1

©2005 Charles M. Cottle RD2 Exercises www.riskdoctor.com

Table of Contents:

Chapter 1 Exercises 2

Chapter 1 Exercises (Key) 3

Dissection Exercises 4

Dissection Exercises (Key) 5

Greeks Exercises 7

Greeks Exercises Key 9

Exercise Problems 11

Exercise Problems (Key) 12

Butterfly Dissection Exercise 14

Butterfly Dissection Exercise (Key) 15

2

©2005 Charles M. Cottle RD2 Exercises www.riskdoctor.com

Chapter 1 Exercises

You are long 10oo Underlying shares of EBAY going for 93.40 ($93,400). The purchase of 10 October 90 Puts can

provide a floor, limiting your downside risk.

If you buy 10 Puts for .80 each (each $80 for a total of $800);

1. What will you then want to happen to the Underlying stock?

2. What will be the most you can lose between now and expiration?

3. What is your break-even point(s) in terms of the Underlying price?

4. What is the simplest trade you can make to stop the exposure (locking in the gain or the loss, whatever it may

be)?

3

©2005 Charles M. Cottle RD2 Exercises www.riskdoctor.com

Chapter 1 Exercises (Key)

You are long 10oo Underlying shares of EBAY going for 93.40 ($93,400). The purchase of 10 October 90 Puts can

provide a floor, limiting your downside risk.

If you buy 10 Puts for .80 each (each $80 for a total of $800);

1. What will you then want to happen to the Underlying stock?

You want it to go up because this is synthetically long 10*90 Calls for 4.20 each ($4200).

2. What will be the most you can lose between now and expiration?

$4200 just like owning 10 real Calls for 4.20 each. (that is .80 for each Put becoming worthless while the stock drifts

lower from 93.40 to 90 losing the 3.40.

3. What is your break-even point(s) in terms of the Underlying price?

94.20 because the stock makes back the .80 that the Put will lose by expiration.

4. What is the simplest trade you can make to stop the exposure (locking in the gain or the loss, whatever it may

be)?

Sell the real call to complete the conversion. (you may be wondering what then? But that is for a later discussion).

4

©2005 Charles M. Cottle RD2 Exercises www.riskdoctor.com

Dissection Exercises

A government estimate will be announced in one minute. Which one (only one) vehicle (stock or calls, or puts)

would you buy or sell, and in what quantity in order to neutralize to a safe exposure (Hint: Card up and dissect

position.) Remember to check your Net Call Units and Net Put Units.

1. The DJX is at 102.80. You are short 16 futures, long 27 of the 104 calls and short 16 of the 104 puts.

2. The Bonds are at 103.02. You are short 15 of the 103 calls and long 13 of the 103 Puts.

3. The Bonds are at 102.30. You are short 58 futures, long 61 of the 103 calls and short 35 of the 103 puts.

4. The DJX is at 104.42. You are short 24 of the 102 calls and long 32 of the 102 Puts.

5

©2005 Charles M. Cottle RD2 Exercises www.riskdoctor.com

Dissection Exercises (Key)

A government estimate will be announced in one minute. Which one (only one) vehicle (stock or calls, or puts)

would you buy or sell, and in what quantity in order to neutralize to a safe exposure (Hint: Card up and dissect

position.) Remember to check your Net Call Units and Net Put Units.

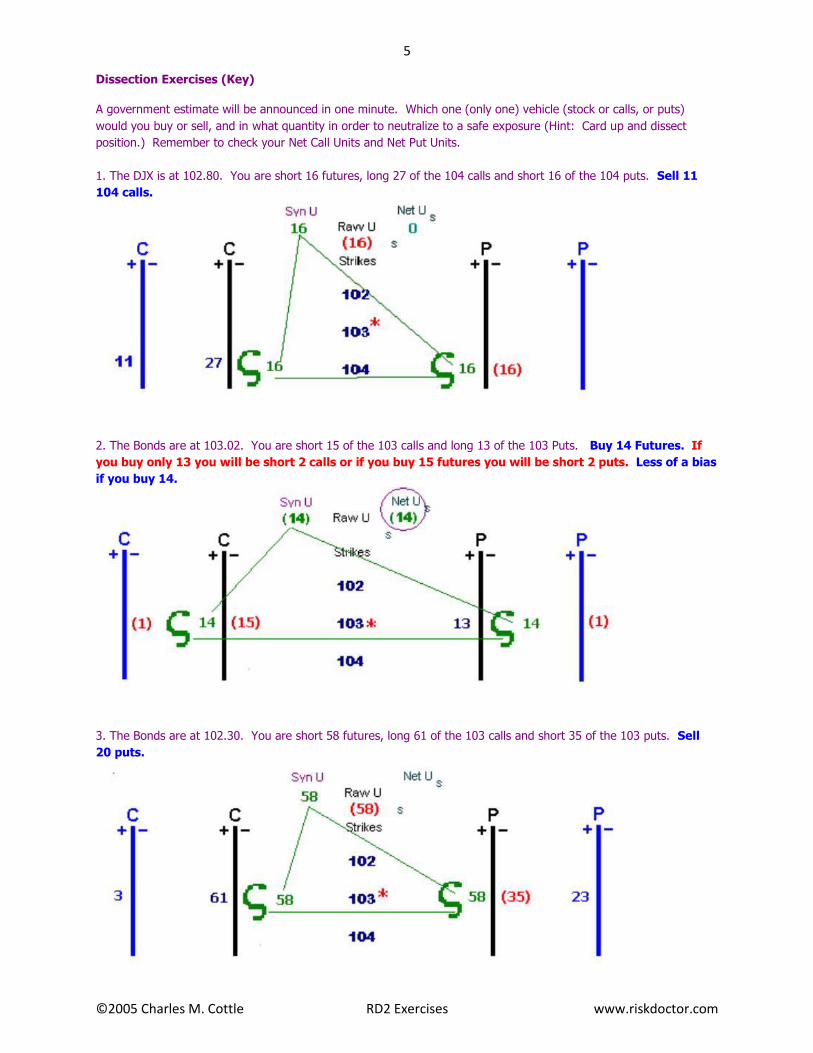

1. The DJX is at 102.80. You are short 16 futures, long 27 of the 104 calls and short 16 of the 104 puts. Sell 11

104 calls.

2. The Bonds are at 103.02. You are short 15 of the 103 calls and long 13 of the 103 Puts. Buy 14 Futures. If

you buy only 13 you will be short 2 calls or if you buy 15 futures you will be short 2 puts. Less of a bias

if you buy 14.

3. The Bonds are at 102.30. You are short 58 futures, long 61 of the 103 calls and short 35 of the 103 puts. Sell

20 puts.

6

©2005 Charles M. Cottle RD2 Exercises www.riskdoctor.com

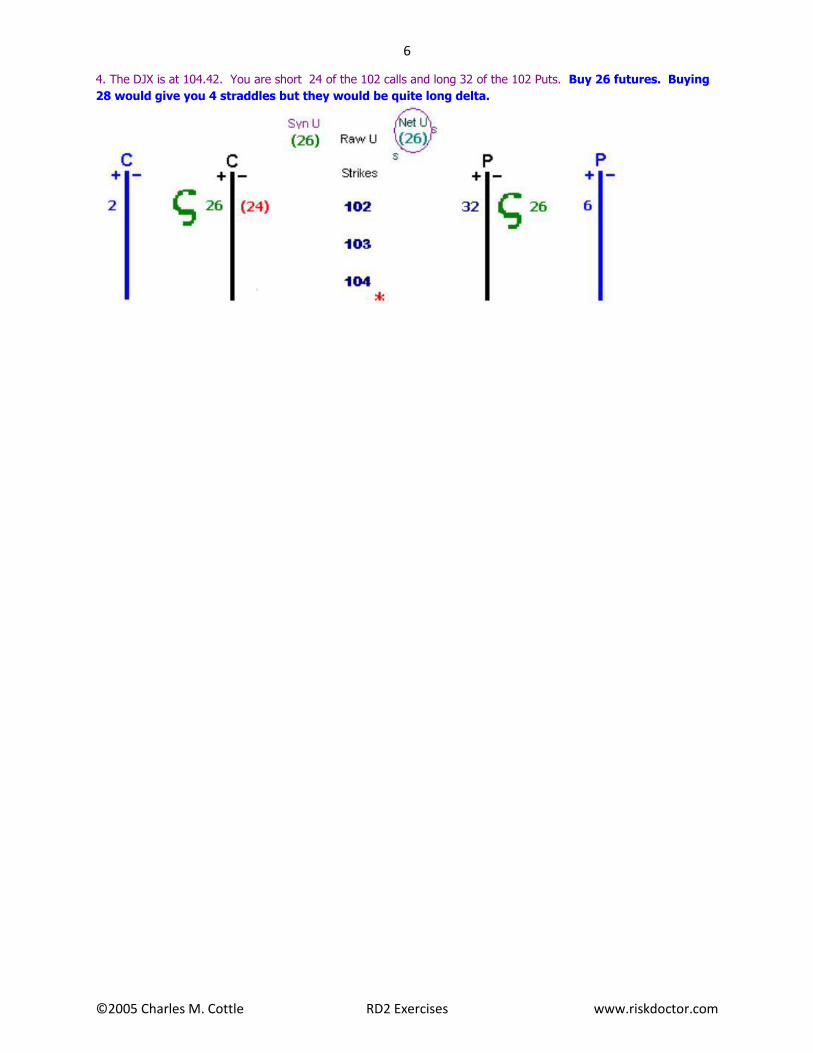

4. The DJX is at 104.42. You are short 24 of the 102 calls and long 32 of the 102 Puts. Buy 26 futures. Buying

28 would give you 4 straddles but they would be quite long delta.

7

©2005 Charles M. Cottle RD2 Exercises www.riskdoctor.com

Greeks Exercises

Multiple choice questions 1-16 are in effect True/False questions in that more than one choice may be correct. Circle

all that apply. If there is a questionable nuance that makes you unsure, then qualify your answer by writing a note

regarding your thoughts or reservations about a particular choice. If your argument or point is valid you will receive

credit.

Conceivably none could be True so Write “None”.

1. When scalping positive gamma on an up move with futures, you are

a. selling deltas

b. in effect selling calls and buying puts for intrinsic value plus or minus interest.

c. adding net units to calls and decreasing net put units

d. adding net units to puts and decreasing net call units

2. The key point when buying an ATM timespread (buy deferred, sell front month), is that the position is:

a. Long vega, short gamma

b. Long gamma, short vega

c. Long vega, long gamma

d. Short vega, short gamma

3. Over time, Deltas of …

a. …ITM options decrease (puts to a lesser negative, calls to a lesser positive)

b. …OTM options decrease (puts to a lesser negative, calls to a lesser positive)

c. …ATM options increase (puts to a greater negative, calls to a greaer positive)

4. As implied volatility increases, Deltas of…

a. …ITM options decrease (puts to a lesser negative, calls to a lesser positive)

b. …OTM options decrease (puts to a lesser negative, calls to a lesser positive)

c. …ATM options increase (puts to a greater negative, calls to a greaer positive)

5. As the price of the underlying rises. Deltas of …

a. …ITM call options decrease

b. …OTM call options decrease

c. …ATM call options increase

6. With regard to Gamma which of the following interpretations are valid? Gamma…

a. …is the greatest for ITM options

b …is the rate of change of the options Delta in a one point move in the underlying.

c. …when long creates longer deltas when the market is dropping

d. …when short creates shorter deltas when the market is rising

7. As implied volatility increases, Gammas of…

a. …Deep ITM options decrease

b. …Way OTM options decrease

c. …ATM options increase

8. As the price of the underlying rises. Gammas of …

a……ITM put options decrease

b……OTM call options decrease

c……ATM call options that are moving away from the money, increase

9. As the price of the underlying falls. Gammas of …

a……ITM put options decrease

b……OTM call options decrease

c……ATM call options that are moving away from the money, increase

8

©2005 Charles M. Cottle RD2 Exercises www.riskdoctor.com

10. Vega is the sensitivity of an options…

a……implied volatility for a 1 percent change

b……theotetical value with regard to a 1perctage point change in implied volatility

c……theoretical value and when long means that if implied volatility increases by 1 percentage point then your rate of

return will be 1% for your whole position

d……theoretical value and when long in one month and short the same amount of contracts in a different month

means that a 1% higher for both will mean no profit or loss

11. As implied volatility increases, Vegas of…

a……deep ITM options increase

b……way OTM options increase

c……ATM options increase

12. As the price of the underlying rises, Vegas of …

a……ITM put options increase

b……OTM call options decrease

c……ATM call options, moving away from the money, increase

13. As the price of the underlying falls, Vegas of …

a……ITM put options decrease

b……OTM call option, decrease

c……ATM options, moving away from the money, increase

14. Over time, positive Thetas of

a. …short deep ITM options (calls or puts), decrease

b. …short way OTM options (calls or puts), decrease

c …short ATM options (calls or puts), increase

15. As the price of the underlying rises. Thetas of …

a……ITM put options decrease

b……OTM call options decrease

c……ATM call options, moving away from the money, increase

16. As the price of the underlying falls. positive Thetas of …

a……short ITM put options decrease

b……short OTM call options decrease

c……short ATM call options, moving away from the money, increase

9

©2005 Charles M. Cottle RD2 Exercises www.riskdoctor.com

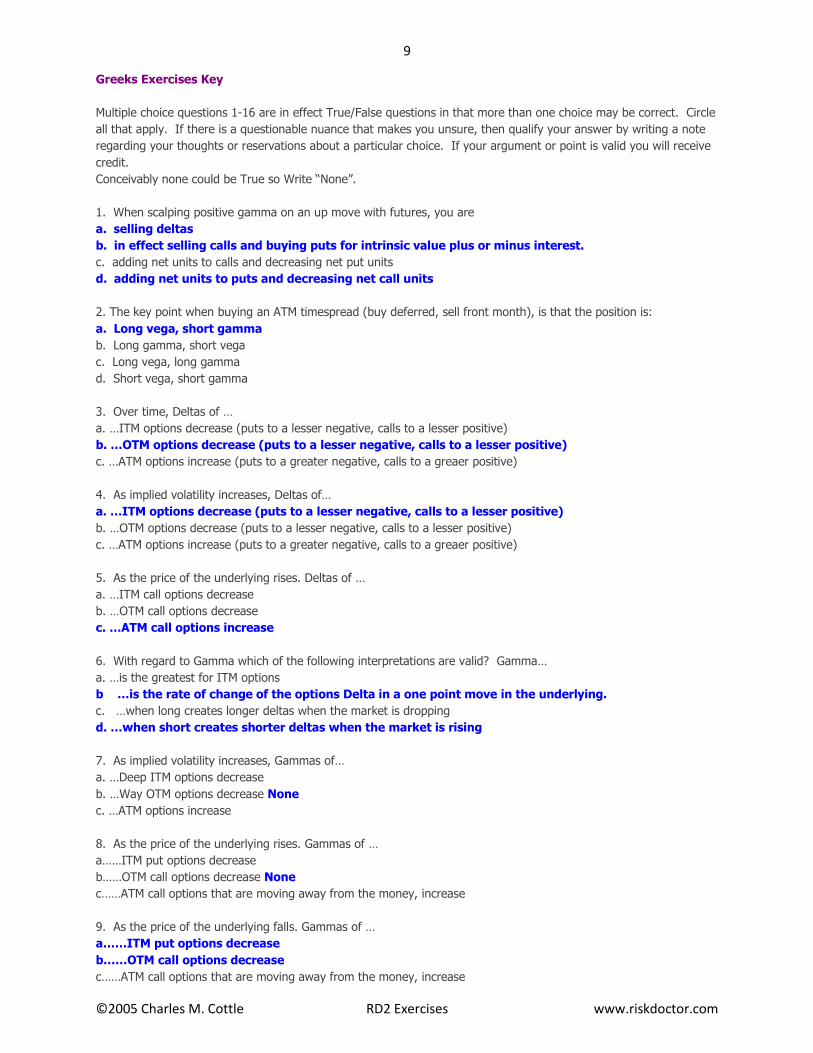

Greeks Exercises Key

Multiple choice questions 1-16 are in effect True/False questions in that more than one choice may be correct. Circle

all that apply. If there is a questionable nuance that makes you unsure, then qualify your answer by writing a note

regarding your thoughts or reservations about a particular choice. If your argument or point is valid you will receive

credit.

Conceivably none could be True so Write “None”.

1. When scalping positive gamma on an up move with futures, you are

a. selling deltas

b. in effect selling calls and buying puts for intrinsic value plus or minus interest.

c. adding net units to calls and decreasing net put units

d. adding net units to puts and decreasing net call units

2. The key point when buying an ATM timespread (buy deferred, sell front month), is that the position is:

a. Long vega, short gamma

b. Long gamma, short vega

c. Long vega, long gamma

d. Short vega, short gamma

3. Over time, Deltas of …

a. …ITM options decrease (puts to a lesser negative, calls to a lesser positive)

b. …OTM options decrease (puts to a lesser negative, calls to a lesser positive)

c. …ATM options increase (puts to a greater negative, calls to a greaer positive)

4. As implied volatility increases, Deltas of…

a. …ITM options decrease (puts to a lesser negative, calls to a lesser positive)

b. …OTM options decrease (puts to a lesser negative, calls to a lesser positive)

c. …ATM options increase (puts to a greater negative, calls to a greaer positive)

5. As the price of the underlying rises. Deltas of …

a. …ITM call options decrease

b. …OTM call options decrease

c. …ATM call options increase

6. With regard to Gamma which of the following interpretations are valid? Gamma…

a. …is the greatest for ITM options

b …is the rate of change of the options Delta in a one point move in the underlying.

c. …when long creates longer deltas when the market is dropping

d. …when short creates shorter deltas when the market is rising

7. As implied volatility increases, Gammas of…

a. …Deep ITM options decrease

b. …Way OTM options decrease None

c. …ATM options increase

8. As the price of the underlying rises. Gammas of …

a……ITM put options decrease

b……OTM call options decrease None

c……ATM call options that are moving away from the money, increase

9. As the price of the underlying falls. Gammas of …

a……ITM put options decrease

b……OTM call options decrease

c……ATM call options that are moving away from the money, increase

10

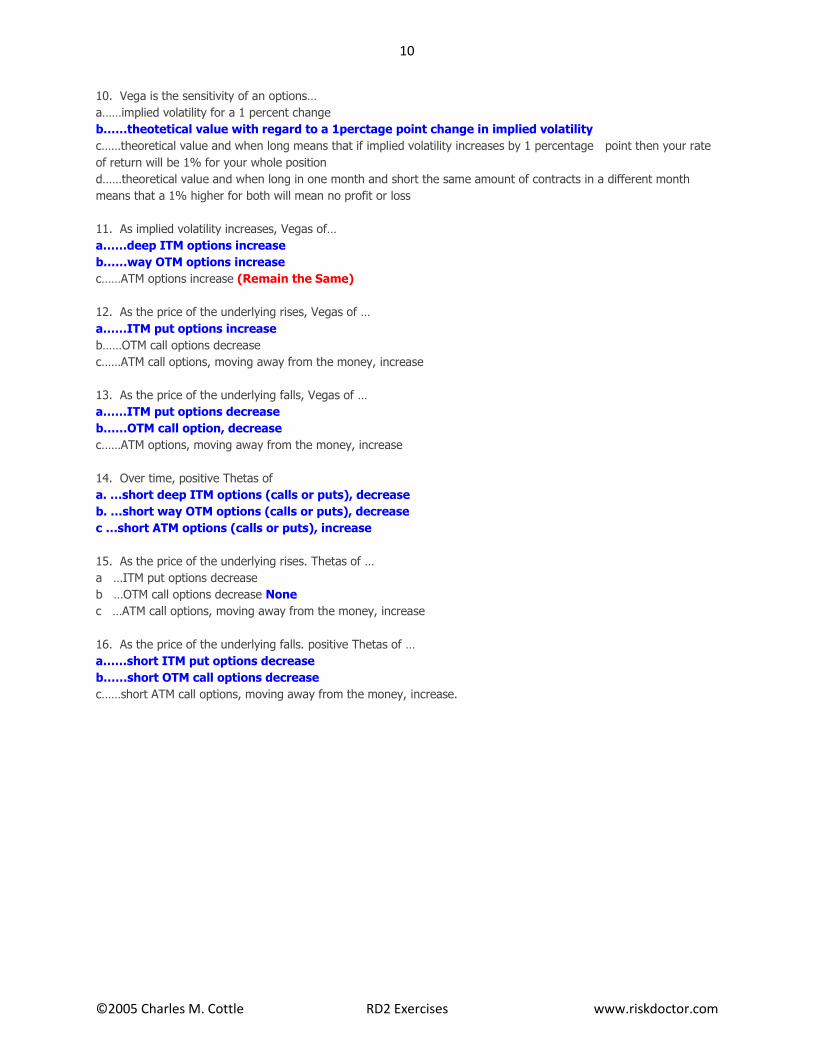

©2005 Charles M. Cottle RD2 Exercises www.riskdoctor.com

10. Vega is the sensitivity of an options…

a……implied volatility for a 1 percent change

b……theotetical value with regard to a 1perctage point change in implied volatility

c……theoretical value and when long means that if implied volatility increases by 1 percentage point then your rate

of return will be 1% for your whole position

d……theoretical value and when long in one month and short the same amount of contracts in a different month

means that a 1% higher for both will mean no profit or loss

11. As implied volatility increases, Vegas of…

a……deep ITM options increase

b……way OTM options increase

c……ATM options increase (Remain the Same)

12. As the price of the underlying rises, Vegas of …

a……ITM put options increase

b……OTM call options decrease

c……ATM call options, moving away from the money, increase

13. As the price of the underlying falls, Vegas of …

a……ITM put options decrease

b……OTM call option, decrease

c……ATM options, moving away from the money, increase

14. Over time, positive Thetas of

a. …short deep ITM options (calls or puts), decrease

b. …short way OTM options (calls or puts), decrease

c …short ATM options (calls or puts), increase

15. As the price of the underlying rises. Thetas of …

a …ITM put options decrease

b …OTM call options decrease None

c …ATM call options, moving away from the money, increase

16. As the price of the underlying falls. positive Thetas of …

a……short ITM put options decrease

b……short OTM call options decrease

c……short ATM call options, moving away from the money, increase.

11

©2005 Charles M. Cottle RD2 Exercises www.riskdoctor.com

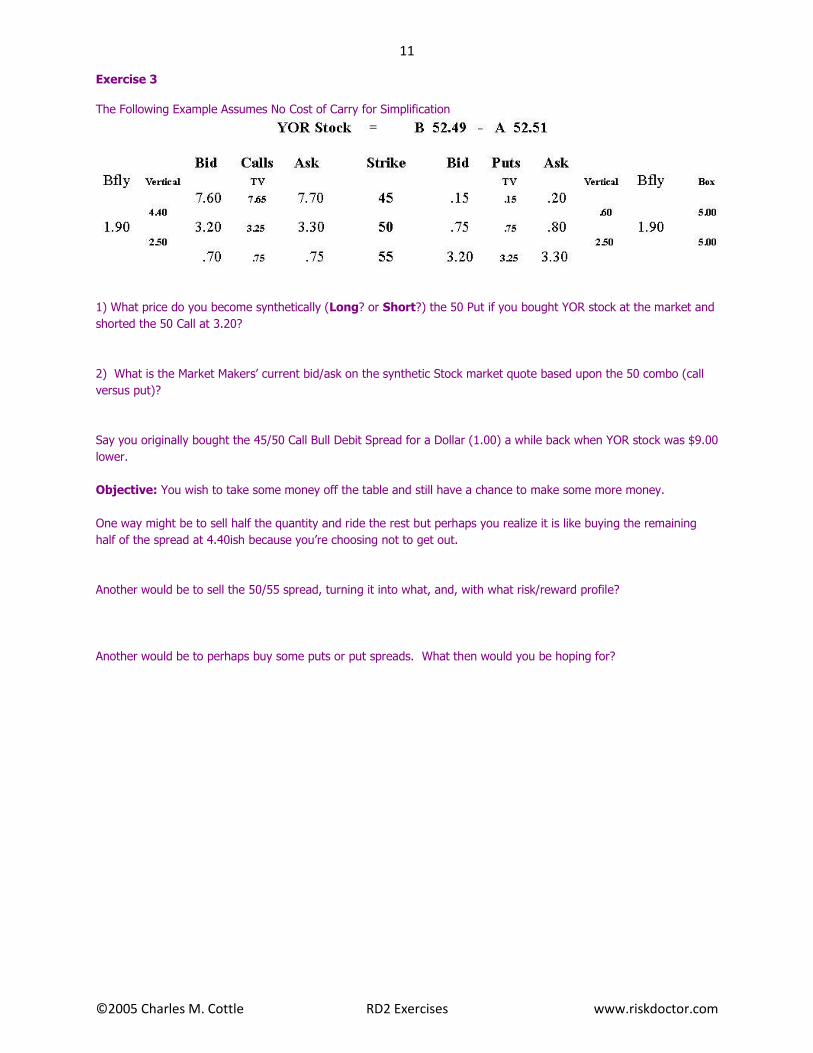

Exercise 3

The Following Example Assumes No Cost of Carry for Simplification

1) What price do you become synthetically (Long? or Short?) the 50 Put if you bought YOR stock at the market and

shorted the 50 Call at 3.20?

2) What is the Market Makers’ current bid/ask on the synthetic Stock market quote based upon the 50 combo (call

versus put)?

Say you originally bought the 45/50 Call Bull Debit Spread for a Dollar (1.00) a while back when YOR stock was $9.00

lower.

Objective: You wish to take some money off the table and still have a chance to make some more money.

One way might be to sell half the quantity and ride the rest but perhaps you realize it is like buying the remaining

half of the spread at 4.40ish because you’re choosing not to get out.

Another would be to sell the 50/55 spread, turning it into what, and, with what risk/reward profile?

Another would be to perhaps buy some puts or put spreads. What then would you be hoping for?

12

©2005 Charles M. Cottle RD2 Exercises www.riskdoctor.com

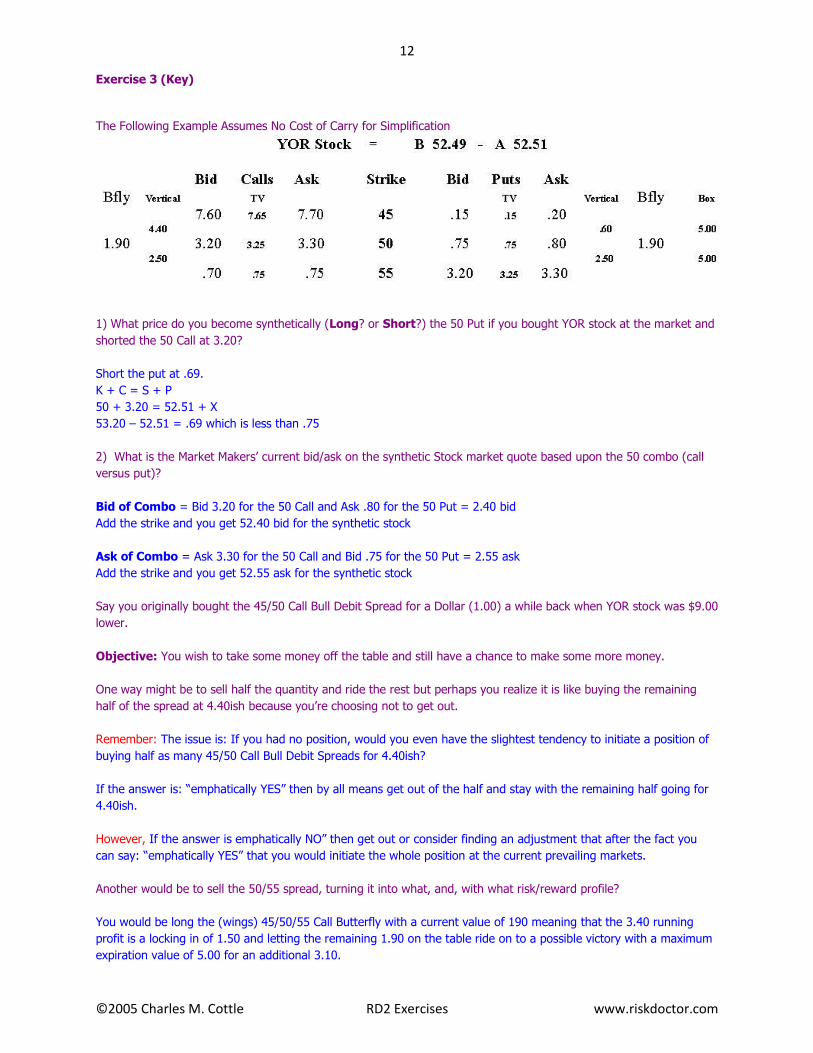

Exercise 3 (Key)

The Following Example Assumes No Cost of Carry for Simplification

1) What price do you become synthetically (Long? or Short?) the 50 Put if you bought YOR stock at the market and

shorted the 50 Call at 3.20?

Short the put at .69.

K + C = S + P

50 + 3.20 = 52.51 + X

53.20 – 52.51 = .69 which is less than .75

2) What is the Market Makers’ current bid/ask on the synthetic Stock market quote based upon the 50 combo (call

versus put)?

Bid of Combo = Bid 3.20 for the 50 Call and Ask .80 for the 50 Put = 2.40 bid

Add the strike and you get 52.40 bid for the synthetic stock

Ask of Combo = Ask 3.30 for the 50 Call and Bid .75 for the 50 Put = 2.55 ask

Add the strike and you get 52.55 ask for the synthetic stock

Say you originally bought the 45/50 Call Bull Debit Spread for a Dollar (1.00) a while back when YOR stock was $9.00

lower.

Objective: You wish to take some money off the table and still have a chance to make some more money.

One way might be to sell half the quantity and ride the rest but perhaps you realize it is like buying the remaining

half of the spread at 4.40ish because you’re choosing not to get out.

Remember: The issue is: If you had no position, would you even have the slightest tendency to initiate a position of

buying half as many 45/50 Call Bull Debit Spreads for 4.40ish?

If the answer is: “emphatically YES” then by all means get out of the half and stay with the remaining half going for

4.40ish.

However, If the answer is emphatically NO” then get out or consider finding an adjustment that after the fact you

can say: “emphatically YES” that you would initiate the whole position at the current prevailing markets.

Another would be to sell the 50/55 spread, turning it into what, and, with what risk/reward profile?

You would be long the (wings) 45/50/55 Call Butterfly with a current value of 190 meaning that the 3.40 running

profit is a locking in of 1.50 and letting the remaining 1.90 on the table ride on to a possible victory with a maximum

expiration value of 5.00 for an additional 3.10.

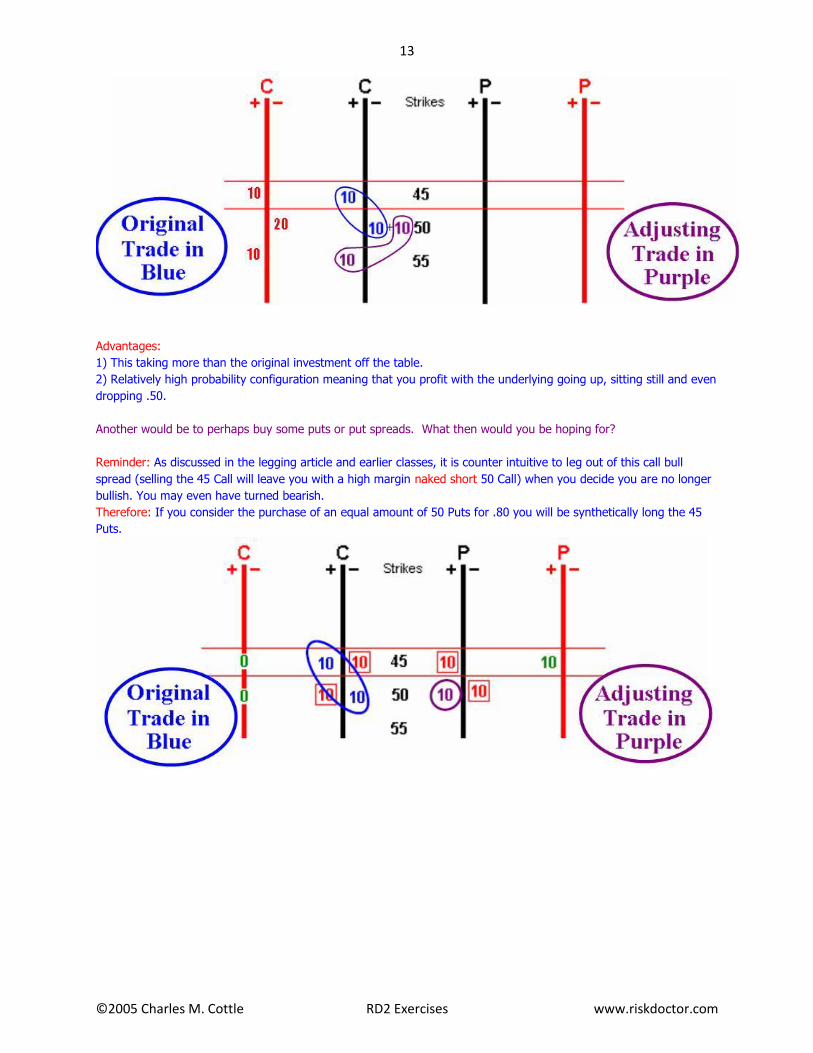

13

©2005 Charles M. Cottle RD2 Exercises www.riskdoctor.com

Advantages:

1) This taking more than the original investment off the table.

2) Relatively high probability configuration meaning that you profit with the underlying going up, sitting still and even

dropping .50.

Another would be to perhaps buy some puts or put spreads. What then would you be hoping for?

Reminder: As discussed in the legging article and earlier classes, it is counter intuitive to leg out of this call bull

spread (selling the 45 Call will leave you with a high margin naked short 50 Call) when you decide you are no longer

bullish. You may even have turned bearish.

Therefore: If you consider the purchase of an equal amount of 50 Puts for .80 you will be synthetically long the 45

Puts.

14

©2005 Charles M. Cottle RD2 Exercises www.riskdoctor.com

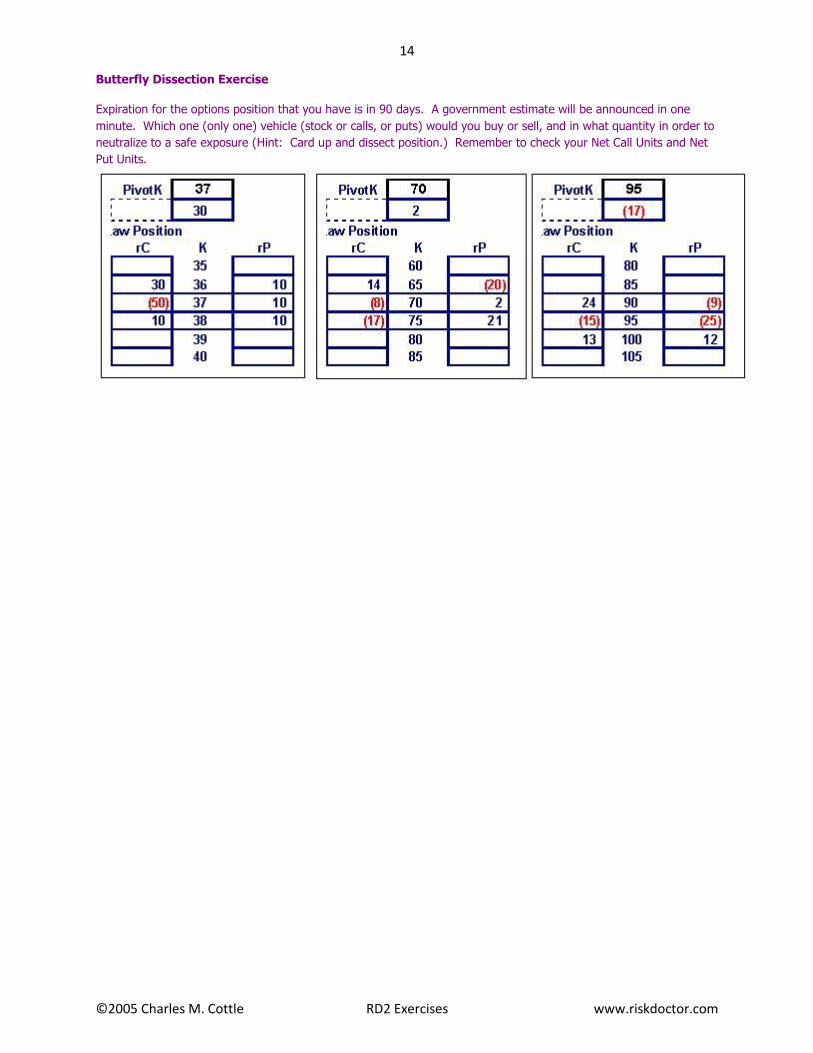

Butterfly Dissection Exercise

Expiration for the options position that you have is in 90 days. A government estimate will be announced in one

minute. Which one (only one) vehicle (stock or calls, or puts) would you buy or sell, and in what quantity in order to

neutralize to a safe exposure (Hint: Card up and dissect position.) Remember to check your Net Call Units and Net

Put Units.

15

©2005 Charles M. Cottle RD2 Exercises www.riskdoctor.com

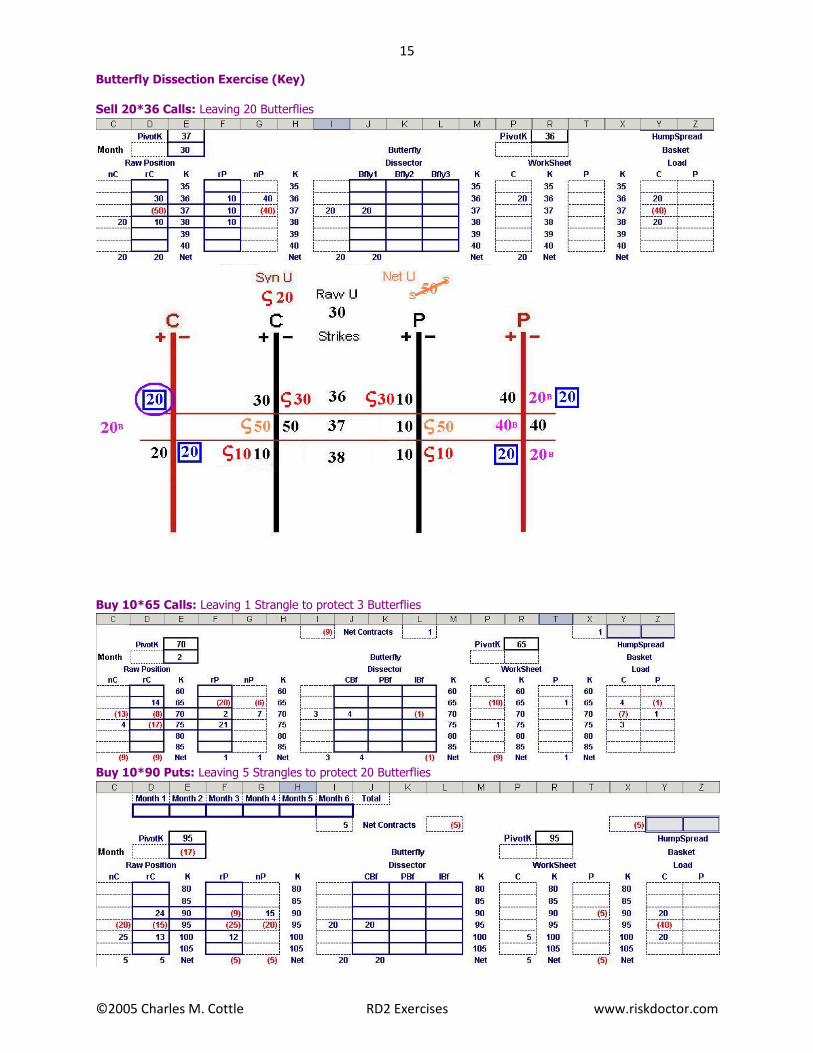

Butterfly Dissection Exercise (Key)

Sell 20*36 Calls: Leaving 20 Butterflies

Buy 10*65 Calls: Leaving 1 Strangle to protect 3 Butterflies

Buy 10*90 Puts: Leaving 5 Strangles to protect 20 Butterflies