57

Insights & Analysis of Judicial Pronouncements | Notifications| Circulars What’s ahead Key dates (Tax calendar) TAXPERT JOURNAL September, 2021 “BE UPDATED, BE AHEAD”

Insights & Analysis of

Judicial Pronouncements | Notifications| Circulars

What’s ahead

Key dates (Tax calendar)

TAXPERT JOURNAL September, 2021

“BE UPDATED, BE AHEAD”

Recent Updates

2 © Taxpert Professionals| September, 2021

TABLE OF CONTENTS

Sr

No PARTICULARS

Page

No

DIRECT TAXATION

RECENT JUDICIAL PRONOUNCEMENTS

1. Supreme Court Ruling on Section 14A – to keep Tax system simple & convenient [South

Indian Bank Ltd. V. Commissioner of Income-tax [2021] 130 taxmann.com 178 (SC) [09-

09-2021]

7

2. As per Section 24(b) there is no bar on an Assessee to claim deduction of interest payable

on a loan taken for purchasing a residential property, though, possession of same might

not have been vested with him [Abeezar Faizullabhoy V. Commissioner of Income tax

(Appeals)-28, Maharashtra [2021] 130 taxmann.com 156 (Mumbai - Trib.) [01-09-2021]

8

3. R&D exp. incurred outside India eligible for deduction u/s 35(1)(iv) and not u/s 35(2AB)

[ ITAT MAHLE Behr India (P.) Ltd. V. Deputy Commissioner of Income Tax 130

taxmann.com 7 (Pune - Trib.) [31-08-2021]]

9

4. Difference between agreement value and stamp duty value if less than 10 per cent, no

addition under section 56(2)(vii)(b) was to be made by keeping in view third proviso to

section 50C(1) and provisions of section 56(2)(x)[ Joseph Mudaliar V. Deputy

Commissioner of Income-tax [2021] 130 taxmann.com 250 (Mumbai - Trib.)[14-09-2021]

10

5. Reopening of assessment justified on facts which emanated after rectification application

had been filed by assessee. [M/s. Thiriveni Earthmovers V. Assistant Commissioner of

Income Tax [2021] 130 taxmann.com 183 (Madras)[01-09-2021]

12

NOTIFICATION/ CIRCULARS/ PRESS RELEASE 14

1. TAX CALENDER FOR OCTOBER, 2021 17

2. INDIRECT TAXATION

RECENT JUDICIAL PRONOUNCEMENTS

1 3. No writ admissible if statutory remedy available & there was no violation of principles of

natural justice: SC. (The Assistant Commissioner of State Tax V. M/s Commercial Steel

Limited [2021] 130taxmann.com180(SC)[03-09-2021]

19

Recent Updates

3 © Taxpert Professionals| September, 2021

Sr

No 4. PARTICULARS

Page

No

2 5. Mere suspicion is not a sufficient cause to invoke provision of confiscation of goods. [A.P.

Refinery (P.) Ltd. V. State of Uttarakhand [2021] 130 taxmann.com 307 (Uttarakhand)[10-

09-2021]

20

3. 6. A reasonable opportunity ought to have been granted to all 'registered persons'/taxpayers

to submit/revise/ re-revise electronically their Form GST TRAN-1/TRAN-2: [Ratek

Pheon Friction Technologies Pvt. Ltd Vs. Principal Commissioner, [2021] 130

taxmann.com 367 (Allahabad)[15-09-2021]

22

4. 7. Gauhati HC ruling on refund of accumulated ITC in case of inverted duty [BMG

Informatics Pvt Ltd Vs Union of India [2021] 130 taxmann.com 182 (Gauhati) [02-09-

2021]

23

8. AUTHORITY FOR ADVANCE RULINGS

1. 9. ITC not to be availed if supplier furnishes invoices for FY 2019-20 in GSTR-1 of

November 2020. Authority for Advance Rulings (AAR), West Bengal, Goods & Services

Tax [2021] 130 taxmann.com 232 (AAR - WEST BENGAL) [09-08-2021]

25

2. 10. Tissue Paper not to be covered under Heading No. 4802 of uncoated paper and paperboard

Authority for Advance Rulings, Karnataka [In re Premier Tissues India Limited, GST AAR

Karnataka]

26

3. 11. Charitable Trust running medical store to give medicines without profit required to be

registered under GST [Nagri Eye Research Foundation v. Union of India, Gujarat High

Court SCA [No. 7822 Of 2021]

28

12. NOTIFICATION/ CIRCULARS/ PRESS RELEASE 29

13. TAX CALENDER FOR OCTOBER, 2021 34

14. INTERNATIONAL TAXATION

15. RECENT JUDICIAL PRONOUNCEMENTS

1. 16. Reassessment can be initiated based on materials which weren’t considered during original

assessment [ M/s Cairn India Ltd V. Deputy Director of Income-tax-I, (International

Taxation), Chennai [2021] 130 taxmann.com 167 (Madras)[01-09-2021]

36

Recent Updates

4 © Taxpert Professionals| September, 2021

Sr

No 17. PARTICULARS

Page

No

2. 18. Income earned by company from sale of software licenses and income from support,

maintenance and training services rendered in relation to such software licenses sold

through third parties in India was not chargeable to tax as "Royalty" under section 9 as well

as under article 12 of DTAA [BMC Software Asia Pacific Pvt Ltd. V. Assistant

Commissioner of Income-tax, (International Taxation), Circle-1, Pune [2021] 130

taxmann.com 205 (Pune - Trib.)[08-09-2021]

37

3. Where there was alleged interest-free debt funding of a fully owned overseas special

purpose vehicle (SPV) to use fund for overseas acquisition of a target company, it was held

that there cannot be a transaction of interest-free debt funding of overseas SPV by its

sponsor; even if such a transaction is at all hypothetically possible, arm's length interest on

such funding will be 'nil' [Bennett Coleman & Co. Ltd. V. Deputy Commissioner of

Income-tax [2021] 129 taxmann.com 397 (Mumbai - Trib.)[30-08-2021]

38

4. There cannot be a transaction, between independent enterprises, of interest-free debt

funding of an overseas SPV by its sponsorer; if such a transaction between independent

enterprises is at all hypothetically possible, arm's length interest on such funding will be 'nil'

[Bennett Coleman & Co. Ltd. V. Deputy Commissioner of Income-tax [2021] 129

taxmann.com 398 (Mumbai - Trib.)[30-08-2021]

40

NOTIFICATION/ CIRCULARS/ ORDERS 42

TAX CALENDER FOR OCTOBER, 2021 44

CORPORATE LAWS

RECENT JUDICIAL PRONOUNCEMENTS

1. Parties engaged in commercial litigation must weigh commercial interests and avoid filing

mindless appeals Uflex Ltd. V. Government of Tamil Nadu [2021] 130 taxmann.com 317

(SC)[17-09-2021]

46

2. Due regard would have to be given to inconvenience of flat purchaser and hardship faced

by him if petition was entertained and doctrine of 'forum non-conveniens' applied in full

vigor in instant facts and in favour of flat purchaser Hagwood Commercial Developers (P.)

Ltd. V. Rahul Madhukar Deshmukh [2021] 130 taxmann.com 313 (Bombay)[06-09-2021]

48

Recent Updates

5 © Taxpert Professionals| September, 2021

Sr

No PARTICULARS

Page

No

3. Preferential allotment can be issued by issuer company, however, before issuance of

preferential allotment certain conditions are required to be complied which is mandatory

as per Regulation 160 of ICDR Regulations. Regulation 160(d) provides that issuer is

required to be in compliance with LODR RegulationsAshav Advisory LLP V. Securities

and Exchange Board of India [2021] 130 taxmann.com 204 (SAT - Mumbai) [09-09-2021]

49

4. NCLT held that there was ample power to invoke section 242 at any stage and, therefore,

interim reliefs were to be allowed and petitioners were directed to use all powers available

with them to extend their long arm to thoroughly investigate affairs of companies [Union

of India V. Videocon Industries Limited [2021] 130 taxmann.com 52 (NCLT - Mum.) [31-

08-2021]

51

5. Madras HC remanded matter back as SEBI failed to fix liability on writ-applicant [Golden

Trees Plantation Ltd. V. Securities & Exchange Board of India [2021] 130 taxmann.com

410 (Gujarat) [06-09-2021]

53

NOTIFICATION/ CIRCULARS/ PRESS RELEASE 54

Recent Updates

6 © Taxpert Professionals| September, 2021

DIRECT

TAXATION

Recent Updates

7 © Taxpert Professionals| September, 2021

RECENT JUDICIAL PRONOUNCEMENTS

Supreme Court Ruling on Section 14A – to keep Tax system simple & convenient [South Indian Bank Ltd. V. Commissioner of Income-tax [2021] 130 taxmann.com 178 (SC) [09-09-2021]

FACT OF THE CASE:

1) The South Indian Bank Ltd [hereinafter referred “Appellant (s)”] are scheduled banks and in course

of their banking business, they are also engaged in the business which earned income from

investments made in tax-free securities.

2) In Finance Act, 2001, Section 14A of Income Tax Act, 1961 (hereinafter referred as “Act”) was

retrospectively amended from 01.04.1962 and inserted that no deduction for expenses incurred

to earn exempt income.

3) A proviso later introduced by the Finance Act, 2002 with effect from 11.05.2001 whereunder,

re-assessment, and rectification of assessment was prohibited for any assessment year, up-to the

A.Y. 2000-2001.

4) The Appellant(s) were concerned about the allowances made under Section 14A of the Act for

A.Y. commencing from 2001-2002 onwards or for pending assessments.

5) None of the Appellant(s) banks, maintained separate accounts for the investments made in

bonds, securities and shares wherefrom the tax-free income was earned so that disallowances

could be limited to the actual expenditure incurred by them.

6) The Appellant(s) did not maintain separate accounts for the investments made in bonds,

securities and shares wherefrom the tax-free income was earned so that disallowances could be

limited to the actual expenditure incurred by them.

7) During the Assessment, the Assessing Officer made proportionate disallowance of interest

attributable to the funds invested to earn tax-free income. Since there was no actual income

available in figured, the Assessing Officer worked out proportionate disallowance by referring

to the average cost of deposit for the relevant year.

8) The CIT (A) had concurred with the view taken by the Assessing Officer.

9) This was further appealed in ITAT wherein the ITAT after considering the Appellant(s) nature

of business and after noticing the surplus reserves and funds accepted that the Appellant(s) that

investments were not made out of interest or cost bearing funds alone. Thus, it was held by the

ITAT that disallowance under Section 14A is not warranted, in absence of clear identity of funds.

10) ITAT decision was reversed by the High Court.

11) The Appellant(s) then filed the appeal in Hon’ble Supreme Court for clear interpretation of

Section 14A.

ISSUE:

i. Whether proportionate disallowance of interest paid by the banks is called for under Section 14A

of Income Tax Act for investments made in tax free bonds/ securities which yield tax free

dividend and interest to Appellant(s) Banks when Appellant(s) had sufficient interest free own

funds which were more than the investments made.

Recent Updates

8 © Taxpert Professionals| September, 2021

RECENT JUDICIAL PRONOUNCEMENTS

OBSERVED:

The Hon’ble Supreme Court observed that Section 14A of the Act does not allow the department to make

presumptions and disallow an expenditure for earning tax free income in cases where assessee, do not

maintain separate accounts for the investments and other expenditures incurred for earning the tax-free

income. It also observes that for a good mechanism of tax regulations the department should make the

keep the compliances simple and convenient. Further the Circular no. 18 of 2015 dated 02-11-2015, clearly

explained that all the shares and securities held by a bank which are not bought to maintain Statutory

Liquidity Ratio (SLR) are its stock-in-trade and not investments and all income received on these shares

will be considered as business income.

HELD:

The Hon’ble Supreme Court answered these appeals against the Revenue and in favour of the Appellant(s)

agreed with the view taken by ITAT. The appeals by the Appellant(s) are accordingly allowed with no

order on costs and no deduction was disallowed on the grounds of Section 14A of the Act.

As per Section 24(b) there is no bar on an Assessee to claim deduction of interest payable on a loan taken for purchasing a residential property, though, possession of same might not have been vested with him [Abeezar Faizullabhoy V. Commissioner of Income tax (Appeals)-28, Maharashtra [2021] 130 taxmann.com 156 (Mumbai - Trib.) [01-09-2021]

FACT OF THE CASE:

1) The Abeezar Faizullabhoy (hereinafter referred to “Assessee”) who is a lawyer by profession had filed his

Return of Income (ROI) for A.Y. 2015-16 on 31.03.2017, declaring a total income of Rs.1,19,68,190/-

2) The case of the assessee was selected for scrutiny assessment u/s 143(2) of the Income Tax Act, 1961

(hereinafter referred as “Act”)

3) Assessing Officer (AO) observed that the assessee had under the head “Income from House

property” claimed deduction of interest paid on borrowed capital of Rs. 2,00,000/- under Section

24(b) of the Act.

4) It was submitted by the assessee that the aforesaid claim for deduction of interest pertained to the

funds which were borrowed by him for purchasing a residential property.

5) It was a noted that the assessee has not taken the possession of the said flat, henceforth the AO

issued the order u/s 143(3) of the Act, dated 27.12.2017 and assessed the income of the assessee at

Rs.1,21,68,190/-.

6) The Assessee appealed before Commissioner of Income Tax (Appeals) [CIT-(A)] (hereinafter referred to

as “Respondents”) which upheld the decision of AO. Aggrieved by the order the appeal was filed before

Hon’ble ITAT.

Taxpert Professional’s comments:

The Supreme Court clearly mentioned that for good and smooth compliances of the tax the

department/government have to bring in simple and convenient regulations and also marked

that there are no rooms for presumptions in the Taxation regime.

Recent Updates

9 © Taxpert Professionals| September, 2021

RECENT JUDICIAL PRONOUNCEMENTS

ISSUE:

i. Whether or not the lower authorities were justified in law and the facts of the case in declining the

assessee’s claim for deduction of the interest paid on loan that was utilized for purchasing a residential

house vide a registered “agreement‟ dated 20.09.2009.

OBSERVED:

The Hon’ble ITAT observed that the assessee had provided the certificate evidencing the payment of the

aforesaid amount of interest on borrowed funds was filed by the assessee in the course of the assessment

proceedings. The AO and the CIT-(A) erred in appreciating the evidences provided by the assessee. In

respect of deduction claimed by the assessee u/s 24(b) of the act there is neither any such precondition

nor an eligibility criterion prescribed that the assessee should have taken possession of the property so

purchased or acquired by him. Thus, the view of the AO and CIT-(A) was bad in law.

HELD:

The Hon’ble ITAT stated that the 1 & 2 proviso to Section 24(b) does not jeopardize the entitlement of

assessee to claim deductions on interest payable on property acquired by him. It was interpreted by the

ITAT that Section 24(b) does not bar deductions of interest even though the assessee might not be in

possession of the property and the appeal filed by the assessee was allowed.

R&D exp. incurred outside India eligible for deduction u/s 35(1)(iv) and not u/s 35(2AB) [ ITAT MAHLE Behr India (P.) Ltd. V. Deputy Commissioner of Income Tax 130 taxmann.com 7 (Pune - Trib.) [31-08-2021]]

FACT OF THE CASE:

1) M/s MAHLE Behr India (p.) Ltd (hereinafter referred to “Assessee”) filed its return declaring total

income of Rs.3.56 crore and odd.

2) The assessee has three Associate Enterprises (AEs) situated in the USA, Japan and Germany

respectively for which the assessee had claimed weighted deduction u/s.35 (2AB) of Income Tax

Act, 1961 (hereinafter referred as “Act”) amounting to Rs. 26,73,42,263/- on Research and

Development expenses (R&D)

3) Assessing Officer (AO) observed that the assessee claimed weighted deduction on R&D costs of

Rs.9,61,80,237/- carried outside India. Therefore, AO disallowed a sum of Rs.8,86,84,811/-, being,

the amount of capital R&D expenditure incurred outside India.

4) Thereafter the assessee appealed in CIT-(A) which disallowed for all the weighted deductions prior

to grant of approval.

5) Hence the Assessee approach the ITAT.

Taxpert Professional’s comments:

Taxpayer will be eligible to claim deduction for payment of interest on home loan for purchase

of house property, if the property is acquired or purchased even though possession of such

house property is not taken by the taxpayer.

Recent Updates

10 © Taxpert Professionals| September, 2021

RECENT JUDICIAL PRONOUNCEMENTS

ISSUE:

i. Whether the denial of weighted deduction claimed by the assessee u/s 35 (2AB) of the act on

R&D expenditure is valid

OBSERVED:

The fact that the claim of the assessee cannot be entertained under one provision does not oust it from

consideration under any other provision, if it is otherwise allowable under such latter provision. We have

noticed that the amount of capital expenditure incurred on research and development outside India is

eligible for deduction u/s.35(1)(iv). The same, therefore, has to be allowed as such. The ld. DR’s

contention in this regard is sans merit and hence repelled.

HELD:

The entire amount of R&D expenditure incurred in India is eligible for weighted deduction u/s 35(2AB);

revenue R&D expenditure incurred outside India as claimed by the assessee got allowed in the assessment

itself; total of capital R&D expenditure incurred outside India will be eligible for deduction u/s 35(1)(iv)

of the Act. The Appeal is partly allowed.

FACT OF THE CASE:

1) Joseph Mudaliar, an individual (hereinafter referred to “Assessee”), is stated to be engaged in the business

of trading in imitation jewellery.

2) The assessee filed the Return of Income (ROI) on 30.09.2015 declaring total income of Rs.

6,28,420/- and current year loss of Rs. 76,18,500/-. Later, on 30.09.2016 assessee filed a revised

return of income declaring total income of Rs. 6,20,650/- and current year loss of Rs.79,43,584/-

3) During the assessment proceeding the Assessing officer (AO) found that that assessee had

purchased four immovable properties at lower rate than the market value having a difference of

Rs.23,30,695/- between the two values.

4) Hereinafter, the AO called upon assessee to show cause why the difference amount should be

added u/s 56(2)(vii)(b) of the Income Tax Act, 1961 (hereinafter referred as “Act”)

5) Aggrieved by the decision of AO the assessee further appealed to CIT-(A) which disallowed

assesee’s contentions. Hence, the present appeal is with Hon’ble ITAT.

Difference between agreement value and stamp duty value if less than 10 per cent, no addition under section 56(2)(vii)(b) was to be made by keeping in view third proviso to section 50C(1) and provisions of section 56(2)(x)[ Joseph Mudaliar V. Deputy Commissioner of Income-tax [2021] 130 taxmann.com 250 (Mumbai - Trib.)[14-09-2021]

Taxpert Professional’s comments:

The assessee would be eligible to claim deduction of revenue R&D Expenditure incurred

outside India u/s 35(2AB) whereas capital R&D expenditure incurred for business purpose

outside India would be allowed as deduction u/s 35(1)(iv) of the Act.

Recent Updates

11 © Taxpert Professionals| September, 2021

RECENT JUDICIAL PRONOUNCEMENTS

ISSUE:

i. Whether the Learned CIT(A) has erred in making addition of Rs. 23,30,694/- difference between

the agreement value & stamp duty value on purchase of office premises u/s 56 (2) (viib), ignoring

the fact that property was booked under construction in Oct’ 2013 when the property market price

was lower.

OBSERVED:

The Hon’ble ITAT observed that the Hon’ble ITAT relied on the case of Shri Sandip Patil vs ITO (supra)

and Maria Fernandes Cheryl vs ITO (supra) and stated that assessee would be eligible to get the benefit

of ten per cent margin difference in the valuation between the value determined by the stamp duty

authority and the declared sale consideration if the variation between the aforesaid two values falls within

the range of ten per cent, no addition can be made.

HELD:

The issue is no more res integra in view of a number of decisions of different benches of the Tribunal.

The Tribunal has consistently expressed the view that since the aforesaid amendments made by Finance

Act, 2018 with effect from 01-04-2019 are curative in nature and beneficial provisions, it would apply

retrospectively. The addition of Rs. 23,30,694/- was deleted and the ground was allowed.

Taxpert Professional’s comments:

There is no more an ambiguity and the benefit of marginal variation is given to the assessee

that he can get the benefit of 10% of margin difference between Stamp Duty valuation

determined by the authority and sale consideration value as per the agreement.

Recent Updates

12 © Taxpert Professionals| September, 2021

RECENT JUDICIAL PRONOUNCEMENTS

FACT OF THE CASE:

1. M/s. Thiriveni Earthmovers Private Limited (hereinafter referred as “Assessee”) filed the Return of Income

(ROI) for the A.Y. 2008-09 on 30.09.2008 declaring a total income of Rs. 117,55,95,560/- A notice

under Section 143 of Income Tax Act, 1961 (hereinafter referred as “Act”) dated 23.09.2009 was issued

with a total tax demand of Rs. 38,82,78,150/- after credit of TDS of Rs. 8,51,06,508/- instead of Rs.

9,04,19,747/- claimed by the assessee.

2. Thus, a rectification request was filed by the Assessee where a rectification order was passed and a

revised demand for Rs. 38,05,14,782/- was issued after a credit of Rs. 8,51,06,508/- instead of Rs.

9,04,19,747/- because of which interest was payable by the assessee.

3. The assessee appeals that if the deduction of TDS for Rs. 55,65,195 will be allowed then they will not

be liable to pay any tax

4. While the rectification u/s 154 was in process, under section 148 of the Act the notice was issued and

the case was reopened after 4 years, on the ground that income had escaped assessment stating that

from the Form 26AS downloaded the assessee was in receipt of Rs. 419,47,44,777/- as opposed to the

total amount credited to the P&L account of Rs. 387,30,50,376/- and therefore the Deputy

Commissioner of Income Tax had a reason to believe that income of Rs. 41,59,51,722/- had escaped

assessment.

5. The assessee filed a writ petition to high court in view of the re-opening of assessment after 4 years

by the Assessing officer (AO) submitting that the re-opening was completely not tenable as complete

information was available with the Assessing Officer even at the time of scrutiny under section 143 of

the Act and the reopening was contrary to law

6. The AO resisted the petition by stating the huge mismatch of the information in Form 26AS and the

amount in P&L in the books of the assessee and also proved that it had reasons to believe that income

has escaped assessment as the assessee mentioned about the TDS amount in the rectification appeal

and not in the notice issued u/s 143.

OBSERVED:

As the assessee failed to make full and true disclosure of all material facts during original assessment and

a huge difference between Form 26AS and Amount booked in P&L constitutes that AO had sufficient

material to reopen the assessment even after 4 years in AY 2012-13 and the reopening of the assessment

was not based on the change of opinion but the facts which emanated after the rectification application

was filed by the assessee.

Reopening of assessment justified on facts which emanated after rectification application had

been filed by assessee. [M/s. Thiriveni Earthmovers V. Assistant Commissioner of Income

Tax [2021] 130 taxmann.com 183 (Madras)[01-09-2021]

Recent Updates

13 © Taxpert Professionals| September, 2021

RECENT JUDICIAL PRONOUNCEMENTS

HELD:

As there were reasons for AO to believe that income has escaped assessment due to mismatch of amount

in Form 26As and P&L of the assessee and further the details of TDS amount claimed were disclosed by

the assessee in the rectification appeal and not during the assessment proceedings u/s 143. Therefore, the

reopening of the assessment for the AY 2008-09 was valid and the appeal of the assessee was dismissed.

Taxpert Professional’s comments:

The AO has the power to reopen the assessment u/s 148 even after time barred period of 3

years on the basis of non-disclosure of income while assessment u/s 143 and the reopening

would be held valid.

Recent Updates

14 © Taxpert Professionals| September, 2021

NOTIFICATIONS/CIRCULARS/PRESS RELEASE

1. The replacement of the Authority for Advance Rulings (‘AAR’) with the Board for Advance

Rulings ‘Board’

[Notification No. 96/2021/F. No. 370142/31/2021-TPL (Part II) & Notification No. 97

/2021/F. No. 370142/31/2021-TPL (Part II) dated 01st September, 2021]

CBDT has issued Notification Nos. 96 & 97 of 2021, whereby it has been provided that:

a. The AAR shall cease to operate on and from 1 September 2021.

b. Three Boards will become operational for the purposes of giving advance rulings on or after

1 September 2021:

i. Board for Advance Rulings-I headquartered at Delhi

ii. Board for Advance Rulings-II headquartered at Delhi

iii. Board for Advance Rulings-III headquartered at Mumbai

c. As a part of this transition, all applications pending before the AAR shall be transferred to

the Board on 1 September 2021. An application would be said to be pending if either:

i. no order for allowing or rejecting the application has been passed before 1 September

2021, or

ii. no advance ruling with respect to the application has been pronounced before 1

September 2021.

2. CBDT notifies Form 12BBA to be submitted by senior citizens wishing to claim benefit of

Sec. 194P [Notification G.S.R 612(E) [no. 99/2021/F.No.370142/11/2021-TPL], dated 2-9-

2021] [Notification S.O. 3595(E) [No. 98/2021/F. No. 370142/11/2021-Tpl], Dated 2-9-

2021]

In the notification by the Income-Tax (twenty-sixth amendment) rules, 2021 CBDT amended rules

31 and 31A and inserted rule 26D and clarifies the terms ‘Specified Bank’ for the purpose of IT

Section 194P relating to TDS in the case of Specified Senior Citizens (of age 75 or more having

pension/ interest income only), who have been exempted from filing of ITR u/s 139, in respect

of FY 2021-22/ AY 2022-23.

The new Rule 26D to provide that senior citizens are required submit Form 12BBA with specified

bank in order to claim the benefit of section 194P. The board has also amended Form 16, Form

24Q, Form 26QC and Form 26QD to incorporate necessary changes related to provisions of

section 194P.

Further, Central Government notifies specified Bank to mean a banking company which is a

scheduled bank and has been appointed as agents of Reserve Bank of India under section 45 of

the Reserve Bank of India Act, 1934 (2 of 1934).

3. Income-Tax (Twenty-Seventh Amendment) Rules, 2021 - Insertion of Rule 14c [Notification No. G.S.R. 616(E) [No. 101/2021/F.No.370142/35/2021-Tpl (Part I), Dated 6-9-2021] It has been notified that The Income Tax (I-T) Department has inserted a new Rule 14C to ease authentication of electronic records submitted in faceless assessment proceedings. If electronic records are submitted through registered account of taxpayer on the income tax portal, separate authentication through EVC is not required to be done

NOTIFICATIONS

Recent Updates

15 © Taxpert Professionals| September, 2021

NOTIFICATIONS/CIRCULARS/PRESS RELEASE

4. Income-Tax (Twenty-Eighth Amendment) Rules, 2021 - Amendment In Rule 11UAC

[Notification G.S.R. 623(E) [No. 105/2021/F. No. 370149/158/2021-TPL], Dated 10-9-2021] The Central Board of Direct Taxes notifies that in the Income-tax Rules, 1962, in rule 11UAC, after clause (3), the following clause shall be inserted, namely: — i. "(4) any movable property, being equity shares, of the public sector company, received by a

person from the Central Government or any State Government under strategic disinvestment.

Explanation. —For the purpose of this clause, „strategic disinvestment‟ shall have the same

meaning as assigned to it in clause (iii) of Explanation to clause (d) of sub-section (1) of section

72A.".

5. Income-Tax (Twenty-Ninth Amendment) Rules, 2021 - insertion of rule 12F

[Notification G.S.R. 627(E) [No. 109/2021/F. No. 370142/27/2021-Tpl (Part I)], Dated 13-9-2021] The CBDT notifies that in the Income-tax Rules, 1962, after rule 12E, the following rule shall be

inserted, namely: —

i. "12F. Prescribed Income-tax authority under second proviso to clause (i) of sub-section (1) of

section 142. —The prescribed Income-tax authority under second proviso to clause (i) of sub-

section (1) of section 142 shall be an income-tax authority not below the rank of Income Tax

Officer who has been authorized by the Central Board of Direct Taxes to act as such authority

for the purposes of that clause.".

1. CBDT extends due dates for filing of Income Tax Returns and various reports of audit for

the Assessment Year 2021-22 dated

(Circular No. 17/2021 [F. No. 225/49/2021/ITA-1I] dated: 09/09/2021)

Due to technical glitches in the new Income Tax Portal, the taxpayers & other stakeholders are

facing difficulty in filing Income Tax Returns (ITR) & various other compliances as required by

the Income Tax Act, 1961. Taking the same into consideration, the Central Board of Direct Tax

(CBDT) has further extended the deadlines for filing ITR and various Audit reports for

Assessment Year 2021-22.

CIRCULARS

NOTIFICATIONS

Recent Updates

16 © Taxpert Professionals| September, 2021

NOTIFICATIONS/CIRCULARS/ PRESS RELEASE

Summary of extended ITR and other due dates

Taxpayers Category Original Due

Date

Extended Due

Date

Revised

Extended Due

Date

ITR-Individuals/ HUF/Firm/Trust

(Where tax audit is Not Applicable)

31-Jul-2021 30-Sep-2021 31-Dec-2021

Tax Audit u/s 44AB or u/s 10B 30-Sep-2021 31-Oct-2021 15-Jan-2022

Transfer Pricing (TP) Audit u/s 92E 31-Oct-2021 30-Nov-2021 31-Jan-2022

ITR [Company or Individuals/HUF/Firm/

Trust where Tax Audit is applicable]

31-Oct-2021 30-Nov-2021 15-Feb-2022

ITR-Taxpayers where TP Audit is applicable 30- Nov-2021 31-Dec-2021 28-Feb-2022

Belated/ Revised ITR 31-Dec-2021 31-Jan-2022 31-Mar-2022

1. Section 132 of the Income-Tax Act, 1961 - search and seizure - general - Income Tax department conducts searches in Delhi, Gujarat and Dadra [Press release, dated 2-9-2021] The Income-tax Department carried out a search and seizure operation on 1-9-2021 on a manufacturer and distributor of synthetic yarns and polyester chips having corporate office in Delhi and factories at Dadra & Nagar Haveli and Dahej.

PRESS RELEASE

Recent Updates

17 © Taxpert Professionals| September, 2021

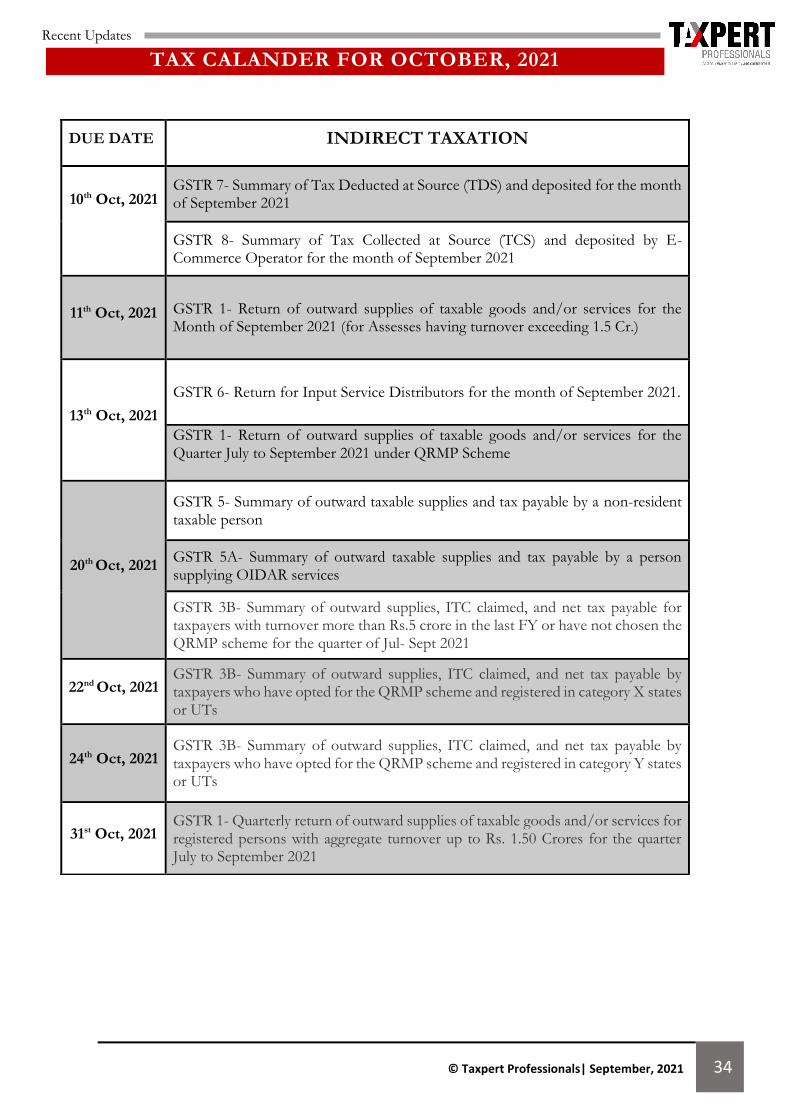

TAX CALANDER FOR OCTOBER, 2021

DUE DATE DIRECT TAXATION

07th Oct, 2021

Deposit of Tax deducted/collected (TDS/TCS) for the month of September, 2021.

Due date for deposit of TDS for the period July 2021 to September 2021 when Assessing Officer has permitted quarterly deposit of TDS under Section 192, 194A, 194D or 194H.

15th Oct, 2021

Furnishing of Form 24G by an office of the Government where TDS/TCS for the month of September, 2021 has been paid without the production of a challan

Due date for issue of TDS Certificate for tax deducted under Section 194-IA, Section 194-IB & Section 194M in the month of August, 2021

Quarterly statement in respect of foreign remittances (to be furnished by authorized dealers) in Form No. 15CC for quarter ending September, 2021

Quarterly statement of TCS deposited for the quarter ending September 30, 2021

30th Oct, 2021

Due date for furnishing of challan-cum-statement in respect of tax deducted under section 194-IA, Section 194-IB & Section 194M in the month of September, 2021

Quarterly TCS certificate (in respect of tax collected by any person) for the quarter ending September 30, 2021

31st Oct, 2021

Intimation by a designated constituent entity, resident in India, of an international group in Form no. 3CEAB for the accounting year 2020-21

Quarterly statement of TDS deposited for the quarter ending September 30, 2021

Due date for furnishing of Annual audited accounts for each approved programme under section 35(2AA)

Quarterly return of non-deduction of tax at source by a banking company from interest on time deposit in respect of the quarter ending September 30, 2021

Recent Updates

18 © Taxpert Professionals| September, 2021

INDIRECT

TAXATION

Recent Updates

19 © Taxpert Professionals| September, 2021

RECENT JUDICIAL PRONOUNCEMENTS

No writ admissible if statutory remedy available & there was no violation of principles of natural justice: SC. (The Assistant Commissioner of State Tax V. M/s Commercial Steel Limited[2021]130taxmann.com180(SC)[03-09-2021]

FACT OF THE CASE:

1) M/s Commercial Steel Limited (Herein referred to as Respondent) is a proprietary concern engaged

in the business of iron and steel and is registered under the Central Goods and Services Tax Act 2017

and has been allotted a GST code.

2) The Respondent purchased certain goods from a dealer, JSW Steel Limited, Vidyanagar, Karnataka,

under a tax invoice dated 11 December 2019. The consignment of goods was being carried in a truck

bearing registration No KA 35 C 0141. While it was proceeding from the State of Karnataka, it was

intercepted on 12 December 2019 at 5.30 pm at Jeedimetala.

3) The tax invoice indicated that the goods were earmarked for delivery at Balanagar, Telangana. The

case of the appellants is that Balanagar is situated between the State of Karnataka and Jeedimetala and

that no reasonable person would cross Balanagar and then turn around to go back to the place of

destination. The purchase value of the goods appeared to be in the amount of Rs 11,14, 579 from the

tax invoices.

ISSUE:

i. Whether the High Court was appropriate in entertaining the writ under Article 226 of the

Constitution.

OBSERVED:

The Hon’ble Supreme Court observed that respondent had a statutory remedy under section 107. Instead

of availing of the remedy, the respondent instituted a petition under Article 226. The existence of an

alternate remedy is not an absolute bar to the maintainability of a writ petition under Article 226 of the

Constitution. But a writ petition can be entertained in exceptional circumstances where there is:

(i) A breach of fundamental rights;

(ii) A violation of the principles of natural justice;

(iii) An excess of jurisdiction; or

(iv) A challenge to the vires of the statute or delegated legislation.

In this case none was established. Thus it was not appropriate of High Court to Entertain the writ.

Recent Updates

20 © Taxpert Professionals| September, 2021

Mere suspicion is not a sufficient cause to invoke provision of confiscation of goods. [A.P.

Refinery (P.) Ltd. V. State of Uttarakhand [2021] 130 taxmann.com 307 (Uttarakhand)[10-09-

2021]

RECENT JUDICIAL PRONOUNCEMENTS

HELD:

The Hon’ble Supreme court in the judicial pronouncement allowed the appeal and set aside the impugned

order of the High Court. The writ petition filed by the respondent shall stand dismissed. However, this

shall not preclude the respondent from taking recourse to appropriate remedies which are available in

terms of Section 107 of the CGST Act to pursue the grievance in regard to the action which has been

adopted by the state in the present case.

FACT OF THE CASE:

1) M/s A.P. Refinery Private. Ltd, is engaged in the supply of Rice Bran Oil (Grade-II). It is registered

with the GST Department, having GSTIN No. 03AAFCA1352B1ZX. It is registered both under the

CGST Act, 2017, and under the Punjab Goods and Services Tax Act, 2017.

2) The petitioner was transporting Rice Bran Oil from its factory located in Jagraon, Punjab to a dealer,

namely M/s Sheel Chand Agroils Pvt. Ltd, located in Lalpur, District Udham Singh Nagar in the State

of Uttarakhand by generating all E-invoices and E-Way bills.

3) The trucks left the petitioner’s place on 27.03.2021. However, as 29.03.2021 was the festival of Holi,

the drivers of the three trucks decided to wait in Ambala on 28.03.2021, lest the hooligans on the road

intercept the trucks, or damage the consignment in the garb of celebrating Holi.

4) Since the e-Way bills had expired within three days, the respondent, the Assistant Commissioner

(GST-State), issued three separate orders, all dated 01.04.2021, for physical verification/inspection of

the consignment. Upon physical verification, the description on the e-Invoices was found to be

matching with the physical goods verified in the vehicle, namely fixed vegetable oils of vegetable grade

i.e. mango kernel oil, mahua oil and rice bran oil. Even the quantity of the goods recorded in the e-

Invoices matched with the physically verified quantity.

ISSUE:

i. The department issued confiscation order and the petitioner challenged the confiscation orders by

filing writ petition.

ii. It was contended that no opportunity of being heard was given before passing the confiscation

orders under Section 130 in Form GST MOV-11.

Taxpert Professional’s comments:

The High Court erred entertaining its writ petition under Article 226 of the Constitution even

though the respondent had alternate remedy u/s 107 of CGST Act. The Hon’ble Supreme court

set a precedent by this judicial pronouncement so as to further avoid unnecessary writs in cases

where alternate remedies are not exhausted.

Recent Updates

21 © Taxpert Professionals| September, 2021

RECENT JUDICIAL PRONOUNCEMENTS

OBSERVED:

The Hon’ble High Court observed that an order enhancing any fee or penalty or fine in lieu of confiscation

or confiscating goods of greater value or reducing the amount of refund or Input Tax Credit shall not be

passed unless the appellant has been given a reasonable opportunity of showing cause against the proposed

order. The Revenue had completely failed to show that petitioner was given an opportunity of being heard

before passing orders of confiscation in Form GST MOV-11, hence, confiscation orders not found to be

passed in accordance with law, were to be quashed and set aside

HELD:

Both the writ petitions are allowed partly. Consequently, the Hon’ble High Court quash and set aside the

impugned orders dated 23.04.2021, passed by the respondent no.3 under Section 130 in Form GST MOV-

11, and the respondents are directed to release the vehicles and goods in question, which have been

detained since 31.03.2021, upon execution of a bond for the value of the goods in Form GST INS-04 and

furnishing of a security in form of a bank guarantee equivalent to the amount of applicable tax, interest

and penalty payable, by the petitioner. The release of the vehicles and goods are subject to the final

outcome of the confiscation proceedings.

It is clarified that after giving an opportunity of being heard to the petitioner, the respondents may proceed

further in accordance with law.

Taxpert Professional’s comments:

The hon’ble High Court of Uttarakhand observed that the GST department failed to prove that

the opportunity of being heard was given to the assessee before the passing the orders of the

confiscation in Form GST MOV-11. Moreover, before invoking the provisions of Section 130

for confiscation, there should be a very strong base to proceed for confiscation. Mere suspicion

is not sufficient to invoke the provision of the confiscation. Therefore, it was found that order

under Section 130 was not passed in accordance with law and liable to be set aside. The court

also directed to release the vehicles and goods upon execution of a bond for the value of the

goods in Form GST INS-04 and furnishing of a security in form of a bank guarantee.

Recent Updates

22 © Taxpert Professionals| September, 2021

A reasonable opportunity ought to have been granted to all 'registered persons'/taxpayers to

submit/revise/ re-revise electronically their Form GST TRAN-1/TRAN-2:[Ratek Pheon

Friction Technologies Pvt. Ltd Vs. Principal Commissioner, [2021] 130 taxmann.com 367

(Allahabad)[15-09-2021]

RECENT JUDICIAL PRONOUNCEMENTS

FACT OF THE CASE:

1) M/s Ratek Pheon Friction Technologies Pvt. Ltd (hereafter referred as the Petitioner) contents that

it filed its return under the Central Excise Act, 1944 on Form ER-1, on 13.07.2017 for the period

ending 30.06.2017, disclosing total CENVAT credit available Rs. 52,54,954/-. Also, it submitted

electronically its Form GST TRAN-1, for the period ending 30.06.2017, within time granted.

2) Inadvertently, it submitted the figure Rs. 50,702/- as admissible CENVAT in place of the actual

entitlement figure Rs. 52,54,954/-. The Form GST TRAN-1 containing the aforesaid error was

submitted electronically on 13.07.2017 on the GST portal. Despite best efforts, the petitioner could

not submit electronically the revised Form GST TRAN1 before the cut-off date 27.12.2017 as that

function on the GST portal had not been activated or not made fully functional.

3) Besides making unsuccessful attempts to revise the Form GST TRAN-1, manually, the petitioner

further claims to have written to the Principal Commissioner CGST on 10.9.2020 and 12.2.2021 to

verify the correct amount of ITC available to it and to resolve the issue in favour of the petitioner. In

the reply of the same, with respect to communication dated 15.3.2021, the Principal Commissioner

CGST refused that resolution since the petitioner’s request was received on 26.05.2020, after expiry

of the last date for that purpose, 31.03.2020.

ISSUE:

i. Whether submission/revision/ re-revision electronically allowed to the taxpayer in the Form GST

TRAN-1/TRAN-2.

OBSERVED:

i. The Hon’ble High Court noted that the general difficulty obtaining with all the “registered

persons”/taxpayers and have considered the same to be generic in nature and also make this order

applicable to all other “registered persons”/taxpayers within the State of U.P. (who are not before

this Court), within a period of eight weeks from today. The further timelines provided by this

Court shall stand modified accordingly.

ii. As to the evidence of technical difficulties experienced by the petitioners and the glitches suffered

on the GST Portal. A reference has been made to repeated extensions of time granted by all the

statutory authorities and the legislative action taken to extend the timeline to submit Form GST

TRAN-1, for that reason. Then reference has been made to Circular no. 39/13/2018-GST dated

03.04.2018 issued by CBIC. Last, reference has been made to various decisions of different High

Courts, that the GST TRAN-1 and/or TRAN-2 on the GST portal was not a local phenomenon

or a rare event but a common and generic difficulty faced by all “registered persons”/tax payers

across the country, while working on the newly designed GST Portal.

Recent Updates

23 © Taxpert Professionals| September, 2021

Gauhati HC ruling on refund of accumulated ITC in case of inverted duty [BMG Informatics

Pvt Ltd Vs Union of India [2021] 130 taxmann.com 182 (Gauhati)[02-09-2021]

RECENT JUDICIAL PRONOUNCEMENTS .

HELD:

It was held that the Court has no hesitation in observing that a reasonable opportunity ought to have been

granted to all “registered persons”/taxpayers to submit/revise/re-revise electronically their Form GST

TRAN-1/TRAN-2. The GST Network shall thereupon (After filing physical forms by the petitioner)

either itself upload the GST TRAN-1/TRAN-2, within two weeks of receipt of such communication or

allow that petitioner opportunity to upload those details, within a reasonable time.

FACT OF THE CASE:

1) M/s BMG Informatics Pvt. Ltd (Hereafter Referred as Assessee) is a company dealing with IT system

integrator and is a service provider primarily engaged in sales and service of information and

technology products to Government Departments, PSU and to other Research and Educational

Institutes located in the North Eastern region.

2) The assessee is a registered dealer under the Central Goods and Service Tax Act 2017 (for short, the

CGST Act of 2017) bearing registration No. GSTIN 18AADCB2203Q3ZL.

3) The assessee submitted a claim for a refund under FORM-GST-RFD-02. In response thereof, the

department had issued a show-cause notice dated 10.04.2020 that the assessee had misdeclared the

amount of total turnover in Annexure-1 to the RFD-01 for the period October – December 2018

and, therefore, the refund claimed is liable to be rejected.

4) A reply dated 25.04.2020 showing their reasons as to why there was no mis-declaration. The Assistant

Commissioner CGST, Central Excise and Customs, Guwahati (to be referred to as the Assistant

Commissioner) in consideration of the claim of the assessee for the refund had passed the order dated

22.05.2020, whereby the claim for refund for an amount of Rs.3,92,594/- for the period from

01.10.2018 to 31.12.2018 stood rejected.

Taxpert Professional’s comments:

The clear intent of the legislature is to grant benefit of CENVAT and ITC under the pre-existing

laws, as may have been carried forward on the appointed date 01.07.2017. In such circumstances,

if the GST Portal had worked seamlessly, all petitioners would have submitted/revised/re-

revised electronically, their Forms GST TRAN-1 and/or TRAN-2 within the time granted. In that

situation, all petitioners would clearly be entitled to avail ITC under the CGST Act and the

UPGST Act, without any objection by the State/revenue authorities. Taxing statute and equity

considerations are not natural allies. At the same time, in the context of a purely procedural

requirement and transition provision, we cannot act unmindful of that consequence - if the

respondents had offered a functional system, the State could not have deprived the petitioners of

transition credit of CENVAT and ITC (under the repealed laws).

Recent Updates

24 © Taxpert Professionals| September, 2021

RECENT JUDICIAL PRONOUNCEMENTS

ISSUE:

i. Whether the refund claimed by the assessee was admissible by law by taking into consideration

of facts and circumstances of the case and the order passed by the assessee is liable for set aside

as the same would be unsustainable or unreasonable from the point of view of the assessee.

OBSERVED:

The law in this respect is settled to the extent that whenever there is a conflict between the provisions of

a statutory Act and that of a notification or circular issued by an administrative authority, the provisions

of the statutory Act would prevail over such conflicting provisions of a notification or a circular of an

administrative authority. It has been interpreted by the Supreme Court in a plethora of decisions that the

provisions of such notification or circular, which would be in conflict with the provisions of a statutory

Act, would have to be ignored and not taken into consideration for the purpose of arriving at any such

decision.

Consequently, in view of the clear unambiguous provisions of Section 54(3) (ii) providing that a refund of

the unutilized input tax credit would be available in the event the rate of tax on the input supplies is higher

than the rate of tax on output supplies, the provisions of paragraph 3.2 of the circular No.135/05/2020-

GST dated 31.03.2020 providing that even though different tax rate may be attracted at different point of

time, but the refund of the accumulated unutilized tax credit will not be available under Section 54(3)(ii)

of the CGST Act of 2017 in cases where the input and output supplies are same, would have to be ignored.

HELD:

The Hon’ble Guwahati High Court held that the rejection of the claim for refund by the petitioner assessee

in the order dated 22.05.2020 of the Assistant Commissioner by referring to the provisions of paragraph

3.2 of the circular No.135/05/2020-GST dated 31.03.2020 would be unsustainable in law. The matter

stands remanded back to the Assistant Commissioner, GST, Guwahati to consider the matter afresh and

arrive at his own factual satisfaction as to whether the actual rate of tax on the input supplies made by the

petitioner assessee is higher than the actual rate of tax on the output supplies made by them and depending

upon the satisfaction that may be arrived to pass a reasoned order on the claim of the petitioner assessee

for refund under Section 54(3)(ii) of the CGST Act of 2017.

Taxpert Professional’s comments:

It was found by the facts of the case read with the rules and provisons made under GST law,

there was a conflict between provisions of paragraph 3.2 of Circular No.135/05/2020-GST dated

31-3-2020 with provisions of section 54(3)(ii) and whenever there is a conflict between provisions

of a statutory Act and that of a notification or circular issued by an administrative authority,

provisions of statutory Act would prevail over such conflicting provisions of a notification or a

circular of an administrative authority. Thus, the order passed by the assistant commissioner is

unsustainable and unreasonable and was liable to set a side and the same was held by above

judicial pronouncement.

Recent Updates

25 © Taxpert Professionals| September, 2021

AUTHORITY FOR ADVANCE RULINGS [AAR]

FACT OF THE CASE:

1) Eastern Coalfields Limited (hereinafter referred to as, the applicant) is stated to be a producer and

supplier of coal. The applicant submits that he has received services from M/s Gayatri Projects

Ltd (GSTIN: 19AAACG8040K1ZG) and has availed of Input Tax Credit during the tax periods

January’20, February’20 and March’20 respectively against 03 (three) invoices bearing number 43

dated 01.01.2020, 44 dated 01.02.2020 and 45 dated 02.03.2020 issued by the said supplier of

services. Payments against such supplies have also been made by the applicant.

2) However, M/s Gayatri Projects Ltd has furnished FORM GSTR-1 and FORM GSTR-3B for the

aforesaid tax periods i.e., January’20, February’20 and March’20 in the month of November’20

which has restricted input tax credit in respect of above-noted invoices in the auto-drafted FORM

GSTR-2B of the applicant for the month of November’20 with the remark ‘Return Filed Post

Annual Cut-off’.

3) Based on the aforesaid facts, the applicant has made this application under sub-section (1) of

section 97 of the GST Act and the rules made there under raising the application in FORM GST

ARA-01.

ISSUE:

i. Whether the applicant is entitled for Input Tax Credit already claimed by him on the invoices raised

by M/s Gayatri Projects Ltd. pertaining to the period Jan-2020, Feb2020 and March-2020 for which

the supplier has actually paid the tax charged in respect of such supply to the Government, either in

cash or through utilization of input tax credit admissible in respect of such supply.

ii. Whether the applicant has to reverse the said ITC already availed by him where M/s Gayatri Project

Ltd. has actually paid the tax, though belatedly and fulfilled the responsibility cast upon them by

Section 16(2)(c) of CGST Act, 2017 and all other conditions as mentioned in Section 16(2)(a),

16(2)(b), and 16(2)(d) are fulfilled by the applicant.

OBSERVED:

The Authority observed that there can be no denying that section 16 of the GST Act specifies conditions

and restrictions towards entitlement of Input Tax Credit. The said section contains four subsections which

are to be read in a conjoint manner and the same must be read together with the rules prescribed in this

regard as sub-section (1) of section 16 entitles a registered person to take Credit of Input Tax Subject to

fulfillment of such conditions and restrictions as may be prescribed. Since FORM GSTR- 2B has been

made effective from 01.01.2021, the submission made by the applicant that the auto-drafted FORM

GSTR-2B generated for the month of November’20 i.e., prior to the enactment of the amended rule, does

not have any statutory force towards entitlement of input tax credit for the tax period January-20,

February-20 and March-20. In the light of the aforesaid provisions of the GST Act and rules made there

under, the applicant has availed of input tax credit in excess of his entitlement prescribed under sub-rule

(4) of rule 36.

ITC not to be availed if supplier furnishes invoices for FY 2019-20 in GSTR-1 of November

2020. Authority for Advance Rulings (AAR), West Bengal, Goods & Services Tax [2021] 130

taxmann.com 232 (AAR - WEST BENGAL) [09-08-2021]

Recent Updates

26 © Taxpert Professionals| September, 2021

AUTHORITY FOR ADVANCE RULINGS [AAR]

RULING: We pronounce the Ruling:

The applicant is not entitled for input tax credit claimed by him on the invoices raised by M/s Gayatri

Projects Ltd. pertaining to the period Jan-2020, Feb-2020 and March-2020 for which the supplier has

furnished FORM GSTR-1 and FORM GSTR-3B in the month of November’20 and the applicant is,

therefore, required to reverse the said input tax credit.

This Ruling is valid subject to the provisions under Section 103until and unless declared void under Section

104(1) of the GST Act.

FACT OF THE CASE:

1) The applicant is engaged in the business of manufacturing of tissue paper in various categories such

as facial tissues, kitchen towel, toilet roll & napkins. These tissue papers are manufactured from

waste paper, cup stock, tissue brokes and soft wood pulp.

2) The applicant is seeking advance ruling on question as to whether the supply of tissue papers by the

applicant is covered under Sl No. 112 of Schedule II of the Notification No. 01/2017 – Central Tax

(Rate) and, therefore, is leviable to GST at the rate of 12 per cent.

ISSUE:

i. The Applicant is engaged in the manufacture of tissue paper in various categories like facial tissues,

kitchen towel, toilet roll & napkins. The applicant has sought advance ruling in respect of the

following question:

ii. Whether the supply of tissue papers by the applicant is covered under Serial No. 112 of Schedule

II of the Rate Notification No. 01/2017 Central Tax (R) and therefore, is leviable to GST at the

rate of 12%?

iii. Admissibility of the application: The question is about classification of their product falling under

"classification of any goods or services or both;" and hence is admissible under section 97(2)(a) of

the CGST Act, 2017.

Taxpert Professional’s comments:

According to section 16(4) of CGST Act, 2017, the registered person can avail ITC of the

previous year on or before filing of GSTR-3B for the month of September of the following

year or filing of annual return whichever is earlier. Hence, in the said case the ITC of FY

2019-20 would be eligible to claim on or before filing of GSTR-3B of September, 2020 and

the assessee claimed the same in the month of Nov 2020. Even Though the supplier

furnishes the invoices in Nov 2020 the same should have been claimed only before Sep 2020.

The above ruling passed by the West Bengal AAR explains or clarifies the same.

Tissue Paper not to be covered under Heading No. 4802 of uncoated paper and paperboard

Authority for Advance Rulings, Karnataka [In re Premier Tissues India Limited , GST AAR

Karnataka]

Recent Updates

27 © Taxpert Professionals| September, 2021

AUTHORITY FOR ADVANCE RULINGS [AAR]

OBSERVED:

i. The Entry No. 112 of Schedule II of the Notification No. 1/2017 - Central Tax (Rate), dated 28-

6-2017 covers the goods, falling under HSN 4802, that attract GST at rate of 12 per cent.

ii. The impugned products are not covered under the Heading No. 4802. The said product does not

get covered under the required description of Entry No. 112 of Schedule II to the Notification

No. 1/2017 - Central Tax (Rate), dated 28-6-2017, i.e., Heading No. 4802. Therefore, the GST

rate of 12 per cent is not applicable to the instant case.

iii. GST rate of 12 per cent is applicable only to uncoated paper and paperboard used for writing,

printing or other graphic purposes. Further the paper of Heading Nos. 4801 and 4803 are excluded

from the Heading No. 4802. The impugned products being the tissue papers fall under other paper

and paperboard not containing fibers obtained by a mechanical or chemi-mechanical process and,

hence, do not get covered under uncoated paper and paperboard. Therefore, the impugned

products of the applicant are not covered under the Entry No. 112 of Schedule II to Notification

No. 1/2017 - Central Tax (Rate), dated 28-6-2017 and, hence, the GST rate of 12 per cent is not

applicable to them.

iv. Thus, the supply of tissue papers by the applicant is not covered under the Entry No. 112 of

Schedule II to the Notification No. 1/2017 - Central Tax (Rate) and, therefore, GST rate of 12

per cent is not applicable to the supply of the applicant.

RULING: We pronounce the Ruling:

The impugned products being the tissue papers fall under other paper and paperboard not containing

fibres obtained by a mechanical or chemi-mechanical process and hence do not get covered under

uncoated paper and paperboard. Therefore, the impugned products of the applicant are not covered under

the entry No. 112 of Schedule II to Notification supra and hence the GST rate of 12% is not applicable

to them.

Taxpert Professional’s comments:

The impugned products being the tissue papers fall under other paper and paperboard not

containing fibres obtained by a mechanical or chemi-mechanical process and hence do not

get covered under uncoated paper and paperboard. Therefore, the impugned products of the

applicant are not covered under the entry No. 112 of Schedule II to Notification supra and

hence the GST rate of 12% is not applicable to them.

Recent Updates

28 © Taxpert Professionals| September, 2021

AUTHORITY FOR ADVANCE RULINGS [AAR]

FACT OF THE CASE:

1) M/s Nagri Eye Research Foundation (Herein referred to as Petitioner) is a charitable trust set up with and objective to undertake eye and research activities as well as manage funds for purpose of education and charitable activities in eye research and prevention of blindness.

2) The petitioner is running a medical store where medicines are sold to indoors and outdoors patients at low rates.

3) The petitioner filed an application before Gujrat Advance Rulings Authority (GAAR) for seeking answers wherein the GAAR passed the ruling that the sale of medicine at low rates amounts to supply of goods.

4) Aggrieved by the decision of the GAAR the Petitioner appealed before the Gujrat Appellate Advance Rulings Authority (GAAAR), which in turn dismissed the appeal.

5) Thus the Petitioner filed petition in High Court against ruling of GAAAR.

ISSUE:

i. Whether GST registration is required for medical store run by Charitable Trust?

ii. Whether supply of medicines at lower rates amount to supply of goods?

OBSERVED:

The Hon’ble high court observed that the as per Section 7(1) of the CGST Act the word supply includes

all form of supply of goods made for consideration irrespective of the amount of consideration paid. The

term business u/s 2(7) of CGST Act includes any trade, commerce, manufacture, profession, wager

whether or not done for pecuniary benefits. The petitioner failed to justify his submissions how the sale

of lower rates of medicines is not said to be trade and commerce.

RULING: We pronounce the Ruling:

That the medical store run by Charitable trust would require GST registration and Medical store providing

medicine at lower rates would amount to supply of goods.

The Hon’ble high court dismissed the appeal of the petitioner

Charitable Trust running medical store to give medicines without profit required to be

registered under GST [Nagri Eye Research Foundation v. Union of India, Gujarat High

Court SCA [No. 7822 Of 2021]

Taxpert Professional’s comments:

The Hon’ble Gujarat High Court stated that every supplier who falls within ambit of Section

22(1) of the Central Goods and Services Tax Act, 2017 (CGST Act) has to get himself registered

under the CGST Act. The Petitioner would require GST Registration even if supplied at lower

rate would amount to supply of goods if the aggregate turnover exceeds the threshold limit.

Recent Updates

29 © Taxpert Professionals| September, 2021

NOTIFICATIONS/CIRCULARS/PRESS RELEASE

1. Central Goods and Services Tax (Eighth Amendment) Rules, 2021 - Amendment in Rules 10a [Notification No. 35/2021- Central Tax] i. By issuing the given notification the GST authorities made the Eighth amendment in the Central

Goods and Services Tax Rules, 2021. The Rule 10A was amended to insert the words “which is

in name of the registered person and obtained on Permanent Account Number of the registered

person” in place of “details of bank account” and the proviso inserted as in case of a

proprietorship concern, the Permanent Account Number of the proprietor shall also be linked

with the Aadhaar number of the proprietor.

ii. Further, Rule 10B regarding the Aadhaar authentication for registered person was also inserted.

It is stated that the registered person shall undergo authentication of the Aadhaar number of the

proprietor, in the case of proprietorship firm, or of any partner, in the case of a partnership firm,

or of the karta, in the case of a Hindu undivided family, or of the Managing Director or any whole

time Director, in the case of a company, or of any of the Members of the Managing Committee

of an Association of persons or body of individuals or a Society, or of the Trustee in the Board

of Trustees, in the case of a Trust and of the authorized signatory for filing of application for

revocation of cancellation of registration in FORM GST REG-21 under Rule 23 and For filing

of refund application in FORM RFD-01 under rule 89 and For refund under rule 96 of the

integrated tax paid on goods exported out of India. The manner of Aadhar Authentication is also

clarified in the said notification.

2. Section 25 of the Central Goods and Services Tax Act, 2017 - registration - procedure for notified persons for whose registration provision regarding aadhaar authentication shall not apply [Notification No. 36/2021-Central Tax dated 24/09/2021]

In exercise of the powers conferred by sub-section (6D) of section 25 of the Central Goods and Services Tax Act, 2017, the Central Government, on the recommendations of the Council, made the amendment in the notification of the Government of India in the Ministry of Finance (Department of Revenue) No. 03/2021-Central Tax, dated the 23rd February, 2021. In the notification number 36/2021, the section 25(6A) is inserted which states that every person who makes a supply from the territorial waters of India shall obtain registration in the coastal State or Union territory where the nearest point of the appropriate baseline is located. The provision of the same shall not be applicable to the person referred under notification No. 3/2021.

3. Section 25 Of The Customs Act, 1962 - Power to Grant Exemption from Duty - Exemption &

Effective Basic and Additional Customs Duty for Specified Goods - Amendment in

Notification Nos. 50/2017-Customs. [Notification No. 42/2021-Customs]

i. The Notification amend the previously issued Notification No. 50/2017 dated 30th June, 2017.

In the notification it was stated that due to need for public interest the CBIC by excise of powers

under section 25(1) of Customs Act, 1962, exempts some tariff items when such mentioned items

imported to India.

ii. By issuing the Notification No. 42/2021-Customs, the CBIC seeks to insert some Standard rate

as pertaining to the particular entry. The Standard rate in column (4) of Notification No. 50/2017

2.5% inserted for Sr. No. 57, 61,70 and the Standard rate 32.5% in column (4) inserted for Sr.

No. 62, 65, 71.

NOTIFICATIONS

Recent Updates

30 © Taxpert Professionals| September, 2021

NOTIFICATIONS/CIRCULARS/PRESS RELEASE/

iii. Further, the same notification seeks to amend notification No. 11/2021-Customs which sought

to prescribe effective rate of Agriculture Infrastructure and Development Cess for specified

goods, in the same against Sr. No. 7, in column (3), for the entry, the entry “Crude Palm Oil”

shall be substituted and against Sr. No. 7, in column (4), for the entry, the entry “20%” shall be

substituted.

iv. It came into force from 11th September, 2021.

4. Section 25 Of The Customs Act, 1962 - Power to grant Exemption from Duty - Exemption to

Specified goods when imported into India - rescission of Notification No. 34/2021-Customs

[Notification No. 43/2021 – Customs]

This Notification Seeks to rescinds the notification of the Government of India in the Ministry of

Finance (Department of Revenue) No. 34/2021- Customs, dated the 29th June, 2021 published in the

Gazette of India which sought to reduce the basic custom duty on Crude Palm Oil [1511 10] and Palm

Oil other than Crude Palm Oil [1511 90] till 30th September 2021.

5. Section 25 Of The Customs Act, 1962 - Power to grant Exemption from Duty - Exemption &

Effective Basic and Additional Customs Duty for Specified Goods [Notification No. 44/2021

– Customs]

The Notification amend the previously issued Notification No. 50/2017 dated 30th June, 2017. In the

notification it was stated that due to need for public interest the CBIC by excise of powers under

section 25(1) of Customs Act, 1962, exempts some tariff items when such mentioned items imported

to India.

By issuing the Notification 44/2021 the CBIC seeks to amend Sr. No. 21F in Column (4) in which

Standard Rate 20% shall be inserted.

1. Easing Container Availability for Export Cargo [Circular No. 21/2021-Customs dated 24-9-

2021]

i. The circular was issued in order to ease container availability for export cargo – registration.

ii. By issuing notification the CBIC invites attention to para 4 of Board`s Circular No.83/1998-

Customs dated 05.11.1998 issued in connection with exemption to containers of durable nature in

terms of Notification No. 104/1994-Customs dated 16.03.1994, as amended. This notification

inter-alia specifies that in any particular case, the initial period of re-exporting said type of

containers imported within 6 months can be extended by the Assistant Commissioner on sufficient

cause being shown.

iii. The Circular No. 83/1998-Customs has the provision the following provision after the application

above circular–“The Assistant Commissioner may grant an extension beyond 6 months upto

further 3 months for the reasons to be recorded in writing”.

iv. As a temporary measure to ease containers available presently for export of containerised cargo

and with aim of promoting export of laden marine containers, it is guided that, where the initial

period of 6 months is till on or before 31.03.2022, the above provision of the Circular may also be

applied on receiving intimation before expiry of initial period of 6 months from the concerned

importer that the container shall be re-exported in laden condition within the next 3 months.

CIRCULARS

Recent Updates

31 © Taxpert Professionals| September, 2021

NOTIFICATIONS/CIRCULARS/PRESS RELEASE

2. Clarification regarding extension of time-limit to apply for revocation of cancellation of

registration in view of Notification No. 34/2021-Central Tax, [Circular No. 158/14/2021-GST

dated 6-9-2021]

i. The circular was issued in order to provide the clarification regarding extension of time limit to

apply for revocation of cancellation of registration in view of Notification No. 34/2021-Central

Tax dated 29th August, 2021 – Registration where Vide Circular No. 148/04/2021-GST, dated

18th May, 2021, detailed guidelines for implementation of the provision of extension of time limit

to apply for revocation of cancellation of registration under section 30 of the Central Goods and

Services Tax Act, 2017 (hereinafter referred to as "the CGST Act / said Act") and rule 23 of the

Central Goods and Services Tax Rules, 2017 (hereinafter referred to as "the CGST Rules") have

been specified, till the time an independent functionality for extension of time limit for applying

in FORM GST REG-21 is developed on the GSTN portal. It may be noted that notification

No.14/2021-Central Tax, dated 1st May, 2021, as amended, had, inter-alia, extended the date of

filing of application for revocation of cancellation of registration till 30th June, 2021, where the

due date of filing of application was falling between 15th April, 2021 to 29th June, 2021.

Government has now issued notification No. 34/2021-Central Tax dated 29th August, 2021

(hereinafter referred to as "the said notification") under section 168A of the said Act to extend the

timelines for filing of application for revocation of cancellation of registration to 30th September,

2021, where the due date of filing of application for revocation of cancellation of registration falls

between 1st March, 2020 to 31st August, 2021. This extension is applicable for those cases where

registrations have been cancelled under clause (b) or clause (c) of sub-section (2) of section 29 of

the said Act.

ii. In order to ensure uniformity in the implementation of the said notification across field

formations, the Board, in exercise of its powers conferred by section 168(1) of the said Act, hereby

clarifies by circular the issues relating to the extension of timelines.

iii. The suitable trade notices may be issued to publicize the contents of this circular.

3. Clarification on doubts related to scope of "INTERMEDIARY" [Circular No. 159/15/2021-

GST dated 20-9-2021]

i. This Circular clarifies and provides the insights of the definition of “Intermediary Services”. Many

taxpayers sought the clarifications for the same before the Authorities of GST. Hence, in view of

the difficulties being faced by the trade and industry and to ensure uniformity in the

implementation of the provisions of the law across field formations, the Board, in exercise of its

powers conferred by section 168 (1) of the Central Goods and Services Tax Act, 2017, CBIC

clarified the concept of Intermediary Services.

ii. From the perusal of the definition of “intermediary” under IGST Act as well as under Service Tax

law, it is evident that there is broadly no change in the scope of intermediary services in the GST

regime vis-à-vis the Service Tax regime, except addition of supply of securities in the definition of

intermediary in the GST Law. The following are the requirements in order to fall in the definition

of Intermediary Services:

(i) Minimum of Three Parties; (ii) Two distinct supplies; (iii) Ancillary supply, (iv) Intermediary service provider to have the character of an agent, broker or any other similar

person;

Recent Updates

32 © Taxpert Professionals| September, 2021

NOTIFICATIONS/CIRCULARS/PRESS RELEASE

(v) Sub-contracting for a service is not an intermediary service; iii. The specific provision of place of supply of ‘intermediary services’ under section 13 of the IGST

Act shall be invoked only when either the location of supplier of intermediary services or location

of the recipient of intermediary services is outside India. The same was also explained by issuing

many illustrations in the circular.

4. Clarification in respect of certain GST related issues [Circular No. 160/16/2021-GST, dated

20-9-2021]

i. The said Circular issued in respect of various representations received from taxpayers and other

stakeholders seeking clarification in respect of certain issues pertaining to GST laws. The issues

have been examined by the GST Authorities in order to ensure uniformity in the implementation

of the provisions of the law across field formations, the Board, in exercise of its powers conferred

by section 168(1) of the Central Goods and Services Tax Act, 2017 (hereinafter referred to as

“CGST Act”), hereby clarifies each of these issues as under:

ii. The clarification in respect of Section 16(4) of CGST Act, 2017 where the intent of law as specified

in the Memorandum explaining the Finance Bill, 2020 states that “Clause 118 of the Bill seeks to

amend sub-section (4) of section 16 of the Central Goods and Services Tax Act so as to delink the

date of issuance of debit note from the date of issuance of the underlying invoice for purposes of

availing input tax credit.

iii. Further, it was to clarify whether carrying physical copy of invoice is compulsory during

movement of goods in cases where suppliers have issued invoices in the manner prescribed under

rule 48 (4) of the CGST Rules, 2017 (i.e. in cases of e-invoice). Accordingly, it is clarified that there

is no need to carry the physical copy of tax invoice in cases where invoice has been generated by

the supplier in the manner prescribed under rule 48(4) of the CGST Rules and production of the

Quick Response (QR) code having an embedded Invoice Reference Number (IRN) electronically,

for verification by the proper officer, would suffice.

iv. The last issue held was only those goods which are actually subjected to export duty i.e., on which

some export duty has to be paid at the time of export, will be covered under the restriction imposed

under section 54(3) from availment of refund of accumulated ITC. Goods, which are not subject

to any export duty and in respect of which either NIL rate is specified in Second Schedule to the

Customs Tariff Act, 1975 or which are fully exempted from payment of export duty by virtue of

any customs notification or which are not covered under Second Schedule to the Customs Tariff

Act, 1975, would not be covered by the restriction imposed under the first proviso to section 54(3)

of the CGST Act for the purpose of availment of ITC.

5. Clarification relating to Export of Services-Condition (v) of Section 2(6) of the IGST ACT 2017

[Circular No. 161/17/2021-GST, dated 20-9-2021]

i. The circular was issued to provide the Clarification relating to export of services-condition (v) of

section 2(6) of the IGST Act 2017. In view of the above, it is clarified that a company incorporated

in India and a body corporate incorporated by or under the laws of a country outside India, which

is also referred to as foreign company under Companies Act, are separate persons under CGST

Act, and thus are separate legal entities. Accordingly, these two separate persons would not be

considered as “merely establishments of a distinct person in accordance with Explanation 1 in

section 8”. Therefore, supply of services by a subsidiary/ sister concern/ group concern, etc. of a

foreign company, which is incorporated in India under the Companies Act, 2013 (and thus

Recent Updates

33 © Taxpert Professionals| September, 2021

NOTIFICATIONS/CIRCULARS/PRESS RELEASE

ii. qualifies as a ‘company’ in India as per Companies Act), to the establishments of the said foreign

company located outside India (incorporated outside India), would not be barred by the condition

(v) of the sub-section (6) of the section 2 of the IGST Act 2017 for being considered as export of

services, as it would not be treated as supply between merely establishments of distinct persons

under Explanation 1 of section 8 of IGST Act 2017. Similarly, the supply from a company