33

Title goes here Subtitle goes here Name Surname One Name Surname Two Tax planning and the family home 3 October 2014 Gregory Laming

Title goes here Subtitle goes here

Name Surname One

Name Surname Two

Tax planning and the

family home

3 October 2014

Gregory Laming

Content

o Introduction

o Gift and leaseback approaches

o The co-ownership exemption

o Nil Rate Band discretionary trusts under

Wills

o Shearing approaches/double trust schemes

Gifts With Reservation (“GWR”)

o Section 102 Finance Act 1986 (“FA 1986”) – caught if an

individual disposes of property way of gift and either:

– possession and enjoyment is not bona fide assumed by

donee; or

– not enjoyed to the entire exclusion, or virtually to the entire

exclusion, of the donor, or of any benefit to him by contract or

otherwise

o Property in estate immediately before death for purposes of

Inheritance Tax Act 1984 (“IHTA 1984”) only – no CGT

rebasing!

GWR continued

o Revenue interpretation RI55 re meaning of “virtually”

for Section 102 and the November 1993 Tax Bulletin

issue No 9 in relation to the de minimis rule.

o Key exemptions to GWR for use with the family home:

– Sch 20 paragraph 6(1)(a) FA 1986 – full consideration in

money or monies worth - see also the Inland Revenue

letter dated 18 May 1987

– Section 102B FA 1986

Gift and leaseback

o Bob, a widower, has a home worth £1m

o Bob has an available NRB of £325,000 and wishes to gift a

share of his house into trust for his grandchildren

o Transfer of value = loss to donor’s estate

o After gift, as he remains a co-owner, value of his remaining

share is discounted by 10%

o Bob gives a 25% share

o Bob’s transfer value is £1m minus (£750,000 reduced by

10%) = £325,000

Gift and leaseback continued

o Full market rent negotiated by two valuers : one for Bob and one

for the trustees - 25% of the full rent payable – review or GWR!

o Bob must survive gift into trust by seven years

o Income tax efficient with grandchildren

o No main residence relief exemption for the trustees’ 25% share

o On Bob’s death, IHT discount of 10% on his retained interest

o Grant lease first to nominee? Issues - control/SDLT/valuation?

o Higher values? - outright gifts, leases over part, L&T obligations?

o POAT exemption - para 11(5)(d) Sch 15 Finance Act 2004

Co-ownership exemption s102B FA

1986 o Hansard debate on FA 1986 – the then Minister of State said “For

example, elderly parents make unconditional gifts of undivided shares in

their house to their children and the parents and the children occupy the

property as their family home, each owner bearing his or her share of

the running costs. In those circumstances, the parents’ occupation or

enjoyment of the part of the house that they have given away is in

return for similar enjoyment of the children of the other part of the

property. Thus the donors’ occupation is for a full consideration” [my

emphasis]

o s102B was introduced in Finance Act 1999 to put a co-

ownership exemption on a statutory footing

The co-ownership exemption – Section 102B continued o Section 102B(4) applies when:

– the donor and the donee occupy the land; and

– the donor does not receive any benefit other than a negligible

one, which is provided by or at the expense of the donee for

some reason connected with the gift

o Occupation, but not necessarily as a family home, is required

o “Occupation”?- POAT guidance at IHTM44003 helpful?

o Problems if children leave home

o While no GWR by parents they are making potentially exempt

transfers – what if they die within seven years?

The co-ownership exemption – Section 102B continued o The donee for these purposes must be an individual

o What if children die before the parents?

o What if parents need to go into a nursing home?

o Unlike Hansard Statement, s102B makes no reference

to occupation being for full consideration, so can

unequal shares be used? HMRC scrutiny expected

because of 2nd limb to s102B - see also foot note to

IHTM14332

o POAT exemption at paragraph 11(5)(c)

s102B co-ownership exemption

continued o Example: Bob lives in London and has three adult

children. Child 1 lives with him and works in London;

Child 2 stays there at weekends but works away during

the week; and Child 3 is in the RAF and stays there

when on leave. All 3 have their own keys, leave their

possessions there and come and go as they please

o Lots of issues not least potential lack of ability to elect

PPR for Child 2 and Child 3 children from 6 April 2015

o Bob could just give a share to Child 1- equality issues?

Nil rate band discretionary trusts (“NRBDTs”) o Is there any need for these since the introduction of the

transferable Nil Rate Band – Sections 8A-C of IHTA 1984?

o Nil Rate Band frozen at £325,000 until tax year 2017/18

o Do new rules from 6/6/14 on SNRBs affect matters?

o If it is thought that assets may appreciate in value more

quickly than the Nil Rate Band, it may be sensible to put

some assets into a NRBDT on the first death – this could be

part of the family home

o Contentious – see SP 10/79 + STEP and CIOT Q&As with

HMRC in Autumn 2007

NRBDTs

o HMRC’s Statement of Practice 10 (1979) – “many Wills and

settlements contain a clause empowering the trustees to permit a

beneficiary to occupy a dwelling house which forms part of trust

property on such terms as they think fit. The Commissioners for

HM Revenue & Customs (HMRC) do not regard the existence of

such a power as excluding any interest in possession of the

property”

o “….if the power is drawn in terms wide enough to cover the

creation of an exclusive or joint residence, albeit revocable, for a

definite or indefinite period and is exercised with intention of

providing a particular beneficiary with a permanent home, HMRC

will normally regard the exercise of a power as creating an

interest in possession”

NRBDTs continued

o How does one minimise the opportunity for HMRC

to argue an interest in possession has arisen on

first death?

o Judge and Judge (Walden’s PR) v HMRC (2005)-

have trustees knowingly used their powers to give

exclusive occupation?

o BUT consequence of an interest in possession

arising means in effect there will be a transferable

Nil Rate Band + CGT uplift – so not a big disaster?

NRBDTs continued

o Example: Bob and Margaret have a house worth £650,000 and a

pension. Bob leaves his estate to Margaret outright. On Margaret’s

death the house is worth £1.3m. Bob’s unused Nil Rate Band is

transferred to Margaret. The inheritance tax payable on the house will

be (£1.3m minus £650,000) at 40% = £260,000

o Alternatively, Bob includes a NRBDT in his Will and his half share of the

house worth £325,000 is placed in an NRBDT. On Margaret’s death, the

IHT will be calculated on just Margaret’s half share as (£650,000 minus

£325,000) at 40% = £130,000 (even ignoring co-ownership discounts)

o So IHT saving and asset protection BUT no PPR under s225 TCGA

1992 on half share in NRBDT (as trustees have not exercised power to

allow occupation) and 10 year/exit charges to consider

Historic use of NRBDTs and shares

of houses o On account of SP10/79 before 22 March 2006 equitable

charges and promissory notes were common, for example

Bob and Margaret own a house worth £650,000. On Bob’s

death, instead of his half share of the house passing into

the NRBDT, the executors assent his half share to Margaret

subject to a charge in favour of the trustees of the NRBDT

for £325,000 plus an uplift e.g. the RPI

o Before 17 July 2013 and the introduction of s175A Finance

Act 2013 IHTA 1984, on Margaret’s death the inheritance

tax calculation would be, crudely, (£1.3m less £325,000

less £325,000 index linked with RPI) all at 40%

Historic use of NRBDTs and shares

of houses continued o The monies owed to the trustees of Bob’s NRBDT i.e.

£325,000 plus RPI might not be called for in full and the

premium element e.g. the RPI might be waived to prevent a

tax charge in the hands of the trustees of the NRBDT

o Is there any point in implementing this type of arrangement

anymore – asset protection?

o How do we deal with these historical arrangements?

Existing debt/charge schemes re

NRBDTs o Usually the monies owed were linked to the RPI

o Repayment in full necessary to get IHT deduction under s175A IHTA

1984, but taxation somewhat unclear

o 3 possibilities:

– CGT on basis RPI increase is capital gain - trustee rate 28%

– Income tax on basis debt is deeply discounted security (“DDS”) -

trustee rate is 45%

– Income tax on basis that RPI increase is interest-trustee rate of

45%, but possibility of reclaim by beneficiaries

Tax treatment of RPI uplift - CGT?

o CGT exemption at s251(1): ”where a person incurs a debt to another…no chargeable

gain shall accrue to that (that is the original) creditor or his PRs or legatee on a disposal

of the debt, except in the case of the debt on a security (as defined in section 132)”

o Is the RPI element part of the debt and so capable of being relieved by section

251(1), or is it some other stand alone type of asset? Arguably a debt on case

law c.f. Marren v Ingles [1980] 3 All ER 95 (HL)

o Is the debt a “debt on a security”? WT Ramsay v IRC [1982] AC 300 suggests

two essential elements required:

– it is suitable to hold as an investment; and

– it can be realised at a profit

o Taylor Clark Int. Ltd v Lewis STC 1259 (CA) : a debt with no fixed term and

repayable on demand without penalty or additional consideration- not a suitable

investment and not debt on a security. It is thought therefore that no CGT

charge can arise on redemption

Tax treatment of RPI uplift - DDS

o Is the RPI element a DDS?

o s430(1) ITTOIA 2005 defines what a DDS is - “a security” where the amount

payable on maturity will or may exceed the issue price by more than 0.5% for

each year in the redemption period

o What is a “security” in this context? If it is the same as “a debt on a security” in

the CGT context then the debt is not a DDS

o Two characteristics seem to apply for s430 ITTOIA 2005 to apply:

– the security must be “issued”- is this a suitable term to describe the relationship

between the NRBDT trustees and a beneficiary?

– the implication from the legislation is that there should be a time fixed for redemption

of the security, but there is usually no such period with NRBDT debts/charges

o So most likely not a DDS so s427 ITTOIA 2005 should not lead to an income tax

charge on the profit from the RPI element?

Tax treatment of RPI uplift – interest?

o HMRC could seek to charge the RPI premium as interest since s381(1)

ITTOIA 2005 provides all discounts, other than discounts in DDSs, are

treated as interest

o Despite reference to ”all discounts” HMRC do accept that the discount

or premium must be in the nature of income, rather than capital to be

taxed as interest –SAIM2230

o To charge RPI to income tax as ordinary interest, we are understand

that HMRC have previously relied on Lomax v Peter Dixon [1943]

KB671 (HL). However, this case was in a commercial context. Also,

the charge/IOU documentation usually provided that none of the

amounts payable were interest and the aim of the RPI is to preserve the

capital value of the NRBDT fund rather than provide income

Where have we got to?

o Worse case position is taxation as DDS- 45% income tax

and cannot reduce by appointing income in NRBDT to

non/low rate tax payers - as capital for trust purposes

o Best result is that premium is capital and exempt under

s251(1) TCGA 1992 and failing that at 28% - also an IHT

exit of capital from the NRBDT but there is no hold over as

no one would acquire the asset on redemption

o Most likely result is that HMRC will argue it is interest -

consider appointing life interests to beneficiaries to make

use of their lower rates of income tax?

So what do we do?

o Depends on the circumstances, but perhaps most straightforward in

some cases simply to waive the premium and accept no deduction of

premium (RPI) element on account of s175A IHTA 1984?

o If the premium element is a DDS then waiver doesn’t constitute a

disposal for s437 ITTOIA 2005- “not a redemption, transfer by sale,

exchange, gift or otherwise”

o If RPI premium is to be treated as interest then under Dewar v CIR

[1935] 2 K.B. 351 – there should be no charge on the waiver as

“interest” never paid

o If premium is liable to CGT then if s251(1) applies there should be no

chargeable gain. No one becomes absolutely entitled as against the

trustees of the NRBDT to trigger a disposal – s71(1) TCGA 1992

Shearing approaches

o What is a shearing arrangement?

o There are two types of shearing arrangements: “Ingram”

and reversionary lease types

o “Ingram” type – the freehold of the house is carved up,

usually using a nominee arrangement, into a leasehold

interest for less than 21 years in favour of the donor (or

possibly a surviving spouse in a Will context) and the

freehold reversion subject to the lease is gifted down the

family

Shearing approaches continued

o Reversionary leases involve the freehold remaining with the

donor (or on IPDI trusts for the surviving spouse in a Wills

context). The freehold is subject to a lease in favour of the

children - usually a long lease of 299 years, which doesn’t

start for say another 20 years

o History of shearing schemes and Section 102A of Finance

Act 1986 (which followed the Lady Ingram case in 1999)

o Upshot is reversionary lease schemes are less contentious

than “Ingram” schemes

Shearing approaches continued

o Both types lead to a wasting value within the estate of the

donor (or the surviving spouse in a Wills context)

o Lifetime planning unattractive except for let property:

– Post Finance Act 1999 “Ingram” schemes are largely ineffective-

caught by s102A. Schemes prior to 1999 are effective for IHT but

caught by POAT and all have CGT downsides

– Reversionary lease schemes arguably still effective (HMRC have

argued caught post 1999 - see IHTM14360 - but see also GAAR

D2.5.4 where impliedly accepted they work). s102A isn’t wide

enough to catch them. Caught by POAT and CGT downsides

How might we use them?

o Lifetime shearing arrangements generally not viable for homes in

occupation. Exceptions to this are with (1) let property, (2) with existing

pre 22 March 2006 interest in possession trusts where there is an

elderly life tenant occupying his home, and (3) Will trusts with IPDIs in

favour of the surviving spouse

o Example: Bob and Margaret have a house worth £1m which is owned

solely by Bob. Bob dies with a flexible Will and a reversionary lease

over the home is carved out such that Margaret has a life interest in the

freehold which is subject to a 299 year lease commencing in 20 years.

This reversionary lease is appointed to the children – a PET by

Margaret

How might we use them? continued

o Margaret lives for 15 years and on her death the value in her estate will

be the value of the right to live in the house for the remaining five years

before the long lease to the children commences - perhaps the value of

five years’ rent?

o NB Section 102ZA of FA 1986 deems coming to end of interest in possession

as a gift only for the purposes of Section 102 and Schedule 20 of FA 1986 but

not Section 102A. Margaret has no GWR in the reversionary lease

o Pre-owned assets tax –in trust so Margaret has not disposed of an

“interest in land”?

o CGT issues? Structure to rely on s225 TCGA 1992?

o Caution needed where the property is already a leasehold property –

the Buzzoni [2012] UKUT 360 (TCC)

GAAR – are reversionary leases over

land caught? o HMRC don’t like shearing schemes - IHTM 14360

o Para D2.5.4 of GAAR Guidelines now suggests that,

contrary to IHTM 14360, lifetime reversionary lease

planning is OK – ref POAT and CGT collected. D27.4.1.

shearing schemes in general acceptable except where the

Government’s policy on certain arrangements has led to

legislative changes e.g. for land e.g. s102A-C FA 1986

o Planning with trusts looks very attractive, but must be

susceptible to scrutiny – as no POAT- so keep it simple?

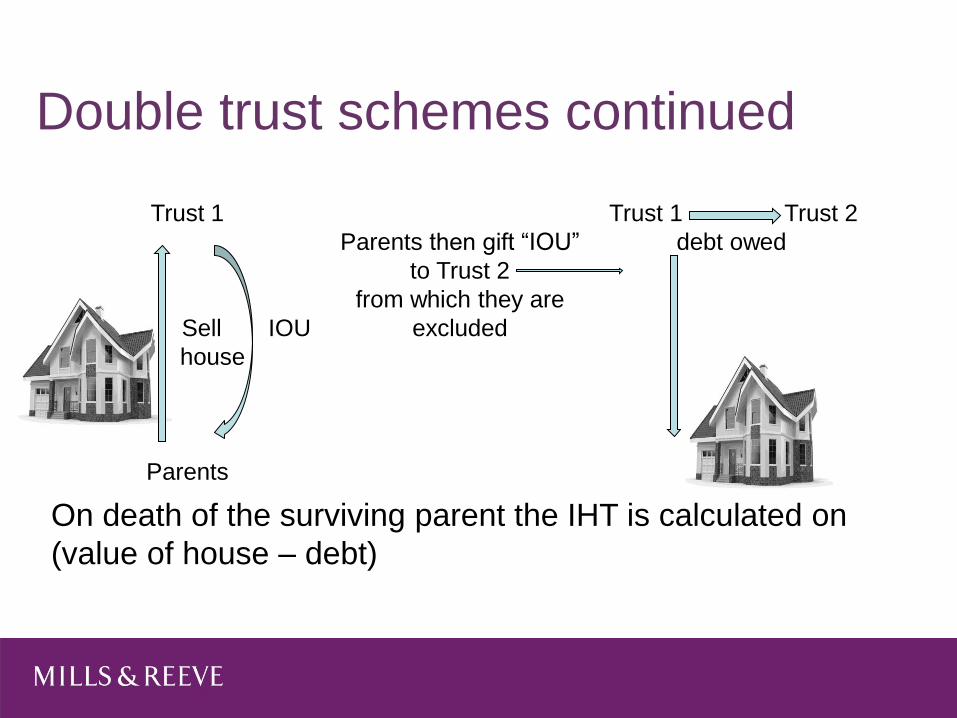

Double trust schemes continued

Trust 1

Sell IOU

house

Parents

Parents then gift “IOU”

to Trust 2

from which they are

excluded

Trust 1 Trust 2

debt owed

On death of the surviving parent the IHT is calculated on

(value of house – debt)

Double trust schemes continued

o Up until HMRC changed their Pre-owned Assets

Guidance Section 5 in October 2010 HMRC accepted

that double trust schemes worked provided the debt

was not repayable during the lifetime of the parents

o Change of attitude

o HMRC’s arguments

o Any test case on the horizon?

o Present hiatus and HMRC’s approach where are we

now?

DOTAS

o HMRC have just issued a Consultation on the DOTAS

regime

o The aim is to widen the scope of DOTAS to catch

inheritance tax planning generally and the concept of

grandfathering is to fall away

o There will be reporting requirements on lifetime and

Will planning - more compliance and administration

Conclusion

IHT planning

for the family

home

DOTAS