TAX ISSUES TO CONSIDER IN COMMON ACQUISITION SCENARIOS December 13, 2005 Panelists: Scott D. Vaughn, Partner – Ernst & Young LLP Annette M. Ahlers, Corporate Tax Partner – Pepper H Moderator: Herb S. Ezrin, President – Potomac Business Group, Inc.

Transcript

TAX ISSUES TO CONSIDER INCOMMON ACQUISITION SCENARIOS

December 13, 2005

Panelists: Scott D. Vaughn, Partner – Ernst & Young LLP Annette M. Ahlers, Corporate Tax Partner – Pepper Hamilton LLPModerator: Herb S. Ezrin, President – Potomac Business Group, Inc.

Taxable Acquisitions—Stock vs. Asset

General Differences

Basic Structure

BuyerBuyer SellerSeller$

Buyer acquires the stock of Target Corporation for cash.

TargetCorporation

TargetCorporation

Taxable Stock Purchase: Results to Buyer

• Buyer takes a purchase price basis in the stock of Target Corporation (“Target”).

• However, Target itself does NOT get a stepped-up basis in its assets. (The assets retain their historic tax basis.)

Taxable Stock Purchase: Tax Attributes of Target

• The tax attributes (e.g., Net Operating Loss carryovers, tax credits, earnings & profits, etc.) of Target are generally retained by Target.

• Utilization of such attributes following the acquisition may, however, be limited under anti-loss trafficking rules:

- See, for example, §§382, 383, 384, 269 (use of NOL carryovers following ownership changes, etc.)

Taxable Stock Purchase:Results to Seller

• Individual Sellers- Generally, gain or loss determined based upon the difference between the proceeds received and the seller’s basis in the stock of Target sold.- Gain generally taxed at long-term capital gain rate (Federal =15%)

• Consolidated Group Seller- Any gain is taxed at corporate rates. - Previously deferred group income or gains could become triggered.- In certain circumstances, losses may be disallowed or deferred.

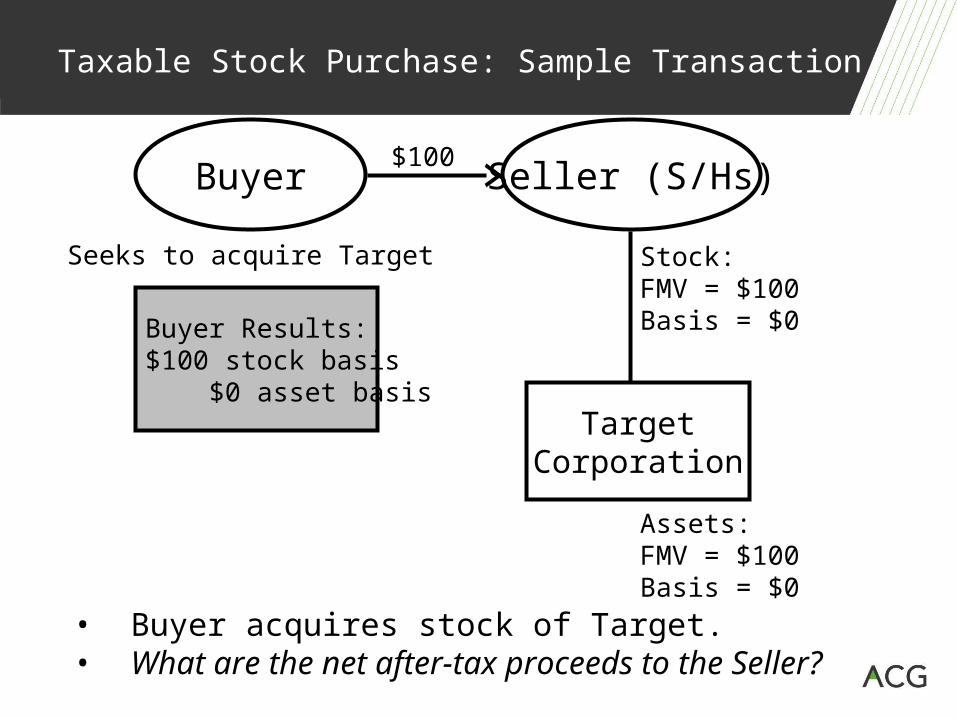

Taxable Stock Purchase: Sample Transaction

Seller (S/Hs)

TargetCorporation

Buyer

Stock:FMV = $100Basis = $0

Assets:FMV = $100Basis = $0

Seeks to acquire Target

$100

• Buyer acquires stock of Target.• What are the net after-tax proceeds to the Seller?

Buyer Results:$100 stock basis $0 asset basis

Taxable Stock Purchase:Sample Transaction Results

• Seller (Target S/Hs) receives $100 in consideration for its shares of Target stock.

• Seller recognizes $100 of capital gain and pays roughly 20%, or $20, in federal and state taxes on the transaction.

• Seller is left with $80 at the end of the day.

Proceeds $100Basis – 0Capital Gain = $100

Capital Gain $100Rate (x 20%)

Tax = $20

Proceeds $100Tax - 20Net $80

Taxable Stock Purchase:Issues to Consider

• Since tax (and other) liabilities remain with Target after the purchase transaction, thorough tax due diligence on Target is recommended.

Taxable Stock Purchase:Issues to Consider

• Advisable Purchase Agreement considerations. – The Buyer typically requires a full indemnity for taxes

paid in prior years and that all required returns have been filed.

– If there are significant issues with respect to certain tax filings or positions, an escrow can be established to hold back amounts until a matter is resolved (i.e., the Target is undergoing a state sales and use tax audit which will be resolved in 12 months.)

– Recently, Buyers have been requiring representations that no “listed or reportable” transactions have been entered into.

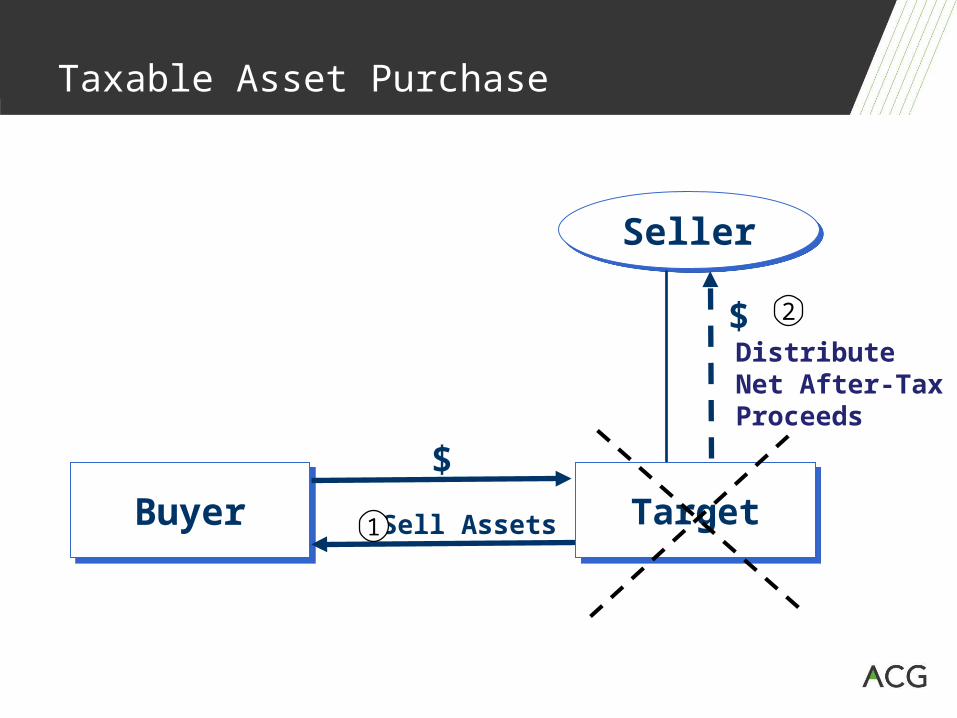

Taxable Asset Purchase

BuyerBuyer

SellerSeller

$

Sell Assets TargetTarget1

2$DistributeNet After-TaxProceeds

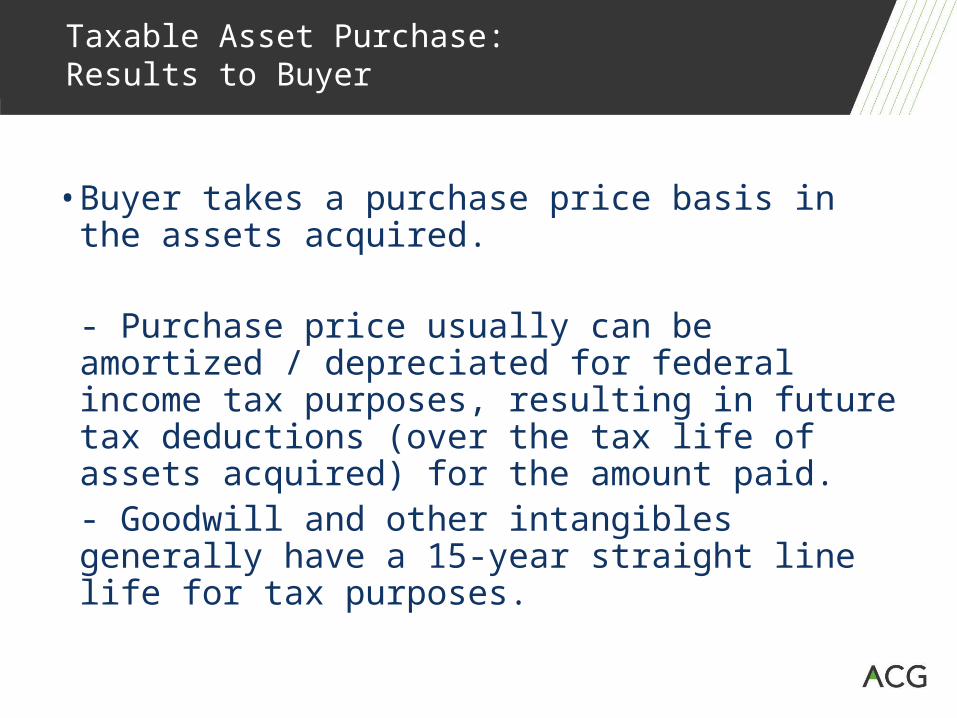

Taxable Asset Purchase: Results to Buyer

• Buyer takes a purchase price basis in the assets acquired.

- Purchase price usually can be amortized / depreciated for federal income tax purposes, resulting in future tax deductions (over the tax life of assets acquired) for the amount paid.- Goodwill and other intangibles generally have a 15-year straight line life for tax purposes.

Taxable Asset Purchase: Results to Seller/Target

• Seller recognizes gain/loss based upon the difference between the proceeds it received and the seller’s basis in the assets sold.

• Character of gain may be part ordinary and part capital.

• The tax attributes—e.g., NOLs—of Target (seller of assets) remain with Target.

• After corporate level tax is paid by Target, only net after-tax proceeds are available to be distributed to the shareholders of Target. The shareholders then generally recognize gain/loss based on the difference between the proceeds they receive and the shareholders’ basis in the Target stock that becomes cancelled.

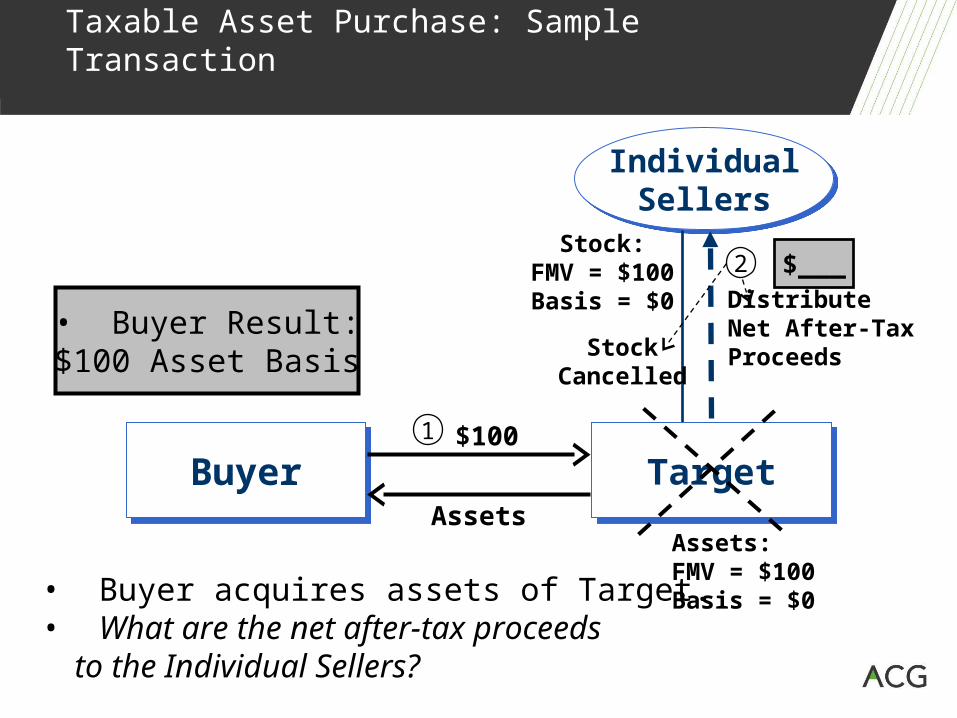

Taxable Asset Purchase: Sample Transaction

BuyerBuyer

IndividualSellers

IndividualSellers

TargetTarget1

2

DistributeNet After-TaxProceeds

• Buyer acquires assets of Target.• What are the net after-tax proceeds to the Individual Sellers?

• Target receives $100 in consideration for its assets and recognizes a $100 gain at the corporate level.

• Target pays roughly 40%, or $40, in federal and state taxes on the transaction.

• Target distributes the remaining $60 to its S/Hs (the Sellers) in a liquidation.

• Sellers recognize a $60 capital gain on the liquidation and pay roughly 20%, or $12 in federal and state taxes on the transaction.

• Sellers are left with $48 at the end of the day.

Target Proceeds $100Asset Basis – 0

Ordinary and/or Capital Gain = $100 Corporate Tax Rate (x 40%)

Tax = $40

Proceeds $100Corporate Tax - 40

Net Cash Available to S/Hs $ 60

Sellers (S/Hs) Net Cash to S/Hs $60Stock Basis - 0

Capital Gain = $60Individual Tax Rate (x 20%)

Tax = $12

Proceeds to S/Hs $60Individual Tax - 12

Net Cash to Sellers $48

Taxable Asset Purchase: Issues to Consider

• Buyer of assets generally does not inherit any past income tax liabilities associated with the business acquired, such liabilities remaining behind with the Seller/Target.

- As such, generally non-income tax due diligence—e.g., sales/use tax, property tax, etc.—is primary focus of tax due diligence efforts.

• Buyer and Seller often have adverse interests in allocating the purchase price among the assets sold. Tax rules set forth a method for allocating purchase price among seven classes of assets.

Taxable Asset Purchase: Issues to Consider

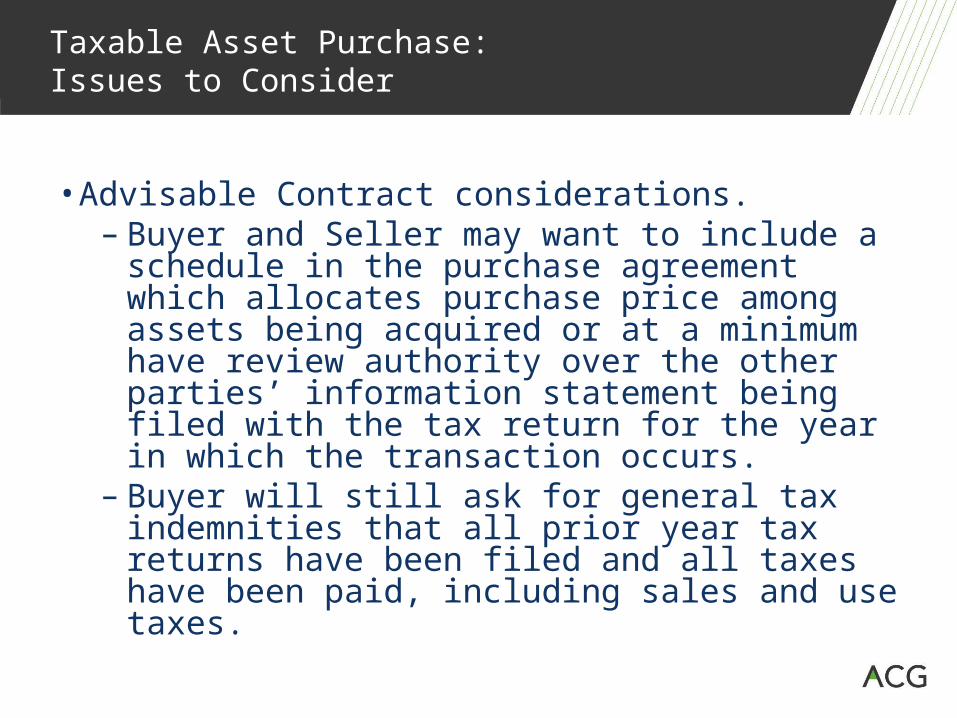

• Advisable Contract considerations.– Buyer and Seller may want to include a

schedule in the purchase agreement which allocates purchase price among assets being acquired or at a minimum have review authority over the other parties’ information statement being filed with the tax return for the year in which the transaction occurs.

– Buyer will still ask for general tax indemnities that all prior year tax returns have been filed and all taxes have been paid, including sales and use taxes.

Modeling: Buyers and Sellers Need to Compare and Contrast the Tax and Other Consequences of Each Structure

• What if Target has NOLs to offset?

• Buyer may want to buy assets (because Buyer can generally depreciate the purchase cost).

• Corporate Seller, however, may not want to sell assets (because Seller is often subject to the corporate double tax).

Elective Asset Acquisitions:

Taxable Acquisitions of S Corporations (or of Certain Subsidiaries in Affiliated Groups)

Section 338(h)(10) Elections

Elections to Treat Certain Stock Acquisitions as Asset Acquisitions

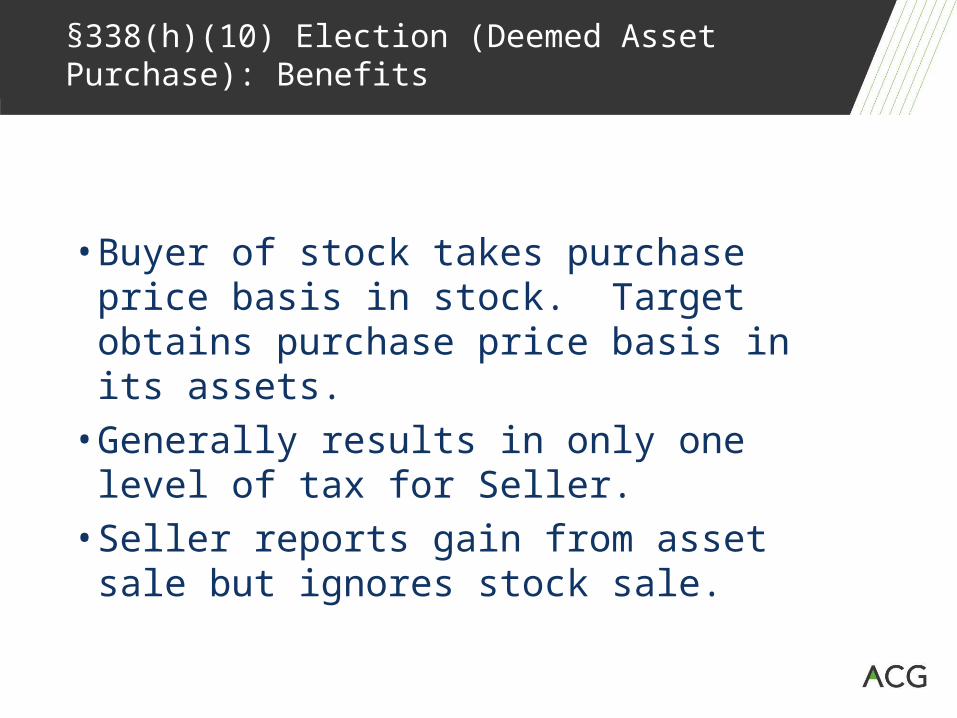

• In certain circumstances, if 80% or more of the stock of an S corporation (or an 80%-owned corporate subsidiary of an affiliated group) is acquired in a taxable transaction, then an election can be made to treat a stock sale transaction as an asset sale transaction solely for tax purposes (a Section 338(h)(10) election).

• BOTH Buyer and Seller must join in making the Section 338(h)(10) election.

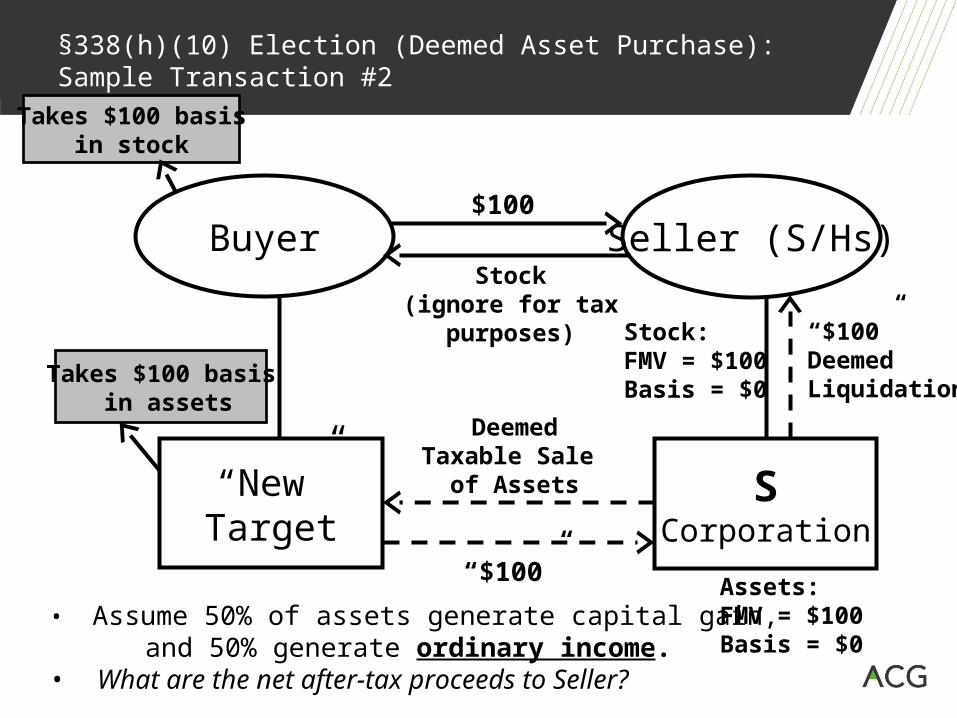

§338(h)(10) Deemed Asset Purchase

Actual Sale of T Stock Ignored

Deemed TaxableSale of Assets

PP

NewT

NewT

CorporateS/Hs

CorporateS/Hs

OldT

OldT

Deemed Liquidation of Old T for Proceeds

Fiction of an asset purchase by “New” Target; asset sale by “Old” Target

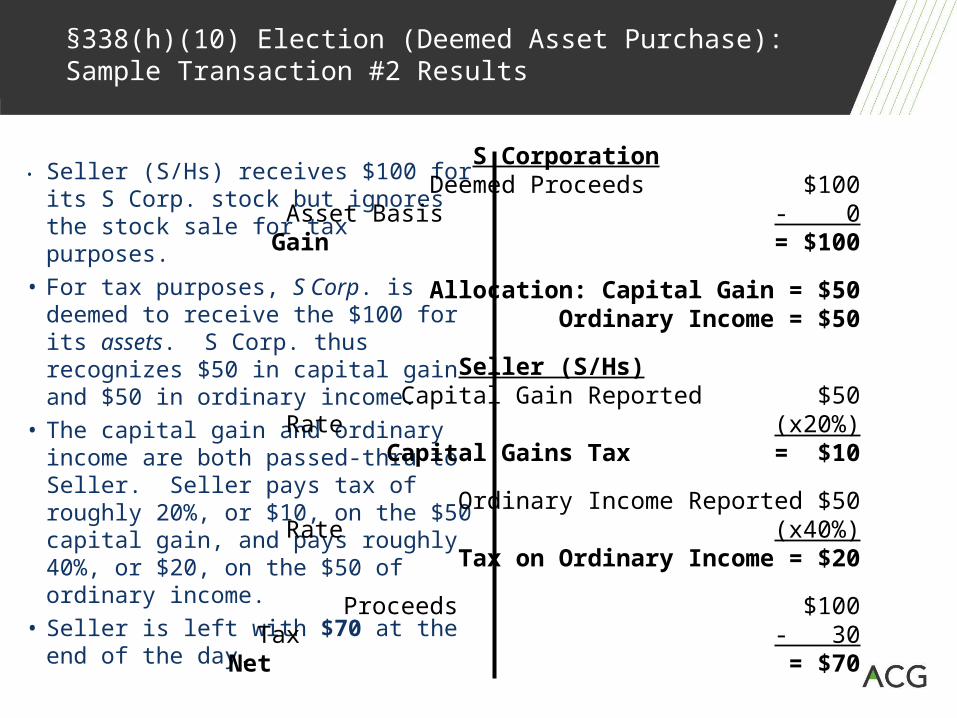

• Seller (S/Hs) receives $100 for its S Corp. stock but ignores the stock sale for tax purposes.

• For tax purposes, S Corp. is deemed to receive the $100 for its assets. S Corp. thus recognizes $50 in capital gain and $50 in ordinary income.

• The capital gain and ordinary income are both passed-thru to Seller. Seller pays tax of roughly 20%, or $10, on the $50 capital gain, and pays roughly 40%, or $20, on the $50 of ordinary income.

• Seller is left with $70 at the end of the day.

S Corporation Deemed Proceeds $100Asset Basis - 0

Gain = $100

Allocation: Capital Gain = $50Ordinary Income = $50

Seller (S/Hs) Capital Gain Reported $50Rate (x20%)

Capital Gains Tax = $10

Ordinary Income Reported $50Rate (x40%)

Tax on Ordinary Income = $20

Proceeds $100Tax - 30

Net = $70

§338(h)(10) Election (Deemed Asset Purchase):

Issues to Consider

• For S Corporation targets, tax due diligence is critical to establish the validity of the S Corporation’s status as such. This is critical for two reasons:

(1) if S Corporation status was not maintained, then the corporation would have been subject to corporate level tax as if it were a “C” corporation and thus there could be tax exposure in the Target, and

(2) the Buyer will not obtain the expected step-up in the basis of the Target’s assets if the Target was not an “S” corporation (and thus ineligible for the Section 338(h)(10) election).

§338(h)(10) Election (Deemed Asset Purchase):

Issues to Consider

• Contract Points.– Parties specifically state in the agreement that the

transaction is intended to be treated as a 338(h)(10) transaction.

– Buyer may ask for additional representation that target has always been an S Corporation for fiscal income tax purposes.

– General indemnities on filing returns and paying taxes.

§338(h)(10) Election (Deemed Asset Purchase): Additional Tax Issues for S Corporations Including Those that were Former C Corporations

• Application of Built-in Gain Tax (§1374)• Other potential entity-level taxes

-application of LIFO recapture tax

-passive investment income tax

• State taxes at the entity and shareholder levels

• Character of gain on asset sale—ordinary vs. capital

• Modeling is crucial to understanding potential for Gross-up

Tax-Free Transactions

• In certain circumstances the Seller can dispose of the Target Corporation in a tax-deferred manner including by merging the target into an Acquiring corporation for stock of the Acquiring corporation or by exchanging the stock of Target solely for stock of Acquirer.

-There are a number of different permutations and tax rules that govern when such transactions are tax-free.