26

Tanzania Energy Sector-Challenges and Opportunities Babu Ram African Development Bank Main DPG Meeting, Dar Es Salaam, 2 nd June 2015

| Date post: | 27-Dec-2015 |

| Category: |

Documents |

| Upload: | bruce-armstrong |

| View: | 221 times |

| Download: | 1 times |

Tanzania Energy Sector-Challenges and Opportunities

Babu Ram

African Development Bank

Main DPG Meeting, Dar Es Salaam, 2nd June 2015

Agenda

1) Increasing energy access2) Addressing cooking energy supply 3) Natural Gas Economy4) Renewable Energy5) Current EDPG Dialogue with government6) Future Dialogue Issues

Main DPG Meeting, Dar Es Salaam, 2nd June 2015

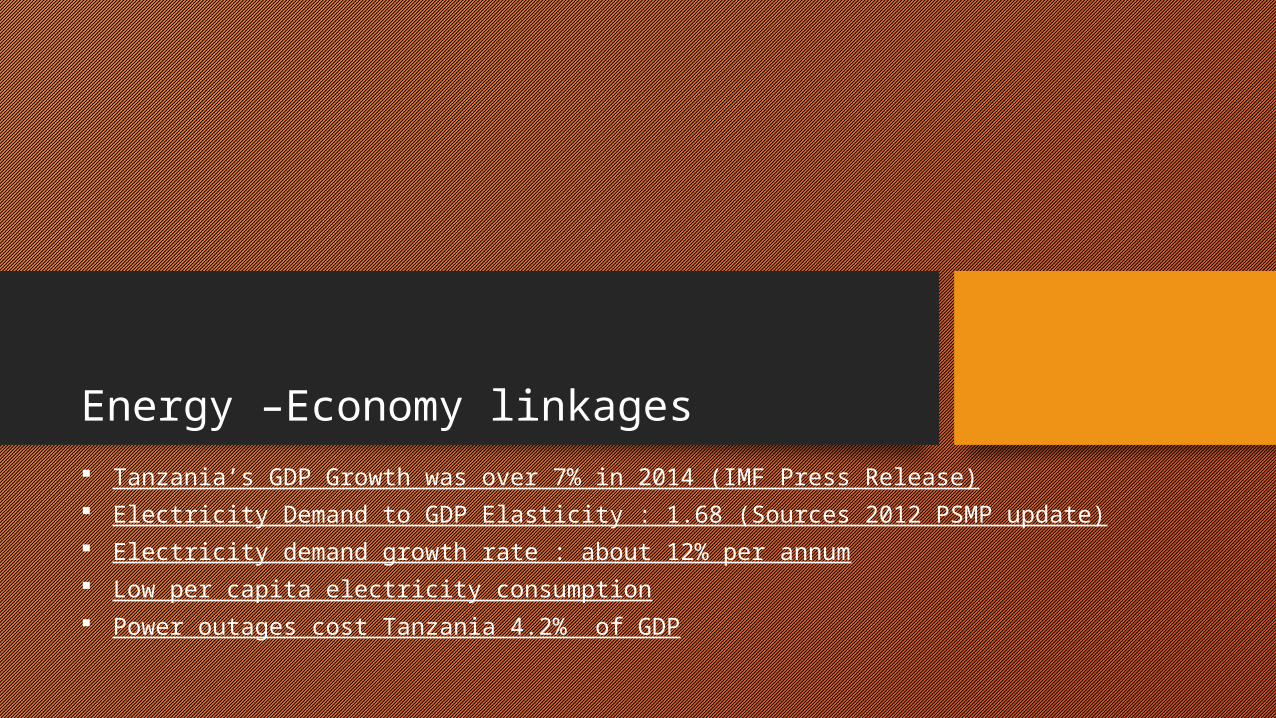

Energy –Economy linkages

Tanzania’s GDP Growth was over 7% in 2014 (IMF Press Release) Electricity Demand to GDP Elasticity : 1.68 (Sources 2012 PSMP update) Electricity demand growth rate : about 12% per annum Low per capita electricity consumption Power outages cost Tanzania 4.2% of GDP

Electricity Supply Industry: Demand

Peak demand (2020) : 2100 MW Energy Demand (2020) : 13460 GWH

Electricity Supply Industry: Supply Side

Capacity Requirement to meet peak demand in 2020 over Five Year = 3500 MW

700 MW per annum from 2015 through 2020.

Big Results Now (BRN) Initiative

(a)Mtwara-Lindi-Dar Es Salaam Pipeline, to be commissioned by September 2015;

(b)7 new power generation projects-1300 MW (natural gas and liquid fuel) by 2015/16;

(C) 7 new transmission projects, prioritised for completion in 2015/16 ;

(d) power sector reforms;

(e) Water and dam Management;and

(f) streamlining critical processes.

Electricity Supply Industry: Challenges

Low access to reliable electricity and per capita electricity use Managing electricity demand (Energy Conservation and Time of Use Pricing) Institutional and Supply side Inefficiencies Poor creditworthiness of TANESCO Investment and Capacity Constraints

Electricity Supply Industry: Challenges Energy Conservation and Demand Management Sector Governance (Transparency and Accountability-processes and institutions) Financial Resources versus Subsidy Issue Life line Tariff versus High connection fees Climate Change Risks

Electricity Supply Industry: Opportunities Second Generation Small Power Producer Framework Effective from 1st April 2015;

competive bidding documents for solar and wind prepared by June 2015; EOI by Sept15 Power Sector Reforms : Investment in Electricity Generation, Transmission and Distribution Capacity Building; Energy Conservation; and demand side management. Diversify fuel mix :Invest in Natural Gas Infrastructure (power plants, pipelines and gas

distribution network)

Cooking Energy Sources of Energy for Cooking in Tanzania (Tanzania D & H Survey,2010)

Cooking Energy

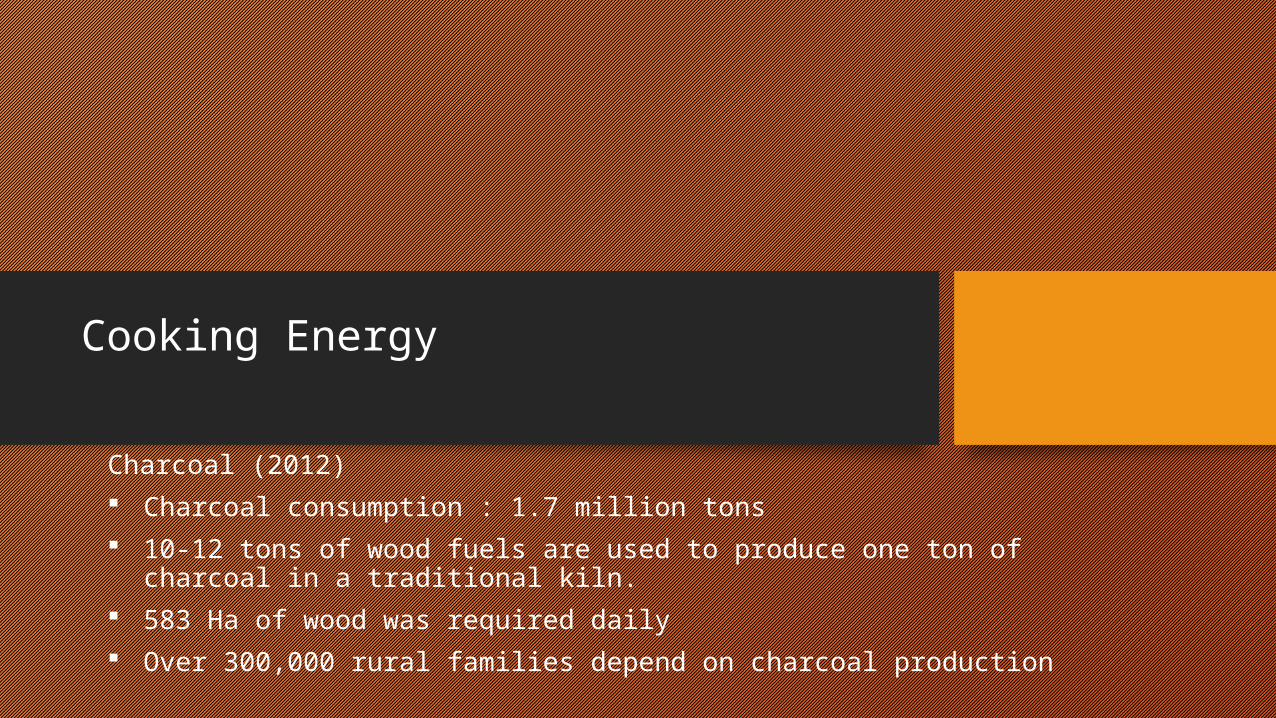

Charcoal (2012) Charcoal consumption : 1.7 million tons 10-12 tons of wood fuels are used to produce one ton of charcoal in a

traditional kiln. 583 Ha of wood was required daily Over 300,000 rural families depend on charcoal production

Cooking Energy : Charcoal

Challenges: Weak Governance and weak law enforcements : Access to wood is free Inefficient production and utilization technology Informal sector and is unregulated Health and Environmental Impacts

Natural Gas Economy

Tanzania: onshore and off-shore gas reserves : 54.5 TCF GIP. Shell is exploring blocks off shore Zanzibar-no large commercial discovery

yet. Majors : Statoil, Shell, Ophir and Exxon Mobil Corp. Final Investment Decision ? First LNG Plant become operational ?

Natural Gas Economy : Challenges

Managing Expectations

Governance

Sovereign Wealth Fund

Local Content

Capacity Building

Renewable Energy (Biomass)

Sugar bagasse (1.5 million MTPY);sisal (0.2 MTPY);coffee husk (0.1 MTPY);rice husk (0.2 MTPY);municipal solid waste (4.7 MTPY); and forest residue (1.1 MTPY).

Sustainably harvested fuelwood from fast-growing tree plantations.

Biomass for Power Production

Renewable Energy

Under the SPPA program: TPC, a major sugar producer with an SPPA for 9 MW of power; TANWATT, a tannin producer with an SPPA for 1.5 MW; Ngombeni 1MW project, commissioned in February 2014, supplies power to

TANESCO’s isolated grid on Mafia Island. TANESCO signed SPPAs for three additional biomass projects with a total

capacity of 9.6 MW.

Renewable Energy

Donor Interventions in Biomass Sector

The EU is supporting the preparation of a Biomass Energy Strategy. NORAD and SIDA are supporting institutional and legal frameworks for developing the

bioenergy (biodiesel and ethanol) subsector. CAMARTEC is implementing a four-year, country-wide biogas programme (2009–13)

supported by the Netherlands, which aims to construct 12,000 digesters of various sizes for household cooking and lighting and electricity production.

REA, under the TEDAP, is providing matching grants for development of several biomass mini- and micro-grids.

Renewable Energy (Small Hydropower)

Potential (below 10MW): 480 MW SPPA signed for four mini hydropower projects- 20.5 MW letters of intent signed for six small hydro projects with a combined capacity of

29.9 MW. MEM is conducting small hydro feasibility studies in eight regions: Morogoro,

Iringa, Njombe, Mbeya, Ruvuma, Rukwa, Katavi and Kagera. Development partners are supporting several mini-micro grid projects

throughout the country.

Renewable Energy (Geothermal Energy)

Potential: 650 MW Geothermal sites are grouped into three main prospect zones: north-

eastern (Kilimanjaro, Arusha and Mara regions), south-western (Rukwa and Mbeya regions) and the eastern coastal belt (Rufiji Basin).

Surface Exploration of Ngozi –Sogwe prospect in Mbeya region Sub-surface exploration / drilling : not yet African Development Bank’s SREP for geothermal energy development

Renewable Energy (Solar)

Solar Insolation: 4-7 kWh/m2/day Off-grid solar photovoltaic : 6 MWp (megawatt peak) Sustainable Solar Market Package (SSMP) is a contracting mechanism that

bundles the supply, installation and maintenance of PV systems for public facilities.

REA’s Lighting Rural Tanzania competitive grant programme (financed under AFREA and TEDAP), which supports private enterprises in developing new business models to supply affordable energy in rural areas.

Renewable Energy (Solar)

Grid Connected Solar Photovoltaic: The potential for grid-tied solar PV : about 800 MW In the short-term, the PSMP envisages 120 MWp of solar in the power expansion plan

by 2018. Several private firms have expressed interest in investing in 50–100 MWp of solar PV. NextGen Solawazi signed an SPPA with TANESCO to supply 2 MWp of electricity from

PV to an isolated grid. TANESCO has also signed a letter of intent for a 1 MWp isolated grid-tied PV project.

Renewable Energy (Wind)

Only Kititimo (Singida) and Makambako (Iringa), identified as having adequate wind speeds for grid-scale electricity generation. At Kititimo wind speeds average 9.9 miles per second and at Makambako averaged 8.9 miles per second at a height of 30 m.

Interested Developers : Geo-Wind Tanzania, Ltd. and Wind East Africa in Singida, and Sino Tan Renewable Energy, Ltd. and Wind Energy Tanzania, Ltd. in Makambako.

These companies are considering investments in wind farms in the 50–100 MW range.

Current EDPG Dialogue with Government

Joint Energy Sector Working Group PAF 14 Indicators (Subsidy Cap Indicator is not fulfilled) PAF15-17 Indicators Power Sector Reforms Draft Energy Policy –Feb2015 Arrears

Future EDPG Dialogue with Government

Sound management of natural gas revenues to ensure shared prosperity and increased development spending.

Natural gas economy (e.g. gas regulatory framework policy, Natural Gas Act, Gas Utilization Master Plan )

Power Sector Reforms Road Map Financial Viability of TANESCO

Future Dialogue with Government

Subsidy Policy Biomass Strategy Natural Gas Utilization Natural Gas Exports via LNG Route

Thank You for Your Kind Attention

![ICES REPORT 16-01 The DPG methodology applied to different … · 2016. 1. 29. · DPG. The optimal stability DPG methodology [16,18], referred here simply as “DPG”, was originally](https://static.documents.pub/doc/80x56/60c9ac6187230b2a2d2cdffd/ices-report-16-01-the-dpg-methodology-applied-to-different-2016-1-29-dpg-the.jpg)