“Taking Action” With Your Farm Accounting System Farm Business Planning 101 – January 24 th 2015 MN Farm Bureau Leadership Conference Pete Henslin – VP Agriculture/Business Banking Owatonna, MN Pam Uhlenkamp – Farm Business Management Instructor Southern Minnesota Center of Agriculture

Transcript

“Taking Action” With Your Farm Accounting System

Farm Business Planning 101 – January 24th 2015 MN Farm Bureau Leadership Conference

Pete Henslin – VP Agriculture/Business Banking Owatonna, MN

Pam Uhlenkamp – Farm Business Management InstructorSouthern Minnesota Center of Agriculture

2

Agenda For Today

• The Importance Of Farm Records

• Characteristics of Record Keeping systems

• How the Accuracy of Farm Records Can Affect Your Operation

• The “C”s of Credit

• Preparing For Your Lender

• Beginning Farmer Lending Options

• Questions /Discussion

3

Importance Of Farm Records

• Three Main Reasons For A Good Farm Record Keeping System

Income Tax Reporting

Obtaining Credit

Management Tool

4

Records For Income Tax Reporting

• Income and Expenses Categories Need to Match Schedule “F”

• Good Records will dictate a fair taxable income rate.

• Deprecation Schedules for prorating original costs of Assets Purchased and Capital Gains Tax on Asset Sales

5

Records For Obtaining Credit

• Financial Records Beyond Income and Expense Records

• Balance Sheet

• Income Statement

• Cash Flow Statements

• Cost of Production

• Demonstration of Loan Repayment Capacity

6

Records For Management Tool

• Financial

• Production

• Risk

• Marketing

• Personnel

• Strategic

7

Characteristics Of Record Keeping Systems

• KISS

• Appropriate Level of Detail

• Your Records Should Provide Essential Information On A Timely Basis

• Integration of Financial and Production Information

8

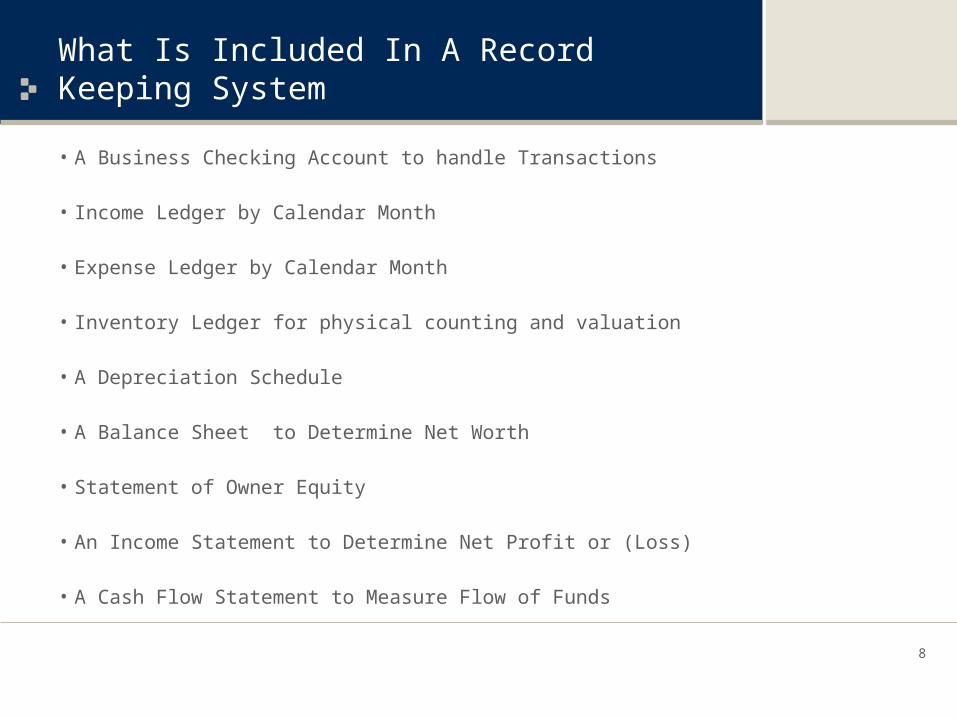

What Is Included In A Record Keeping System

• A Business Checking Account to handle Transactions

• Income Ledger by Calendar Month

• Expense Ledger by Calendar Month

• Inventory Ledger for physical counting and valuation

• A Depreciation Schedule

• A Balance Sheet to Determine Net Worth

• Statement of Owner Equity

• An Income Statement to Determine Net Profit or (Loss)

• A Cash Flow Statement to Measure Flow of Funds

9

The “C”s of Credit

• Character

• Capital

• Capacity

• Collateral

• Conditions

• Common Sense/Cranium

10

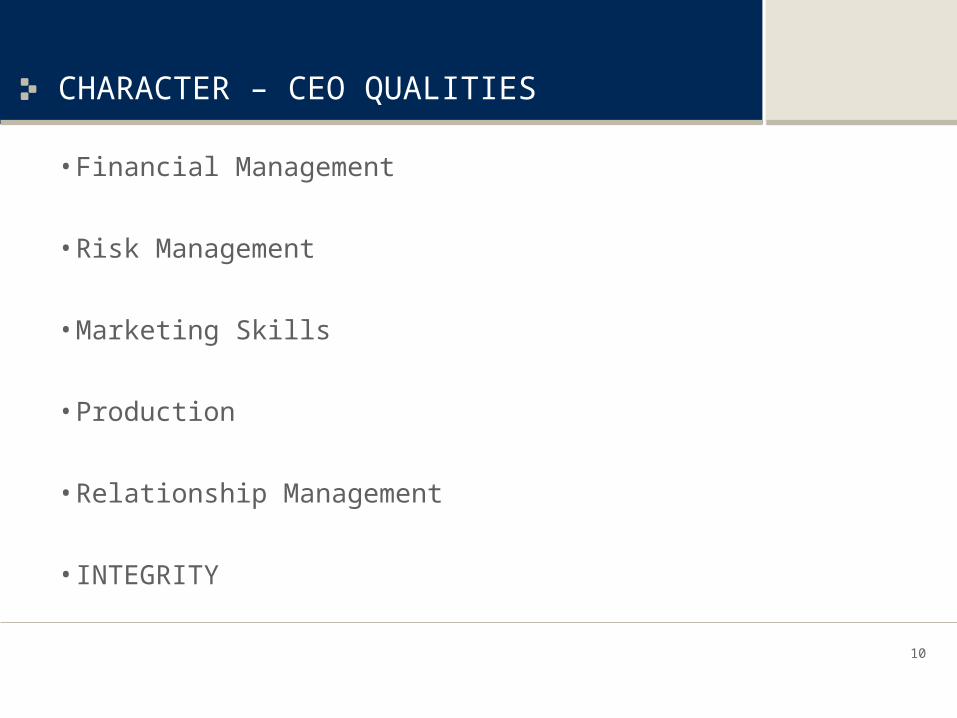

CHARACTER – CEO QUALITIES

• Financial Management

• Risk Management

• Marketing Skills

• Production

• Relationship Management

• INTEGRITY

11

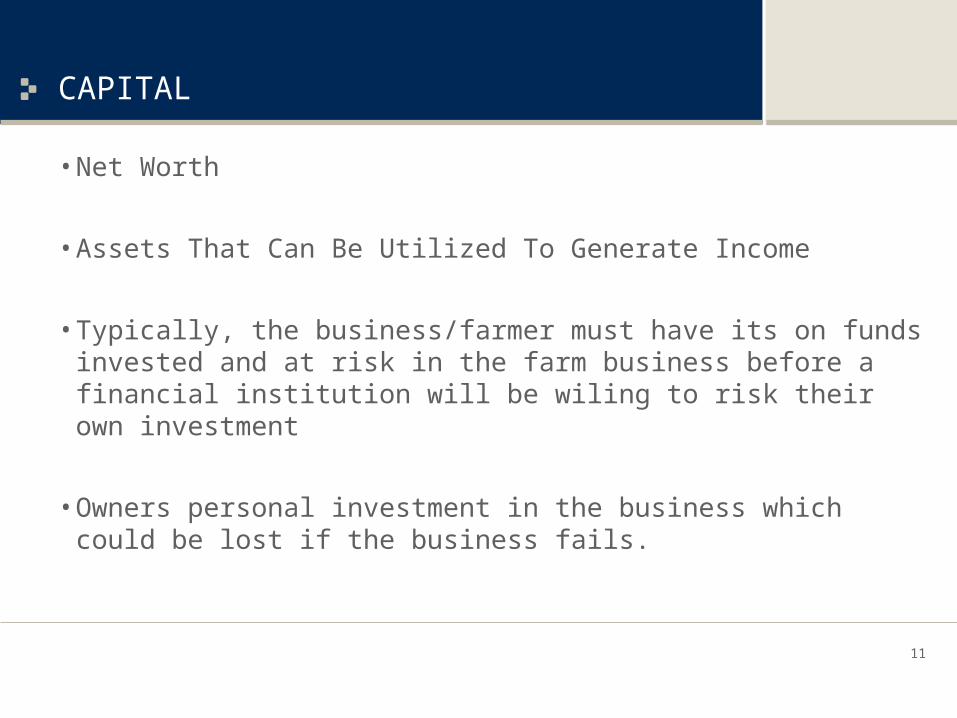

CAPITAL

• Net Worth

• Assets That Can Be Utilized To Generate Income

• Typically, the business/farmer must have its on funds invested and at risk in the farm business before a financial institution will be wiling to risk their own investment

• Owners personal investment in the business which could be lost if the business fails.

12

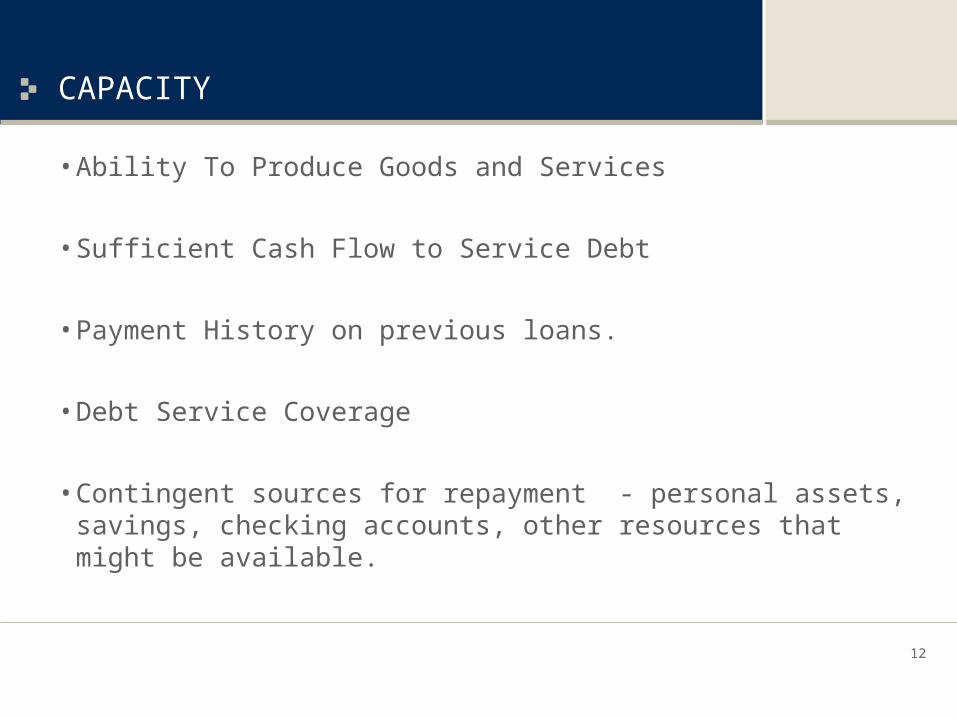

CAPACITY

• Ability To Produce Goods and Services

• Sufficient Cash Flow to Service Debt

• Payment History on previous loans.

• Debt Service Coverage

• Contingent sources for repayment - personal assets, savings, checking accounts, other resources that might be available.

13

COLLATERAL

• Assets to Secure Debt

• Market Value as what could be generated upon sale

• Type of Asset determines advance rate and length of allowable repayment period.

• Useful Life Of Asset – Short - Intermediate - Long Term • Crop inventory • Machinery • Livestock • Titled Vehicles • Buildings/Facilities • Land

14

CONDITIONS

• Borrower and Overall Economy

• An Event, Action or Obligation That Must Be Fulfilled Or Completed Before Another Proposition Is Fulfilled

• Often Associated With Contracts

• General Purpose of the Loan • Increase Income or Reduce Expenses

15

COMMON SENSE/CRANIUM

• Importance of Personal Relationships

• Communication Skills

• Vision/Values

• Realistic Expectations

• Problem Solving Ability

16

Top 10 Things To Do Before Seeing Your Lender

• Be Prepared to Tell Your StoryBe Prepared to Tell Your Story• An Introduction to Your Management TeamAn Introduction to Your Management Team• Know How Much You Need To Borrow and WhyKnow How Much You Need To Borrow and Why• Get Your Financial House In OrderGet Your Financial House In Order• Understand Your Internal/External Historical Cash Flow SourcesUnderstand Your Internal/External Historical Cash Flow Sources• Prepare A Capital Expenditure BudgetPrepare A Capital Expenditure Budget• Know What You OweKnow What You Owe• Complete Credit Request PackageComplete Credit Request Package• The UnmentionablesThe Unmentionables• Be Prepared For The MeetingBe Prepared For The Meeting

17

Two Definitions To Help You “Take Action”

• INSANITY

•Expecting different results while continuing to do the same things ……. The same way

•STRESS

•Stress comes from knowing what is right and doing what is wrong.

18

“Take Action” - Keep Sane and Avoid Stress

• Examine New Recommendations That Will Preserve Capital Without Abandoning Tactics That Have Proved Valuable In The Past

• Develop A Financial Plan & A Business Plan- In Writing

• Save At Least 10% Of Your Earnings

• Manage All Your Resources Wisely – especially long term assets

• Keep Debt to a Minimum

• Spend Less Than You Make

• Build A Cash Reserve - called ‘Working Capital’

• Insure Risk Where Possible

• Watch Your Health – physical, mental, spiritual

Producers That Will Thrive

• Strong Productive Asset Base • Records That Talk To the Business• Modest Living Expenses • Modest Non-Farm Capital Expenses • Working Capital – 33% of Revenue • Burn Rate of Working Capital Above 3.5 years • Know Cost of Production via Enterprise• Strategy/Alternatives• History of Handling Adversity • Are Not “Victims” NOR “Know It All’s”

19

Two Definitions To Help You “Take Action”

• INSANITY

•Expecting different results while continuing to do the same things ……. The same way

•STRESS

•Stress comes from knowing what is right and doing what is wrong.

20

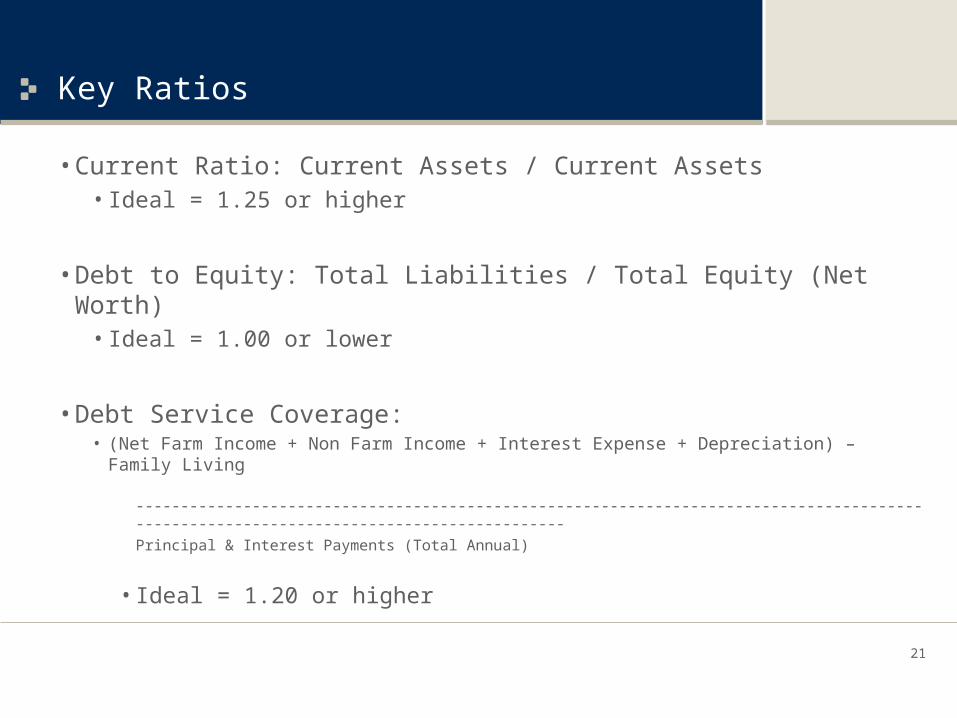

Key Ratios

• Current Ratio: Current Assets / Current Assets• Ideal = 1.25 or higher

• Debt to Equity: Total Liabilities / Total Equity (Net Worth)• Ideal = 1.00 or lower

• Debt Service Coverage:• (Net Farm Income + Non Farm Income + Interest Expense + Depreciation) – Family Living