull global economic growth higher, helping emerging markets.

The question is whether developing markets will be allowed to participate, given Mr. Trump’s trade threats. We expect he will embrace a more practical agenda.

Another headwind: After many years, we finally are seeing change in the trajectory of U.S. interest rates, and higher interest rates are resurrecting some of the concerns for emerging markets about lower capital flows and weaker currencies.

However, most emerging market countries are in much better positions to weather what should be modest increases in U.S. rates. We would only be concerned if we saw a dramatic and accelerated rise in U.S. rates.

Despite these concerns, emerging markets present very interesting pockets of growth that are hard to find in the slower-growing developed markets. The prospects for these markets, particularly over the medium and long term, are attractive. ■

Emerging market investments are particularly subject to market, currency, political, and economic risks, as well as the risk of abrupt and severe price declines.

...emerging markets present very interesting pockets of growth that are hard to find in the slower-growing developed markets.

9T R O W E P R I C E . C O M

Figure 1 Global Monetary Expansion PersistsCentral Bank Balance Sheet Growth

*China data only through 11/16. Source: T. Rowe Price.

U.S

. Bill

ion

Dol

lar E

quiv

alen

ts

0

1,000

2,000

3,000

4,000

5,000

$6,000

12/15

12/14

12/13

12/12

12/11

12/10

12/09

12/08

12/07

12/06

12/05

12/04

12/03

12/02

12/01

12/00

EurozoneU.S.JapanChina*

12/16

GLOBAL FIXED INCOME

Political Developments Continue to Dominate World Bond MarketsThe Trump administration’s policies will be the most important factor for global bonds in 2017.

BY MARK J. VASELKIV, MANAGER OF THE HIGH YIELD FUND AND CO-MANAGER OF THE GLOBAL HIGH INCOME BOND FUND

KEY POINTSρ Donald J. Trump’s election as U.S. president has raised

the prospect of U.S. tax cuts, increased spending, and higher growth and inflation.

ρ This could lead to higher U.S. yields, while yields in most of the rest of the world could remain low.

ρ Emerging markets may be hit hardest by higher U.S. yields, while Europe faces a year of uncertainty as a series of elections tests the extent of growing anti-establishment sentiment.

ρ U.S. floating rate loans and high yield bonds may offer the best value, but it will pay to adopt a prudent approach overall, focusing on selective, high-conviction positions.

Dramatic sell-offDonald J. Trump’s victory in November’s U.S. presidential election led to a dramatic sell-off in fixed income amid anticipation that his proposed infrastructure spending, tax cuts, and regulatory reforms will lead to higher U.S. growth and inflation. Yields on U.S., UK, German, and Japanese government debt rose from record lows, wiping out more than $1 trillion from global bond markets as the dollar surged and U.S. equities rallied.

In 2017, political developments will continue to dominate bond markets—not just in the United States, where there is a question of whether the new president can deliver on his campaign promises, but also in Europe, where elections will gauge the extent to which populist forces are a threat to the established order. The heightened uncertainty necessitates a cautious approach to fixed income, with highly selective country, sector, and currency positioning.

The impact of the Trump administration’s policies on the U.S. economy will not be the only factor influencing global fixed income markets in 2017, but it likely will be the most important one: The

U.S. bond market is the deepest and most liquid in the world, and anything that happens there will inevitably have a major impact elsewhere.

Mr. Trump’s pledges to spend $1 trillion on infrastructure and cut taxes are expected to lead to higher growth and inflation. However, the U.S. economy is already healthy and is getting stronger, with the unemployment rate below 5%. Prices and wages were rising prior to the election; any further stimulus that Mr. Trump injects is likely to further increase inflationary pressures.

Meanwhile, the Fed is expected to make two or three interest rate hikes this year. If inflation picks up quicker than expected, the Fed could come under pressure to hike more aggressively, although the weak global economic environment may lead to a more restrained approach. But even a relatively modest cycle of rate hikes would differentiate the United States from much of the rest of world, where historically low rates persist.

The monetary policies that created this situation are reaching the end of their useful life. Debt levels on central banks’ balance sheets have risen to enormous proportions (see Figure 1), and political patience with accommodative monetary policy is wearing thin as it has notably failed to deliver the desired growth. However, we continue to expect yields in most developed markets outside the United States to remain low for some time to come.

Japan and EuropeThe Bank of Japan has stated its intent to anchor its sovereign rates through “yield curve control.” Essentially, this will involve using targeted quantitative easing to keep 10-year government bond yields at zero, thereby maintaining a steep yield curve (as Japanese short-term bond rates are negative). Steeper yield curves typically increase profits for banks, which in turn leads to greater

continued on page 10 >

10

ISSUE NO. 131 WINTER 2017

economic activity and inflation. However, the Bank of Japan’s move is expected to only have an incremental impact on the sluggish Japanese economy.

Yields in Europe also likely will remain low as the Continent navigates a year of political uncertainty amid a backdrop of growing anti-globalization sentiment. The Netherlands’ Freedom Party, France’s National Front, and Germany’s Alternative for Germany will compete in their respective nations’ general elections. While none are expected to win, the populist forces they represent could cause considerable turbulence.

Overall, Europe looks likely to register moderate growth in 2017. And while the European Central Bank will slow the pace of its monthly corporate bond purchases, we do not expect this to lead to a significant spike in yields given an absence of inflation pressures.

Emerging marketsPrior to the U.S. election, emerging markets were well positioned coming into 2017. Local currencies had stabilized, inflation had come down, and central banks were either lowering rates or tightening less aggressively.

However, Mr. Trump’s victory—and the expectation that it will mean higher U.S. rates and a stronger dollar—changed that. Emerging market bonds sold off sharply following the election, and the signs are that the “Trump tantrum” will not end soon. A stronger dollar will make it more expensive for overseas borrowers to service their debt commitments and may lead to capital outflows as money rapidly returns to U.S. markets.

It is possible that last fall’s deal struck by the Organization of Petroleum Exporting Countries (OPEC) to cut oil production will benefit emerging markets, particularly Brazil and Mexico, by putting a floor under oil prices. Before the agreement, the prospect of a continued oversupply of oil was a significant headwind for emerging markets as it threatened to keep the price of a barrel below $45. If the deal holds, however, the price may settle at a higher range in the first half of 2017.

After that, the benefits of the deal for emerging markets fades as the higher price may simply encourage more drilling in the United States and other non-OPEC members. Overall, any opportunities to invest in emerging market debt are likely to be more tactical than strategic in nature.

Best valuesIn this challenging environment, it pays to consider the full range of the fixed income universe. Figure 2 shows how fixed income sectors have responded when U.S. Treasury yields have risen by 1% or more. Floating rate bank loans, for example, have performed well in these periods as their coupon rates reset regularly—an

Bloomberg Barclays U.S. Corporate Investment Grade Bond Index

Bloomberg Barclays U.S. Aggregate Bond Index

J.P. Morgan CEMBI Broad Index

J.P. Morgan Emerging Markets Bond Index Global

J.P. Morgan Global High Yield Index

S&P/LSTA Performing Loan Index

Figure 2 Bond Market Returns in Periods When Treasury Yields Rose by 100 Basis Points*Not All Sectors Have Followed the Same Pattern With Rising Rates

*A basis point (bps) is 1/100th of 1%. Past performance cannot guarantee future results. Source: T. Rowe Price.

A stronger dollar will make it more expensive for overseas borrowers to service their debt commitments and may lead to capital outflows...

continued from page 9 >

11T R O W E P R I C E . C O M

advantage over fixed rate bonds in rising-rate environments. We expect floating rate loans to perform well this year.

U.S. high yield bonds also appear well positioned for positive returns in 2017. High yield bonds sold off along with the rest of the global bond market in the wake of Mr. Trump’s election, but risk premiums have not risen and companies look set to continue issuing bonds—indicating that the market retains a positive outlook for the U.S. economy.

Defaults in high yield bonds are not expected to rise meaningfully this year thanks to higher oil prices arising from the OPEC deal, and their lower sensitivity to interest rate changes will provide some downside protection against rising yields at the long end of the curve.

Within high yield, the technology sector has strong potential value. Corporate tax reform should provide more free cash flow for capital spending, and technology applications are expected to be high on companies’ priorities. Mr. Trump’s infrastructure spending plans also could boost the metals and mining sector, particularly as the president-elect has pledged to take a tough line on steel imports.

Heavy borrowing among investment-grade issuers over the past five to six years has led to deterioration in credit quality within the asset class. If rates in investment-grade corporates rise again to 5% to 6%, the sector may begin to offer value. For the time, however, yields and spreads available in these bonds generally do not offer significant opportunities.

SelectivityThe interplay between U.S. monetary tightening, a relatively firm anchoring of Japanese and core European bond yields, and expected volatility in emerging markets in 2017 will provide

opportunities to exploit the spreads between international markets as well as the shapes of their yield curves.

Global investors may benefit from blending countries’ varying cycles and particularly from exploring opportunities beyond traditional benchmarks. Overall, though, U.S. credit looks set to offer the most potential if the Trump administration delivers on its pledge to spend heavily on infrastructure, cut taxes, and reduce regulation. However, until there is further clarity about how the U.S. economy will perform, it likely will pay to adopt a prudent approach, focusing on selective, high-conviction positions and embracing the global opportunity set. ■

Diversification cannot assure a profit or protect against loss in a declining market. Yields can vary with interest rate changes, and certain bond holdings are subject to credit risk. International investing, particularly in emerging markets, entails additional risks, including currency and political risks.

Figure 3 Global Fixed Income Performance Rebounded in 2016 From Low to Negative Returns in 20152016 Full-Year Bond Returns Versus 2015 Full-Year Bond Returns

Chart represents total returns for the following: Credit Suisse High Yield Index; J.P. Morgan Emerging Markets Bond Index Global; and Bloomberg Barclays U.S. Corporate Investment Grade Bond, U.S. Treasury Bond, U.S. Mortgage Backed Securities, Municipal Bond, and Global Aggregate ex-USD Bond indices. Source: T. Rowe Price.

Tota

l Ret

urns

-10

-5

0

5

10

15

20

25%

InternationalBonds

MunicipalsMortgage-BackedSecurities

U.S.Treasuries

U.S. CorporateInvestment Grade

EmergingMarkets

High Yield

20162015

-4.9

18.4

1.2

10.2

-0.7

6.1

0.8 1.0 1.73.3

0.3

-6.0

1.51.5

...until there is further clarity about how the U.S. economy will perform, it likely will pay to adopt a prudent approach, focusing on selective, high-conviction positions and embracing the global opportunity set.

12

ISSUE NO. 131 WINTER 2017

EM BONDS

Emerging Markets Debt Attractive vs. Developed Market Sovereign BondsBut emerging markets face risks resulting from rising developed market rates.

BY SAMY MUADDI, MANAGER OF THE EMERGING MARKETS CORPORATE BOND FUND

Less vulnerableEmerging markets debt generated strong returns through most of 2016, outperforming most fixed income sectors as oil prices stabilized and ultralow or negative yields on high-quality developed markets debt pushed investors into higher-yielding sectors. While these conditions may not last in 2017, emerging markets bonds remain more attractive than the sovereign debt of developed countries.

Emerging markets have become structurally less vulnerable in terms of fiscal health, private sector liabilities, external obligations, and political stability.

Also, external funding pressures from current account deficits, which were a major vulnerability of emerging economies in the recent past, have receded.

Moreover, most developing countries have made great strides in bringing inflation under control, thanks largely to a shift toward independent central banks with policy mandates to target price stability.

While political risk has increased in many developed markets—as

demonstrated by the UK’s Brexit vote and Donald J. Trump’s election as U.S. president—emerging countries’ political risks have been broadly trending downward.

Structural reformsEmerging markets countries that can implement structural reforms to position their economies for growth are most likely to offer the best long-term investment opportunities going forward.

Heading into 2017, certain Latin American countries appear best positioned for reforms, particularly Brazil and Argentina. Outside Latin America, India’s Prime Minister Narendra Modi

should be able to continue to make reforms aimed at growth.

Additionally, many investors may under-appreciate the potential for further reforms in China as it evolves from an export-driven economy to one based primarily on domestic consumption.

While China’s economic transition creates opportunities for structural reform, it also presents a potential risk to emerging markets. If China’s government were to fail to engineer an economic “soft landing” as the country moves toward a more balanced but slower growth rate, it could have profound negative effects around the world. However, this risk may be mitigated in 2017 by Beijing’s desire to sustain its economy in advance of the Communist Party Congress in the fall.

Dollar-denominated debtThe three most significant risks facing emerging markets debt in 2017 are a possible further rise in yields in developed markets, the potential for another downturn in oil prices, and a possible push by the Trump administration toward restrictive trade policies. Yields on high-quality sovereign debt from developed markets increased meaningfully after the U.S. presidential election, and further increases would eliminate part of the yield advantage that helped emerging markets bonds post strong returns in 2016.

These risks would weigh most heavily on emerging markets currencies versus the U.S. dollar. While emerging markets now can better handle the consequences of currency depreciation, bonds denominated in local currencies are our least-favored emerging markets debt sector. Sovereign bonds denominated in U.S. dollars appear best positioned for relative outperformance in 2017, followed by dollar-denominated emerging markets corporate debt. ■

Emerging markets investments are particularly subject to market, currency, political, and economic risks, as well as the risk of abrupt and severe price declines. Bonds are subject to risks from rising interest rates, credit rating downgrades, and default.

Sovereign bonds denominated in U.S. dollars appear best positioned for relative outperformance in 2017, followed by dollar-denominated emerging markets corporate debt.

13T R O W E P R I C E . C O M

Risk-adjusted returnsT. Rowe Price has opened a U.S.-focused, multi-sector bond fund that offers more diversification and flexibility than a traditional core fixed income portfolio with the goal of generating attractive, risk-adjusted returns over a wide range of market conditions.

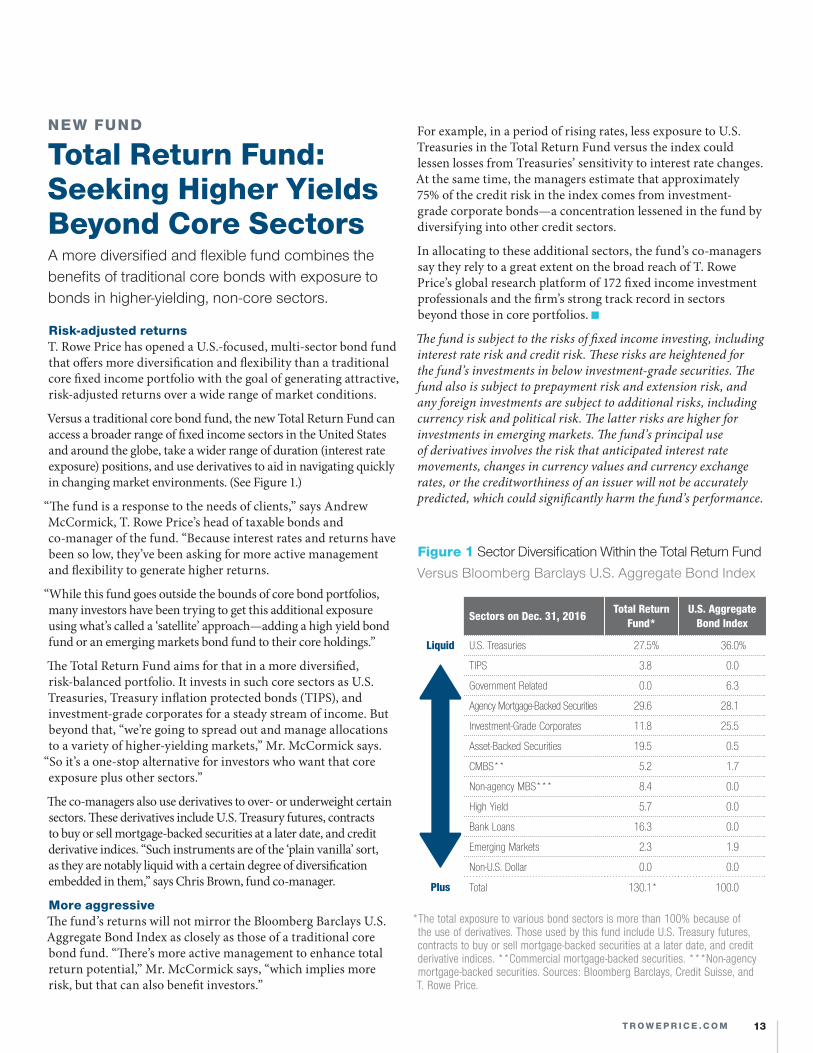

Versus a traditional core bond fund, the new Total Return Fund can access a broader range of fixed income sectors in the United States and around the globe, take a wider range of duration (interest rate exposure) positions, and use derivatives to aid in navigating quickly in changing market environments. (See Figure 1.)

“The fund is a response to the needs of clients,” says Andrew McCormick, T. Rowe Price’s head of taxable bonds and co-manager of the fund. “Because interest rates and returns have been so low, they’ve been asking for more active management and flexibility to generate higher returns.

“While this fund goes outside the bounds of core bond portfolios, many investors have been trying to get this additional exposure using what’s called a ‘satellite’ approach—adding a high yield bond fund or an emerging markets bond fund to their core holdings.”

The Total Return Fund aims for that in a more diversified, risk-balanced portfolio. It invests in such core sectors as U.S. Treasuries, Treasury inflation protected bonds (TIPS), and investment-grade corporates for a steady stream of income. But beyond that, “we’re going to spread out and manage allocations to a variety of higher-yielding markets,” Mr. McCormick says.

“So it’s a one-stop alternative for investors who want that core exposure plus other sectors.”

The co-managers also use derivatives to over- or underweight certain sectors. These derivatives include U.S. Treasury futures, contracts to buy or sell mortgage-backed securities at a later date, and credit derivative indices. “Such instruments are of the ‘plain vanilla’ sort, as they are notably liquid with a certain degree of diversification embedded in them,” says Chris Brown, fund co-manager.

More aggressiveThe fund’s returns will not mirror the Bloomberg Barclays U.S. Aggregate Bond Index as closely as those of a traditional core bond fund. “There’s more active management to enhance total return potential,” Mr. McCormick says, “which implies more risk, but that can also benefit investors.”

For example, in a period of rising rates, less exposure to U.S. Treasuries in the Total Return Fund versus the index could lessen losses from Treasuries’ sensitivity to interest rate changes. At the same time, the managers estimate that approximately 75% of the credit risk in the index comes from investment-grade corporate bonds—a concentration lessened in the fund by diversifying into other credit sectors.

In allocating to these additional sectors, the fund’s co-managers say they rely to a great extent on the broad reach of T. Rowe Price’s global research platform of 172 fixed income investment professionals and the firm’s strong track record in sectors beyond those in core portfolios. ■

The fund is subject to the risks of fixed income investing, including interest rate risk and credit risk. These risks are heightened for the fund’s investments in below investment-grade securities. The fund also is subject to prepayment risk and extension risk, and any foreign investments are subject to additional risks, including currency risk and political risk. The latter risks are higher for investments in emerging markets. The fund’s principal use of derivatives involves the risk that anticipated interest rate movements, changes in currency values and currency exchange rates, or the creditworthiness of an issuer will not be accurately predicted, which could significantly harm the fund’s performance.

Sectors on Dec. 31, 2016 Total Return Fund*

U.S. Aggregate Bond Index

Liquid U.S. Treasuries 27.5% 36.0%

TIPS 3.8 0.0

Government Related 0.0 6.3

Agency Mortgage-Backed Securities 29.6 28.1

Investment-Grade Corporates 11.8 25.5

Asset-Backed Securities 19.5 0.5

CMBS** 5.2 1.7

Non-agency MBS*** 8.4 0.0

High Yield 5.7 0.0

Bank Loans 16.3 0.0

Emerging Markets 2.3 1.9

Non-U.S. Dollar 0.0 0.0

Plus Total 130.1* 100.0

Figure 1 Sector Diversification Within the Total Return FundVersus Bloomberg Barclays U.S. Aggregate Bond Index

*The total exposure to various bond sectors is more than 100% because of the use of derivatives. Those used by this fund include U.S. Treasury futures, contracts to buy or sell mortgage-backed securities at a later date, and credit derivative indices. **Commercial mortgage-backed securities. ***Non-agency mortgage-backed securities. Sources: Bloomberg Barclays, Credit Suisse, and T. Rowe Price.

NEW FUND

Total Return Fund: Seeking Higher Yields Beyond Core SectorsA more diversified and flexible fund combines the benefits of traditional core bonds with exposure to bonds in higher-yielding, non-core sectors.

14

ISSUE NO. 131 WINTER 2017

Long-term perspectiveAfter several years of relatively placid, rising markets, volatility has returned to global equity markets. Although this is an inevitable part of investing, market setbacks can be stressful for investors, who may undermine their long-term strategies by overreacting emotionally.

“We counsel investors all the time to maintain a long-term perspective,” says Judith Ward, CFP®, a T. Rowe Price senior financial planner. “It’s important to remember the roles that stocks and bonds play in a portfolio. Over long periods of time, stocks have outperformed other financial assets and provided a better hedge against inflation, while bonds have provided steady income and usually helped reduce portfolio volatility.

“We also encourage investors not to react to daily headlines and focus on what they can control, such as their asset allocation strategy and how much they save and spend,” she adds. “Diversifying broadly across and within asset classes is not a guarantee that you won’t lose money, but investors should maintain a diversified strategy that reflects their long-term goals and risk tolerance—a strategy that they can stick with during periods of short-term volatility.”

Rebalancing actOne approach for doing that involves periodically rebalancing a diversified portfolio. Shifting money among asset classes to adhere to long-term allocation targets can prevent risk exposure from drifting higher when markets are performing well and potentially enable investors to take advantage of market declines by investing at lower prices.

Rebalancing may seem counterintuitive to some investors, Ms. Ward says. “It’s sometimes difficult to trim areas that have been doing well in favor of areas that have been under pressure. However, you’re

Figure 1 Over Both 10- and 20-Year Periods, Rebalancing Reduced Volatility With Similar ReturnsAnnualized Returns and Standard Deviations* for Portfolios Not Rebalanced and Rebalanced Quarterly and Annually

*Standard deviation is a measure of volatility that indicates the range of possible outcomes for a portfolio—positive or negative—over a given period of time. The higher the standard deviation, the greater the volatility or risk. Past performance cannot guarantee future results. The initial asset allocation for each of the 3 $100,000 portfolios invested from December 31, 1995, to December 31, 2015, was the same: 60% equities and 40% bonds, including 36% large-cap U.S. stocks (Russell 1000 Index), 6% small-cap U.S. stocks (Russell 2000 Index), 18% international stocks (MSCI EAFE Index), and 40% U.S investment-grade bonds (Bloomberg Barclays U.S. Aggregate Bond Index). It is not possible to invest directly in an index. Source: T. Rowe Price.

0

3

6

9

12

15%

AnnuallyRebalancedPortfolio

QuarterlyRebalancedPortfolio

Non-rebalancedPortfolio

Standard Deviation (%)Annualized Return (%)

6.21

12.21

6.02

9.78

6.16

9.56

0

3

6

9

12

15%

AnnuallyRebalancedPortfolio

QuarterlyRebalancedPortfolio

Non-rebalancedPortfolio

Standard Deviation (%)Annualized Return (%)

7.10 7.03

9.31

7.10

9.15

12.00

10-Year Period 20-Year Period

PERSONAL FINANCE

Periodic Portfolio Rebalancing May Reduce VolatilityA recent study on periodic rebalancing shows it can help maintain a consistent strategy, lower market risks, and cushion losses.

KEY POINTSρ Investors should not overreact to market downturns.

ρ Rebalancing portfolios can enable investors to take advantage of market declines.

ρ A recent study shows how rebalancing cushioned losses through two severe bear markets.

15T R O W E P R I C E . C O M

rebalanced portfolio achieved roughly the same annualized return over 10 and 20 years as the non-rebalanced one.

During the technology bubble of the late 1990s, for example, the U.S. stock market consistently racked up double-digit gains, greatly benefiting the non-rebalanced portfolio. However, when the U.S. market then fell precipitously, the non-rebalanced portfolio experienced a larger loss (32%) than the annually rebalanced portfolio (19%) at the trough of the bear market in late 2002. Much the same happened as the U.S. stock market rebounded to a new high in 2007 and then fell significantly in the global financial crisis.

Annual reviewsBecause the asset mix within a portfolio constantly changes in line with market performance, Ms. Ward advises investors to review their asset allocations at least annually and evaluate whether they are comfortable with their overall risk exposure. Keep in mind that while rebalancing a portfolio in a tax-deferred account, such as an individual retirement account (IRA) or workplace savings plan, is not a taxable event, selling within a taxable account may result in taxable capital gains.

To avoid these tax consequences, investors can allocate new investments to underweighted asset classes to help bring the portfolio back in line with their target allocations. Another way to reduce portfolio turnover is to rebalance at the end of the year only if one of the asset classes has strayed by a certain amount (three to five percentage points, for example) from the allocation target. Again, rebalancing does not protect against loss in a declining market. ■

Many IRA service providers (including T. Rowe Price) and workplace savings plans offer rebalancing services. For more information on investing and personal finance, see troweprice.com/insights.

Figure 2 Rebalancing Before and After the Last Two U.S. Bear Markets Produced a Smoother Ride

Past performance cannot guarantee future results. The initial asset allocation of the non-rebalanced and rebalanced portfolios-—each reflects an investment of $100,000 on December 31, 1995—is the same as described in the note below Figure 1. The annual rebalancing of the portfolio takes place on December 31. Source: T. Rowe Price.

actually selling high and buying low. It is a way to be more disciplined in your approach and minimize the emotional aspects of investing.”

Over the long term, rebalancing may not deliver significantly higher returns than a static strategy, but it can enable investors to weather market setbacks. “When you have a smoother ride,” Ms. Ward says, “you’re more likely to stay invested. That’s important because investors who stay the course can come out ahead, while others who encounter extreme volatility may buy and sell at the wrong time. As a result, they can fall short of meeting their financial objectives.”

Rebalancing is inherently linked to diversification, notes Stefan Hubrich, T. Rowe Price’s director of asset allocation research. “A non-rebalanced portfolio can become nondiversified over time, as it becomes more concentrated in the assets with the highest prior performance,” he says. “Rebalancing is a way to remain diversified, and that may provide a better risk-adjusted return over time.”

Recent studyT. Rowe Price examined the 10- and 20-year performance and volatility of three well-diversified, $100,000 portfolios invested on December 31, 1995-with one portfolio never rebalanced, another rebalanced quarterly, and the other rebalanced annually to the initial target allocation of 60% stocks and 40% bonds.

Figure 1 shows the portfolios’ volatility over 10 and 20 years (as measured by their standard deviations) and their average annualized returns. It illustrates how the annually and quarterly rebalanced portfolios lagged the non-rebalanced portfolio—but with lower levels of risk. The annually rebalanced portfolio also helped preserve capital during the two major bear markets over the past 20 years: the technology bubble in 2000 and the global financial crisis in 2008−2009. (See Figure 2.) The annually

16

ISSUE NO. 131 WINTER 2017

LAST WORD

Women Can Set Themselves Up for a More Financially Secure RetirementNew video series addresses the retirement savings gap faced by many women.

Savings gapWomen face unique challenges in positioning themselves for retirement: They tend to make less than men—79 cents for every dollar earned by men*—and spend fewer years working but have a longer life expectancy.

Moreover, a savings gap opens between women and men early in their working careers:

ρ T. Rowe Price’s 2015 Retirement Spending and Saving study found that millennial women had saved significantly less money in their 401(k) workplace savings plans—with a median account balance of $10,600 compared with $22,200 for millennial men.

ρ The study also found that women were contributing a lower percentage of their salaries to their 401(k)s—a median of 5% compared with 7% for men.

Combine that with the reality that women outlive men by an average of five years,** preparing for retirement can be particularly challenging for many women.

To address that, T. Rowe Price has created a series of seven short videos in which 23 women share their experiences taking control of their finances. Each video speaks to a specific issue, such as investing or retirement saving for millennials and

single women. See troweprice.com/WomenOnRetirement.

Five stepsJudith Ward, CFP®, a senior financial planner at T. Rowe Price, offers tangible steps that women can start to take now to prepare for retirement:

ρ Educate yourself. Be actively involved in your financial future and know what your options are when it comes to saving. Does your company have a 401(k) plan? How much are you contributing?

ρ Prepare for the unexpected. Start an emergency fund that can cover

three to six months of expenses so you can handle an unexpected expense without tapping credit cards or your 401(k).

ρ Aim to save 15%. T. Rowe Price research shows that saving 15% of your annual salary, including any employer match in your 401(k) plan, can help generate a more powerful stream of income in retirement, even after accounting for inflation. Those who can’t save 15% right now can start lower and increase each year.

ρ Make the most of your 401(k). An employee match program or automated services in which an employee’s 401(k) contribution percentage increases every year, can help you get closer to that 15% savings rate. For example, if you

are saving 6% today and your employer matches 50% of your contribution, that’s a 9% savings rate. Using an auto-increase feature to raise your savings rate by 1% or 2% each year would get you to 15% in just a few years.

ρ Invest to meet your needs. Your overall asset allocation should be based on your time horizon, or when you plan to retire. If you’re not sure how to choose investments, vehicles like target date funds*** are designed to provide appropriate investment allocations and diversification. ■

*DuMonthier, A., and Hegewisch, A., The Gender Wage Gap: 2015; Annual Earnings Differences by Gender, Race, and Ethnicity. Institute for Women’s Policy Research. **World Health Organization, World Health Statistics: 2016. ***The principal value of target date funds is not guaranteed at any time, including at or after the target date, which is the approximate date when an investor plans to retire. These funds typically invest in a broad range of underlying mutual funds that include stocks, bonds, and short-term investments and are subject to the risks of different areas of the market. In addition, the objectives of target date funds typically change over time to become more conservative. All funds are subject to market risk, including possible loss of principal.

...saving 15% of your annual salary, including any employer match in your 401(k) plan, can help generate a more powerful stream of income in retirement...