Taxation ➢ Tax is a compulsory levy that the state imposes on the citizens. The tax is a binding force which connects the two important pillars of the democracy i.e. state/government with citizens. Each citizen enjoys certain entitlements from government and in return has to contribute to the government in the form of tax payments. If the citizen doesn’t pay the tax, either he becomes a free rider (consumes services of the government but doesn’t pay tax) or exits (doesn’t consume the services of the government). In either case, the accountability factor on the government reduces. So it could be said that tax is an agreement between the state and the citizen wherein the government promises to provide certain entitlements to the citizen and in return the citizen makes the tax payments. ➢ Types of Taxation Systems Progressive Regressive As the income goes up, taxes also go up As the income goes up, taxes go down Income inequality is reduced Income inequality is increased Eg-Income Tax Direct Indirect Incidence and impact are on the same person Incidence on one person and impact is someone else Contribution is greater than 50% Contribution is relatively lesser Major contributors are corporate and income taxes Major contributors are excise (cenvat), customs and services Ex-income tax, wealth tax, corporate tax Ex- Cenvat, sales tax, service tax etc

Transcript

Taxation

➢ Tax is a compulsory levy that the state imposes on the citizens. The tax is a

binding force which connects the two important pillars of the democracy i.e.

state/government with citizens. Each citizen enjoys certain entitlements from

government and in return has to contribute to the government in the form of tax

payments. If the citizen doesn’t pay the tax, either he becomes a free rider

(consumes services of the government but doesn’t pay tax) or exits (doesn’t

consume the services of the government). In either case, the accountability

factor on the government reduces. So it could be said that tax is an agreement

between the state and the citizen wherein the government promises to provide

certain entitlements to the citizen and in return the citizen makes the tax

payments.

➢ Types of Taxation Systems

Progressive Regressive

As the income goes up, taxes also go up As the income goes up, taxes go down

Income inequality is reduced Income inequality is increased

Eg-Income Tax

Direct Indirect

Incidence and impact are on the same person

Incidence on one person and impact is someone else

Contribution is greater than 50% Contribution is relatively lesser

Major contributors are corporate and income taxes

Major contributors are excise (cenvat), customs and services

Ex-income tax, wealth tax, corporate tax

Ex- Cenvat, sales tax, service tax etc

o Surcharge- is a charge imposed whenever the income crosses certain level

Cess- a tax imposed to achieve a certain objective

o Countervailing duty- imposed so as to bring the prices of imports on par

with domestic prices

Anti dumping duty- imposed by the government whenever a country

exports the goods at a lower prices

➢ Features of Indian Taxation System

o Progressive-most of the taxation imposed by the government are in the

form of progressive taxes eg-Corporate tax, Income tax etc

o Complex- even though the various reforms have been implemented over a

period of time in India the taxation structure is considered to be complex

with respect to exemptions, filing etc

o Loopholes- there are various loopholes using which tax evasion is followed

o No tax on income from agriculture

➢ Some of the taxes

o Service Tax

▪ Introduced in 1994-95 with 3 services

▪ Levied by central government

▪ Gradually the list was expanded and covered more than 100

services

▪ From 2012 shifted to negative list approach

▪ 2015 it was increased to 14% (inclusive of 3% education cess)

▪ Present rate is 15%

Advalorem Specific

Imposed on the basis value of the commodity

Imposed based on the specific attributes of the commodities

Chelliah committee recommended more of these taxes

producer/intermediary will pay certain tax based on the value

addition

▪ VAT-central VAT (CENVAT) and state VAT (Sales Tax)

▪ The offsetting is allowed in case of movement of goods either is in

the stage of value addition or in the process of being sold from one

distributor to another distributor

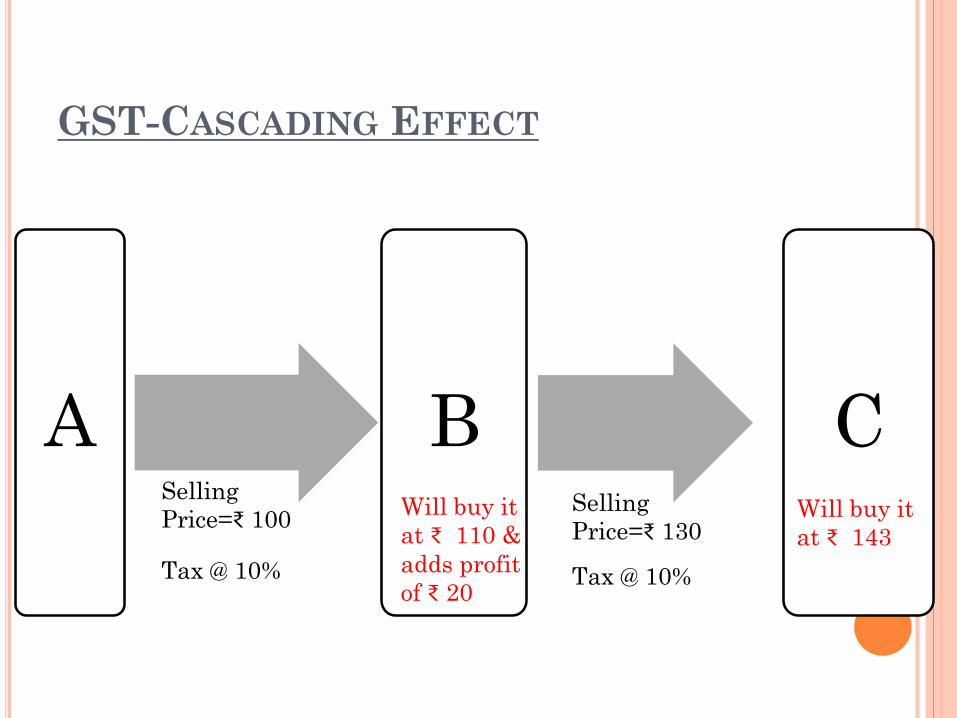

▪ The VAT was introduced in order to reduce the cascading effect

➢ CESS-

o Imposed as per the article 270

o Recent Cesses-Swachh Bharat Cess, Krishi Kalyan Cess

➢ Presumptive Taxation

o Refers to imposition of tax on the presumption that a certain

individual/entity/company earns/enjoys profits enough to be able to pay

tax, yet they avoid taxes. The government imposes taxes in such scenario

referred to as Presumptive taxation

o MAT

▪ MAT is a tax levied on profit-making entities that don’t pay

corporate income tax because of exemptions and incentives

▪ Tax levied on book profits

▪ FPIs completely exempted

▪ Justice A P Shah Committee recommended that FPIs cannot be

levied MAT

o GAAR (General Anti-Avoidance Rules)

▪ These are a set of provisions which try and check tax avoidance.

GAAR would come into implementation from 1st April

▪ Observations of Parliamentary Standing Committee

• GAAR gives arbitrary powers to tax authorities to challenge

complex deals

• Onus lies on the taxpayer

• Created uncertainty and ambiguity amongst investors

▪ Parthasarathi Shome Committee

• No retrospective application

• Deferred till 2016-17

• Not applicable on Singapore and Mauritius

• Not on intra-group transactions

• No short-term capital gains tax

• Rate of STT must be increased

➢ Problems with Indian Taxation System

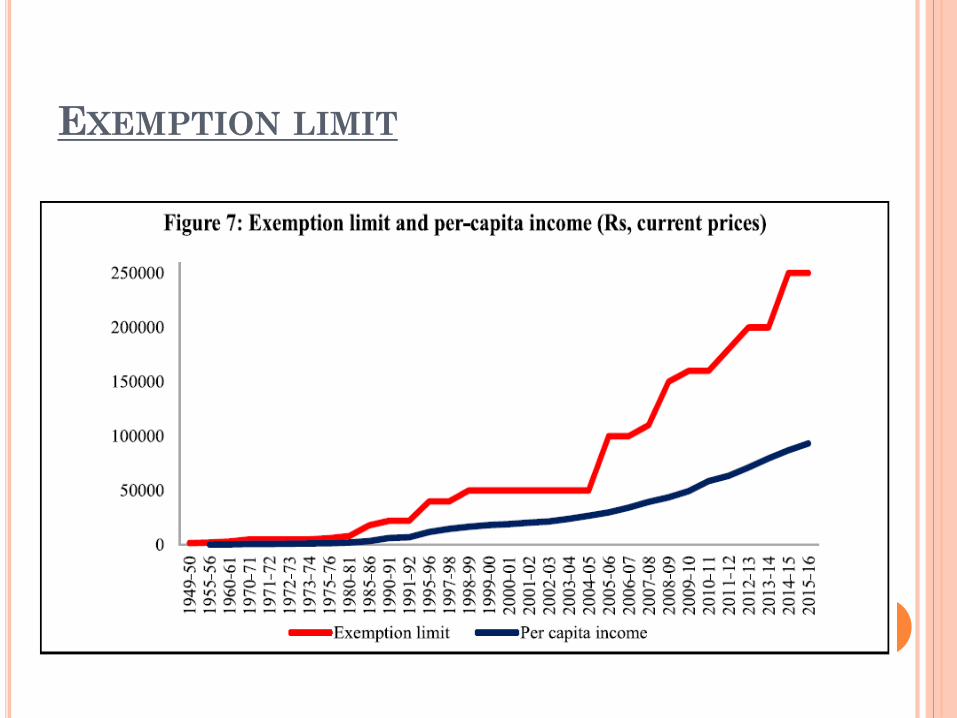

o The income tax exemption limit has been periodically increased which has

led to more income tax payers being exempted. The last time it was raised

from Rs 1,50,000 in 2012-13, as a result of this exemption government had

to forego Rs 31500 crore

o Problems with coverage

▪ Only 5.5% of the income earners pay tax

▪ The ratio of tax payers to population in voting age comes around to

4%, which should be more than 23%

o Government provides a large tax exemptions to the corporate sector

which is a revenue foregone

o Indian Government under-taxes as well as under spends compared to the

developed countries

o As a result of presence of unorganized sector, more than 85% of the

economy is not covered under taxation

GST

The GST will be a revolutionary tax reform which will streamline the indirect tax

structure in India. Before India implements GST, throughout the world more than 140

countries have shifted to GST (Malaysia implemented it in 2015).

GST bill was introduced (through 115th CAB) during UPA II, as the Lok Sabha was

dissolved the bill lapsed and the new NDA government has re-introduced it as 122nd

CAB. The features of the bill are

• It will be subsuming all the indirect taxes (some exemptions have been provided

as of now)

• It will streamlining the taxation procedures (only indirect taxes)

• It will be a dual GST-central and state GST

• It will lead to creation of GST council

o Set up by the president

o Union Finance Minister + state Finance ministers

o Functions-model GST laws, taxes/surcharge/cess to be levied by the centre

and state, exemptions to be given etc

o GST council to decide regarding resolution of disputes

• It provides for the input credit across segments

• It further reduces the cascading effect

• The states loosing revenues will be provided compensation

• It will lead to formation of national market

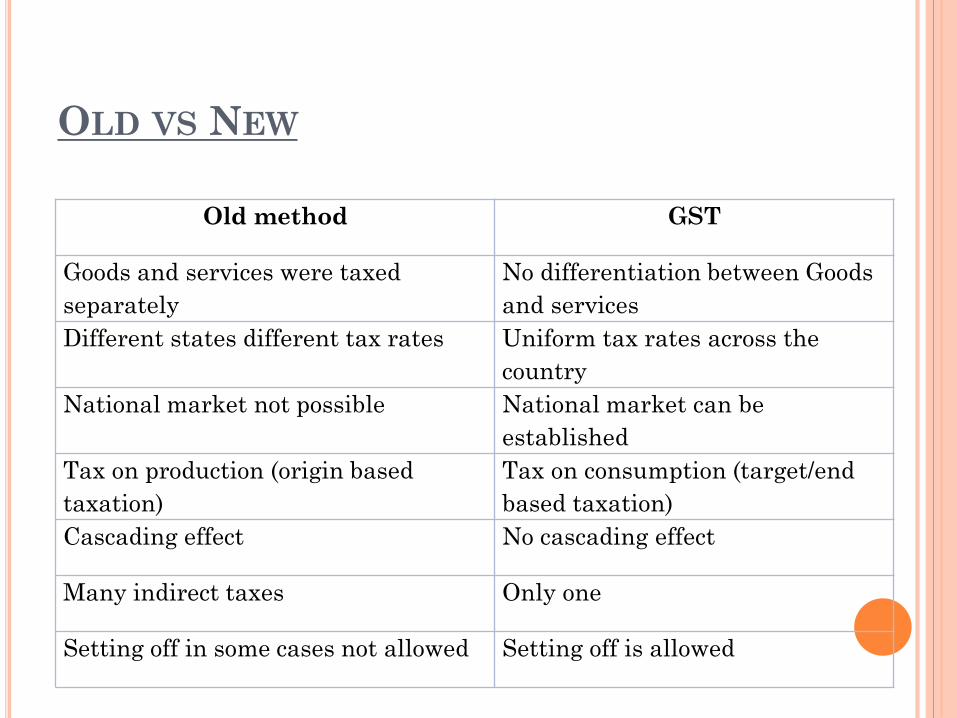

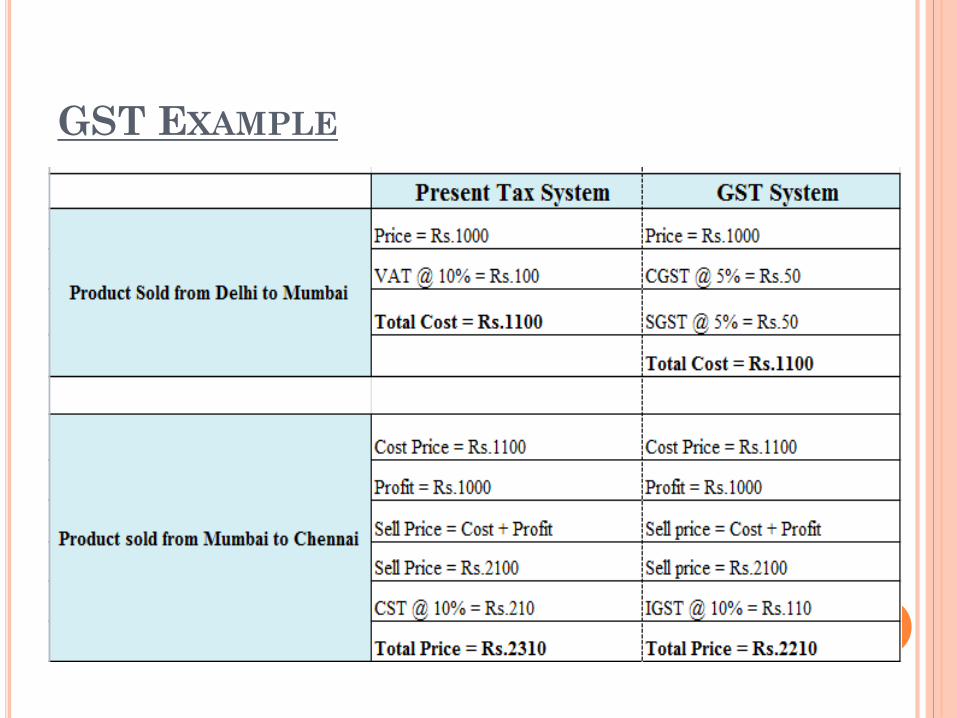

GST vs. Old method

Old taxation method GST

Goods and services were taxed separately No differentiation between Goods and services

Different states different tax rates Uniform tax rates across the country

National market not possible National market can be established

Tax on production (origin based taxation) Tax on consumption (target based taxation)

Cascading effect No cascading effect

Many indirect taxes Only one

Setting off in some cases not allowed Setting off is allowed

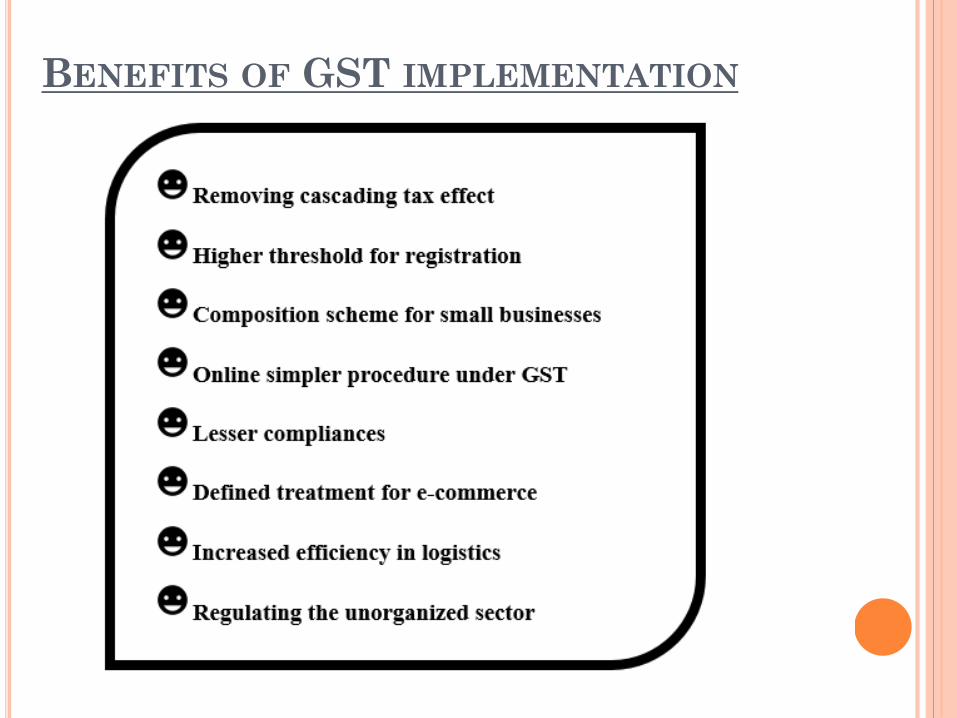

Advantages of GST

• Overall o It will lead to a unified national market by bringing in uniform indirect tax

rates, and bringing in certainty. GST would make doing business in India tax neutral, irrespective of the choice of place of doing business

o It will be remove the cascading effect thereby removing the hidden cost of doing business. This reduction in costs is expected to increase the competitiveness.

• For companies o GST will have a robust IT framework which will compliances such as filing

of registrations, returns, payments etc much more easy and transparent

• For Central and State Governments o The multiplicity of taxes is being replaced by a single robust system with

end-to-end IT framework. This will make it easier and simpler to administer the taxes

o Will lead to better compliance and increased revenues and also lower the cost of collection of taxes (will lead to revenue efficiency)

• For the consumer o Because of removal of cascading effect and efficient method of imposing

and collecting taxes, the tax burden will come down on the common man

Concerns of the states

• The compensation to be paid – the states want a mechanism to be laid down

regarding the payment of compensation (full) to be paid to them for the next 5

years

• The rate of GST

• Dispute Resolution Mechanism – in the original Bill there was a proposal to set up

an Independent Tax Dispute Settlement Authority but was watered down in the

bill of the present BJP government under which the GST council will have the

power to set up Dispute Resolution Mechanism on case-to-case basis. Some of

the states agree to this and some are not comfortable.

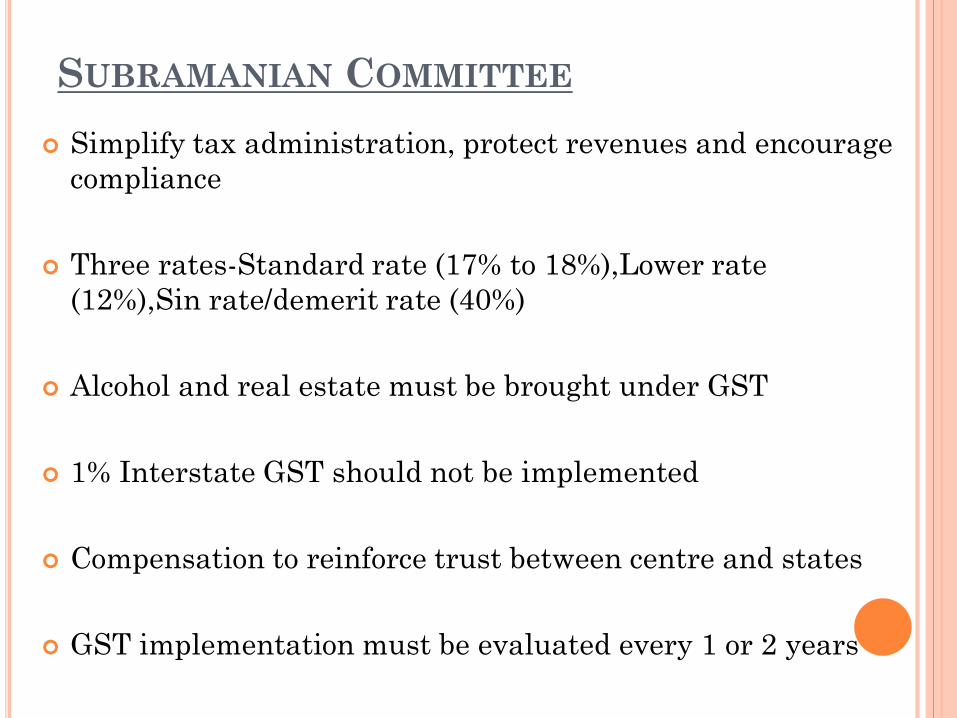

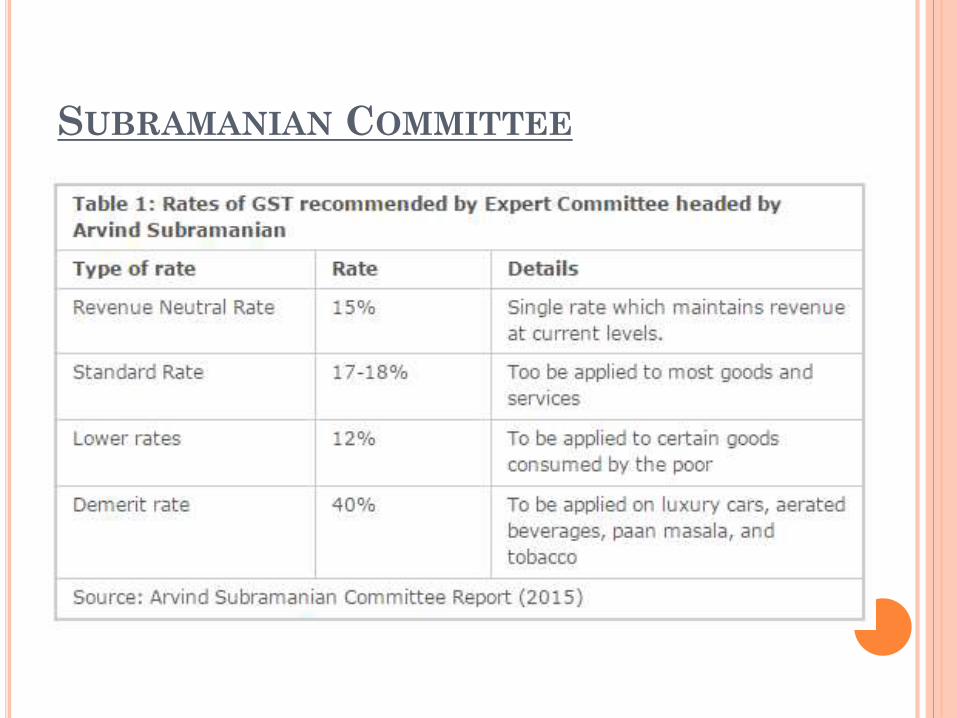

Subramanian committee

• The design of the tax must be correct hence it must simplify tax administration,

protect revenues and encourage compliance

• Three rates-Standard rate (17% to 18%),Lower rate (12%),Sin rate/demerit rate

(40%) . over a period India must impose a single tax that would increase the

simplification and compliance

• The exemption of the goods and services under GST will lead to market

distortions and increased standard rate, hence the exemption list must be very

narrow and consist of the goods and services consumed by the poor. Hence

alcohol, real estate etc must be brought under GST

• The tax base of the central government must be the same as that of the state

government (as central government exempts around 300 goods whereas the

state governments exempt only 90 goods)

• 1% Interstate GST should not be implemented as it will prohibit formation of

national market

• The shift to new tax regime may not lead to huge losses of the states, hence fair

and timely compensation must be provided by the centre to reinforce trust

between centre and states

• GST implementation must be evaluated every 1 or 2 years

Hurdles in implementing GST in India

• Deciding the tax rate (there is a huge debate going on regarding this and the FM

has said it would be decided by the GST council)

• Inflationary pressures

• Promoting the adoption amongst the small companies

• Training tax collectors (as per one of the estimates there is a need to train 60000

tax collectors), IT backbone, bringing the companies up to speed

• Deciding the threshold (annual turnover of the company beyond which the GST

will be applicable-Centre and some states are vying for Rs 25 lakh whereas others

want it to be Rs 10 lakh)

• GSTN (GST Network)- it’s a SPV formed by the government wherein the central

government and the state governments hold 24.5% stake each and remaining

51% is held by the private companies HDFC Bank, HDFC Ltd, ICICI Bank, NSE

Strategic Investment Corporation and LIC Housing Finance (some of them have a

significant of foreign holding). The argument is that the tax information is very

sensitive and should completely come under the control of the government. The

GSTN provides the IT framework/backbone for the implementation of the GST.

GSTN will be set up as a section 25 company and its functions will involve

o Common IT infrastructure to central & state governments, tax payers and

other stakeholders

o Back end services to be provided to the state/central tax department

Global Experience of GST implementation

• The rationalization of tax rates has been the biggest hurdle in various countries.

The only country which has successfully implemented dual GST with rationalized

rates is Canada which varied the tax rates many a times even after the

implementation.

• In some of the cases it has been observed that the implementation of GST has led

to inflationary spikes (in 1994, when GST was introduced in Singapore, it led to

inflation)

• Difficult to make the businesses comply with new tax regime. It was observed in

Malaysia that there was a huge resentment from the business community to

adapt a new tax regime even after giving more than 1.5 years. With very less time

remaining in India (to be implemented from 1st April 2017) it makes the task

more challenging (in Malaysia, sector specific papers regarding practices were

published which provided a smooth passage)

• The infrastructure, training etc. if not implemented well enough could lead to

problems with small, medium enterprises, delay input credits etc.

• Has been regressive in some instances i.e. it has more impact on the poor rather

than rich

Recent Initiatives

➢ TPRU and TPC

The Tax Administration Reforms Council (TARC) which was headed by

Parthasarathi Shome has made the following observations

o In the present scenario there are multiple bodies which give

recommendations-CBDT, CBEC

o The revenue secretary is not a tax expert but takes the call regarding these

taxes

o There is a lack of co-operation between CBDT and CBEC; and the selection

of members is based on seniority not on expertise

o India has one of the highest number of disputes and lowest rate of

recovery of tax arrears

o There’s absence of research based policy and impact assessment studies;

and ICT benefits have not been reaped

Hence the TARC has given the following recommendations

o The Pre-filing of tax returns must be made available to all the individuals

o CBDT and CBEC must be integrated in the next 10 years

o Post of Revenue Secretary must be abolished and the functions must be

allocated to two boards

Governing Council – to oversee the functioning of the two boards

Tax Council – to suggest policy and legislation

o There should be focus on specialization

o Retrospective legislation should be avoided

o Both the boards must start a drive to liquidate the current the current

cases

The Ministry of Finance announced the formation of the Tax Policy Research Unit

(TPRU) and the Tax Policy Council (TPC) on February 2, 2016

TPRU – Tax Policy Research Unit

o Functions

• Conduct studies on issues of fiscal and tax policies referred to it by CBDT and CBEC and will provide independent analysis of such issues

• Will prepare and disseminate policy papers and background papers on various tax policy issues

• To assist Tax Policy Council chaired by FM in taking appropriate tax policy decisions

• To co-operate with State Commercial Tax Departments. Tax Policy Council

o The Tax Policy Council will look at all the research findings coming from Tax Policy Research (TPRU) Unit and suggest broad policy measures for taxation.

o The Council will be advisory in nature, which will help the Government in identifying key policy decisions for taxation.

o Tax Policy Council under the Union Finance Minister with 9 other members will be constituted

SHYAM S KAGGOD

(ECONOMICS FACULTY-BYJU’S)

POINTS TO BE COVERED

Taxation-concept

Types of taxation systems

Some concepts-GST, Capital gains tax, cess etc

Problems with Indian Taxation System

Progressive & Regressive

Direct & Indirect

Advalorem & Specific

Tax avoidance and Tax evasion

Surcharge & Cess

Countervailing & Antidumping

Types of Taxation Systems

SOME OF THE CONCEPTS

Service tax

VAT

Presumptive Taxation

GAAR

Capital Gains tax

GST

GST-CASCADING EFFECT

A B CSelling

Price=₹ 100Selling

Price=₹ 130

Tax @ 10%

Will buy it

at ₹ 110 &

adds profit

of ₹ 20Tax @ 10%

Will buy it

at ₹ 143

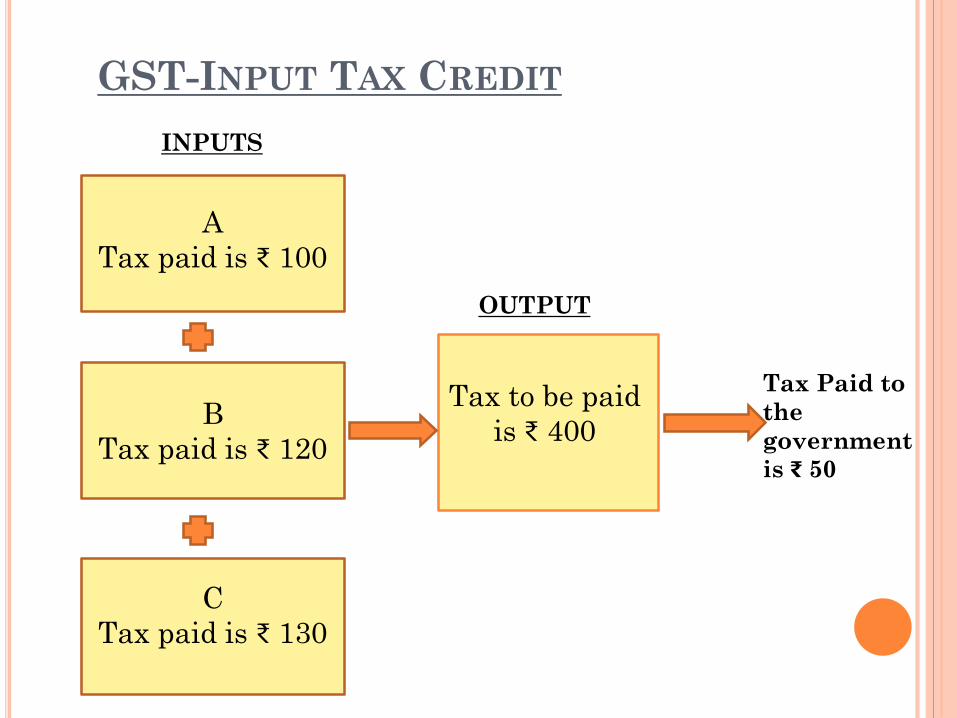

GST-INPUT TAX CREDIT

A

Tax paid is ₹ 100

B

Tax paid is ₹ 120

C

Tax paid is ₹ 130

Tax to be paid

is ₹ 400

INPUTS

OUTPUT

Tax Paid to

the

government

is ₹ 50

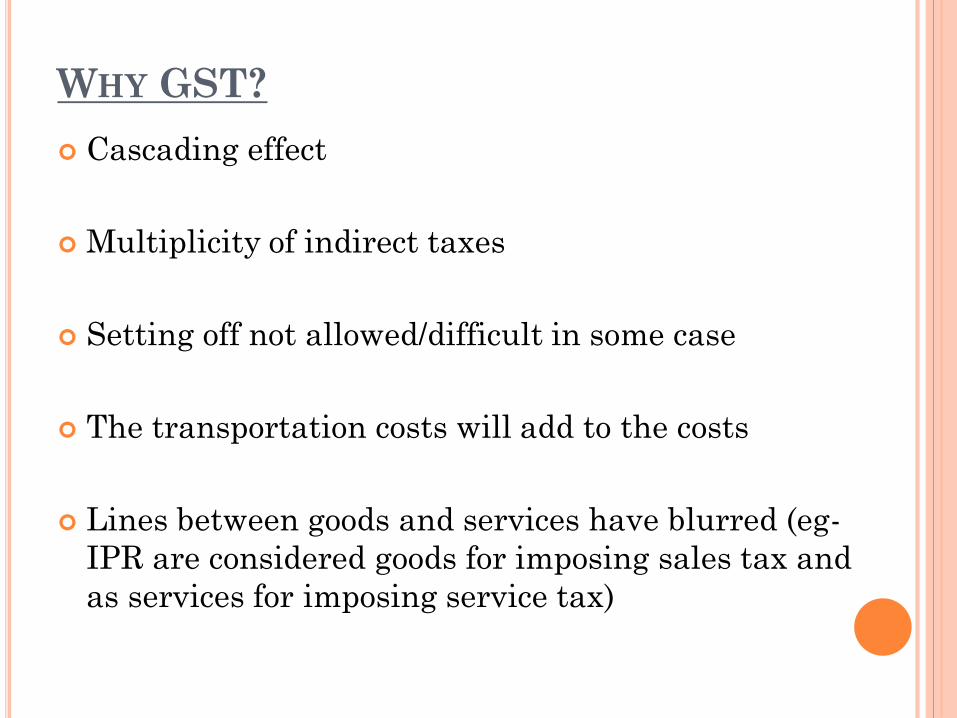

WHY GST?

Cascading effect

Multiplicity of indirect taxes

Setting off not allowed/difficult in some case

The transportation costs will add to the costs

Lines between goods and services have blurred (eg-

IPR are considered goods for imposing sales tax and

as services for imposing service tax)

GST

Streamlining/subsuming all the indirect taxes-

one nation one indirect tax

First introduced in 2011 and again in December

2014

115th CAB and 122nd CAB

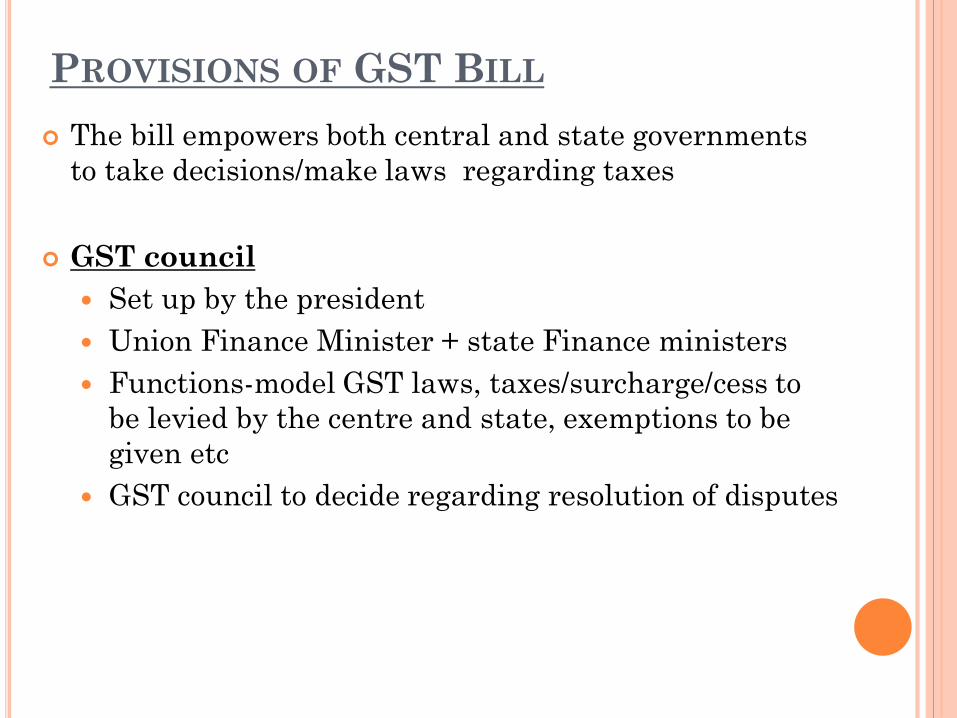

PROVISIONS OF GST BILL

The bill empowers both central and state governments

to take decisions/make laws regarding taxes

GST council

Set up by the president

Union Finance Minister + state Finance ministers

Functions-model GST laws, taxes/surcharge/cess to

be levied by the centre and state, exemptions to be

given etc

GST council to decide regarding resolution of disputes

PROVISIONS OF GST BILL

PROVISIONS OF GST BILL

The additional Interstate GST will be levied by

central government (additional levy of 1%

withdrawn)

Exemption-alcoholic liquor for human

consumption, GST council to decide when to

impose taxes on crude petroleum, high speed

diesel, petrol, natural gas and Aviation Turbine

Fuel (ATF)

Compensation to be given for 5 years

GST

OLD VS NEW

Old method GST

Goods and services were taxed

separately

No differentiation between Goods

and services

Different states different tax rates Uniform tax rates across the

country

National market not possible National market can be

established

Tax on production (origin based

taxation)

Tax on consumption (target/end

based taxation)

Cascading effect No cascading effect

Many indirect taxes Only one

Setting off in some cases not allowed Setting off is allowed

GST EXAMPLE

SUBRAMANIAN COMMITTEE

Simplify tax administration, protect revenues and encourage

compliance

Three rates-Standard rate (17% to 18%),Lower rate

(12%),Sin rate/demerit rate (40%)

Alcohol and real estate must be brought under GST

1% Interstate GST should not be implemented

Compensation to reinforce trust between centre and states

GST implementation must be evaluated every 1 or 2 years

SUBRAMANIAN COMMITTEE

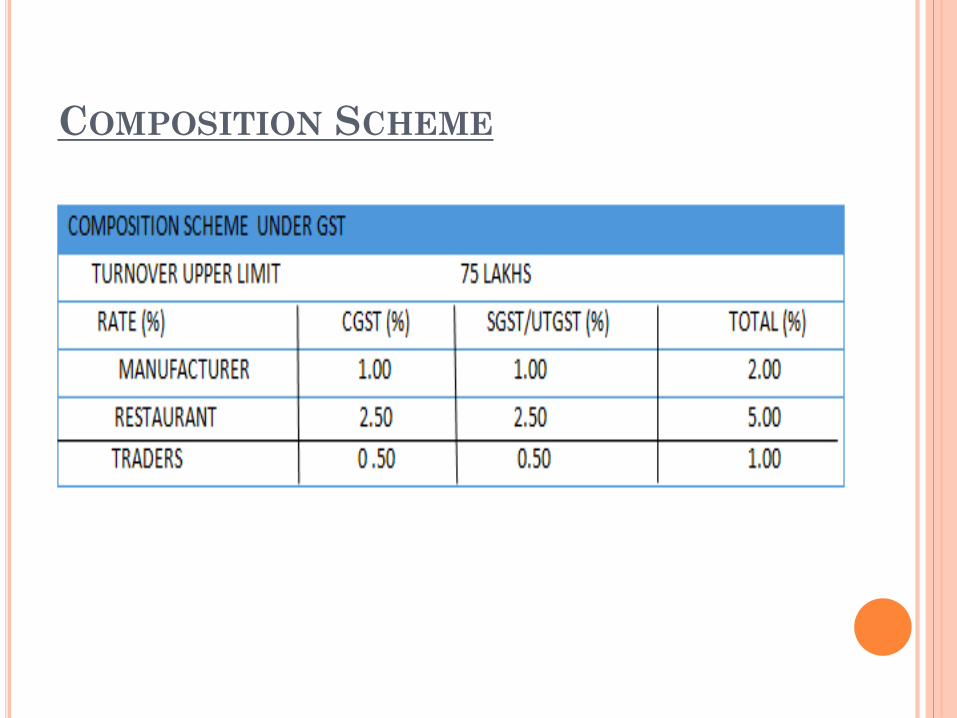

COMPOSITION SCHEME

BENEFITS OF GST IMPLEMENTATION

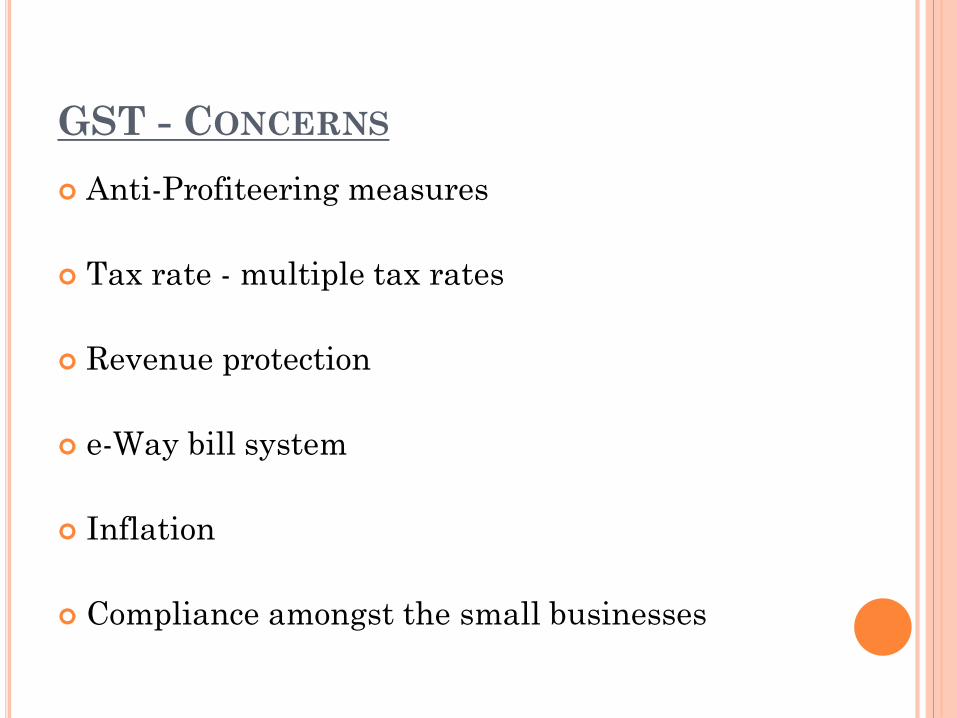

GST - CONCERNS

Anti-Profiteering measures

Tax rate - multiple tax rates

Revenue protection

e-Way bill system

Inflation

Compliance amongst the small businesses

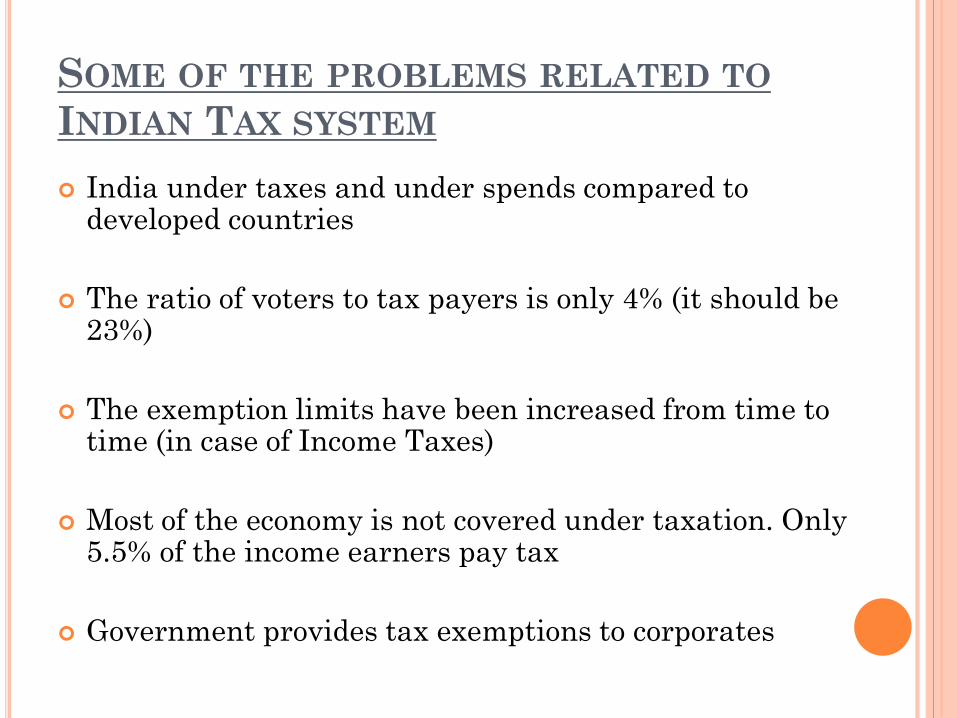

SOME OF THE PROBLEMS RELATED TO

INDIAN TAX SYSTEM

India under taxes and under spends compared to developed countries

The ratio of voters to tax payers is only 4% (it should be 23%)

The exemption limits have been increased from time to time (in case of Income Taxes)

Most of the economy is not covered under taxation. Only 5.5% of the income earners pay tax

Government provides tax exemptions to corporates

EXEMPTION LIMIT

STEPS TO BE TAKEN BY GOI

To refrain from raising exemption thresholds

Reducing corruption

Subsidies for the well-off need to be scaled back

Property tax needs to be developed

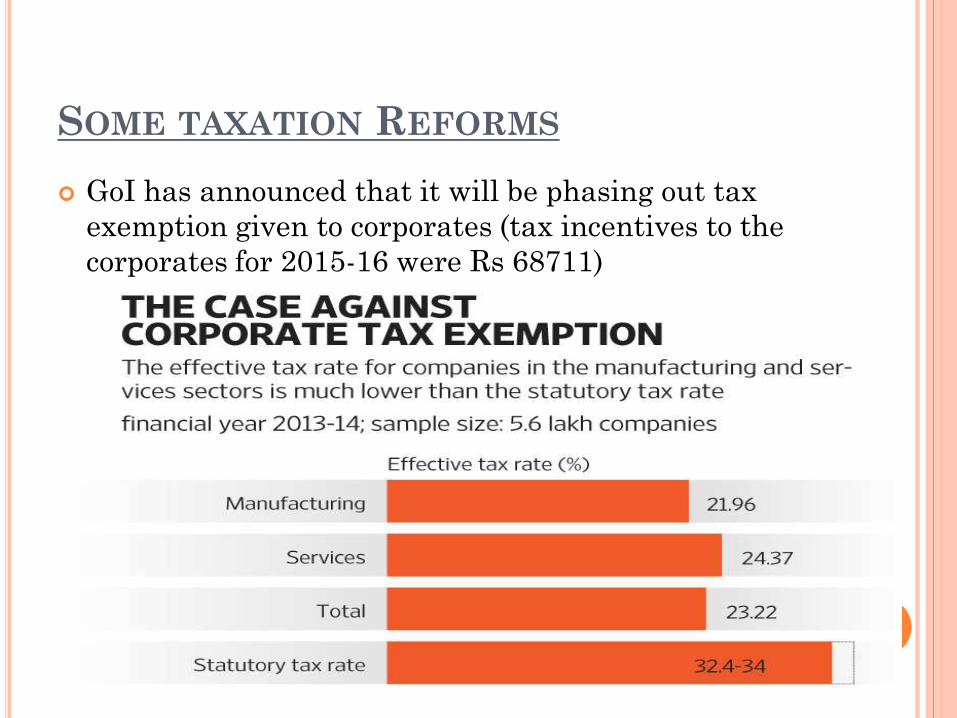

SOME TAXATION REFORMS

GoI has announced that it will be phasing out tax

exemption given to corporates (tax incentives to the

corporates for 2015-16 were Rs 68711)

SOME TAXATION REFORMS

Recommendations of R V Easwar committee report to be implemented

Computerization of IT department work

The tax refunds must be provided faster and in case of delays the beneficiary has to be incentivized

Treat stock trading returns up to Rs 5 lakh as capital gains and not as business income

TDS rates for individuals must be reduced from 10% to 5%

GST reform

GAAR reform

QUESTIONS

Which one of the following is not a feature of “Value Added Tax”? (2011)

(a) It is a multi-point destination-based system of taxation

(b) It is a tax levied on value addition at each stage of transaction in the production-distribution chain

(c) It is a tax on the final consumption of goods or services and must ultimately be borne by the consumer

(d) It is basically a subject of the Central Government and the State Governments are only a facilitator for its successful implementation

QUESTIONS

The sales tax you pay while purchasing a

toothpaste is a

(a) tax imposed by the Central Government.

(b) tax imposed by the Central Government but

collected by the State Government

(c) tax imposed by the State Government but

collected by the Central Government

(d) tax imposed and collected by the State

Government

QUESTIONS

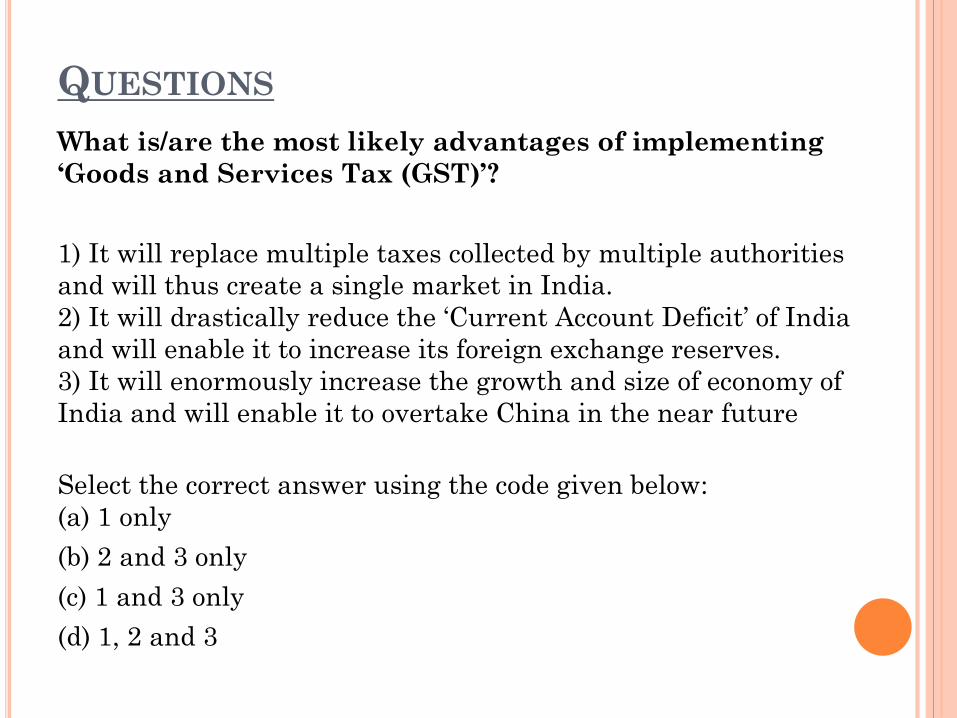

What is/are the most likely advantages of implementing

‘Goods and Services Tax (GST)’?

1) It will replace multiple taxes collected by multiple authorities

and will thus create a single market in India.

2) It will drastically reduce the ‘Current Account Deficit’ of India

and will enable it to increase its foreign exchange reserves.

3) It will enormously increase the growth and size of economy of

India and will enable it to overtake China in the near future

Select the correct answer using the code given below:

(a) 1 only

(b) 2 and 3 only

(c) 1 and 3 only

(d) 1, 2 and 3

QUESTIONS

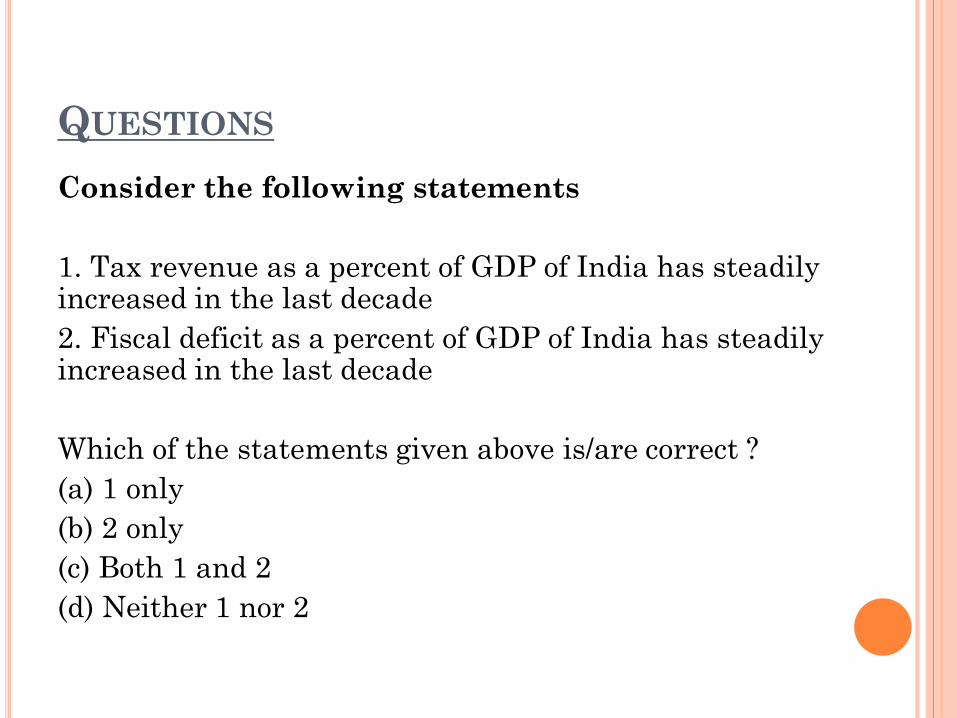

Consider the following statements

1. Tax revenue as a percent of GDP of India has steadily increased in the last decade

2. Fiscal deficit as a percent of GDP of India has steadily increased in the last decade

Which of the statements given above is/are correct ?

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

QUESTIONS (200 WORDS)

Discuss the recommendations of Subramanian

Committee on GST

Discuss the recent initiatives of the Indian

government in the taxation segment

‘GST is not the panacea for all the ills of Indian

Economy’ –critically evaluate

GST regime represents an improvement in form as

well as substance compared to previous tax regime-

![GENERAL PROVISIONS [s.141] CENVAT/VAT CREDIT INPUT CREDIT ...](https://static.documents.pub/doc/80x56/61fc1d913698cc76b03fd6f6/general-provisions-s141-cenvatvat-credit-input-credit-.jpg)

![Cenvat Accounting[1]](https://static.documents.pub/doc/80x56/54193e3a7bef0a05088b4642/cenvat-accounting1.jpg)