25

Tara McCarthy, Chief Executive Food Wise 2025 Conference Croke Park, 4 th December 2017

Tara McCarthy, Chief Executive

Food Wise 2025 Conference

Croke Park, 4th December 2017

OUTLINE

Export trends for Irish Food & Drink

Market Prioritisation Study

Key Findings

Next Steps

x

x x

x

x

x

xx

xx

x

x

BORD BIA’S MISSION

To drive the success of a world class Irish food, drink and horticulture industry through

strategic market development, promotion & information services

x

x

xxx

x

xx

x

x

x

x

x

Main Growth Categories

FOOD & DRINK EXPORTS

€12.2 billion

(including forestry &

non-edible agri-food)

€11.15 billion

the value of Irish food

& drink exports

The sector recorded

the 7th consecutive

year of growth in

exports during 2016

Irish food &

drink is sold in

180 markets

worldwide

Growth of

41% or €3.27

billion since

2010

DISTRIBUTION OF IRISH FOOD & DRINKEXPORTS

41%

31%28%

37%

32% 31%35%

33% 32%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

UK Other EU International

2015 2016 2017 (est)

UK: UP 7%

OTHER EU: UP17%

INTERNATIONAL: UP 18%

2017 EXPORTS JAN – SEPT (est)

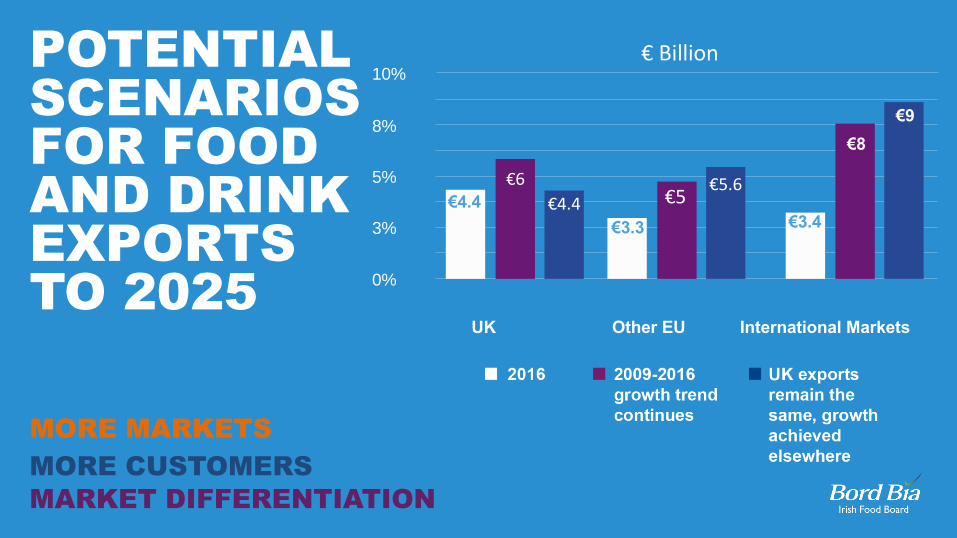

POTENTIALSCENARIOSFOR FOOD AND DRINKEXPORTSTO 2025

0%

8%

10%

5%

3%

UK International MarketsOther EU

€4.4

€3.3 €3.4

€8

€9

MORE MARKETS

MORE CUSTOMERS

MARKET DIFFERENTIATION

€6€5€4.4

€5.6

€ Billion

MACRO-TRENDSDRIVING THECONSUMPTION OFFOOD AND DRINK

New Buying Habits

Greater Transparency

New Forms of food production

Holistic Health

Time Poverty

New Ways of buying food

REGIONALTRENDS DRIVINGCONSUMPTION

UK

Food inflation further driving move towards

Discounters

Europe

The Big shift: from large to small brands

North America

ASIA Global Urbanisation spurring demand for western

food and drink

Middle East Growing heath awareness and increasing income

levels driving premium markets

Food shopping revolution: traditional grocery

declines as price wars heat up

OBJECTIVES:

Assess attractiveness of markets by category

Examine ability of Ireland to supply

MARKETPRIORITISATIONSTUDY

Consultation with industry throughout project

SUMMARY REPORT FOR

EACH MARKET

DEEP DIVE ON 5-10

MARKETS

Published end 2017

Published 2018

CRITERIA FOR INITIAL SCREENING

Market size and trends

• Size of middle class

• Urbanisation

• Rate of growth in the food market

• Currency trends

Projections

• Population

• Income per capita

• Import demand

Imports

• Import levels by category/sub category

• Import price levels

• Tariffs rates

Doing business

• Ease of doing business ranking

• Ease of logistical access

• Market access status

ASIA

China

South Korea

Japan

Malaysia

Indonesia

Vietnam

Taiwan

Iran

UAE

Singapore

Hong Kong

AMERICAS

Mexico

Chile

AFRICA

South Africa

Egypt

OCEANIA

Australia

New Zealand

All 3 Meats Beef Pork Mutton

TOP 15 MARKETS FOR MEAT

TOP 15 MARKETS FOR DAIRY

Africa

Algeria

Nigeria

Egypt

South America

Brazil

Mexico

Asia

China

Indonesia

Japan

Malaysia

Philippines

S. Korea

Saudi Arabia

UAE

Vietnam

North America

US

WPC80/WPI Cheddar WMP

ASIA

South Korea

Hong Kong

Japan

Saudi Arabia

UAE

Qatar

Kuwait

NORTH AMERICA

Canada

USA

EUROPE

France

Belgium

Netherlands

Germany

Sweden

OCEANIA

Australia

Value Added Bakery Premium Frozen

Meats Chocolate

TOP 15 MARKETS FOR PREPARED CONSUMER FOODS

Asia

Japan

North America

United States

Canada

Mexico

Europe

Netherlands

Czech Republic

France

Germany

Russia

Poland

Italy

Denmark

Slovakia

Lithuana

Africa

Sth. Africa

Oceania

Australia

TOP 15 MARKETS FOR BEVERAGES

Whiskey Beer Cream Liqueur’s

Molluscs Crustaceans Salmon Pelagics

TOP 15 MARKETS FOR SEAFOOD

Asia

Hong Kong

Malaysia

Indonesia

Saudi Arabia

UAE

Kuwait

Israel

North America

USA

Canada

Oceania

Australia

Europe

Switzerland

Czech Republic

Finland

Denmark

Belgium

SAMPLE CONTENTSFOR SUMMARY REPORTS

Market summary

• Category volume

• Growth rates

• Market trends, segmentation

• Level of self-sufficiency

• Significant cultural, religious and social factors

Market channels

• In-market distribution structure

• Cost of doing business (food/beverage specific)

• Significant / trends in E-commerce

Competitive situation

• Main competitors present

• Relative price levels by sub category

• Competitiveness of Ireland

Logistics / Shipping time to market

• Track record of Irish food and drink sector

• Ease of access for Ireland

- Tariff / regulatory / technical / other barriers

KEY FINDINGS

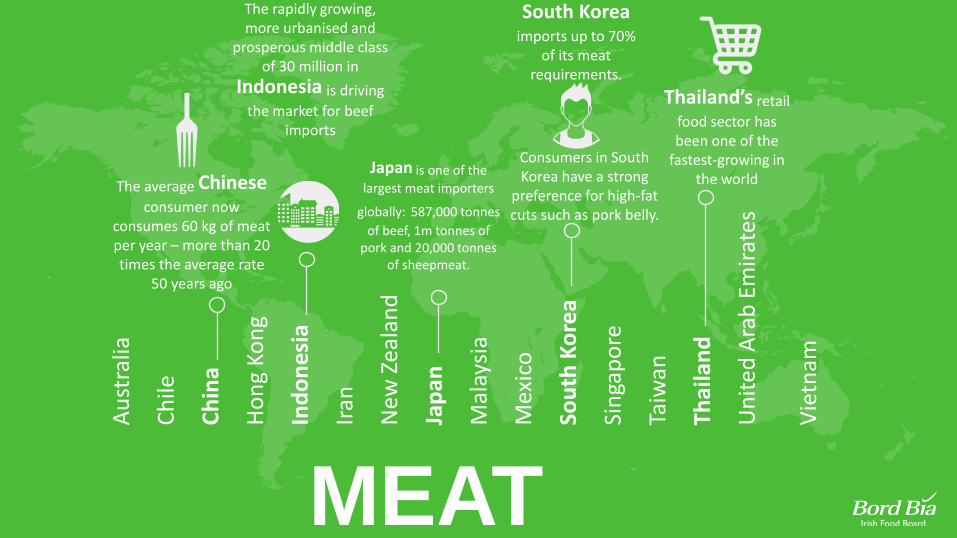

MEAT

Au

stra

lia

Ch

ile

Ch

ina

Ho

ng

Kon

g

Ind

on

esia

Iran

New

Zea

lan

d

Jap

an

Mal

aysi

a

Mex

ico

Sou

th K

ore

a

Sin

gap

ore

Taiw

an

Thai

lan

d

Un

ited

Ara

b E

mir

ates

Vie

tnam

The average Chinese consumer now

consumes 60 kg of meat per year – more than 20 times the average rate

50 years ago

The rapidly growing, more urbanised and

prosperous middle class of 30 million in

Indonesia is driving

the market for beef imports

South Korea imports up to 70%

of its meat requirements.

Japan is one of the

largest meat importers

globally: 587,000 tonnes

of beef, 1m tonnes of pork and 20,000 tonnes

of sheepmeat.

Consumers in South Korea have a strong

preference for high-fat cuts such as pork belly.

Thailand’s retail

food sector has been one of the

fastest-growing in the world

DAIRY

Alg

eri

a

Bra

zil

Ch

ina

Egypt

Ind

on

esia

Nig

eri

a

Ja

pa

n

Mala

ysia

Sa

ud

i A

rab

ia

Me

xic

o

Ph

ilip

pin

es

So

uth

Ko

rea

Un

ite

d A

rab

Em

ira

tes

US

A

Vie

tna

m

China is 75% self sufficient in dairy and

this is expected to reduce to 65% by

2025. It is the world’s largest importer of whole milk powder

at over 400,000

tonnes.

Nigeria is 30%

self-sufficient in milk and is the world’s largest

importer of Full Fat Milk Powder at

91,000 mt.Imports have grown

25% over last five years.

Saudi Arabia is

the world’s no 5 importer of cheddar, which has increased dairy imports over

recent years

South Korea is the

world’s no 7 importer of cheddar at

20,000 tonnes.

The USA is the 9th

largest importer of cheddar and the

world’s no 1 importer of casein.

KEY FINDINGSSUMMARY

Meat and dairy demand across all categories is growing

Strong potential to disrupt new markets based on price and emerging preferences for premium and traceable products

Growth opportunities for Irish offering is strong

Deep Dive Reports will support further work needed to fully understand how markets operate

NEXT STEPS

•

• Industry Briefing Days in January

• Commence target market deep dives with industry

• Trade Missions starting with Canada/US in Spring 2018

• Marketplace April 12th 2018

BORD BIASTRATEGIC PILLARSStatement of Strategy 2016 - 2018

1 2 3 4 5

Informed by consumer

insight

Enabled by valued

people, talent and

infrastructure

Under pinned

by Origin GreenRealised by effective

routes to market

Supported by strong

brand communications

in the digital age

MARKETPLACE 2018

• Unique, invitation-only,

trade event bringing together

world class Irish food

and drink exporters and

international trade buyers

from around the world.

500+ Buyers

April 12th 2018, Dublin

SNAPSHOT REPORT AVAILABLE

IN BORD BIA’S BREAKOUT ROOM

THANK YOU