24

TAX ADMINISTRATION ACT, 2011 By Johan Kotze Head of Tax Dispute Resolution

| Date post: | 27-Dec-2015 |

| Category: |

Documents |

| Upload: | shawn-dorsey |

| View: | 215 times |

| Download: | 0 times |

TAX ADMINISTRATION ACT, 2011

By Johan Kotze

Head of Tax Dispute Resolution

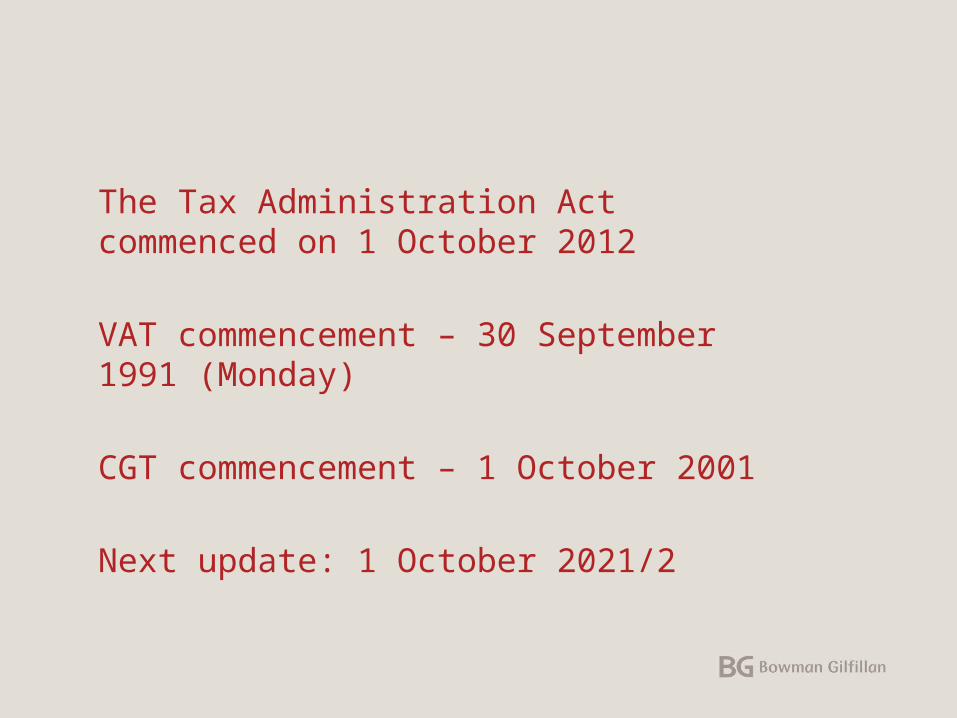

The Tax Administration Act commenced on 1 October 2012

VAT commencement – 30 September 1991 (Monday)

CGT commencement – 1 October 2001

Next update: 1 October 2021/2

Understatement penalty

Voluntary disclosure

Third party appointments

4

UNDERSTATEMENT PENALTY

5

Understatement penalty - general

The current open-ended discretion to impose 200% additional tax, is replaced with a framework to ensure consistent treatment of taxpayers in comparable circumstances.

Different rates of an understatement penalty based on the type of behaviour or degree of culpability involve.

The penalty will be determined by selecting the highest percentage from the table, on a case by case basis.

6

Understatement penalty - table

Item /Behaviour Standard Case

If obstructive,

or repeat case

Voluntary disclosure

after notification

of audit

Voluntary disclosure

before notification

of audit

i. Substantial understatement

25% 50% 5% 0%

ii. Reasonable care not taken in completing return

50% 75% 25% 0%

iii. No reasonable grounds for ‘tax position’ taken

75% 100% 35% 0%

iv. Gross negligence

100% 125% 50% 5%

v. Intentional tax evasion

150% 200% 75% 10%

7

Understatement penalty - Definitions

‘Repeated case’ - a second or further case of any of the behaviours listed under items (i) to (v) of the table within five years of the previous case

‘Substantial Understatement’ - a case where the prejudice to SARS or the fiscus exceeds the greater of 5% of the amount of ‘tax’ properly chargeable or refundable for the relevant tax period, or R1 000 000

8

Understatement penalty - Definitions

‘Understatement’ - any prejudice to SARS or the fiscus in respect of a tax period as a result of:

(a) a default in rendering a return;

(b) an omission from a return;

(c) an incorrect statement in a return; or

(d) if no return is required, the failure to pay the correct amount of ‘tax’.

9

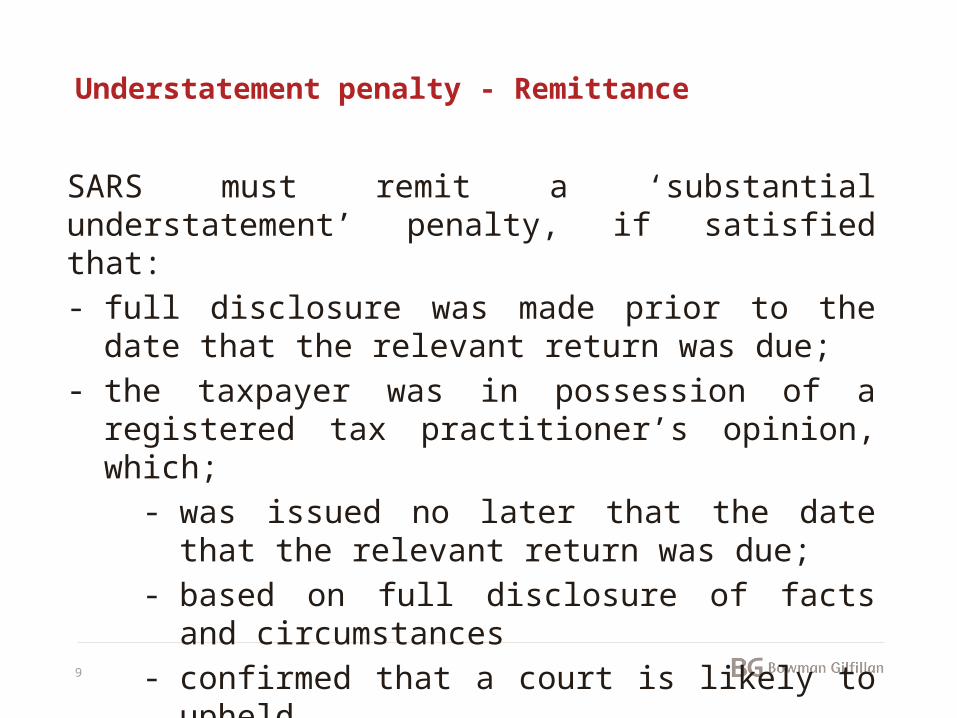

Understatement penalty - Remittance

SARS must remit a ‘substantial understatement’ penalty, if satisfied that:- full disclosure was made prior to the date that the

relevant return was due;- the taxpayer was in possession of a registered tax

practitioner’s opinion, which;- was issued no later that the date that the

relevant return was due;- based on full disclosure of facts and

circumstances- confirmed that a court is likely to upheld

10

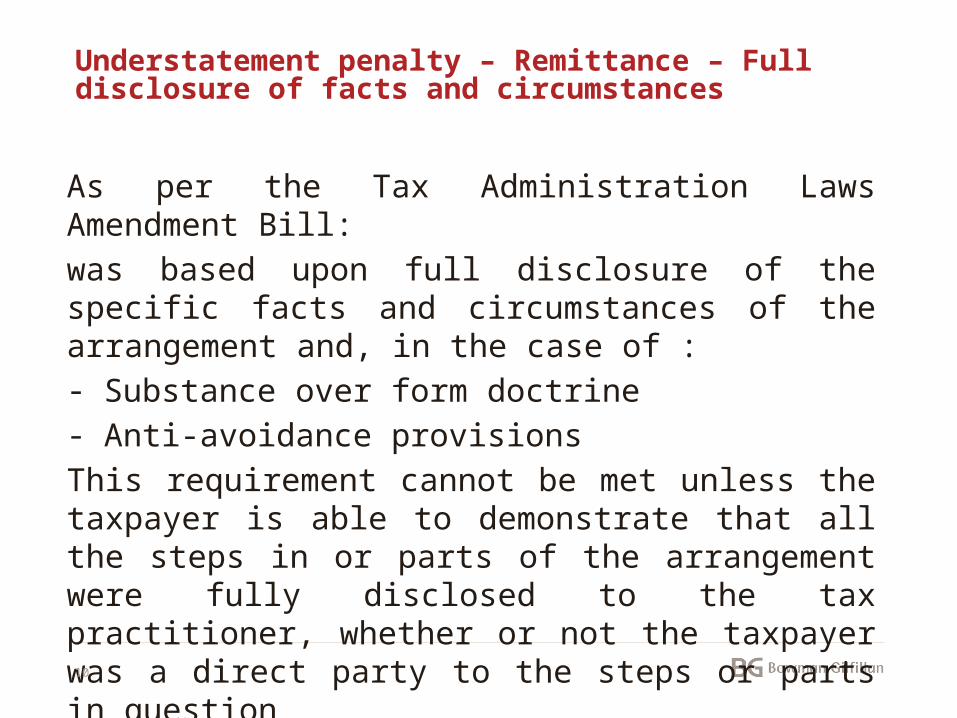

Understatement penalty – Remittance – Full disclosure of facts and circumstances

As per the Tax Administration Laws Amendment Bill:

was based upon full disclosure of the specific facts and circumstances of the arrangement and, in the case of :- Substance over form doctrine- Anti-avoidance provisions

This requirement cannot be met unless the taxpayer is able to demonstrate that all the steps in or parts of the arrangement were fully disclosed to the tax practitioner, whether or not the taxpayer was a direct party to the steps or parts in question

11

Understatement penalty – Remittance, objection & appeal

A decision by SARS not to remit an understatement penalty is subject to:

-objection and -appeal

The same procedures concerning objection, appeal, and alternative dispute resolution apply to the understatement penalty.

12

VOLUNTARY DISCLOSURE PROGRAMME

13

Voluntary Disclosure Programme

An interim voluntary disclosure programme expired in October 2011,

but a permanent legislative framework for voluntary disclosure that applies to all tax types is included in TAAct.

14

Voluntary Disclosure Programme

The provisions to give effect to the VDP:- introduce the concept of voluntary disclosure; - prescribe the relief that may be provided under the

VDP; - state who qualifies to may make a disclosure; and- prescribe when, where and how to apply for the VDP.

15

Voluntary Disclosure Programme – Relief granted to defaulting taxpayer

A defaulting taxpayer will be granted relief under the programme, provided:- the disclosure is complete; - SARS was not aware of the default; and - an administrative non-compliance penalty or

understatement penalty would have been imposed had SARS discovered the default in the normal course of business.

16

Voluntary Disclosure Programme – Extent of relief

No relief: - Interest- exchange control- penalties imposed for the late submission of returns or - for the late payment of tax

A person cannot qualify for VDP relief if this will result in a refund being payable to the person.

17

Voluntary Disclosure Programme – Extent of relief

Permanent relief: - Administrative non-compliance penalty: 100%- Understatement penalty, as determined in the

applicable column in the understatement penalty table- SARS’ criminal prosecution.

18

Voluntary Disclosure Programme – No name basis

A mechanism available to apply for relief on an anonymous basis.

It involves SARS providing a non-binding private opinion on the applicants eligibility.

The application must clearly contain sufficient information to enable an opinion to be formed.

19

THIRD PARTY APPOINTMENT

20

Third party appointments – 179(1)

Senior SARS official

Senior SARS official

- The Commissioner

- SARS official who has specific written authority from the Commissioner

- SARS official occupying a post designated by the Commissioner of this purpose

21

Third party appointments – 179(2)

Unable to comply with requirement:

- must advise the senior SARS official

- with reasons

- within period specified

Thus:

- contact details of senior SARS official

- reasonable timeperiod

22

Third party appointments – 179(3)

Agents personal liability if parting with funds, contrary to the notice,

23

Third party appointments – 179(4)

On request by an affected person,

SARS may amend request to be spread over a period,

To allow for ‘basic living expenses of the taxpayer and his or her dependants’

Thank you

![[VigChr Supp 071] Annemare Kotze Augustines Confessions Communicative Purpose and Audience, 2004.pdf](https://static.documents.pub/doc/80x56/577cc14d1a28aba71192b14b/vigchr-supp-071-annemare-kotze-augustines-confessions-communicative-purpose.jpg)