Tassal Group Limited Tassal Group Limited Results Presentation Financial Year Ended 30 June 2008 27 August 2008 The following slides should be read in conjunction with Tassal Group Limited’s Appendix 4E: Preliminary Final Report for the Year Ended 30 June 2008 lodged with the Australian Securities Exchange on 27 August 2008 1 Australian Securities Exchange on 27 August 2008

Transcript

Tassal Group LimitedTassal Group Limited

Results Presentation

Financial Year Ended 30 June 2008

27 August 2008

The following slides should be read in conjunction with Tassal Group Limited’s Appendix 4E: Preliminary Final Report for the Year Ended 30 June 2008 lodged with the

Australian Securities Exchange on 27 August 2008

1

Australian Securities Exchange on 27 August 2008

AgendaAgenda

• Executive Summary

• Historical Performance • Historical Performance

• Financial Detail

• Superior Gold Update

• Priorities

• Outlook

2

Executive SummaryExecutive Summary

Tassal is pleased to announce a strong Full Year Normalised result for 2008 1Tassal is pleased to announce a strong Full Year Normalised result for 2008 1

Revenue of $167.3m (+16% on pcp)

EBITDA of $34.7m (+22% on pcp)

NPAT of $21.2m (+33% on pcp)

Basic EPS 17.1 cps (+22% on pcp)

Net Debt reduced to $32 6m (from $52 1m at 30 June 2007)Net Debt reduced to $32.6m (from $52.1m at 30 June 2007)

Final dividend of 3.5c per share (+27% on pcp)

30-June-2008 30-June-2007 Change ChangeU d l i ti l lt $’000 $’000 $’000 %Underlying operational result $’000 $’000 $’000 %Revenue (from all sources) 167,266$ 144,001$ 23,265$ 16.16%EBITDA 34,661$ 28,431$ 6,230$ 21.91%Depreciation (2,457)$ (1,623)$ (834)$ 51.39%EBIT 32,204$ 26,808$ 5,396$ 20.13%Borrowing Costs (4 114)$ (4 590)$ 476$ (10 37)%Borrowing Costs (4,114)$ (4,590)$ 476$ (10.37)%Profit before income tax expense 28,090$ 22,218$ 5,872$ 26.43%Tax expense (6,890)$ (6,230)$ (660)$ 10.59%NPAT 21,200$ 15,988$ 5,212$ 32.60%EPS 0.171$ 0.140$ 0.031$ 21.83%

31. Underlying operational earnings (i.e. normalised earnings) have been adjusted for the impact of AASB141 and non-recurring items to reflect the underlying financial performance of the Group

Executive SummaryExecutive Summary

Key Highlights:y g g

Strong growth in salmon demand – overall sales volume growth of 14.3%

Improved operating metrics – increase in harvested fish size, reduced cost of production and higher effective price for domestic and export

The underlying finished goods cost (i.e. cost of fish, processing, third party contractors and packaging) was reduced to $6.54 kg hog [FY2007: $6.91kg hog]

Proceeds from capital raising employed towards acquisition of Superior Gold, pursuing growth opportunities, accelerating capital investment and reducing debt

Superior Gold performing to plan with $8.3m revenue contribution for the period –achieving synergies on supply and trading terms

Accelerated capital investment focused on growth, efficiency and risk mitigation Accelerated capital investment focused on growth, efficiency and risk mitigation

Continued research & development with focus on fish husbandry and selective breeding program

4

Strong cash generation and reduction in net debt

Historical Performance Historical Performance

Growth in domestic demand for Salmon + trout leading to strong volume growth g g g

16,000 16,000

10 000

12,000

14,000

'000

)

10 000

12,000

14,000

'000

)

6,000

8,000

10,000

og kgs sold (

Export

Domestic6,000

8,000

10,000

og kgs sold (

Export

Domestic

‐

2,000

4,000 Ho Domestic

‐

2,000

4,000 Ho Domestic

2004 2005 2006 2007 2008

Year ended 30 June

2004 2005 2006 2007 2008

Year ended 30 June

5

Historical Performance Historical Performance

Tassal continues to consistently deliver a reducing cost base Cost improvement of 37% over period

Fish growing costs on track to deliver FY2015 global best practice target of $3 50 kg

$‐

$2.00

2004 2005 2006 2007 2008

Finishe

$‐

$2.00

2004 2005 2006 2007 2008

Finishe

$3.50 kg

(nb: Data not broken down due to competitor sensitivities)

2004 2005 2006 2007 2008

Year ended 30 June

2004 2005 2006 2007 2008

Year ended 30 June

6* Underlying finished goods cost = cost of fish, processing, third party contractors, and packaging expressed as a cost per head on gutted equivalent kilogram

Historical Performance Historical Performance

Strong growth in underlying NPAT and EPSStrong growth in underlying NPAT and EPS

$0 16

$0.18 $25,000

$0 16

$0.18 $25,000

$0 10

$0.12

$0.14

$0.16

$15,000

$20,000

ing EPS

g NPA

T

$0 10

$0.12

$0.14

$0.16

$15,000

$20,000

ing EPS

g NPA

T

EPS CAGR: FY2004 – FY2008 37.6%

$0.06

$0.08

$0.10

$10,000 Und

erlyi

Und

erlyin

$0.06

$0.08

$0.10

$10,000 Und

erlyi

Und

erlyin

$‐

$0.02

$0.04

$0

$5,000

2004 2005 2006 2007 2008

$‐

$0.02

$0.04

$0

$5,000

2004 2005 2006 2007 20082004 2005 2006 2007 2008

Year ended 30 June

Underlying NPAT Underlying EPS

2004 2005 2006 2007 2008

Year ended 30 June

Underlying NPAT Underlying EPS

7

Historical Performance Historical Performance

Continuing to return an increasing dividend payment Continuing to return an increasing dividend payment to shareholders – payout ratio circa 40%

7 00$10 000 7 00$10 000

DRP active - cash saved is being 5.00

6.00

7.00

$8,000

$10,000

000) 5.00

6.00

7.00

$8,000

$10,000

000)

utilised to grow the business from both an operational and infrastructure

3.00

4.00

$4,000

$6,000

ts per sh

are

ividen

d paid ($'0

3.00

4.00

$4,000

$6,000

ts per sh

are

ividen

d paid ($'0

perspective, as well as reducing gearing

‐

1.00

2.00

$0

$2,000

CentDi

‐

1.00

2.00

$0

$2,000

CentDi

2004 2005 2006 2007 2008

Year ended 30 June

Quantum ($'000) CPS

2004 2005 2006 2007 2008

Year ended 30 June

Quantum ($'000) CPS

8

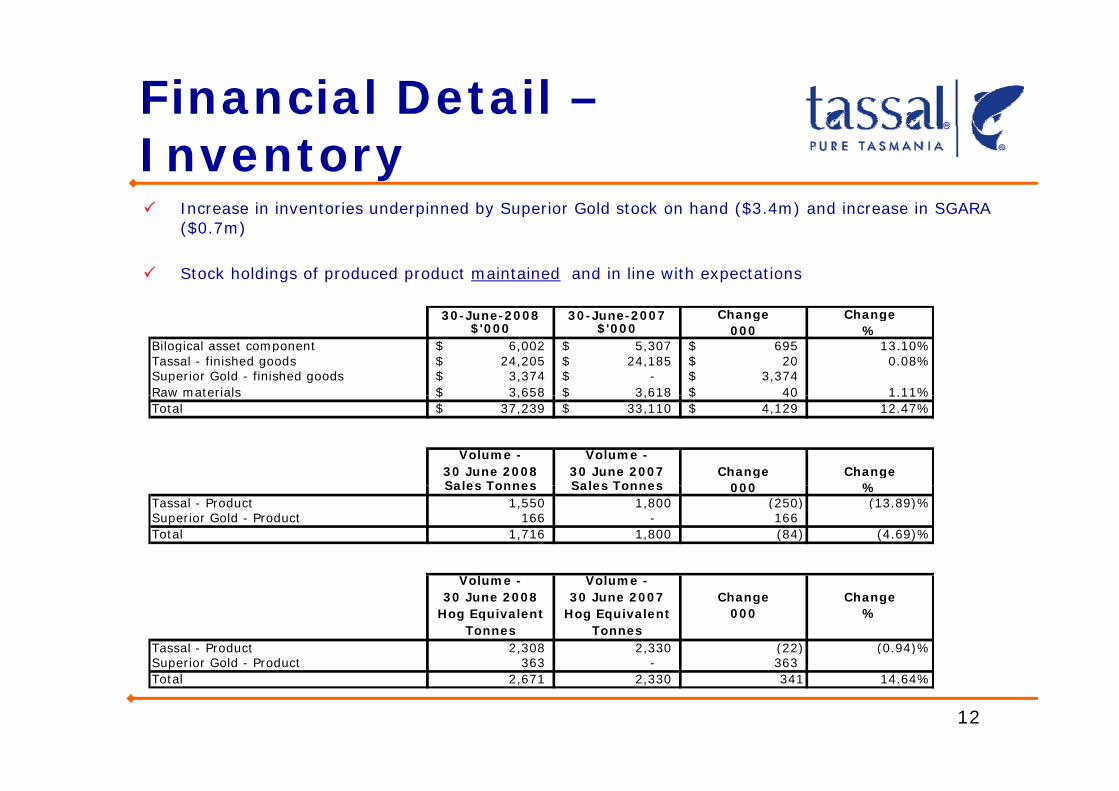

Financial DetailFinancial Detail

Strong underlying (“Normalised”) NPAT $21.2 million (+33% compared to pcp)Strong underlying ( Normalised ) NPAT $21.2 million (+33% compared to pcp)

Strong growth in sales revenue (16.1%) and sales volume (14.3%)

Strong growth in EBITDA (21 9%) underpinned by strong domestic salmon sales and Strong growth in EBITDA (21.9%) underpinned by strong domestic salmon sales and reduction in cost of growing and processing

“Normalised” results remove the impact of AASB 141 “Agriculture” and add FY2008

Superior Gold Product 363 363 Total 2,671 2,330 341 14.64%

Financial Detail – Net Debt Bridge

Strong cash generation and reduction in net debtStrong cash generation and reduction in net debt

Proceeds from capital raising employed towards acquisition of Superior Gold, pursuing growth opportunities, accelerating capital investment and reducing debt

$65.6m$3.0m$29.1m

$m

Strong underlying

$52.1m

$25.4m Strong underlying cash flow from operations

Utilised to underpin growth in inventory$5

$11.4m

$32.6m

growth in inventory

Net debt Superior Gold Capital Net Capital OperatingDividend / Net debt

Gearing 17.2%Gearing 49.7%

13

Net debt 30 June 2007

Superior GoldBrand & Inventory

Capital Investment

Net CapitalRaising

Operating Cash Flow

Dividend /Other

Net debt 30 June 2008

Financial Detail – Cash “drill down”

Strong operating cash flow supporting growth in working

Significant cash profit

Strong operating cash flow supporting growth in working capital and capital investment and reducing net debt

Movement Movement12 Months 12 Months Period

Ended Ended Movement Significant cash profit uplift from operations

2008 focus on targeted and planned investment in live fish growth

ded ded o e e t30/06/2008 30/06/2007 Differential

Profit after tax add back non-cash items $34,979 $28,363 $6,616

(Increase) / decrease in assets:

Inventories (net of AASB 141 Impact) ($3 434) ($17 884) $14 450 in live fish growth

2007 focus on processed stock build to the required level to meet both future demand

Inventories (net of AASB 141 Impact) ($3,434) ($17,884) $14,450Biological assets (net of AASB 141 Impact)) ($16,341) ($5,104) ($11,237)

Combined inventory category movement ($19,775) ($22,988) $3,213

Current trade and other receivables ($9,580) ($1,702) ($7,878)Other ($311) ($474) $163

requirements and accompanying sales lead times

Debtors increase reflects

Total (Increase) / decrease in assets: ($29,666) ($25,164) ($4,502)

Increase / (decrease) in liabilities

Current trade and other payables $3,360 $6,091 ($2,731)Other $354 $96 $258

increased retail sales and Petuna sales commencement in H2 FY2008.

Total Increase / (decrease) in liabilities $3,714 $6,187 ($2,473)

Net cash from operating activities for the period $9,027 $9,386 ($359)

Adjustment for Superior Gold inventory acquired at brand purchase date $2,366

14

Underlying net cash from operating activities for the period $11,393 $9,386 $2,007

Financial Detail –Capital Investment Tassal’s accelerated capital investment plan is focused on growth, efficiency and p p g , yrisk mitigation capital items

Efficiency related items target pay back less than 2 years and IRR + 30%.

Hatchery

Automatic feeders

Harvest vessels

Margate expansiong p

Processing automation

Product innovationProduct innovation

15

HatcheryHatchery

Rookwood Hatchery - on stream Q4 FY2009 4 million SmoltCost – circa $15m -$18m Funding via debt /

Rookwood Hatchery - on stream Q4 FY2009

Funding via debt / operating cash flowWill allow significant improvement in smolt size and smolt size and reduction of late smoltsLow water requirement -q209,500,000 fewer litres water per dayControlled environment

OxygenTemperature

Easier to staffCloser to farms = Closer to farms lower transport cost

16

Automatic FeedersAutomatic Feeders

All stock now fed via automatic feedersNo missed feeding No missed feeding opportunitiesScale down marine labour force numbersScale down vessel Scale down vessel fleetMaximise technologyMaximise our Feed Conversion Ratio Conversion Ratio –i.e. “kgs of feed in for a kg of growth out”:Cost (3 units) -$2.5m - $3.0m$2.5m $3.0mPayback < 1 yearIRR + 50%

17

Harvest Vessels Harvest Vessels

“Tassal 1” in useArctic Bear en routeReduced risk

EscapementEscapementMortalitySpread of disease

QualityS i ld h iSuperior cold chain managementLower stress

Margate facility to be upgraded to be primary fresh primary fresh processing siteInfrastructure investment as part of FY2015 t t i Pl FY2015 strategic Plan and 30,000 tonnes platformUnlikely to materially impact FY2009

20

Product InnovationProduct Innovation

21

Superior Gold UpdateSuperior Gold Update

Superior Gold made a positive EBIT contribution for the 4.5 months to 30 June p p2008 in line with expectations.

Completed acquisition on 15 February 2008

Acquisition price $25.4m, comprising brand value ($23.1m), inventory ($2.3m)

Superior Gold achieved sales of $8.3m for the 4.5 months to 30 June 2008

Sales comprise Salmon $6.8m and Trout $1.5m.

Planning for annualised revenue, net of discontinued lines, of $25m.

22

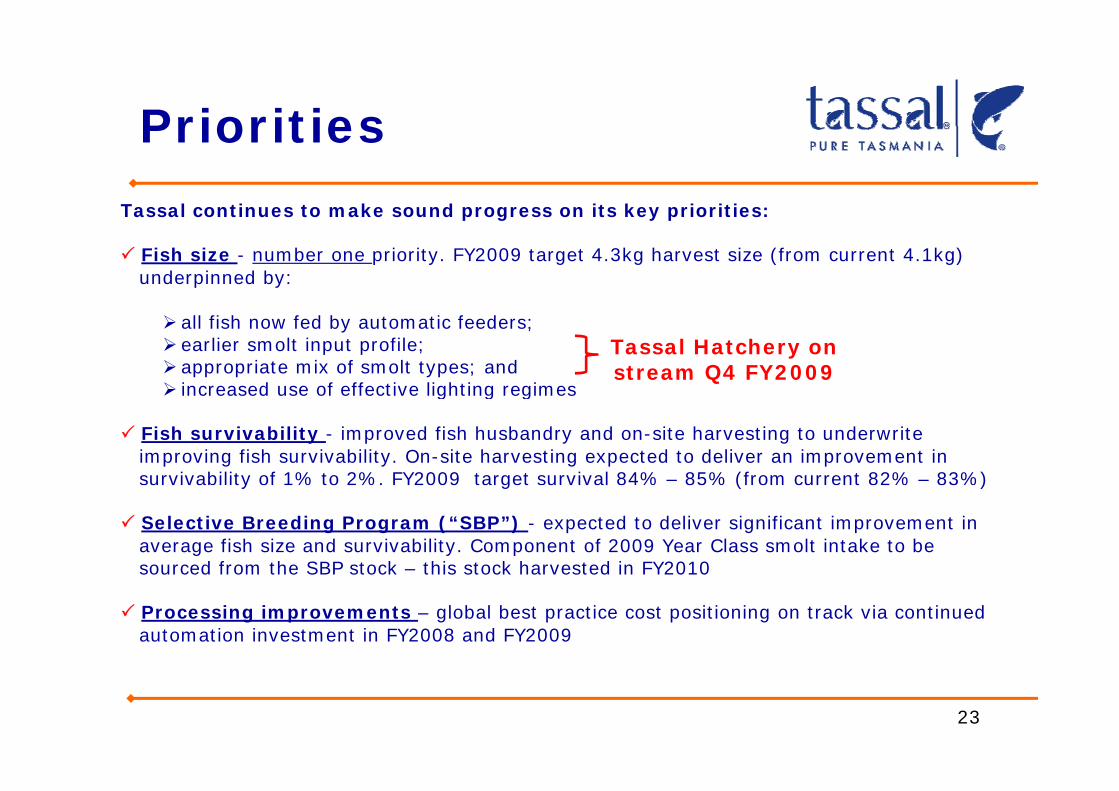

PrioritiesPriorities

Tassal continues to make sound progress on its key priorities:Tassal continues to make sound progress on its key priorities:

Fish size - number one priority. FY2009 target 4.3kg harvest size (from current 4.1kg) underpinned by:

all fish now fed by automatic feeders; earlier smolt input profile; appropriate mix of smolt types; andincreased use of effective lighting regimes

Tassal Hatchery on stream Q4 FY2009

increased use of effective lighting regimes

Fish survivability - improved fish husbandry and on-site harvesting to underwrite improving fish survivability. On-site harvesting expected to deliver an improvement in survivability of 1% to 2%. FY2009 target survival 84% – 85% (from current 82% – 83%)y g ( )

Selective Breeding Program (“SBP”) - expected to deliver significant improvement in average fish size and survivability. Component of 2009 Year Class smolt intake to be sourced from the SBP stock – this stock harvested in FY2010

Processing improvements – global best practice cost positioning on track via continued automation investment in FY2008 and FY2009

23

PrioritiesPriorities

Branding opportunities - essential that Tassal has a strong Tassal “Pure Tasmania” brand. Creating a strong brand:

strengthens product range positioning; strengthens product range positioning; provides innovation delivery conduit to consumers; builds on existing customer loyalty; andprovides imported products protection

Imported Product – must maintain vigilance and not become complacent - we have strong competition from both our local competitor (from a fresh Salmon perspective) and imports (from a smoked and frozen Salmon perspective). The Superior Gold acquisition was an important strategic acquisition in this contextp g q

Revenue Initiatives - Tassal continues to seek out new profitable markets and products both from a domestic and export sales perspective. With limited global supply and an ever increasing demand, we remain confident of strong growth in the 2009 financial year and g , g g ybeyond

24

Outlook Outlook

Tassal is well positioned to deliver continued earnings momentum in 2009 p g

Tassal will continue to implement the financial and operational strategies underpinning the Strategic Plan to FY2015

Will continue to fast track push to become globally cost competitive

Expect global supply will grow by a nominal 1% p.a. which should translate into an improved export price in 2009

Disease issues in Chile remain a significant constraint to global supply

Expect to benefit from lower AUD exchange rate

Tassal is well positioned to benefit from the investments made in 2008. Tassal is experiencing strong earnings momentum and expects to achieve an p g g g punderlying NPAT of $30 million for FY2009, in line with its previous guidance

25

Questions Questions

Have fun,

work hard,

stay healthystay healthy,

eat salmoneat salmon

26

DisclaimerDisclaimer

This presentation has been prepared by Tassal Group Limited for professional investors The information This presentation has been prepared by Tassal Group Limited for professional investors. The information contained in this presentation is for information purposes only and does not constitute an offer to issue, or arrange to issue, securities or other financial products. The information contained in this presentation is not investment or financial product advice and is not intended to be used as the basis for making an investment decision. The presentation has been prepared without taking into account the investment objectives, financial situation or particular need of any particular person.

No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness or correctness of the information, opinions and conclusions contained in the presentation. To the maximum extent permitted by law, none of Tassal Group Limited, its directors, employees or agents, nor any other extent permitted by law, none of Tassal Group Limited, its directors, employees or agents, nor any other person accepts any liability, including, without limitation, any liability arising out of fault or particular, no representation or warranty, express or implied is given as to the accuracy, completeness or correctness, likelihood of achievement or reasonableness of any forecasts, prospects or returns contained in this presentation nor is any obligation assumed to update such information. Such forecasts, prospects or returns are by their nature subject to significant uncertainties and contingenciesare by their nature subject to significant uncertainties and contingencies.

Before making an investment decision, you should consider, with or without the assistance of a financial adviser, whether an investment is appropriate in light of your particular investment needs, objectives and financial circumstances. Past performance is no guarantee of future performance.

The distribution of this document is jurisdictions outside Australia may be restricted by law. Any recipient of this document outside Australia must seek advice on and observe such restrictions.