126

MARKETING STRATEGY OF TATA AIG INSURANCE COMPANY

| Date post: | 04-Dec-2015 |

| Category: |

Documents |

| Upload: | suryakant-shrotriya |

| View: | 236 times |

| Download: | 3 times |

MARKETING STRATEGY

OF

TATA AIG INSURANCE COMPANY

TABLE OF CONTENTS

Sr. No. Topic

1- INTRODUCTION TO INSURANCE AND

TATA AIG

2- COMPANY PROFILE AND SWOT

ANALYSIS OF THE COMPANY

3- OBJECTIVE OF STUDY

4- RESEARCH METHODOLOGY

5- DATA ANALYSIS AND INTERPRETATION

6- FINDING AND ANALYSIS

7- RECOMMENDATIONS AND

SUGGESTION:CONCLUSION

8- LIMITATION

9- QUESTIONNAIRE

10- BIBLOGRAPHY

INSURANCE

INTRODUCTION

The business of insurance is related to the protection of the economic

value of assets. Every asset has a value.

The asset gets lost earlier, being destroyed or made non-functional,

through an accident or other unfortunate event, the owner and those

deriving benefits there from suffer. Insurance is a mechanism the helps

to reduce such adverse consequences.

PURPOSE & NEED OF INSURANCE

Assets are insured, because they are likely to be destroyed or made

non-functional, through an accidental occurrence. Such possible

occurrences are called perils. Fire, floods, breakdowns, lightning,

earthquakes, etc, are perils.

Risk : A possibility of loss or damage. It may or may not happen.

There has to be an uncertainty about the risk. Insurance is done

against the contingency that it may happen.

Insurance : People/Assets must be exposed to the same risks

Insurance : Risk is spread among the community and the likely big

impact on one is reduced to smaller manageable impacts on all.

Insurance companies: collect money in advance and create a fund

from which the losses are paid.

A human life is also an income generating asset. This asset also can

be lost through unexpectedly early death – Accidents may or may not

happen.

Living too long can be as much as problem as dying too young. These

are risks which need to be safeguarded against.

Insurance covers economic or financial loses – tangible and intangible

assets.

HOW INSURANCE WORKS

People facing common risks come together and make their small

contributions to a common fund. The contribution to be made by each

person is determined on the assumption that while it may not be possible

to tell beforehand, which person will suffer, it is possible to tell, on the

basis of past experiences, how many persons, on an average, may suffer

losses.

Insurance is about

Sharing the same risk

Paying out compensation (claims)

Insurer ensures: no body takes undue advantage.

BUSINESS OF INSURANCE

The business of insurance done by insurance companies, called

insurers, is to bring together persons with common insurance interests

collecting the share or contribution from all of them and paying out

compensations to those who suffer.

The business of insurance is nothing but one of sharing. It spreads

losses of an individual over the group of individuals who face

common risk.

It ensures that nobody takes undue advantage of the arrangement.

FUNDAMENTAL PRICIPLES

Life Insurance Contracts

A contract may be defined as an agreement between two or more

parties to do or to abstain from doing an act, with an intention to

create a legally binding relationship. A simple contract to be

enforceable must have following essentials :-

- Offer and acceptance

- Consideration

- Capacity to contract

- Consensus ‘ad idem’

- legality of object

Commercial contracts

Commercial contracts are normally subject to the principle of caveat

emptor i.e. let the buyer beware. In most of these contracts each party

to the contract can examine the item or service. Which is the subject

matter of contract.

Insurance contracts

As for insurance contracts, the product sold is intangible. It cannot be

seen or felt. Moreover, most of the facts relating to health, habits,

personal history, family history are known to one party only, the

proposer.

PRINCIPLE OF UTMOST GOOD FAITH (Uberrimae Fides)

Proposer must disclose every material known to him. This type of

contract is called Uberrimae Fides i.e. contract of utmost good faith.

Facts that would influence the judgement of a prudent insurer in fixing

the premium or determining whether he will take the risk. Therefore,

facts regarding age, height, weight, build, previous medical history,

smoking / drinking habits, operations, non-disclosure of earlier

insurances, ‘hazardous’ occupation must be disclosed.

There are certain circumstances, a facts which need not be disclosed.

For example :

(1) Facts which every one is supposed to know.

(2) Facts of common knowledge.

(3) Facts which lessen the risk.

(4) Facts which could be reasonably discovered, by reference to

previous policies, records of which are available with the insurer.

INSURABLE INTEREST

All risks are not insurable. In order to be insurable, the risk must be

capable to financial measurement, there must be sufficient number of

similar risks, the risk must be capable of statistical (actuarial) estimation.

It must not be against public policy, and there must be insurable interest

in the property to be insured/risk to be covered.

The Insurance Act, 1938 does not define insurable interest. Insurable

interest is said to exist when the person insuring stands to lose if the event

insured against occurs.

Person has insurable interest in his own life to an unlimited extent.

Insures take into account a proposer’s capacity to pay premiums and his

need for insurance, while granting the sum insured.

Instances of Insurable Interest

Common people having insurable interest

- Spouses have insurable interest in each other.

- Partners can insure each other’s lives.

- Creditors have insurable interest in debtors

- Employers have insurable interest in the life of employees.

The legal position about children’s assurances is not quite clear. It is

presumed that parents have insurable interest in the life of a child as a

child i.e. so long as he is a child. Therefore most of the LIC’s

children’s policies incorporate a vesting clause, whereby the policy

vests in the child on attainment of majority.

CAREER OPPORTUNITY

DISCOVER A WORLD OF GREAT OPPORTUNITY WITH THE

LEADING SERVICE INDUSTRY

THE INSURANCE SECTOR

NATIONALISED IN 1956 :

LIC WAS THE ONLY PLAYER TILL 2000

GOVERNMENT HAS DE-REGULATED THE INDUSTRY

THE FASTEST GROWING BUSINESS IN India TODAY

LIFE INSURANE PENETRATION IN India IS 1.4%

PER CAPITA SPEND IN India – Rs. 235.00

LIFE INSURANCE : THE

FASTEST GROWING INDUSTRY

A Rs. 30,000 CRORE BUSINESS

GROWING AT 20% EVERY YEAR

ONLY 1.4 % OF THE India IS INSURED

HUGE INCOME POTENTIAL FOR YOU

OBJECTIVES

THE MAIN OBJECTIVES OF THE STUDY ARE AS FOLLOWS :

To present an overview of Tata AIG Insurance company with its

marketing strategies.

To study the history of Tata AIG.

To assess the nature of Joint Venture, Investment Pattern, Entry

Strategies and product of Prudential Tata AIG Insurance Company.

To collect Data through market survey.

To analyze the comparative marketing strategies of Tata AIG with

other Companies.

To change the profile of Insurance Agents.

To analyze a data collected using factor analysis.

COMPANY PROFILE

VSERV- A PROFILE

As the name suggests VSERV is here to serve its people, promote ease to

its client & insure the best of its service to all.

Established in March 99 by Mr. Herpreet Singh. VSERV was initially

formed distributing mutual funds & bonds. The company slowly

broadened its horizon & in the year 2001 when insurance fell into the

hands of Pvt. sector VSERV entered into life & general Insurance with

TATA AIG. By April 2001 there were two companies founded under the

banner of VSERV namely, VSERV CAPITAL SERVICES PVT LTD.&

VSERV INSURANCE SERVICE PVT LTD, both catering to the

insurance needs of its customers.

VSERV CAPITAL SERVICES PVT LTD.

Incorporated under companies act 1956, VSERV CAPITAL

SERVICES PVT LTD is the sister concern of VSERV that deals in

investment , stock brooking , management consulting & recruiting &

training activities as business associates for TATA AIG.

The company under the administration of its board of directors

comprising of Mr. Harpreet Singh , Harpreet Kaur & Vir Singh Veer

operate through a team of people of which 300 are directly employed &

over 2000 indirect employees . The company has an extensively

networked area of operation which covers states of Delhi , Punjab ,

Haryana , Rajasthan , Uttar Pradesh & the metropolitan city of Chennai .

As the " Annual Convention 2003 ", Dubai, puts it - VSERV is the

number 1 Business Associate with TATA AIG for past 3 years

VSERV INSURANCE SERVICES PRIVATE LTD.

Incorporated in the same year, April 2001, under the companies act 1956,

the company is headed by a directorial panel under Mr. Harpreet Singh

and Mr. Vir Singh Veer.

This company deals in both life and general insurance and is operative in

the capital city, Delhi.

CLIENTS

VSERV proudly assests its cliental to over 10,000 accounts in the past

three years. It has over 20 co-operate clients serving names like HCL

Group & Barista.

STRENGTHS

"When it comes to service we don’t look at the cost"

The company lives by this Motto. It practices a highly customer focus

approach & believes in retaining clients by providing them with

exceptional services.

To achieve this state of professionalism the company has experienced &

qualified professionals at its disposal. Along with this the company also

has a well recruited managing team & staff with trained & knowledgeable

personnel who are well versed in the fields of insurance & financial

services.

Tata-AIG Life Insurance

PROFILE

Tata-AIG Life Insurance company is a joint venture between the Tata

Group and American International Group Inc (AIG), the leading US-

based international insurance and financial services organisation and the

largest underwriter of commercial and industrial insurance in America.

Its member companies write a wide range of commercial, personal and

life insurance products through a variety of distribution channels in

approximately 130 countries and jurisdictions throughout the world.

AIG’s global businesses also include financial services and asset

management, including aircraft leasing, financial products, trading and

market making, consumer finance, institutional, retail and direct

investment fund asset management, real estate investment management,

and retirement savings products.

Areas of business

Tata-AIG Life Insurance products include a broad array of life insurance

coverage to both individuals and groups. For groups, the company has

life products whereas for individuals, it has term products, endowment

products as well as money-back products. For groups and individuals,

various types of add-ons and options are available to give consumers

flexibility and choice.

INTRODUCTION

TATA GROUP

The Tata Group is the most respected industrial business house serving

India for 123 years with reventues of over Rs. 42,000 crores, with 80

companies present in seven business sectors.

The Group had a long association with India’s Insurance sector, having

been the largest Insurance Company in India prior to nationalization of

Insurance.

Specialty Group Companies :

TELCO

TATA INFOTECH

TATA CONSULTANCY SERVICES

TATA STEEL (TISCO)

TATA HOTELS (TAJ)

AND MANY MORE

Deep routed commitment towards Indian society.

AIG: A LEADER IN THE

INSURANCE BUSINESS

American International group Inc. (AIG), the leading US Based

International Insurance and Financial Services Organization with a

presence in over 149 countries and jurisdiction throughout the world.

AIG is the largest Insurance Co., founded in 1919 and it has

successful 84 years of history.

AIG global business also includes financial services and asset

management, financial products, consumer finance etc.

AIG IS AMONGST THE FEW ‘AAA’ RATED COMPANIES IN

THE WORLD

Sales Force of 115,000 World Wide.

Revenue $ 62.4 billion (Rs. 3,12,000 crores)

Net Income $ 7.66 billion (Rs. 38,300 crores)

Assets $ 492.98 billion (Rs. 24,64,900 crores)

Cutting Edge Training

Outstanding Rating

4 in Forbes 500

12 in fortunes 500

“Every cent of Premium we collect must one day be returned to our

Policy Holders”

- C.V. Starr, founder of AIG.

TATA AIG

INTRODUCTION

Tata AIG is a joint venture that is backed by the Tata Group, one of the

India’s most respected Industrial Conglomerates, with revenue of over

Rs. 40,000 crores, and American International Group, Inc. (AIG), the

leading US based international insurance & Financial Services

Organization.

THE TATA GROUP 74%

AIG 26%

Tata AIG offers a gamut of innovative products in the Life Insurance

Sector. Tata AIG is one of the few partnership in the Indian Insurance

Industry that brings you arrange of Insurance Products : from automobile

to life Insurance, from travel to personal accident coverage, and more.

TATA AIG LIFE

A joint venture bringing to household names together, launched in April

2001 in Mumbai, Delhi, Kolkata, Chennai, Banglore, Hyderabad and

expending rapidly.

In the Private Insurance Market Tata AIG life is :

Fastest growing new life insurance co. in India.

Presence in 14 cities and expanding constantly.

The leading Whole of Life provider with 50% of all policyholders

choosing Mahalife

Number One in Providing Term assurance

Our biggest seller is the Money Back Plan with 29% market share

Last year our annual bonus was amongst the largest paid in the

industry @ 5% compounded.

AREA OF BUSINESS

Tata AIG like Insurance products include a broad array of Life Insurance

coverage to both individual and groups.

For groups, the company has life products whereas for individual, it has

term products, endowment products as well as money back products. For

groups and individuals, various types of options are available to give

consumers flexibility and choices.

TATA AIG – VISION

Profitably

Deliver consistently excellent

Service and develop our

People in a constantly

Changing environment.

Bidest range of products to cater to needs of all segments

A unique career progression structure for advisors.

Not offer by all other companies in India.

HISTORY

TATA HISTORY - FAMILY TREE

JAMSETJI TATA

Founder of India’s largest and

internationally best non group of companies.

Began with a textile mill in central

India in the 1870s.

SIR DORABJI TATA SIR RATAN TATA

Sir Dorabji Tata

Trust (1932)

JEHANGIR RANTANJI

DADABHOY TATA

(1904 – 1993)

Pioneered civil aviation

on the subcontinent in

1932

Funding Dr. Homi

Bhabha

RATAN N. TATA

Group Chairman

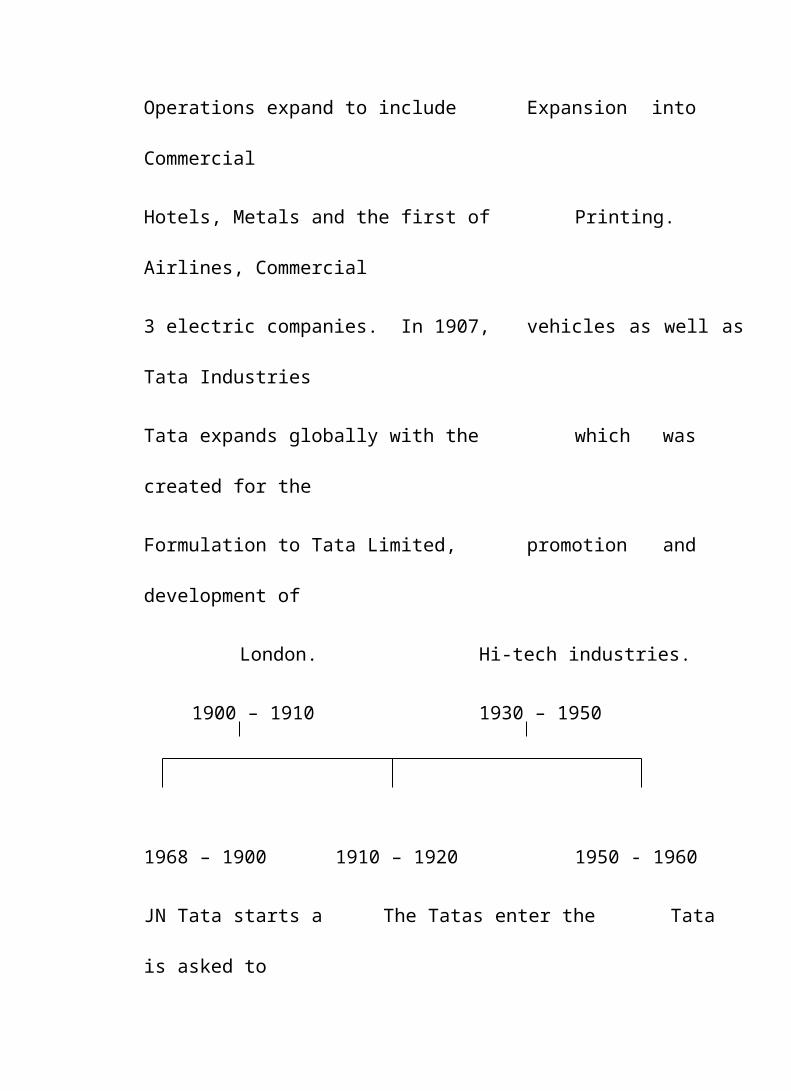

TATA HISTORY : 1868 – 1960

Operations expand to include Expansion into Commercial

Hotels, Metals and the first of Printing. Airlines, Commercial

3 electric companies. In 1907, vehicles as well as Tata Industries

Tata expands globally with the which was created for the

Formulation to Tata Limited, promotion and development of

London. Hi-tech industries.

1900 – 1910 1930 – 1950

1968 – 1900 1910 – 1920 1950 - 1960

JN Tata starts a The Tatas enter the Tata is asked to

private trading firm consumer goods with the manufactures

laying the Tata oil mills Companies in

foundation for the Company making soaps, India. India’s

Tata empire. First detergents and cooking Major

operation include oils. Manufacturing

textiles, spinning and engineering

and weaving organization,

companies Voltas, is

in 1887, Tata and Sons established.

is established

TATA HISTORY : 1960 – 1990

Tata moves into the fields of Ratan N. Tata appointed

Publishing, Techno - Chairman of Air India long

Economic research & after J.R.D. Tata, founder of

Engineering Product. Tata Air India, Ceased to occupy

Opens the World’s largest that post

Palm Oil processing facility

1970 – 1980 1986

1960 – 1970 1980 – 1990 1980 - 1990

Tata exports and Marked by Tata watches

Tata Switzerland collaborations with launches its

formed to promote Hands Motor Co. Rs. 22 crores.

the export of and Honey well Tata Central

Indian Products. International. Archives

Tata expands into first 500 MW is created.

Tea, Nuclear and Power plant Tatamobile and

Aeronautical commissioned. Tata 406 by

Consulting. Tata Tata Engineering.

consultancy

services is formed

TATA HISTORY : 1990 – 1998

Seven major Tata New Tata Group

Group companies corporate logo and

formality adopt the mark are launched.

Tata Group code of

conduct.

1998 1998

1991 1998 1998

After 50 years at The first Tata electric

The helm, JRD Tata indigenously companies

steps Down as designed, acquire power

Chairman of developed and facilities from

Tata sons. He is manufacture ACC.

replaced by the car is introduced

present chairman, by Tata Indica.

Ratan N. Tata.

TATA HISTORY : 1998 – PRESENT

Tata Tea acquires Tata Steel becomes

the Tetley group, UK. The first Tata Group Co.

this is the first major to win the JRD QV award

acquisition of an Tata.

international brand by

an Indian Group.

2000 2000

2000 2000 2001

The Aditya Birla Significant changes Tata announces

Group, AT&T announced in the a partnership

and Tata Tata Sons board with AIG to offer

industries to improve corporate insurance and

sign an MOU governance. financial

to merge their services products

cellular properties in India

into a joint venture

AIG HISTORY : 1919 – PRESENT

1919 : C.V. Starr founds Americal Asiatic under writers.

1921 : Asia life insurance Co. is formed.

1926 : AAU opens American International under writers.

1930’s : AIU begins a Worldwide expansion.

1939 : Headquarters moved to New York.

1940’s : Latin America penetration begins

1946 : AIU becomes the first foreign insurance operation

allowed back into Japan & Germany after W WII.

1950’s : AIU’s presence includes over 75 offices Worldwide.

1960’s : Acquisition. Basic structure in place for DBG.

1967 : M.R. Greenberg becomes president and CEO. AIG

established as a holding Co.

1969 : AIG goes public.

1970’s : AIG acquires and creates specialty companies.

1984 : AIG lists its shares on the New York Stock Exchange.

1990’s : Expansion in China, Latin America, Israel, and the former

Eastern Bloc.

1990 : Financial Services begins expansion.

1992 : AIG becomes the first foreign the first foreign insurance

organization to receive an operating license from the

Chinese government.

1994 : AIG enters the untapped markets of Russia and Uzbekistan.

1996 : The Asian Infrastructure Fund raises $ 1.1 billion.

1998 : Reopening of the Bund Building.

1999 : Acquisition of Sun America Inc.

2001 : AIG Acquires American General AIG’s net income rises to

a record high of $ 7.66 Bn. Consolidated assets approximate

$ 492B.

SWOT ANALYSIS

STRENGTHS:

1. No. 1 Private Player in the insurance industry in India.

2. Life Insurance linked with Investments

3. Tax benefits

4. Security against loans

5. Helps in future planning and provides financial consultancy.

6. Covers risk.

WEAKNESS:

1. Negativity relating insurance and ‘Agents’.

2. No fixed Salary.

OPPORTUNITIES:

1. High Network Individuals (HNI)

2. A clear career path

3. All round support through exclusive advertising, own in house

consultant, and world-class training.

4. A comprehensive benefit package.

THREATS:

1. Dynamic environment

2. Increasing Competition

3. Non-creativity

4. An Unfocused approach

5. Complacency and arrogance

METHODOLOGY

Data can be classified under the two main categories, depending upon the

sources used for the collection purposes, i.e., ‘Primary data’ and

‘Secondary data’. The validity and accuracy of final judgement is most

crucial and depends heavily upon how well the data is gathered in the

first place. The methodology adopted for data gathering also affects the

conclusions drawn there from.

Primary data: Primary data are those data, which are collected by the

investigator himself for the purpose of a specific enquiry or study. Such

data are original in character and are generated by surveys conducted by

individuals or research institutions. Thus we can say that the data that is

being collected for the first time is called primary data.

Methods that can be used for collection of primary data are as follows:

Direct personal observation: Under this method, the

investigator presents himself personally before the

informant and obtains first hand information. This method

provides greater degree of accuracy.

Telephone survey: Under this method the investigator,

instead of presenting himself before the informants,

contacts them on telephone and collects information from

them.

Indirect personal interview: Under this method, instead

of directly approaching the informants, the investigator

interviews several third persons who are directly or

indirectly concerned with the subject – matter of the

enquiry and who are in possession of the requisite

information. This method is highly suitable where the

direct personal investigation is not practicable either

because the informants are unwilling or reluctant to

supply the information or where the information desired is

complex or the study in hand is extensive.

Questionnaire method: Under this method, the

investigator prepares a questionnaire containing a number

of questions pertaining to the field of enquiry. Under this

method, the investigator directly contact the person and

collect the information through questionnaire related to

the data. The aims and objectives of collecting the

information, and requesting the respondents to cooperate

by furnishing the correct replies and fill the questionnaire

with correct information. The success of this method

depends upon the proper drafting of the questionnaire and

the cooperation of the respondents.

Secondary data: When a person uses data, which has already been

collected by someone else, then such data is known as secondary data.

Secondary data should be used with extra caution since someone else has

collected it for his/her use. Before using such data the investigator must

be satisfied with regard to the reliability, accuracy, adequacy and

suitability of the data to the given problem under investigation.

Methods that can be used for collection of secondary data are as follows:

Published sources: There are a number of national

organisations and international agencies, which collect

and publish statistical data relating to business, trade,

labour, price, consumption, production, etc. These

publications of the various organisations are useful

sources of secondary data.

Unpublished sources: The records maintained by private

firms or business houses who may not like to release their

data to any outside agency are known as unpublished

sources of collection of secondary data.

Both ‘Primary data collection methods’ and ‘Secondary data collection

methods’ have various advantages as well as limitations. Thus it would

be prudent to use both these methods to one’s advantage.

More of the primary data has been used in this project.

INSURANCE ADVISOR

IRDA TRAINING

The Insurance Act, 1938 lays down that an insurance agent will be issued

a license under section 42 of the Act, by the IRDA of an officer

authorized by it in this behalf.

Tata AIG offices and approved by INSURANCE REGULATORY

AND DEVELOPMENT AUTHORITY (IRDA). A licence issued by

the IRDA will be valid for three years. The licence may be to act as an

agent for a life insurer, for a general insurer or as a “Composite Insurance

Agent” working for a life insurer as well as a general insurer.

An Insurance agent have undergone practical training for at least 100

hours in life or general insurance business. He should have also passed

the pre-recruitment examination conducted by the Insurance Institute of

India.

An Insurance Agent have to give a demand draft for Rs. 1000 payable in

favor of Tata AIG Life Insurance Co. Limited.

COMPETITION DISTRIBUTION STRATEGIES

TATA AIG AGENCY

Managing Director

Director - Agency Director – alternate channels

Asst. Director – Agency(Three Zones)

Zone Head

Agency Manager

Management Business Associate

Senior Business Associate

Business Associate

Insurance Advisor

Recruit and manage sales teams

Future to grow Earn – BIG !!!!!

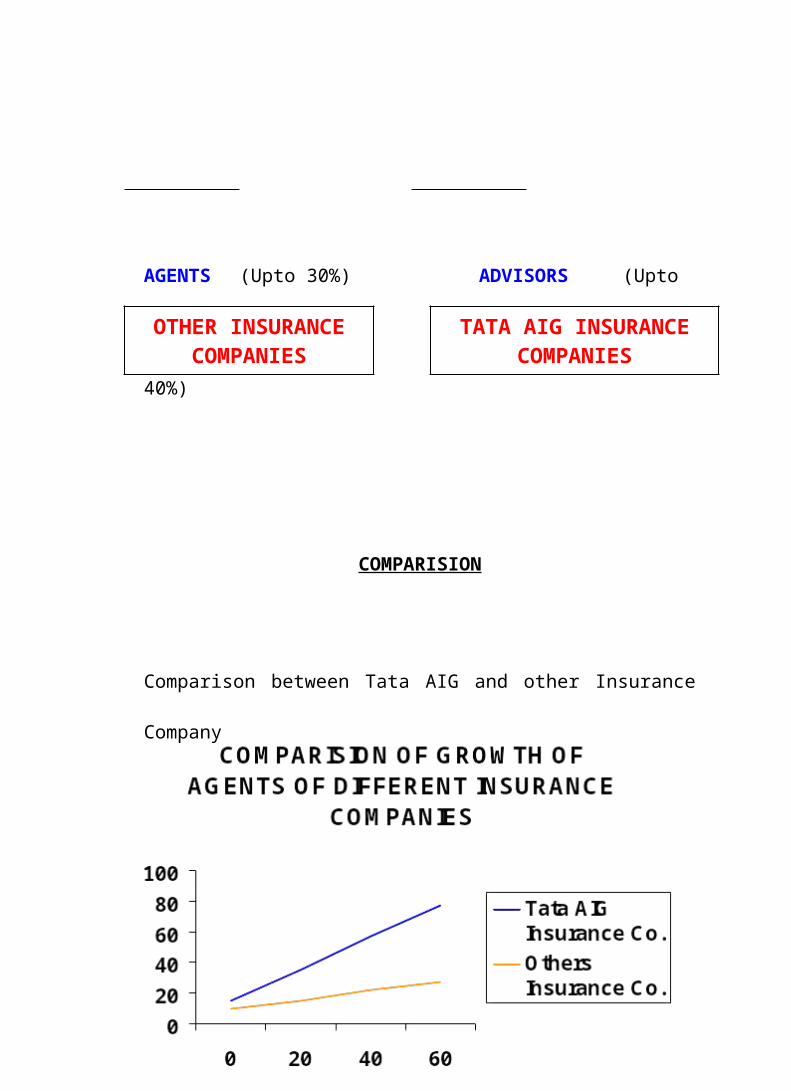

CAREER GROWTH CHART

MANAGEMENT BUSINESS (4% of

SBA)

ASSOCIATES

SENIOR BUSINESS (8% of BA)

ASSOCIATES

(CAN’T GO BUSINESS ASSOCIATES (25% of Total

Advisors)

BEYOND THIS)

AGENTS (Upto 30%) ADVISORS (Upto

40%)

COMPARISION

Comparison between Tata AIG and other Insurance Company

OTHER INSURANCE COMPANIES

TATA AIG INSURANCE COMPANIES

MARKETING STRATEGIES OF

TATA AIG INSURANCE

TATA AIG HEALTH FIRST

Quality healthcare is expensive; you need a policy that covers all

contingencies. HealthFirst provides you with security by guaranteeing a

lump sum irrespective of your medical bills. You can purchase this policy

while your existing medical insurance policy is still in force and renew it

until age 64 without additional medical examinations.

Key features include:

THE BENEFITS SHOWN BELOW ARE FOR A POLICY

PURCHASED FOR 10 UNITS

Daily Hospitalization Benefit (DHB): During hospitalization, we

will pay an allowance of Rs. 2,500 per day.

Surgical Benefit: A lump sum of Rs. 1,25,000 is paid for specified

surgical procedures. We pay the complete amount, even if the

procedures costs less. This benefit is payable only if DHB is

payable.

Post-hospitalization Benefit: After hospitalization, we will pay Rs.

1,250 a day for follow-up treatment (up to a maximum of 3 days).

This benefit is payable only if DHB is payable.

Critical Illness Cover: You get Rs. 12.50 lakhs in the case of first

diagnoses of specified of the 12 critical illnesses.

Death Benefit: In the unfortunate event of your death, coverage of

Rs. 10,000 is provided to protect your family.This benefit is

payable if no other benefit has been claimed for.

Policy can be purchased from 1 to 10 units.

TAX BENEFITS AND AGE ELIGIBILITY

Premiums paid for Health Insurance Benefits are eligible for tax

benefits under section 80D, while premiums for Life Insurance

Benefits are eligible for tax benefits under section 80C of the

Income Tax Act, 1961.*

Policy available for persons between 18 and 60 years of age.

Treatment must occur at a pre-approved hospital.

MAHALIFE GOLD

This unique policy is an ideal planning vehicle to fund your

retirement. It provides a steady income and insurance coverage for

life. Premiums are payable only for the first 15 years, and can be used

to cover the future expenses of your children.

Key features include:

A guaranteed annual coupon of 5% of the sum assured every

year for the rest of the insured’s term from the 10th policy

anniversary.

Yearly cash dividends are available from the 6th policy

anniversary onwards (depending on Company performance).

The entire sum assured is paid tax-free as per current Income

Tax Laws.

INVESTASSURE GOLD

InvestAssure Gold is a non-participating Whole Life Unit Linked

insurance plan, which offers you the unique advantage of

combining the protection and tax advantages of life insurance with

the attractive prospects of investing in different kinds of securities

through multiple fund options. With this plan, you can direct the

investments by creating your own investment fund portfolio from a

range of options to suit your needs and preferences.

Key features include:

Flexibility to choose your premium payment term: 5 years or

for the entire duration of the policy.

Benefit period: For the entire life till 100 years of age.

Facility to increase the premium through Top up Premium.

Provides security to your family in case of your unfortunate

death.

Facility to increase the Sum Assured through Top up

Premium.

Gives you the flexibility to choose your fund based on your

risk profile - Whole Life Mid Cap Equity, Whole Life

Aggressive Growth, Whole Life Stable Growth, Whole Life

Income, and Whole Life Short Term Fixed Income. You

may choose to switch between the funds, anytime subject to

certain conditions.

Enables you to enjoy market-linked returns with a potential

for higher growth.

Opportunity to bring you additional income on funds that

might have otherwise given you minimum returns in your

savings account, subject to market performance.

Loyalty Benefit: Additional 0.25% of units under the

Regular Premium Account every 5 years provided the policy

is in force.

INVESTASSURE PLUS

InvestAssure Plus is a single premium Unit Linked insurance plan

especially designed for the investment-savvy. It gives you the

flexibility of choosing your own investment strategy, besides

providing protection to your loved ones in case of a misfortune.

This plan gives you an opportunity to make the most of good market

returns, albeit with an increased investment volatility. At the same

time, it does not compromise the security that you want to provide to

your loved ones.

Multiple benefits of Invest Assure Plus:·

Provides security to your family in case of your unfortunate

death.

Gives you the flexibility to choose your fund based on your risk

profile.

Enables you to enjoy market-linked returns with a potential for

higher growth.

Key features include:

Policy terms of 15, 20, 25 or 30 years.

No penalty charges for surrendering the policy any time after

the 3rd year.

Flexibility to choose your Sum Assured, depending on your age

profile and your needs.

You have a choice of premium multiples to choose from.

Any premium not deducted for coverage and charges will be

invested in the funds chosen by you viz. Equity Fund, Income

Fund, Aggressive Growth Fund, Stable Growth Fund and a

Short Term Fixed Income Fund.

Flexibility to switch between funds and partial withdrawal.

InvestAssure Plus also offers Top-ups premiums and the facility

to have a Sum assured on the Top-up premium as well.

Tax Benefits

Premiums paid under this plan are eligible for tax benefits under

Section 80C of the Income Tax Act, 1961. Any sum received

under this plan is exempt from tax under section 10(10D) of the

Income Tax Act, 1961.*

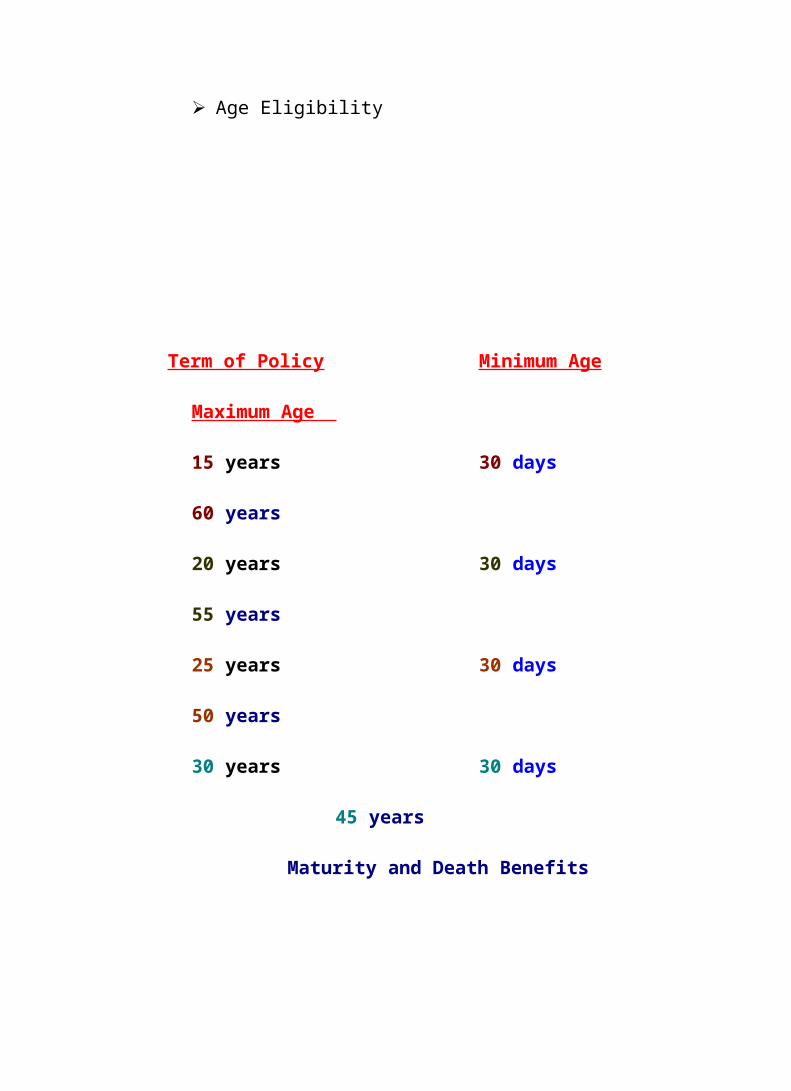

Age Eligibility

Term of Policy Minimum Age

Maximum Age

15 years 30 days 60 years

20 years 30 days 55 years

25 years 30 days 50 years

30 years 30 days 45 years

Maturity and Death Benefits

LIFE PLUS

If you outlive the 20-year term of a LifePlus policy, all of your

premium payments will be refunded; if you die by natural causes

while the policy is in force, your beneficiaries will receive the sum

assured; should you die due to accidental causes, your beneficiaries

will receive double the sum assured.

Key features include:

All premiums paid are returned (without interest) in the event

you outlive the policy’s 20-year term.

Premiums are payable only for the first 15 years of the 20-year

term.

ASSURE 21 YEARS MONEY SAVER

This savings plan gives you the cash payments at specified intervals to

fund your family’s needs at critical milestones or support your

financial obligations. You get the dual benefits of life insurance

coverage plus the flexibility of periodic payments.

Key features include:

10% of the sum assured is paid on survival on the 3rd /6th

/9th /12th /15th and 18th policy anniversaries.

40% of the sum assured will be paid on maturity (i.e. on the

21st anniversary of this policy).

The entire sum assured is distributed to your beneficiaries,

irrespective of cash payments already made, in the unfortunate

event of your death before the end of the policy’s term.

A 10% Guaranteed Addition is payable on death or maturity, if

the policy has been inforce for 10 years.

A reversionary and terminal bonus payable on death or

maturity. Terminal bonus is available only if policy is in force

for more than 10 years.

Bonuses are paid depending on performance of the company.

MAHALIFE

This distinctive policy provides a steady income and insurance

coverage for life. Premiums are payable only for the first 12 years.

You can even use this to cover future expenses of your children.

Key features include:

A guaranteed annual coupon of 5% of sum assured, every

year for the rest of the insured’s life from the 12th policy

anniversary onwards.

If Tata AIG Life performs well, you get yearly cash dividend

from the 6th policy anniversary onwards.

On death or at maturity at age 100, the entire sum assured

will be paid tax-free according to current Income Tax Laws.

SHUBHLIFE

Have you been delaying getting life insurance because you cannot

afford to pay high monthly premiums? Then we have the ideal

product for you.

ShubhLife provides you 100% life insurance protection and a range

of bonuses but the premiums you pay are among the lowest of any

similar endowment policy.

Key features include:

Term policies just give you death cover. This policy gives

you bonuses along with death cover.

You can choose a term of 10, 15, 20, 25 or 30 years.

Apart from full premium paying term, you can pay your

premiums over 3, 5, 7 or 10 years.

Guaranteed addition of 3% of sum assured of the Basic

Policy is added on the first (1st) policy anniversary and on

every alternate policy anniversary thereafter up till a

maximum of half the policy term. The GA will be payable if

the insured dies while the policy has been in force or if the

policy matures.

A simple reversionary bonus will be credited from the sixth

policy anniversary until the end of the plan term depending

on the performance of our Company.

TAX BENEFITS, RIDERS AND AGE ELIGIBILITY

Premiums paid under this plan are eligible for tax benefits

under Section 80C of the Income Tax Act, 1961. Any sum

received under this plan is exempt from tax under section

10(10D) of the Income Tax Act, 1961.*

Attach Disability, Accident, Term, Waiver of premium and

Critical Illness riders to this policy for added protection.

Endowment Plan Age Eligibility

10 Years 18 to 65 Years

15 Years 18 to 60 Years

20 Years 18 to 55 Years

25 Years 18 to 50 Years

30 Years 18 to 45 Years

ASSURE GOLDEN YEARS PLAN

Assure Golden Years is an endowment policy that provides both

safety and steady returns. In the unfortunate event of your death,

your dependants will receive the sum assured; otherwise your

savings will continue to grow. Should you live past the term of the

policy, you will receive both the sum assured as well as a host of

bonuses.

Key features include:

A guaranteed addition of 10% of the sum assured if the

policy has been in force for 10 years or more, is payable on

death or maturity.

A reversionary bonus is payable on death or maturity.

A Terminal bonus paid on maturity or death if the policy has

been in force for a minimum 10 years.

Reversionary and Terminal bonuses are non-guaranteed and

are dependent on Company performance.

TATA AIG LIFE NIRBHAY LIFE

Tata AIG Life has a whole new participating plan which will

surprise you continually with its remarkable benefits. Premiums

are payable only for the first 9 years, after which you will

receive all your money and much more!

You can opt for a policy that lasts 12, 15 or 20 years.

During the term of the policy, you will receive 130% of the sum

assured.

Tax Benefits, Additional Benefits and Age Eligibility

Premiums paid under this plan are eligible for tax

benefits under Section 80C of the Income Tax Act, 1961.

Any sum received under this plan is exempt from tax

under section 10(10D) of the Income Tax Act, 1961.*

For insured age of less than 18 years, the Payor benefit is

inbuilt.

For insured age of 18 years and above, waiver of

premium and accidental death benefit are inbuilt.

Anyone in the age group 6 years - 55 years is eligible for

the policy.

FINDINGS

QUESTIONNAIRE ANALYSIS

Q.1. Have you taken life Insurance for you?

Yes No

57% 43%

INFERENCE:

57% of the Respondents had taken the life insurance

However 43% of the Respondents had not taken any policy

Q.2. Who is your Insurer

LIC Private Sector Insurer Both

75% 19% 6%

INFERENCE:

75% of the respondents felt that the lic os best policy

While 19% of respondents thought it was not so good, 6% thought that

both policy are good

Q.3. What made you buy from Private Sector?

Better

Service

Attractive

Plans

Better

Returns

Agent

known

Other

22% 27% 37% 9% 5%

INFERENCE:

22% people said that they buy from private sector because of better

service,27% thought because of attractive plans 37% because of better

returns and 9% because of agent known to them and 5 % of some other

factor

Q.4. Who is your Agent?

Old family agent

for years

Professional Acquaintance/

Someone

referred

Friend/Family

member/relative

Other

17% 27% 12% 42% 2%

INFERENCE:

17% agent are old family agent, 27% are professional,12% are acquaintance,

42% are family and friends while 2% are others

Q.5. How much is the maximum annual income a layman can think of

for an Insurance Agent?

Upto Rs. 5 lacs Rs. 5 to Rs.

10 lacs

Rs. 10 to Rs.

50 lacs

Rs. 50 lacs +

77% 16% 6% 1%

INFERENCE:

77% People think that an insurance agent has 5lacs salary annually, 16%

thinks that it is upto 10 lacs, 6% thinks that it is upto 50 lacs and 1 %

thinks that it is above 5o lacs

Q.6. Given an opportunity, would you like to earn a big and stable

income by being a part of Tata AIG?

Yes No

87% 13%

We

INFERENCE:

87% people said that they will be part of tata aig in future

13% said that they will not be the part of tata aig

RECOMMENDATIONS

RECOMMENDATIONS

More emphasis should be on promotional activities.

Plenty of advertisement should be done through T.V, Newspaper

and Radio as these media’s are having maximum recall value.

Total financial planning and advice should be given to every

customer.

More business opportunity seminars should be conducted to make

people aware of the offer given.

The company should quite frequently send their agent to the

customer so that they should be aware of the latest offer.

The company should attempt to open more and more of its

branches in the country so as to promote their product publicity.

CONCLUSION

After making an in depth study about the Tata AIG Insurance Co., have

come to the conclusion that there has been tremendous changes in the

Insurance History. And with it there has been continuous growth in this

sector both in Indian as well as world context. The opening up of

Insurance Sector has changed the whole look of Insurance Industry.

A joint venture between Tata and AIG has shown a positive progress in

Insurance Industry. Tata AIG has been growing year after year and this

company has made a strong position in India. It has become the number

one company in customer satisfaction.

The game is old but the rules are new and still developing. The same

strategy adopt by Tata AIG. Insurance Agent has a career growth

opportunity in this Insurance Co. as compare to other Insurance Co. An

Insurers advisor of Tata AIG can earn a big and stable income by being a

part of Tata AIG Insurance Company.

LIMITATIONS

Every study has to have limitations in terms of time cost, human error &

so on the best efforts were put in to get information from the company.

During the entire research period witch spanned for 2 months there were

certain constraints faced because of circumstances and capabilities. The

research conducted was under the following constraints :

There are - neck to neck competition between Insurance Companies.

As the project had a time limit of 8 weeks. Getting appointments from

the respondents takes time.

Non participation of the respondents in the research process due to

fear of disclosing the details about the influencers.

Time and distance were another factor that sewed as the limitation

since located in outskirts of Delhi.

The company did not gave any information regarding the finance.

QUESTIONNAIRE

CHANGING PROFILE OF INSURANCE AGENT

A PRACTICAL CASE STUDY

Respondent Details

Name: Date of Birth:

Age:

Address:

Telephone: (Mobile) (off) (Resi)

Marital status: Single / Married Sex: M / F

Education: Undergraduate / Graduate / Post Graduate

Occupation:

Annual Income (Rs.): Up to 1 lakh/1 - 2 lakh/2 - 3 lakh/3 - 5 lakh/5 -

10 lakh/10 lakh +

TICK IN THE APPROPRIATE ANSWERS GIVEN BELOW.

(1) Have you taken Life Insurance for you?

Yes / No

(IF YES MOVE TO SET 1 ; IF NO MOVE TO SET 2)

SET 1

(2) Who is your Insurer?

(a) LIC

(b) Private Sector Insurer

(C) Both

(if the choice is (b) or (c) for question number 2 then answer 3

otherwise move to 4)

(3) What made you buy from private sector?

a) Better service

b) Attractive plans

c) Better returns

d) Agent known

(4) Who is your agent?

(a) Old family agent for years

b) Professional

c) Acquaintance / someone referred

d) Friend / family member / relative

(5) What do you think is expected of an Insurance Agent?

a) Better service

b) Knowledge of product & competition

c) Analysing needs & suggest right product

d) Must be well-known

(Move to set III)

Set - II

(6) What is the reason of your not being Insured?

a) I am too young to have Life Insurance

b) Cannot afford

c) Do not need Insurance - no Dependents

d) No one ever guided me properly

(7) If you think of buying an Insurance policy, what qualities would you

look for in the Agent?

a) Better service

b) Knowledge of product & competition

c) Analyze need & suggest right product

d) Must be well-known

(move to set III)

Set - III

How much is the maximum annual income you can think of for an

Insurance Agent?

a) Up to Rs. 5 lakhs

b) Rs. 5 to 10 lakhs

c) Rs. 10 - 50 lakhs

d) Rs. 50 lakhs +

Prompt: Are you aware that AIG has a large number of insurance

advisor who are making many times more than Rs. 50 lakhs per annum

and in TATA AIG, in India, there are advisor who have started touching

the 50 lakhs figure and are slated to achieve much more than that within

this year.

(8) Are you aware of a large number of successful insurance advisor of

a company growing up the value change and becoming leaders with

stable earning of much more than Rs. 50 lakhs per annum?

Yes / No

Prompt: AIG offers a growth plan to its advisor worldwide and a large

number of such business partner earn more than one million dollars per

annum. Similar plan in India makes the advisor grow into Business

Associate, who recruit, develop and manage large sales team. Successful

Business Associate are earning up to more than Rs. 25 lakhs per annum,

with the income growing rapidly every year. The day of Indian

Millionaires (In US dollar terms) is not far.

(9)Do you think that future lives in service & knowledge sectors?

Yes / No

(10) Do you believe you have the capability to get fresh knowledge and

use it in betterment of the society by analzing their needs & providing

right solutions?

Yes / No

(11) Do you believe you have the capability of successfully leading a

team?

Yes / No

(13) Given an opportunity, would you like to earn a big and stable

income by being a part of Tata AIG?

Yes / No

Prompt: TATA AIG is a joint venture of the well-known, well respected

and the most trusted TATA Group of India & AIG (American

International Group) the biggest insurer in the world by market value.

Present in over 130 countries, AIG has assets of over $ 600 billion &

annual income of over $ 10 billion. AIG ranks among the top in FORBES

& FORTUNE 500 companies & is the only AAA rated company in the

world.

(14) Do you know someone who could be interested in taking up

insurance selling as a career?

Yes / No

(if answer to question number 14 is Yes please take the details on a

separate sheet)

Trainee Name……………………City………………

Institute………………..

Remarks……Very Interested / Interested / Not Interested Follow

UPdate……………..

BIBLIOGRAPHY

WWW.TATAAIGINSURANCE.COM

WWW.TATA.COM

WWW.AIG.COM

WWW.INSURANCE.COM

WWW.GOOGLE.COM

WWW.YAHOO.COM

COMPANY PROVIDED MATERIAL

TEXT BOOK FOR LIFE INSURANCE PRESCRIBED BY IRDA.

TATA AIG BROSHERS

MAGAZINES AND NEWSPAPERS

COMPANY LITERATURE

MARKETING RESEARCH