26

Tax Ethics & Legal Duties MD

Tax Ethics & Legal Duties

MD

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

1

OVERVIEW

A. Code of Professional Ethics of the AICPA

B. AICPA Statements on Standards for Tax Services (SSTS)

C. State Boards of Accountancy regulations

D. Treasury Circular 230

E. Internal Revenue Code penalty provisions

Notes:

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

2

SSTS

A. Statements on Standards for Tax Services (SSTS) Overview

1. Seven statements most recently revised and effective January 1, 2010

2. Interpretations No. 1-1 and 1-2 (interpretations of Statement 1)

B. Number 1, Tax Return Positions

A member should know and comply with any standards related to recommending a tax return position or preparing or signing a tax return that are imposed by the relevant taxing authority. When recommending a tax return position, a member has both the right and responsibility to be an advocate for the taxpayer with respect to any position, insofar as it still satisfies this standard.

1. Probably the most important

2. SSTS and the two proposed interpretations are designed to coordinate withTreasury Circular 230 and IRC §§ 6662 and 6694

C. Number 2, Answers to Questions on Returns

A member should make a reasonable effort to obtain from the taxpayer the information necessary to provide appropriate answers to all questions on a tax return before signing as preparer.

D. Number 3, Certain Procedural Aspects of Preparing Returns

In preparing or signing a return, a member may rely, in good faith and without verification, on information furnished by the taxpayer or by third parties.

E. Number 4, Use of Estimates

Unless prohibited by statute or by rule, a member may use the taxpayer’s estimates in the preparation of a tax return if it is impractical to obtain exact data and if the member determines that the estimates are reasonable based on known facts and circumstances. If estimates are used, they should be presented in a manner that does not imply greater accuracy than exists.

Member=CPA, Lawyer, Enroll agent

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

3

F. Number 5, Departure From a Position Previously Concluded in an Administrative Proceeding or Court Decision

The tax return position with respect to an item as determined in an administrative proceeding or court decision does not restrict a member from recommending a different tax position in a later year’s return, unless the taxpayer is bound to a specified treatment in the later year, such as by a formal closing agreement.

G. Number 6, Knowledge of Error: Return Preparation and Administrative Proceedings

A member should inform the taxpayer promptly upon learning of an error in a previously field return, upon learning of an error in a return that is the subject of an administrative proceeding, or upon learning of a taxpayer’s failure to file a required return.

H. Number 7, From and Content of Advice to Taxpayers

A member should use judgment to ensure that tax advice provided to a taxpayer reflects professional competence and appropriately serves the taxpayer’s needs. A member should use professional judgment about providing oral advice. A member is not required to follow a standard format or guidelines in communicating or documenting written or oral advice to a taxpayer.

Notes: SSTS=Statement on Standards for Tax Services

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

4

TREASURY CIRCULAR 230

A. Overview

1. Applies to all persons “practicing” before the Department of the Treasury,including the IRS

2. Contains both ethical guidelines and disciplinary rules

B. Eligibility to Practice

1. A practitioner can be barred from practice before the IRS, censured and/or fined.Firms also can be sanctioned.

2. Handled by Office of Professional Responsibility (OPR), often with referral tostate disciplinary body

C. Similar to AICPA Rules: Due diligence, client return, confidentiality, disreputable conduct, etc.

D. Requirements to sign tax returns, get PTIN, provide copy to client, and standards for positions taken on tax return.

E. Tax Shelter Opinions: Specific requirements coordinated with provisions of the Internal Revenue Code

Notes: OPR=Office of Professional Responsibility

PTIN=Preparer Tax Identification Number

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

5

POSITIONS ON TAX RETURNS

A. Unrealistic Position: A return preparer may be liable for a penalty imposed by the IRC for signing a return with an unrealistic position that results in understatement of tax.

1. Consistent with Circular 230 and AICPA SSTS No. 1 and Interpretation

2. Similar penalty for taxpayer

B. Positions

1. Substantial authority for position: No requirement to disclose

2. Reasonable basis for position: Disclosure (Form 8275 or 8275-R)

3. More likely than not: For tax shelters and reportable transactions

Filing of Form 8886, Reportable transaction disclosure

C. Reasonable cause/good faith defense of IRC § 6664 available

1. Except for understatement caused by lack of economic substance (common lawdoctrine codified in 2010)

2. Must be competent tax advisor

3. Taxpayer must have disclosed all relevant facts

Notes:

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

6

PREPARER REQUIREMENTS

A. Tax return preparers must obtain a PTIN

1. Pay a fee to the IRS annually

2. Eventually, preparers will have IRS-mandated CPE requirements unless a CPA,attorney, or enrolled agent

B. Beginning in 2011, preparers submitting more than 9 returns must use e-filing.

C. No common law CPA-client privilege as for attorneys

D. Limited statutory privilege under IRC §7525, with exceptions

1. No privilege for tax returns

2. No privilege involving criminal matters

3. No privilege for tax shelter cases

Independently answer multiple-choice questions (MCQ) 1-13 (Questions start on page 16.)

Notes: e-filing

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

7

LEGAL DUTIES TO CLIENTS

A. Contractual Liability

1. Express Duties: Imposed by contract terms

2. Implied Duties: Imposed by common practice

a. Duty to Perform: Contract for personal services may not be delegated

(1) Liable for the wrongful acts of subordinates committed in the course of their employment.

(2) Still liable if a member of a professional limited liability company (PLLC) or PLLP

b. Failure to Fulfill Contract Terms

(1) Substantial Failure (Material Breach): No real benefit from accountant’s performance

(2) Minor Inaccuracies (Immaterial Breach): Compensated for service, but fee may be reduced.

c. Professional Standards: Comply with standards of competence and care.

d. Discovery of Fraud: Generally, no duty to discover fraud

(1) Only if contract expressly includes a duty to discover fraud

(2) Unless accountant’s own negligence prevents discovery of fraud

e. No liability if non-performance caused by client’s interference.

3. Breach

a. May be subject to liability for damages and losses as a result of breach

b. Generally, no punitive damages for simple breach

Audit, Review

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

8

B. Negligence: Failure to exercise degree of care that reasonable person would exercise under similar circumstances

1. Degree of quality, accuracy, and completeness demonstrated by averageaccountant when performing with reasonable care.

2. Honest inaccuracies and judgmental errors do not equal negligence if accountantused reasonable care. Regardless, negligence may be based on unintentionalerrors, intent unnecessary.

3. Contributory Negligence: Liability reduced or eliminated by client’s own negligence

4. Damages: Based on loss that would have been avoided with reasonable care

Notes: Breach

Negligence---Failure to exercise degree of care

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

9

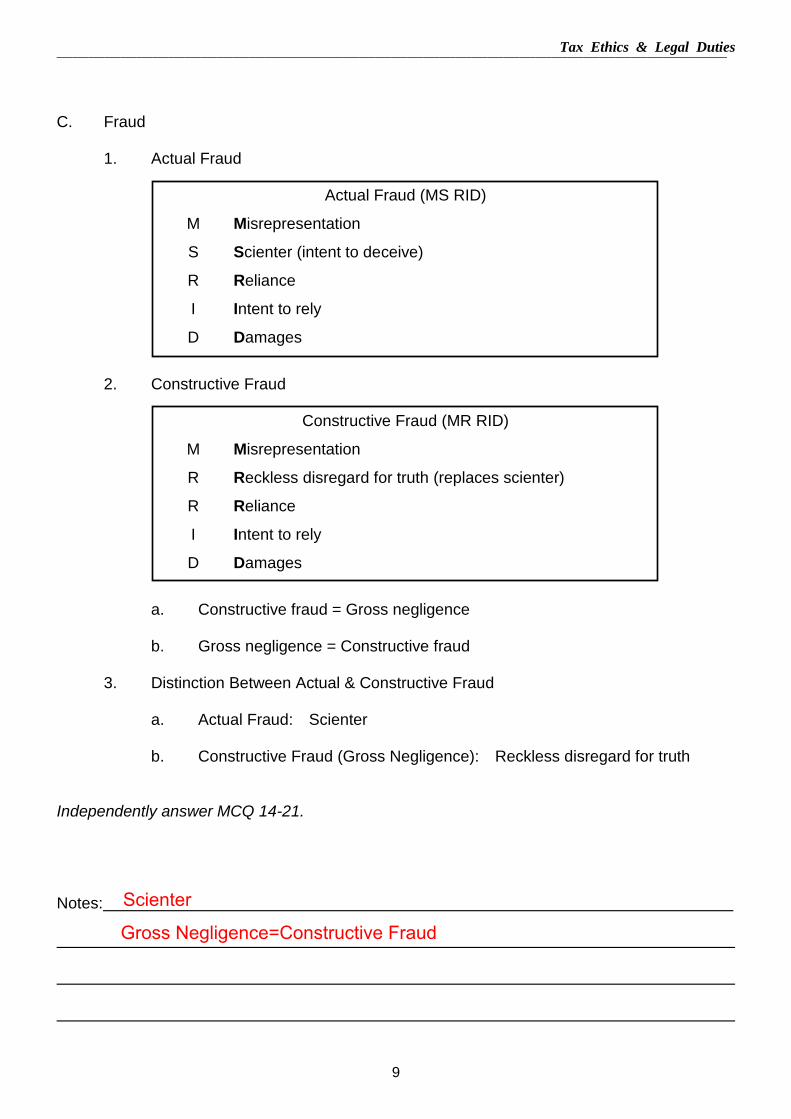

C. Fraud

1. Actual Fraud

Actual Fraud (MS RID)

M Misrepresentation

S Scienter (intent to deceive)

R Reliance

I Intent to rely

D Damages

2. Constructive Fraud

Constructive Fraud (MR RID)

M Misrepresentation

R Reckless disregard for truth (replaces scienter)

R Reliance

I Intent to rely

D Damages

a. Constructive fraud = Gross negligence

b. Gross negligence = Constructive fraud

3. Distinction Between Actual & Constructive Fraud

a. Actual Fraud: Scienter

b. Constructive Fraud (Gross Negligence): Reckless disregard for truth

Independently answer MCQ 14-21.

Notes: Scienter

Gross Negligence=Constructive Fraud

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

10

COMMON LAW & THIRD PARTIES

A. Negligence: Accountant knew (or should have known) third parties would be users of his or her work product.

1. Privity: Relationship between contracting parties

2. Ultramares case: Specific identity known

B. Fraud: Duty to all third parties to make reports without either actual or constructive fraud

1. Third party must show reliance

2. No need to show Privity in case of fraud or gross negligence

Notes: Privity

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

11

FEDERAL LAW

A. Securities Act of 1933 (initial offering)

1. Section 11 liability for false statements in registration or prospectus

2. Due Diligence Defense: CPA must show due diligence at

a. Filing date

b. Effective date

3. Statute of limitations: One year from date error was (or should have been)discovered

B. Securities & Exchange Act of 1934 (subsequent trading)

1. Section 10(b)(5): Liability for false or misleading statements of a material fact insubsequent reports

2. Investor

a. Must prove scienter

b. Must prove reliance

3. No liability for negligence

4. Good Faith Defense: CPA acted in good faith

C. Private Securities Litigation Reform Act of 1995

1. Auditor must have procedures to detect fraud

2. Auditor must report and further investigate suspected fraud

D. Sarbanes-Oxley Act

1. Established PCAOB to oversee auditors

2. Established auditor independence rules

3. Requires audit committee to oversee auditor’s work

Notes:

One business day

1933-Section11

1934-Section 10(b)(5)

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

12

ACCOUNTANTS’ RESPONSIBILITIES

A. Duty of Non-Disclosure

1. Work papers belong to accountant, not client, but custodial arrangement

2. Generally confidential, but no legal privilege

a. Tax advice (not criminal activity, returns, or tax shelters)

b. Attorney Work Product: CPA retained by attorney

3. Exceptions to Non-Disclosure

a. Quality control panel (AICPA or PCAOB)

b. Subpoena: Unless state recognizes accountant-client privilege

c. Client waiver

B. Potential Liability Situations

1. Audits and attest engagements

2. Unaudited financial statements

3. Securities acts

4. Tax law

5. State law

6. Other

Independently answer MCQs 22-41.

Notes: Work papers---Accountant

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

13

TAX LEGISLATIVE PROCESS

A. Background

1. First income tax 1913

2. Internal Revenue Code

a. Fundamental codification (1939); complete revision (1954); comprehensiverewrite (1986)

b. Constant revisions, a number of tax enactments each year

3. Code supplemented by IRS regulations, other administrative guidance, and finallythe courts.

B. Congress

1. House (Ways and Means Committee & floor) must initiate all revenue measures

2. Senate Finance Committee & Floor

3. Conference Committee

4. Joint Committee on Taxation: Note committee reports and Blue Book forlegislative intent

C. Timing

1. Effective date of legislation

Stated date or date of enactment

2. Expired provisions and “extenders”

3. Revenue estimates and budget process

4. Many state tax systems “piggyback” on IRC, but recent efforts to “decouple,” i.e.,bonus depreciation

Notes:

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

14

TAX PLANNING

A. Continuous Process

1. Current law vs. prospective changes

2. Time value of money concepts

3. Basic Strategy

a. Defer income and accelerate expenses

b. If AMT might apply, reverse the strategy

4. Also must consider state tax implications

B. Strategies

1. Elections: Expense vs. capitalization

2. Use of net operating loss, capital loss, and credit carryovers

3. Estimated taxes

4. Passive income/passive losses

5. Changing tax rates and phase-out ranges

6. Switching entities (conversions, etc.)

7. Impact of audit adjustments on both federal and state returns

C. Avoid tax shelters

D. Ultimately consider tax implications in decision-making, but don’t let the tax tail wag the financial dog.

Notes:

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

15

RECAP

A. Ethics in Tax Practice (SSTS, IRC & Circular 230)

1. Positions taken on tax returns

a. No Disclosure: Substantial authority

b. Disclosure: Reasonable basis

c. Tax Shelter: More likely than not

2. Confidentiality & due diligence

B. Responsibilities to Clients

1. Negligence

a. Privity

b. Reliance

2. Actual Fraud (MS. RID)

3. Constructive Fraud (MR. RID)

C. Responsibilities to Third Parties

1. Common Law

2. Federal Law

a. Securities Act of 1933

b. Securities & Exchange Act of 1934

D. Tax Legislative Process & Planning

Notes:

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

16

MULTIPLE-CHOICE QUESTIONS

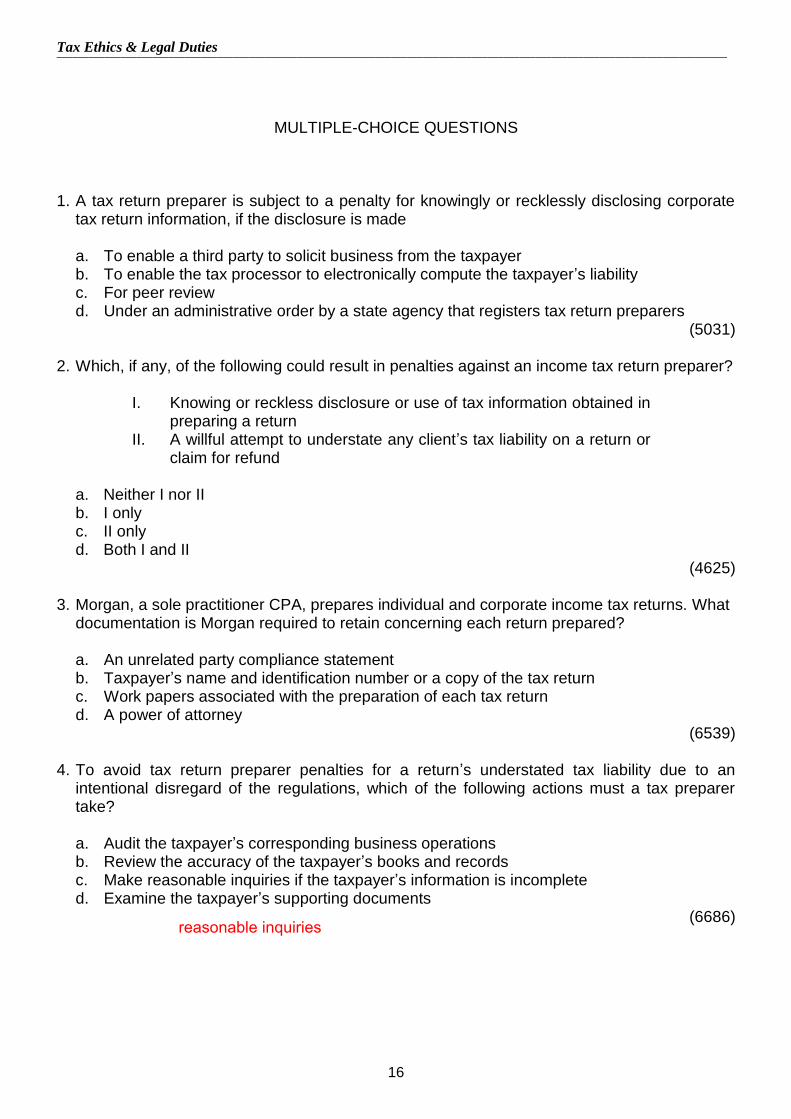

1. A tax return preparer is subject to a penalty for knowingly or recklessly disclosing corporatetax return information, if the disclosure is made

a. To enable a third party to solicit business from the taxpayerb. To enable the tax processor to electronically compute the taxpayer’s liabilityc. For peer reviewd. Under an administrative order by a state agency that registers tax return preparers

(5031)

2. Which, if any, of the following could result in penalties against an income tax return preparer?

I. Knowing or reckless disclosure or use of tax information obtained in preparing a return

II. A willful attempt to understate any client’s tax liability on a return orclaim for refund

a. Neither I nor IIb. I onlyc. II onlyd. Both I and II

(4625)

3. Morgan, a sole practitioner CPA, prepares individual and corporate income tax returns. Whatdocumentation is Morgan required to retain concerning each return prepared?

a. An unrelated party compliance statementb. Taxpayer’s name and identification number or a copy of the tax returnc. Work papers associated with the preparation of each tax returnd. A power of attorney

(6539)

4. To avoid tax return preparer penalties for a return’s understated tax liability due to anintentional disregard of the regulations, which of the following actions must a tax preparertake?

a. Audit the taxpayer’s corresponding business operationsb. Review the accuracy of the taxpayer’s books and recordsc. Make reasonable inquiries if the taxpayer’s information is incompleted. Examine the taxpayer’s supporting documents

(6686) reasonable inquiries

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

17

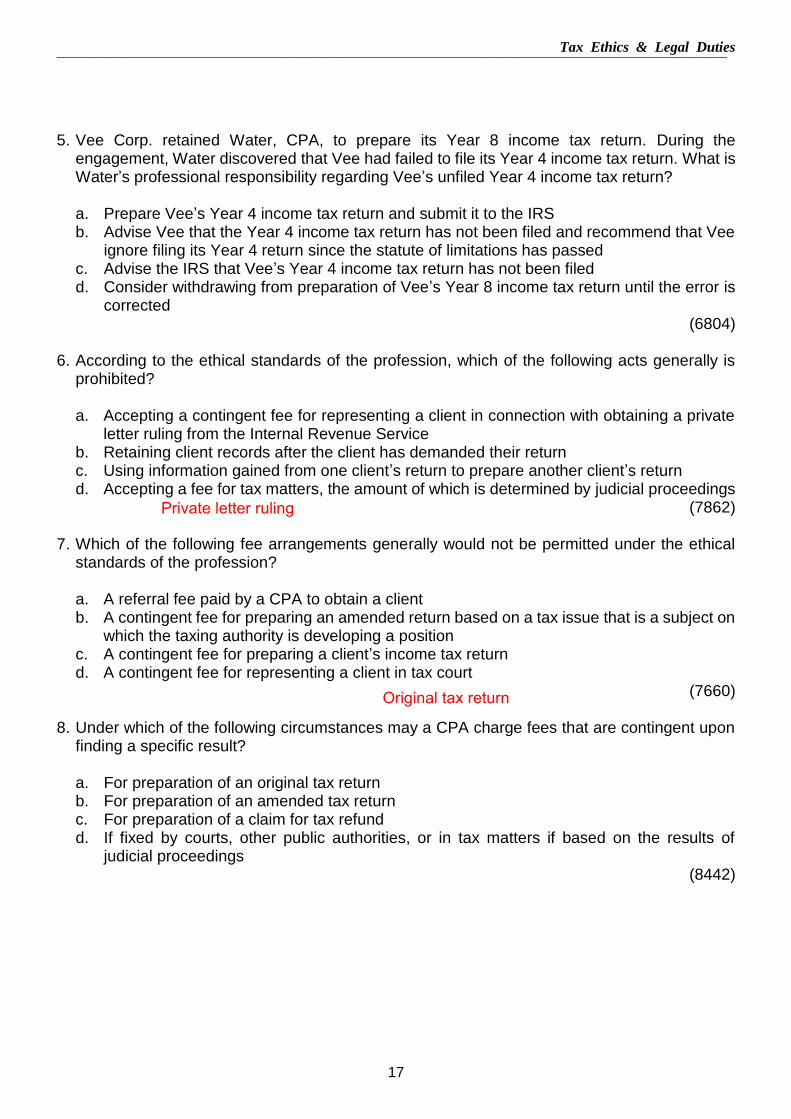

5. Vee Corp. retained Water, CPA, to prepare its Year 8 income tax return. During theengagement, Water discovered that Vee had failed to file its Year 4 income tax return. What isWater’s professional responsibility regarding Vee’s unfiled Year 4 income tax return?

a. Prepare Vee’s Year 4 income tax return and submit it to the IRSb. Advise Vee that the Year 4 income tax return has not been filed and recommend that Vee

ignore filing its Year 4 return since the statute of limitations has passedc. Advise the IRS that Vee’s Year 4 income tax return has not been filedd. Consider withdrawing from preparation of Vee’s Year 8 income tax return until the error is

corrected(6804)

6. According to the ethical standards of the profession, which of the following acts generally isprohibited?

a. Accepting a contingent fee for representing a client in connection with obtaining a privateletter ruling from the Internal Revenue Service

b. Retaining client records after the client has demanded their returnc. Using information gained from one client’s return to prepare another client’s returnd. Accepting a fee for tax matters, the amount of which is determined by judicial proceedings

(7862)

7. Which of the following fee arrangements generally would not be permitted under the ethicalstandards of the profession?

a. A referral fee paid by a CPA to obtain a clientb. A contingent fee for preparing an amended return based on a tax issue that is a subject on

which the taxing authority is developing a positionc. A contingent fee for preparing a client’s income tax returnd. A contingent fee for representing a client in tax court

(7660)

8. Under which of the following circumstances may a CPA charge fees that are contingent uponfinding a specific result?

a. For preparation of an original tax returnb. For preparation of an amended tax returnc. For preparation of a claim for tax refundd. If fixed by courts, other public authorities, or in tax matters if based on the results of

judicial proceedings(8442)

Private letter ruling

Original tax return

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

18

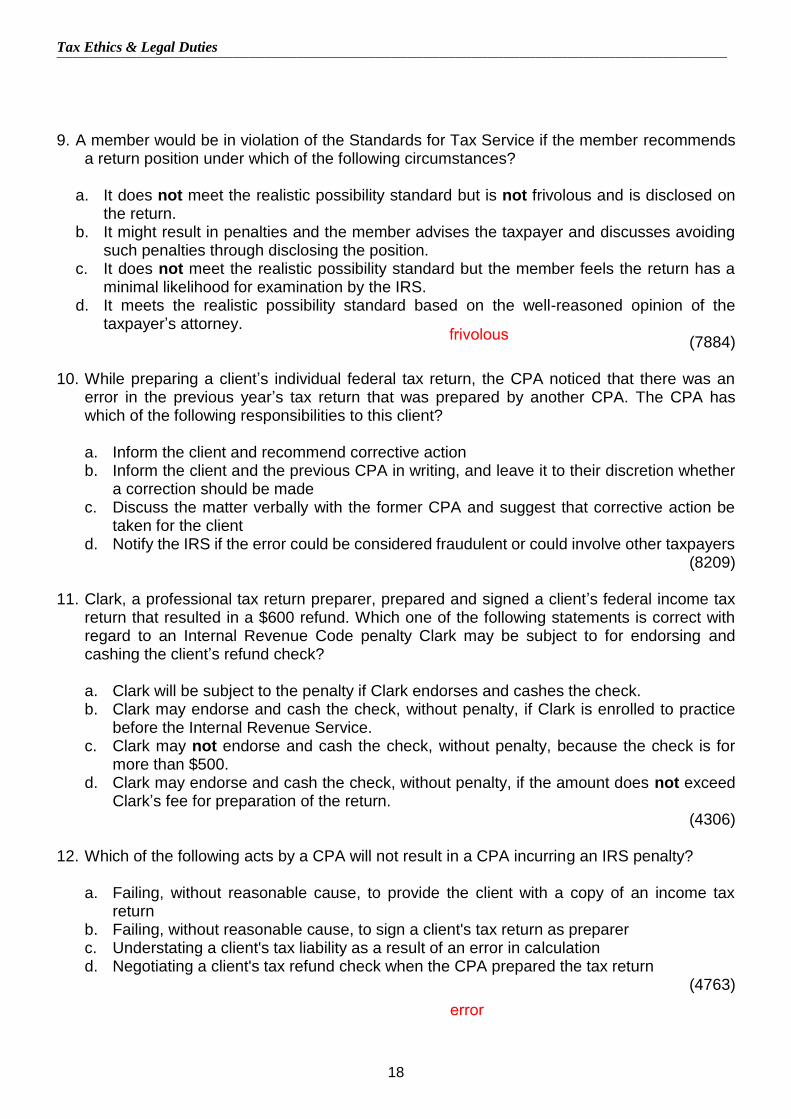

9. A member would be in violation of the Standards for Tax Service if the member recommendsa return position under which of the following circumstances?

a. It does not meet the realistic possibility standard but is not frivolous and is disclosed onthe return.

b. It might result in penalties and the member advises the taxpayer and discusses avoidingsuch penalties through disclosing the position.

c. It does not meet the realistic possibility standard but the member feels the return has aminimal likelihood for examination by the IRS.

d. It meets the realistic possibility standard based on the well-reasoned opinion of thetaxpayer’s attorney.

(7884)

10. While preparing a client’s individual federal tax return, the CPA noticed that there was anerror in the previous year’s tax return that was prepared by another CPA. The CPA haswhich of the following responsibilities to this client?

a. Inform the client and recommend corrective actionb. Inform the client and the previous CPA in writing, and leave it to their discretion whether

a correction should be madec. Discuss the matter verbally with the former CPA and suggest that corrective action be

taken for the clientd. Notify the IRS if the error could be considered fraudulent or could involve other taxpayers

(8209)

11. Clark, a professional tax return preparer, prepared and signed a client’s federal income taxreturn that resulted in a $600 refund. Which one of the following statements is correct withregard to an Internal Revenue Code penalty Clark may be subject to for endorsing andcashing the client’s refund check?

a. Clark will be subject to the penalty if Clark endorses and cashes the check.b. Clark may endorse and cash the check, without penalty, if Clark is enrolled to practice

before the Internal Revenue Service.c. Clark may not endorse and cash the check, without penalty, because the check is for

more than $500.d. Clark may endorse and cash the check, without penalty, if the amount does not exceed

Clark’s fee for preparation of the return.(4306)

12. Which of the following acts by a CPA will not result in a CPA incurring an IRS penalty?

a. Failing, without reasonable cause, to provide the client with a copy of an income taxreturn

b. Failing, without reasonable cause, to sign a client's tax return as preparerc. Understating a client's tax liability as a result of an error in calculationd. Negotiating a client's tax refund check when the CPA prepared the tax return

(4763)

frivolous

error

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

19

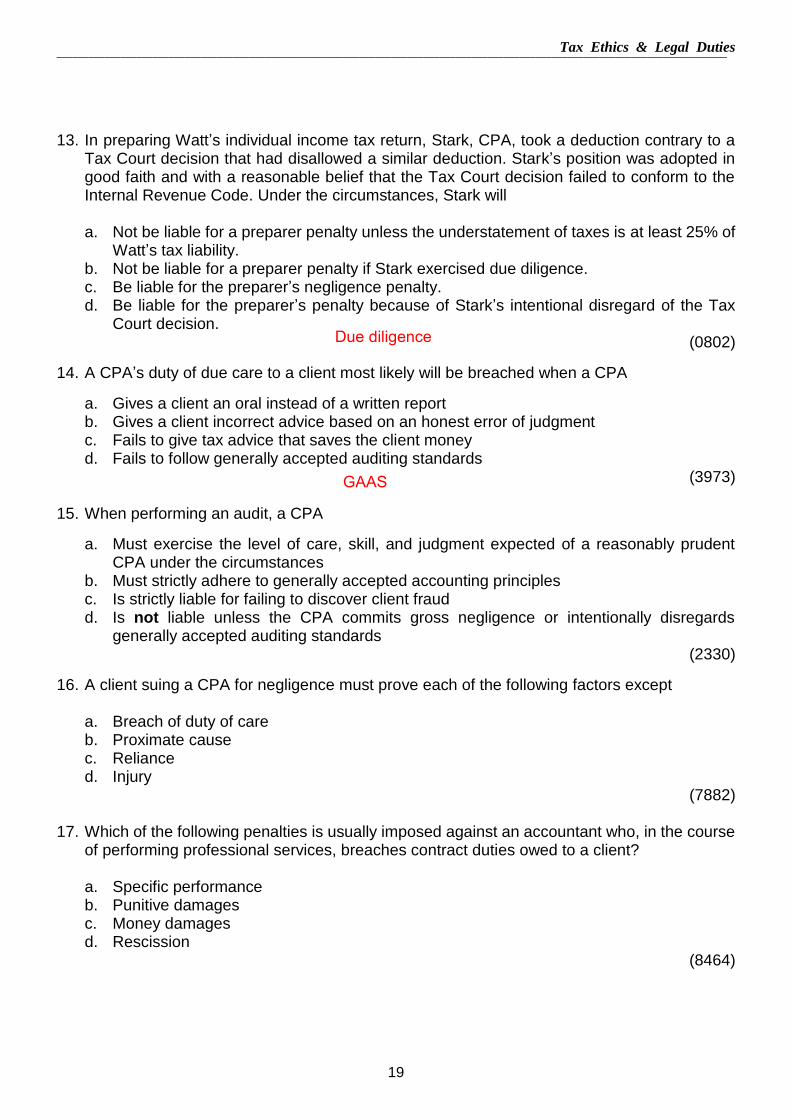

13. In preparing Watt’s individual income tax return, Stark, CPA, took a deduction contrary to aTax Court decision that had disallowed a similar deduction. Stark’s position was adopted ingood faith and with a reasonable belief that the Tax Court decision failed to conform to theInternal Revenue Code. Under the circumstances, Stark will

a. Not be liable for a preparer penalty unless the understatement of taxes is at least 25% ofWatt’s tax liability.

b. Not be liable for a preparer penalty if Stark exercised due diligence.c. Be liable for the preparer’s negligence penalty.d. Be liable for the preparer’s penalty because of Stark’s intentional disregard of the Tax

Court decision.(0802)

14. A CPA’s duty of due care to a client most likely will be breached when a CPA

a. Gives a client an oral instead of a written reportb. Gives a client incorrect advice based on an honest error of judgmentc. Fails to give tax advice that saves the client moneyd. Fails to follow generally accepted auditing standards

(3973)

15. When performing an audit, a CPA

a. Must exercise the level of care, skill, and judgment expected of a reasonably prudentCPA under the circumstances

b. Must strictly adhere to generally accepted accounting principlesc. Is strictly liable for failing to discover client fraudd. Is not liable unless the CPA commits gross negligence or intentionally disregards

generally accepted auditing standards(2330)

16. A client suing a CPA for negligence must prove each of the following factors except

a. Breach of duty of careb. Proximate causec. Relianced. Injury

(7882)

17. Which of the following penalties is usually imposed against an accountant who, in the courseof performing professional services, breaches contract duties owed to a client?

a. Specific performanceb. Punitive damagesc. Money damagesd. Rescission

(8464)

Due diligence

GAAS

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

20

18. Which of the following statements is(are) correct regarding the common law elements thatmust be proven to support a finding of constructive fraud against a CPA?

I. The plaintiff has justifiably relied on the CPA’s misrepresentation. II. The CPA has acted in a grossly negligent manner.

a. I onlyb. II onlyc. Both I and IId. Neither I nor II

(6853)

19. When CPAs fail in their duty to carry out their contracts for services, liability to clients may bebased on

Breach of contract Strict liability

a. Yes Yes b. Yes No c. No No d. No Yes

(0791)

20. Sun Corp. approved a merger plan with Cord Corp. One of the determining factors inapproving the merger was the financial statements of Cord that were audited by Frank & Co.,CPAs. Sun had engaged Frank to audit Cord's financial statements. While performing theaudit, Frank failed to discover certain irregularities that later caused Sun to suffer substantiallosses. For Frank to be liable under common law negligence, Sun at a minimum must provethat Frank

a. Knew of the irregularitiesb. Failed to exercise due carec. Was grossly negligentd. Acted with scienter

(3970)

21. Which of the following statements best describes whether a CPA has met the requiredstandard of care in conducting an audit of a client’s financial statements?

a. The client’s expectations with regard to the accuracy of audited financial statementsb. The accuracy of the financial statements and whether the statements conform to

generally accepted accounting principlesc. Whether the CPA conducted the audit with the same skill and care expected of an

ordinarily prudent CPA under the circumstancesd. Whether the audit was conducted to investigate and discover all acts of fraud

(4299)

Gross Negligence = Constructive Fraud

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

21

22. Which of the following statements is generally correct regarding the liability of a CPA whonegligently gives an opinion on an audit of a client's financial statements?

a. The CPA is only liable to those third parties who are in privity of contract with the CPA.b. The CPA is only liable to the client.c. The CPA is liable to anyone in a class of third parties who the CPA knows will rely on the

opinion.d. The CPA is liable to all possible foreseeable users of the CPA's opinion.

(6442)

23. Which of the following facts must be proven for a plaintiff to prevail in a common lawnegligent misrepresentation action?

a. The defendant made the misrepresentations with a reckless disregard for the truth.b. The plaintiff justifiably relied on the misrepresentations.c. The misrepresentations were in writing.d. The misrepresentations concerned opinion.

(5350)

24. If a CPA recklessly departs from the standards of due care when conducting an audit, theCPA will be liable to third parties who are unknown to the CPA based on

a. Negligenceb. Gross negligencec. Strict liabilityd. Criminal deceit

(4764)

25. Which of the following is the best defense a CPA firm can assert in a suit for common lawfraud based on its unqualified opinion on materially false financial statements?

a. Contributory negligence on the part of the clientb. A disclaimer contained in the engagement letterc. Lack of privityd. Lack of scienter

(5879)

Privity, all

Scienter

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

22

Items 26 and 27 are based on the following:

While conducting an audit, Larson Associates, CPAs, failed to detect material misstatements included in its client’s financial statements. Larson’s unqualified opinion was included with the financial statements in a registration statement and prospectus for a public offering of securities made by the client. Larson knew that its opinion and the financial statements would be used for this purpose.

26. In a suit by a purchaser against Larson for common law negligence, Larson’s best defensewould be that the

a. Audit was conducted in accordance with generally accepted auditing standards.b. Client was aware of the misstatements.c. Purchaser was not in privity of contract with Larson.d. Identity of the purchaser was not known to Larson at the time of the audit.

(4301)

27. In a suit by a purchaser against Larson for common law fraud, Larson’s best defense wouldbe that

a. Larson did not have actual or constructive knowledge of the misstatements.b. Larson’s client knew or should have known of the misstatements.c. Larson did not have actual knowledge that the purchaser was an intended beneficiary of

the audit.d. Larson was not in privity of contract with its client.

(4302)

28. Beckler & Associates, CPAs, audited and gave an unqualified opinion on the financialstatements of Queen Co. The financial statements contained misstatements that resulted ina material overstatement of Queen's net worth. Queen provided the audited financialstatements to Mac Bank in connection with a loan made by Mac to Queen. Beckler knew thatthe financial statements would be provided to Mac. Queen defaulted on the loan. Mac suedBeckler to recover for its losses associated with Queen's default. Which of the following mustMac prove in order to recover?

I. Beckler was negligent in conducting the audit. II. Mac relied on the financial statements.

a. I onlyb. II onlyc. Both I and IId. Neither I nor II

(4298)

GAAS

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

23

29. Under the liability provisions of Section 11 of the Securities Act of 1933, a CPA may be liableto any purchaser of a security for certifying materially misstated financial statements that areincluded in the security’s registration statement. Under Section 11, which of the followingmust be proven by a purchaser of the security?

Reliance on the financial statements Fraud by the CPA

a. Yes Yes b. Yes No c. No Yes d. No No

(5191)

30. Under the liability provisions of Section 11 of the Securities Act of 1933, an auditor may helpto establish the defense of due diligence if

I. The auditor performed an additional review of the audited statements to ensure that the statements were accurate as of the effective date of a registration statement.

II. The auditor complied with GAAS.

a. I onlyb. II onlyc. Both I and IId. Neither I nor II

(6854)

31. Under the liability provisions of Section 11 of the Securities Act of 1933, which of thefollowing must a plaintiff prove to hold a CPA liable?

I. The misstatements contained in the financial statements certified by the CPA were material.

II. The plaintiff relied on the CPA’s unqualified opinion.

a. I onlyb. II onlyc. Both I and IId. Neither I nor II

(6966)

32. Which of the following circumstances is a defense to an accountant's liability under Section11 of the Securities Act of 1933 for misstatements and omissions of material facts containedin a registration statement?

a. The absence of scienter on the part of the accountantb. The absence of privity between purchasers and the accountantc. Due diligence on the part of the accountantd. Nonreliance by purchasers on the misstatements

(8438)

GAAS

Due diligence

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

24

33. Under Section 11 of the Securities Act of 1933, which of the following standards may a CPAuse as a defense?

Generally accepted accounting principles

Generally accepted fraud detection standards

a. Yes Yes b. Yes No c. No Yes d. No No

(5881)

34. Spinner, CPA, had audited Lasco Corp.'s financial statements for the past several years.Prior to the current-year's engagement, a disagreement arose that caused Lasco to changeauditing firms. Lasco has demanded that Spinner provide Lasco with Spinner's workingpapers so that Lasco may show them to prospective auditors to help them prepare their bidsfor Lasco's audit engagement. Spinner refused and Lasco commenced litigation. Under theethical standards of the profession, will Spinner be successful in refusing to turn over theworking papers?

a. Yes, because Spinner is the owner of the working papers.b. Yes, because Lasco is required to direct prospective auditors to contact Spinner to make

arrangements to view the working papers in Spinner's office.c. No, because Lasco has a legitimate business reason for demanding that Spinner

surrender the working papers.d. No, because it was Lasco's financial statements that were audited.

(8878)

35. Which of the following acts by a CPA is a violation of professional standards regarding theconfidentiality of client information?

a. Releasing copies of tax returns to a local bank with the approval of the client’s mail clerkb. Allowing a review of professional practice without client authorizationc. Responding to an enforceable subpoenad. Faxing a tax return to a loan officer at the request of the client

(8675)

36. Page, CPA, has T Corp. and W Corp. as audit clients. T Corp. is a significant supplier of rawmaterials to W Corp. Page also prepares individual tax returns for Time, the owner of T Corp.and West, the owner of W Corp. When preparing West's return, Page finds information thatraises going-concern issues with respect to W Corp. May Page disclose this information toTime?

a. Yes, because Page has a fiduciary relationship with Timeb. Yes, because there is no accountant-client privilege between Page and Westc. No, because the information is confidential and may not be disclosed without West's

consentd. No, because the information should only be disclosed in Page's audit report on W Corp.'s

financial statements(8193)

GAAP

Tax Ethics & Legal Duties

̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄ ̄

25

37. Which of the following statements is correct with respect to ownership, possession, oraccess to a CPA firm’s audit working papers?

a. Working papers may never be obtained by third parties unless the client consents.b. Working papers are not transferable to a purchaser of a CPA practice unless the client

consents.c. Working papers are subject to the privileged communication rule which, in most

jurisdictions, prevents any third-party access to the working papers.d. Working papers are the client’s exclusive property.

(4765)

38. To which of the following parties may a CPA partnership provide its working papers withouteither the client's consent or a lawful subpoena?

The IRS The FASB

a. Yes Yes b. Yes No c. No Yes d. No No

(6967)

39. Which of the following statements is correct regarding a CPA’s working papers? The workingpapers must be

a. Transferred to another accountant purchasing the CPA’s practice even if the client hasn’tgiven permission.

b. Transferred permanently to the client if demanded.c. Turned over to any government agency that requests them.d. Turned over pursuant to a valid federal court subpoena.

(5883)

40. At a confidential meeting, an audit client informed a CPA about the client's illegalinsider-trading actions. A year later, the CPA was subpoenaed to appear in federal court totestify in a criminal trial against the client. The CPA was asked to testify to the meetingbetween the CPA and the client. After receiving immunity, the CPA should do which of thefollowing?

a. Take the Fifth Amendment and not discuss the meetingb. Site the privileged communications aspect of being a CPAc. Discuss the entire conversation including the illegal actsd. Discuss only the items that have a direct connection to those items the CPA worked on

for the client in the past(8189)

41. Which of the following statements concerning an accountant’s disclosure of confidentialclient data is generally correct?

a. Disclosure may be made to any state agency without subpoena.b. Disclosure may be made to any party on consent of the client.c. Disclosure may be made to comply with an IRS audit request.d. Disclosure may be made to comply with generally accepted accounting principles.

(5192)

Subpoena

Fifth Amendment