1 Tax Treatment of Image Programs Forget everything you thought you knew! With Robert Davis III and J. Wayne Robbins Jr., CPAs of Dixon Hughes Goodman LLP Moderated by Mike Bowers, Executive Editor of DealersEdge Thursday, April 19, 2012 1 – 2:30pm ET J. Wayne Robbins, Jr, CPA -Dixon Hughes Wayne Robbins has been with the Firm for 24 years. A partner in the Raleigh office, he concentrates primarily on income tax issues, tax planning and mergers/acquisitions. He has a strong background in client service with a variety of industries. Additionally, Wayne has more than 15 years of experience in the automobile dealership industry. His seasoned experience includes assisting his clients with an array of services. Working extensively in the automobile dealership industry, Wayne advises more than 50 dealership clients of all sizes. Education: University of North Carolina-Charlotte, B.S. (Accounting) Professional/Civic Organizations * American Institute of Certified Public Accountants (AICPA) * North Carolina Auto Dealers Association (NCADA) * North Carolina Association of Certified Public Accountants (NCACPA) Robert C. Davis III, CPA -Dixon Hughes Goodman LLP A Member in the Firm’s Memphis office, Robert Davis brings over 20 years of public accounting experience to his clients. He also gained valuable experience in the car business by spending countless hours in his father’s Lincoln-Mercury dealership when he was a child. Currently, Robert serves dealership clients in the areas of accounting, audit, tax, and management advisory services. In addition, he is heavily involved in buy/sell agreements and litigation support services. Dealers around the country recognize Robert for his operational knowledge of automobile dealerships and the impact his Strategic Assessments have had on dealerships. Education * University of Texas, M.P.A. (Taxation) * University of Arkansas, B.S. (Business Administration) Professional/Civic Organizations * American Institute of Certified Public Accountants (AICPA) * President of Olive Branch Country Club * Volunteer Pilot for Angel Flight South Central

Transcript

1

Tax Treatment of Image Programs Forget everything you thought you knew!

WithRobert Davis III and J. Wayne Robbins Jr., CPAs

of Dixon Hughes Goodman LLP Moderated by

Mike Bowers, Executive Editor of DealersEdge

Thursday, April 19, 20121 – 2:30pm ET

J. Wayne Robbins, Jr, CPA - Dixon HughesWayne Robbins has been with the Firm for 24 years. A partner in the Raleigh office, he concentrates primarily on income tax issues, tax planning and mergers/acquisitions. He has a strong background in client service with a variety of industries. Additionally, Wayne has more than 15 years of experience in the automobile dealership industry. His seasoned experience includes assisting his clients with an array of services. Working extensively inthe automobile dealership industry, Wayne advises more than 50 dealership clients of all sizes.

Education: University of North Carolina-Charlotte, B.S. (Accounting)

Professional/Civic Organizations* American Institute of Certified Public Accountants (AICPA) * North Carolina Auto Dealers Association (NCADA) * North Carolina Association of Certified Public Accountants (NCACPA)

Robert C. Davis III, CPA - Dixon Hughes Goodman LLPA Member in the Firm’s Memphis office, Robert Davis brings over 20 years of public accounting experience tohis clients. He also gained valuable experience in the car business by spending countless hours in his father’s Lincoln-Mercury dealership when he was a child. Currently, Robert serves dealership clients in the areas of accounting, audit, tax, and management advisory services. In addition, he is heavily involved in buy/sell agreements and litigation support services. Dealers around the country recognize Robert for his operational knowledge of automobile dealerships and the impact his Strategic Assessments have had on dealerships.

Education* University of Texas, M.P.A. (Taxation) * University of Arkansas, B.S. (Business Administration)

Professional/Civic Organizations* American Institute of Certified Public Accountants (AICPA) * President of Olive Branch Country Club * Volunteer Pilot for Angel Flight South Central

2

The New 2012 Temporary Repair Regulations

Reg. §1.263(a)

Today’s Presenter

• Robert Davis, PartnerOffice phone number – (901) 684-5646Email address – [email protected] Office location - Memphis, TN

• Wayne Robbins, PartnerOffice phone number - (919) 875-4990Email address – [email protected] Office location - Raleigh, NC

4

3

Circular 230 Disclosure

5

To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication is not intended or written to be used, and cannot be used, for the purpose of avoiding penalties under the Internal Revenue Code.

• Overview• Unit of Property (UOP)

– Buildings– Other Tangible Property

• Building Systems• Leasehold Improvements• Improvements to Tangible Property

– Betterment vs. Refresh

– Restoration

– Adaptation

6

Agenda

4

Agenda (continued)

• Structural Component Disposition– Loss Recognition– GAA Retroactive Election Option

• Key Changes for Buildings• Planning

– New Automatic Changes– Form 3115

7

Overview• New regulations were issued on December 23, 2011

• Effective for tax years beginning January 1, 2012

– Release of new temporary regulations effectively withdraws the 2008 proposed regulations

– Reduces scope of what qualifies under case law and 2008 proposed regulations

• Revenue Procedures

– Rev. Proc. 2012-19 and Rev. Proc. 2012-20 were issued on March 7, 2012 to provide additional guidance on procedures for filing form 3115. Provides for 19 new automatic method changes most of which can be filed on a single 3115.

8

5

Overview (continued)

• IRC Section 263(a) provides that no deduction is allowed for :1) Any amount paid out for new buildings or permanent

improvements or betterments made to increase the value of any property or estate;

2) Or any amount expended in restoring property or in making good the exhaustion thereof for which an allowance has been made.

3) Generally requires the capitalization of amounts paid to acquire, produce, or improve tangible property.

9

Overview – Cont’dQ. Who is affected by the temporary repair regulati ons?A. The temporary regulations affect all taxpayers with tangible property. If a taxpayer owns or leases property, they must comply with the temporary regulations. These regulations affect corporations, pass-through entities, CFC earnings and profits, and even individual rental property owners.

-One of the most pervasive changes seen recently

Q. What happens if I don’t comply? What are the po tential implications?A. Filing a 3115 will allow the taxpayer to spread the positive 481(a) adjustment over 4 years. If the taxpayer is examined by the IRS and the taxpayer has not adopted the new temporary regulations, then the IRS can require the taxpayer to include the 481(a) into income immediately.

Additionally, if taxpayer does not file the 3115 and makes the necessary 481(a) adjustment, the taxpayer could be subject to the 20% accuracy-related penalty for negligence or disregard of rules or regulations.

The taxpayer may need to include a FIN 48 disclosure in footnotes to it’s financial statements.

If the statute of limitations has expired, the tax basis that would have been a component disposal loss may be lost – no future deductions.

May be required to file Form 8275-R, Regulation Disclosure Statement to report a position taken contrary to a regulation.

6

UNIT OF PROPERTY

11

Unit of Property defined for other than buildings

• For property other than buildings – all components that are functionally interdependent will constitute a single unit of property.

• Functional interdependence is where one component is dependent on another in order to fulfill its purpose.

• This definition has limited applicability to dealerships.

12

7

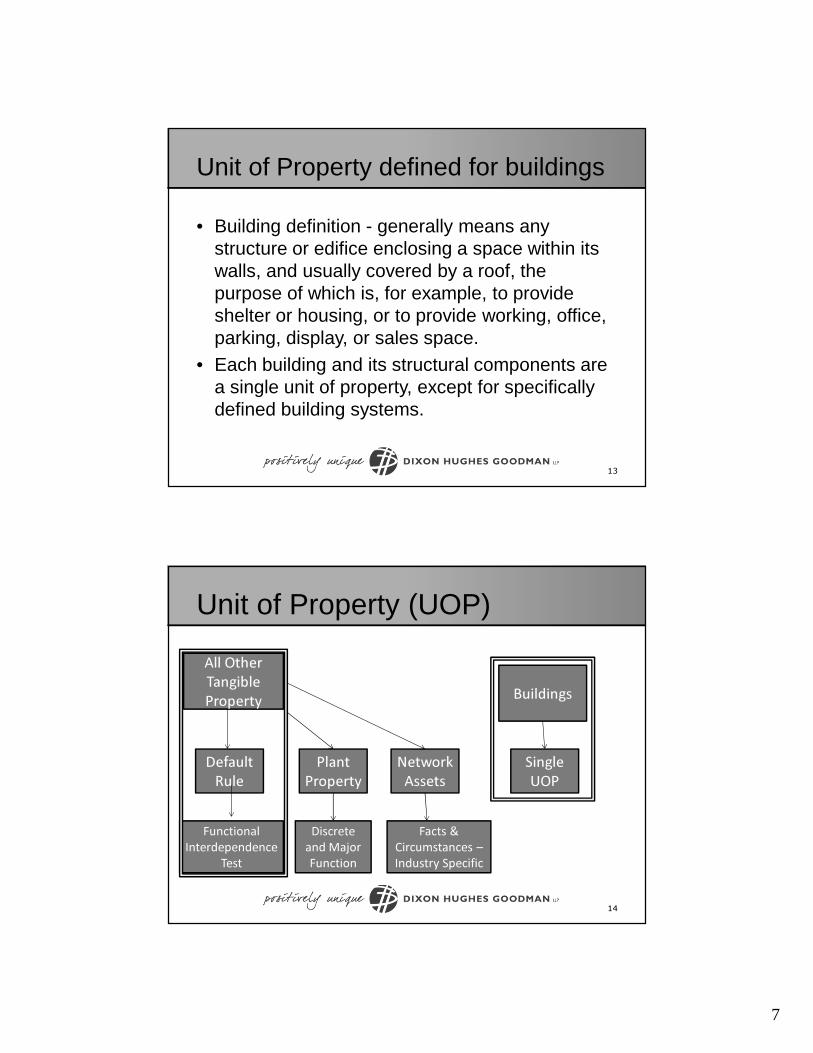

Unit of Property defined for buildings

• Building definition - generally means any structure or edifice enclosing a space within its walls, and usually covered by a roof, the purpose of which is, for example, to provide shelter or housing, or to provide working, office, parking, display, or sales space.

• Each building and its structural components are a single unit of property, except for specifically defined building systems.

13

Unit of Property (UOP)

14

BuildingsAll Other Tangible Property

Default Rule

Plant Property

Network Assets

Single UOP

Functional Interdependence

Test

Discrete and Major Function

Facts & Circumstances –Industry Specific

8

Unit of Property - Buildings

15

Apply Capitalization

StandardsDetermine

UOPCapitalize

Improvements to UOP

Entire Building

Building Structure

Building Systems

Entire Building

UOP = Building and Structural Components - §1.48-1(e)(1)

BUILDING SYSTEMS

16

9

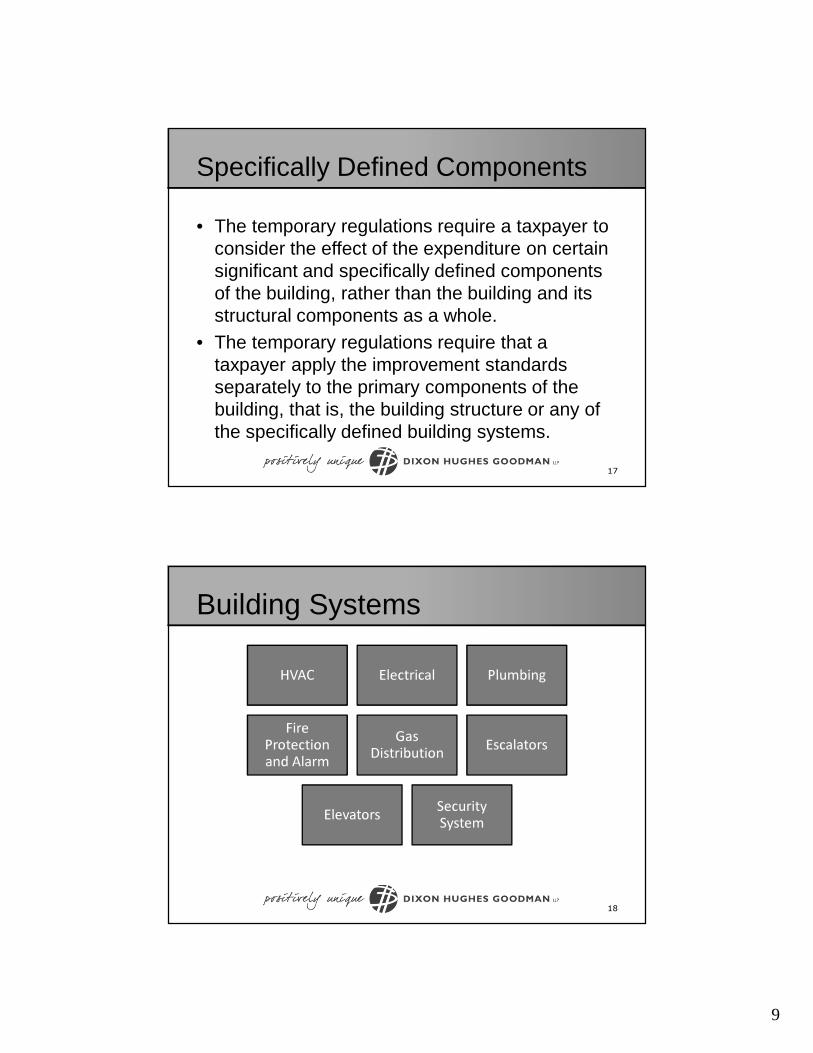

Specifically Defined Components

• The temporary regulations require a taxpayer to consider the effect of the expenditure on certain significant and specifically defined components of the building, rather than the building and its structural components as a whole.

• The temporary regulations require that a taxpayer apply the improvement standards separately to the primary components of the building, that is, the building structure or any of the specifically defined building systems.

17

Building Systems

HVAC Electrical Plumbing

Fire Protection and Alarm

Gas Distribution Escalators

Elevators Security System

18

10

Leasehold Improvements

19

Unit of Property for Leaseholds

The temporary regulations define the unit of property for leased buildings and provide that if a taxpayer is a lessee of all or a portion of one or more buildings (such as an office, floor, or certain square footage), the unit of property is each building and its structural components or the portion of each building subject to the lease and the structural components associated with the leased portion.

20

11

Leasehold Improvements

• Lessee’s UOP = building and its structural components subject to the lease– Amounts paid for the initial lessee improvements are

treated as the acquisition of a new unit of property

• Lessor’s UOP = building– Amounts paid for lessor improvement are treated as

an improvement to the underlying property

21

Capitalization

Betterment, Restoration and Adaptation

22

12

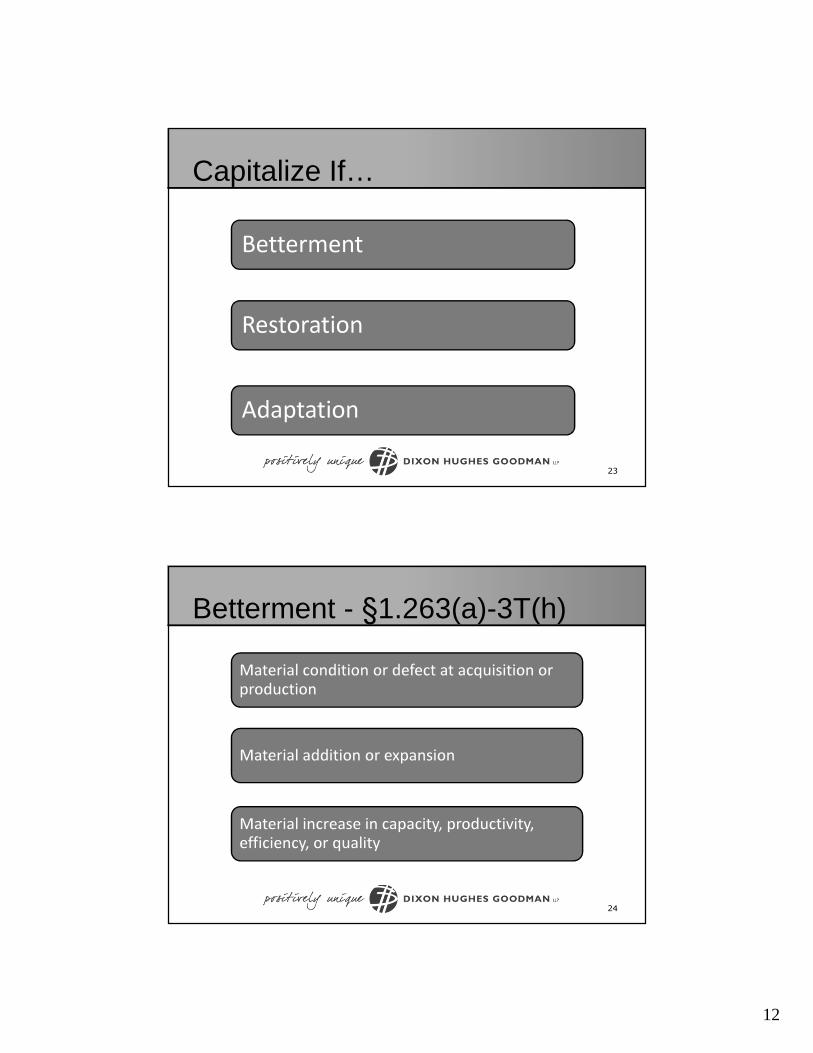

Capitalize If…

Betterment

Restoration

Adaptation23

Betterment - §1.263(a)-3T(h)

Material condition or defect at acquisition or production

Material addition or expansion

Material increase in capacity, productivity, efficiency, or quality

24

13

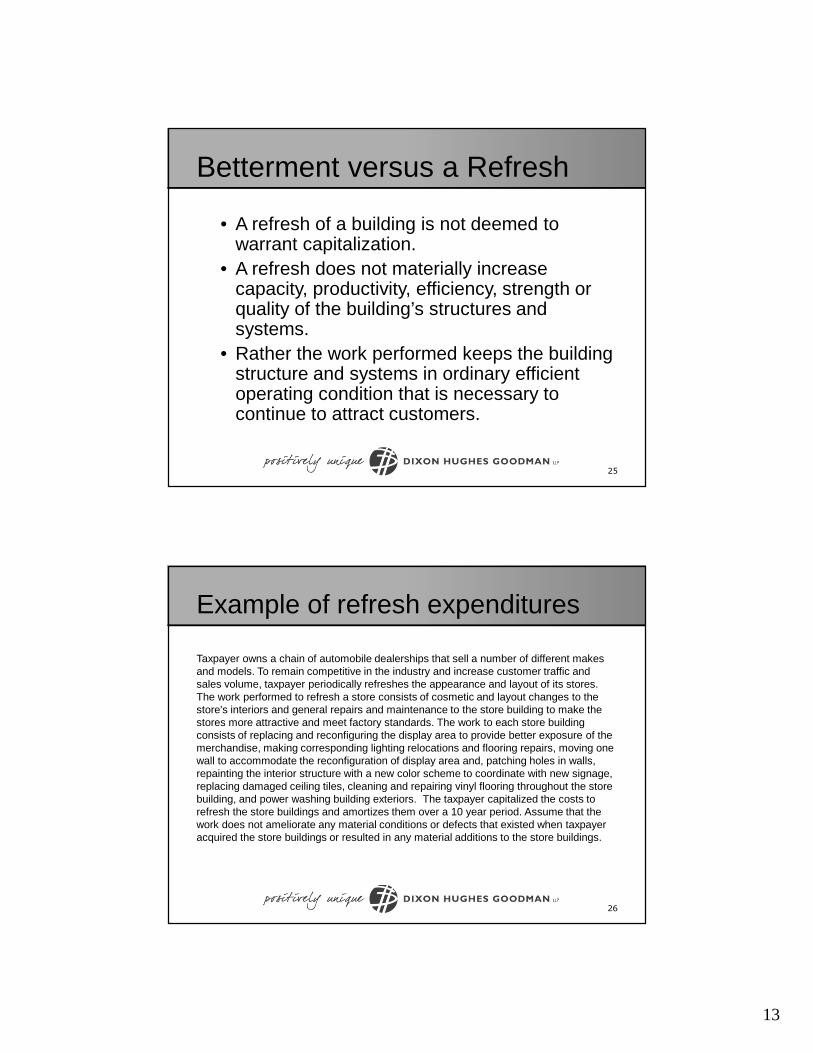

Betterment versus a Refresh

• A refresh of a building is not deemed to warrant capitalization.

• A refresh does not materially increase capacity, productivity, efficiency, strength or quality of the building’s structures and systems.

• Rather the work performed keeps the building structure and systems in ordinary efficient operating condition that is necessary to continue to attract customers.

25

Example of refresh expenditures

Taxpayer owns a chain of automobile dealerships that sell a number of different makes and models. To remain competitive in the industry and increase customer traffic and sales volume, taxpayer periodically refreshes the appearance and layout of its stores. The work performed to refresh a store consists of cosmetic and layout changes to the store's interiors and general repairs and maintenance to the store building to make the stores more attractive and meet factory standards. The work to each store building consists of replacing and reconfiguring the display area to provide better exposure of the merchandise, making corresponding lighting relocations and flooring repairs, moving one wall to accommodate the reconfiguration of display area and, patching holes in walls, repainting the interior structure with a new color scheme to coordinate with new signage, replacing damaged ceiling tiles, cleaning and repairing vinyl flooring throughout the store building, and power washing building exteriors. The taxpayer capitalized the costs to refresh the store buildings and amortizes them over a 10 year period. Assume that the work does not ameliorate any material conditions or defects that existed when taxpayer acquired the store buildings or resulted in any material additions to the store buildings.

26

14

Example of refresh expenditures

(continued)Considering the facts and circumstances, as required under the new temporary regulations including the purpose of the expenditure, the physical nature of the work performed, the effect of the expenditure on buildings' structure and systems, and the treatment of the work on the taxpayer’s applicable financial statements, the amounts paid for the refresh of each building do not result in material increases in capacity, productivity, efficiency, strength, or quality of the buildings' structures or any building systems as compared to the condition of the buildings' structures and systems after the previous refresh. Rather, the work performed keeps the store buildings' structures and buildings' systems in the ordinary efficient operating condition that is necessary for the taxpayer to continue to attract customers to its stores. Therefore, the taxpayer is not required to treat the amounts paid for the refresh of its store buildings' structures and buildings' systems as betterments.

27

Restorations (§1.263(a)-3T(i))

Replacement and recognition of a loss on disposed component

Recognized a gain/Loss on sale of a component

Basis adjustment as a result of a casualty loss under section 165Return to former operating condition – no longer functioning/ state of disrepairRebuild the property to like-new condition after the end of its economic useful lifeReplacement of major component or substantial structural part

28

NEW

15

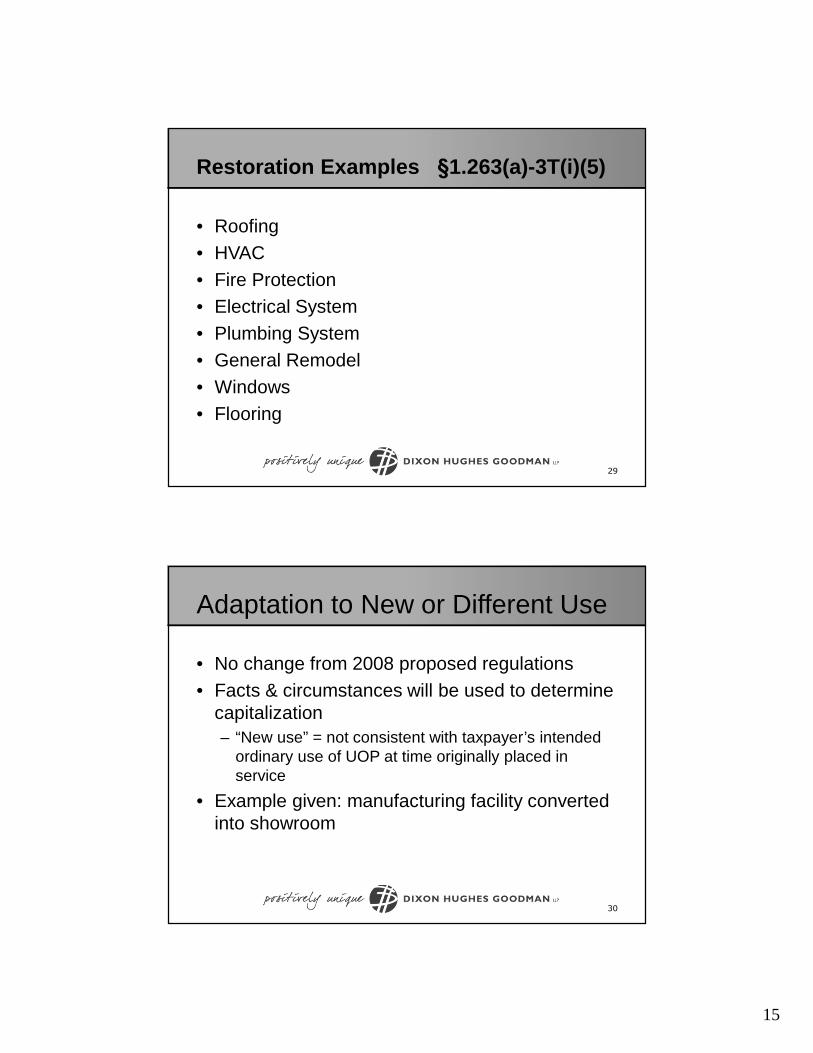

Restoration Examples §1.263(a)-3T(i)(5)

• Roofing• HVAC• Fire Protection• Electrical System• Plumbing System• General Remodel• Windows• Flooring

29

Adaptation to New or Different Use

• No change from 2008 proposed regulations• Facts & circumstances will be used to determine

capitalization– “New use” = not consistent with taxpayer’s intended

ordinary use of UOP at time originally placed in service

• Example given: manufacturing facility converted into showroom

30

16

Changes to Disposition Rules

Sale or Exchange Retirement Physical Abandonment

DestructionTransfer to a

supplies, scrap or similar

Involuntary Conversion

Retirement of a Structural

Component of a Building

31

Updated the definition of “disposition” to include the retirement of a structural component of a building

NEW

Disposition of Structural Components• Expanded definition prevents taxpayers from

having to capitalize and depreciate simultaneously amounts paid for both the removed and replacement property– Old Rule: Replace Roof, depreciate old and new roof– New Rule: Replace a roof, deduct the NBV of old roof

• Recognition of loss is mandatory unless General Asset Account (GAA) election is made. – Election is retroactive– Check box election on Form 4562– Must keep records of GAA groupings

32

17

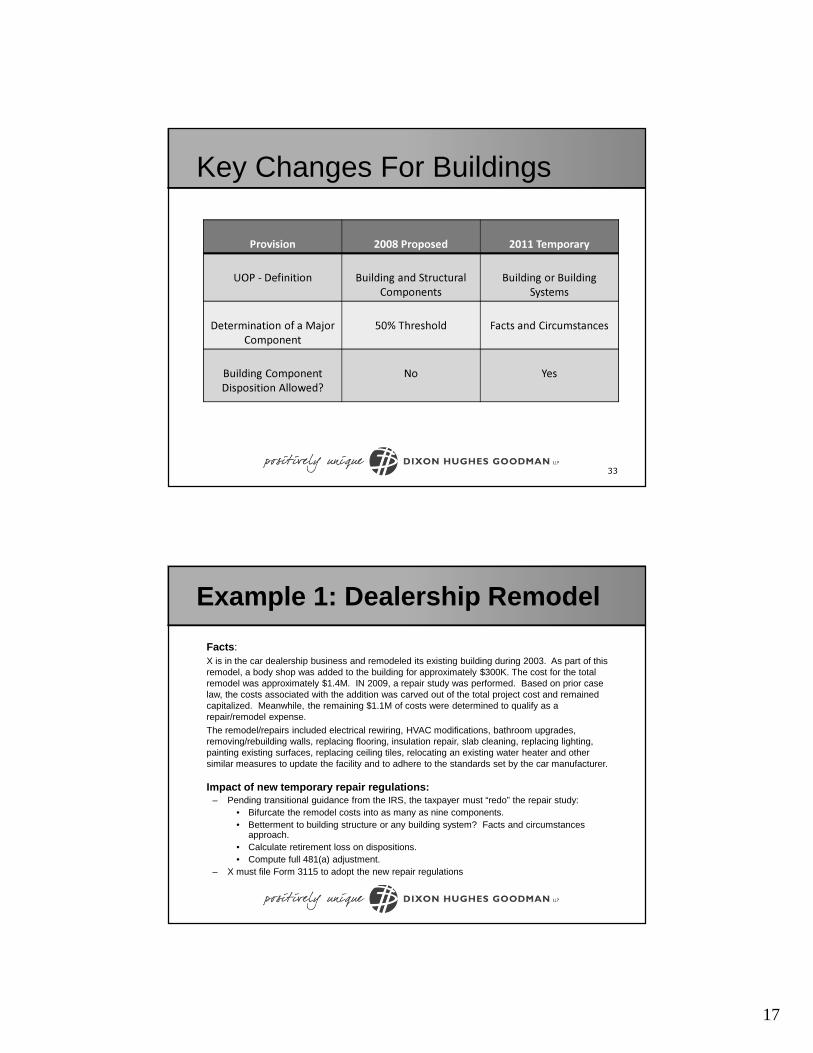

Key Changes For Buildings

Provision 2008 Proposed 2011 Temporary

UOP - Definition Building and Structural Components

Building or Building Systems

Determination of a Major Component

50% Threshold Facts and Circumstances

Building ComponentDisposition Allowed?

No Yes

33

Example 1: Dealership Remodel

Facts :X is in the car dealership business and remodeled its existing building during 2003. As part of this remodel, a body shop was added to the building for approximately $300K. The cost for the total remodel was approximately $1.4M. IN 2009, a repair study was performed. Based on prior case law, the costs associated with the addition was carved out of the total project cost and remained capitalized. Meanwhile, the remaining $1.1M of costs were determined to qualify as a repair/remodel expense.

The remodel/repairs included electrical rewiring, HVAC modifications, bathroom upgrades, removing/rebuilding walls, replacing flooring, insulation repair, slab cleaning, replacing lighting, painting existing surfaces, replacing ceiling tiles, relocating an existing water heater and other similar measures to update the facility and to adhere to the standards set by the car manufacturer.

Impact of new temporary repair regulations:– Pending transitional guidance from the IRS, the taxpayer must “redo” the repair study:

• Bifurcate the remodel costs into as many as nine components.• Betterment to building structure or any building system? Facts and circumstances

approach.• Calculate retirement loss on dispositions.• Compute full 481(a) adjustment.

– X must file Form 3115 to adopt the new repair regulations

18

Example 2: Roof ReplacementFacts:In 2002, X replaced its roof due to its deteriorated condition. Roof insulation was mechanically fastened over the existing surface. Also, the existing metal copings and flashings were re-installed. X incurred $175K in costs to replace the roof.There was no substructure replacement; therefore, it was determined that the work done did not result in betterment or structural improvement to the roof. Based on prior case law, it was determined that the expenses incurred by X were to keep the unit of property (the building and its structural components) in its operating condition and did not increase the economical useful life of the building. As a result, the costs were treated as currently deductible repairs and maintenance.

Impact of new temporary repair regulations:– Does the roof replacement result in a restoration of the building structure?

• Has a major component or substantial structural part of the building structure been replaced?– Entire roof – a substantial structural part of the building structure– Roof membrane – not a substantial structure part of the building structure

• Should X make a GAA election?– Decide whether the GAA election should be made

• X must apply the restoration rules contained in the temporary regulations to the costs incurred to replace the roof and make a determination whether a 481(a) adjustment must be made.

Example 3: Exterior Glass

Q. X owns a large office building with 300 exterior windows. During 2012, X replaced 30 of the exterior windows that had become damaged. Is X required to capitalize the amounts paid to replace the windows?A. The exterior windows are part of the building structure. The 30 replacement windows do not comprise a large portion of the physical structure of the office building structure, and, by themselves, do not perform a discrete and critical function in the operation of X’s building structure. Therefore, amounts paid to replace the windows is not a restoration of a building system.

Q. Same facts as above, but X replaced 200 of the 3 00 exterior windows . Does this change the answer?A. Yes. The 200 exterior windows comprise a large part of the physical structure of X’s building and perform a discrete and critical function in the operation of the building structure. The 200 windows comprise a major component or substantial structural part of the building structure and X must treat the amounts paid to replace the 200 windows as a restoration of a building system.

19

Example 4: Lessee Improvements

Q. AB Real Estate owns a 60,000 square foot buildin g that is being used as a car dealership. On 1/1/X1, John Toyota, a car dealer signed an init ial 10 year lease on the building. As an incentive, AB Real Estate agreed to upfit the buildi ng to the lessee’s specification. AB Real Estate properly capitalized the leasehold improveme nts to the building. Several years later, the car manufacturer requested that John Toyota rem odel the dealership facility. In year X6, John Toyota spent $1,000,000 to remodel the facilit y which included upgrading the façade, replacing flooring, moving walls, rearranging offic es, upgrading lighting fixtures, and upgrading bathrooms. Is John Toyota required to tr eat the amounts paid for the remodel as a betterment to the building structure and the buil ding systems?

A. The temporary regulations provide that the amounts paid must be capitalized as a lessee improvement, and constitutes a separate unit of property from the leased property being improved. Treating the lessee’s initial improvement as a separate unit of property is based on the premise that, when making a leasehold improvement, the lessee should be treated as if it acquired or produced new property. This new property interest is separate and distinguishable from the lessee’s interest in the underlying property.

Rev. Proc. 2012-19 and Rev. Proc. 2012-20

Automatic changes in accounting methods

38

20

Changes in accounting methods - Form 3115

• Elect by filing Form 3115• Calendar year taxpayers have until the tax

year beginning January 1, 2014 to comply with method change rules and not be subject to the scope limitations of section 4.02.

• Need an effective plan by making appropriate elections in 2012 & 2013

39

Automatic Changes Highlights

• Deducting repairs and maintenance costs (#162)

• Deducting de minimis amounts (#169)• Capitalizing acquisition or production costs

(#173)• Capitalizing improvements to tangible

property (#174)

40

21

Automatic Changes Highlights

(continued)• Depreciation of leasehold improvements

(#175)• Permissible to permissible method of

accounting for depreciation of MACRS property (#176)

• Disposition of a building or structural component (#177)

41

Automatic Changes Highlights

(continued)• Dispositions of tangible depreciable assets

(other than a building or its structural components) (#178)

42

22

Looking Forward

• Regulation comment period still open• What is the affect on cost segregation studies?• Do we now have the requirement to conduct building

systems studies?• At present IRS audit activity on this matter has been

suspended for tax years beginning prior to January 1, 2012.

• For tax years beginning on or after January 1, 2014, IRS examiner should apply the regs in effect and follow normal examination procedures.