Introduction The amount of tax charged against profit in any period is, as we will see in Chapter 26, an important determinate of earnings per share and thus the price earnings (PE) ratio. Unfor- tunately, the tax charge calculated under revenue law is not simply a matter of computing a given rate of accounting profits, as taxable profits defined by revenue law are not the same as accounting profits assessed in accordance with the Companies Act and SSAPs/FRSs. We also must consider the effect of value added tax on company accounts. Value added tax SSAP 5 relating to accounting for value added tax (VAT) is completely uncontroversial and is of passing interest only. The central requirements are that: 1 turnover in the P&L account should exclude VAT 2 irrecoverable VAT on fixed asset acquisition should be included with the cost of the asset; and 3 the net debit or credit carried in the balance sheet need not be separately disclosed. Taxation (SSAPs 5 and 15 and FRSs 16 and 19) After reading this chapter you should be able to: ■ describe the requirements of SSAP 5 accounting for value added tax ■ describe the effect of the imputation tax system on accounting profits ■ describe the requirements of FRS 16 ■ explain deferred tax ■ describe the arguments for and against providing for deferred tax ■ identify several possible methods of accounting for deferred tax ■ critically examine the Accounting Standards Board’s approach ■ identify and critically appraise the requirements of FRS 19 ‘Deferred Tax’. 21

Transcript

IntroductionThe amount of tax charged against profit in any period is, as we will see in Chapter 26, animportant determinate of earnings per share and thus the price earnings (PE) ratio. Unfor-tunately, the tax charge calculated under revenue law is not simply a matter of computinga given rate of accounting profits, as taxable profits defined by revenue law are not the sameas accounting profits assessed in accordance with the Companies Act and SSAPs/FRSs.

We also must consider the effect of value added tax on company accounts.

Value added taxSSAP 5 relating to accounting for value added tax (VAT) is completely uncontroversial andis of passing interest only. The central requirements are that:

1 turnover in the P&L account should exclude VAT2 irrecoverable VAT on fixed asset acquisition should be included with the cost of the asset;

and3 the net debit or credit carried in the balance sheet need not be separately disclosed.

Taxation (SSAPs 5 and 15 and FRSs 16and 19)

After reading this chapter you should be able to:■ describe the requirements of SSAP 5 accounting for value added tax■ describe the effect of the imputation tax system on accounting profits■ describe the requirements of FRS 16■ explain deferred tax■ describe the arguments for and against providing for deferred tax■ identify several possible methods of accounting for deferred tax■ critically examine the Accounting Standards Board’s approach■ identify and critically appraise the requirements of FRS 19 ‘Deferred Tax’.

21

Corporation tax (CT)The tax levied on UK corporate profits is called corporation tax and it is generally due forpayment nine months after the end of the accounting period. This rule applies unless thecompany is designated as a large company which occurs when a company’s corporationtax profits for an accounting period are more than £1.5m. Such large companies will paytheir CT in 4 quarterly instalments as follows:

6 months and 14 days after the start of the accounting period (AP)9 months and 14 days after the start of the AP14 days after the end of the AP6 months and 14 days after the end of the AP

Activity 1

Company A and company B both have accounting periods ending 31 December 2000. CompanyA’s taxable profits are in the region of £1m and company B’s £2m. Identify the due dates, foreach company, for payment of CT.

Activity 1 FeedbackCompany B will be classed as a large company and will pay tax in 4 equal instalments on 14 July 2000, 14 October 2000, 14 January 2001, and 14 July 2001. Company A will not be classed as a large company and therefore will pay its CT on 14 October 2001.

The clear winner in cash flow terms is company A, the smaller company, in the aboveactivity. The above rules were enacted as from AP ending on or after 30 June 1999 and areas a result of the modernisation of the tax system which reached its final stages in April1999.

The old CT payment timing rules.Prior to the modernisation of the CT system companies paid their CT 9 months after the

end of the AP unless they paid dividends during the year. (Note here that the revenue , byaltering the rules, have accelerated their tax cash flows from large companies). When div-idends were paid during the year the revenue required advance instalments of a company’scorporation tax. The advance instalment was calculated as the tax credit associated to a div-idend payment and was due 14 days after the end of the quarter in which the dividend waspaid. These advance payments could be deducted, within limits, from the total corporationtax bill and the remainder, known as mainstream corporation tax, was paid under the 9month rule.

This old regime was known as the imputation tax system and, as dividends were paid bya company out of profit after tax, the revenue took the view that tax had already been deduct-ed from these dividends. Thus the dividend in the hands of the shareholder was assessedas if tax had already been deducted at basic rate and a tax credit was imputed to the divi-dend received. The result was known as franked investment income. A simple exampleexplains how this used to operate for an individual.

CORPORATION TAX (CT) 407

408 TAXATION (SSAPS 5 AND 15 AND FRSS 16 AND 19)

Example 1Company S declares and pays a dividend of £80 to shareholder A. The basic rate of incometax is 20%. If the shareholder is a basic rate taxpayer then the tax credit imputed and thetax payable by A would be as follows:

Tax credit at 20% = 1/4 × £80 = £20Amount received by A before tax = £80 + £20 = £100

–––––Tax payable by A (basic rate tax payer) £20Tax deemed to have been paid £20

–––––Tax remaining payable by A £0

–––––

If A paid tax at 40% then:

Tax payable by A (40% tax payer) £40Tax deemed to have been paid £20

–––––Tax remaining payable by A £20

–––––Of course companies could themselves be shareholders and the old rules for accountingfor the imputation tax system embodied in SSAP 8 required that:

1 The total franked investment income and a tax credit based on the current income taxrate should be disclosed in the accounts in accordance with appropriate Companies Actpresentation format

2 The tax credit thus credited to the P&L account would be debited ‘lower down’ beingincluded within the total tax charge for the year.

The following example demonstrates how this used to operate.

Example 2Company A receives a dividend of £20 000 from company B. Basic rate of income tax is20%. This would be reflected in company A’s books as follows:

Dividend received account P &L account

Cash 20 000 Tax charge 5 000 InvestmentTaxation Profit after tax 20 000 Income 25 000

The above treatment was required by SSAP 8 so as to provide consistency with otherelements of profit appearing above the taxation charge line in the P&L account as thesewere also shown gross.

Activity 2

Beta plc, accounting year end 31 March 1995, paid a dividend of £80 000 on 19 February 1995.The corporation tax assessment for the company was £158 000, and was due nine months afterthe accounting year end. Show the liabilities for tax that would have existed in the year end

CORPORATION TAX (CT) 409

accounts and the relevant ledger accounts (income tax rate 20%) under the old imputation taxsystem rules and SSAP 8.

Activity 2 feedback(ACT is advance corporation tax.)

Limit on offset of ACTOffset of ACT against corporation tax was limited to an amount equal to the current basicrate of income tax applied to taxable profits for the year. In Activity 2 if taxable profitswere £330 000 then the limit of offset would be £66 000. Excess ACT could be recoveredagainst the previous six years’ tax bills, always remembering the offset rules, or carriedforward for offset against future tax bills. This introduced the accounting problem of whetheror not this unrecovered ACT would be recovered in the future. Note what prudence shouldhave dictated here and then read on!

ACT and proposed dividendsACT was also due on proposed dividends and was therefore shown as a liability at the year-end, but this ACT could not be offset against current year’s tax only future year’s tax. Wetherefore had a debit balance appearing on the ACT recoverable account at the year-end.The question we needed to answer in respect of this debit balance was, is it an asset? Whatwould prudence have dictated?

SSAP 8 which was issued in 1974, ‘The treatment of taxation, under the imputation system in the accounts of companies’ gave us an answer to the above problem as follows:

6 For accounting purposes it is necessary to decide whether recovery of the ACTis reasonably certain and foreseeable or whether it should be written off in theprofit and loss account. If the taxable income of the year under review and theamounts available from the preceding year or years are insufficient to coverthe ACT, then recoverability of ACT will depend on the extent to which incomeis earned in future periods in excess of dividends paid or on the existence ofa deferred taxation account of adequate size. Although the relief remains avail-able indefinitely it will be prudent to have regard only to the immediate andforeseeable future; how long this future period should be will depend uponthe circumstances of each case, but it is suggested that where there is nodeferred taxation account it should normally not extend beyond the nextaccounting period.

8 Any irrecoverable ACT (i.e. ACT the recoverability of which is not reason-ably certain and foreseeable) should be written off in the profit and loss accountin which the related dividend is shown.

Accounting treatment of irrecoverable ACTSSAP 8 states:

9 There are two differing views on the presentation in the profit and loss accountof irrecoverable ACT written off. One view is that irrecoverable ACT shouldbe treated as part of the tax charge upon the company to be deducted in arriv-ing at profits after tax: the other that the irrecoverable ACT, being a cost stem-ming from the payment of a dividend, should be treated as an appropriationlike the dividend itself. Of the two methods the first is supported as the appro-priate accounting treatment because unrelieved ACT constitutes tax upon thecompany or group, as opposed to tax on the shareholders, and is not an appro-priation of profits. It is appreciated however that some readers or analysts ofaccounts may wish for their purposes to regard irrecoverable ACT in someother manner. The amount of irrecoverable ACT should therefore be separatelydisclosed if material.

Thus, the irrecoverable ACT affected the profit after tax figure and therefore earningsper share (eps).

Another twistThe imputation tax system allowed companies to reduce the ACT payable by the amountof tax credit on franked investment income (FII) received by the company if it was receivedin the same quarter as the dividend was paid. Note that this allowance did not reduce theamount of the tax bill in any way just the timing of payments. However, consider the fol-lowing activity.

410 TAXATION (SSAPS 5 AND 15 AND FRSS 16 AND 19)

Activity 3

A company proposes a dividend of £28 000 at the accounting year-end, 31 March 1996, whenthe income tax rate is 20%. The company expects to receive dividends of £8000 from one ofits investments on 2 May 1996. Which liability should the company have shown in its year-endaccounts – £7000 or £5000?

Activity 3 feedbackACT payable is 1/4 × £28 000 = £7000 which is due in less than one year and would there-fore appear as a liability on the balance sheet.

However, if investment dividend is received on 2 May 1996 then a tax credit of £2000would have occurred and the company paid ACT of £5000. The liability eventually paidwas thus £5000, but the liability which prudence and SSAPs (particularly SSAP 17) dic-tates we should declare was £7000. Strange how some companies actually reported onlythe £5000 as a liability!

We make no apology for working through the old regime of corporation tax and ACT asyou will need to understand this when we come to the issue of transitional arrangementsunder the new regime.

The new tax credit rulesAlthough ACT has now been abolished shareholders will still receive a tax credit on theirdividend income. From the 6 April 1999 the tax credit is 10% of the gross dividend anddividends will only be taxable for companies who hold investments as trading assets andfor individuals paying high rate tax.

Activity 4

Alpine plc has taxable profits for the year ended 31.12.X1 of £3 000 000. Corporation tax rateis 30%. Alpine paid a dividend of £500 000 on 31.5.X1.

Calculate the tax payable and the tax payments under the previous regime, assuming ACT is1/4 for the year in question, and under the new regime.

Activity 4 FeedbackPrevious regime;

Total tax payable is £3 000 000 × 30% = £900 000. ACT on dividend is £500 000 × 25%= £125 000. Payments are £125 000 July X1 and £775 000 September X2.

New regime;Total tax payable is still £900 000 but payments are now £225 000 July X1, £225 000

October X1, £225 000 January X2 and £225 000 April X2. Note Alpine is classed as a largecompany.

ACCOUNTING TREATMENT OF IRRECOVERABLE ACT 411

FRS 16 current taxIn December 1999 the ASB finally withdrew SSAP 8, which was based upon the old taxsystem, by the issue of FRS 16. This deals with accounting for tax under the new tax regime with the exception of deferred tax which we will deal with later in this chapter. The new tax regime, by abolishing ACT, made accounting for tax much simpler but transitional arrangements were required for the move from one tax regime to the other and the problem of how to deal with tax credits on dividends received still needed resolving.

Transitional arrangementsThese are identified in an appendix to FRS 16 and are essentially a shadow ACT system.The shadow system is designed to ensure that ACT c/f after April 1999 is recovered onlyif it would have been recovered had the ACT system still existed. It was estimated that therewas approximately £7bn surplus ACT still awaiting recovery when the legislation waschanged. All of this £7bn will now be subject to the shadow arrangements which will allowoffset against future tax bills (and actually reduce the tax bill) but only up to the amountthat could have been offset if ACT had continued.

Activity 5

Apex plc has surplus ACT of £100 000 and taxable profits for the year ended 31.3.2000 of £250 000. It pays a dividend at the year end of £60 000 and received at that time a dividend of £16 000. Corporation tax rate is 30% and income tax rate 20%, implying an ACT rate of 25%. Identify the ACT set-off possible under the transitional arrangements ofFRS 16.

Activity 5 FeedbackIf ACT still applied Apex plc would be liable to pay in ACT

25% × £60 000 – tax credit on dividends received of 25% × £16 000 = £11 000

Maximum offset of ACT would have been

20% × £250 000 = £50 000

New regulations CT liability of Apex plc year ended 31.3.2000 is

30% × 250 000 = £75 000

ACT set off possibleMaximum offset available £50 000Shadow ACT 11 000

–––––––––Therefore surplus to be set off is 39 000 (of £100 000 total surplus)

––––––––––––––––––Actual MCT payable for the year is 75 000 − 39 000 = £36 000

––––––––––––––––––––––––––––––––––Surplus ACT c/f is £61 000 (100 000 − 39 000) and this can be offset in future years.

412 TAXATION (SSAPS 5 AND 15 AND FRSS 16 AND 19)

FRS 16 CURRENT TAX 413

The treatment of tax creditsUnder SSAP 8 dividends received were grossed up by their tax credit and shown as incomein the P&L account and the tax credit was shown as a deduction from the P&L accountunder the tax charge element. We saw this at example 2 earlier. The change in the tax reg-ulation now requires that this method of accounting be reviewed as the majority of com-panies will no longer be able to recover the tax credit.

FRS 16 provides us with the following definitions:

Tax credit ‘The tax credit given under UK tax legislation to the recipient of a div-idend from a UK company. The credit is given to acknowledge that the incomeout of which the dividend has been paid has already been charged to tax, ratherthan because any withholding tax has been deducted at source. The tax credit maydischarge or reduce the recipient’s liability to tax on the dividend. Non-taxpay-ers may or may not be able to recover the tax credit.’

Withholding tax ‘Tax on dividends or other income that is deducted by the payer of the income and paid to the tax authorities wholly on behalf on therecipient.’

There are three essential differences between tax credits and withholding tax:

■ Withholding (WH) tax is a tax that has actually been paid by the recipient (or at leastpaid on his behalf).

■ Income on which withholding tax has been suffered is treated as taxable and subject tofurther tax unless the amount of withholding tax is sufficient to discharge the liability;whereas in many circumstances no further tax is payable on dividends received with atax credit. This dividend is treated as non-taxable income.

■ The amount at which the dividend is measured, if it is subject to further tax, is the amount of the cash dividend received i.e. without the tax credit whereas income (divi-dend) subject to withholding tax is taxed on the amount received plus the withholdingtax.

FRS 16 requires that ‘Outgoing dividends paid and proposed, interest and other amountspayable should be recognized at an amount that:

(a) includes any withholding taxes; but(b) excludes any other taxes, such as attributable tax credits, not payable wholly on behalf

of the recipient. (para. 8 FRS 16) and

Incoming dividends, interest or other income receivable should be recognized at anamount that:

(a) includes any withholding taxes; but(b) excludes any other taxes, such as attributable tax credits, not payable wholly on behalf

of the recipient. (para. 9 FRS 16).

In addition the FRS also ensures that tax is correctly attributed between the P&L accountand the STRGL as follows:

Current tax should be recognized in the profit and loss account for the period,except to the extent that it is attributable to a gain or loss that is or has beenrecognized directly in the STRGL. (para. 5 FRS 16)

414 TAXATION (SSAPS 5 AND 15 AND FRSS 16 AND 19)

Where a gain or loss is or has been recognized directly in the statement of total recog-nized gains and losses, the tax attributable to that gain or loss should also be recognizeddirectly in that statement.’ (para. 6 FRS 16)

Measurement of taxFRS 16 requires that current tax should be measured at the amounts expected to be paid (or recovered) using the tax rates and laws that have been enacted or substantially enactedby the balance sheet date (para 14 FRS 16). Substantially enacted is where a Bill has beenpassed through the House of Commons and is awaiting House of Lords approval etc. at thebalance sheet date or a resolution having statutory effect that has been passed under theProvisional Collection of Taxes Act 1968. This brings FRS 16 in line with IAS 12 IncomeTaxes.

Activity 6

The following information is available for Beta plc for the year ended 30.9 2000.

Accounting profit before taking account of dividends received or paid/proposed is £1 500 000.Corporation tax due for the year ended 30.9.2000 is £520 000 (before taking effect of any

tax paid on the company’s behalf) which includes tax of £35 000 attributable to a gain recog-nized in the STRGL.

Dividends paid (cash) and proposed (cash) amount to £54 000 and £27 000 respectively andboth were subject to withholding tax of 10%. They also have attributable tax credits of £15 000and £7500 respectively.

The company received dividends (cash) of £72 000. These had been subject to withholdingtax of 10% and have an attributable tax credit of £20 000.

The company is aware that the corporation tax rate may change from that used in the cal-culations above and before the due date of payment of the tax and asks for advice on how todeal with this.

Show the profit and loss account for the period ended 30.9.2000 as far as the above infor-mation permits and advise the company in respect of the change in tax rate.

Activity 6 FeedbackAbridged profit and loss account for the period ended 30.9.2000 for Beta plc

£000 £000Accounting profit before dividends 1500Dividends received (gross up for WH tax but not tax credit) 80

Dividends paid (grossed up for WH tax) 60Dividends proposed (but not tax credit) 30 90

––––––1013––––––––––––

DEFERRED TAXATION 415

Note 1:The £35 000 tax due on the gain recognized in the STRGL will also be recognized in theSTRGL. The £8000 withholding tax has been paid on behalf of the recipient company andwill be deducted from the CT due as given as the figure was calculated before taking accountof this.

The possibility of the change in tax rate will not be actioned by the company as FRS 16requires that current tax should be measured at the amounts expected to be paid using thetax rates and laws that have been enacted or substantively enacted by the balance sheet date.Neither enaction or substantive enaction by the balance sheet date of 30.9.2000 is suggestedby the information given above.

Disclosure requirements of FRS 16These are quite straightforward and require a company to disclose UK or Republic of Irelandtax and foreign tax separately both for the P&L account and the STRGL.

Deferred taxationIntroductionIn the UK the amount of tax payable by a business for a particular period often bears lit-tle relationship to profit as reported by the accountants in the P&L account. The tax author-ities (the Inland Revenue) take the accountant’s reported profit figure as their starting point,but they make all sorts of adjustments to it. These adjustments are presented by Parliamentin the Finance Acts. There is at least one Finance Act each year, sometimes two. Thisprocess enables Parliament to make fairly rapid changes (and often extremely frequentchanges). The separation of taxable profit from accounting profit also means that Parliamentcan pursue its objectives (whatever they are!) without treading on the accountants’ toes,and similarly the accountants can pursue their true and fair view unhindered by tax legis-lation. This separation, although common in the English-speaking world, is by no meansuniversal. Much of mainland Europe, for example, requires tax adjustments to be incorpo-rated in the published accounts.

The most important difference between the accountant’s profit and the taxable profit con-cerns the treatment of depreciation. As we have seen (Chapter 16) the ‘appropriate’ chargefor depreciation is a highly uncertain, subjective, amount. This would be unacceptable tothe Revenue, who requires certainty and precision. Additionally governments have fre-quently felt that by varying the tax allowances, they can provide incentives to businessesto invest more, or to invest in some particular way. So the first thing that the Revenue doesto the accountant’s profit figure, as calculated and published, is to remove all the depreci-ation entries put in by the accountant. In other words the depreciation figure, which willhave been deducted in arriving at the accountant’s profit figure, is simply added back again(a profit on disposal that will have been added by the accountant will of course need to beremoved by deduction). From the resulting figure the Revenue now deducts whatever theappropriate Finance Act tells them to, under the heading of ‘capital allowances’. The impli-cations arising from this have led to a long, complicated and sometimes badly argued debateover the last three decades.

416 TAXATION (SSAPS 5 AND 15 AND FRSS 16 AND 19)

What is deferred tax?First let us look at the difference between taxable profits and accounting profits.

Activity 7

An asset attracting 25% capital allowances per annum costs Deftax Ltd £100. It has an expect-ed life of five years at the end of which it is estimated it can be sold for £25. Taxation is payableat the rate of 33%. Complete the following table (note that capital allowances apply to thereducing balance of the asset).

Year1 2 3 4 5£ £ £ £ £

accounting profit (after depreciation charge) 100 100 100 100 100depreciation capital allowancetaxable profitprofit before taxtaxation 33% taxable profitprofit after taxprofit before taxtaxation charge calculatedon accounting profitsprofit after accounting tax

profit before tax 100 100 100 100 100taxation charge if calculated on accounting profit 33 33 33 33 33

profit after accounting tax 67 67 67 67 67

The profit after tax figures, which are used for the eps and PE ratio (see Chapter 26) wouldindicate that in year 2 the performance of the company decreased and continued to do sofor the next three years. But has the firm and the management been less successful?Arguably not! Over the five-year period the company has made the same accounting prof-it with the same resources each year (excluding the problems of historical cost here). Thus,the profit after accounting tax figures provides a better guide to performance of the company.

If we look carefully at the above table we note that the total tax charge is £165 over thefive-year period using either method. Thus the use of capital allowances does not alter thetotal tax due, only the timing of those tax payments. The capital allowance has the effectof deferring tax payments in year 1, £3 and year 2, £1, and then collecting these in year 4and 5.

So we have an eventual payment that relates to year 1 and 2 and arises as a result of thetransactions and results of years 1 and 2 and it is therefore arguable that there is a liabili-ty created at year 1 and increased at year 2. We are in effect suggesting that:

1 The tax charge for year 1 and year 2 should really be £33, as this is the amount thatmust eventually be paid as a result of the year 1 and 2 activities.

2 There is a liability of £3 at the end of year 1, in respect of tax related to year 1 but payablein later years which increases to £4 by the end of year 2.

We can easily allow for both these considerations by creating a liability account, knownas a deferred tax account. This is shown in the table below. The amount to be transferredto the credit of the deferred tax account can be formally calculated as follows.

Amount equals:

Tax rate × (capital allowances given – depreciation disallowed)

For year 4 and year 533% × (11 − 15) = −1 33% × (8 − 15) = −3

So the transfer for year 4 is a debit to deferred tax account of £1 (or in effect, a credit of −£1, if you find that easier to see), and a credit of £1 to the appropriation account. For year5 we have a debit to deferred tax account of £3 and a credit of £3 to the appropriationaccount.

Arguments for deferred taxFrom the above discussion we can note that:

1 The tax charge by including deferred tax is £67 for years 1–5, which provides a profitafter tax figure which reflects the performance of the company.

2 There is a liability balance remaining at the end of each year in respect of tax related tothe current or earlier years but not yet paid or due for payment. This, we also suggest-ed, was a desirable outcome.

3 The total position viewed over the five years as a whole remains unaltered. This is to beexpected as nothing we are doing, and also nothing that Parliament is doing, throughcapital allowances, alters the total tax eventually payable as a result of a year’s profits.

All the above appears totally logical and in accord with accounting principles. So whereis the problem?

Arguments against deferred taxA problem occurs with the previous logic if a company buys assets regularly, which is arealistic assumption as companies tend to become more capital intensive. Let us demon-strate the problem with an activity.

418 TAXATION (SSAPS 5 AND 15 AND FRSS 16 AND 19)

ARGUMENTS AGAINST DEFERRED TAX 419

Activity 8

In addition to the information given in Activity 7 Deftax Ltd buys an asset in year 2 for £100, onein year 3 for £120 and one in year 4 for £220 and two in year 5 for £250 and £300, respectively.All these assets also have an expected life of five years, but unlike the first asset, all these laterones have an expected scrap value of zero. Complete the table in Activity 7 using the new infor-mation and show the deferred tax account over the five-year period. Comment upon the results.

To help you with the above activity we provide the workings for years 2 and 3 for the cal-culation of depreciation and capital allowances. Years 4 and 5 follow the same pattern.

Comparing the tables from Activities 7 and 8 we see that the total position over the fiveyears is no longer the same. The total tax charge is increased by £8. This is not surprising,as it equals the liability provided for at the end of year 5 on the deferred tax account. Thetransfer to the deferred tax account can be seen to be the result of an amalgam of positiveoriginating timing differences relating to depreciation. The resultant figure of profit aftertax, £67 per annum, reflects the underlying profitability of the company. It does not givean impression of improved profitability because of the effect of tax allowances related toasset acquisitions. Everything appears fine so where is the problem? The problem is the £8remaining on the deferred tax account. Does this liability actually exist?

In the long term we can suggest that:

1 If the company reaches the state where it has a constant volume of fixed assets, merelyreplacing its existing assets as they wear out, and also the price it has to pay for replace-ment fixed assets does not rise over time, then the balance of liability on the deferredtax account will remain a more or less constant figure.

2 If the company finds that it is effectively in the position of paying gradually more andmore money for fixed assets each year, then the balance of liability on the deferred taxaccount will gradually rise, apparently without limit.

3 Only if the monetary amount of reinvestment in fixed assets actually falls will the bal-ance of liability on the deferred tax account start to fall.

How likely is each of these three outcomes? In general 2 will tend to be the most fre-quent for three reasons:

1 firms have a tendency to expand2 firms have a tendency to become more capital intensive

420 TAXATION (SSAPS 5 AND 15 AND FRSS 16 AND 19)

3 inflationary pressures tend to cause the amount of money paid for assets to increase overtime.

So the most likely outcome, if full provision is to be made for deferred tax in this way,is of a liability figure on the balance sheet that is apparently ever-increasing. But what is aliability? Informally, we can say that it is an amount to be paid out in the future. We havean account representing a liability to the Inland Revenue. The balance on this account isgradually getting bigger and bigger and, as far as can reasonably be foreseen, this processis going to continue. Therefore the liability balance does not seem to be getting paid, nor,in the foreseeable future is it likely to be paid. Therefore it appears that it is not a liabilityat all within the meaning of the word liability! If the liability account seems all set to keepon growing, is there a probable future sacrifice?

It should be observed that one way of summarizing the two arguments as regards the lia-bility aspect is that we can consider the position for each individual asset, or we can con-sider the position for all assets in the aggregate. In the former case the tax ‘deferred’ willall have become payable by the end of the asset’s life, so deferred tax provision would seemto be necessary. In the latter case the aggregate liability is likely to go on increasing sodeferred tax provision would seem to be unnecessary.

The accountants’ responseFormally, three approaches have been distinguished:

1 The flow-through approach, which accounts only for that tax payable in respect of theperiod in question, i.e. timing differences are ignored.

2 Full deferral, which accounts for the full tax effects of timing differences, i.e. tax isshown in the published accounts based on the full accounting profit, and the elementnot immediately payable is recorded as a liability until reversal.

3 Partial deferral, which accounts only for those timing differences where reversal is like-ly to occur in aggregate terms (because, for example, replacement of assets and expan-sion is expected to exceed depreciation).

These alternatives are discussed and explained in the following activities.

Activity 9

Should the flow through approach be identified as the method to be used for accounting fortax?

Activity 9 feedbackArguments in favour:

■ Tax is assessed on taxable profits not accounting profits. The only liability for tax forthe period therefore is that accordingly assessed.

■ Future years’ tax depends on future events and is therefore not a present liability (seedefinition of liability from the Statement of Principles)

THE ACCOUNTANTS’ RESPONSE 421

■ Even if current events were giving rise to future tax liabilities then, as the tax chargewill be based on a complex set of future transactions, it cannot be measured with relia-bility and therefore should not be recognized.

Arguments against:

■ As tax charges can be traced to individual transactions and events then any future taxconsequences arising from these should be provided for at the outset

■ Flow through method can understate an entity’s liability to tax.

SSAP 11 Accounting for deferred tax issued 1975 rejected flow through as did its suc-cessor SSAP 15 issued 1978 and the revised version 1985. The latest statement from theASB on the issue, FRS 19 Deferred Tax, still rejects the flow through approach.

The ASB also provides another reason for rejecting the flow through approach, ‘flowthrough accounting would not have moved the UK accounting more into line with inter-national practice’ (FRS 19 Appendix V para 21).

Activity 10

Should the full deferral method be adopted as the method to be used for accounting for tax?

Activity 10 feedbackThis was the approach recommended by the ASC in their first standard in 1975, as out-lined in paragraph 9 of SSAP 11:

The view is taken that the amount of the tax saving should not appear as a benefitof the year for which it was granted, but should be carried forward and re-cred-ited to the profit and loss account (by way of reduction of the tax charged there-in) in the year or years in which there are reversing time differences. The accountin which these deferred tax savings are held, has, by custom, become known asthe ‘deferred taxation account’.

In effect, therefore, the full unreversed element is shown as a liability.Applying this to the circumstances of Deftax Ltd, we arrive at the position in Activity

7. Thus we could well be showing a liability that will never crystallize.

Activity 11

Should partial deferral be the method adopted for accounting for tax?

Activity 11 feedbackAs we have seen, the one major problem with full deferral is that the balance on the deferredtax account is likely to increase continuously where there is expansion and replacement atincreased prices. If, however, timing differences are regarded in aggregate terms rather than

422 TAXATION (SSAPS 5 AND 15 AND FRSS 16 AND 19)

as relating to individual assets, then this could be taken as evidence that the differences werenot reversing. In short, is a liability that is never likely to become payable, a liability at all?

The ASC’s second standard on deferred tax, SSAP 15 (1978), followed this approach,as explained below:

In many businesses timing differences arising from accelerated capitalallowances are of a recurring nature, and reversing differences are themselves off-set, wholly or partially, or are exceeded, by new originating differences therebygiving rise to continuing tax reductions or the indefinite postponement of anyliability attributable to the tax benefits received. It is therefore appropriate thatin the case of accelerated capital allowances, provision be made for deferred tax-ation except in so far as the tax benefit can be expected with reasonable proba-bility to be retained in the future in consequence of recurring timing differencesof the same type.

However the successor to SSAP 15, FRS 19, rejects the partial provision method for thefollowing reasons:■ the recognition rules and anticipation of future events are subjective and inconsistent with

the principles underlying other aspects of accounting, particularly the principle thatliabilities should be determined on the basis of obligations rather than managementdecisions or intentions

■ SSAP 15 was already inconsistent at it had been amended in 1992 to account for long-term deferred tax assets associated with post-retirement benefits on a full provision basis

■ comparability between companies in the deferred tax area was reduced as similar com-panies with similar circumstances were making different judgements on the amount ofdeferred tax to be provided

■ by adopting partial provision the UK was out of step with standard setters in other coun-tries who were rejecting it, particularly the US FASB and the IASB.

Activity 12

On the assumption that the directors of Deftax Ltd foresee no reversal of timing differences forsome considerable time, and using the information from Activity 7, show the taxation effectusing the partial deferral method.

The liability for tax will never crystallize therefore no provision for deferred tax. No netreversal appears ever to be expected.

Activity 13

A company Partax Ltd acquires a fixed asset for £100 in year 1 with residual value at end ofuseful life £20 and another for £200 with nil residual value in year 5. Assuming, assets are depre-ciated using straight line and a life of five years, that profits before tax are £250 per annum,that corporation tax is 33%, assets receive a 25% capital allowance, and that after year 5 newassets will be acquired annually, show the taxation charges using partial deferral method ofprovision for the first four years.

Thereafter should be originating as assets are bought annually.

424 TAXATION (SSAPS 5 AND 15 AND FRSS 16 AND 19)

FRS 19 REQUIREMENTS 425

Reversals of 7 need to be provided for in total, thus a deferred tax provision of £2.3 isrequired at year 1 (7 × 33%). This very clearly illustrates that the deferred tax is only being‘partially’ provided for.

FRS 19 ‘Deferred tax’In December 2000 the ASB issued its new standard on deferred tax which was based onFRED 19 and the preceeding discussion paper of 1995. The discussion paper explored againthe three methods of providing for deferred tax: flow through, full provision and partial pro-vision. It argued the case for full provision in that:

■ It is consistent with international and USA standards■ It is based on the position of the entity at the balance sheet date, not on an assessment

of future transactions, but acknowledges that it can give rise to a deferred tax liabilitythat may not become payable.

However, this non-payment will be due to future transactions not past. This is consistentwith the ASB’s definition of a liability in its Statement of Principles – an obligation to trans-fer economic benefits as a result of past transactions or events.

We can also argue the case for partial provision. As partial provision provides for theprobable obligation to transfer economic benefits then this is the liability that should beshown. Any other probable, possible or remote deferred tax provision should then be dealtwith using FRS 12 Provisions, contingent liabilities and contingent assets.

The discussion paper suggested that the apparent overstatement of the deferred taxationliability could be dealt with by using discounting – a further major complication for con-sideration.

FRS 19 supersedes SSAP 15 for those accounting periods ending on or after 23 January2002 but earlier adoption, as usual, was encouraged.

FRS 19 requirementsMethod of provisionThe standard requires full provision to be made for deferred tax assets and liabilities aris-mg from timing differences between the recognition of gains and losses in the financial state-ments and their recognition in a tax computation. It clearly states in the FRS that transactionsor events that give the entity an obligation to pay more or less tax in the future must haveoccurred by the balance sheet date and this is in accordance with the ASB’s definition ofan asset or liability.

The FRS requires deferred tax to be recognized on timing differences attributable to:

■ accelerated capital allowances■ accruals for pension costs and other post-retirement benefits that will be deductible for

tax purposes only when paid■ elimination of unrealised intragroup profits on consolidation■ unrelieved tax losses■ other sources of short-term timing differences

and prohibits the recognition of deferred tax on timing differences arising when:

■ a fixed asset is revalued without there being any commitment to sell the asset■ the gain on sale of an asset is rolled over into replacement assets

■ the remittance of a subsidiary, associate or joint venture’s eamings would cause tax tobe payable, but no commitment has been made to the remittance of the earnings. (FRS19 Summary para. (b)(a and b)).

There is one interesting exception to the above requirements and that is:

As an exception to the general requirement not to recognise deferred tax on reval-uation gains and losses, the FRS requires deferred tax to be recognised whenassets are continuously revalued to fair value, with changes in fair value beingrecognised in the profit and loss account. (FRS 19 Summary para.(c))

The assets to which this paragraph applies are those that are ‘marked to market’. Thus wewould include investments and current assets here where fluctuations in value are recog-nised in the profit and loss account.

DiscountingThe FRS permits but does not require entities to adopt a policy of discounting deferred taxassets and liabilities. This is a change from FRED 19 which proposed discounting shouldbe mandatory. This optional approach to discounting could lead to a loss of comparabilitybetween companies but the ASB argued that this would not be the case as:

providing discounting was applied consistently from one period to the next, andthe impact of discounting on the financial statements was highlighted clearly therewould not be a serious loss of comparability if not all entities discounted deferredtax. (FRS 19 appendix V para 10 1(c))

We could question whether the user of the financial statements would actually understandthe discounting impact. It is also worth noting that although the ASB adopted a full pro-vision approach to deferred tax on the grounds of international harmonisation, they wereless concerned with it as far as discounting was concerned. With reference to discountingthe ASB state at appendix V para 101(b) ‘A methodology was being introduced in the UKbefore an international concensus had been reached.’ However the IASB is as part of itsproject on discounting considering whether deferred tax should be discounted.

Where a reporting entity opts for discounting of deferred tax assets and liabili-ties to reflect the time value of money then all deferred tax balances that havebeen measured by reference to undiscounted cash flows and for which the impactof discounting is material should be discounted. (FRS 19 para 44)

FRS 19 also determines the discount rate to be used:

post tax yields to maturity that could be obtained at the balance sheet date on gov-ernment bonds with maturity dates and in currencies similar to those of thedeferred tax assets and liabilities. (FRS 19 para 52)

Example 1 (adapted from appendix 1 FRS 19)Given that the original cost of fixed assets of an entity is £3300, depreciation to date £1000and capital allowances to date on fixed assets £2186, calculate the deferred tax provisionrequired under FRS 19.

426 TAXATION (SSAPS 5 AND 15 AND FRSS 16 AND 19)

Answer 1Full provision for deferred tax is required which is calculated as

30% × (2186 − 1000) = £356.

Example 2Further to the information given in Example 1 the following is available. It is assumed thatthe reversal of timing differences will occur as follows and that government bond post taxrates are as per column 4.

Year Reversal of Deferred tax Gov. bondtiming difference liability (at 30%) post tax rate (%)

Calculate the discounted deferred tax provision required under FRS 19.

Answer 2FRS 19 requires us to discount at a rate equivalent to the post tax yields to maturity thatcould be obtained at the balance sheet date on government bonds with maturity dates, andin currencies similar to those of deferred tax assets and liabilities. These we will assumeare those given in column 4 above. When discounted the deferred tax liability becomes £290(i.e. 7/(1.047)1 + 27/(1.044)2 + 43/(1.042)3 + 62/(1.04)4, etc.) The liability has in fact beendiscounted by £66.

Unwinding of the discountingThe FRS requires us to show, ‘changes in the amount of discount deducted in arriving atthe deferred tax balance’ (para. 60(a)(ii)) and in the balance sheet ‘the impact of discountingon and discounted amount of the deferred tax balance’ (para. 61(b)). Thus we need to beable to calculate the unwinding of the discounting. Using the example above and discountingthe deferred tax liabilities from the end of year 1 onwards gives a discounted deferred taxfigure of £295 compared to an undiscounted figure of £349, a discounting effect of £54.Comparing this with the discounting effect at year 0 of £66 identifies an unwinding of £12.Another way to calculate this unwinding is to multiply the discounted deferred tax liabil-ities by the bond rate again.

This £12 will be shown as an increase to the deferred tax provision due to the unwindingof the discounting.

Deferred tax assetsPara 23

Deferred tax assets should be recognised to the extent that they are regarded asrecoverable. They should be regarded as recoverable to the extent that, on the basisof all available evidence, it can be regarded as more likely than not that there willbe suitable taxable profits from which the future reversal of the underlying timingdifferences can be deducted.

Para 24

Suitable taxable profits from which the future reversal of timing differences couldbe deducted are those that are:(a) Generated in the same taxable entity (or in an entity whose profits would be avail-

able via group relief) and assessed by the same taxation authority as the incomeor expenditure giving rise to the deferred tax asset;

(b) Generated in the same period as that in which the deferred tax asset is expectedto reverse, or in a period to which a tax loss arising from the reversal of the deferredtax asset may be carried back or forward; and

(c) Of a type (such as capital or trading) from which the taxation authority allows thereversal of the timing differences to be deducted.

Recognition of deferred tax in Statements of Performance Para 34

Deferred tax should be recognised in the profit and loss account for the period,except to the extent that it is attributable to a gain or loss that is or has been recog-nised directly in the statement of total recognised gains and losses.

428 TAXATION (SSAPS 5 AND 15 AND FRSS 16 AND 19)

Para 35

Where a gain or loss is or has been recognised directly in the statement of totalrecognised gains and losses, deferred tax attributable to that gain or loss shouldalso be recognised directly in that statement.

Measurement of deferred tax Para 37

Deferred tax should be measured at the average tax rates that are expected to applyin the period in which the timing differences are expected to reverse, based ontax rates and laws that have been enacted or substantially enacted by the balancesheet date. This follows FRS 16 and the liability method of providing for deferredtax as discussed below.

The deferred tax amount is dependent on the tax rate used. When calculating the amountwe could either use:

■ the tax rate applying when the timing difference originated – deferral method■ or the tax rate (or the best estimate of it) ruling when the tax will become payable – lia-

bility method.

A simple example is used to illustrate the difference.

Example 3An enterprise purchases a non-current asset for £5 000 000 on 1.1.20X0. It is depreciatedon a straight line basis over five years. It attracts tax allowances of £200 000 in 20X0 and£150 000 in 20X1. The tax rate in 20X0 is 30% and in 20X1 25%.

The (5000) in 20X1 under the liability method adjusts the carry forward of 30 000 to 25 000which is the timing difference of 100 000 at 25% tax rate. The 37 500 is now the best esti-mate of the tax payable if the timing differences reversed, whereas the 42 500 does notrepresent the best estimate of the likely liability.

One further problem with paragraph 37 of the standard is that we are required to use theaverage tax rates that are expected to apply. The average calculation will become neces-sary when different tax rates apply to different levels of taxable income. It will thus be nec-essary in these circumstances to make a judgement on the levels of profits expected in theperiods in which the timing differences are expected to reverse. This judgement of profitscould be made we presume by reference to the past.

DISCOUNTING 429

430 TAXATION (SSAPS 5 AND 15 AND FRSS 16 AND 19)

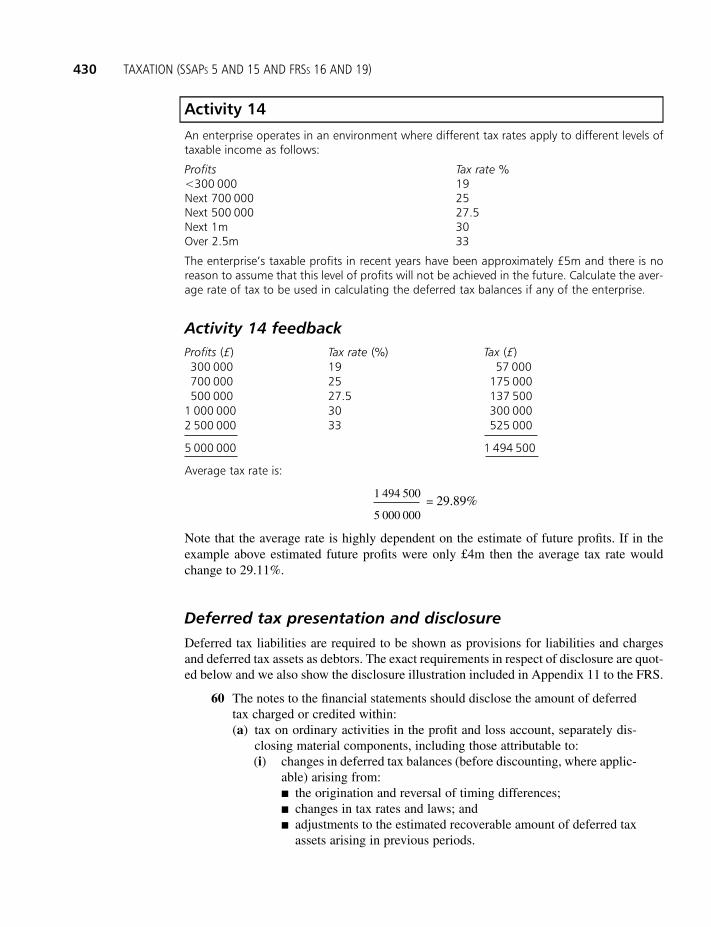

Activity 14

An enterprise operates in an environment where different tax rates apply to different levels oftaxable income as follows:

The enterprise’s taxable profits in recent years have been approximately £5m and there is noreason to assume that this level of profits will not be achieved in the future. Calculate the aver-age rate of tax to be used in calculating the deferred tax balances if any of the enterprise.

Note that the average rate is highly dependent on the estimate of future profits. If in theexample above estimated future profits were only £4m then the average tax rate wouldchange to 29.11%.

Deferred tax presentation and disclosureDeferred tax liabilities are required to be shown as provisions for liabilities and chargesand deferred tax assets as debtors. The exact requirements in respect of disclosure are quot-ed below and we also show the disclosure illustration included in Appendix 11 to the FRS.

60 The notes to the financial statements should disclose the amount of deferredtax charged or credited within:(a) tax on ordinary activities in the profit and loss account, separately dis-

closing material components, including those attributable to:(i) changes in deferred tax balances (before discounting, where applic-

able) arising from:■ the origination and reversal of timing differences;■ changes in tax rates and laws; and■ adjustments to the estimated recoverable amount of deferred tax

assets arising in previous periods.

(ii) where applicable, changes in the amounts of discount deducted inarriving at the deferred tax balance.

(b) tax charged or credited directly in the statement of total recognised gainsand losses for the period, separately disclosing material components,including those listed in (a) above.

61 The financial statements should disclose:(a) the total deferred tax balance (before discounting, where applicable),

showing the amount recognised for each significant type of timing dif-ference separately;

(b) the impact of discounting on, and the discounted amount of, the deferredtax balance; and

(c) the movement between the opening and closing net deferred tax balance,analysing separately:(i) the amount charged or credited in the profit and loss account for the

period;(ii) the amount charged or credited directly in the statement of total

recognised gains and losses for the period; and(iii) movements arising from the acquisition or disposal of businesses.

61 The financial statements should disclose the amount of a deferred tax assetand the nature of the evidence supporting its recognition if:(a) the recoverability of the deferred tax asset is dependent on future taxable

profits in excess of those arising from the reversal of deferred tax liabil-ities; and

(a) the reporting entity has suffered a loss in either the current or precedingperiod in the tax jurisdiction to which the deferred tax asset relates.

1 Tax on profit on ordinary activities(a) Analysis of charge in period 200Y 200X

£m £m £m £mCurrent tax:UK corporation tax on profits of the period 40 26Adjustments in respect of previous periods 4 (6)

–––––– ––––––44 20

Foreign tax 12 16–––––– ––––––

Total current tax (note 1(b)) 56 36

Deferred tax:Origination and reversal of timing differences 67 60Effect of increased tax rate on opening liability 12 –Increase in discount (14) (33)

–––––– ––––––Total deferred tax (note 2) 65 27

–––––– ––––––Tax on profit on ordinary activities 121 63

–––––– –––––––––––– ––––––(b) Factors affecting tax charge for periodThe tax assessed for the period is lower than the standard rate of corporation tax in the UK(31 per cent). The differences are explained below:

200Y 200X

DISCOUNTING 431

£m £mProfit on ordinary activities before tax 361 327

––––– –––––––––– –––––Profit on ordinary activities multiplied by standard rate of

corporation tax in the UK of 31% (200X: 30%) 112 98

Effects of:Expenses not deductible for tax purposes

(primarily goodwill amortisation) 22 10Capital allowances for period in excess of depreciation (58) (54)Utilisation of tax losses (17) (18)Rollover relief on profit on disposal of property (10) –Higher tax rates on overseas earnings 3 6Adjustments to tax charge in respect of previous periods 4 (6)

–––––– ––––––Current tax charge for period (note 1(a)) 56 36

––––– –––––Undiscounted provision for deferred tax 426 347Discount (80) (66)

––––– –––––Discounted provision for deferred tax 346 281

––––– –––––––––– –––––Provision at start of period 281Deferred tax charge in profit and loss

account for period (note 1) 65–––––

Provision at end of period 346–––––

International aspectsIAS 12 ‘Income Taxes’ deals with deferred tax and like FRS 19 it requires deferred tax tobe recognised on a full provision basis. However IAS 12 requires recognition of deferredtax on the basis of temporary differences rather than on the basis of obligations arising fromtiming differences. Thus the IAS view focuses on a balance sheet approach to deferred taxwhereas the UK, even under FRS 19, still uses an income statement approach.

Example 4An enterprise buys an asset for £100 depreciated over five years on a straight line basis.Tax allowances on capital assets are 50% in the first year and tax rate is 30%. Under theincome statement approach, known as limiting difference, the deferred tax provided for atthe end of the first year is:

Circumstances giving rise Deferred tax required to be recognised byto deferred tax

FRS 19 IAS 12

Note well that IAS 12 does not permit deferred tax balances to be discounted even as an option.

1. Revaluation of non-monetary assets

Provision is required whether or not it isintended that the asset will be sold andwhether or not rollover relief could be claimed

Provision is required only if either: (a) the assetis revalued to fair value each period withchanges in fair value being recognised in theprofit and loss account; or (b) the entity hasentered into a binding agreement to sell therevalued asset, has revalued the asset to itsselling price and does not expect to obtainrollover relief

2. Sale of assets, where gainhas been or might berolled over intoreplacement assets

Provision is required. The deferred tax ismeasured on the difference between thereplacement asset’s cost and its tax base (i.e. cost less taxable gain rolled over)

Provision is required only if rollover relief hasnot been obtained and it is not expected to beobtained

3. Adjustments to recogniseassets and liabilities attheir fair values on theacquisition of a business

5. Exchange differences arisingon consolidation of non-monetary assets of an entityaccounted for under thetemporal method

Provision is made for all differences betweenthe fair values recognised for assets andliabilities and their tax base. The only exceptionis that no provision is required in respect ofthe temporary difference arising on therecognition of non-deductible goodwill

Provision is required on the unremitted earningsof associates in all circumstances. Provision isrequired on the unremitted profits ofsubsidiaries, branches and joint ventures if eitherthe parent/investor is unable to control thetiming of the remittance of the earnings or it isprobable that remittance will take place in theforeseeable future

Provision is required on the temporarydifference between the carrying amount (athistorical exchange rate) and the tax base (atbalance sheet date exchange rates)

The amendment to FRS 7 ‘Fair values inacquisition accounting’ introduced by FRS 19requires deferred tax to be provided for as ifthe adjustments had been gains or lossesrecognised before the acquisition. Deferred taxwould not normally be recognised onadjusting non-monetary assets to marketvalues. No provision is recognised in respect ofacquired goodwill

Provision is required only to the extent thatdividends payable by a subsidiary, associate orjoint venture have been accrued at the balancesheet date or a binding agreement todistribute the past earnings in future has beenmade

No provision is required because there is notiming difference

6. Unrealised intergroupprofits (for example, instock) are eliminated onconsolidation

Provision is required on the temporarydifference. IAS 12 states that this is thedifference between the (reduced) carryingamount of the stock in the balance sheet andits higher tax base (the amount paid by thereceiving company). The provision is measuredusing the receiving company’s rate of tax

Provision is required on the timing difference,i.e. the profit that has been taxed but notrecognised in the consolidated accounts. It istherefore measured using the supplyingcompany’s rate of tax

Deferred tax 9

The balance sheet approach, temporary difference, isNet book value of asset at end year 1 80Tax base (tax written down value) 50

30Deferred tax 9

In this example there is no difference between the two methods.If the asset had been revalued to £200 at the end of year 1 then only the balance sheet

calculation would change:

NBV 200Tax base 50Temporary difference 150Deferred tax 45

The argument for providing deferred tax on the temporary difference (note there is no tim-ing difference) is that it is presumed the revalued carrying amount of the asset will be recov-ered through use and will generate taxable income that will be taxable in the future andtherefore there is a deferred tax liability. There is a problem with this logic, though, giventhe definition of a liability as ‘a present obligation arising out of a past event’. The futuretaxable income referred to here is not a past event.

IAS 12 also requires provisions to be made for deferred tax when the critical event caus-ing the deferred tax to become payable in future has not occurred by the balance sheet date.

The main differences between the recognition requirements of IAS 12 and those of FRS19 are detailed in Table 21.1 extracted from Appendix IV of FRS 19.

SummaryWithin this chapter we have considered some problem areas of accounting for taxation,particularly those relating to deferred tax. We have noted the various solutions the ASC/Bhave produced for deferred tax:

■ Prior to SSAP 11 flow through approach■ SSAP 11 full deferral approach■ SSAP 15 1978 and 1985 partial approach■ FRS 19 full provision with a discounting optionand demonstrated the differences between these approaches.

We have also noted that even though the ASB is concerned to harmonise UK standards withthose of the IASB there are at least two major differences between FRS 19 and IAS 12:

■ IAS 12 does not permit discounting■ IAS 12 takes a balance sheet approach to provision of deferred tax whereas FRS 19 still

focuses on the income statement.

It is anticipated that when the UK listed companies report under IASs as from 2005 severalof them with large investment property portfolios will have to recognise several million morein deferred tax on revaluations of these properties, which will have an impact on net assetvalues.

434 TAXATION (SSAPS 5 AND 15 AND FRSS 16 AND 19)

Exercises

1 Outline the major arguments in favour of always providing for deferred tax where theamounts would be material.

2 Explain and distinguish between:(a) the flow-through approach(b) full deferral(c) partial deferral.

3 Explain and distinguish between:(a) the deferral method(b) the liability method.Do you agree with the choice made by the ASB?

4 ‘Comparability requires that either all companies provide in full for deferred tax, or that itis always ignored. Therefore the concept of partial deferral must be unacceptable.’ Consider.

5 Draft a memorandum to your client, a non-accountant, outlining what deferred tax is andwhy there are problems in suggesting the appropriate treatment.

6 Does the required accounting treatment of taxation in published financial statements leadto a true and fair view?

7 Does the ASB’s decision to permit optional discounting lead to a lack of comparabilitybetween companies?

8 (a) FRS 19 ‘Deferred Tax’ was issued in December 2000. It details the requirements relat-ing to the accounting treatment of deferred tax.

Required:Explain why it is considered necessary to provide for deferred tax and brieflyoutline the principles of accounting for deferred tax contained in FRS 19‘Deferred Tax’.(b) Bowtock purchased a fixed asset for £2 000 000 on 1 October 2000. It had an esti-

mated life of eight years and an estimated residual value of £400 000. The plant isdepreciated on a straight-line basis. The Inland Revenue allow 40% of the cost of thistype of asset to be claimed against corporation tax in the year of purchase and 20%per annum (on a reducing balance basis) of its tax written down value thereafter. Therate of corporation tax can be taken as 25%.

Required:In respect of the above item of plant, calculate the deferred tax charge/creditin Bowtock’s profit and loss account for the year to 30 September 2003 and thedeferred tax balance in the balance sheet at that date. (ACCA FR Dec. 2003)

9 Spencer plc has produced draft consolidated financial statements for the year ended 30June 2003. These financial statements include deferred tax liability of £8 million. However,no account has been taken of the potential deferred tax implications of the following:(a) On 30 June 2003, the group revalued all its properties and a surplus of £7 million

was taken to the statement of total recognised gains and losses. The group has nointention of disposing of any of these properties in the foreseeable future.

(b) One of the subsidiaries of Spencer plc made a loss adjusted for tax purposes of £2million in the year ended 30 June 2003. This loss can only be relieved against futuretrading profits made by the subsidiary. The directors of Spencer plc believe the lossmade by the subsidiary to be attributable to nonrecurring factors.

Required:What is the deferred tax liability of Spencer plc at 30 June 2003 under the pro-visions of FRS 19 after taking account of both the events above? (CIMA FR