38

Tax Information Reporting Overview Riley Stroik & Mike Weisenbeck, Convey November 19, 2014

| Date post: | 08-Sep-2018 |

| Category: |

Documents |

| Upload: | nguyenthien |

| View: | 215 times |

| Download: | 0 times |

Tax Information Reporting

Overview

Riley Stroik & Mike Weisenbeck, Convey November 19, 2014

About Convey

• Convey is the industry leader in providing flexible, on-

demand tax information reporting and withholding

management solutions, leveraging a unique

application of technology and proven experience

• Nearly 30 years experience

• We serve almost half of the Fortune 500

“I would absolutely recommend

Convey to others.”

Associate Director of Tax, Sun

Life Financial

This is not legal advice

Agenda

• Welcome

• Tax Information Reporting – Specific Forms:

• 1099

• 1042-S

• W-9

• W-8

• B-Notice

• ACA Reporting

Tax Information Reporting

• Tax Gap

– The amount of tax liability faced by

taxpayers that is not paid

– Any ideas of the latest tax gap numbers?

Tax Gap

$450,000,000,000

Now what?

• Increase Revenue Without Increasing Taxes

• How? – New Information Reporting

• Closing The Gap

– Increasing Penalties

– Less Abatement

– States Following Suit

Why this is problematic

Your business

Improve service

Reduce/manage risk

Optimize cost structure

Improve margin

Regulatory requirements

Federal, state, local reporting

Regulatory updates

Withholding

Taxpayer identity verification

1099’S

Increase in 1099s & Penalties

New York Auto Body Reporting

3921/3922

6041

6050W

FATCA

Time of Filing Penalty Maximum 30 days or less $30 $250,000 Before August 1st $60 $500,000 After August 1st $100 $1,500,000

Intentional Disregard $250 No Limitation

More Forms, More Penalties, More Money.

Recent Examples:

• 1098T and 5498 added

to P-Notice

• 1099K

What’s new with 1099’s • More Federal forms with State withholding

– 1099K now requires backup withholding, requiring state reporting

• More states requiring direct reporting

• Combined Federal State (CFS) continues to grow

• EINs for recipients on recipient statements can be truncated. • Not EINs for Payors or for any statements that are sent to

the IRS.

1042-S

1042-S

• Required when a payment of U.S. source income is made to a non-U.S. person – Common types include:

• Payments to vendors for services

• Payments to board members

• Payments to related legal entities

• Payments to shareholders – e.g., dividends

• Payments to debt holders – e.g., interest

1042-S

• If your organization makes payments of

U.S. source income to non-U.S. persons,

you must complete both Form 1042-S and

Form 1042 filing requirement

– A form 1042 is required whenever a form

1042-S is issued

1042-S Updates • 1042 & 1042-S updated

for 2014

W-9

W-9 • This form is used to provide your correct TIN to

the person who is required to file and information return with the IRS to report – Income paid to you

– Real estate transactions

– Mortgage interest you paid

– Acquisition or abandonment of secured property

– Cancelation of debt

– Contributions you made to an IRA

W-9 (Draft) • Changes are only

instructional – Box Numbers

were added

– Designed to assist the requestor and the recipient to correctly fill out the form

W-8

W-8

• Filled out by foreign entities (citizens and

corporations) in order to claim exempt

status from certain tax withholdings.

– Used to declare an entity’s status as non-

resident alien or foreign national who works

outside the United States

W-8 • There are many different types of W-8 forms

– Typically requested by withholding agents (firms or brokers) and not the IRS

• W-8BEN – lower withholdings from dividends from foreign nationals

• W-8ECI – used by foreign entities to certify that all income on the form is associated with trade or business within the U.S.

• W-8EXP – filled out by foreign governments, international organizations, banks of issue, tax-exempt organizations, private foundations and governments of US possessions.

• W-8IMY – filled out by foreign financial intermediaries

• W-8CE – used to certify that a tax payer is “covered expatriate” and subject to special tax rules

“B” NOTICE

What is a “B” Notice • Backup Withholding Notice due to Missing or Incorrect

Name/TINs

• Form Types Include: • 1099-B

• 1099-Div

• 1099-Int

• 1099-Misc

• 1099-OID

• W-2G

• 1099-K *Changes for TY 14

• CP2100 or CP2100A

• Based on Prior Year Transmittal(s)

What do I have to do? • Search for any accounts that have the same

name/TIN combination • For Matches

• For Non Matches • No Solicitation Required

15 business days to send “B” Notice solicitation

15 business days to respond

If you fail to gather correct information, you must begin back-

up withholding! You should withhold immediately for missing

TINs

First or Second “B” Notice?

• IRS Does Not Track This For You!

• “Two-in-three year” rule

• First “B” Notice if:

• An account identified on one “B” Notice

• An account identified on two “B” Notices outside of three calendar

years

• Second “B” Notice if:

• An account identified on two “B” Notices within three calendar year

• Penalty: $100 fine per non-compliant record. As of 2011, the maximum penalty any organization

will have to pay is $1.5 million.

First B Notice

Second B Notice

TY 2014 Changes for 2nd “B” Notice

• Changes to the Validation for 2nd B Notices

– SSN print outs no longer valid for 2nd B Notice

• Copy of the SSN card

• Current Procedure

– Collect W9 (required) for 1st B notice

– 2nd B notice a W9 TIN certification NOT enough

Notice of Proposed Penalty

• What is Penalized? – Records filed with a missing/incorrect TIN

– Late returns

– Bad format (wrong media)

• Penalties: Time of Filing Penalty Maximum

30 days or less $30 $250,000

Before August 1st $60 $500,000

After August 1st $100 $1,500,000

Intentional Disregard $250 No Limitation

Proactive Process

• Identify Incorrect Information

• No Rules on How to Solicit or Collect Data

• Multipronged Approach

Solicit

Collect Responses

Update Data

TIN Match

The IRS has strict phishing rules. A violation leads to a 96 hour lockout!

ACA REPORTING

Pillars of ACA

Minimum

Essential

Coverage

Healthcare

Exchanges

Healthcare

Tax /

Subsidies

Medicare

Advantage

Plan

Changes

Medical

Loss Ratio

Business Implications for Insurers

• Increased Cost

• Decreased Margins

• Customer Attrition

• Regulatory Risk

• Increased Competition

• Change Management

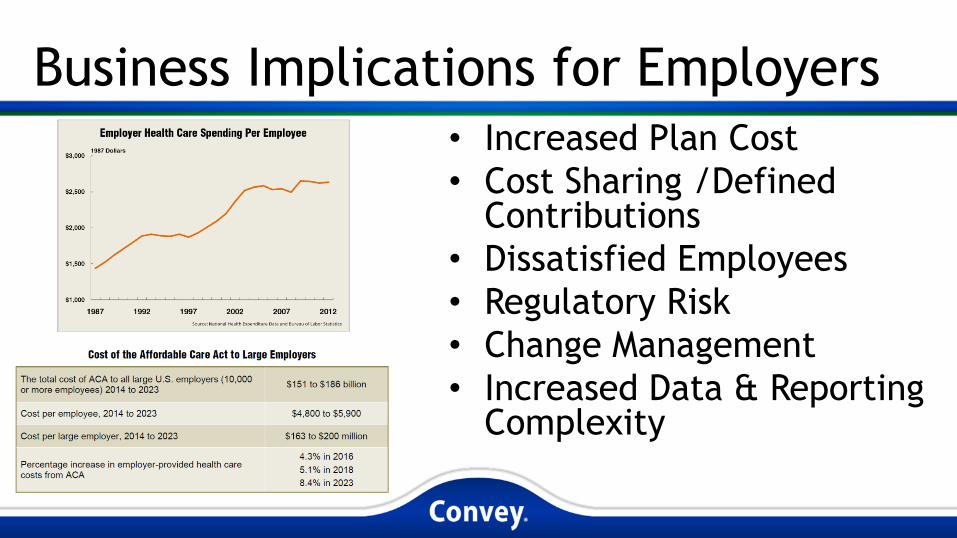

Business Implications for Employers

• Increased Plan Cost

• Cost Sharing /Defined Contributions

• Dissatisfied Employees

• Regulatory Risk

• Change Management

• Increased Data & Reporting Complexity

ACA Information Reporting Wage

Reporting Coverage

Reporting

Large Employer

Reporting

Large Self-Insured Employer

Reporting

Marketplace

Reporting

Insurer Employer Employer Govt

Some of the ACA fees

• For the Employer – 4980H- this is assessed if requirements are not

met and 1 or more employees claim the premium tax credit (1/1/15)

• This is assessed by the IRS and not the employer

• $3,000 for not providing – $250 per employee per month!

• For the provider of insurance – Same penalties as other non-wage forms

Planning Timelines

•IRS announced that 2014 reporting is not required •“BETA” trial much like 1099-K

•Individuals still required to carry coverage and report such on their year-end tax filing

•IRS announced that those who perform a “good faith” effort will not be penalized

•Full reporting implementation in place

2014 2015 2016

• Change Management over Time

• Low Risk Member Service

Impact / Training

• Data testing / improvement

• Delight clients with forms they

need

• Increased ability to adapt to

further changes

• Accelerated Change Management

• Reduced room for error / ability to

adapt to changes

• Reduced solicitation / response

timeframe

• Full solution must be in place

• Penalties imposed

Questions?

Contact Information

Riley Stroik

Enterprise Account Executive

Mike Weisenbeck

Enterprise Account Executive

Stay up to date…

Blog:

1099news.com

Twitter:

@Convey1099

Search for

‘Convey Compliance’

Latest Compliance Updates Taxport Compass: Guiding you through non-wage

reporting