The End of White Picket Finance: Reform and Reality in the US Mortgage Market July 5, 2011 Executive Summary: The $11 trillion mortgage market, which has been fostered and supported by the government for 80 years, stands to undergo sweeping r eforms. The way homes have been financed for 40 years could change drastically over just a few years. We stand at the cusp of the largest privatization scheme in history. Its impacts will be far reaching across markets. For investors, trillions of dollars are at stake.

Transcript

8/6/2019 Talkot Capital - The End of White Picket Finance

Executive Summary: The $11 trillion mortgage market, which has been fostered and supportedby the government for 80 years, stands to undergo sweeping reforms. The way homes havebeen financed for 40 years could change drastically over just a few years. We stand at thecusp of the largest privatization scheme in history. Its impacts will be far reaching acrossmarkets. For investors, trillions of dollars are at stake.

8/6/2019 Talkot Capital - The End of White Picket Finance

Talkot Capital | The End of White Picket Finance 2

A cornerstone of the American Dream is the ability to purchase a home. For generations,homeownership has been considered a smart choice. A home has meant security, prosperity, andfinancial safety. Once upon a time, the dream of homeownership was once reserved only for thewealthy. New government programs and institutions, over the last half century, however,democratized mortgage credit, ushering in a unique era of White Picket Finance. The promise of a home became a reality for more and more Americans. Home prices seemingly never went down.For decades, our culture s faith in homeownership appeared vindicated. The financial crisis hassince changed everything. Financing the American Dream has turned out to be an unsustainablenightmare.

Since the Great Depression, the US government has been the force and direction of America s homefinance markets. It has founded agencies to facilitate the delivery of credit and enacted specialprograms to promote homeownership. It kick-started the securitization market which allowedaverage American households to tap sovereign borrowing rates at 30 year terms. The aggregategovernment effort and intervention has afforded the average American a net housing subsidy thathas drastically reduced the cost of homeownership.

A subsidy is any form of financial assistance that lowers the cost of a product or economic activity.Lowering the effective cost of a product makes it more affordable to more people. Policymakersuse subsidies to further policy goals. Homeownership is exemplary in this respect. In America, wewant people to own homes. The formation of households is the formation of healthy and stablefamily units. In short, American families are not just helping themselves; they are helping the entirenation.

But subsidies also have a dark side. They make market behaviors that are in reality expensiveappear cheap. Subsidies distort the incentives of individual actors and thereby distort markets.With housing, their impacts can burrow deep, obfuscating their true costs.

The massive housing subsidy enjoyed by American households has gradually snowballed to anunsustainable size. What was once small has become large. Between Freddie Mac and Fannie Mae(Government Sponsored Enterprises or GSEs ) alone, the US government today guarantees $5.5trillion in residential mortgage debt. 1 That s larger than China s 2010 GDP and almost whatAmerica will spend on our military over the next seven years combined. 2 The magnitude of theguarantee was always known, but the financial crisis has since exposed the magnitude of its costs.For the GSEs, the bill could be as large as $400 billion. 3 Total costs to taxpayers will depend on therecovery of the housing market. Sadly, the housing subsidy ended up financially crippling the verypopulations middle-class homeowners and taxpayers that it was meant to help.

Most importantly, the crisis has illuminated the unsustainability of the housing subsidy. The recent

economic and social misery inflicted by the aftereffects of the bubble has now culminated in a new- 1 Initially, the Treasury committed $100 billion in bailouts to each GSE. In December 2009, the Treasury agreed toprovide through 2012 an unlimited amount of capital to Freddie Mac and Fannie Mae. At present, this capital line hasbeen utilized to cover guarantees and other obligations of both companies, but the Treasury has the right and ability tosever these capital lines. What remains of the original $400 billion in capital support will support the entities after2012. The structure of the bailout supposedly incentivizes the GSEs to recognize more losses up front. Through thethird quarter of 2010, the GSEs combined had drawn down just over $150 billion.2 World Bank data and Talkot estimates from linear trends.3 Peter J. Wallison s 2010 estimate.

8/6/2019 Talkot Capital - The End of White Picket Finance

Talkot Capital | The End of White Picket Finance 3

found political ardor to fix a lopsided and broken mortgage finance system. Regulators andlegislators are now proposing far-reaching reforms to withdraw the very subsidies that helped growthe US mortgage market into one of the largest credit markets in the world. Many of these subsidieshave been in place for many decades. Now the aim of legislators is privatization.

On February 11, the Treasury and Housing and Urban Development (HUD) issued a special reportto Congress titled Reforming America s Housing Finance Market (The White Paper). Itexamines the history of government support of the housing market and addresses the fundamentalflaws in our housing finance infrastructure. Its core conclusions seem to agree with the nowpervasive opinions of most regulators and legislators that the housing subsidy, which has beenintegral to American homeownership for so many decades, is no longer tenable. The Americantaxpayer can no longer be the primary financer and insurer of the national housing stock. Theprivate sector must instead provide the bulk of American mortgage credit and stand in a risk position to assume possible losses. To achieve this end, The White Paper calls to slowly wind downthe two mortgage giants Freddie Mac and Fannie Mae in a vision of a narrower government roleproviding: (1) oversight; (2) consumer protection; (3) assisting low- and moderate-incomehomeowners and renters; and (4) support and stability to markets in crisis.

The White Paper is clearly not a hard guideline for reform, but it s significant in its desire forchange and its imagination of a housing finance system vastly different from the one we have today.Given the politics surrounding housing market reform, outcomes are difficult to predict. Butwhatever the particulars, it is clear that the upcoming transition from public to private will requireentirely novel finance architectures.

The scope of reforming the housing subsidy rivals the sweeping reforms that followed the 1929crisis that created landmark institutions like the SEC, FDIC, and FHA. And today, the stakes couldnot be higher. Any slip up in the changeover could threaten already fragile real estate markets,vulnerable bank balance sheets, and a weak economy. For legislators, managing the short-term

impacts of implementing these longer-term reforms will be an incredibly complex process. Theobstacles are many and the potential for bottlenecks numerous. Every layer of the home financemachine is fraught with risk.

As the mortgage market is increasingly privatized and borrowers and investors are rendered moreresponsible for their own decisions risk will have to be re-priced. Before the dust has time tosettle, the investment opportunities will be vast. To capitalize on these opportunities and managenew emerging risks will require gauging the trajectory of possible reforms, and intelligentlypredicting the effect of those dynamics on the various, interrelated parts of the next mortgagefinance system. As investors, to disregard the magnitude and macro-level complexity of this task issimply to leave money on the table or worse: to risk devastating loss by not understanding the

potential ripple effects of possible changes.

Put simply, the magnitude of these reforms compels us to write this paper. We stand at thecusp of the largest privatization scheme in history. There are literally trillions of dollars atstake. Now, more than ever, it will be crucial to stay focused on the bigger picture. This doesnot mean, of course, that short-term gains are unimportant. To the contrary, it means that short-termprudence will require a long-term outlook. It is precisely that kind of synthesis that the ensuingpaper aims to adopt.

8/6/2019 Talkot Capital - The End of White Picket Finance

Talkot Capital | The End of White Picket Finance 5

Total Residential Mortgage DebtOutstanding as of Q1 of 2011

Private Se ctor Issued MBS

GSE or

Ginnie MaeMBS

Other $0.49Trillion

$5.87Trillion

$2.87 Trillion

Unsecuritized WholeLoans

$1.21 Trillion

Source: Federal Reserve, Inside MBS

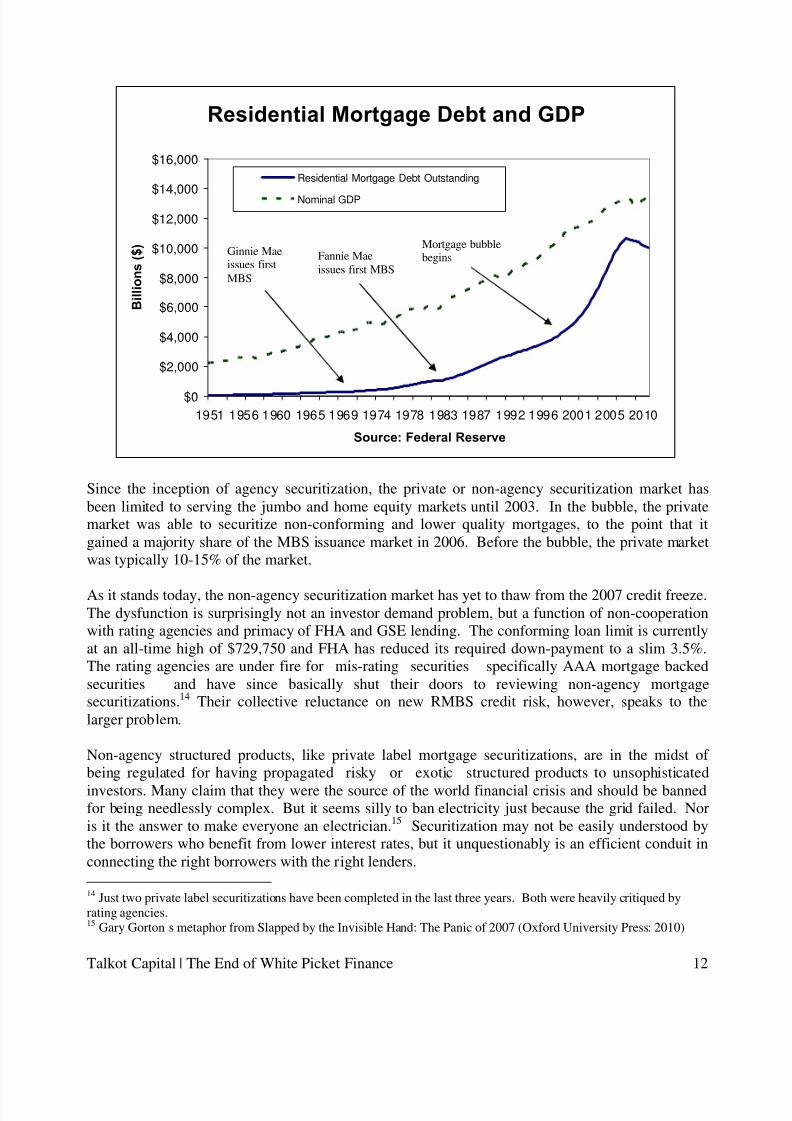

Today, the GSEs continue to guarantee over half of the $11 trillion of residential mortgage creditoutstanding. 5 And combined with the FHA, government agencies have originated and guaranteednearly 100% of mortgages since the 2008 crisis. This incredible market share is a function of a stillbroken private market; however, it is not entirely surprising in light of history. Before the bubbleyears of 2003-2007, government agencies generally securitized more than 80% of residentialmortgages issued per year since the MBS market has existed .

Residential MBS Issuance Market Share since 1970

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

2 0 1 0

Sources: SIFMA, Federal Reserve

M a r k e

t S h a r e

Agency Market Share Private Label or Non-Agency Market Share

5 The White Paper states that the Treasury will provide the necessary capital to ensure that the GSEs continue to honorall of its general obligations and guarantees.

8/6/2019 Talkot Capital - The End of White Picket Finance

Talkot Capital | The End of White Picket Finance 6

Simply put, the GSEs are and have been the market. So while the need to at least reduce the role of these agencies appears obvious, without them the housing market will require vastly differentmortgage credit delivery mechanisms.

Reform of any scale, however, will be tempered by political and social interests that have alwayscomplicated general housing policy. As such, understanding the next iteration of the housingfinance market what is likely to replace the GSEs historic role requires a deeper understandingof the politics of housing policy. This political process has always revolved around anunderstanding of some fundamental housing problem . In the 19 th and early 20 th centuries, it was aquality problem. In the 1930s, the problem was tied to a deflating economy. 1949, however,marked an important shift . That year Congress conceived of its mission in housing to help providea decent home in a suitable living environment for every American family . 6 Quality and

affordability particularly for low- and moderate-income areas have since been the two primaryissues framing housing politics. In 1977, the passing of the Community Reinvestment Act (CRA)aimed to mitigate discriminatory lending practices or redlining by commercial banks and S&Lsthat tended to under-serve low- and moderate-income neighborhoods. In the 1990s, amendments tothe CRA directed more lending into these communities. Those amendments have since beencriticized as contributing to the deterioration of underwriting standards. 7

Today, the housing problem has again shifted in the aftermath of the financial crisis, creating twodistinct camps loosely defined by political affiliations. To simplify matters, this paper will call eachcamp the Left and the Right. The Left continues to emphasize issues of affordability and to a lesserextent housing quality. Included in the Left s view is concern for new affordability problems for

6 Congressional affirmation set forth in section 1441 of title 42.7 Mortgage underwriting standards began to decline meaningfully in the early 2000s, but the increase in originatingnon-traditional mortgages began in 1995 primarily due to the Clinton administration s amendments to the Community

Reinvestment Act (CRA). The CRA aimed to mitigate geographic or other types of discriminating lending practices inlow- and moderate-income areas. But this discrimination was largely a function of underwriting costs. Underwritingcosts are more or less the same for $50k and $500k loans. Hence, lower priced homes like those in low- and moderate-income areas are disproportionately more costly to underwrite. In aim to mitigate this apparent lending problem, theCRA required FDIC insured institutions to meet the credit needs of these areas. As such regulators pressured banksto make more loans, especially mortgage loans, to low income borrowers and neighborhoods, but it was more often thecase that CRA banks en masse actually directed too much lending to these areas. Interest rates on CRA loans werecounter-intuitively low, reflecting not the actual credit risk of the loan but the mandate of this capital allocationguideline. Two banking reforms exacerbated the problem. In 1994 there was the Riegle-Neal Interstate Banking andBranching Efficiency Act (RN Act) which allowed banks to merge across state lines under federal law; and then in 1999the Gramm-Leach-Bliley Act (GLB Act) was passed, which repealed the part of the Glass-Steagall Act that hadprohibited banks from offering a full range of financial services from commercial, insurance, and investment banking.Together these reforms would cause a renaissance in banking as banks could now enlarge their footprints and merge or

expand into other types of financial institutions. But through it all CRA compliance was paramount. After passing theRN Act, federal bank regulators withheld merger approvals involving those banks which did not comply with the CRA.And in similar fashion, the GLB Act was passed such that any financial institution seeking re-designation would alsohave to follow and comply with the CRA. Bill Clinton explained it very clearly, "as we expand the powers of banks, wewill expand the reach of the [Community Reinvestment] Act." Unsurprisingly, both events caused banks to devote moreresources to their CRA programs and thus, more lending into low- and moderate-income areas.

Home borrower risk as such quickly began to be mispriced, but many banks admittedly knew this and fearedholding owning these credits themselves. Two features to the home finance system allowed them to export these knownrisks off-balance sheet. First were the GSEs who purchased newly originated loans which met their underwritingstandards, which widened in the mid 2000s; and second was the securitization market, which allowed banks to poolloans together and sell them to the secondary private label mortgage market.

8/6/2019 Talkot Capital - The End of White Picket Finance

Talkot Capital | The End of White Picket Finance 7

the millions of current homeowners who have negative equity or are facing foreclosure. The Right,on the other hand, has attacked the latent costs of housing subsidies. They seek to mitigate, if noteradicate, these liabilities to taxpayers. In particular are the GSEs, FHA, and other implicitliabilities that compel, or may compel, taxpayers to incur significant losses and fund possiblebailouts.

The Left s arguments for promoting high quality, affordable housing for homeowners arenumerous. Housing is more than just simple shelter. The home is the primary setting for theAmerican family, a key to stable household formation benefiting the broader economy and aprimary source of most Americans wealth. The location of a home largely determines access toeducation, employment, and other amenities. Property ownership also engenders a certain sense of American equity , given that homeowners want to protect the value of their home. As

stakeholders, they are more likely to be active citizens and voters. And more generally, high-quality, affordable housing relieves a significant social and economic burden on low- and middle-income families allowing them to prosper not to mention the tax revenues generated at every levelof the homeownership process. Today, physically deficient housing makes up only a smallpercentage of the US housing stock, making affordability a cornerstone issue of the housing policydebate. Only 6% of households live in physically deficient or overcrowded conditions, while in2007 30% of all homeowners and more than 45% of all renters were commonly classified assuffering an affordability problem . 8

The Right s arguments, on the other hand, attack the latent costs of subsidizing housing andmortgage credit. Government housing programs, policies, and GSE obligations are taxpayer backed liabilities with the potential to incur significant credit losses. Additionally, there is the risk of ataxpayer bailout of the financial sector, which remains highly levered to real estate. Furthermore,these collective obligations and financial risks must be considered against the backdrop of the fiscalposition at the US Treasury, which impacts sovereign borrowing rates and the value of the dollaramongst numerous other political, social, and economic effects. Recently, this second set of

concerns has come to the fore, given the fresh memory of trillions in government interventions andstimuli, sparking debates about the soundness of the Treasury s fiscal position. These issues haverecently been compounded by an S&P downgrade warning on America s sovereign credit rating.

In short, both sides agree that the debate revolves around the issue of affordability. The Rightworries over government balance sheets and the Left, household balance sheets. But these concernsare fundamentally intertwined governments are ultimately taxpayer liabilities and households areultimate drivers of tax revenues. These two concerns are actually one and the same, pointing to themore important variable the state of the American economy. As Tim Geithner said after therelease of the Treasury s White Paper, "One reason why we've been so careful not to lock in a pathfor phasing out the government's role is there's no certainty in this context and we have to be careful

again not to do damage to the recovery.

8 A housing affordability problem is defined by the US Census Bureau as a homeowner or renter who spends more than30% of their pre-tax income on housing.

8/6/2019 Talkot Capital - The End of White Picket Finance

Talkot Capital | The End of White Picket Finance 8

As a substantial driver of GDP (17 to 18% in 2009) and tax revenues, the housing industry is criticalto both the economy and the budget. 9 But what supports the housing market and home prices isleverage. One must remember the golden rule of asset markets: an asset s price is driven by theamount of leverage available to it . And for the last decade, housing values have been priced withGSE and FHA available financing and, worse, government financing is now the only financingcurrently available to prospective home buyers. To suddenly withdraw or change the availability of home financing will force the housing market to re-price itself. The new pricing model will insteadbe dictated by the availability and terms of new, private market leverage sources, which may not beaccessible at every point of the business cycle. Depending on the severity of such reform, suchchanges could be the death knell for home prices, pressuring as much as four years of presentforeclosure and shadow foreclosure inventory. 10 Diminishing equity in the nation s housing stock means destroying household wealth and risking asset values on bank balance sheets; and highermortgage capital costs means restricting the mobility of American households to seek out betteropportunities in different American markets. In short, policy makers must balance the Left s desireto ration mortgage credit and the Right s desire for fiscal consolidation, while keeping the Americanrecovery afloat. That proper mix will largely determine the future value of the American home.

Imagining the Future of Housing Finance

A GSE-less world will require a private market that can originate and portfolio the bulk of American mortgage credit risk. A new system, therefore, will have to (1) efficiently connectborrowers and lenders through private capital markets in similar volume and (2) be the balancesheets to hold these mortgage credits. As we ve discussed, the GSEs have been significant in fillingboth these roles. They acted as issuers of mortgage backed securities (MBS) and investors in thosesame securities.

At present, the government continues to shed billions of MBS that will have to be absorbed byprivate capital. The GSEs investment portfolios have already shrunk substantially to just $600

billion at March 31st

2011 since peaking over $1.5 trillion in 2007. They have been shrinking inaccord with the government mandate to decrease their portfolios 10% a year. The Federal Reserve sportfolio has shrunk from $1.25 trillion to $925 billion and continues to shrink as MBSprepayments are re-invested into treasuries. Going forward as such, private balance sheets willeventually become the primary if not the sole repository for legacy and new production residentialmortgage securities. But which balance sheets will hold them? There are two options: commercialbank balance sheets (FDIC insured financial institutions) and non-bank balance sheets (e.g. moneymanagers, sovereign wealth funds, mortgage REITs).

9 According to the National Association of Home Builders (NAHB) historically, residential investment has averagedroughly 5 percent of GDP while housing services have averaged between 12 and 13 percent, for a combined 17 to 18percent of GDP.10 Data from LPS Mortgage Monitor Report from December 2010

8/6/2019 Talkot Capital - The End of White Picket Finance

Talkot Capital | The End of White Picket Finance 9

Before moving on, it is worth noting how features unique to mortgages have shaped thedevelopment of the mortgage market.

Mortgages, themselves, are tricky assets to own. They have typical bond-like characteristics likeinterest-rate risk, but carry two additional risks: prepayment and, to a lesser extent, credit risk. Thelender has effectively sold the borrower an option to: (1) prepay his mortgage principal in part or infull at any time; and (2) delay or default (including walking away ), leaving the lender with onlyrecourse to take possession of the collateral property or home.

Prepayments historically have been a function of interest rates. When interest rates decline,borrowers have an incentive to refinance into a new mortgage with a lower interest rate. Wheninterest rates rise, borrowers have a decreasing incentive to prepay as their interest rate moves

below the market rate. This is a bad option to own as an investor. As interest rates decline, investorsreceive early principal payments which now can be re-invested at lower rates. Conversely, asinterest rates rise, lower prepayments means investors are now stuck with an asset extending inmaturity earning a below market return. This is the primary reason why 15- and 30-year fixed ratemortgage products are particularly difficult to own for investors. This maturity problem (alsoknown as negative convexity) is amplified for the leveraged spread investor who assumes additionalrisks in floating rate funding costs and possible margin calls.

8/6/2019 Talkot Capital - The End of White Picket Finance

Talkot Capital | The End of White Picket Finance 10

Credit risk is less tied to interest rates and more a function of employment and the general economy.Declining employment and income negatively impact the borrower s ability to service the debt.The recent crisis also demonstrates that borrowers will often strategically default or walk away froma property when the market value of the home falls below the outstanding mortgage balance.

Today, bank balance sheets are inefficient destinations for mortgage credits. For starters, bank credit at US-chartered commercial banks totals just over $8 trillion while total multifamily andresidential mortgage debt stands at roughly $12 trillion. 11

The banking system simply isn t big enough to finance the nation s housing stock. Secondly, newcapital requirement rules imposed by Dodd-Frank and Basel III will make holding mortgage creditson bank balance sheets increasingly more expensive. Bank officials last year agreed to raise theminimum common equity requirement for lenders to 4.5 percent from 2 percent of assets weightedfor risk, with an added buffer of 2.5 percent for a total of 7 percent of assets weighted for risk. Therequirements will be even more stringent for mortgages, such that non-bank private capital will beable to own mortgages with lower capital reserves than banks. 12 This mirrors the post-bailout viewthat banks, as now explicit government liabilities, will increasingly be regulated like utility

11 Federal Reserve (2011) and Mortgage Bankers Association (2011).12 As JPM CEO Jamie Dimon said, Why would we own mortgages if you can own them at 7 percent capital and I haveto own them at 10 percent?

8/6/2019 Talkot Capital - The End of White Picket Finance

Talkot Capital | The End of White Picket Finance 11

companies to serve a public finance function. Thirdly, holding long duration assets like a 30-yearfixed rate mortgage exposes the banking system to significant interest rate volatility risk. This wasactually a rationale for the GSEs to foster a secondary mortgage market. Lastly, transferring thebulk of mortgage risk to the banking system does not mitigate systemic risk: taxpayers are still onthe hook. One must not forget that the banking system, as debt crises repeatedly expose, is justanother implied government liability.

Non-bank balance sheets, on the other hand, offer a means to disperse risk while efficientlyconnecting private capital sources and end borrowers. Unlike banks, they do not benefit from thegovernment backstop of the FDIC and hence, suffer fewer regulations. This allows them to takemore risk, but these are risks that are willingly assumed to earn a return. Non-bank balance sheetsare composed of private capital pools that are raised to manage such risks. This doesn t mean bankswon t have a role in the future of mortgage finance. It simply means that we should expect non-banks to be a more primary acquirer of mortgage assets in the near future because of thesedynamics.

Beyond the balance sheet issue, there remains the issue of origination or how the private sector willefficiently connect borrowers and lenders through capital markets. The clear answer issecuritization.

Securitization created the first mortgage backed securities in the 1970s and has since beeninstrumental in scaling the growth of the mortgage finance market. Mortgage backed securities aredebts issued against a pool of mortgage cash flows. By bundling tens to hundreds of similarmortgages, idiosyncratic risk decreases. Other key innovations for secondary market investors weretranching the prioritization of debt classes or tranches within a securitization and the guaranteeof timely payment of principal and interest by GSE issued MBS or agency MBS.

Together these innovations make securitization beneficial to all market participants. For the

financial system, securitization freed up capital allowing banks to underwrite more mortgageswithout having to hold them on balance sheet and observe capital requirements and charges. Forborrowers, securitization provides a lower cost of credit to households and businesses by connectingthem to previously inaccessible capital sources. For investors, it affords them attractive investmentsin a liquid market with built-in features which allow them more prepayment certainty and the abilityto vary their credit risk exposure. Securitization swiftly transformed the residential mortgage creditsector. Outstanding mortgage debt grew from a mere 25% of US GDP in the 1970s to over 80% in2007. 13

13 Source: World Bank, Federal Reserve

8/6/2019 Talkot Capital - The End of White Picket Finance

Talkot Capital | The End of White Picket Finance 12

Since the inception of agency securitization, the private or non-agency securitization market hasbeen limited to serving the jumbo and home equity markets until 2003. In the bubble, the privatemarket was able to securitize non-conforming and lower quality mortgages, to the point that itgained a majority share of the MBS issuance market in 2006. Before the bubble, the private marketwas typically 10-15% of the market.

As it stands today, the non-agency securitization market has yet to thaw from the 2007 credit freeze.The dysfunction is surprisingly not an investor demand problem, but a function of non-cooperationwith rating agencies and primacy of FHA and GSE lending. The conforming loan limit is currentlyat an all-time high of $729,750 and FHA has reduced its required down-payment to a slim 3.5%.The rating agencies are under fire for mis-rating securities specifically AAA mortgage backedsecurities and have since basically shut their doors to reviewing non-agency mortgagesecuritizations. 14 Their collective reluctance on new RMBS credit risk, however, speaks to thelarger problem.

Non-agency structured products, like private label mortgage securitizations, are in the midst of being regulated for having propagated risky or exotic structured products to unsophisticatedinvestors. Many claim that they were the source of the world financial crisis and should be bannedfor being needlessly complex. But it seems silly to ban electricity just because the grid failed. Noris it the answer to make everyone an electrician. 15 Securitization may not be easily understood bythe borrowers who benefit from lower interest rates, but it unquestionably is an efficient conduit inconnecting the right borrowers with the right lenders.

14 Just two private label securitizations have been completed in the last three years. Both were heavily critiqued byrating agencies.15 Gary Gorton s metaphor from Slapped by the Invisible Hand: The Panic of 2007 (Oxford University Press: 2010)

Talkot Capital | The End of White Picket Finance 13

That being said, it is undeniable that non-agency securitization as it existed in the 2000s created amisalignment of incentives in the securitization chain. Originators would often securitize anythingas long as they could get the rating agencies AAA stamp of approval. This gave birth to thepernicious alchemy that was re-securitizing dubious and subordinated collateral into seeminglypristine products that were then sold to the marketplace. In the originate-and-distribute

business model, writes the SEC, lenders did not bear the credit risk of borrower default, which ledto a deterioration in credit quality of the underlying assets. Instead, that risk was passed on toinvestors. With no regulatory oversight of the rating agencies due diligence, the only check against the system was the discretion of private investors. Unfortunately, as the world learned,investors and lenders largely trusted these ratings and historical credit performance of RMBScredits. In 2005, Moody s historical model estimated that Aaa RMBS or HELOC (home equityloan) losses to be just 2.3%. 16 In 2009, Moody s released a report that now projects 2005-2007 non-subprime HELOCs to suffer cumulative losses of 25-55%. 17 In other words, we can t just rely onthe rating agencies. We need a better grid a new architecture capable of handling and managinghow securitization connects lenders and borrowers.

In summary, to supplant the GSEs dual role in originating and investing in mortgage securities, theprivate sector will need time and money. It will take time to construct new origination architecturesthat meet the efficiency and scale of the GSEs; and capital equity capital - to finance theownership of the legacy securities that are being run off government balance sheets and the newmortgages our future system will produce. Each of these tasks by itself will be a taxing, multi-yearprocess. For both to happen in sequence, or possibly simultaneously, would be a truly extraordinaryevent in the history of financial markets.

RMBS 2.0: QRM

Addressing these recent weaknesses in the non-agency securitization market, the Dodd-Frank Wall

Street Reform and Consumer Protection Act has aimed to prevent the originate-and-distributebusiness model. Regulators will require private securitizers to retain a risk portion of eachsecuritization sold to the market. Regulating the non-agency securitization market, however, doesnot pair well with the grander vision of unwinding government programs. We have to rememberthat the private market before the bubble was always little brother to the government. The onlytime it was a force in mortgage securitization was during the bubble years of 2003-2006 when itmainly issued toxic, unstable securities which nearly brought down the system. Before the bubble,the private market performed a select role for jumbo and home equity loans. Today there is noprivate securitization market to speak of. In short, policy-makers may be, in effect, regulating amarket that does not exist . Moreover, these regulations, which will raise mortgage costs, could not

come at a worse time for deleveraging households.

Under Dodd-Frank, securitizers will be required to retain 5% of the credit risk for eachsecuritization they create unless that securitization is wholly composed of qualified residentialmortgages (QRM). The FHA and GSEs would be exempt from risk retention rules. A QRM hasyet to be permanently defined. On March 29, 2011 regulators proposed a tentative definition of a

16 Moody s Investor Service 200517 Moody s Investor Service 2008

8/6/2019 Talkot Capital - The End of White Picket Finance

Talkot Capital | The End of White Picket Finance 14

QRM as a mortgage with a maximum loan-to-value of 80% with standardized debt-to-income ratios(28% / 36% or less) and product requirements. So far market participants and commentators havecalled this first definition too narrow. Only about 20% of GSE acquired mortgages since 1997 meetthe proposed QRM definition. Moreover, based on 2009 data, it would take 15 years for an averagefamily to save the $43,000 or 20% down payment on a median priced home. Not such an easy thingfor households to do when roughly a quarter of current borrowers owe more than their homes areworth. 18

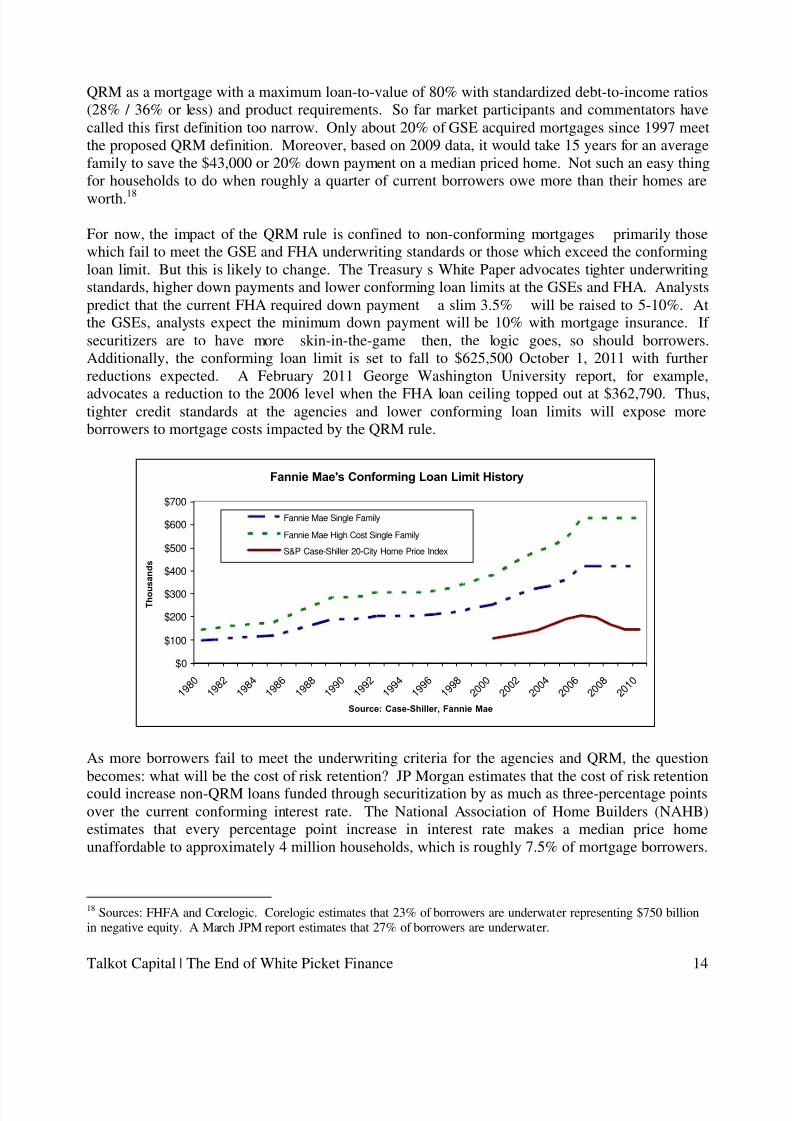

For now, the impact of the QRM rule is confined to non-conforming mortgages primarily thosewhich fail to meet the GSE and FHA underwriting standards or those which exceed the conformingloan limit. But this is likely to change. The Treasury s White Paper advocates tighter underwritingstandards, higher down payments and lower conforming loan limits at the GSEs and FHA. Analystspredict that the current FHA required down payment a slim 3.5% will be raised to 5-10%. Atthe GSEs, analysts expect the minimum down payment will be 10% with mortgage insurance. If securitizers are to have more skin-in-the-game then, the logic goes, so should borrowers.Additionally, the conforming loan limit is set to fall to $625,500 October 1, 2011 with furtherreductions expected. A February 2011 George Washington University report, for example,advocates a reduction to the 2006 level when the FHA loan ceiling topped out at $362,790. Thus,tighter credit standards at the agencies and lower conforming loan limits will expose moreborrowers to mortgage costs impacted by the QRM rule.

Fannie Mae's Conforming Loan Limit History

$0

$100

$200

$300

$400

$500

$600

$700

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

2 0 1 0

Source: Case-Shiller, Fannie Mae

T h o u s a n

d s

Fannie Mae Single Family

Fannie Mae High Cost Single Family

S&P Case-Shiller 20-City Home Price Index

As more borrowers fail to meet the underwriting criteria for the agencies and QRM, the questionbecomes: what will be the cost of risk retention? JP Morgan estimates that the cost of risk retentioncould increase non-QRM loans funded through securitization by as much as three-percentage pointsover the current conforming interest rate. The National Association of Home Builders (NAHB)estimates that every percentage point increase in interest rate makes a median price homeunaffordable to approximately 4 million households, which is roughly 7.5% of mortgage borrowers.

18 Sources: FHFA and Corelogic. Corelogic estimates that 23% of borrowers are underwater representing $750 billionin negative equity. A March JPM report estimates that 27% of borrowers are underwater.

8/6/2019 Talkot Capital - The End of White Picket Finance

Talkot Capital | The End of White Picket Finance 15

So while QRM is likely to be successful in facilitating a sustainable private securitization market,an increasing number of households will struggle to afford the costs imposed by these regulations.

Examine the finances of the average American household with a mortgage. Our average family hasannual income of $63,000, which leaves them with about $46,500, assuming an all-in tax rate of 30% (and deducting mortgage interest, of course). 19 We assume that they have a 5% 30-yearconforming $180k loan against their median priced home, which equates to roughly a $960 monthlymortgage payment. After all other necessary expenses, they are left with just under $500 foremergencies, education, cell phones, internet, cable, home repairs, entertainment and perhaps evensavings. There might not be a lot of room for error, but if jobs are kept, our average family cansqueak by.

Now consider what happens when we substitute their conforming mortgage with two possible typesof non-conforming, non-QRM mortgages. If their mortgage rate rises to 7.5%, their monthlypayment jumps almost $250. Alternatively, a 15-year mortgage at 5% raises their mortgagepayment over $450 dollars.

Income Statement for the Average American Household with a Credit Card

Per Year Per MonthPerMonth

PerMonth

Assumed Mortgage Type30-year 5%Conforming

30-year 5%Conforming

30-year7.5%

15-year5%

Income $62,857 $5,238 $5,238 $5,238Tax Liability* $16,400 $1,367 $1,367 $1,367

Talkot Capital | The End of White Picket Finance 16

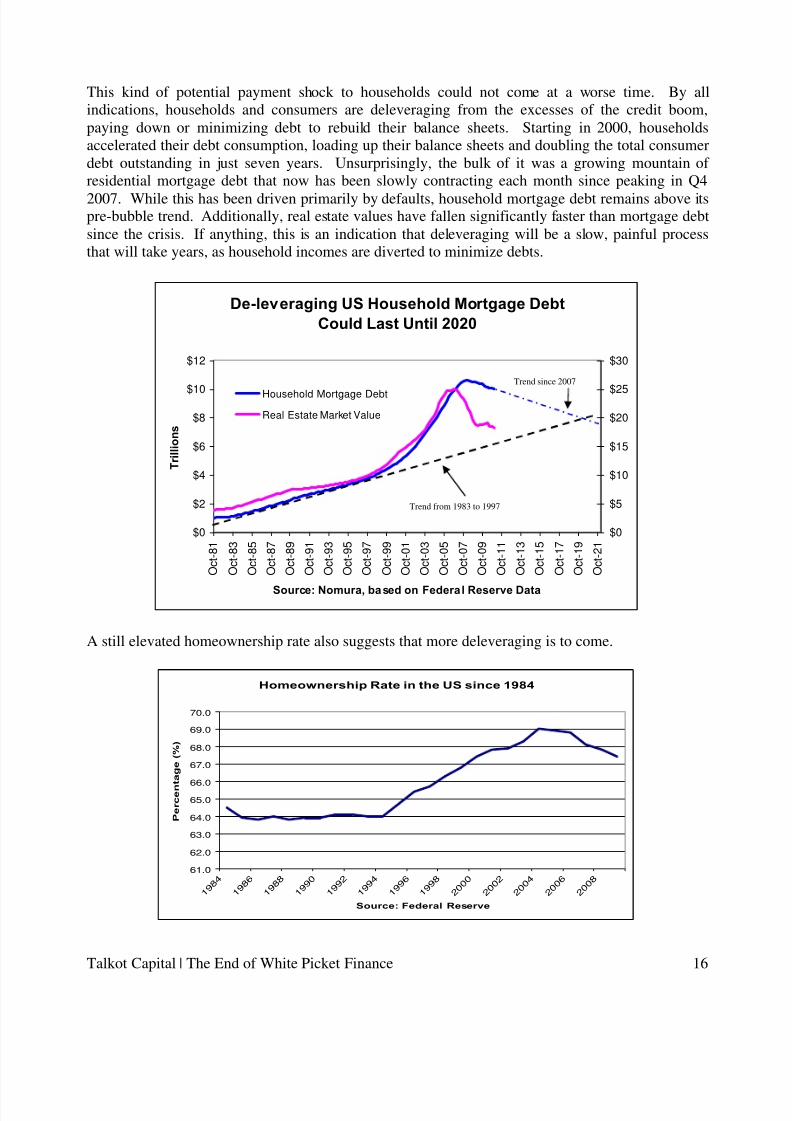

This kind of potential payment shock to households could not come at a worse time. By allindications, households and consumers are deleveraging from the excesses of the credit boom,paying down or minimizing debt to rebuild their balance sheets. Starting in 2000, householdsaccelerated their debt consumption, loading up their balance sheets and doubling the total consumerdebt outstanding in just seven years. Unsurprisingly, the bulk of it was a growing mountain of residential mortgage debt that now has been slowly contracting each month since peaking in Q42007. While this has been driven primarily by defaults, household mortgage debt remains above itspre-bubble trend. Additionally, real estate values have fallen significantly faster than mortgage debtsince the crisis. If anything, this is an indication that deleveraging will be a slow, painful processthat will take years, as household incomes are diverted to minimize debts.

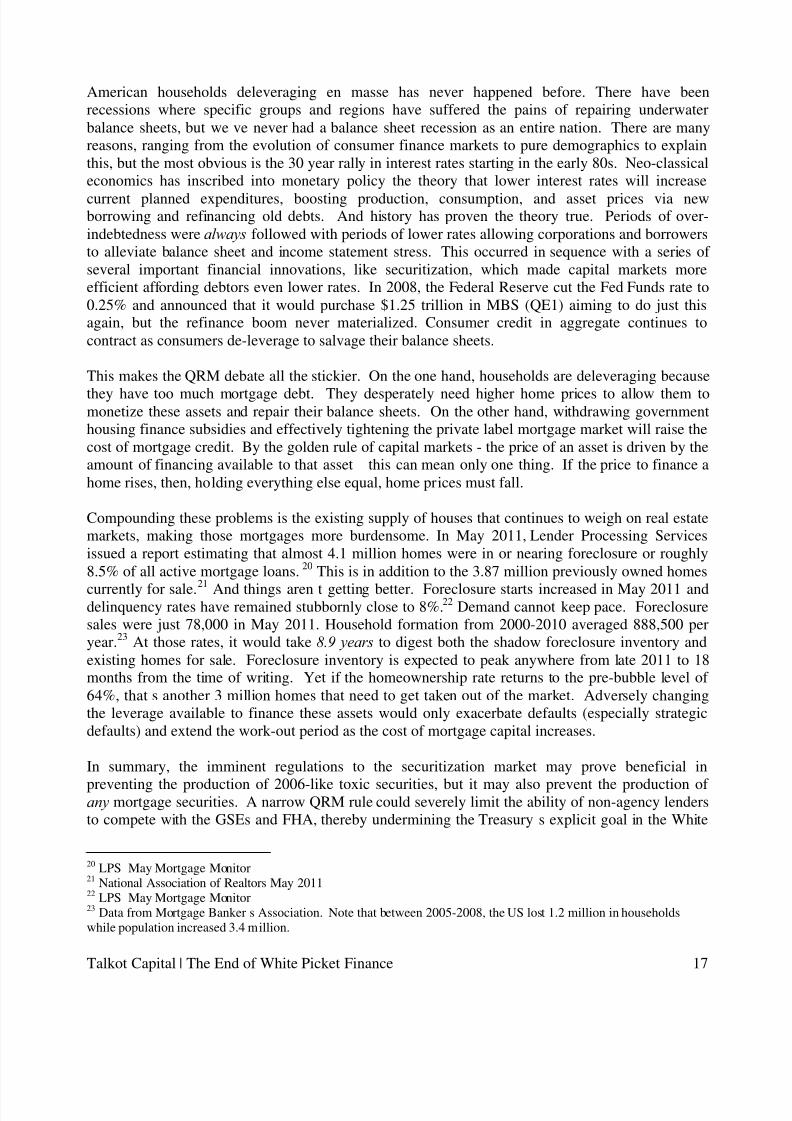

A still elevated homeownership rate also suggests that more deleveraging is to come.

Homeownership Rate in the US since 1984

61.0

62.0

63.0

64.0

65.0

66.0

67.0

68.0

69.0

70.0

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

Source: Federal Reserve

P e r c e n

t a g e

( % )

De-leveraging US Household Mortgage DebtCould Last Until 2020

$0

$2

$4

$6

$8

$10

$12

O c t - 8 1

O c t - 8 3

O c t - 8 5

O c t - 8 7

O c t - 8 9

O c t - 9 1

O c t - 9 3

O c t - 9 5

O c t - 9 7

O c t - 9 9

O c t - 0 1

O c t - 0 3

O c t - 0 5

O c t - 0 7

O c t - 0 9

O c t - 1 1

O c t - 1 3

O c t - 1 5

O c t - 1 7

O c t - 1 9

O c t - 2 1

Source: Nomura, ba sed on Federa l Reserve Data

T r i l l i o n s

$0

$5

$10

$15

$20

$25

$30

Household Mortgage Debt

Real Estate Market Value

Trend from 1983 to 1997

Trend since 2007

8/6/2019 Talkot Capital - The End of White Picket Finance

Talkot Capital | The End of White Picket Finance 17

American households deleveraging en masse has never happened before. There have beenrecessions where specific groups and regions have suffered the pains of repairing underwaterbalance sheets, but we ve never had a balance sheet recession as an entire nation. There are manyreasons, ranging from the evolution of consumer finance markets to pure demographics to explainthis, but the most obvious is the 30 year rally in interest rates starting in the early 80s. Neo-classicaleconomics has inscribed into monetary policy the theory that lower interest rates will increasecurrent planned expenditures, boosting production, consumption, and asset prices via newborrowing and refinancing old debts. And history has proven the theory true. Periods of over-indebtedness were always followed with periods of lower rates allowing corporations and borrowersto alleviate balance sheet and income statement stress. This occurred in sequence with a series of several important financial innovations, like securitization, which made capital markets moreefficient affording debtors even lower rates. In 2008, the Federal Reserve cut the Fed Funds rate to0.25% and announced that it would purchase $1.25 trillion in MBS (QE1) aiming to do just thisagain, but the refinance boom never materialized. Consumer credit in aggregate continues tocontract as consumers de-leverage to salvage their balance sheets.

This makes the QRM debate all the stickier. On the one hand, households are deleveraging becausethey have too much mortgage debt. They desperately need higher home prices to allow them tomonetize these assets and repair their balance sheets. On the other hand, withdrawing governmenthousing finance subsidies and effectively tightening the private label mortgage market will raise thecost of mortgage credit. By the golden rule of capital markets - the price of an asset is driven by theamount of financing available to that asset this can mean only one thing. If the price to finance ahome rises, then, holding everything else equal, home prices must fall.

Compounding these problems is the existing supply of houses that continues to weigh on real estatemarkets, making those mortgages more burdensome. In May 2011, Lender Processing Servicesissued a report estimating that almost 4.1 million homes were in or nearing foreclosure or roughly8.5% of all active mortgage loans. 20 This is in addition to the 3.87 million previously owned homes

currently for sale.21

And things aren t getting better. Foreclosure starts increased in May 2011 anddelinquency rates have remained stubbornly close to 8%. 22 Demand cannot keep pace. Foreclosuresales were just 78,000 in May 2011. Household formation from 2000-2010 averaged 888,500 peryear. 23 At those rates, it would take 8.9 years to digest both the shadow foreclosure inventory andexisting homes for sale. Foreclosure inventory is expected to peak anywhere from late 2011 to 18months from the time of writing. Yet if the homeownership rate returns to the pre-bubble level of 64%, that s another 3 million homes that need to get taken out of the market. Adversely changingthe leverage available to finance these assets would only exacerbate defaults (especially strategicdefaults) and extend the work-out period as the cost of mortgage capital increases.

In summary, the imminent regulations to the securitization market may prove beneficial in

preventing the production of 2006-like toxic securities, but it may also prevent the production of any mortgage securities. A narrow QRM rule could severely limit the ability of non-agency lendersto compete with the GSEs and FHA, thereby undermining the Treasury s explicit goal in the White

20 LPS May Mortgage Monitor 21 National Association of Realtors May 201122 LPS May Mortgage Monitor 23 Data from Mortgage Banker s Association. Note that between 2005-2008, the US lost 1.2 million in householdswhile population increased 3.4 million.

Talkot Capital | The End of White Picket Finance 18

Paper to reduce the government s footprint in the housing finance market. The costs imposed byQRM could also make mortgage credit significantly less affordable, precipitating another leg downfor home prices. Rationing mortgage credit and supporting home prices is not possible. There is nowin-win magic bullet. Either somebody loses or we all lose together.

A New World of Mortgages: Privatization and a Mother of Capital Calls

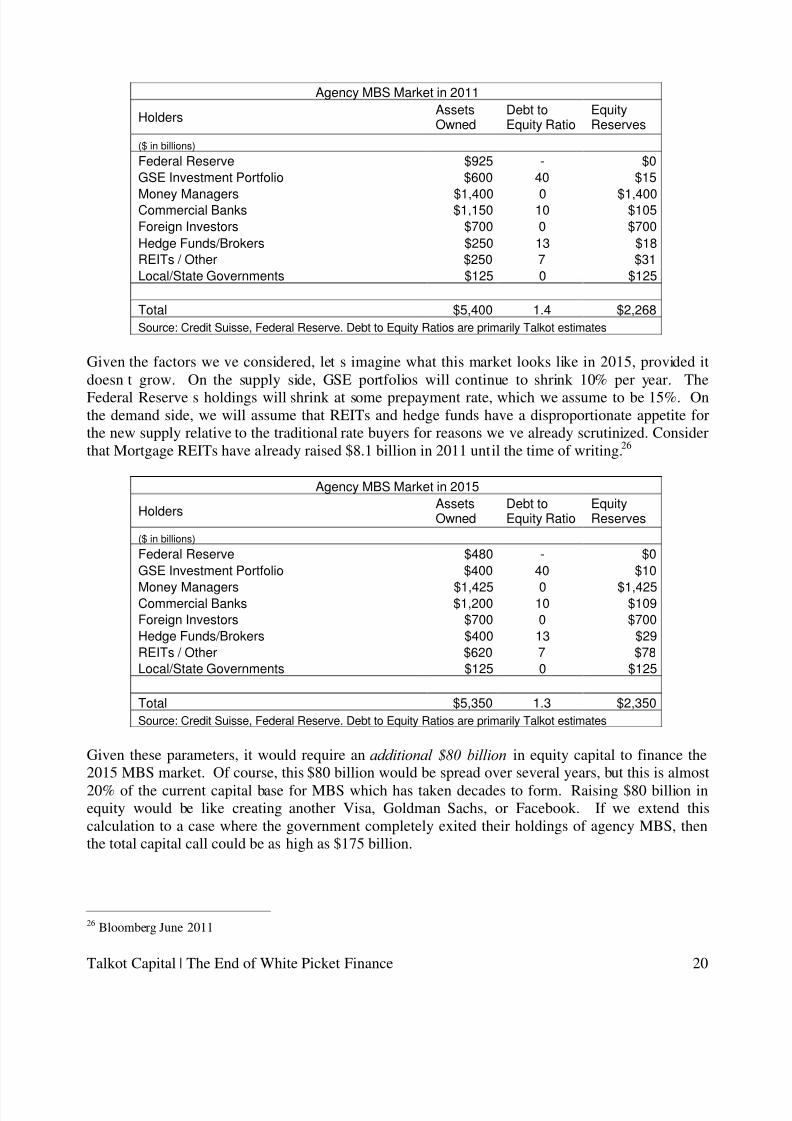

At present, just over $1.5 trillion of agency MBS is owned across the balance sheets of Freddie,Fannie, and the Federal Reserve. 24 Again, the GSEs are mandated to decrease their portfolios by10% per year and the Federal Reserve is reinvesting MBS prepayments into treasury securities. Asthese portfolios run-off and shrink, private market balance sheets will have to portfolio these assets.Assuming prepayments don t fall significantly, it s estimated that the private market will have toportfolio anywhere from $200 to $300 billion in 2011 alone. To finance these assets at 10:1leverage, private markets would have to raise $18 to $28 billion in equity capital in 2011 andpossibly as much as $175 billion over the life of the government runoff. This transition of agencyMBS from government to private balance sheets is a de facto privatization of mortgage assets andwill effectively act as a slow and steady capital call.

This is the price of having had these assets under-collateralized on government balance sheets for solong. Lower private market leverage ratios will necessarily tie up more equity capital reserveskeeping mortgage spreads wide and pressuring rates higher. And all of this is before we overlay theTreasury s desire to shift more of the share of mortgage originations to the private sector. Shiftingthe composition of mortgage origination, in turn, shifts the composition of collateral types in theMBS market. More non-agency securities means higher financing costs, which encumbers evenmore equity capital. And lastly, more mortgage collateral backed by credit risk increases thesecondary or shadow banking system s vulnerability to repo runs.

For the GSEs and the Federal Reserve, owning agency MBS portfolios was and continues to be

easy. The GSEs only need to hold $2.5 dollars in equity capital against $100 in assets. The FederalReserve s monopoly on the printing press gives it theoretically infinite leverage. The private sector,on the other hand, is much more constrained in its access to leverage.

Many portfolios of agency MBS are financed through the repurchase agreement or repo marketwhere securities are sold for cash and pledged to be repurchased at some future contracted date andprice. In essence, a repo is a loan collateralized by a security. The difference between the value of the security and the loan is the capital requirement or haircut . Haircuts are a key constraint forleverage bigger haircuts mean holding more equity capital. A 5% haircut means that to purchasea $100 of securities, the purchaser must post $5 of equity capital to finance the other $95 of purchases. That translates into a 19:1 debt to equity ratio, but lenders typically keep these ratios in

check. Agency MBS typically fetch 3-5% haircuts. Non-Agency MBS, on the other hand, typicallyfetch slightly higher haircuts of 5-25% depending on credit quality. Thus, by private marketstandards, agency MBS held on government balance sheets has been inadequately reserved. Assuch, the transition of assets from government to the private balance sheets will necessarily requirenew equity capital.

24 At the time of writing the agency MBS holdings for the Federal Reserve was $927 billion. At 3/31/2011 FreddieMac s investment portfolio was $263.6 billion and Fannie Mae s investment portfolio $349 billion.

8/6/2019 Talkot Capital - The End of White Picket Finance

Talkot Capital | The End of White Picket Finance 19

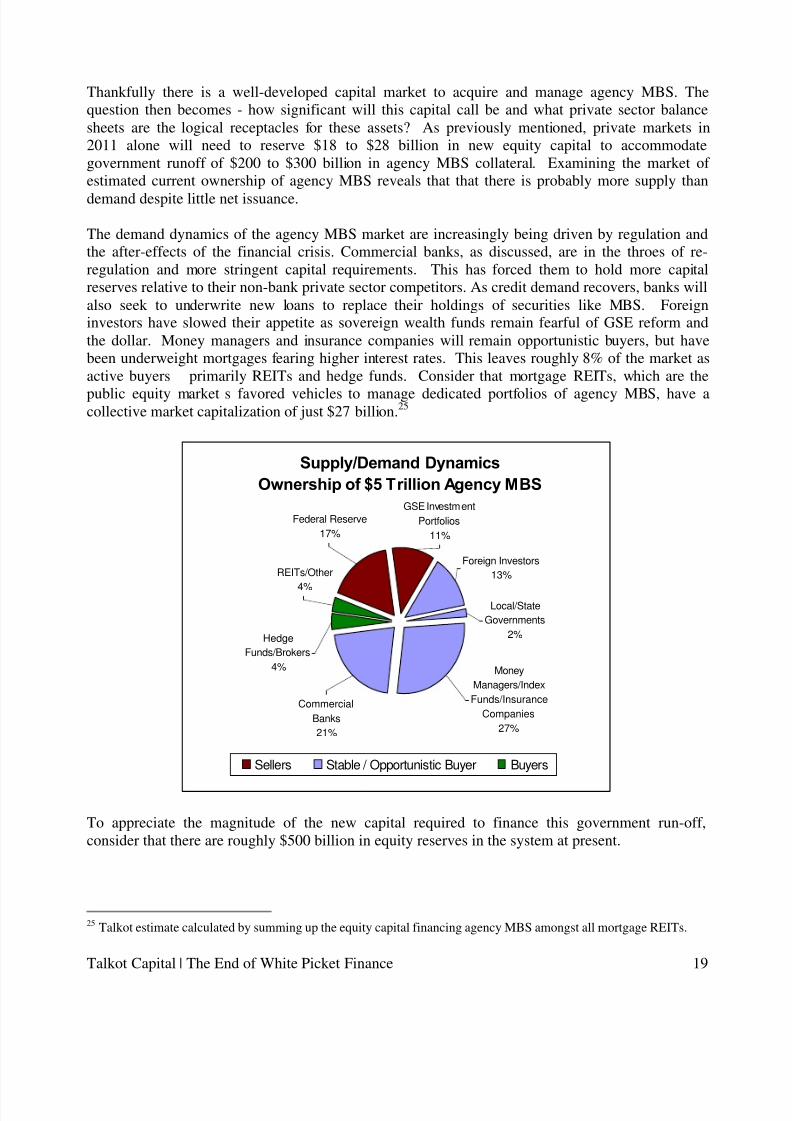

Thankfully there is a well-developed capital market to acquire and manage agency MBS. Thequestion then becomes - how significant will this capital call be and what private sector balancesheets are the logical receptacles for these assets? As previously mentioned, private markets in2011 alone will need to reserve $18 to $28 billion in new equity capital to accommodategovernment runoff of $200 to $300 billion in agency MBS collateral. Examining the market of estimated current ownership of agency MBS reveals that that there is probably more supply thandemand despite little net issuance.

The demand dynamics of the agency MBS market are increasingly being driven by regulation andthe after-effects of the financial crisis. Commercial banks, as discussed, are in the throes of re-regulation and more stringent capital requirements. This has forced them to hold more capitalreserves relative to their non-bank private sector competitors. As credit demand recovers, banks willalso seek to underwrite new loans to replace their holdings of securities like MBS. Foreigninvestors have slowed their appetite as sovereign wealth funds remain fearful of GSE reform andthe dollar. Money managers and insurance companies will remain opportunistic buyers, but havebeen underweight mortgages fearing higher interest rates. This leaves roughly 8% of the market asactive buyers primarily REITs and hedge funds. Consider that mortgage REITs, which are thepublic equity market s favored vehicles to manage dedicated portfolios of agency MBS, have acollective market capitalization of just $27 billion. 25

Supply/Demand DynamicsOwnership of $5 Trillion Agency MBS

CommercialBanks21%

Federal Reserve17%

Foreign Investors13%

Local/StateGovernments

2%

GSE InvestmentPortfolios

11%

HedgeFunds/Brokers

4%

REITs/Other

4%

MoneyManagers/IndexFunds/Insurance

Companies27%

Sellers Stable / Opportunistic Buyer Buyers

To appreciate the magnitude of the new capital required to finance this government run-off,consider that there are roughly $500 billion in equity reserves in the system at present.

25 Talkot estimate calculated by summing up the equity capital financing agency MBS amongst all mortgage REITs.

8/6/2019 Talkot Capital - The End of White Picket Finance

Total $5,400 1.4 $2,268Source: Credit Suisse, Federal Reserve. Debt to Equity Ratios are primarily Talkot estimates

Given the factors we ve considered, let s imagine what this market looks like in 2015, provided itdoesn t grow. On the supply side, GSE portfolios will continue to shrink 10% per year. TheFederal Reserve s holdings will shrink at some prepayment rate, which we assume to be 15%. Onthe demand side, we will assume that REITs and hedge funds have a disproportionate appetite forthe new supply relative to the traditional rate buyers for reasons we ve already scrutinized. Considerthat Mortgage REITs have already raised $8.1 billion in 2011 until the time of writing. 26

Agency MBS Market in 2015

Holders AssetsOwned

Debt toEquity Ratio

EquityReserves

($ in billions)

Federal Reserve $480 - $0GSE Investment Portfolio $400 40 $10

Total $5,350 1.3 $2,350Source: Credit Suisse, Federal Reserve. Debt to Equity Ratios are primarily Talkot estimates

Given these parameters, it would require an additional $80 billion in equity capital to finance the2015 MBS market. Of course, this $80 billion would be spread over several years, but this is almost20% of the current capital base for MBS which has taken decades to form. Raising $80 billion inequity would be like creating another Visa, Goldman Sachs, or Facebook. If we extend thiscalculation to a case where the government completely exited their holdings of agency MBS, thenthe total capital call could be as high as $175 billion.

26 Bloomberg June 2011

8/6/2019 Talkot Capital - The End of White Picket Finance

Talkot Capital | The End of White Picket Finance 21

These already high estimates, however, do not account for the impact of the Treasury s desire toshift mortgage origination volumes away from the GSEs and the FHA. In pre-bubble timesagencies had been the issuers of roughly 80% of annual MBS issuance (the 80/20 world). Now, theTreasury s White Paper envisions the private sector becoming the primary issuer of MBS. To beconservative, let s imagine that the private sector only meets the agencies half-way, where each isresponsible for half of annual MBS issuance (50/50 world). So assuming a $1 trillion in annualissuance (mortgage origination volumes have averaged more than $1.25 trillion the last three years)that means $500 billion will be originated from the agencies and $500 billion from our new robustmarket of non-agencies or securitized QRMs. In the 80/20 world, it would require $85 billion inequity to finance this $1 trillion. 27 In the 50/50 world, it would take closer to $100 billion anadditional $15 billion capital call . And this doesn t consider that over 2/3 of MBS investors arerate-sensitive buyers which is to say that they cannot take credit risk and possibly could be

restricted from buying QRM-like products. Many of these traditional rate-sensitive investors haveprovisions in their operating documents that prevent them from investing in credit-sensitivesecurities. $15 billion is roughly equal to the equity raised since 1997 by the largest publicly tradedportfolio of agency MBS Annaly Capital Management but there is an arguably more trenchantproblem in granting the Treasury the 50/50 world.

$15 billion in equity is sizable but still digestible. The more salient problem is how a 50/50 worldwill necessarily change the composition of collateral types in the repo market.

One of the key features of agency MBS is that they bear interest rate but not credit risk because of the government guarantee . The credit component of their risk profile carries the default risk of theirsovereign backer, which for America translates to almost zero. This special feature makes agencyMBS fundamentally what economists like Gary Gorton would call information-insensitive. 28 Inother words, when transacting these securities in a purchase, sale or repurchase agreement, neitherside has an asymmetrical information-advantage relative to the other transacting party. As such,agency MBS are afforded extremely attractive financing rates because repo lenders can know the

value of the collateral without further inspection. Conversely, securities like non-agency MBS,equities, and securities that bear pronounced default risk are necessarily more information-sensitive . For such securities, it is possible for one party to have non-public or even secretinformation about the value of the debt. Speculators who have knowledge of this information cantake advantage of those who do not.

These dynamics were key in the formation of the securitized products and key in how thoseproducts blew up financing markets. Daily repo volumes are massive, but a precise measure of thisopaque market can only be estimated. The Fed estimates that tri-party repo peaked at $2.8 trillionin 2008, but even the Fed admits this is just a fraction of the greater repo market. 29 The BISestimated that in 2008 the US repo market exceeded $10 trillion (including double counting of repos

and reverse repos).30

Gorton estimates it to be close to $12 trillion.31

That would make it slightlylarger than the US banking system, which undeservedly garners more attention and concern. The

27 Assuming 12:1 leverage for agencies and 7:1 for non-agencies.28 Gorton 2010.29 Copeland, Martin, and Walker, The Tri-Party Repo Market before the 2010 Reforms. Federal Reserve Bank of NewYork Staff Reports, November 2010.30 King and Hordahl, Developments in repo markets during the financial turmoil. BIS Quarterly Review, December2008.31 Gorton 2010.

8/6/2019 Talkot Capital - The End of White Picket Finance

Talkot Capital | The End of White Picket Finance 22

repo market is primarily composed of lenders who have cash accounts so large that the traditionalbanking system cannot accommodate them. Money market funds and current account surpluscountries like Qatar or China are good examples.

In 2006, we briefly glimpsed a 50-50 world. For the first time ever, private label securitizationeclipsed the agencies in issuance, producing vast quantities of non-agency collateral. This wasprimarily a function of the repo market s voracious demand for high quality collateral securitiescarrying AAA ratings which manifested as incredibly attractive financing rates. The now defunctThornburg Mortgage held just 4.51% capital against a portfolio of AAA non-agencies. 32

The Spike of Private Label Securitization

$-

$0.25

$0.50

$0.75

$1.00

$1.25

$1.50

$1.75

$2.00

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

2 0 1 0

Source: SIFMA, Inside MBS, and the Federal Reserve

M B S I s s u a n c e

i n T r i l l i o n s

( $ )

GSEs Private Label

A dearly underappreciated fact is how the repo market s demand for high- quality collateral spurredthe creation of highly- rated structured products. AAA ratings were the designation of information-

insensitive debt in 2006 AAA MBS had a historical default rate of 0.00%.33

But there was asignificant turning point in the market when repo depositors discovered that some of the highquality securities collateralizing their deposits - specifically private label RMBS - carriedsignificant credit and default risk. Almost overnight, information-insensitive securities becameinformation-sensitive securities and the repo markets seized up. In not unusual fashion, thisfomented what could be called a bank run and has been now appropriately dubbed a "repo" run.Like hasty depositors lining up outside a bank demanding their money, repo lenders panicked and

asked for more collateral, increased haircuts, or simply refused to roll or renew financingagreements with particular forms of collateral. As financing dried up, asset prices plunged forcingmargin calls and liquidations, which in turn sent prices plummeting further, causing more margincalls and liquidations. That many repo agreements had to be rolled overnight exacerbated the panic.

The leveraged non-agency investor was suddenly bankrupt.Ratings for non-agency MBS became meaningless, given the panic in the repo market. AgencyMBS, on the other hand, did not crater quite the same way. The non-agency contagion did affectagency MBS prices and agency repo terms to the extent that several large hedge funds managing

32 Thornburg Mortgage s 2006 Annual Report. It should be noted that TMA also funded itself through CDOs.33 S&P and UBS calculations from 2006. They also detail that AAA CMBS, HELs, and ABS all had below 0.03% 5year default rates.

8/6/2019 Talkot Capital - The End of White Picket Finance

Talkot Capital | The End of White Picket Finance 23

AAA agency MBS went bankrupt (e.g. Carlyle Capital Corporation was levered 31:1 before having toliquidate in March 2008 34). Nevertheless, agency MBS was remarkably resilient. This is partlybecause the Federal Reserve will lend against agency MBS at its discount window, which assuresall lenders that no matter what, the Federal Reserve is a fundamental backstop to the repo market(and it was). Non-agency MBS lenders do not enjoy the security of a lender of last resort. Theresiliency of agency MBS in the crisis, however, is primarily a function of a more salient feature,which provides the reason why the Fed accepts agency MBS as collateral. This, of course, is thegovernment guarantee which makes agency MBS information-insensitive.

This leads us to an important and much underappreciated point. As a market that is estimated to belarger than the US banking system, we can t ignore the repo market s effects and systemicimportance in global finance. Yet, its health is more or less tied to the quality of the collateral thatcomposes it. Just as when depositors in the early part of the 20 th century worried about the value of bank assets, repo lenders worry about the health of the collateral assets backing their loans in a repo.So how do we prevent supposedly information-insensitive securities from becoming information-sensitive again? This is a problem with the Treasury s vision shifting the share of originations toprivate markets will in turn shift the composition of MBS collateral types in the repo market. Thismeans more potentially information- sensitive securities in financing markets supplanting moreinformation- insensitive securities like agencies which maintain their integrity through crises. Thus,depending on how we define QRM and the kinds of securities the new non-agency securitizationmarkets produces, we could be increasing the systemic risks yet again in broader financing markets.

For this reason, the creation of sustainable high quality collateral will go a long way in supportingthe health of this part of the financial world and mitigating the potential for future repo runs.Thankfully, we are at a point in the cycle where these kinds of risks are probably not imminent. Yetregulators should be sensitive to these variables in crafting the next iteration of the mortgagefinance market.

Reform Moving Forward: Revolution or Evolution?

Markets tend to function more or less in a Darwinian fashion. Amongst various types of economicendeavors, certain ones are better suited to particular environments. The well-adapted survive andproliferate. Mal-adapted ones do not. Government institutions, on the other hand, are establishedfor one kind of environment and have no automatic mechanism to adjust themselves to newenvironments. The fate of a designed institution is inevitably left in the hands of policy-makers andlegislators. They must be ready and able to react to fundamental changes in circumstance withmirrored shifts in the institutions they oversee. Anything less entails political and economic decay,which could yield the next crisis. As such, the aftermath of the credit crisis has necessitated reformsof institutions like the GSEs and the FHA. The real question, as we have discovered, is one of

timing and scope. Do we pursue a policy of immediacy to reform our current dysfunctional

34 The details provided by Carlyle s press release explaining the company s imminent and complete default illuminatethe anatomy of a repo run: During the last seven business days, the Company received margin calls in excess of $400million. As the Company was unable to pay these margin calls, its lenders proceeded to foreclose on the RMBScollateral. In total, through March 12, the Company has defaulted on approximately $16.6 billion of its indebtedness.The remaining indebtedness is expected soon to go into default Overall, it has become apparent to the Company thatthe basis on which lenders are willing to provide financing against the Company s collateral has changed sosubstantially that a successful refinancing is not possible.

8/6/2019 Talkot Capital - The End of White Picket Finance

institutional equilibrium and risk economic growth? Or do we instead maintain a broken system foras long as it takes consumers to heal and risk fiscal rectitude?

The post-crisis world has forced the government s hand it has to act but how? Will reform begradual or sudden? Will we get an evolution or a revolution?

The gradualist approach to reform appears most likely. As we ve discussed, the government hasbecome the primary insurer of the nation s housing stock and deleveraging households can t affordmore debt or higher costs of housing. The other side of reality is that the American economy andUS fiscal position simply cannot afford another housing dip. A logical conclusion is that thegovernment must facilitate a period to work-through the roughly 5 or more million homes that needowners. In this case, privatization does not mean dramatic or sudden shifts that force borrowersinto more expensive QRM and other non-agency mortgage products. Instead, it means extendingthe time frame in which government agencies continue to be the primary residential housing lender.The origination shift envisioned by the Treasury will have to be postponed probably at least 10years. It could take 5 years to digest foreclosures and excessive mortgage debt and another 5 yearsto begin the wind-down of GSE and FHA origination share to pass the mortgage baton to privatelabel securitization market.

What seems certain, however, is that GSE and Federal Reserve balance sheets will run-off roughly10-15% of their $1.5 trillion in MBS per year, necessitating nearly $80 billion in equity capital overthe next 5 years. This is already happening and should keep MBS spreads wide, creating aprolonged period where investors can reinvest cash flows at attractive spreads. For rate-sensitiveinvestors, this will be a boon.

A revolutionary approach to home finance reform, on the other hand, could potentially bury theeconomy. A serious rationing of mortgage credit could double or triple foreclosure inventory,

setting off another downward spiral of debt deflation. Such a scenario would reduce incomes,making debts more burdensome, threatening the US fiscal position and crushing households further.If even just half of underwater residential borrowers default, that could tack on roughly another 5years supply of homes. And if those foreclosures cause home prices to fall another 10%, cause half of the remaining underwater borrowers to default and add close to another 5 years of foreclosureinventory. As it stands, households, banks, and the American economy will be hard pressed todigest 4 to 5 million foreclosures. An avalanche of 10 to 12 million foreclosures would makeJapan s Lost Decade look desirable.

As investors, our job is not to boil the situation down to one, single view. It is, instead, to

understand many different views simultaneously, and in doing so, to predict how different actorswill respond to the maneuvers of both sides of an intricate political discourse (or even stalemate). Itis also our job to be ready to respond to the potentially serious economic impacts of various politicaloutcomes if and when they become visible. This white paper has attempted to outline our particularview on the important issues framing reform. It is an idiosyncratic view, designed less to present anauthoritative vision than to underscore the complexity and magnitude of mortgage finance reform.Uncertainty looms large. There will be incredible opportunities, but also staggering risks, on theroad ahead. For investors, finesse will not just be rewarded. It will be required.