T7.1 Chapter Outline Chapter 7 Interest Rates and Bond Valuation Chapter Organization 7.1 Bonds and Bond Valuation 7.2 More on Bond Features 7.3 Bond Ratings 7.4 Some Different Types of Bonds 7.5 Bond Markets 7.6 Inflation and Interest Rates 7.7 Determinants of Bond Yields 7.8 Summary and Conclusions CLICK MOUSE OR HIT SPACEBAR TO ADVANCE Irwin/McGraw-Hill

Transcript

T7.1 Chapter Outline

Chapter 7Interest Rates and Bond Valuation

Chapter Organization

7.1 Bonds and Bond Valuation

7.2 More on Bond Features

7.3 Bond Ratings

7.4 Some Different Types of Bonds

7.5 Bond Markets

7.6 Inflation and Interest Rates

7.7 Determinants of Bond Yields

7.8 Summary and ConclusionsCLICK MOUSE OR HIT SPACEBAR TO ADVANCE

Irwin/McGraw-Hill

Irwin/McGraw-Hill Slide 2 2005

Bond Valuations

In the bond market there are 2 basic situations:

For a given bond and a given interest rate – what is the bond worth – what should I pay for this bond?

For a given bond and a price for that bond – what is the yield to maturity (YTM) I will earn?

Basic premise – bonds are tradeable financial instruments that change in value driven by a range of factors but in large part by changing interest rates.

Irwin/McGraw-Hill Slide 3 2005

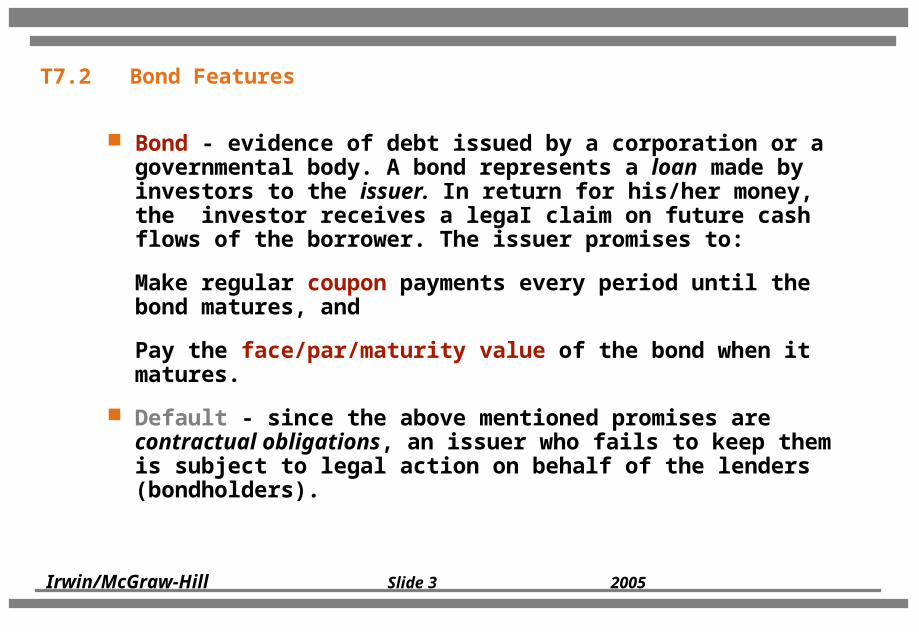

T7.2 Bond Features

Bond - evidence of debt issued by a corporation or a governmental body. A bond represents a loan made by investors to the issuer. In return for his/her money, the investor receives a legaI claim on future cash flows of the borrower. The issuer promises to:

Make regular coupon payments every period until the bond matures, and

Pay the face/par/maturity value of the bond when it matures.

Default - since the above mentioned promises are contractual obligations, an issuer who fails to keep them is subject to legal action on behalf of the lenders (bondholders).

Irwin/McGraw-Hill Slide 4 2005

If a bond has five years to maturity, an $80 annual coupon, and a $1000 face value, its cash flows would look like this:

Time 0 1 2 3 4 5

Coupons $80 $80 $80 $80 $80

Face Value $ 1000

Market Price $____

How much is this bond worth? It depends on the level of current market interest rates. If the going rate on bonds like this one is 10%, then this bond has a market value of $924.18.

T7.2 Bond Features (concluded)

Irwin/McGraw-Hill Slide 5 2005

A bond has five years to maturity, an $80 annual coupon, and a $1000 face value, its cash flows would look like this:

Time 0 1 2 3 4 5

Coupons $80 $80 $80 $80 $80

Face Value $ 1000

Coupons - the stated interest payments made on the bond

Face Value - (Par Value) - the principal amount of a bond that is repaid at the end of the term

Coupon rate - annual coupon divided by the face value

Maturity - specified date at which the principal amount is paid

T7.2 Bond Features (concluded)

Irwin/McGraw-Hill Slide 6 2005

A bond has five years to maturity, an $80 annual coupon, and a $1000 face value, its cash flows would look like this:

Time 0 1 2 3 4 5

Coupons $80 $80 $80 $80 $80

Face Value $ 1000

Market Value = ‘s

PV of the coupon payments (annuity)

+

PV of the principal (PV of a single cash flow)

T7.2 Bond Value

Irwin/McGraw-Hill Slide 7 2005

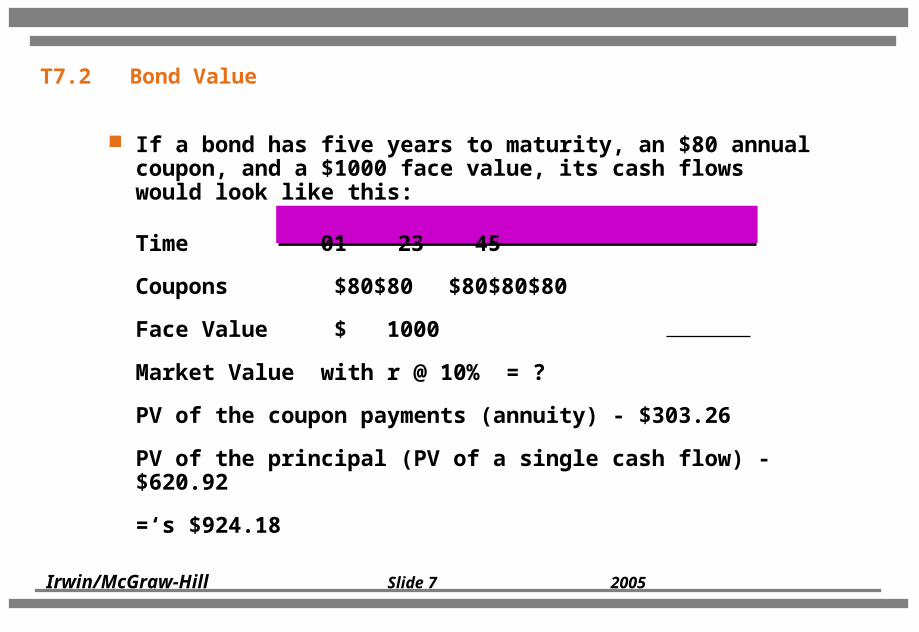

If a bond has five years to maturity, an $80 annual coupon, and a $1000 face value, its cash flows would look like this:

Time 0 1 2 3 4 5

Coupons $80 $80 $80 $80 $80

Face Value $ 1000

Market Value with r @ 10% = ?

PV of the coupon payments (annuity) - $303.26

PV of the principal (PV of a single cash flow) - $620.92

=‘s $924.18

T7.2 Bond Value

Irwin/McGraw-Hill Slide 8 2005

T7.3 Bond Rates and Yields

Consider again our example bond. It sells for $924.18, pays an annual coupon of $80, and it matures in 5 years. It has a face value of $1000. What are its coupon rate, current yield, and yield to maturity (YTM)?

1. The coupon rate (or just “coupon”) is the annual dollar coupon as a percentage of the face value:

Coupon rate = $80 /$1000 = 8%

2. The current yield is the annual coupon divided by the current market price of the bond:

Current yield = $80 / 924.18 = 8.66%

Irwin/McGraw-Hill Slide 9 2005

A bond has five years to maturity, an $80 annual coupon, and a $1000 face value, its cash flows would look like this:

Time 0 1 2 3 4 5

Coupons $80 $80 $80 $80 $80

Face Value $ 1000

YTM - the market interest rate that equates a bond’s present value of interest payments and principal repayment with its price

If you paid $924.18 for this bond and received the above cash flows - what is the YTM?

T7.2 Bond Yield to Maturity - YTM

Irwin/McGraw-Hill Slide 10 2005

T7.3 Bond Rates and Yields (concluded)

3. The yield to maturity (or “YTM”) is the rate that makes the market price of the bond equal to the present value of its future cash flows. It is the unknown r in the equation below:

$924.18 = $80 [1 - 1/(1 + r)5]/r + $1000/(1 + r)5

The only way to find the YTM (long hand) is by trial and error:

Let’s understand what has happened before going much further........

• We have a 5 year bond that with a coupon of $80

• Face Value is $1000 - principal repayment in 5 years time will be $1000

• Interest rates for 5 year bonds were about 8% when the bond was issued - let’s assume this - so the bond would have been issued at $1000

• interest rates change - 5 year interest rates move up to the 10% level

The value of this bond has declined - because there are competing products in the market place paying 10% interest when this bond only pays 8% - to buy this bond and still earn a 10% YTM I should only pay $924.18

What should we conclude? - bond values move up and down in response to financial events - in this case a change in interest rates

Irwin/McGraw-Hill Slide 12 2005

Bond Values and Yields - what is the relationship?

there is a relationship between the value of the bond and rates of return (YTM) in market equilibrium

when interest rates change - we suddenly do not have market equilibrium - to achieve equilibrium the values of existing bonds in the marketplace need to shift to reflect the new financial reality!

If interest rates move up - bond values decline If interest rates move down - bond values increase

.....as the bond market strives for equilibrium in the face of changes in the financial/business marketplace

Irwin/McGraw-Hill Slide 13 2005

T7.4 Valuing a Bond

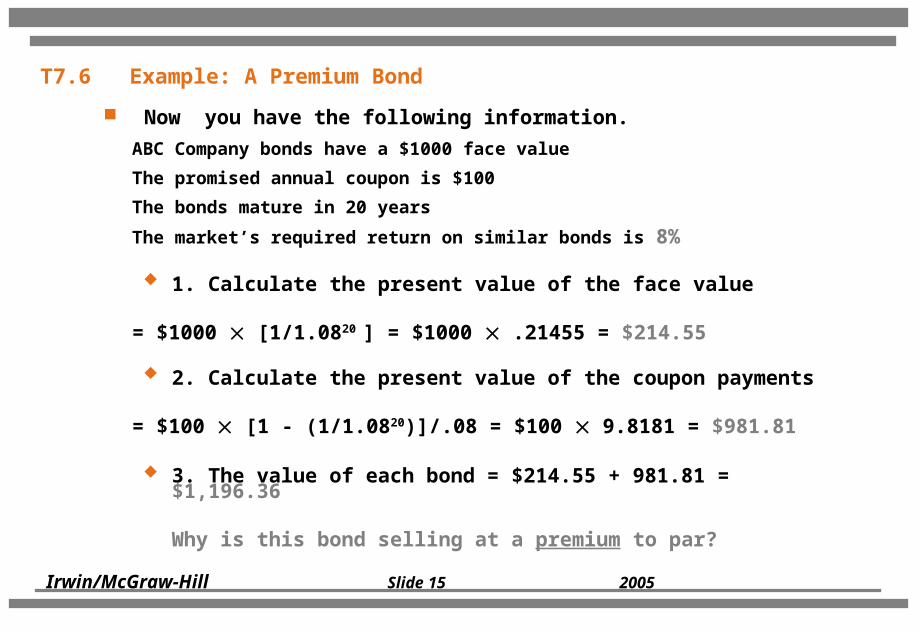

Let’s do another one. Assume you have the following information.

ABC company bonds have a $1000 face value.

The promised annual coupon is $100.

The bonds mature in 20 years.

The market’s required return on similar bonds is 10%

What is the bond’s value?

1. Calculate the present value of the face value

= $1000 [1/1.1020 ] = $1000 .14864 = $148.64

2. Calculate the present value of the coupon payments

3. The value of each bond = $214.55 + 981.81 = $1,196.36

Why is this bond selling at a premium to par?

Irwin/McGraw-Hill Slide 16 2005

T7.7 Bond Price Sensitivity to YTM

4% 6% 8% 10% 12% 14% 16%

$1,800

$1,600

$1,400

$1,200

$1,000

$ 800

$ 600

Bond price

Yield to maturity, YTM

Coupon = $10020 years to maturity$1,000 face value

Key Insight: Bond prices and YTM’s are inversely related.

Irwin/McGraw-Hill Slide 17 2005

T7.8 The Bond Pricing Equation

Bond Value = Present Value of the Coupons

+ Present Value of the Face Value

= C [1 - 1/(1 + r )t]/r + F 1/(1 + r )t

where: C = Coupon paid each period

r = Rate per period

t = Number of periods

F = Bond’s face value

Irwin/McGraw-Hill Slide 18 2005

T7.9 Interest Rate Risk and Time to Maturity (Figure 7.2)

Irwin/McGraw-Hill Slide 19 2005

Interest Rate Risk

the ‘risk that arises for bond owners from fluctuating interest rates (market yields)’

the risk or sensitivity to interest rate changes is a function of • time to maturity - the longer the time to maturity the

greater the interest rate risk• coupon rate - the lower the coupon rate the greater the

interest rate risk

time to maturity - longer term bonds have greater interest rate risk due to the timing of the the principal repayment - if it occurs in 30 years a small interest rate change can have a major impact on the PV of that cash flow vs if the principal is due in one year

coupon rate - for a given YTM a higher coupon bond has larger cash flows earlier than another bond with the same YTM but lower coupon payments (more of the YTM is made up of the face amount to be received at maturity)

Irwin/McGraw-Hill Slide 20 2005

Reinvestment Risk

Uncertainty concerning the interest rates at which cash flows e.g. coupon payments can be reinvested

Irwin/McGraw-Hill Slide 21 2005

T7.10 Summary of Bond Valuation (Table 7.1)

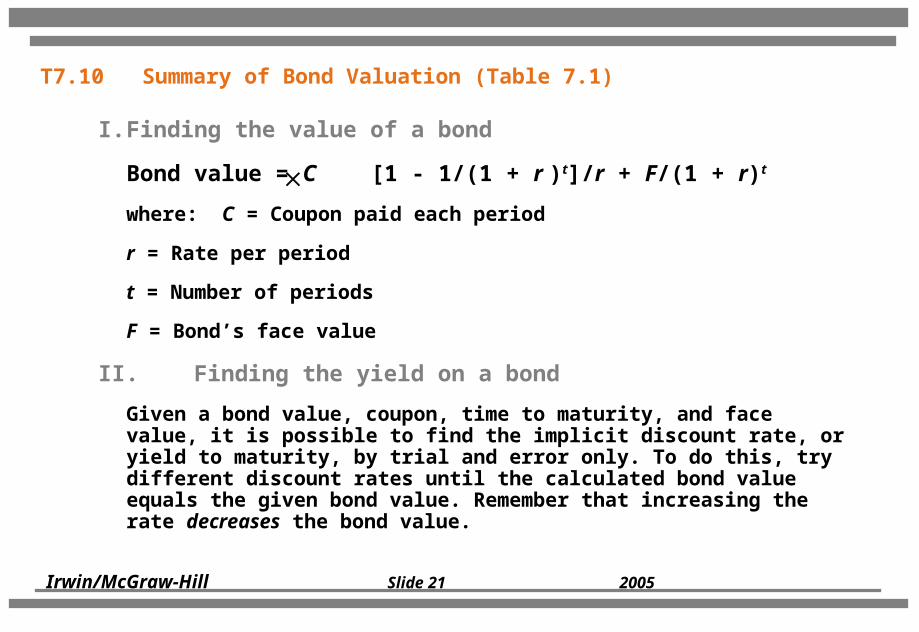

I. Finding the value of a bond

Bond value = C [1 - 1/(1 + r )t]/r + F/(1 + r)t

where: C = Coupon paid each period

r = Rate per period

t = Number of periods

F = Bond’s face value

II. Finding the yield on a bond

Given a bond value, coupon, time to maturity, and face value, it is possible to find the implicit discount rate, or yield to maturity, by trial and error only. To do this, try different discount rates until the calculated bond value equals the given bond value. Remember that increasing the rate decreases the bond value.

Irwin/McGraw-Hill Slide 22 2005

T7.11 Bond Pricing Theorems

The following statements about bond pricing are always true.

1. Bond prices and market interest rates move in opposite directions.

2. When a bond’s coupon rate is (greater than / equal to / less than) the market’s required return, the bond’s market value will be (greater than / equal to / less than) its par value.

3. Given two bonds identical but for maturity, the price of the longer-term bond will change more (in percentage terms) than that of the shorter-term bond, for a given change in market interest rates.

4. Given two bonds identical but for coupon, the price of the lower-coupon bond will change more (in percentage terms) than that of the higher-coupon bond, for a given change in market interest rates.

Irwin/McGraw-Hill Slide 23 2005

Differences Between Debt and Equity 7.2

Debt Not an ownership interest Bondholders do not have

voting rights Interest is considered a

cost of doing business and is tax deductible

Bondholders have legal recourse if interest or principal payments are missed

Excess debt can lead to financial distress and bankruptcy

Equity Ownership interest Common shareholders

vote for the board of directors and other issues

Dividends are not considered a cost of doing business and are not tax deductible

Dividends are not a liability of the firm and shareholders have no legal recourse if dividends are not paid

An all equity firm can not go bankrupt

Irwin/McGraw-Hill Slide 24 2005

Bond Characteristics cont’d

Bonds vs Debentures a bond is a form of secured debt - certain assets are pledged

as security a debenture is a form of unsecured debt - specific assets are

not pledged as security

However, typically the term ‘bond’ is used for all forms of debt

Public vs Private Debt Public debt is offered to the public while private debt is where

the debt is placed with a single lender - often a pension fund, insurance firm, etc.

Irwin/McGraw-Hill Slide 25 2005

T7.12 Features of a May Department Stores Bond

Term Explanation

Amount of issue $200 million The company issued $200 million worth of bonds.

Date of issue 8/4/94 The bonds were sold on 8/4/94.

Maturity 8/1/24 The principal will be paid 30 years after the issue date.

Face Value $1,000 The denomination of the bonds is $1,000.

Annual coupon 8.375 Each bondholder will receive $83.75 per bond per year (8.375% of the face value).

Offer price 100 The offer price will be 100% of the $1,000 face value per bond.

Irwin/McGraw-Hill Slide 26 2005

T7.12 Features of a May Department Stores Bond (concluded)

Term Explanation

Coupon payment dates 2/1, 8/1 Coupons of $83.75/2 = $41.875 will be paid on these dates.

Security None The bonds are debentures.

Sinking fund Annual The firm will make annual payments beginning 8/1/05 toward the sinking fund.

Call provision Not callable The bonds have a deferred call feature.before 8/1/04 (See Appendix 7C on Canada plus calls.)

Call price 104.188 initially, After 8/1/04, the company can buy back declining to 100 the bonds for $1,041.88 per bond,

declining to $1,000 on 8/1/14.

Rating Moody’s A2 This is one of Moody’s higher ratings. The bonds have a low probability of default.

Irwin/McGraw-Hill Slide 27 2005

7.13 The Bond Indenture

The Bond Indenture

The bond indenture is a three-party contract between the bond issuer, the bondholders, and the trustee. The trustee is hired by the issuer to protect the bondholders’ interests. The indenture includes

The basic terms of the bond issue The total amount of bonds issued A description of the security The repayment arrangements The call provisions Details of the protective covenants

Irwin/McGraw-Hill Slide 28 2005

Additional Bond Features

registered vs bearer

security bond debenture collateral mortgage securities

seniority senior junior subordinated debt

Irwin/McGraw-Hill Slide 29 2005

Additional Bond Features

Repayment repaid at maturity early repayment

• sinking fund - an account managed by a bond trustee for the purpose of repaying the bonds - the trustee uses the funds and purchases the required amounts in the open market or calling in a fraction of the outstanding bonds.

• value of a sinking fund to investors - reduces the risk that the company will be unable to repay the principal at maturity thus improving the marketability of the bonds

call provisions protective covenants

• part of the loan agreement that limits actions of the borrowing firm - e.g. restrictions on dividends and sales of major assets

Irwin/McGraw-Hill Slide 30 2005

T7.14 Bond Ratings

Low Quality, speculative, Investment-Quality Bond Ratings and/or “Junk”

High Grade Medium Grade Low Grade Very Low Grade

Moody’s Aaa Aa A Baa Ba B Caa Ca C DDBRS (S&P) AAA AA A BBB BB B CCC CC C D

Moody’s DBRS

Aaa AAA Debt rated Aaa and AAA has the highest rating. Capacity to pay interest and principal is extremely strong.

Aa AA Debt rated Aa and AA has a very strong capacity to pay interest and repay principal. Together with the highest rating, this group

comprises the high-grade bond class.

A A Debt rated A has a strong capacity to pay interest and repay principal, although it is somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than debt in high rated categories.

Irwin/McGraw-Hill Slide 31 2005

T7.14 Bond Ratings (concluded)

Baa BBB Debt rated Baa and BBB is regarded as having an adequate capacity to pay interest and repay principal. Whereas it normally exhibits adequate protection parameters, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity to pay interest and repay principal for debt in this category than in higher rated categories. These bonds are medium-grade obligations.

Ba, B BB, B Debt rated in these categories is regarded, on balance, as Ca, CCC, C predominantly speculative with respect to capacity to pay

interest and repay principal in accordance with the terms of the obligation. BB and Ba indicate the lowest degree of speculation, and CC and Ca the highest degree of speculation. Although such debt will likely have some quality and protective characteristics, these are out-weighed by large uncertainties or major risk exposures to adverse conditions. Some issues may be in default.

D D Debt rated D is in default, and payment of interest and/or repayment of principal is in arrears

Irwin/McGraw-Hill Slide 32 2005

Different Types of Bonds

Stripped bonds - a bond that makes not coupon payments and is initially priced at a deep discount

because all of the YTM is in the form of the principal repayment

interest is both deductible by the issuer and must be claimed by the investor - even though there is no interest coupon payments per se....it is imputed from discount

Floating Rate Bonds (floaters) - the coupon payments are adjustable (not fixed like a traditional bond)

were introduced by issuers to control the risk of price fluctuations due to interest rate shifts.

Income bond - coupon payments are dependent on company income - only if that income is sufficient

Irwin/McGraw-Hill Slide 33 2005

Different Types of Bonds Cont’d

Real Return Bonds - coupons and principal are indexed to inflation to provide a stated real return

Convertible Bonds - can be ‘converted’ for a fixed number of shares of the issuer’s stock - anytime before maturity and at the holder’s option - are considered a ‘hybrid’ of debt and equity. The convertible aspect provides the investor with additional incentive to purchase the bond

Retractable Bonds or ‘put’ bonds - allows the holder to ‘put’ the bonds back to the issuer or force the issuer to buy the bonds back at a stated price - this effectively establishes a floor price for the bonds

......issuers will combine various features at any given point in time to encourage investors to buy a new bond issue!

Irwin/McGraw-Hill Slide 34 2005

Bond Markets

OTC (over the counter) market with dealers connected electronically

the bond market in trading volume is many times larger than the trading volume in stocks

the U.S. Treasury market is the largest securities market in the world in terms of trading volume

Bond Price Reporting unlike stocks that are traded on an exchange - bonds do not

have that price ‘transparency’ - bonds prices are indications only and are typically provided by bond dealers (not by the TSE for example)

the Monday edition of the Globe & Mail is one of the best sources for bond information

Irwin/McGraw-Hill Slide 35 2005

Inflation and Interest Rates

Real vs Nominal Rates of Return nominal rates - interest rates or rates of return that have not

been adjusted for inflation real rates - interest rates or rates of return that have been

adjusted for inflation

nominal rate on an investment is the % change in the number of dollars you have

real rate on an investment is the % change in how much you can purchase with your dollars or the % change in buying power

Fisher Effect ( or theory) R = (r+h) +( r*h) where R is the Nominal rate, r is the real rate

and h is the rate of inflation

Irwin/McGraw-Hill Slide 36 2005

T7.16 Inflation and Returns

Key issues:

What is the difference between a real return and a nominal return?

How can we convert from one to the other?

Example:

Suppose we have $1000, and Coke costs $2.00 per six pack. We can buy 500 six packs. Now suppose the rate of inflation is 5%, so that the price rises to $2.10 in one year. We invest the $1000 and it grows to $1100 in one year. What’s our return in dollars (nominal)? In six packs (real buying power)?

Irwin/McGraw-Hill Slide 37 2005

T7.16 Inflation and Returns (continued)

A. Dollars. Our return is

($1,100 - $1,000)/$1,000 = $100/$1,000 = .10.

The percentage increase in our investment is 10%; our return is 10%....this is the nominal return

B. Six packs. We can buy $1,100/$2.10 = 523.81 six packs, so our return is

(523.81 - 500)/500 = 23.81/500 = 4.76%

The percentage increase in the amount of coke is 4.76%; our ‘real’ return is 4.76%....this is our buying power

Irwin/McGraw-Hill Slide 38 2005

T7.16 Inflation and Returns (continued)

Real versus nominal returns:

Your nominal return is the percentage change in the amount of money you have.

Your real return is the percentage change in the amount of ‘stuff’ you can actually buy.

Irwin/McGraw-Hill Slide 39 2005

T7.16 Inflation and Returns (concluded)

The relationship between real and nominal returns is described by the Fisher Effect. Let:

R = the nominal return

r = the real return

h = the inflation rate

According to the Fisher Effect:

1 + R = (1 + r) (1 + h)

Or R = (r+h) + (r*h)

From the example, the real return is 4.76%; the nominal return is 10%, and the inflation rate is 5%:

(1 + R) = 1.10

(1 + r) (1 + h) = 1.0476 x 1.05 = 1.10

Irwin/McGraw-Hill Slide 40 2005

Factors Affecting Bond Yields

What factors affect observed bond yields?

Term Structure of Interest Rates

The real rate of interest

Expected future inflation

Interest rate risk

Other factors

Default risk premium

Taxability premium

Liquidity premium

Irwin/McGraw-Hill Slide 41 2005

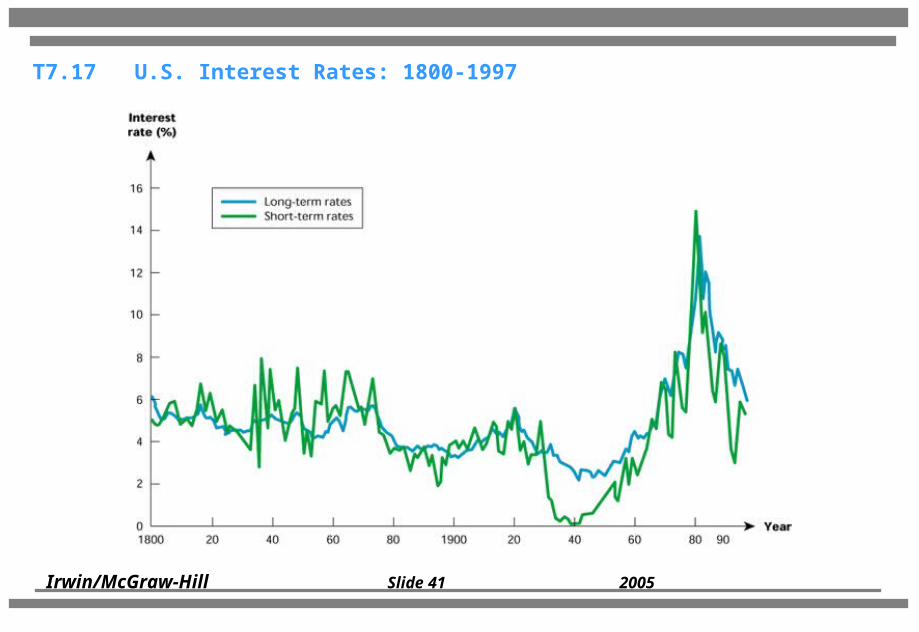

T7.17 U.S. Interest Rates: 1800-1997

Irwin/McGraw-Hill Slide 42 2005

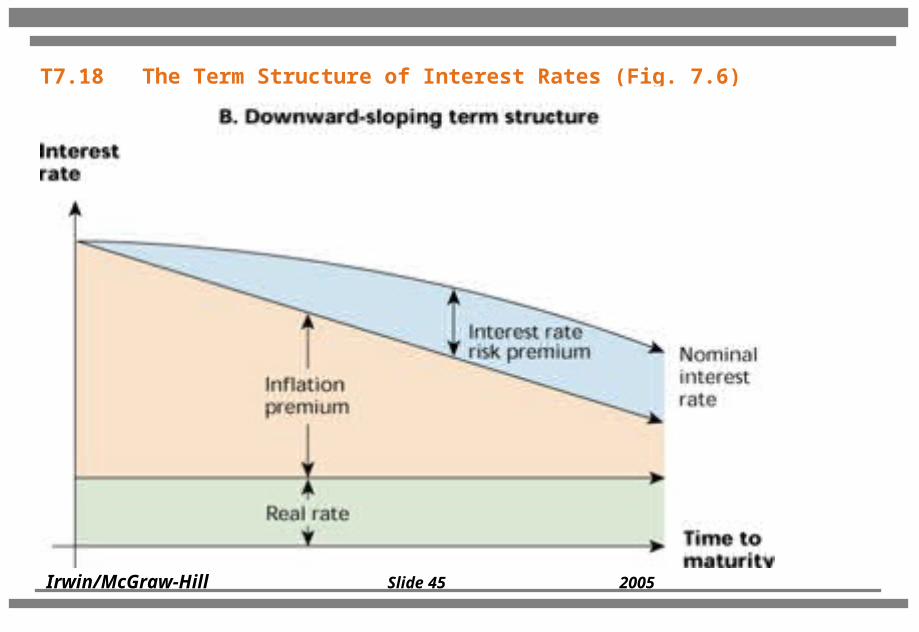

Term Structure of Interest Rates

Term structure of interest rates is the relationship between short and long term interest rates or

‘the relationship between nominal interest rates on default- free, pure discount securities and the time to maturity

What determines the shape of the term structure? Real rate of interest - pure time value of money rate of inflation interest rate risk

Irwin/McGraw-Hill Slide 43 2005

Term Structure of Interest Rates

Real rate of interest - basic component underlying every interest rate - it is the ‘economic rent’ or compensation that investors demand for forgoing the use of their money.

Tends to influence the overall level of rates more so than the shape of the structure

Rate of Inflation - investor demand extra compensation or an ‘inflation premium’ for the expected erosion of the value of their investment from inflation -

the key here is the expected inflation - if inflation is expected to be higher in the future then long term rates will reflect this and be higher than short term rates

Interest Rate Risk - risk of interest rates changing and the resulting impact on the value of the security

risk is greater over the longer term so this risk increases with the length of maturity

Irwin/McGraw-Hill Slide 44 2005

T7.18 The Term Structure of Interest Rates (Fig. 7.6)

Irwin/McGraw-Hill Slide 45 2005

T7.18 The Term Structure of Interest Rates (Fig. 7.6)

Irwin/McGraw-Hill Slide 46 2005

Factors Affecting Bond Yields

Other factors in addition to the Term Structure of Interest Rates

Credit risk & the default risk premium• if the risk of default is perceived to be higher - investors

will demand higher compensation - importance of bond ratings

Taxation - is the return taxable and how is it taxed U.S. Vs Canada interest and capital gains

Liquidity & liquidity premium - investors like ‘liquid’ issues where there is high levels of trading of that issue - provides confidence - low liquidity leads to higher yields - liquidity premium demanded by investors increases

Irwin/McGraw-Hill Slide 47 2005

Yield Curve

the ‘yield curve’ is a reflection of the term structure of interest rates

the ‘Canada Yield Curve’ reflecting Govt. of Canada bond yields is essentially the same

Corporate yield curves - however bring in these other factors affecting yields - e.g. default risk premium, etc.

....what does the yield curve look like today?

Irwin/McGraw-Hill Slide 48 2005

Figure 7.5 – Government of Canada Yield CurveNovember 29, 2002