1 1 BUDGET 2008 LEMBAGA HASIL DALAM NEGERI MALAYSIA 2 BUDGET 2008 THREE MAIN STRATEGIES 1.Enhancing the nation’s competitiveness 2. Strengthening human capital development 3. Ensuring the well-being of all Malaysians

Transcript

1

1

BUDGET 2008

LEMBAGA HASIL DALAM

NEGERI MALAYSIA

2

BUDGET 2008

THREE MAIN STRATEGIES

1.Enhancing the nation’s competitiveness

2. Strengthening human capital

development

3. Ensuring the well-being of all Malaysians

2

3

Overview of Presentation

1. Amendments to Legislation

- Income Tax Act 1967

- Petroleum Income Tax Act 1967

- Stamp Act 1949

- Labuan Off Shore Business Activity Tax Act (LOBATA 1990)

2. Rules

3. Exemption Orders

4

PART 1

AMENDMENTS TO

INCOME TAX ACT 1967

3

5

Offshore Business Activity

Current provision – subsec. 44(11A)

– sec. 3B

• Offshore business activity not subject to

tax under ITA 1967

Proposal

• Offshore company may make irrevocable

election under LOBATA charged to tax

under ITA

• Zakat deduction from aggregate income

wef YA 2008

6

Special Deduction for Business

Current provision – para. 34(6)(e)

• Special deduction in ascertaining the

adjusted income of a business.

• Provision of equipment to assist disabled

person

• Deduction = amount of expenditure

cont.

4

7

Special Deduction for Business

Proposal – para. 34(6)(e)

• Deduction extended to alteration or

renovation of premises to assist disabled

person

• No more deduction or allowance under

section 33 or schedule 3 in respect of the

same expenditure

wef YA 2008

8

Special Deduction for Business

• RM5,000 – renovation of restroom

• RM10,000 – walkway (capitalized as part

of cost of factory building &

not claimed IBA)

RM15,000 qualifies for deduction

Example 1

Kilang Maju S/B expended the following for its disabled workers

5

9

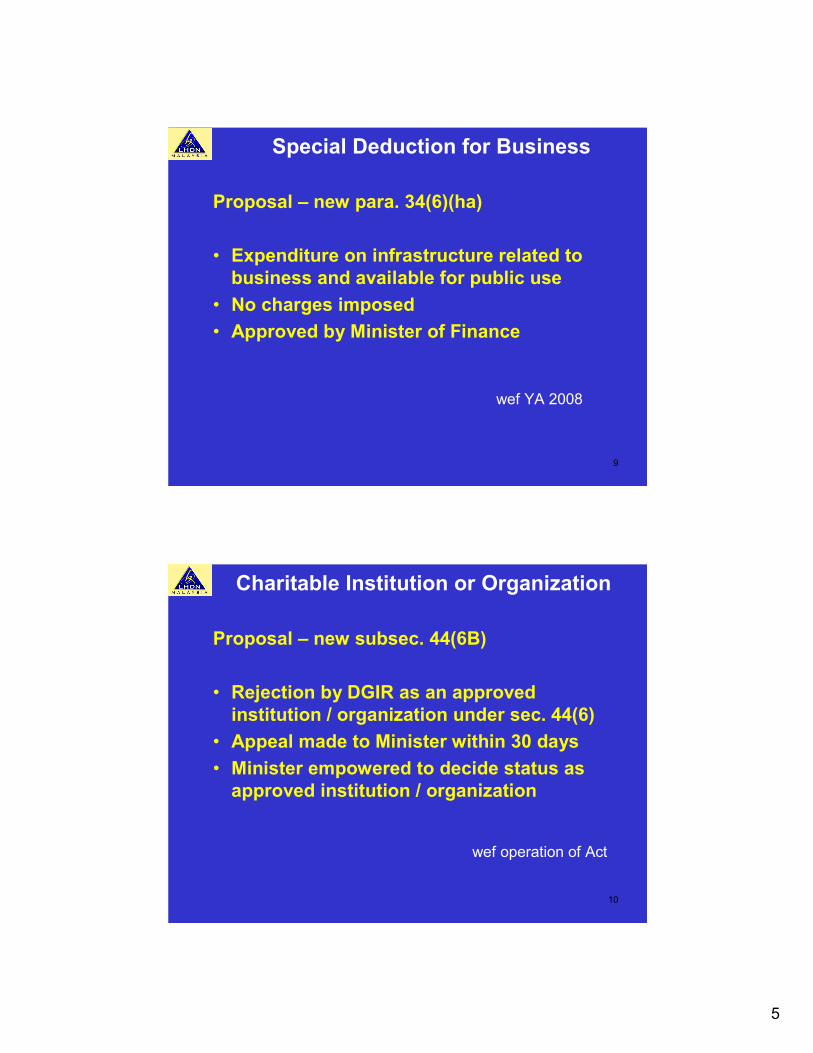

Special Deduction for Business

Proposal – new para. 34(6)(ha)

• Expenditure on infrastructure related to

business and available for public use

• No charges imposed

• Approved by Minister of Finance

wef YA 2008

10

Charitable Institution or Organization

Proposal – new subsec. 44(6B)

• Rejection by DGIR as an approved

institution / organization under sec. 44(6)

• Appeal made to Minister within 30 days

• Minister empowered to decide status as

approved institution / organization

wef operation of Act

6

11

Deduction for Individual

Current provision – para. 46(1)(f)

• Deduction for further education up to

tertiary level in selected courses of study

• Recognized institution or professional

body in Malaysia

• Maximum deduction of RM5,000

Proposal – para. 46(1)(f) (amended)

• Deduction for all courses of study at

Masters or Doctorate levelwef YA 2008

12

Deduction for Individual

Proposal – new para. 46(1)(k)

• Relief given to parents for savings in

Skim Simpanan Pendidikan Nasional

(SSPN)

• Maximum amount RM3,000 each parent

who contributes for the child / children

wef YA 2007

7

13

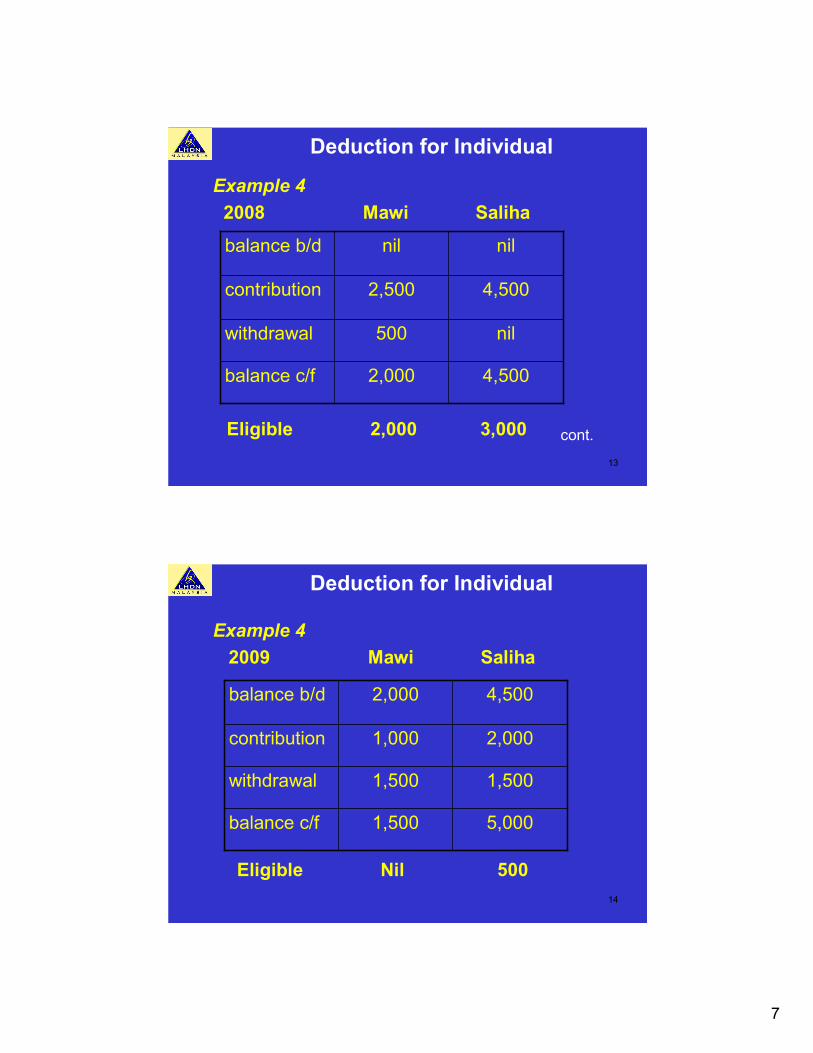

Deduction for Individual

Example 4

2008 Mawi Saliha

cont.

4,5002,000balance c/f

nil500withdrawal

4,5002,500contribution

nilnilbalance b/d

Eligible 2,000 3,000

14

Deduction for Individual

Example 4

2009 Mawi Saliha

5,0001,500balance c/f

1,5001,500withdrawal

2,0001,000contribution

4,5002,000balance b/d

Eligible Nil 500

8

15

Deduction for Individual

• Defined under Sports Development Act 1997

• Maximum relief RM300

• Evidenced by receipt

wef YA 2008

Proposal – new para. 46(1)(l)

Deduction for amount expended on purchase

of sports equipment

16

Deduction for Individual

Proposal – deletion of sec. 46A

• Deduction for interest expended to

finance the purchase of a first residential

property for YAs 2003 – 2005

• Period for deduction has ceased

wef YA 2006

9

17

Deduction for Individual

Current provision – sec. 44(6)

• Donation to approved institutions /

organizations by companies restricted to

7% of aggregate income

Proposal

• 7% restriction extended to donation made

by persons other than companies

wef YA 2008

18

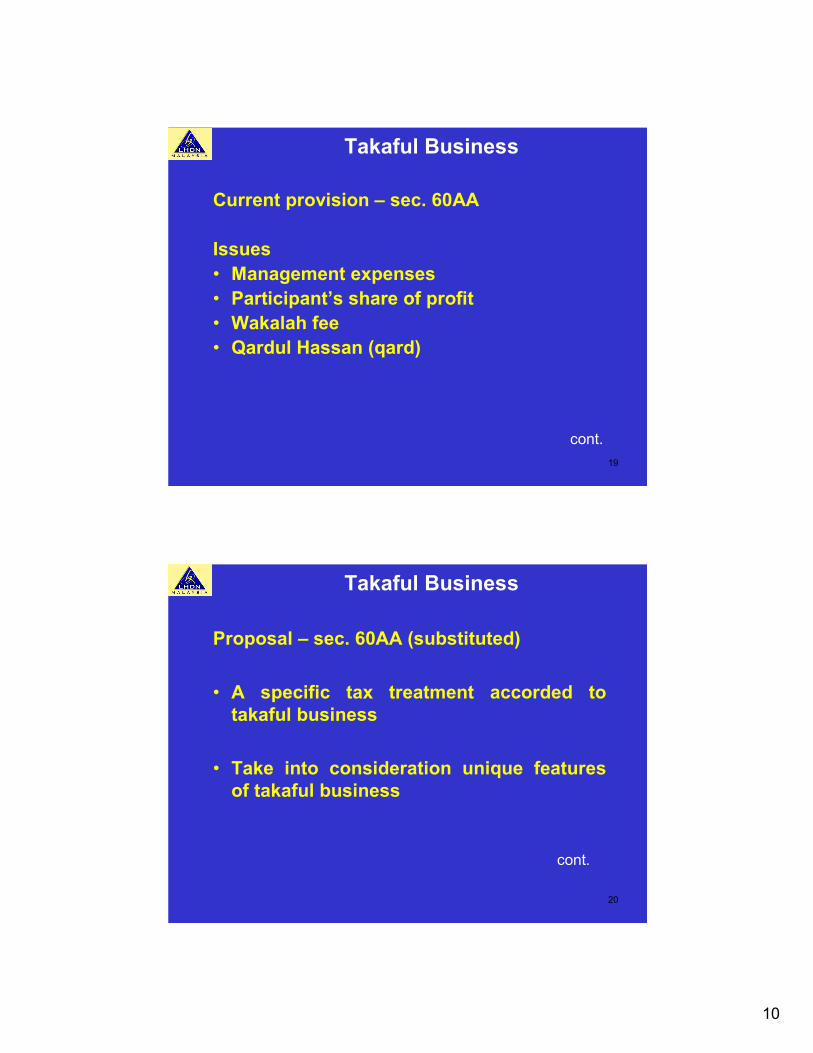

Takaful Business

Current provision – sec. 60AA

• No specific tax treatment in ITA 1967

• Provisions of conventional insurance

applied mutatis mutandis to takaful

cont.

10

19

Takaful Business

Current provision – sec. 60AA

Issues

• Management expenses

• Participant’s share of profit

• Wakalah fee

• Qardul Hassan (qard)

cont.

20

Takaful Business

Proposal – sec. 60AA (substituted)

• A specific tax treatment accorded to

takaful business

• Take into consideration unique features

of takaful business

cont.

11

21

Takaful Business

Proposal - new sec. 109E & Part XI Sch. 1

Withholding tax on participants’ share of

profit from takaful business - investment

income portion only

• To be remitted by operator

• Individuals – 8%

• Non-resident companies – 26%

wef 01/01/2008

22

Access to documents, etc

Current provision – sec. 80(1) & 80(2)

DGIR has power-

• to access to lands, buildings and places

• to inspect, copy or make extracts from any such books or document

• to take possession of books and documents

Proposal – sec. 80(1) & 80(2) (amended)

• To extend effective power of DGIR, to take

possession of objects, articles, materials and things

wef operation of Act

12

23

Small & Medium companies

Proposal – new subsec. 107C(4A)

SME commences operation in a YA -

• Need not furnish an estimate

• Need not pay monthly instalments for 2 YAs

• Tax payable to be paid on due date

wef YA 2008

24

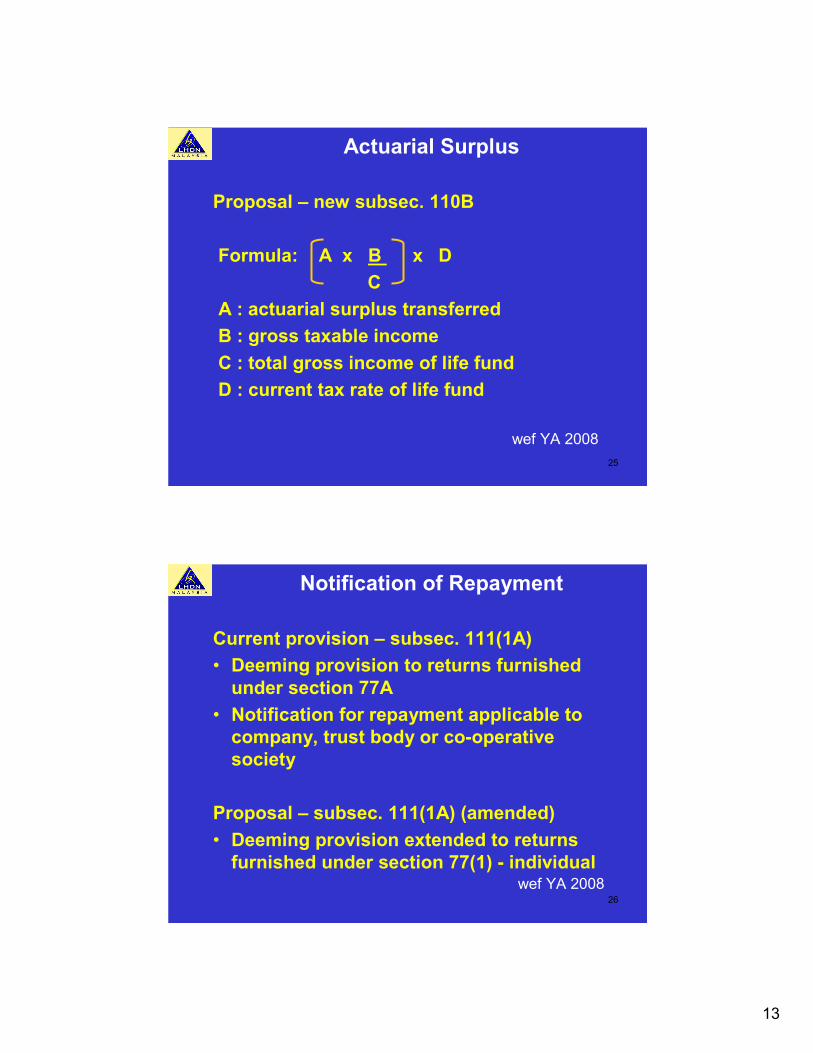

Actuarial Surplus

Current provision – sec. 60

• Actuarial surplus transferred from life fund to shareholders’ fund – taxed twice

Proposal – new sec. 110B

• Deduction be given against tax charged on shareholders’ fund

• Amount of deduction based on formula

prescribed by Minister

• Unabsorbed amount disregarded

cont.

13

25

Actuarial Surplus

Proposal – new subsec. 110B

Formula: A x B x D

C

A : actuarial surplus transferred

B : gross taxable income

C : total gross income of life fund

D : current tax rate of life fund

wef YA 2008

26

Notification of Repayment

Current provision – subsec. 111(1A)

• Deeming provision to returns furnished

under section 77A

• Notification for repayment applicable to

company, trust body or co-operative

society

Proposal – subsec. 111(1A) (amended)

• Deeming provision extended to returns

furnished under section 77(1) - individualwef YA 2008

14

27

Admissibility of electronic record

Proposal – new sec. 142A

• Prescribed form / documents by

electronic medium / transmission to DGIR

• Copy / print-out of electronic record

admissible as evidence in court

• Electronic medium – process where data,

text, images or any other information is

stored, received or communicated by

electronic, magnetic, optical, imaging or

other data processing devicewef operation of Act

28

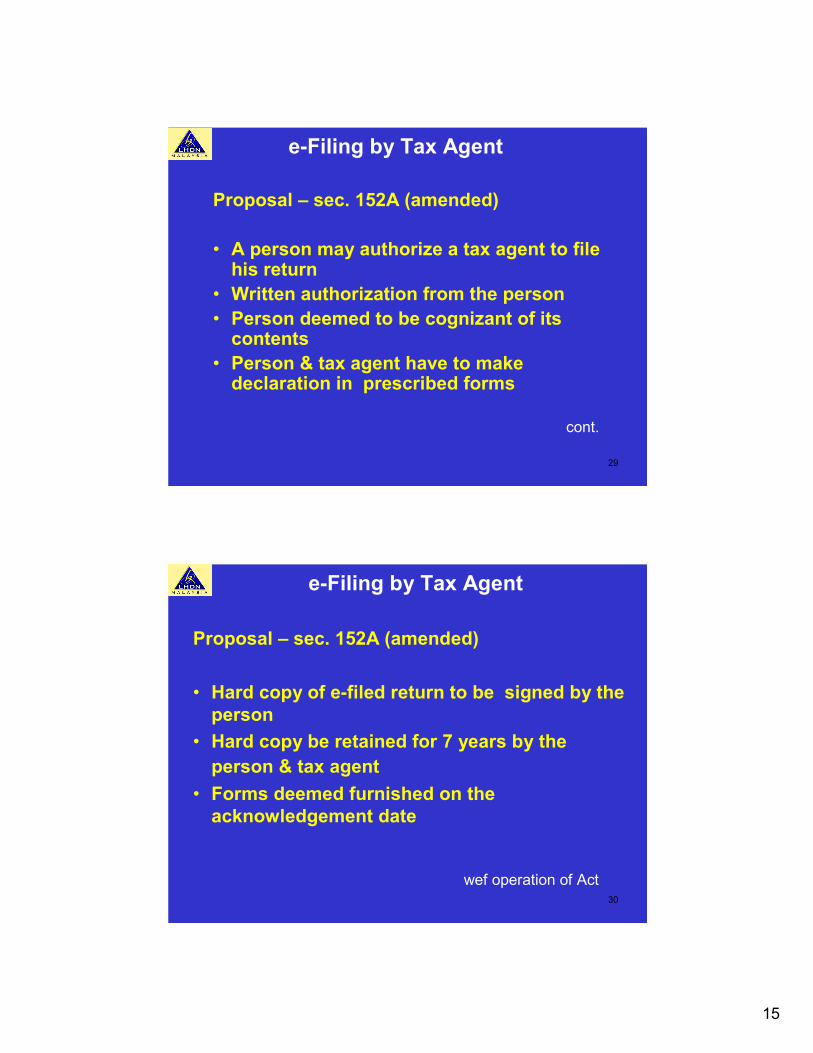

e-Filing by Tax Agent

Current provision – sec.152A

• Prescribed form filed by any person on

his own

• Filing through electronic medium /

electronic transmission

cont.

15

29

e-Filing by Tax Agent

Proposal – sec. 152A (amended)

• A person may authorize a tax agent to file his return

• Written authorization from the person

• Person deemed to be cognizant of its contents

• Person & tax agent have to make declaration in prescribed forms

cont.

30

e-Filing by Tax Agent

Proposal – sec. 152A (amended)

• Hard copy of e-filed return to be signed by the

person

• Hard copy be retained for 7 years by the

person & tax agent

• Forms deemed furnished on the

acknowledgement date

wef operation of Act

16

31

Tax Agent

Current provision – subsec. 153(6)

• Renewal of approval for tax agent –

24 months

Proposal

• Minimum period 24 months

• Extended period approved by the Minister

wef 21 Feb 2007

32

Tax Rate

2

1 & 3

Group

26% (YA 2008)

25% (YA 2009 et seq)

27% (YA 2007)

26% (YA 2008)

25% (YA 2009 et seq)

CI > RM500K

27% (YA 2007)

ProposalCurrent

1. Company, trust body, executor and receiver

– para. 2 Sch. 1

2. Company with paid up capital not more than RM2.5m

– para. 2A Sch. 1

3. Withholding tax NR company receives income from REIT

– subpara. 1(b), Part X Sch. 1

wef YA 2008

17

33

Disposal of Industrial Building

Proposal – new para. 38A Sch. 3

Company disposes industrial building to

REIT / property trust fund

• Para. 39 & 40 Sch. 3 apply

• No BC / BA

• RE of Co = QE of REIT

wef YA 2008

34

Hearing of Appeals

Current provision – Sch. 5

• Only one hearing of appeal by the Special

Commissioners (SCIT) may be heard at any one

time (para.1(3))

• No provision to continue hearing if term of

SCIT expired or other reason

• No authority to dismiss appeal (subsubpara

17(1)(b) & 17(2)(a))

cont.

18

35

Hearing of Appeals

Proposal – Sch. 5 (amended)

• More than one hearing of appeal by the

SCIT can be heard concurrently (para

(1)(3))

• Hearing continued or heard afresh (new

para 1A)

• Extend authority of SCIT to dismiss

appeal (subsubpara 17(1)(b) & 17(2)(a))

wef operation of Act

36

Exemption on Gratuity

Current provision – subsubpara. 25(1)(c) Sch.6

• Partial exemption of gratuity received by private

sector employee on reaching retirement age at

the age of 50 but less than 55 years

• RM6,000 for every year of completed service

Proposal – subsubpara. 25(1)(c) Sch.6 (amended)

• Full exemption on gratuity received by private

sector employee on reaching retirement age

wef YA 2007

19

37

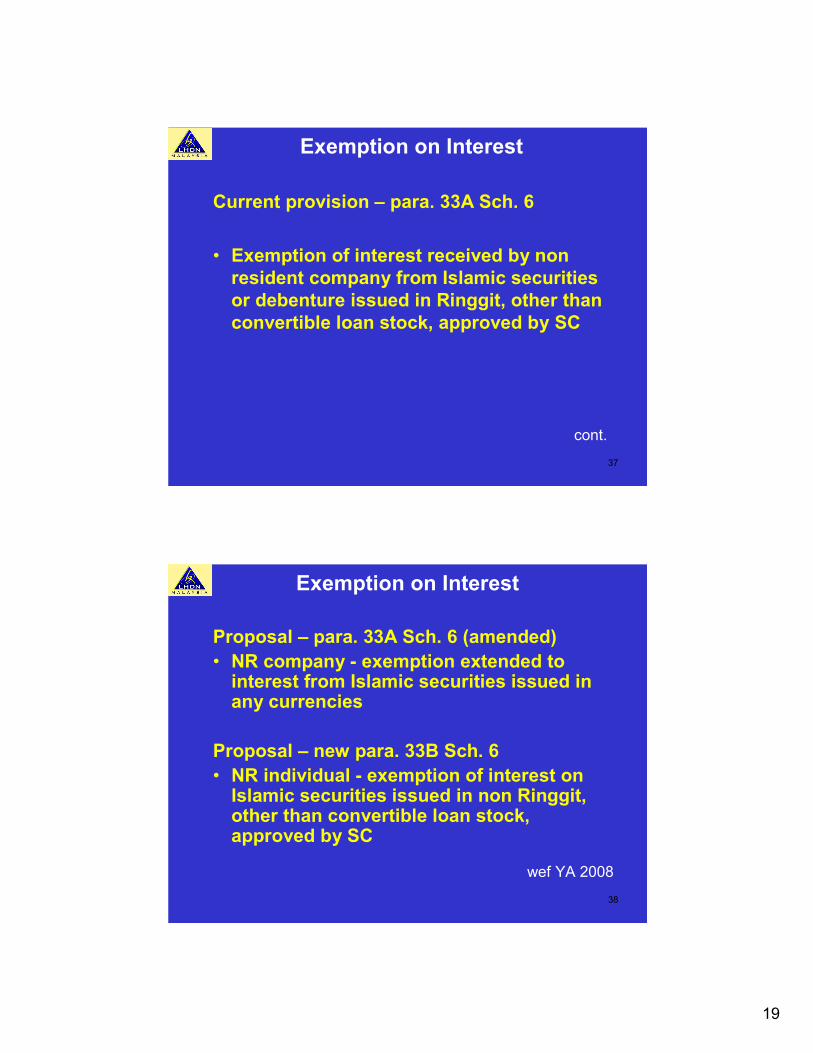

Exemption on Interest

Current provision – para. 33A Sch. 6

• Exemption of interest received by non

resident company from Islamic securities

or debenture issued in Ringgit, other than

convertible loan stock, approved by SC

cont.

38

Exemption on Interest

Proposal – para. 33A Sch. 6 (amended)

• NR company - exemption extended to interest from Islamic securities issued in any currencies

Proposal – new para. 33B Sch. 6

• NR individual - exemption of interest on Islamic securities issued in non Ringgit, other than convertible loan stock, approved by SC

wef YA 2008

20

39

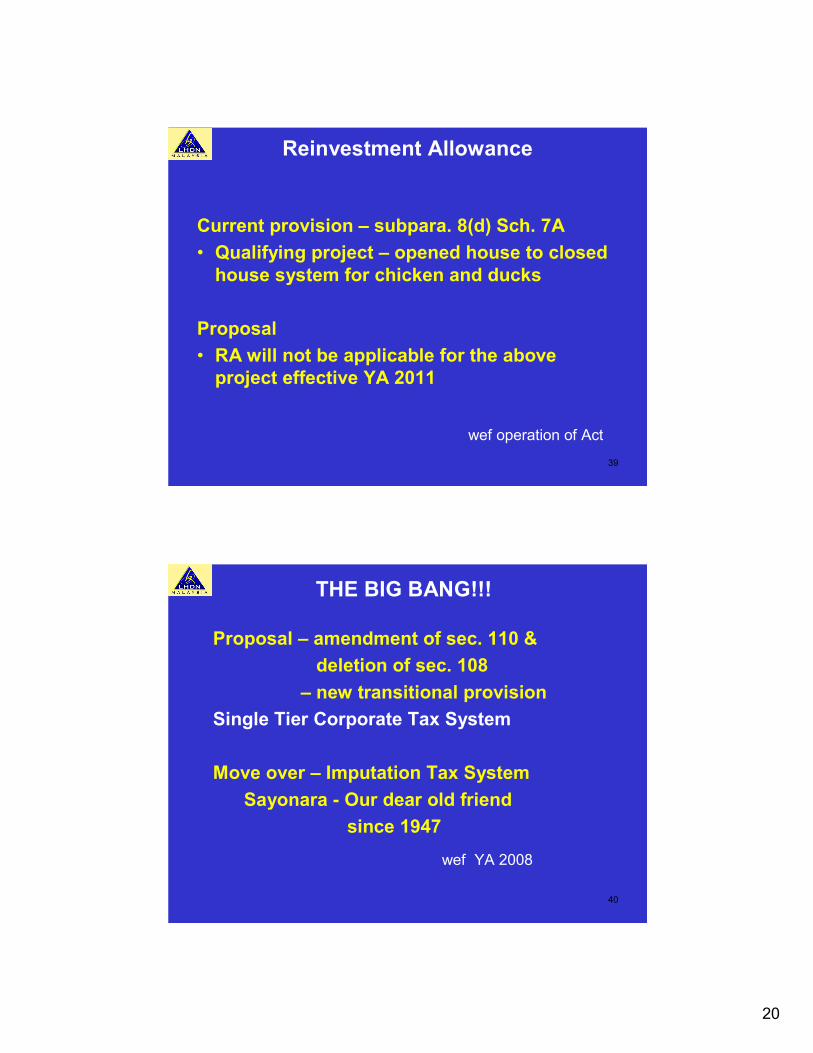

Reinvestment Allowance

Current provision – subpara. 8(d) Sch. 7A

• Qualifying project – opened house to closed

house system for chicken and ducks

Proposal

• RA will not be applicable for the above

project effective YA 2011

wef operation of Act

40

THE BIG BANG!!!

Proposal – amendment of sec. 110 &

deletion of sec. 108

– new transitional provision

Single Tier Corporate Tax System

Move over – Imputation Tax System

Sayonara - Our dear old friend

since 1947

wef YA 2008

21

41

• Tax paid by companies

not final tax

• Tax paid pass to s/holders

as tax credit

• S/holders taxed on gross

dividend & credit sec.110

given

• sec.108 account

mechanism

Imputation vs Single Tier System

• Tax paid by companies is

final tax

• Dividend exempt in s/holders’

hand (single tier dividend)

• No sec.108 & sec.110

• Effective from YA 2008

• Unutilized sec.108 account ?

Imputation System Single Tier System

cont

42

Single Tier Tax System

Consequential amendments

• subsec. 54A(3), 67(4), sec. 110A, 110B,

111A, 120 & 127

• subpara. 13(1), para. 17 & 26 – sch. 6

• subpara. 5(7) – sch. 7A

wef YA 2008

22

43

AMENDMENTS TO

PETROLEUM INCOME TAX 1967

44

PITA 1967

Proposal – subsec.16(7A) (amended)

• Deduction extended to alteration /

renovation of premises to assist disabled

person

Proposal – new subsec. 16(7BA)

• Expenditure on infrastructure for business

available for public use

• No charges imposed

• Approved by Minister of Finance

wef YA 2009

23

45

PITA 1967

Proposal – subsec. 33(1) & 33(2) (amended)

• To extend DGIR’s power to take possession of objects, articles, materials and things

Proposal – subpara. 1(3) Sch. 3

• More than one hearing of appeal by the Special Commissioners (SCIT) can be heard concurrently

wef operation of Act

46

PITA 1967

Proposal – new para. 1A ,

– subpara.15(b) Sch. 3

• Appeals not concluded due to - term of appointment of the SCIT expires or other reason (hearing continued or heard afresh)

• Extend authority of SCIT to dismiss appeal

wef operation of Act

24

47

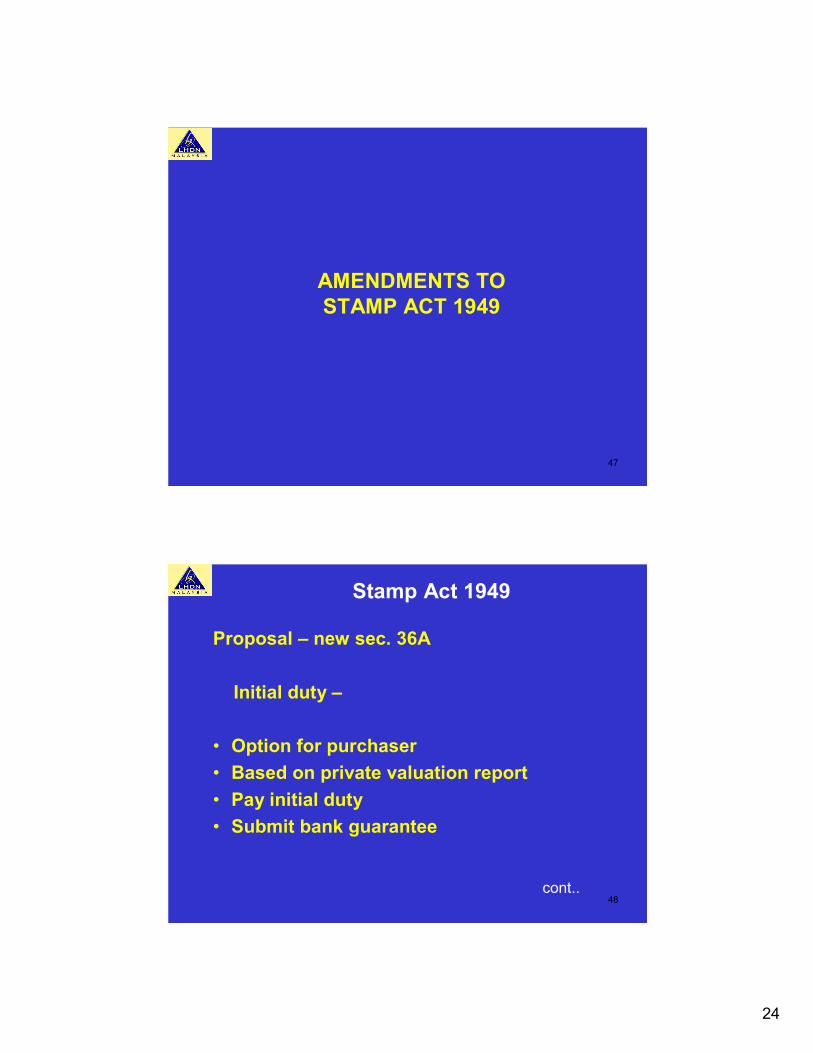

AMENDMENTS TO

STAMP ACT 1949

48

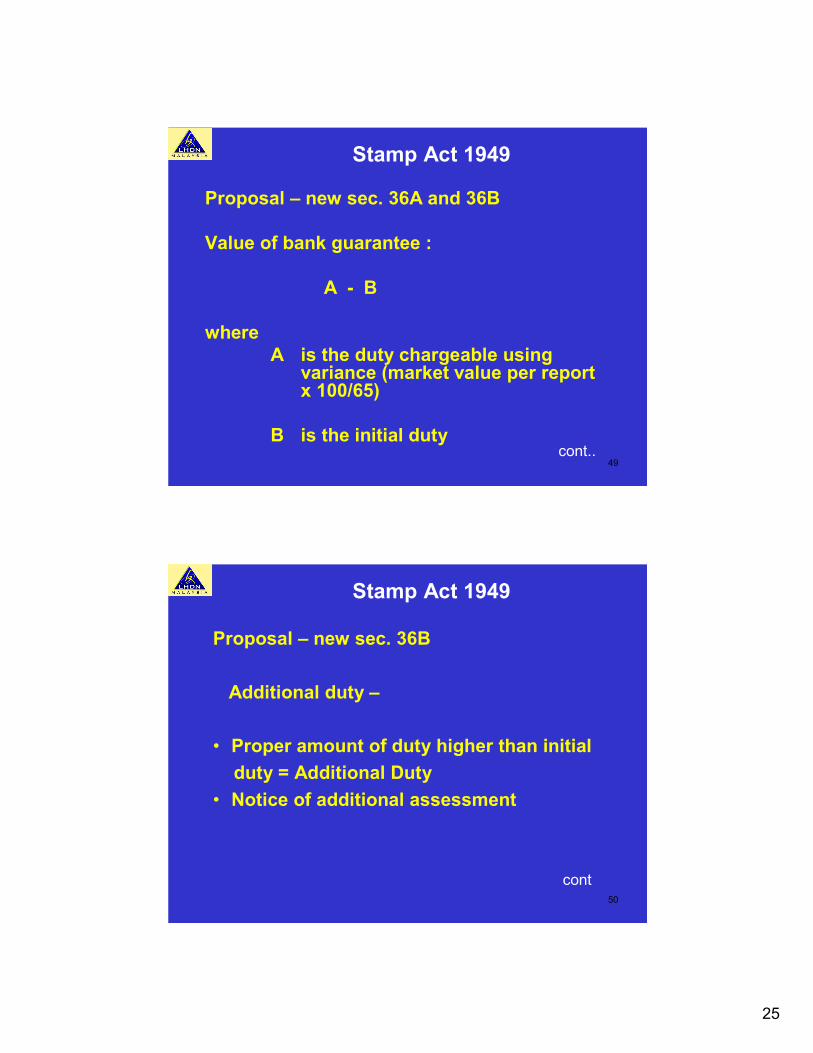

Stamp Act 1949

Proposal – new sec. 36A

Initial duty –

• Option for purchaser

• Based on private valuation report

• Pay initial duty

• Submit bank guarantee

cont..

25

49

Stamp Act 1949

Proposal – new sec. 36A and 36B

Value of bank guarantee :

A - B

where

A is the duty chargeable using variance (market value per report x 100/65)

B is the initial dutycont..

50

Stamp Act 1949

Proposal – new sec. 36B

Additional duty –

• Proper amount of duty higher than initial

duty = Additional Duty

• Notice of additional assessment

cont

26

51

Stamp Act 1949

Proposal – new sec. 36B

Increase on additional duty –

Failure to pay additional duty within 30 days

notice of assessment served

• sum increased by 10%

Difference between proper amount of duty

and (amount of initial duty + bank

guarantee), exceeds 30%

• sum increased by 10% cont..

52

Stamp Act 1949

Consequential amendments -

sec 2, 37, 38, 38A and 39

• Sec. 2- definition “duly stamped” includes

concept of “initial duty”;

• Sec. 37 - indorsement of instrument as

“duly stamped”

• Sec. 38 - consequential amendment

• Sec. 38A and 39 – extend right of appeal to

additional assessment wef 01/01/2008

27

53

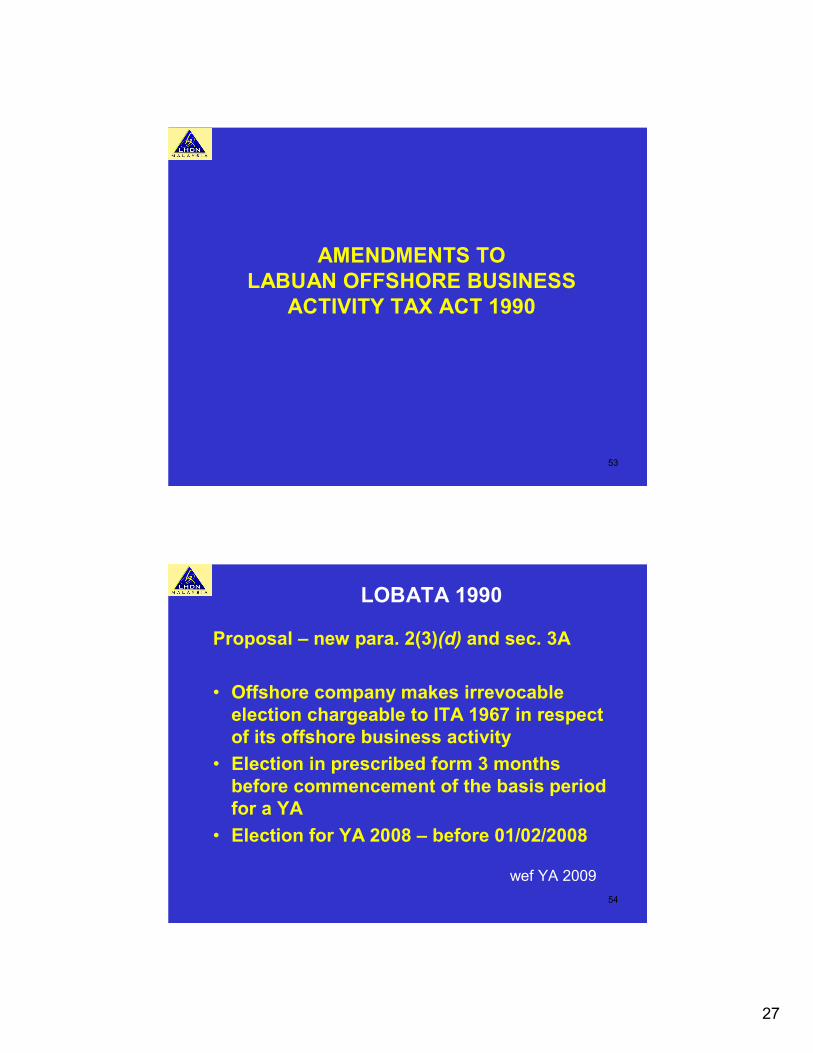

AMENDMENTS TO

LABUAN OFFSHORE BUSINESS

ACTIVITY TAX ACT 1990

54

LOBATA 1990

Proposal – new para. 2(3)(d) and sec. 3A

• Offshore company makes irrevocable

election chargeable to ITA 1967 in respect

of its offshore business activity

• Election in prescribed form 3 months

before commencement of the basis period

for a YA

• Election for YA 2008 – before 01/02/2008

wef YA 2009

28

55

PART 2

INCOME TAX RULES

56

Security Control and Surveillance

EquipmentsCurrent law

Normal capital allowance

• Initial allowance 20% & annual allowance 14%

Proposal

• Initial allowance 20% & annual allowance 80%

• Qualifying equipments determined by Minister

wef YA 2008-2012

29

57

Personal Computer

Current law

Gift of new personal computer (p/c) to

employee

• Deduction given previously from YA

2001 – 2003 (Income Tax Rules

[P.U. (A) 504/2000])

cont

58

Personal Computer

Proposal

Gift of new p/c and broad band

subscription fee to employee

Deduction

• One new computer per employee

• Amount of deduction

= cost of computer + subscription fee

wef YA 2008-2010

30

59

Contribution of used computers

Current law

• No deduction for contributing used

computers to school

Proposal

Deduction:

• RM200 per computer

• Computer used in a business not more than

4 years

• Through PINTAR secretariat under

Khazanah Bhd wef YA 2008-2010

60

Rubber Wood Cultivation

Current law

Accelerated Agriculture Allowance

• IA = 20% and AA= 80%

• Qualifying agriculture expenditure (Sch.3)

• At least 10% of area planted with rubber

wood tree

• Verified by Ministry of Plantation Industries

and Commodities

Proposal

• Claimable until YA 2010 wef YA 2003-YA 2010

31

61

Renewable Energy

Current law

• ACA (within 1 year)

IA – 20% & AA – 80% (Income Tax Rules [P.U.(A) 88/2005])

Proposal

• Investment tax allowance of 100% on plant & machinery used in the business

• Within 5 years determined by MOF

• Deducted against 100% of statutory income

• Existing ITR is revoked from 8/9/2007.

Application to MIDA from 8/9/07-31/12/2010

62

Last mile Current law

Allowance For Service Sector (Sch 7B)

• 60% of qualifying capital expenditure

• Incurred within 5 years

• Deducted up to 70% of SI

Proposal

• Co. provides broadband infrastructure

• 100% of qualifying capital expenditure

• Incurred within 3 years

• Deducted against 70% of SI

Application to MOF from 8/9/07-31/12/2010

32

63

PART 3

INCOME TAX EXEMPTION ORDERS

64

Industry Excellence Awards

Current law

Export Excellence Award (Merchandise)

• Exemption on SI = value of increased exports and restricted to 70% of SI (Exemption Order [P.U.(A) 158/2005])

Proposal

Exemption extended to:

• Export Excellence Award (Services)

• Brand Excellence Award

wef YA 2008

33

65

ExpatriatesCurrent law

Exemption:

• Expatriate employed by Operational Headquarters (OHQ) or regional office (RO)

• Portion of employment income

• Exercised outside Malaysia

(Exemption Order 2003 [P.U.(A) 382])

Proposal

Exemption extended to expatriates employed by-

• International Procurement Centre (IPC)

• Regional Distribution Centre (RDC)

wef YA 2008

66

Gift of new personal computer

Current law

Personal computer and broad band

subscription fee received by employee

• Perquisite chargeable to tax

Proposal

Perquisite is exempted

• One computer during exemption period

• Monthly broad band subscription fee paid by employer